Ten Ways That the House American Health Care Act Could Affect Women

Issue Brief

10 Ways That Repealing and Replacing the ACA Could Affect Women

Women have much at stake as the nation debates the future of coverage in the United States. Because the Affordable Care Act (ACA) made fundamental changes to women’s health coverage and benefits, changes to the law and the regulations that stem from it would have a direct impact on millions of women with private insurance and Medicaid. On May 4, 2017, the House of Representatives passed the American Health Care Act (AHCA), to repeal and replace elements of the ACA (Appendix Table 1). It would eliminate individual and employer insurance mandates, effectively end the ACA Medicaid expansion, cap federal funds for the Medicaid program, make major changes to the federal tax subsidies available to assist individuals who purchase private insurance, and ban federal Medicaid funds from going to Planned Parenthood. It would also allow states to waive the ACA’s Essential Health Benefits requirements and permit health status as a factor in insurance rating for individuals who do not maintain continuous coverage with the goal of reducing insurance costs.1 The Senate will now take up legislation to repeal and replace the ACA and may consider several elements that the House has approved in the AHCA. This brief reviews the implications of the AHCA for women’s access to care and coverage.

ACA’s Impact on Coverage and Access for Women

Since the ACA’s passage, the uninsured rate has declined to record low levels. Between 2013 and 2015, the uninsured rate among women ages 19 to 64 fell from 17% to 11% (Figure 1). This drop was due in large part to the Medicaid expansion that was adopted by 31 states and DC, and the availability of federal tax credits to subsidize premium costs for many low and modest-income women and men. In addition to coverage improvements, fewer women face affordability barriers since the ACA was enacted. Women have consistently been more likely than men to report that they delay or go without needed care because of costs. The ACA addressed some of these financial barriers by providing subsidies for premiums and cost sharing, eliminating out of pocket costs for preventive services, lifting the lifetime limits on expenses insurance will cover, and requiring minimum levels of coverage for ten Essential Health Benefit categories. Since its passage, the share of women who report that they delayed or went without care due to costs has fallen (Figure 2). This drop has been particularly marked among low-income women, although costs continue to be a greater challenge for this group as well.

1. Medicaid Eligibility: Expansion and Work Requirements

Medicaid has been the foundation of coverage gains under the ACA. Eliminating federal funds for the ACA’s Medicaid expansion could leave many of the nation’s poorest women without a pathway to coverage.

Women comprise the majority of Medicaid beneficiaries—before the passage of the ACA and today. Prior to the ACA, compared to men, women were more likely to qualify for Medicaid because of their lower incomes and because they were more likely to meet one of the program’s eligibility categories: pregnancy, parent of a dependent child, over 65, or disability. The ACA eliminates the program’s “categorical” requirements, allowing states to extend Medicaid eligibility to all individuals based solely on income. In the 31 states and DC that have chosen to expand Medicaid, individuals with household incomes up to 138% of the Federal Poverty Level (FPL) qualify, and the federal government finances 95% of the costs.2

It is estimated that by 2015, 11 million adults had gained coverage as a result of the ACA’s Medicaid expansion. This opened the door for continuous coverage to pregnant women who often became ineligible for coverage 60 days after the birth of their baby and had no other pathway to coverage as new mothers. The Medicaid expansion has also helped women who do not have children gain access to coverage, since before the expansion they were ineligible for coverage in most states. If passed, the AHCA bill would withdraw the enhanced federal funds for the Medicaid expansion except for beneficiaries enrolled as of December 31, 2019 who do not have a break in eligibility for more than 1 month. This loss of federal financing would leave states without the funds needed to continue supporting this expansion, potentially forcing some states to roll back eligibility for parents to the very low levels that were in place before the ACA (Figure 3). For example, a single mother of two living in Louisiana or Indiana would not have qualified for Medicaid if her income exceeded $4,687. The Congressional Budget Office (CBO) estimates that, under the House AHCA bill, some states that have already expanded their Medicaid programs would not continue that coverage (some states might also begin to reduce coverage prior to 2020), and that no new states will adopt the expansion.

The AHCA bill would also amend the federal Medicaid statute to allow states to require some beneficiaries, including parents of children 6 and older and adults without disabilities, to show proof of employment. States would have flexibility to design the details of the work requirement within federal guidelines and would receive additional federal support to help cover the administrative costs of this change. Back to top

2. Capping Federal Medicaid Spending

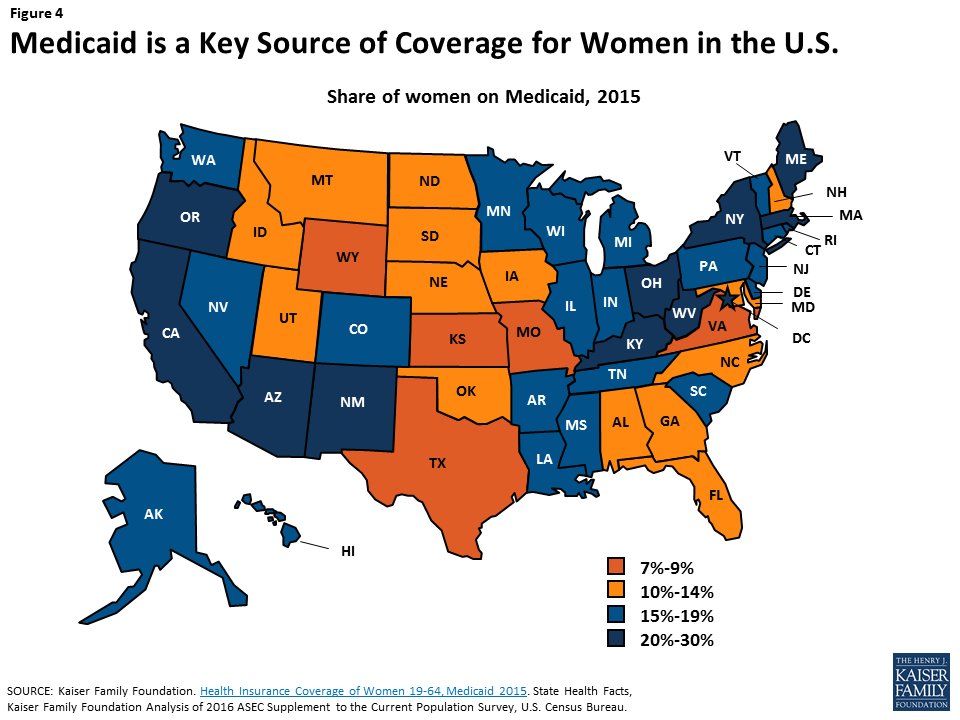

Medicaid provides health coverage to nearly one in five women in the U.S. Capping the program would limit the federal dollars that states would receive for a program that pays for half of births, three-quarters of all public family planning, and provides supplemental coverage for nearly 1 in 5 senior women on Medicare.

Since its inception in 1965, Medicaid has evolved to become a leading source of coverage for low-income women of all ages (Figure 4). The program provides health coverage to one in five women of reproductive age and one in four Latinas and African American women. Over the years, the program has also expanded to be the largest payor of maternity care and publicly-funded family planning in the U.S.

Medicaid is financed by a combination of federal and state dollars. For most beneficiaries, the federal government pays a percentage of costs, ranging between 50-75% depending on the state. Beginning in 2020, the AHCA would convert federal Medicaid funding from an open-ended matching system to an annual fixed amount of federal dollars. States could choose a “block grant” (for payment of services for children under 18 and poor parents of dependent children) or a “per capita cap” approach for five enrollment groups (the elderly, individuals with disabilities, children, newly eligible adults, and all other adults). While a capped approach would reduce federal spending, it would also shift more responsibility to states to pay more of their own dollars if they want to sustain the program at current levels.

While fixed federal financing would affect all individuals insured by Medicaid, one area that is particularly important for women is the program’s coverage of family planning services. Currently, the federal government requires coverage of family planning services and supplies and pays for 90% of the cost of these services, a higher match than for all other services.3 This higher federal payment rate provides states with an incentive to cover the full range of contraceptive methods. Under a per capita cap structure, states will still be required to cover family planning services, but there will no longer be an enhanced federal matching rate for family planning services provided to most beneficiaries. As a result, there may be less up-front financial incentive for states to cover the more expensive methods of contraception like IUDs, even though they are highly effective at preventing unintended pregnancies. Should states select a block grant option, family planning services would no longer be a mandatory benefit for non-disabled women on Medicaid.

If a state chooses a per capita cap structure, the AHCA would not change the financing structure for stand-alone family planning expansions that are currently in place in over half the states. These limited scope programs have allowed states to extend Medicaid coverage for family planning services to low-income women and men who do not have other family planning coverage. Since the AHCA’s per capita cap does not apply to these programs, states could continue to receive a 90% federal matching rate for them. These programs may become increasingly important to women because the CBO predicts that under this bill the number of uninsured would rise by 24 million over the next 10 years, and these Medicaid family planning programs are often an important source of reproductive care for uninsured women.

Both capped financing approaches would limit states’ ability to respond to rising costs, new and costly treatments, or public health emergencies such as the opioid epidemic or Zika. States may decide to make programmatic cuts such as cutting provider payments, particularly when facing fiscal pressures. For example, on average, Medicaid pays ob-gyns 76% of the Medicare rate4 and a smaller share of the commercial rate. If states were to make further cuts to provider payments or to plans, the pool of participating providers could shrink in response to reduced rates, which could make it harder for many women enrollees to find a participating ob-gyn or cause delays in scheduling appointments. Back to top

3. Medicaid and Planned Parenthood

Planned Parenthood provides reproductive health services for many low-income women across the nation. Cutting off federal Medicaid payments to the organization could limit the availability of the most effective contraceptives, as well as STI and cancer screenings for many women on Medicaid.

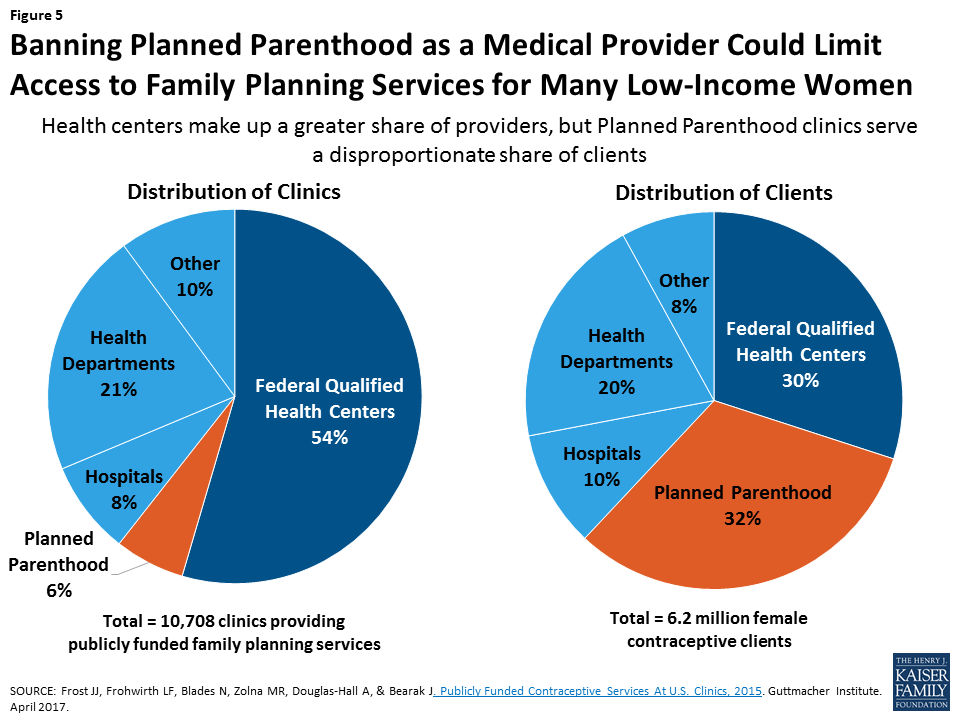

Many low–income women obtain reproductive care at safety-net clinics that receive public funds to pay for the care they provide. The network includes a range of clinics that provide a broad range of primary care services, such as community health centers (CHCs) and health departments as well as specialized clinics that focus on providing family planning services. The largest organization of specialized family planning clinics is Planned Parenthood, which receives federal support through reimbursement for care delivered to women and men on Medicaid, as well as grant funds from the federal Title X family planning program. Despite comprising only 6% of the safety-net clinics that provided subsidized family planning services in 2015, Planned Parenthood clinics served 32% of women (nearly 2 million women) seeking contraceptive care at these centers (Figure 5).

Should it become law, the AHCA would prohibit federal Medicaid payments to Planned Parenthood for one year, even though federal law already prohibits federal dollars from being used to pay for abortions other than those to terminate pregnancies that are a result of rape, incest or a threat to the pregnant woman’s life. The AHCA bill would provide additional funds to CHCs, presumably to compensate for loss of a major provider of care to women, but there are no specifics in the bill that would require the health centers to use these funds to provide services to women. There is also concern that CHCs do not currently have the capacity to fill the gap in care that would arise if Planned Parenthood were no longer a participating Medicaid provider.5 Not all CHCs provide the same range of services as Planned Parenthood, and care at CHCs could be more costly than that provided by specialized family planning providers like Planned Parenthood.6 The CBO’s March 13, 2017 analysis of the AHCA stated that cutting off Medicaid payments to Planned Parenthood for one year would result in loss of access to services in some low-income communities because it is the only public provider in some regions. The report also stated that the policy would result in thousands of additional unintended pregnancies that would be financed by Medicaid.7 Back to top

4. Abortion Coverage

Private and public coverage of abortion is currently limited in many states through the federal Hyde Amendment and state laws. The AHCA would go further than the ACA to restrict the availability of abortion coverage through private insurance policies.

Since 1976, the federal Hyde Amendment has limited the use of federal funds for abortion only to cases when the pregnancy is a result of rape or incest or is a threat to the woman’s life. Since its first passage over 40 years ago, the amendment has dramatically limited coverage of abortion under Medicaid, as well as other federal programs.8

In private insurance, the ACA explicitly bars abortion from being included as part of the Essential Health Benefit package defined by states and allows states to ban all plans in their Marketplaces from covering abortion. States can also ban abortion coverage in all state regulated private plans.9 As of March 2017, 25 states have laws limiting or banning coverage of abortion in ACA Marketplaces, and of these, 10 states ban abortion coverage in both the Marketplaces and in the private insurance market.

To ensure no federal dollars are used to subsidize abortion coverage, the AHCA bill would no longer make this a state option, rather it would ban abortion coverage in all Marketplace plans as well as prohibit the use of federal tax credits to purchase any plans that cover abortion that are available outside the Marketplace. The bill would limit employer coverage of abortion by disqualifying small employers from receiving tax credits if their plans cover abortion beyond Hyde limitations.

This provision would be in direct conflict with existing state policies in California and New York that require plans to cover abortion. Furthermore, no off market plans in these states would be able to enroll individuals who receive tax credits. Therefore, if enacted, the AHCA’s abortion coverage ban would likely face legal challenges. Back to top

5. Tax Credits, Premium and Cost-Sharing Subsidies

The AHCA would set the level of tax credit assistance using primarily age, and would repeal the ACA’s cost-sharing protections for low-income individuals. Because women have a lower income than men at all ages, this approach could place women at a disadvantage compared to men.

Women comprise more than half (54%) of ACA marketplace enrollees in the 34 states that use the federally facilitated marketplace, healthcare.gov. Approximately eight in ten (81%) Marketplace beneficiaries receive a premium tax credit, which offsets premium costs and makes them more affordable. In 2015, more than one-third (37%) of women who purchased insurance on their own were low-income ($23,540 for a single person) compared to 31% of men. 10 The current subsidy structure under the ACA provides higher levels of subsidies to those who are low-income, older, and who live in areas with more expensive coverage.

The AHCA, in contrast, would take a very different approach and reduce the amount that the federal government would contribute to subsidies with the goal of reducing federal spending. The AHCA would provide a flat tax credit based on age only up until an income of $75,000 for a single individual, and phases out at higher incomes. This would result in a large decrease in tax subsidies to older Marketplace enrollees compared to what is available to them today.

The AHCA would set aside additional federal funds to assist older enrollees as well as services for pregnant women and newborns and individuals with mental health and substance use disorders, but how those funds would be allocated is still to be determined. Nonetheless, under the AHCA’s tax credit methodology, people with lower incomes would receive significantly less than they do under current law. A higher share of women is poor or low-income than men, because women are more likely than men to head single parent households, work part-year or part-time, are paid less than men for similar work, and take breaks from the workforce to stay home and care for children and aging parents. As a result, this approach could disproportionately disadvantage women. In addition, the AHCA proposes to repeal the cost-sharing subsides available today under the ACA that provide additional protection from the high costs of deductibles, cost-sharing, and co-insurance to individuals with incomes below 250% of the federal poverty level. Back to top

6. Insurance reforms

The ACA banned many of the long-standing discriminatory practices in the individual insurance market that translated into higher cost burdens for women. While the AHCA maintains the gender-rating ban and the dependent coverage expansion, it could allow states to permit insurers to charge higher premiums to individuals with health problems if they have a lapse in coverage.

Dependent Coverage

A popular element of the ACA is the provision that requires private health insurers that offer dependent coverage to children to allow young adults up to age 26 to remain on their parents’ insurance plans. This provision was the first in the ACA to take effect, and it increased the availability of insurance to an age group that historically had a high uninsured rate (Table 1). In 2015, 39% of women ages 19 to 25 reported that they were covered as a dependent.11

| Table 1: The ACA Made Many Insurance Reforms Affecting Women | ||

| Before the ACA | ACA Provision | AHCA Provision |

Many employer plans did not offer coverage for adult dependent children.

| Requires plans to extend dependent coverage up to age 26 | AHCA does not change |

Many individual plans used gender rating to charge higher premiums to women for same coverage as men

| Bans gender rating | AHCA does not change |

Insurers could charge more or exclude those with pre-existing conditions including:

| Bans pre-existing condition exclusions | Retains pre-existing condition ban, but would charge those with coverage gaps 30% higher premiums for 1 year upon resuming coverage or state could request a waiver to permit insurers to charge higher rates to those with pre-existing medical conditions for 1 year. |

Gender Rating

Prior to the ACA, non-group insurers in many states charged women who purchase individual insurance more than men for the same coverage, a practice called gender rating.12 Yet, plans sold on the individual market often did not cover many important services for women, such as maternity care, mental health services, and prescription drugs.13 An estimated 6.5 million women purchased coverage on the individual insurance market in 2011, and many of these women paid higher rates than men. Prior to the ACA, most of the women in this market were of reproductive age, working, and had incomes below 250% FPL.14 The ACA bans gender rating and the AHCA would not change this.

Pre-Existing Conditions

One of the most popular provisions of the ACA has been the ban on pre-existing condition exclusions. In the years before the ACA was passed, insurance companies often denied or would not renew coverage to individuals with a “preexisting condition,” which included several conditions common among women such as pregnancy, breast cancer, or a prior C-section. The AHCA would not re-instate this practice, but individuals who do not maintain continuous coverage would be charged a penalty when they try to obtain health insurance after having a coverage gap. The penalty could be in the form of higher premium rates (30%) for one year. Alternatively, states could obtain a waiver to allow insurers to again engage in medical underwriting for one year, charging people with health problems higher rates. This would have the effect of raising premiums for people with pre-existing conditions such as pregnancy, prior C-section, or clinical depression. Back to top

7. Essential Health Benefits

The ACA instituted new rules that require all plans in the individual market as well as Medicaid expansion programs to cover ten categories of benefits. Of particular importance to women has been the inclusion of maternity care, preventive services, and mental health.

The ACA requires all Marketplace plans and Medicaid expansion programs to cover ten categories of “essential health benefits” (EHB). Each state chooses a benchmark benefit plan, which sets the floor for services that plans in that state must cover within each EHB category.15

ACA Required Essential Health Benefits

- Ambulatory patient services

- Emergency services

- Hospitalization

- Maternity and newborn care

- Mental health and substance abuse disorder services including behavioral health treatments

- Prescription drugs

- Rehabilitative and habilitative services and devices

- Laboratory services

- Preventive and wellness services

- Chronic disease management

- Pediatric dental and vision care

Prior to the ACA, there were few federal requirements on what private plans in the individual market had to cover. The ACA established a floor for benefits that individual market plans must cover with the goal of reducing variation and adverse selection by standardizing “meaningful coverage.” This is particularly important for women, as they are the exclusive users of maternity care and more frequent users of services in some other EHB categories, such as prescription drugs and mental health. Mental health services in particular were routinely excluded in individual plans prior to the ACA. Depression, anxiety, and eating disorders are all more common among women than men.

The AHCA would allow states to apply for a waiver to define their own EHBs beginning in 2020. Waivers would be automatically approved unless the HHS Secretary issues a denial within 60 days of submission. This means states could choose to exclude mental health or maternity care (see pregnancy-related care section below) from their EHB requirements. While the idea of choice sounds appealing to some, it is antithetical to how insurance operates ─ by spreading the costs and risks across the pool of insured individuals. Plans that include a broader range of benefits would be considerably more expensive than they are today. In addition to state-level waivers, the AHCA bill would rescind the EHB requirement for Medicaid expansion programs, meaning that beneficiaries in this group would not be entitled to coverage for all ten categories. Existing Medicaid rules require states to cover some of the categories, such as hospitalization and maternity and newborn care, but others such as substance abuse treatment and prescription drugs are optional and offered at state discretion.Back to top

8. Preventive Services

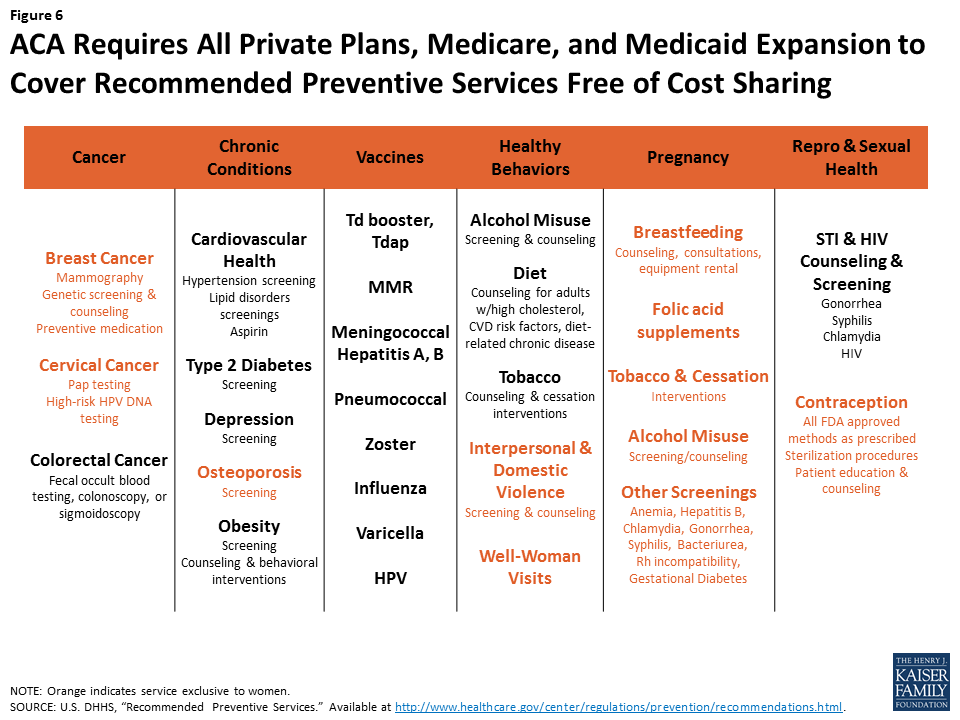

Currently, all private plans, Medicaid expansion programs, and Medicare must cover recommended preventive services without cost sharing. Important services for women include: breast and cervical cancer screening, osteoporosis screening, pregnancy related services, well woman visits, and contraception.

In addition to EHBs, the ACA included a related requirement that all private plans cover federally-recommended preventive services without charging cost-sharing. In contrast to EHBs, which apply to individually purchased plans and Medicaid expansion only, the preventive services requirement applies to all forms of private insurance, including employer-sponsored and individual market plans. Prior to the ACA, the only federal–level requirements that applied to group plans were for coverage of a minimum length of stay after a delivery, availability of reconstructive surgery following a mastectomy, and parity for mental health services. The preventive services coverage requirement also applies to the Medicaid expansion and Medicare programs. This means that most adults with some form of private or public insurance now have coverage without cost-sharing for all of the services recommended by the U.S. Preventive Services Task Force (USPSTF), immunizations recommended by the federal Advisory Committee on Immunization Practices (ACIP), and services for women recommended by the Health Resources and Services Administration.16

Among the slate of services covered, many are exclusively for women or address conditions that have a disproportionate impact on women (Figure 6). These services address some of the most common conditions for women, including breast cancer, cardiovascular disease, and obesity. For older women, the preventive services policy means that Medicare now covers the full cost of mammograms and bone density screenings, which were previously subject to 20% co-insurance before passage of the ACA.

The AHCA would maintain preventive services requirements for private plans, but would repeal the requirements for the Medicaid expansion population. Preventive services for adults are covered at state option for other Medicaid beneficiaries. States could opt to roll back coverage of preventive services for this group. Back to top

9. Contraceptive Coverage

Today, the majority of women with private insurance have no cost contraceptive coverage. This preventive benefit has reduced women’s out-of-pocket spending on birth control and made the most effective, but often costly, contraceptive methods affordable for most insured women. This provision could be eliminated or modified through regulatory changes without the need for Congressional action.

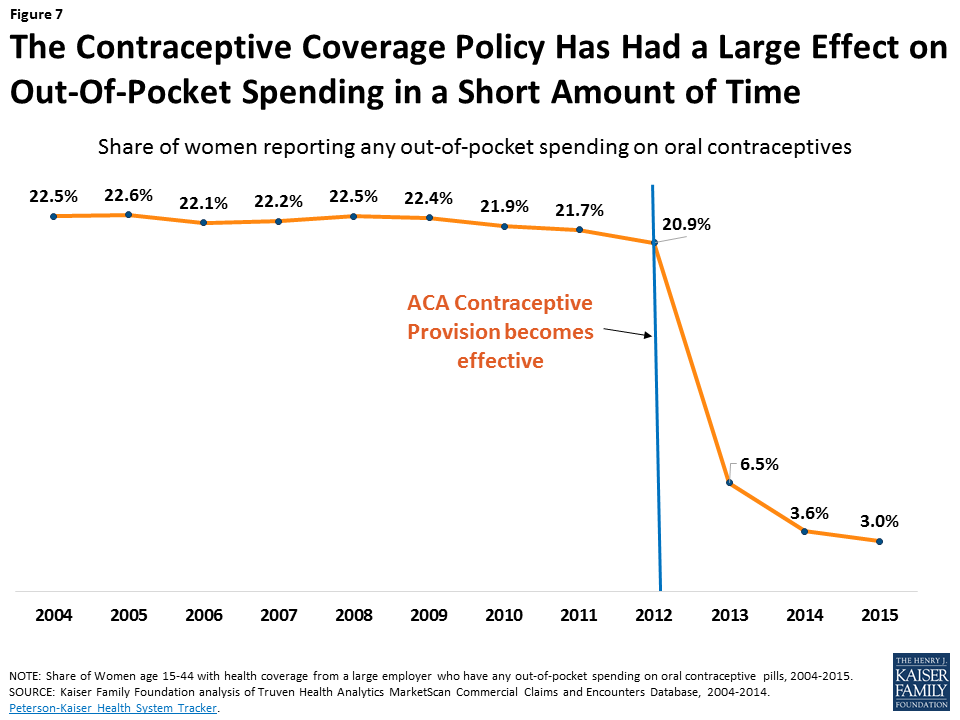

Current law requires that most private plans include coverage of all FDA-approved contraceptive methods for women at no additional cost. Research has found that the requirement has had a large impact in a short amount of time. For example, in the first two years that the policy was in effect, the share of women with any out of pocket spending on oral contraceptives fell sharply to just 3.0% of women with employer-sponsored insurance (Figure 7).17 Similar effects have been documented for other contraceptives, including IUDs.18

The AHCA bill does not specifically address the contraceptive coverage requirement. However, President Trump and Secretary Price have expressed support for advancing “religious freedom,”19 and this provision has been at the heart of two cases that have reached the Supreme Court where employers have claimed that the requirement violates their religious beliefs. The contraceptive coverage requirement was implemented through a series of agency regulations that included contraception in the package of women’s preventive services, defined the religious exemption and accommodation available to houses of worship and faith-based nonprofits respectively, and clarified that plans must cover 18 contraceptive methods. Since these requirements are in regulations, the Trump Administration can issue new regulations and guidance to permit employers and insurers to cover fewer methods, or to exempt more employers with religious objections without the need for congressional action.20 President Trump’s Executive Order Promoting Free Speech and Religious Liberty specifically calls on the Secretaries of Labor, Treasury, and Health and Human Services to amend regulations to protect conscience-based objections to the ACA’s preventive-care mandate.21 The goal of this is to exempt any employer with a religious or moral objection from the contraceptive coverage requirement, even though current regulations already relieve employers from paying for such coverage while assuring that women have coverage for contraceptives.

If the federal requirement is eliminated or scaled back, the scope of contraceptive coverage would again be shaped by employers, insurance plans, and state policy. More than half (28) of states have laws requiring plans in their states to cover contraceptives, but these are more limited than the ACA. Only five of the 28 states require coverage of the full range of contraceptives without cost sharing, but these state-level mandates do not apply to self-funded plans, which cover most insured workers.22 Back to top

10. Pregnancy-Related Care

Today, pregnant and postpartum women have a greater range of protections and benefits than they did prior to the ACA. These range from mandatory maternity and newborn coverage, to no-cost prenatal screening, and breastfeeding supports. The AHCA would allow states to define the Essential Health Benefits requirements with a waiver, potentially excluding coverage for maternity care.

Before the ACA, pregnant women seeking insurance in the individual market were routinely turned away as having a pre-existing condition. Furthermore, many individual plans did not cover maternity services because it was not required in this market. Some individual plans offered separate maternity coverage as a rider which could be costly, ranging from roughly $15 to $1600 a month.23 Some plans also imposed a waiting period before the rider took effect. These discriminatory practices were limited to the individual market because coverage for maternity services has been required for decades both under Medicaid and in most employer-sponsored plans due to the Pregnancy Discrimination Act. The ACA changed this by including maternity and newborn care as part of the EHB package that must be included in individual private plans as well as under Medicaid expansion. While some states had required individual plans in their states to cover maternity services to varying degrees prior to the ACA, most did not.24 In addition, the ACA made other improvements through coverage of preventive services such as no-cost prenatal screenings and breastfeeding supports.

ACA Reforms Improving the Availability of Maternity Care

- Maternity and newborn care are essential health benefits

- Pregnancy no longer a pre-existing condition

- Prenatal visits, recommended screening tests, folic acid supplements covered without cost sharing in all new private plans, and Medicaid expansion

- Medicaid expansion provides pathway to coverage for mothers who previously may have lost coverage postpartum

- Breastfeeding supports for nursing mothers

- Breast pumps and lactation consultation covered without cost sharing

- Breaks and private area to express milk required in workplace

The AHCA would weaken some of the protections for pregnant women that are currently in place. By halting funds for Medicaid expansion, some new mothers would lose coverage once the 60-day postpartum period ends and become uninsured. Furthermore, it would permit states to waive the current federal EHB standards, potentially allowing states to remove or scale back maternity services as a required benefit. The bill would also allot funds to the Patient and State Stability Fund for pregnancy and newborn care, but there are no details on how it will be used.

Some have touted the benefits of excluding maternity coverage for those who will not need it such as men and older women as a way of giving policyholders more flexibility to choose their own coverage and purchase less expensive plans. However, this also means that the risk pool for plans that include maternity services would primarily be comprised of women who anticipate using maternity care, and would likely greatly increase costs for women who sought such coverage. Furthermore, given that nearly half of pregnancies are unintended some women would buy coverage that does not include maternity care thinking they won’t need it, only to find out their coverage falls short when they are pregnant.

Conclusion

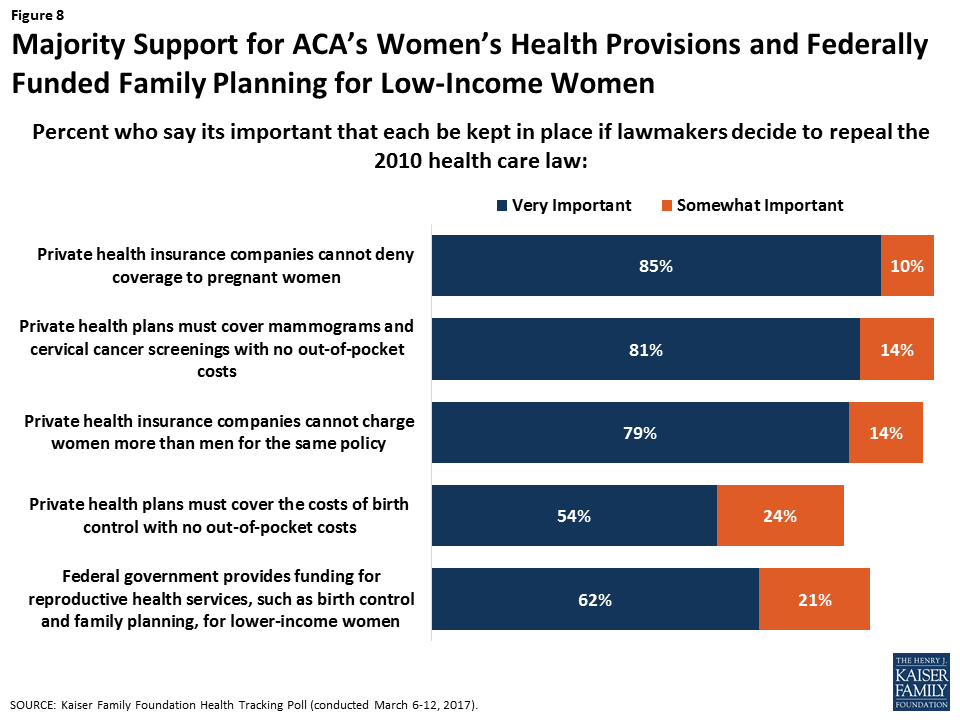

Today, women’s health coverage levels are at an all-time high. In addition to the coverage gains in the Marketplaces and Medicaid, many of the long-standing discriminatory practices in the individual insurance market that translated into higher cost burdens for women have been banned. Minimum standards for benefits that individual plans must cover through the EHB and the preventive services requirements for all private plans have assured that most insured women have coverage for a broad range of recommended services that they need such as maternity care, mental health services, and preventive services such as mammograms, pap smears, and contraceptives. Recent polling shows that the American public values these protections, including those for poorer women (Figure 8). In addition, while the AHCA would prohibit federal Medicaid funds to Planned Parenthood for one year, 75% of Americans say they favor continued federal funding for Planned Parenthood.25

If enacted, the AHCA would alter subsidies for private insurance, eliminate the Medicaid expansion, ban Medicaid funding to Planned Parenthood, place a cap on Medicaid spending, and turn EHB standards over to the states. This legislation would have considerable impact on women, particularly low-income women who rely on subsidies and those who are on Medicaid. The Senate will now take up their own debate about the future of the ACA. In addition to legislation, many of the ACA’s other provisions could be amended through federal-level administrative actions. Given the gains that women have made in access to meaningful and affordable coverage, they have much at stake in the current debate over the future of our nation’s private and public insurance programs.

Appendix

| Appendix 1: Comparison of Women’s Health Provisions in the ACA and House AHCA | |

| Affordable Care Act (ACA) | House American Health Care Act (AHCA) |

| Medicaid Policy | |

| Allow states to expand Medicaid eligibility to all adults up to 138% FPL. | Repeal enhanced federal match for Medicaid expansion except for those enrolled as of December 31, 2019 who do not have a break in eligibility of more than 1 month; Convert federal Medicaid funding to a per capita allotment or block grant and limit growth beginning in 2020 using 2016 as a base year. |

| Planned Parenthood | |

| Planned Parenthood may receive federal reimbursements under Medicaid’s “any willing provider” provision. | Prohibit federal Medicaid funding for Planned Parenthood clinics for one year. |

| Abortion | |

| Prohibit abortion coverage from being required. Federal premium and cost-sharing subsidies cannot pay for abortion beyond Hyde limitations.Allows qualified health plans to cover abortion, but plan must segregate federal subsidy funds from private premium payments or state funds. Prohibit plans from discriminating against a provider because of unwillingness to provide, pay for, cover, or refer for abortions. | Prohibit all qualified health plans from covering abortion beyond Hyde limitations. Prohibit federal premium tax credits from being applied to premiums of non-Marketplace plans that cover abortion services beyond Hyde limitations. Ban small employers from receiving tax credits if their plans include abortion coverage beyond Hyde limitations. |

| Subsidies | |

| Premium tax credits based on age, income and location to eligible individuals with incomes between 100-400% FPL on a sliding scale. Provide cost-sharing subsidies to eligible individuals with household income between 100%-250% FPL. | Replace ACA income-based tax credits with flat tax credit adjusted for age only. Repeals cost-sharing subsides as of January 1, 2020. |

| Preexisting conditions | |

| Prohibit pre-existing conditions exclusions, which historically have included pregnancy, prior C-section, and mental illnesses, and rate surcharges based on health status. | Retain ban on pre-existing conditions exclusions. Those with coverage gaps could be charged 30% more for premiums for the first year of resuming coverage or state could request a waiver to permit insurers to medically underwrite for one year, charging sicker individuals higher rates for that year. |

| Gender Rating | |

| Ban discriminatory premium pricing based on gender in all group and individual insurance plans. | Ban on gender rating is not changed. |

| Essential Health Benefits (EHB) | |

| Require all private insurance plans to cover 10 EHB categories, including maternity care and mental health services. | EHB standards are repealed for the Medicaid expansion population. States could apply for a waiver to re-define EHBs for the individual and small group health insurance markets. |

| Preventive Care | |

| Require almost all private plans to cover preventive care without cost-sharing, including contraception and breast cancer screenings. | Requirement for individual and group plans to cover preventive benefits, without cost sharing is not changed. |

Endnotes

- Amendment to H.R. 1628 Offered by Mr. MacArthur. April 25, 2017. ↩︎

- Legislation extends Medicaid coverage to all individuals with incomes up to 133% of the poverty level (FPL) and includes a provision to disregard first 5% of income, effectively extending Medicaid to all individuals with incomes up to 138% FPL. ↩︎

- Kaiser Family Foundation. (2012). Medicaid Financing: An Overview of the Federal Medicaid Matching Rate (FMAP). ↩︎

- Zuckerman S, Skopec L, McCormack K. (2013). Reversing the Medicaid Fee Bump: How Much Could Medicare Physician Fees for Primary Care Fall in 2015? Urban Institute. ↩︎

- Rosenbaum S. (2017). Can Community Health Centers Fill the Health Care Void Left by Defunding Planned Parenthood? Health Affairs Blog. ↩︎

- Ibid ↩︎

- Congressional Budget Office (CBO). “American Health Care Act.” March 13, 2017. ↩︎

- Salganicoff A, Rosenzweig C, Sobel L. (2016). The Hyde Amendment and Coverage for Abortion Services. Kaiser Family Foundation. ↩︎

- Salganicoff A, Beamesderfer A, Kurani N, Sobel L. (2014). Coverage for Abortion Services and the ACA. Kaiser Family Foundation. ↩︎

- Centers for Medicare and Medicaid Services (CMS). Health Insurance Marketplaces 2017 Open Enrollment Period: January Enrollment Report. January 10, 2017. ↩︎

- Kaiser Family Foundation analysis of the 2016 ASEC Supplement to the Current Population Survey, U.S. Census Bureau. ↩︎

- National Women’s Law Center. (2012). Turning to Fairness: Insurance Discrimination Against Women Today and the Affordable Care Act. ↩︎

- Committee on Energy and Commerce, U.S. House of Representatives. “Memorandum on Maternity Coverage in the Individual Health Insurance Market” at page 37. October 12, 2010. ↩︎

- Kaiser Family Foundation and Urban Institute analysis of 2012 Current Population Survey, Bureau of the Census, 2012. ↩︎

- The Center for Consumer Information & Insurance Oversight. Centers for Medicare and Medicaid Services (CMS). Information on Essential Health Benefits (EHB) Benchmark Plans. ↩︎

- Institute of Medicine (IOM). (2011). Clinical Preventive Services for Women: Closing the Gaps. Washington, DC: The National Academies Press. ↩︎

- Peterson-Kaiser Health System Tracker. (2016). Examining high prescription drug spending for people with employer sponsored health insurance. ↩︎

- Becker NV & Polsky D. (2015). Women Saw Large Decrease In Out-Of-Pocket Spending for Contraceptives after ACA Mandate Removed Cost Sharing. Health Affairs, 34(7), 1204-11. ↩︎

- Letter to Gail Buckley, President Catholic Leadership Conference. October 5, 2016. ↩︎

- Sobel L, Salganicoff S, Rosenzweig C. (2017). The Future of Contraceptive Coverage. Kaiser Family Foundation. ↩︎

- Presidential Executive Order Promoting Free Speech and Religious Liberty. May 4, 2017. ↩︎

- Sobel L, Salganicoff S, Rosenzweig C. (2017). The Future of Contraceptive Coverage. Kaiser Family Foundation. ↩︎

- National Women’s Law Center. (2012). Turning to Fairness: Insurance Discrimination Against Women Today and the Affordable Care Act. ↩︎

- Ibid. ↩︎

- Kaiser Family Foundation. Kaiser Health Tracking Poll: ACA, Replacement Plans, Women’s Health. March, 15 2017. ↩︎