KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

Analysis of Epic Electronic Health Record Data Shows People of Color Fare Worse than White Patients at Every Stage of the COVID-19 Pandemic, Including Higher Rates of Infection, Hospitalization and Death

Disparities in Hospitalization and Death Persist Even after Accounting for Differences in Sociodemographic Factors and Underlying Health Conditions, And People of Color are Sicker When They Test Positive

People of color were more likely to test positive for COVID-19 and to require a higher level of care at the time of diagnosis compared to White patients, according to a new analysis from Epic Health Research Network and KFF. They also were more likely to be hospitalized and die from the novel coronavirus than White patients were.

The racial disparities in illness and death are not fully explained by differences in underlying sociodemographic characteristics and health conditions, finds the study, which analyzed Epic electronic health record data for roughly 50 million patients from 53 health systems representing 399 hospitals across 21 states.

The findings suggest that people of color may face increased barriers to testing that contribute to delays in obtaining testing until they are in more serious condition compared to White patients. They also demonstrate that people of color are bearing a disproportionate burden of negative health outcomes related to the COVID-19 pandemic at every stage – risk of exposure, access to testing, severity of illness, and likelihood of death.

The analysis, a joint project of EHRN and KFF, builds upon the findings of other studies and contributes to the research by providing insight into the experiences of a large patient population across a range of states and health systems, examining variation in the level of care patients required at the time they tested positive for COVID-19 by race and ethnicity, and assessing the extent to which underlying sociodemographic characteristics and health conditions explain racial disparities in hospitalization and death.

Key findings include:

Although testing rates differed little by race and ethnicity, among those tested, Hispanic patients were over two-and-a-half times more likely to have a positive result (311 per 1,000) and Black and Asian patients were nearly twice as likely to test positive (219 and 220 per 1,000, respectively) for COVID-19 compared to White patients (113 per 1,000). Further, larger shares of Black, Hispanic, and Asian patients were in an inpatient setting when they tested positive for COVID-19 compared to White patients. They also were more likely to require oxygen or ventilation at the time of diagnosis.

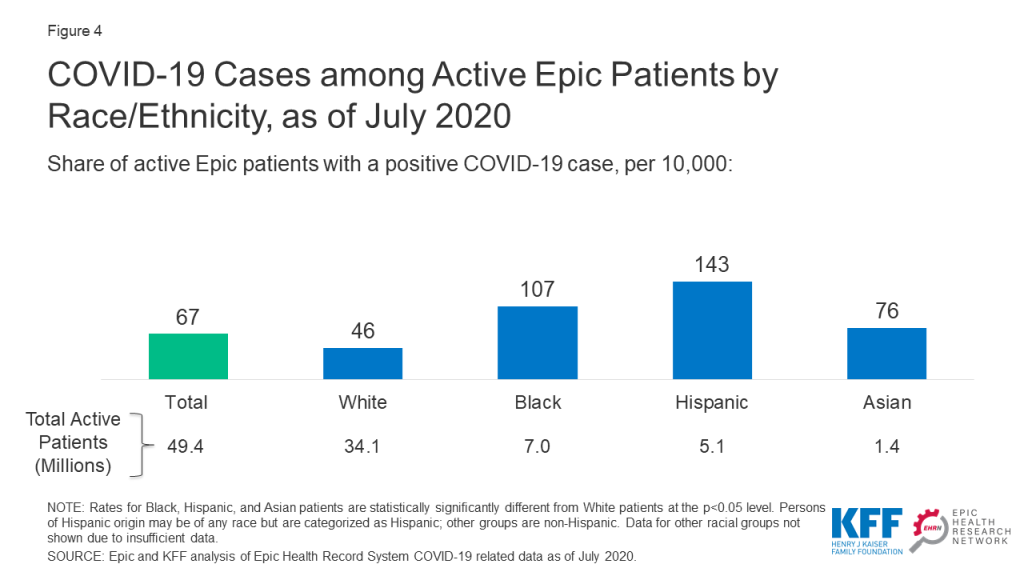

COVID-19 infection rates among Hispanic and Black patients were over three and two times higher, respectively, compared to the rate for White patients (143 and 107 vs. 46 per 10,000).

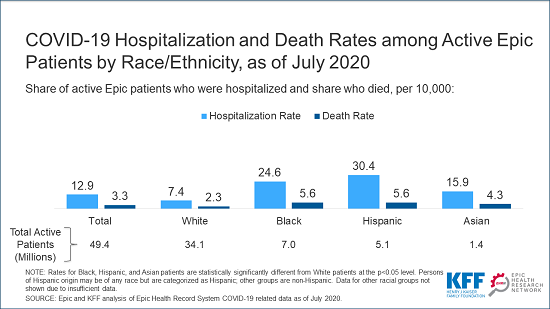

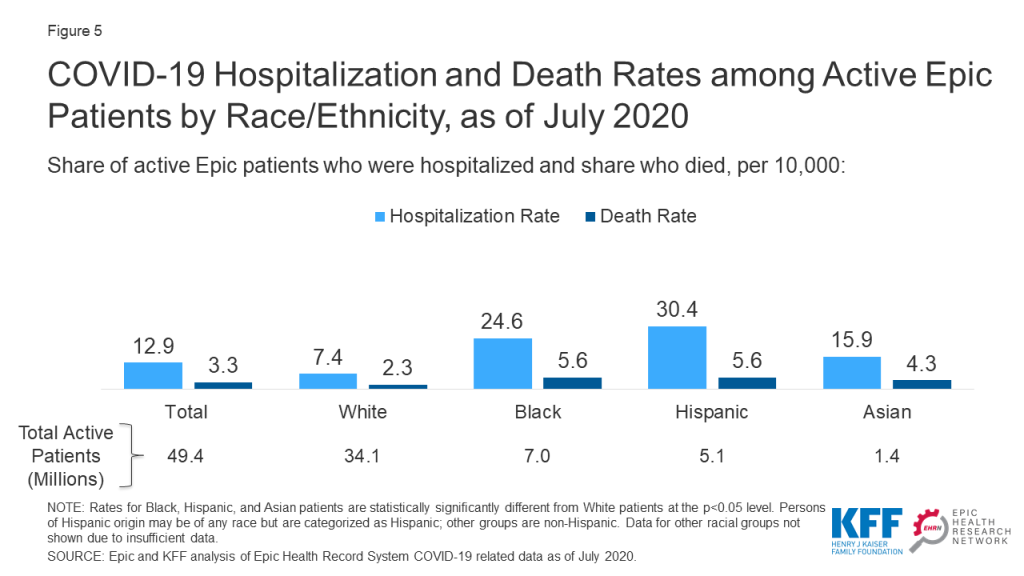

Hospitalization rates for Hispanic and Black patients with COVID-19 were more than four times and over three times higher, respectively, compared to the rate for White patients (30.4 and 24.6 vs. 7.4 per 10,000). Death rates for both groups were over twice as high as the rate for White patients (5.6 and 5.6 compared to 2.3 per 10,000). Asian patients also faced significant disparities in these measures.

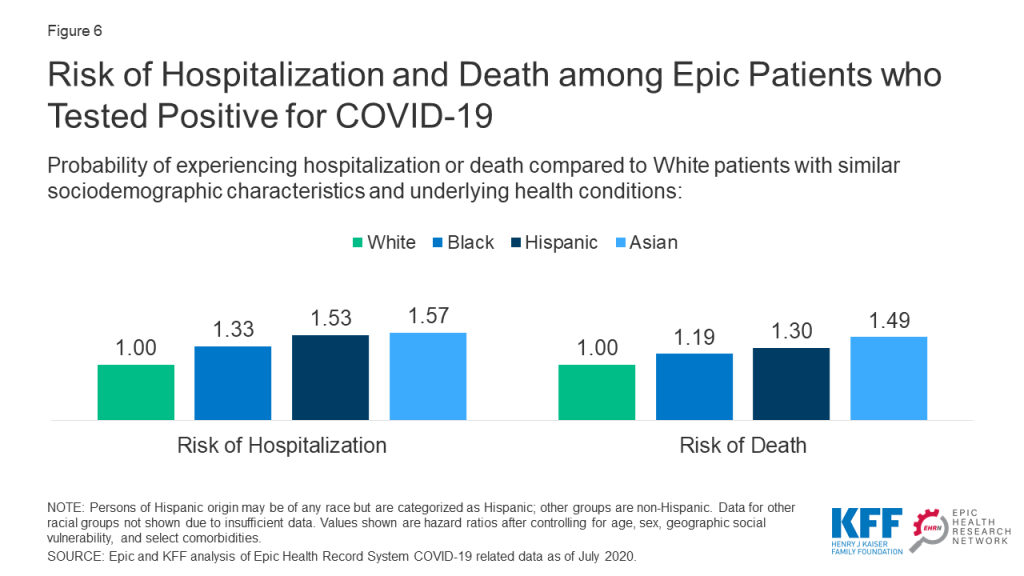

Among patients who tested positive for COVID-19, Black, Hispanic, and Asian patients remained at higher risk for hospitalization and death compared to White patients with similar sociodemographic characteristics and underlying health conditions, suggesting that other barriers, including racism and discrimination, are affecting outcomes through avenues not captured by these measures.

“Understanding the factors underlying COVID-19 infections and severe complications can help us devote resources appropriately to the most vulnerable communities,” said Christopher Alban, MD, Epic Vice President of Clinical Informatics. “This study adds nuance to our understanding of inequities in our COVID-19 response by showing racial and ethnic disparities that persist when comparing populations with similar health and socioeconomic status.”

“This analysis points to delays in testing for people of color, who are sicker and more likely to be infected when they do get tested,” said KFF President and CEO Drew Altman. “The findings highlight the continued importance of addressing racial disparities in responding to COVID-19 as in health care more broadly.”

About Epic Health Research Network

EHRN is a journal for the 21st century, designed for rapid sharing of knowledge with healthcare professionals, researchers, government, and learners to help solve medical problems. For more information, visit ehrn.org.

About KFF

Filling the need for trusted information on national health issues, KFF (Kaiser Family Foundation) is a nonprofit organization based in San Francisco, California. KFF is not affiliated with Kaiser Permanente.

This analysis builds on a continually growing body of research on racial disparities in COVID-19 by examining testing, infection, hospitalization, and death by race and ethnicity among patients in the Epic health record system. It contributes to the research in this area by providing insight into the experiences of a large patient population across a range of states and health systems, examining variation in the level of care patients required at the time they tested positive for COVID-19 by race and ethnicity, and assessing the extent to which underlying sociodemographic characteristics and health conditions explain racial disparities in hospitalization and death. Overall, it shows that, despite being at increased risk of exposure to the virus, people of color did not have markedly higher testing rates compared to White patients and were more likely to be positive when tested and to require a higher level of care at the time they tested positive. Moreover, it builds on previous research showing people of color have higher rates of hospitalization and death due to COVID-19 by finding that these disparities persist after controlling for sociodemographic characteristics and underlying health conditions. Key findings include:

Differences in testing rates by race and ethnicity were small, but people of color were more likely, compared to White patients, to be positive when tested and to require a higher level of care at the time they tested positive for COVID-19. Although there were not large differences in testing by race and ethnicity, among those tested, Hispanic patients were over two and a half times more likely to have a positive result (311 per 1,000) and Black and Asian patients were nearly twice as likely to test positive (219 and 220 per 1,000, respectively) compared to White patients (113 per 1,000). Further, larger shares of Black, Hispanic, and Asian patients were in an inpatient setting when they tested positive for COVID-19 compared to White patients, and they also were more likely to require oxygen or ventilation at the time of diagnosis.

Black, Hispanic, and Asian patients had significantly higher rates of infection, hospitalization, and death compared to their White counterparts. The infection rate for Hispanic patients was over three times higher than the rate in White patients (143 vs. 46 per 10,000), and the rate among Black patients was over two times as high (107 per 10,000). The hospitalization rate for Hispanic patients was more than four times as high as the rate in White patients (30.4 vs. 7.4 per 10,000), and the rate in Black patients was over three times as high (24.6 per 10,000). Death rates for both groups were over twice as high as the rate for White patients (5.6 and 5.6 compared to 2.3 per 10,000). Asian patients also faced significant disparities in these measures.

Racial disparities in hospitalization and death persisted among positive patients even after controlling for certain sociodemographic factors and underlying differences in health, with Asian patients exhibiting the highest relative risk. Among patients who tested positive for COVID-19, Black, Hispanic, and Asian patients remained at higher risk for hospitalization and death compared to White patients with similar sociodemographic characteristics and underlying health conditions. Asian patients were at the highest risk relative to White patients, followed by Hispanic and Black patients.

As previously documented, the higher infection rate among people of color likely reflects their increased risk of exposure to coronavirus due to their work, living, and transportation situations. They are more likely to be working in low-income jobs that cannot be done from home, to be living in larger households in densely populated areas, and to utilize public or shared modes of transportation. Despite being at increased risk of exposure to the virus, people of color did not have markedly higher testing rates compared to White patients and were more likely to be positive when tested and to require a higher level of care at the time they tested positive for COVID-19. These findings suggest that people of color may face increased barriers to testing that contribute to delays in them obtaining testing until they are in more serious condition.

The higher hospitalization and death rates among patients of color, in part, reflect higher infection rates and higher rates of underlying health conditions as well as social and economic inequities and barriers to care. However, the persistence of disparities after controlling for COVID-19 infection, certain sociodemographic factors, and underlying health conditions show that differences in these underlying factors do not fully explain the disparities in hospitalization and death. This finding suggests that other factors, including racism and discrimination, are negatively affecting their health outcomes through additional avenues.

Together, the findings point to the importance of considering health equity in COVID-19 response and relief efforts and health care more broadly, and, in particular, improving access to testing before individuals develop severe illness in order to slow the spread of infections. They also illustrate the importance of considering a wide array of factors both within and beyond the health care system and addressing structural and systemic racism and discrimination as root causes as part of efforts to address health disparities. These efforts will be key for narrowing the disparate effects of COVID-19, ensuring equitable distribution of treatments and a vaccine as they are developed, and preventing widening disparities in health care more broadly looking forward.

Issue Brief

Introduction

A continually growing body of research consistently shows people of color are bearing a disproportionate burden of COVID-19 cases, deaths, and hospitalizations and that they may face barriers to testing. For example, KFF analysis of state reported data shows that Black individuals account for more cases and deaths relative to their share of the population in most states reporting data. Other analysis of state-reported data finds higher mortality rates among Black and American Indian and Alaska Native (AIAN) people, disparities for Asian and Native Hawaiian and Pacific Islander (NHOPI) individuals in certain areas, and a recent rise in mortality rates for NHOPI and Hispanic people. Data also show that Black, Hispanic, and AIAN people are at increased risk of hospitalization due to COVID-19. Information on testing by race and ethnicity has been limited but suggests people of color may face increased barriers to testing.

This analysis builds on this body of research by examining COVID-19 testing, infection, hospitalization, and death as of July 2020 by race and ethnicity among active patients in the Epic health record system, which includes 53 health systems representing 399 hospitals across 21 states (see Methods for more details). It contributes to the research in this area by providing insight into the experiences of a large patient population across a range of states and health systems, examining variation in the acuity of patients by race and ethnicity at the time they test positive for COVID-19, and assessing whether racial disparities in hospitalization and death persist after controlling for sociodemographic characteristics and underlying health conditions.

Overview of the Epic Patient Population

The analysis is based on Epic Health Research Network (EHRN) and KFF analysis of data for roughly 50 million patients in the Epic health record system who have interacted with the health system in the past two years and have known race and ethnicity. Findings are presented for Black, Hispanic, Asian, and White patients. Due to data limitations, we do not present findings for smaller population groups, including AIAN and NHOPI patients, or people who report multiple races. As availability of data for smaller population groups increases over time, it may allow for future analyses focused on the experiences of these populations.

The Epic active patient population includes somewhat higher shares of Black and White patients and lower shares of Hispanic and Asian patients compared to the total U.S. population. For example, among the Epic active patient population, 15% of patients are Black, 10% are Hispanic, 3% are Asian and 69% are White. Among the total U.S. population, 13% of individuals are Black, 19% are Hispanic, 6% are Asian, and 60% are White. Just over half of the active patient population is female (54%), similar to the share of the overall U.S. population (51%). The active patient population includes a smaller share of children under age 19 compared to the total population (13% vs. 24%) and a larger share of adults age 65 or older (24% vs. 16%).

Key Findings

We examined overall rates of testing, infection, hospitalization and death associated with COVID-19 among the total active population by race and ethnicity. In addition, we assessed the share of positive cases among individuals tested and the level of care individuals required at the time they tested positive by race/ethnicity.

Testing, Positivity Rates, and Level of Care at Time Tested

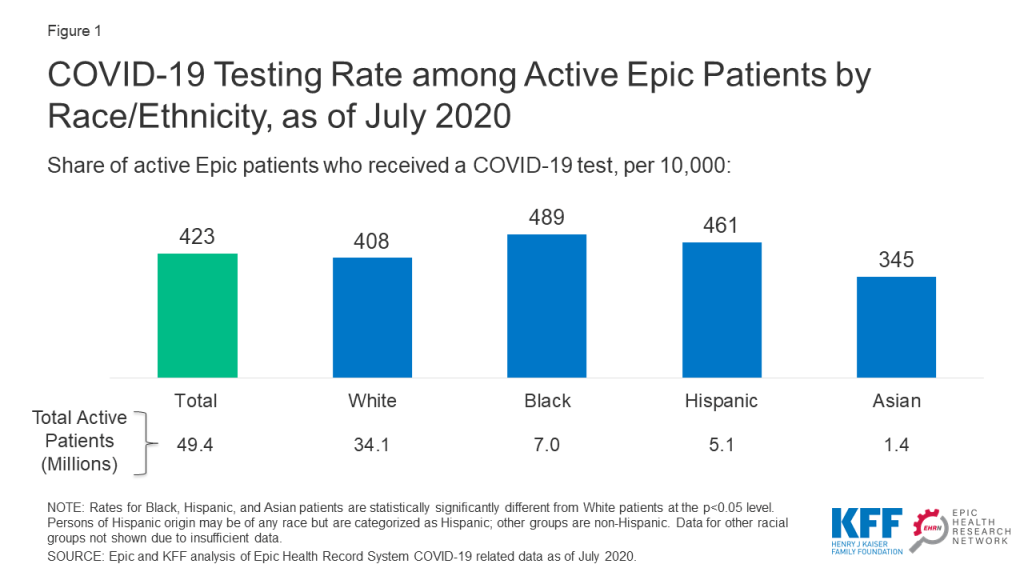

There were small differences in rates of testing by race and ethnicity. Black and Hispanic patients were slightly more likely to be tested compared to White patients (489 and 461 vs. 408 per 10,000) while the testing rate among Asian patients was lower compared to White patients (345 vs. 408 per 10,000) (Figure 1).

Figure 1: COVID-19 Testing Rate among Active Epic Patients by Race/Ethnicity, as of July 2020

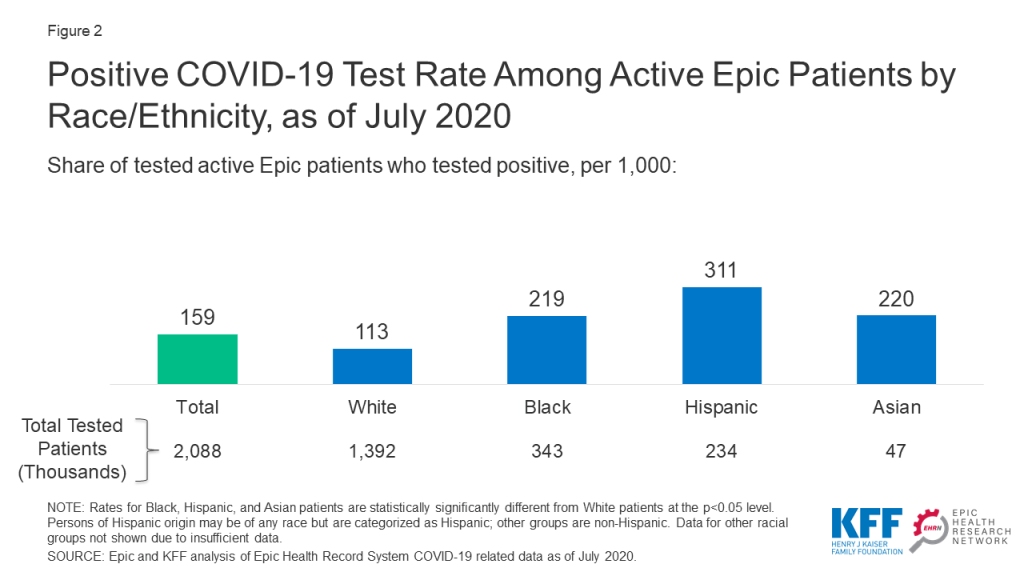

Among those tested, Black, Hispanic, and Asian patients were more likely than White patients to test positive for the virus. Hispanic patients had the highest positivity rate, which was over two and half times higher than the rate for White patients (311 vs. 113 per 1,000) (Figure 2). Black and Asian patients were nearly twice as likely to test positive (219 and 220 per 1,000, respectively) compared to White patients (113 per 1,000).

Figure 2: Positive COVID-19 Test Rate Among Active Epic Patients by Race/Ethnicity, as of July 2020

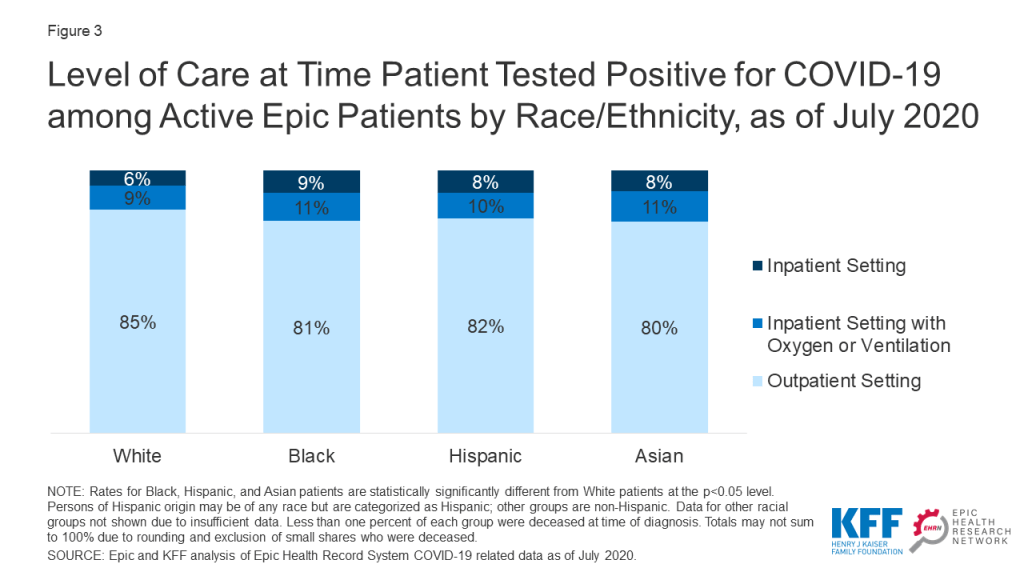

Black, Hispanic, and Asian patients also required a higher level of care at the time they tested positive for COVID-19 compared to White patients. Larger shares of Black, Hispanic, and Asian patients were in an inpatient setting when they tested positive for COVID-19 compared to White patients (Figure 3). They also were more likely to require oxygen or ventilation at the time of they tested positive.

Figure 3: Level of Care at Time Patient Tested Positive for COVID-19 among Active Epic Patients by Race/Ethnicity, as of July 2020

Infection, Hospitalization, and Death Rates

Overall, Black, Hispanic, and Asian patients had significantly higher rates of infection compared to White patients. Infection rates among Black and Hispanic patients were over two and three times higher, respectively, compared to the rate for White patients (107 and 143 vs. 46 per 10,000) (Figure 4). The infection rate among Asian patients was also significantly higher than the rate for White patients (76 vs. 46 per 10,000).

Figure 4: COVID-19 Cases among Active Epic Patients by Race/Ethnicity, as of July 2020

Black, Hispanic, and Asian patients also had significantly higher rates of hospitalization and death due to COVID-19 compared to White patients. The hospitalization rates for Black and Hispanic patients were over three and four times higher, respectively, compared to the rate for White patients (24.6 and 30.4 vs. 7.4 per 10,000), and their death rates were over twice as high as the rate for White patients (5.6 and 5.6 vs. 2.3 per 10,000) (Figure 5). Asian patients also faced significant disparities in these measures.

Figure 5: COVID-19 Hospitalization and Death Rates among Active Epic Patients by Race/Ethnicity, as of July 2020

Risk of Hospitalization and Death by Race/Ethnicity

Building on our examination of hospitalization and death rates, we conducted statistical analysis to assess whether racial disparities in hospitalization and death persist after controlling for certain sociodemographic characteristics and underlying conditions that are known to increase risk of illness and death. This analysis provides insight into the extent to which racial disparities in hospitalization and death are explained by differences in these underlying factors.

In this analysis, we controlled for age, sex, and health conditions that a previous EHRN analysis had identified as being significantly associated with higher risk of hospitalization and death (including, hypertension, diabetes, heart failure, chronic obstructive pulmonary disease (COPD), cerebrovascular disease or stroke, and obesity). We also controlled for social vulnerability based on where each person lives, using the CDC’s Social Vulnerability Index. The CDC’s Social Vulnerability Index identifies the level of social vulnerability associated with a census area based on 15 social factors, including poverty, income, employment, education, age, household composition, housing, transportation, and racial/ethnic distribution. It was developed to help public health officials and emergency response planners identify and map the communities that will most likely need support before, during, and after a hazardous event.

Among patients who tested positive for COVID-19, people of color remained at increased risk for hospitalization and death after controlling for sociodemographic factors and underlying health conditions. Asian patients were at the highest risk relative to White patients, followed by Hispanic and Black patients. Specifically, Asian patients were 57% more likely to be hospitalized and 49% more likely to die than White patients with the same age, sex, social vulnerability, and comorbidities (Figure 6). Similarly, Hispanic patients were 53% and 30% more likely to be hospitalized and die compared to White patients with similar characteristics and underlying health conditions, and Black patients were 33% and 19% more likely to be hospitalized and die after controlling for these factors. These findings show that differences in these underlying sociodemographic factors and health conditions do not fully explain the higher rates of hospitalization and death experienced by people of color. They suggest that other factors, including racism and discrimination, are negatively affecting COVID-19 health outcomes through additional avenues that are not captured by these measures, as discussed further below.

Figure 6: Risk of Hospitalization and Death among Epic Patients who Tested Positive for COVID-19

Implications

Consistent with other research, these findings show that, among patients across a range of health systems and states, people of color were at significantly increased risk for infection from coronavirus compared to their White counterparts. As previously documented, people of color face increased risk of exposure to coronavirus due to their living, working, and transportation situations. They are more likely to be working in low-income jobs that cannot be done from home, to be living in larger households in densely populated areas, and to utilize public or shared modes of transportation.

Despite being at increased risk of exposure to the virus, people of color did not have markedly higher testing rates compared to White patients and were more likely to be positive when tested and to require a higher level of care at the time they tested positive for COVID-19. These findings suggest that people of color may face increased barriers to testing that contribute to delays in them obtaining testing until they are in more serious condition compared to White patients. Other research suggests that people of color may face longer wait and travel times to access testing and have more limited access to testing within their neighborhood. Moreover, people of color are more likely to be uninsured and to face other barriers to health care, which may contribute to delays in obtaining testing or treatment. The findings from this analysis may understate barriers to testing as they represent active patients who are already connected to a health care system. Individuals who are not connected to a health system or provider may face further barriers to testing and care.

The findings build on previous studies that show people of color are at significantly increased risk for hospitalization and death due to COVID-19 and that these disparities persist after controlling for sociodemographic characteristics and underlying health conditions. These findings, in part, reflect their higher infection rates and higher rates of underlying health conditions that increase their risk of experiencing serious illness if they are infected with the virus. They also may reflect increased barriers to care, which can result in them delaying care and ultimately experiencing more serious conditions. However, this analysis further shows that racial disparities persist among patients who tested positive for COVID-19 after controlling for age, sex, social vulnerability, and comorbidities. Given that a wide body of research has demonstrated that racial health disparities are not driven by biologic differences, this finding suggests that there are other ways racism and discrimination may be negatively affecting COVID-19 health outcomes that are not captured by these measures. For example, research shows that people of color receive poorer quality of care. It also shows that the health care system’s historic mistreatment and abuse of communities of color and ongoing bias and discrimination among providers contribute to negative patient experiences and mistrust of the health care system. Research further suggests that chronic exposure to racism and discrimination create physiological or hormonal responses that negatively affect health (i.e., weathering).

In sum, consistent with a growing body of research, these findings show that people of color are bearing a disproportionate burden of negative health outcomes related to the COVID-19 pandemic at every stage – rates of infection, access to testing, and severity of illness and death. Other analysis also shows that the pandemic is taking a larger economic toll on people of color. While these disparities, in part, reflect social and economic inequities and underlying differences in health, the findings also show that they are not fully explained by these differences. Together, the findings point to the importance of considering health equity in COVID-19 response and relief efforts and health care more broadly, and, in particular, improving access to testing before individuals develop severe illness in order to slow the spread of infections. They also illustrate the importance of efforts to address disparities considering a wide array of factors both within and beyond the health care system and addressing structural and systemic racism and discrimination as root causes. These efforts will be key for narrowing the disparate effects of COVID-19, ensuring equitable distribution of treatments and a vaccine as they are developed, and preventing widening disparities in health care more broadly looking forward.

Methods

The analysis is based on EHRN and KFF analysis of data from the Epic health record system, which includes data for patients from 53 health systems representing 399 hospitals across 21 states. Overall, the system includes data for roughly 55 million active patients. Active patients include those who have interacted with the health system in the past two years, as indicated by either a face-to-face visit or an order placed in their chart. The analysis was restricted to the 89% of active patients who had known race/ethnicity, resulting in a total of roughly 50 million active patients included in the analysis.

The analysis presents findings for Black, Hispanic, Asian, and White patients. Due to data limitations, we do not present findings for smaller population groups, including AIAN and NHOPI patients, or people who report multiple races. As availability of data for smaller population groups increase over time, it may allow for future analysis focused on the experiences of these populations.

We examined testing, infection, hospitalization, and death rates related to COVID-19 among active patients. In addition, we identified the level of care required at the time a patient tested positive for COVID-19 by race and ethnicity.

Further, we performed statistical analysis using data from 332,956 people who tested positive for COVID-19 to examine increased risk of hospitalization and death for Black, Hispanic, and Asian patients relative to White patients after controlling certain sociodemographic characteristics and health conditions known to increase risk of illness and death.

Specifically, we controlled for age, sex, and health conditions that a previous EHRN analysis had identified as being significantly associated with higher risk of hospitalization and death. These conditions included hypertension, diabetes, heart failure, chronic obstructive pulmonary disease (COPD), cerebrovascular disease or stroke, and obesity. The prior EHRN analysis also suggested a significant risk for patients who were immunocompromised. However, that condition was not included in the model due to continued refinements in the definition of an immunocompromised state. In addition, we controlled for social vulnerability based on where each person lives, using the CDC’s Social Vulnerability Index. The CDC’s Social Vulnerability Index identifies the level of social vulnerability associated with a census area based on 15 social factors, including poverty, income, employment, education, age, household composition, housing, transportation, and racial/ethnic distribution. It was developed to help public health officials and emergency response planners identify and map the communities that will most likely need support before, during, and after a hazardous event. Statistical controls were performed using Cox Proportional Hazards models using 95% confidence intervals.

Lily Rubin-Miller, MPH, Christopher Alban, MD, MBA and Sean Sullivan, MS, MPH are with the Epic Health Research Network. Samantha Artiga, MHSA is with KFF.

A new KFF brief provides a comprehensive overview of the coverage and use of fertility services in the United States, highlighting cost and insurance coverage gaps as key barriers faced by low-income people, Black and Hispanic people, LGBTQ individuals, infertile couples and single individuals seeking these services.

The coronavirus pandemic has worsened the availability of medical services and the financial situations of many Americans. Utilization of fertility services has declined, and medical professional societies issued guidelines earlier this year to stop new fertility treatment cycles, non-urgent diagnostic procedures and the criteria to resume such care. However, even before the pandemic several populations experienced disparities in access to such services.

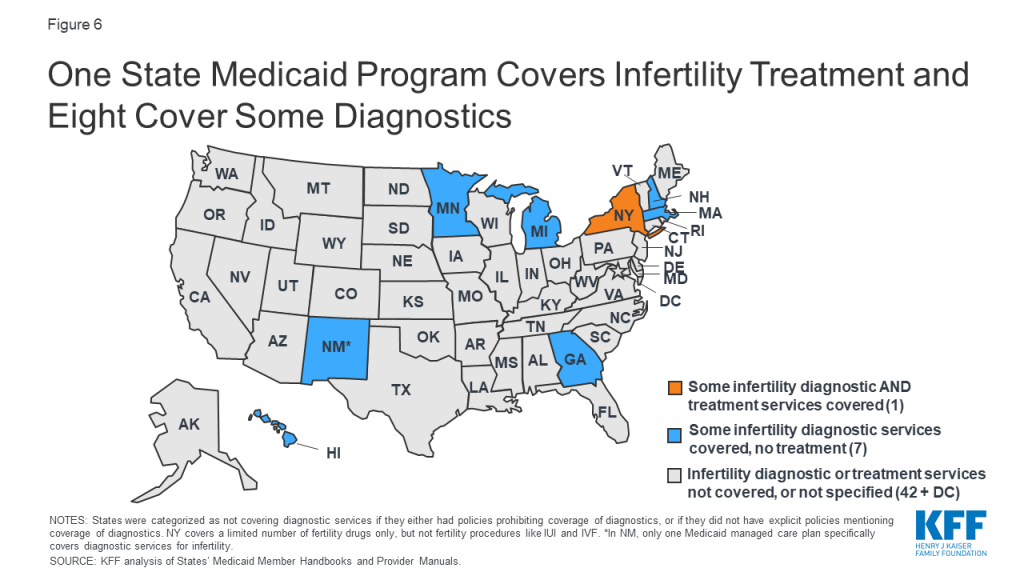

Most patients pay out of pocket for fertility services which typically range in costs based on treatment and duration from the low thousands to tens of thousands of dollars. There is limited coverage of such services by private insurance plans and Medicaid. Fifteen states have laws requiring certain private insurers to cover some infertility treatments and these laws vary widely in the populations eligible and services covered. Only one state, New York, requires its Medicaid program to cover fertility treatment and eight states cover some diagnostic services. Additionally, surveys indicate that about 1 in 5 employers cover some form of infertility treatments.

Many people require fertility assistance. This includes men and women with infertility, many LGBTQ individuals, and single individuals who desire to raise children. An estimated 10% of women report that they or their partners have ever received medical help to become pregnant.

Despite a need for fertility services, fertility care in the U.S. is inaccessible to many due to the cost. More often than not, fertility services are not covered by public or private insurers. Fifteen states require some private insurers to cover some fertility treatment, but significant gaps in coverage remain. Only one state Medicaid program covers any fertility treatment, and no Medicaid program covers artificial insemination or in-vitro fertilization.

Most patients pay out of pocket for fertility treatment, which can amount to well over $10,000 depending on the services received. This means that in the absence of insurance coverage, fertility care is out of reach for many people.

Fewer Black and Hispanic women report ever having used medical services to become pregnant than White women. This is a result of many factors, including lower incomes on average among Black and Hispanic women as well as barriers and misconceptions that may dissuade women from seeking assistance with fertility.

LGBTQ individuals also face heightened barriers to accessing fertility care, as they often do not meet definitions of “infertility” that would qualify them for covered services. Transgender individuals undergoing gender-affirming care may also not meet criteria for “iatrogenic infertility” that would qualify them for covered fertility preservation.

Introduction

Many people require fertility assistance to have children. This could either be due to a diagnosis of infertility, or because they are in a same-sex relationship or single and desire children. While there are several forms of fertility assistance, many services are out of reach for most people because of cost. Fertility treatments are expensive and often are not covered by insurance. While some private insurance plans cover diagnostic services, there is very little coverage for treatment services such as IUI and IVF, which are more expensive. Most people who use fertility services must pay out of pocket, with costs often reaching thousands of dollars. Very few states require private insurance plans to cover infertility services and only one state requires coverage under Medicaid, the health coverage program for low-income people. This widens the gap for low-income people, even when they have health coverage. This brief examines how access to fertility services, both diagnostic and treatment, varies across the U.S., based on state regulations, insurance type, income level and patient demographics.

Diagnosis and Treatment Services

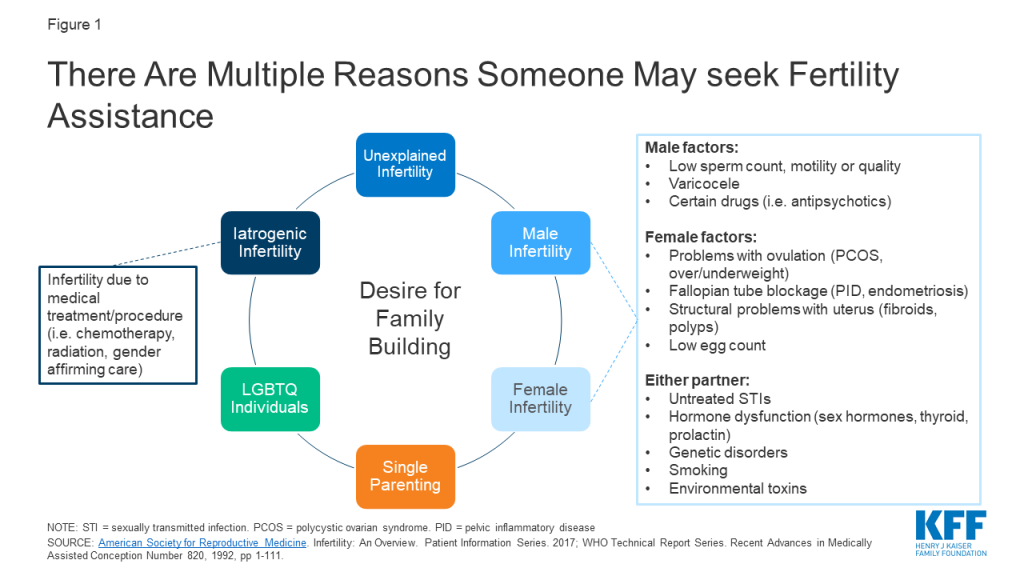

Infertility is most commonly defined1 as the inability to achieve pregnancy after 1 year of regular, unprotected heterosexual intercourse, and affects an estimated 10-15% of heterosexual couples. Both female and male factors contribute to infertility, including problems with ovulation (when the ovary releases an egg), structural problems with the uterus or fallopian tubes, problems with sperm quality or motility, and hormonal factors (Figure 1). About 25% of the time, infertility is caused by more than one factor, and in about 10% of cases infertility is unexplained. Infertility estimates, however do not account for LGBTQ or single individuals who may also need fertility assistance for family building. Therefore, there are varied reasons that may prompt individuals to seek fertility care.

Figure 1: There Are Multiple Reasons Someone May seek Fertility Assistance

A broad array of diagnostic and treatment services may be necessary to assist in fertility (Table 1). Diagnostics typically include lab tests, a semen analysis and imaging studies or procedures of the reproductive organs. If a probable cause of infertility is identified, treatment is often directed at addressing the source of the problem. For example, if someone has abnormal thyroid hormone levels, thyroid medications may help the patient achieve pregnancy. If a patient has large fibroids distorting the uterine cavity, surgical removal of these benign tumors may allow for future pregnancy. Other times, other interventions are needed to help the patient achieve pregnancy. For example, if a semen analysis reveals poor sperm motility or the fallopian tubes are blocked, the sperm will not be able to fertilize the egg, and intrauterine insemination (IUI) or in-vitro fertilization (IVF) may be necessary. These procedures also facilitate family building for LGBTQ and single individuals, with use of donor egg or sperm, with or without a gestational carrier (surrogacy).

NOTES: This is not an exhaustive list of infertility services.SOURCE: ACOG. Evaluating Infertility. 2017; ACOG. Treating Infertility. 2019; American Society for Reproductive Medicine. Infertility: An Overview. Patient Information Series. 2017

Utilization of Fertility Services

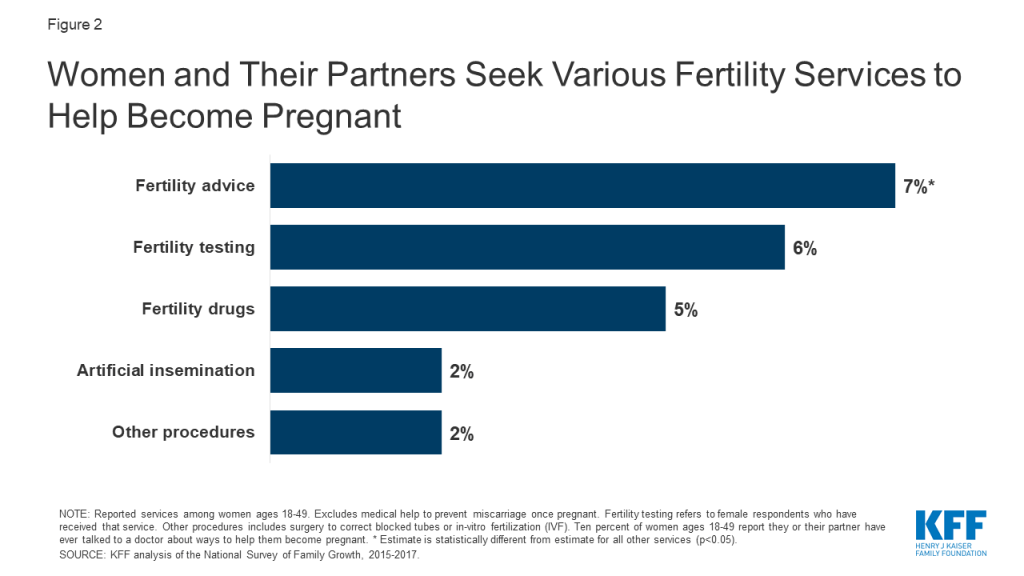

Our analysis of the 2015-2017 National Survey of Family Growth (NSFG) finds that 10% of women2 ages 18-49 say they or their partner have ever talked to a doctor about ways to help them become pregnant (data not shown).3 Among women ages 18-49, the most commonly reported service is fertility advice (Figure 2).

Figure 2: Women and Their Partners Seek Various Fertility Services to Help Become Pregnant

The CDC finds that use of IVF has steadily increased since its first successful birth in 1981. According to the most recent data, an estimated 1.8% of U.S. infants are conceived annually using assisted reproductive technology (ART) (e.g., IVF and related procedures).4 The proportions are highest in the Northeast (MA 4.7%, CN 3.9%, NJ 3.9%), and lower in the South and Southwest (NM 0.4%, AR 0.6%, MS 0.6%).

Utilization of fertility services has dropped drastically during the COVID-19 public health emergency. On March 17, 2020 the American Society for Reproductive Medicine (ASRM) issued guidelines to stop all new fertility treatment cycles and non-urgent diagnostic procedures. Since then, ASRM has provided updated guidance on what conditions should be met and measures should be taken before safely resuming fertility care. During this time, a study by Strata Decision Technology of 228 hospitals across 40 states found patient encounters for infertility services were down 83% from March 22 to April 4, 2020 compared to this time the year prior.

Cost of Services

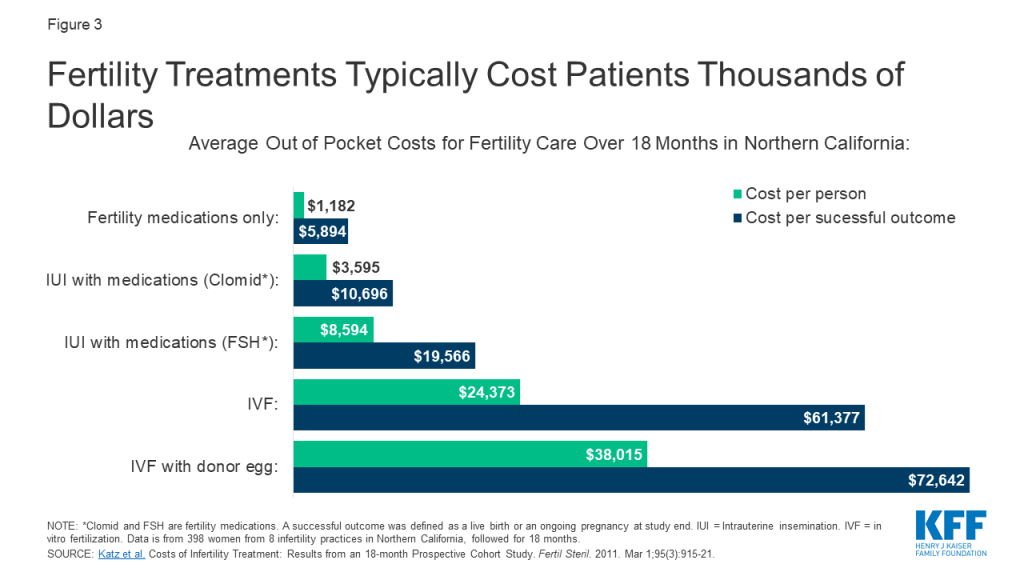

Many patients lack access to fertility services, largely due to its high cost and limited coverage by private insurance and Medicaid. As a result, many people who use fertility services must pay out of pocket, even if they are otherwise insured. Out of pocket costs vary widely depending on the patient, state of residence, provider and insurance plan. Generally, diagnostic lab tests, semen analysis and ultrasounds are less expensive than diagnostic procedures (e.g., HSG) or surgery (e.g., hysteroscopy, laparoscopy). Meanwhile treatment using fertility medications is less expensive than IUI and IVF, but even the less costly treatments can still result in thousands of dollars of out of pocket costs. Many people must try multiple treatments before they or their partner can achieve a pregnancy (typically medication first, followed by surgery or fertility procedures if medications are unsuccessful). A study of nearly 400 women undergoing fertility care in Northern California demonstrates this overall trend, with the lowest out of pocket spending on treatment with medication only and the highest costs for IVF services (Figure 3). Prior research showed the cost of just one standard cycle of IVF was approximately $12,500 in 2009, but is likely higher today due to rising health care costs overall. Furthermore, many patients require several rounds of treatment before achieving a pregnancy, with costs accruing each cycle making these interventions financially inaccessible for many. In addition to costs for the actual treatment, patients can be saddled with out of pocket expenses for office visits, diagnostic tests/procedures, genetic testing, donor sperm/egg use and storage fees and wages lost from time off work.

Figure 3: Fertility Treatments Typically Cost Patients Thousands of Dollars

Insurance Coverage

Insurance coverage of fertility services varies by the state in which the person lives and, for people with employer-sponsored insurance, the size of their employer. Many fertility treatments are not considered “medically necessary” by insurance companies, so they are not typically covered by private insurance plans or Medicaid programs. When coverage is available, certain types of fertility services (e.g., testing) are more likely to be covered than others (e.g., IVF). A handful of states require coverage of fertility services for some fully-insured private plans, which are regulated by the state. These requirements, however, do not apply to health plans that are administered and funded directly by employers (self-funded plans) which cover six in ten (61%) workers with employer-sponsored health insurance. States also have purview over the benefits covered by their Medicaid programs. The federal government has authority over benefit requirements in federal health coverage programs, including Medicare, the Indian Health Service (IHS) and military health coverage.

Private Insurance

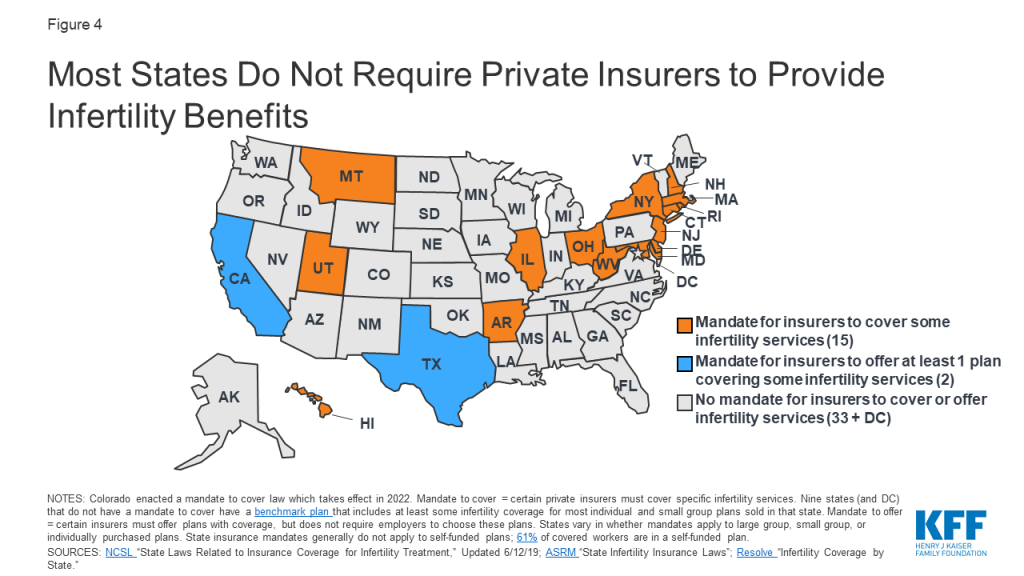

Fifteen states have laws in effect requiring certain health plans to cover at least some infertility treatments (a “mandate to cover”) (Figure 4). Additionally, Colorado recently enacted a requirement for individual and group health benefit plans to cover infertility diagnosis, treatment and fertility preservation for iatrogenic infertility, effective January 2022. Among states that do not have a mandate to cover, nine states5 and DC have a benchmark plan that includes coverage for at least some infertility services (diagnosis and/or treatment) for most individual and small group plans sold in that state.6 Two states (CA and TX7 ) require group health plans to offer at least one policy with infertility coverage (a “mandate to offer”), but employers are not required to choose these plans.

Figure 4: Most States Do Not Require Private Insurers to Provide Infertility Benefits

However, in states with “mandate to cover” laws, these only apply to certain insurers, for certain treatment services and for certain patients, and in some states have monetary caps on costs they must cover (Appendix 1). For example, in OH and WV, the requirement to cover infertility services only applies to health maintenance organizations (HMOs). In other states, almost all insurers and HMOs are included in the mandate. Many states provide exemptions for small employers (<50 employees) or religious employers. In addition, state laws do not apply to self-funded (or self-insured) employer plans, which are regulated by federal law. Sixty-one percent of covered workers are enrolled in a self-funded plan.

Even in states with coverage laws, not all patients are eligible for infertility treatment. In HI, someone with unexplained infertility only qualifies for IVF after five years of infertility. In others, patients are eligible after 1 year. Some states place age limits on female patients who can access these services (e.g., ineligible if 46 or older in NJ or if under age 25 or older than 42 in RI). Others place restrictions based on marital status; for example, until May 2020, IVF benefits were only available to married women in MD. Recently enacted legislation now expands coverage to unmarried women. Additionally, it is not always made clear if LGBTQ individuals meet eligibility criteria for these benefits, without a diagnosis of infertility. Furthermore, many costs associated with surrogacy are often not covered by insurance.

States also vary in which treatment services they require plans to cover. Some states mandate insurers to cover cryopreservation for persons with iatrogenic infertility, while others do not. Four states with insurer mandates do not cover IVF. Eleven states do, but with a dollar limit on coverage (e.g., $15,000 lifetime max in AR and $100,000 in MD and RI) or a limit on the number of cycles they will cover (e.g., one cycle of IVF in HI and three cycles in NY).

Do state mandates for IVF coverage affect use of services?

IVF utilization appears to be higher in states with mandated IVF coverage. CDC data from 2016 showed that in three of the four states deemed by the CDC to have “comprehensive coverage”8 for IVF (IL, MA, NH), use of assisted reproductive technology was 1.5 times higher than the national rate. Similarly, a national study found that IVF availability and utilization9 were significantly higher in states with mandated IVF coverage. A study in MA found IVF utilization increased after implementation of their IVF mandate, but overutilization by patients with a low chance of pregnancy success was not found. State level mandates can also help reduce inequities in access. For example, a recent bill proposed in the CA legislature would reverse existing limitations on fertility coverage and make the benefit available to single women and women in same sex relationships.

What does it cost to cover fertility benefits?

While the costs of fertility treatments can be very expensive for those who lack coverage, the cost of covering fertility benefits varies depending on the services covered and utilization with implications for state budgets, employers, and policy holders. For example, in 2019, New York passed a bill to require IVF and fertility preservation services for comprehensive private health insurance policies. The New York State Department of Financial Services estimated that premiums would increase 0.5% to 1.1% due to mandating IVF coverage, and 0.02% for mandating fertility preservation for iatrogenic infertility (caused by medical treatments).

An analysis of a bill proposed in CA to require private plans and Medi-Cal managed care plans to cover IVF services estimated that per member per month premiums would increase by approximately $5 in the private market and less than a $1.00 for Medi-Cal plans. Overall though, out of pocket spending for individuals seeking services would decrease substantially.

Data from MA, CT and RI suggest that mandating coverage does not appear to raise premiums significantly. All three states have been mandating infertility benefits for over 30 years, and estimate the cost of infertility coverage to be less than 1% of total premium costs. In 2017, California was considering a more limited bill that would require fertility preservation for iatrogenic infertility in certain individual and group health plans. As the bill was introduced, it was estimated to result in a net annual increase of $2,197,000 in premium costs or 0.0015% for enrollees in plans subject to the mandate.

While these costs could be modest in comparison to the costs of paying out-of-pocket for these services, there are other costs to coverage mandates. The ACA requires states to offset some of the costs for any state mandated benefits beyond essential health benefits (EHBs) in the individual and small group market. This requirement was estimated to cost NY $59 to $69 million per year if covering one cycle or $98 to $116 million per year if covering unlimited cycles of IVF.

What share of employers offer fertility benefits?

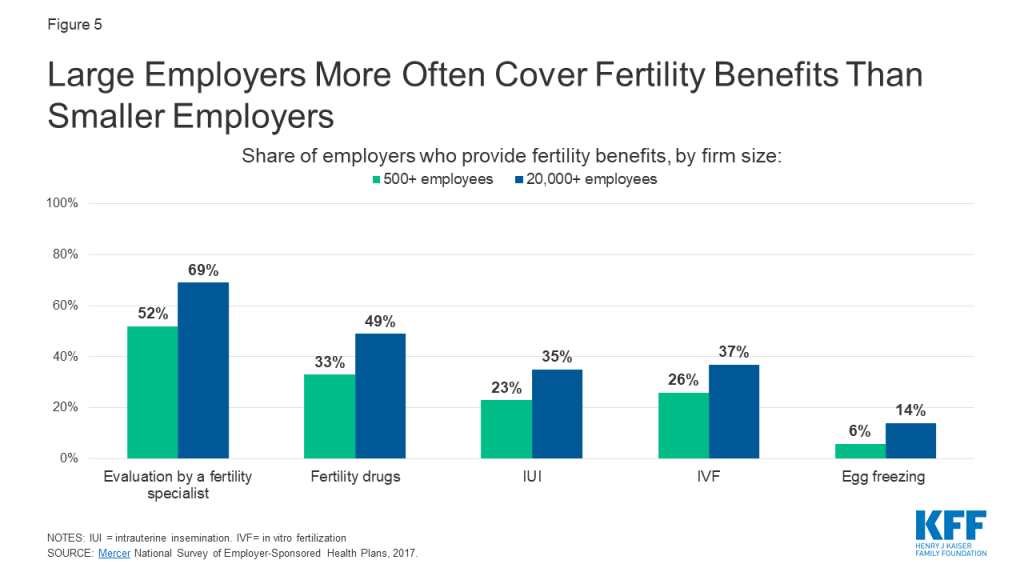

Large employers are more likely than smaller employers to include fertility benefits in their employer-sponsored health plans. According to Mercer’s 2017 National Survey of Employer-Sponsored Health Plans, 56% of employers with 500 or more employees cover some type of fertility service, but most do not cover treatment services such as IVF, IUI, or egg freezing. Coverage is higher for diagnostic evaluations and fertility drugs. Coverage is more common among the largest employers and those that offer higher wages (Figure 5).

Figure 5: Large Employers More Often Cover Fertility Benefits Than Smaller Employers

Public Coverage

Medicaid

NSFG data show that significantly fewer women with Medicaid have ever used medical services to help become pregnant compared to women with private insurance. As of January 2020, our analysis of Medicaid policies and benefits reveal only one state, New York, specifically requires their Medicaid program to cover fertility treatment (limited to 3 cycles of fertility drugs) (Figure 6). However, some states may require Medicaid to cover treatments for conditions that impact fertility, while not directly stated in their policies. For example, states may cover thyroid medications, or cover surgery for fibroids, endometriosis or other gynecologic abnormalities if causing pelvic pain, abnormal bleeding or another medical problem, other than infertility. No state Medicaid program currently covers artificial insemination (IUI), IVF, or cryopreservation (Appendix 2).

Some states specifically cover infertility diagnostic services; GA, HI, MA, MI, MN, NH, NM and NY all offer at least one Medicaid plan with this benefit, but the range of diagnostics covered varies. For example, New York Medicaid specifically covers office visits, HSGs, pelvic ultrasounds and blood tests for infertility. Meanwhile, the infertility assessment covered by Georgia Medicaid includes lab testing, but not imaging or procedural diagnostics. Other states specifically do not cover infertility diagnostics, or more generally do not cover “infertility services,” which likely includes diagnostics. Others do not mention infertility diagnostics in their Medicaid policies, meaning the beneficiary would need to check with their Medicaid program to see if these services are covered (Appendix 2).

The Medicaid program’s lack of coverage of fertility assistance has a disproportionate impact on women of color. Among reproductive age women, the program covers three in ten (30%) who are Black and one quarter who are Hispanic (26%), compared to 15% who are White. Because eligibility for Medicaid is based on being low-income, people enrolled in the program likely could not afford to pay for services out of pocket.

The relative lack of Medicaid coverage for fertility services stands in stark contrast to Medicaid coverage for maternity care and family planning services. Nearly half of births in the U.S. are financed by Medicaid, and the program finances the majority of publicly-funded family planning services. Therefore, while there is broad coverage of many services for low-income people during pregnancy and to help prevent pregnancy, there is almost no access to help low-income people achieve pregnancy.

Figure 6: One State Medicaid Program Covers Infertility Treatment and Eight Cover Some Diagnostics

Medicare

While most beneficiaries of Medicare are over the age of 65+, Medicare also provides health insurance to approximately 2.5 million reproductive age adults with permanent disabilities. According to the Medicare Benefit policy manual, “reasonable and necessary services associated with treatment for infertility are covered under Medicare.” However, specific covered services are not listed, and the definition of “reasonable and necessary” are not defined.

Military

TRICARE: TRICARE, the insurance program for military families, will cover some infertility services, if deemed “medically necessary” and if pregnancy is achieved through “natural conception,” meaning fertilization occurs through heterosexual intercourse. Diagnostic services are covered, including lab testing, genetic testing, and semen analysis. Treatment to correct physical causes of infertility are also covered. However, IUI, IVF, donor eggs/sperm and cryopreservation are not typically covered, unless the service member had a serious injury while on active duty resulting in infertility.

Veterans Affairs (VA): Infertility services are covered by the VA medical benefits package, if infertility resulted from a service-connected condition. This includes infertility counseling, blood tests, genetic counseling, semen analysis, ultrasound imaging, surgery, medications and IVF (as of 2017). However, the couple seeking services must be legally married, and the egg and sperm must come from said couple (effectively excluding same sex couples). Donor eggs/sperm, surrogacy or obstetrical care for non-Veteran spouses are not covered.

Infertility Services In Publicly Funded Clinics

The CDC’s and Office of Population Affairs’ (OPA) Quality Family Planning recommendations address provision of basic infertility services. Family planning providers are recommended to provide at minimum patient education about fertility and lifestyle modifications, a thorough medical history and physical exam, semen analysis, and if indicated, referrals for lab testing of hormone levels, additional diagnostic tests (endometrial biopsy, ultrasound, HSG, laparoscopy) and prescription of medications to promote fertility. However, studies of publicly funded family planning clinics suggest that availability of infertility services is uneven. In a 2013-2014 study of 1615 publicly funded clinics, a high share reported offering preconception care (94% for women and 69% for men), but fewer offered any basic infertility services (66% for women and 45% for men). Provision of any infertility treatment was uncommon (16% of clinics), likely requiring referrals to specialists who may not accept Medicaid or uninsured patients.10 The majority of patients who rely on publicly funded clinics are low-income and would not likely be able to afford infertility services and treatments once diagnosed.

Per the Indian Health Services (IHS) provider manual, basic infertility diagnostics should be made available to women and men at IHS facilities, including a history, physical exam, basal temperature charting (to predict ovulation), semen analysis and progesterone testing. In facilities with OBGYNs, HSG, endometrial biopsy and diagnostic laparoscopy should also be available. However, it is unclear how accessible these services are in practice, and provision of infertility treatment is not mentioned.

Key Populations

Racial and ethnic minorities

The ability to have and care for the family that you wish for is a fundamental tenet of reproductive justice. For those who need it, this includes access to fertility services. The share of racial and ethnic minorities who utilize medical services to help become pregnant is less than that of non-Hispanic White women, despite research that has found higher rates of infertility among women who are Black and American Indian / Alaska Native (AI/AN). Our analysis of 2015-2017 NSFG data shows that while 13% of non-Hispanic White women reported ever going to a medical provider for help getting pregnant, just 6% of Hispanic women and 7% of non-Hispanic Black women did so (Figure 7). A higher share of Black and Hispanic women are either covered by Medicaid or uninsured than White women and more women with private insurance sought fertility help than those with Medicaid or the uninsured. A variety of factors, including differences in coverage rates, availability of services, income, and service‐seeking behaviors, affect access to infertility care. Furthermore, other societal factors also play a role. Misconceptions and stereotypes about fertility have often portrayed Black women as not requiring fertility assistance. Combined with the history of discriminatory reproductive care and harm inflicted upon many women of color over decades, some may delay seeking infertility care or may not seek it at all.

Figure 7: Women Seeking Help to Become Pregnant Tend to Be Age 35+, White, Higher Income, and Privately Insured

Other research has found that use of fertility testing and treatment also varies by race. An analysis of NSFG data found that among women who reported using medical services to help become pregnant, similar shares of Black (69%), Hispanic (70%) and White (75%) women received fertility advice. However, less than half (47%) of Black and Hispanic women who used medical services to become pregnant reported receiving infertility testing, compared to 62% of White women, and even fewer women of color received treatment services. According to an analysis of surveillance data of IVF services, use is highest among Asian and White women and lowest among American Indian / Alaska Native (AI/AN) women. Racial inequities may exist for fertility preservation as well; a study of female patients in NY with cancer found disproportionately fewer Black and Hispanic patents utilized egg cryopreservation compared to White patients. On average, more Black, Hispanic, and AI/AN people live below the federal poverty level than people who are White or of Asian/Pacific Islander descent. The high cost and limited coverage of infertility services make this care inaccessible to many people of color who may desire fertility preservation, but are unable to afford it.

Iatrogenic Infertility

Iatrogenic, or medically induced, infertility refers to when a person becomes infertile due to a medical procedure done to treat another problem, most often chemotherapy or radiation for cancer. In these situations, persons of reproductive age may desire future fertility, and may opt to freeze their eggs or sperm (cryopreservation) for later use. The American Society for Reproductive Medicine (ASRM) encourages clinicians to inform patients about fertility preservation options prior to undergoing treatment likely to cause iatrogenic infertility.

However, the cost of egg or sperm retrieval and subsequent cryopreservation can be prohibitive, particularly if in the absence of insurance coverage. Only a handful of states (CT, DE, IL, MD, NH, NJ, NY, and RI) specifically require private insurers to cover fertility preservation in cases of iatrogenic infertility. No states currently require fertility preservation in their Medicaid plans.

LGBTQ populations

LGBTQ people may face heightened barriers to fertility care, and discrimination based on their gender identity or sexual orientation. Section 1557 of the Affordable Care Act (ACA) prohibits discrimination in the health care sector based on sex, but the Trump Administration has eliminated these protections through regulatory changes. Without the explicit protections that have been dropped in the current rules, LGBTQ patients may be denied health care, including fertility care, under religious freedom laws and proposed changes to the ACA. However, these changes are being challenged in the courts because they conflict with a recent Supreme Court decision stating that federal civil rights law prohibits discrimination based on sexual orientation and gender identity.

In a committee opinion, ASRM concluded it is the ethical duty of fertility programs to treat gay and lesbian couples and transgender persons, equally to heterosexual married couples. They write that assisted reproductive therapy should not be restricted based on sexual orientation or gender identity, and that fertility preservation should be offered to transgender people before gender transitions. This allows transgender individuals the ability to have biological children in the future if desired. Despite this recommendation, in aforementioned states with mandated fertility preservation coverage for iatrogenic infertility, it remains unclear if this benefit extends to transgender individuals, whose gender affirming care can result in infertility. Additionally, many state laws regarding mandates for infertility treatment contain stipulations that may exclude LGBTQ patients. For example, in Arkansas, Hawaii and Texas and at the VA, IVF services must use the couple’s own eggs and sperm (rather than a donor), effectively excluding same sex couples. In other states, same-sex couples do not meet the definition of infertility, and thus may not qualify for these services. Data are lacking to fully capture the share of LGBTQ individuals who may utilize fertility assistance services. Research studies on family building are often not designed to include LGBTQ respondents’ fertility needs.

Single Parents

Single persons are often excluded from access to infertility treatment. For example, the same IVF laws cited above that require the couple’s own sperm and egg, effectively exclude single individuals too, as they cannot use donors. Some grants and other financing options also stipulate funds must go towards a married couple, excluding single and unmarried individuals. This is in opposition to the ASRM committee opinion, which states that fertility programs should offer their services to single parents and unmarried couples, without discrimination based on marital status.

Looking Forward

On a federal level, efforts to pass legislation to require insurers to cover fertility services are largely stalled. The proposed Access to Infertility Treatment and Care Act (HR 2803 and S 1461), which would require all health plans offered on group and individual markets (including Medicaid, EHBP, TRICARE, VA) to provide infertility treatment, is still in committee (and never made it out of committee when proposed during the 115th congress). There has been some more movement on the state level. Some states require private insurers to cover infertility services, the most recent of which was NH in 2020. Currently, NY continues to be the first and only state Medicaid program to cover any fertility treatment.

For those who desire to have children, obtaining fertility care can be a stressful process. Stigma around infertility, intensive and sometimes long or painful treatment regimens, and uncertainty about success can take a toll. On top of that, in the absence of insurance coverage, infertility care is cost prohibitive for most, particularly for low-income people and for more expensive services, like IVF or fertility preservation. Significant disparities exist within access to infertility services across, dictated by state of residence, insurance plan, income level, race/ethnicity, sexual orientation and gender identity. Achieving greater equity in access to fertility care will likely depend on addressing the needs faced by low-income persons, people of color and LGBTQ persons in fertility policy and coverage.

Appendices: Appendix 1: Private Insurance

Appendix 1: States That Require Private Insurance Coverage of Infertility Services

Infertility coverage required:(As of May 2020)

State (Statute year)

By which insurers?

For which indications?

For which treatments?

AR

(1987, 2011)

Included: all individual and group insurers*

Excluded: HMOs; self-insurers

Eligible: Infertility due to male factor, endometriosis, blocked fallopian tube (or unexplained for 2 years)

Ineligible: if egg/sperm not from spouse

Covered: IVF (lifetime max $15,000)

Not covered: Fertility preservation for iatrogenic infertility

CA

(1990)

Mandate to offer, not cover: group insurers must let employers know coverage for diagnostic tests and some treatment is available (excludes IVF and fertility preservation), but employers do not need to provide coverage to employees

CO

(Effective 2022)

Passed House Bill 20-1148 in April 2020 to mandate coverage for infertility diagnosis and treatment, and fertility preservation for iatrogenic infertility. Applies to all individual and group health benefit plans renewed or issued after January 1, 2022, but religious employer may request exemption.

CT

(1989, 2005)

Included: Health insurance organizations

Excluded: Persons on plan for <12 months; religious employers; self-insurers

Eligible: Infertility for 1 year or iatrogenic infertility

Not Covered: Lifetime max of 4 cycles of ovulation induction, 3 cycles of IUI

DE

(2018)

Included: Individual and group insurers, HMOs **

Excluded: <50 employees; religious employers; self-insurers

Eligible: Infertility or iatrogenic infertility

Covered: consultation, diagnostics, medications, IUI, IVF and other treatments; fertility preservation for iatrogenic infertility

Not Covered: Egg retrieval after age 45, >6 egg retrievals, surrogacy compensation, reversal of voluntary sterilization

HI

(1989, 2003)

Included: Individual and group insurers

Excluded: self-insurers

Eligible: 5 years of unexplained infertility, OR infertility due to male factors, endometriosis, blocked/ removed fallopian tubes

Ineligible: if egg/sperm not from spouse

Covered: 1 cycle of IVF, all outpatient expenses arising from IVF

IL

(1991, 1996)

Included: Group insurers and HMOs*; individual insurers for iatrogenic infertility

Excluded: <25 employees; religious employers; self-insurers

Eligible: 1 year of infertility or iatrogenic infertility

Covered: Diagnostics, IUI, IVF, and other treatments; fertility preservation for iatrogenic infertility

Not Covered: More than 6 egg retrievals

MD

(2000)

Included: Individual and group insurers*

Excluded: <50 employees; religious employers; self-insurers

Eligible: Infertility due to male factor, endometriosis, blocked/removed fallopian tubes (or if unexplained for 2 years)

Covered: 3 cycles of IVF per life birth (lifetime max $100,000); fertility preservation for iatrogenic infertility

Not Covered: Storage of sperm/eggs

MA

(1987, 2010)

Included: All insurers and HMOs*

Excluded: self-insurers

Eligible: Infertility for 1 year if age <35, 6 months if 35+

Covered: IUI, IVF, cryopreservation and others (no lifetime limit on cost or cycles)

Not Covered: Surrogacy, reversal of sterilization

MT

(1987)

Included: HMOs

Excluded: all other insurers

Eligible: No definition of infertility

Covered: must cover “infertility services,” does not define which

NH

(2020)

Included: Group insurers***

Excluded: Small business health options program; extended transition to ACA- programs; self-insurers

Eligible: Ability to become/cause pregnancy is impaired

Covered: Diagnostics, treatment including medications, egg/sperm procurement; fertility preservation for iatrogenic infertility

Not Covered: reversal of voluntary sterilization; some aspects of care if surrogate involved

NJ

(2001)

Included: Group insurers; HMOs; State Health Benefits Program; School Employees Health Benefits Program*

Excluded: <50 employees; religious employers; self-insurers

Eligible: Infertility for 1 year if age <35, 6 months if 35+; single female unable to conceive with 12 IUIs if <35, 6 IUIs if >35; persons involuntarily sterilized

Ineligible: >46 years old

Covered: diagnostics, medications, surgery, IUI, IVF, and other treatments (max 4 egg retrievals per lifetime)

Not Covered: reversal of voluntary sterilization; cryopreservation

NY

(1990, 2002, 2020)

Included: Large group insurance market for IVF (>100 employees); all commercial markets for cryopreservation

Excluded: Individual and small group markets for IVF; self-insurers

Eligible: Infertility for 1 year if age <35, 6 months if 35+

Ineligible:

Covered: diagnostic procedures, medications, 3 cycles of IVF; fertility preservation if iatrogenic infertility

Not Covered: surrogacy, reversal of elective sterilization

OH

(1991)

Included: HMOs

Excluded: all other insurers

Eligible: No definition of infertility

Covered: diagnostic and exploratory procedures to correct cause for infertility (endometriosis, blocked fallopian tube, testicular failure)

Not Covered: IVF and other treatments

RI

(1989, 2007)

Included: Insurers and HMOs*

Excluded: Self-insurers

Eligible: Infertility for 1 year; iatrogenic infertility

Ineligible: women aged <25 of >42 (unless for fertility preservation)

Covered: diagnostics and treatment, including IVF; fertility preservation for iatrogenic infertility (up to 20% copay allowed)

Not Covered: >$100,000 on treatment

TX

(1987, 2003)

Mandate to offer, not cover: Group insurers must offer IVF as a benefit, employers can choose whether or not to include it. If choose to include, must be egg/sperm from spouse.

UT

(2014)

Included: Insurers*

Excluded: Self-insurers

Eligible: no definition of infertility; persons wishing to adopt

Covered: $4000 adoption indemnity, can also be used for infertility treatment

WV

(1995)

Included: HMOs

Excluded: all other insurers

Eligible: no definition of infertility

Covered: must cover “infertility services,” does not define which

NOTES: *Insurers must cover if they also provide pregnancy-related benefits. ** Must cover infertility services to same extent as other pregnancy-related services. ***Must cover if also provide medical/hospital expenses.AL, AK, AZ, CO, DC, FL, GA, ID, IN, IA, KS, KY, LA, ME, MI, MN, MS, MO, NE, NV, NM, NC, ND, OK, OR, PA, SC, SD, TN, VT, VA, WA, WI, and WY do not require private insurers to cover infertility treatments.SOURCES: NCSL. State Laws Related to Insurance Coverage for Infertility Treatment. 6/12/2019; American Society for Reproductive Medicine (ASRM). State Infertility Insurance Laws; Resolve. Infertility Coverage by State; Colorado House Bill 20-1158

Appendices: Appendix 2: Medicaid

Appendix 2: State Medicaid Coverage of Infertility Services

Covered and Non-Covered Services by State(As of January 2020)

Not Covered: Infertility studies/procedures for diagnosing/treating infertility (Family Planning Manual)

CO

Covered: Basic fertility and reproductive health counseling is provided (Family Planning Services Benefits)

Not Covered: Sterilization reversal. Infertility treatment, counseling and testing. Tests normally associated with infertility management (e.g., HSG and semen analysis) covered only to confirm success of a sterilization

CT

Covered: Lab tests to detect the presence of conditions affecting reproductive health (Member Handbook)

Covered: infertility diagnosis/treatment when infertility is a symptom of a suspected medical problem (e.g., thyroid disease). No coverage if the sole purpose is achieving pregnancy (Physician services)

Covered: infertility office visits, diagnosis (HSG, pelvic ultrasounds, lab tests), fertility drugs (bromocriptine, clomiphene citrate, letrozole, tamoxifen). Limited to 3 cycles of treatment per lifetime (Infertility Benefit)

Not Covered: Infertility treatments beyond those described above.

NC

Not Covered: Infertility services and related procedures. Services to manage/treat complications of women’s health problems, including heavy bleeding or infertility (Family Planning Services)

ND

Not Covered: Diagnostic, medical, surgical or pharmaceutical services related to infertility. Removal of long acting reversible contraceptive devices to regain fertility (Provider manual)

Not Covered: Will not pay for medical procedures if goal is fertility (semen analysis, fallopian tube repair, laparoscopy). Covered if reproductive system disease requires treatment to maintain overall health, and is medically necessary (Provider Manual). No fertility drugs (Pharmacy manual)

NOTES: * Benefits vary between Medicaid managed care plans. Information collected on individual Medicaid managed care plans when information on fertility benefits not found in member benefits or provider manuals pertaining to all Medicaid plans.ⱡ OR covers basic infertility counseling as part of The Oregon Reproductive Health Program for low income women, but not a Medicaid benefitSOURCES: Information compiled from member handbooks and provider manuals as linked above, available online as of January 2020 (see links above).

Endnotes

The evaluation of fertility can start after six months if the woman is over the age of 35. ↩︎

Data and research often assume cisgender identities and may not systematically account for people who are transgender and non-binary. The language used in this brief attempts to be as inclusive as possible while acknowledging that the data we are citing uses gender labels that we cannot change without misrepresenting the data. ↩︎

The CDC reports the percentage of women (ages 15-49) who have ever received “infertility services” (12.7%) which also includes medical help to prevent miscarriage. We report on the percentage of adult women (ages 18-49) who have ever received medical help to become pregnant, excluding medical help once women are already pregnant. ↩︎

The CDC does not track the number of births as a result of other fertility assistance, like fertility medications or IUI. However, in the 2012 CDC National Public Health Action Plan for the Detection, Prevention and Management of Infertility, they recommended the development of surveillance systems which would monitor the utilization and health outcomes of non-IVF treatment for infertility. ↩︎

IL has a mandate to cover that applies only to group plans; however, the state’s benchmark plan includes coverage for infertility treatment, so individual plans in IL also cover these services. ↩︎

The TX benchmark plan includes coverage for diagnosis of infertility, so individual plans in TX also cover this service. ↩︎

“Comprehensive coverage” for ART defined by CDC as covering at least four oocyte (egg) retrievals. ↩︎

Availability was judged by the number of physicians performing IVF per 1,000 reproductive age women, and utilization was calculated by number of IVF cycles per 100,000 reproductive age women. ↩︎

Definitions of preconception care, basic infertility services and infertility treatment were left up to the interpretation of the respondent. ↩︎

With planning beginning for an eventual COVID-19 vaccine, one important consideration is making sure that distribution processes and outreach and communication strategies reach people of color. COVID-19 vaccination among people of color will be particularly important because they are bearing a heavy, disproportionate burden of the disease, and population immunity is not likely to be reached without high vaccination rates across all communities. However, doing so will require public health officials and providers to overcome a range of barriers to vaccination among people of color, many of which are rooted in a historic legacy of abuse and mistreatment by the medical system and ongoing racism and discrimination today.

Analysis of seasonal flu vaccination rates provides some insight into the potential barriers and issues to be addressed as part of COVID-19 vaccination efforts. Experts recommend an annual flu vaccination for all people age 6 months and older as the primary way to prevent sickness and death caused by the flu, and Healthy People 2030 national health objectives set a goal of vaccinating at least 70% of this population. Despite being widely recommended and fully covered as a preventive service under the Affordable Care Act (ACA), data show that overall flu vaccination rate remains low and that there are persistent racial disparities in uptake of the vaccine.

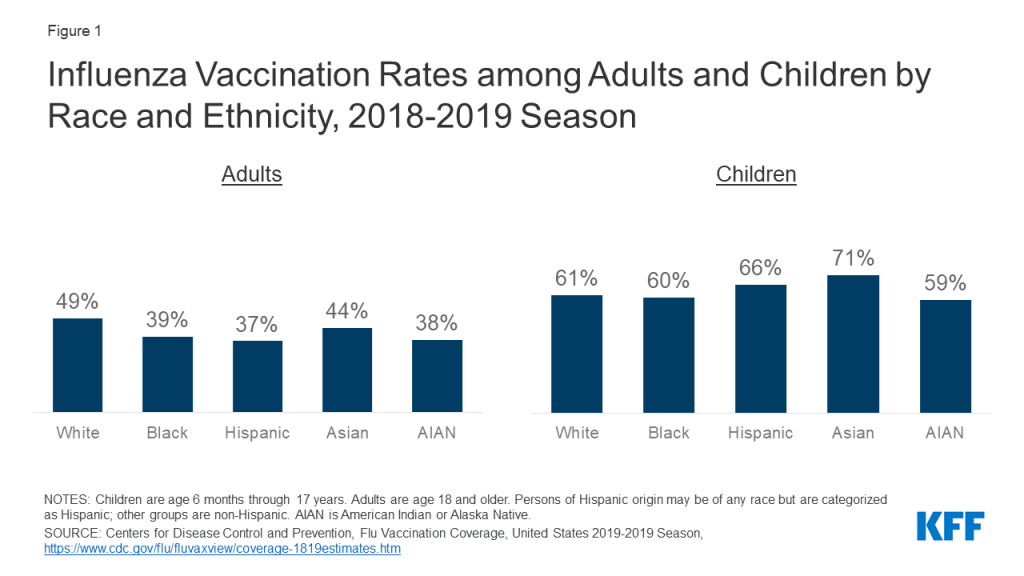

Analysis of flu vaccination rates shows persistent gaps and racial disparities in flu vaccination among adults. Data from the Centers for Disease Control and Prevention (CDC) show that the flu vaccination rate generally has been increasing over time but remains below the target level, with lower rates of vaccination among Black and Hispanic individuals compared to White individuals. These gaps and racial disparities in vaccination are concentrated among adults. During the 2018-2019 flu season, less than four in ten Black (39%), Hispanic (37%), and AIAN (38%) adults were vaccinated compared to nearly half of White adults (49%) (Figure 1). Vaccination rates were higher among children compared to adults and the rates for children of color were generally equal to or higher than those for White children.

Figure 1: Influenza Vaccination Rates among Adults and Children by Race and Ethnicity, 2018-2019 Season

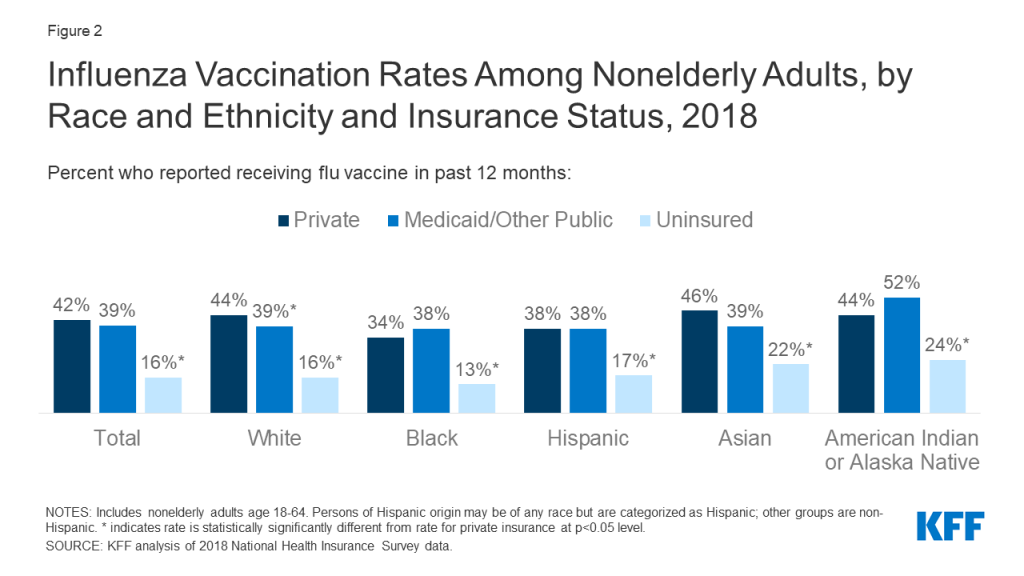

The lower vaccination rates among adults of color, in part, reflect their higher uninsured rates.Data show that people of color are more likely be uninsured and less likely to have a usual source of care. Seasonal flu vaccines, especially for adults, are delivered and administered primarily through a system of private distributors and providers. As a preventive service under the ACA, the vaccine is available at no charge for individuals with insurance. However, uninsured individuals either need to pay out-of-pocket for the vaccine or identify sites, such as clinics or health centers, that are offering it for free. Evidence suggests that the federally-funded Vaccines for Children (VFC) program, which provides vaccines at no cost to children who might not otherwise be vaccinated because of inability to pay, has contributed to the higher vaccination rates among children across racial and ethnic groups. However, analysis of National Health Interview Survey data illustrates the barriers to vaccination facing uninsured adults. Across racial and ethnic groups, uninsured adults were less likely to be vaccinated compared to those with private coverage (Figure 2). Vaccination rates among adults with Medicaid coverage were similar to those with private coverage across most groups.

Figure 2: Influenza Vaccination Rates Among Nonelderly Adults, by Race and Ethnicity and Insurance Status, 2018

Research also shows that distrust, safety concerns, and experiences with discrimination and other factors contribute to disparities in vaccination rates. For example, research shows that, compared to White adults, African American adults perceive a higher risk of side effects from the seasonal flu vaccine, have less knowledge about the vaccine, and have less trust in the vaccine. Another study found that African Americans were more likely than any other group to cite concern over the vaccine causing influenza or serious side effects as the main reason for non-vaccination. Other research shows that African American and AIAN individuals were less likely than White individuals to say they believed the 2009 H1N1 influenza vaccine was “very safe.” Another study found that the majority of people would not accept a new but not yet fully approved vaccine, with Black individuals expressing the highest level of worry. Research also points to variation among Black individuals in willingness to obtain a vaccination, for example, finding that older adults were more likely to have attitudes that increase vaccine acceptance. Additional research finds that perceptions of racial fairness and the influence of race in health care settings as well as experiences with discrimination are associated with attitudes and beliefs about the flu vaccine that may influence willingness to obtain it. Beyond differences in beliefs and attitudes, other work suggests people of color may have more “missed opportunities” for flu vaccination, finding that adults of color were more likely to remain unvaccinated compared to White adults even when they had at least one health care visit during the flu season and indicated that they would be willing to get vaccinated if a healthcare provider strongly recommended it.

Together these findings show that once a COVID-19 vaccine becomes available, accomplishing a high vaccination rate will require addressing multiple barriers to vaccination among people of color, including access-related challenges and distrust and safety concerns. Under federal law, insurers must make the COVID-19 vaccine available at no cost. The Trump administration has also indicated it will make the vaccine available to uninsured individuals at no cost, but questions remain about whether there is sufficient funding to cover these costs. Beyond addressing cost barriers, it also will be important to make the vaccine easily accessible at convenient locations and to ensure people know where and how to access it free of charge. Moreover, effective outreach and media strategies will be important to build public trust and willingness to get the vaccine. People of color’s distrust of the health care system, particularly among Black individuals, reflects the historical legacy of the system’s abuse and mistreatment of people of color and ongoing racism and discrimination today. Distrust and safety concerns are likely to be further compounded in the context of COVID-19 vaccination efforts since the majority of the public is concerned that political pressure from the Trump administration will lead the Food and Drug Administration to rush to approve a vaccine without making sure that it is safe and effective. Research suggests that health care providers and public health agencies can increase education about vaccine recommendations and that health care providers can increase vaccine acceptance by recommending and offering a vaccine at the same time. Previous public health and health coverage enrollment experience further points to the importance of providing information in linguistically and culturally appropriate ways, proactively addressing people’s concerns, and using trusted individuals from the community as messengers. Even with targeted strategies, it likely will be difficult to overcome distrust and safety concerns, further amplifying the importance of using trusted messengers to share information and conduct outreach to the community.

From the Federal Response to COVID-19 to Ongoing Efforts to Repeal the ACA and Proposals for Lowering Drug Prices, President Trump Has an Extensive Record on Health Care

Since taking office in 2017, President Trump has laid down an extensive record on health care, including his response to the COVID-19 pandemic, his early and ongoing efforts to repeal and replace the Affordable Care Act, his annual budget proposals to curb spending on Medicare and Medicaid, his executive orders and other proposals to lower prescription drug prices, and his initiative on hospital price transparency.