Medicaid and CHIP Eligibility, Enrollment, and Renewal Policies as States Resume Routine Operations

Following the Unwinding of the Pandemic-Era Continuous Enrollment Provision

Executive Summary

In 2024, almost all states completed renewals for the 94 million individuals who were enrolled in Medicaid following the pandemic-era three-year pause on disenrollments that was lifted on March 31, 2023. By October 2024, based on the most recent Centers for Medicare and Medicaid Services (CMS) enrollment data, the process known as unwinding had resulted in a net decline in Medicaid and CHIP enrollment of 15 million individuals, including about five million children, but enrollment remained above pre-pandemic levels.

The focus on Medicaid renewal processes during the unwinding revealed their complexity. With states facing an unprecedented volume of work and eligibility worker shortages, CMS provided new options to streamline enrollment and renewal processes, emphasizing automation and the use of reliable data sources to increase accuracy and efficiency. States broadly adopted these strategies, and many emerged from the unwinding with more efficient processes by maximizing the use of technology to verify income, reduce returned mail, and improve communications with enrollees. However, some states continue to struggle with older systems that limit the adoption and effectiveness of some of the new strategies.

Medicaid agencies are now turning their attention to ensuring that state policy aligns with existing and new federal requirements. At the same time, there is significant uncertainty about how potential changes to federal Medicaid financing and policy under consideration by Congress and the Administration will impact states and Medicaid enrollees in the future. Congress is debating cuts to Medicaid of up to $880 billion or more over ten years, citing a desire to curtail spending to help pay for tax cuts and address “fraud, waste, and abuse”. While several proposals would fundamentally restructure who is covered by the program and how it is financed, repeal of regulations finalized in the last administration, including the Eligibility & Enrollment (E&E) rule finalized in April 2024, are also under consideration. The E&E rule included provisions to streamline and enhance the administrative efficiency of Medicaid eligibility and enrollment processes and to make it easier for eligible individuals to retain coverage. The rule also clarified documentation and recordkeeping requirements, providing the first update to these requirements since 1986, to reduce payment errors based on insufficient documentation. By eliminating some barriers to enrollment and reducing churn among people who are eligible but lose coverage for paperwork reasons, the rule is expected to increase Medicaid and CHIP enrollment (CMS projected enrollment would increase by 1.5 million in 2028.) The Congressional Budget Office estimated that rescinding this rule along with a related rule that reduces barriers to enrollment among people eligible for Medicare Savings Plan (MSP) coverage would reduce federal Medicaid spending by $164 billion over ten years.

The 23rd annual survey of state Medicaid and CHIP program officials conducted by KFF and the Georgetown University Center for Children and Families provides a baseline of state Medicaid and CHIP eligibility, enrollment, and renewal policies in place as of January 2025 as states return to routine operations following the unwinding. The report focuses on policies for children, pregnant individuals, parents, and other non-elderly adults whose eligibility is based on Modified Adjusted Gross Income (MAGI) financial eligibility rules. Overall, 49 states and the District of Columbia responded to the survey, although response rates for specific questions varied (Florida did not respond). For the purposes of this report, the District of Columbia is counted as a state.

Key Takeaways

- Building on strategies adopted during the unwinding, most states are continuing to implement policies to increase ex parte, or administrative, renewal rates. During the unwinding period, states employed new approaches to using data and automation to streamline processes for verifying eligibility. Over two-thirds of states plan to continue or newly adopt at least one strategy to facilitate ex parte renewals. While 29 states report that over half of ex parte renewal rates are conducted automatically by their systems, the share of eligibility determinations at application that are automated and conducted in real-time (within 24 hours) lag. Close to half of states say they cannot conduct automated real-time eligibility determinations on new applications or report that less than 10% of these eligibility determinations are automated.

- States increasingly rely on data from trusted sources to automate manual tasks and improve accuracy of Medicaid eligibility, enrollment, and renewal processes. By advancing the use of information from other programs such as SNAP and TANF, states have improved the accuracy of income verification while reducing administrative burden associated with mailing renewal forms and manually processing information submitted by mail or phone. At the same time, periodic checks of income data sources coupled with limited time for enrollees to respond to information requests can increase procedural disenrollments and churn.

- States have incorporated new strategies for updating contact information and communicating with enrollees into routine operations, and some are using artificial intelligence (AI) to assist with the application and renewal processes. Access to the US Postal Service National Change of Address (NCOA) Database and other program data allows states to routinely update mailing addresses, tackling the longstanding problem of returned mail. Nearly all states proactively check available data sources for updated contact information or accept updated addresses from managed care plans or providers. To increase renewal response rates, states contact enrollees multiple times before and after sending renewal notices using multiple modes including email and text. States have also enhanced online tools–online accounts and mobile apps–to provide additional ways to communicate with enrollees and to give enrollees the ability to more easily manage their coverage. A few states use AI to answer consumer questions at different points during the application or renewal process, and a small number have begun using AI to assist with reviewing applications and renewals.

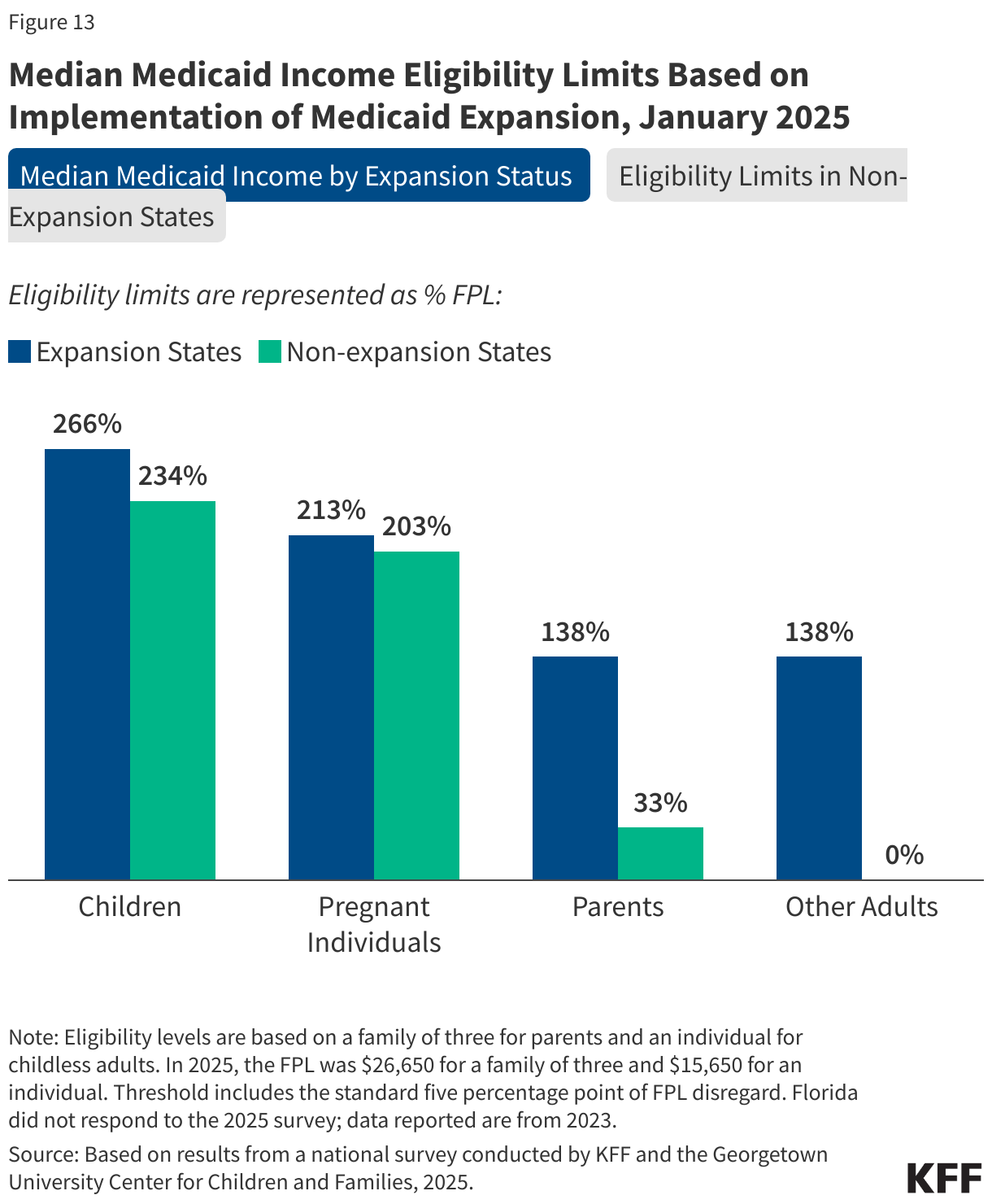

- Continuing a trend over the past few years, two states increased income eligibility for pregnancy coverage. Alaska and Washington state expanded income eligibility for pregnancy and Colorado adopted the From Conception to the End of Pregnancy coverage option in CHIP. Since 2023, five states (Alaska, Nevada, North Dakota, Tennessee, and Washington) have increased pregnancy eligibility levels, but one state (Iowa) is seeking approval to reduce pregnancy income eligibility. The median eligibility level for children (255%) is the highest of all MAGI groups. Eligibility levels for all MAGI groups are lower in non-expansion states compared to expansion states.

- States have taken steps to remove administrative barriers to enrollment and renewal for children and seniors and people with disabilities (non-MAGI groups). Almost all states with separate CHIP programs have eliminated required periods of uninsurance (waiting periods) and lock-out periods following nonpayment of premiums, both of which contribute to gaps in coverage. The E&E rule requires states to phase out waiting and lock-out periods by June 2025. Two states (Utah and Delaware) permanently eliminated CHIP premiums in 2024, and premiums remain temporarily or indefinitely suspended in Arizona and Vermont while Georgia reinstated CHIP premiums after pausing them during the COVID pandemic. All states have taken steps to align non-MAGI renewal rules with those in place for MAGI groups such as conducting annual renewals, eliminating in-person interviews, and giving enrollees more time than 10 days to respond to requests for information. The E&E rule requires states to align non-MAGI renewal policies by June 2027.

Report

Post-Unwinding and Resuming Routine Operations

Renewal Policies

Over half of states report that 50% or more of ex parte renewals are processed automatically by the eligibility system, but only a quarter of states report that 50% or more of eligibility determinations at application are automated. By adopting more efficient processes relying on technology and data from trusted sources, states can automate manual tasks, reduce administrative costs, and improve accuracy. During the unwinding period, ex parte renewal rates increased as states made systems improvements to enhance automation of renewal processes. However, not all ex parte renewals can be processed automatically by the system, and for those ex parte renewals that are not automated, workers manually check data sources to confirm ongoing eligibility. Nearly all states (45) report that 10% or more of ex parte renewals are processed automatically by the eligibility system and over half (29 states) report that processing of more than 50% of ex parte renewals is automated (Figure 1). However, automation of eligibility determinations at application lags automation of ex parte renewals. Thirteen states lack the ability to automatically process eligibility determinations at application in real-time and eight states report that less than 10% of applications are processed by the system without worker intervention. Some states that rely on the FFM to determine eligibility are able to process enrollment in real time since the FFM has already determined eligibility.

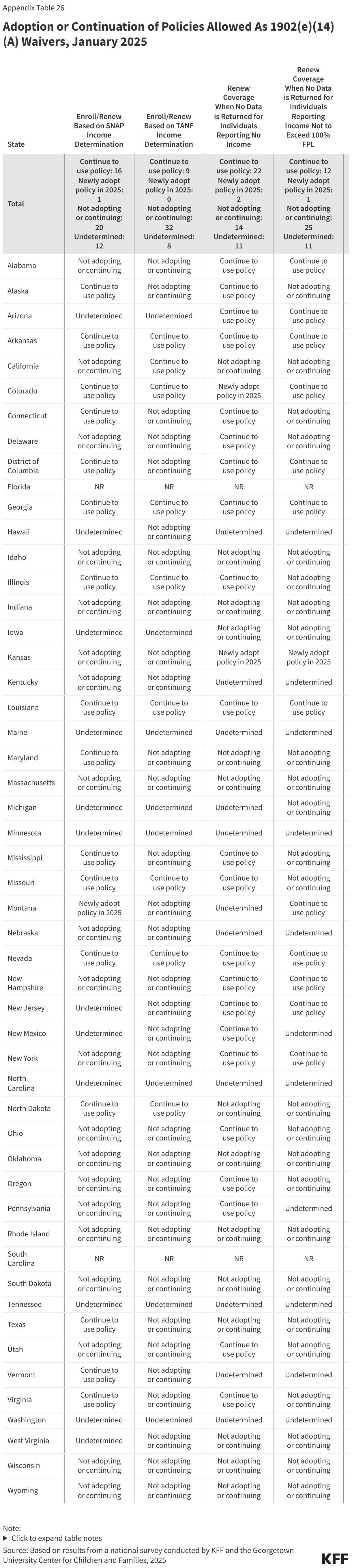

Most states are continuing or newly adopting automated processes for verifying income and taking other steps to increase ex parte renewals. All states must verify income eligibility for Medicaid and CHIP. During the unwinding, states facing system and operational challenges had the option to seek authority under section 1902(e)(14)(A) of the Social Security Act (the Act) to try new approaches to use data to confirm income eligibility. Several of those strategies proved to be effective in increasing state ex parte renewal rates and were made permanently available as state plan options. Over two-thirds of states (34) are continuing or newly adopting one of the new state plan options (Figure 2). In addition, over two-thirds of states are taking other steps to increase ex parte rates; refining system programming (24 states) and expanding data sources (18 states) are the top two strategies.

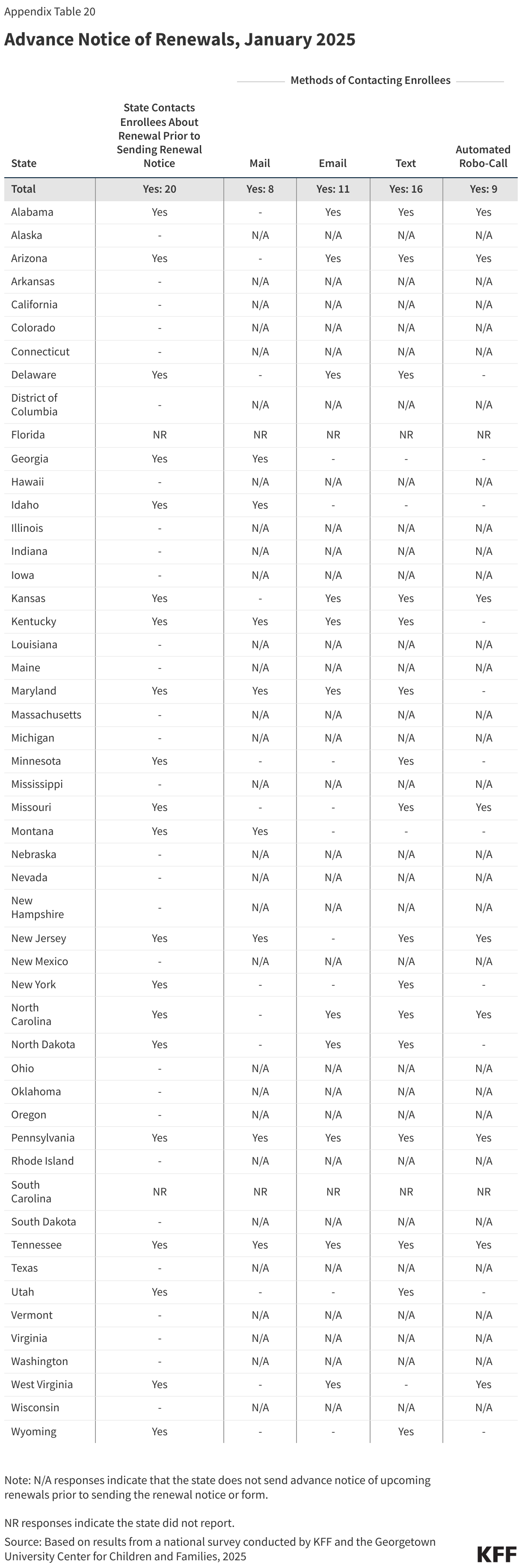

States are doing more to communicate with enrollees during the renewal process. States increased their communication touch points with enrollees during the unwinding period and many have kept that increased communication in place as they return to routine operations. For enrollees whose ongoing eligibility cannot be verified via ex parte processes, 20 states send an advance notice to alert enrollees to an upcoming renewal and 42 states remind enrollees before the end of the renewal period to complete their renewal (Figure 3). They are using multiple ways of reaching enrollees, including relying on cost-effective and timely email and text messages.

States are also taking steps to help eligible individuals regain coverage following procedural disenrollments. States are required to provide a 90-day reconsideration period when an enrollee has been procedurally disenrolled, or disenrolled because they did not complete the renewal process and not because they were determined ineligible. During this reconsideration period, eligible individuals may submit renewal information for redetermination without completing a new application. Half of states (25) include information about the 90-day reconsideration period in termination notices and 12 states provide lists of members who have been procedurally disenrolled to MCOs so they can follow up with those individuals (Figure 3). When an enrollee is determined eligible during the reconsideration period, 31 states reinstate coverage back to the termination date while 12 states reinstate coverage to the first day of the month in which information is received.

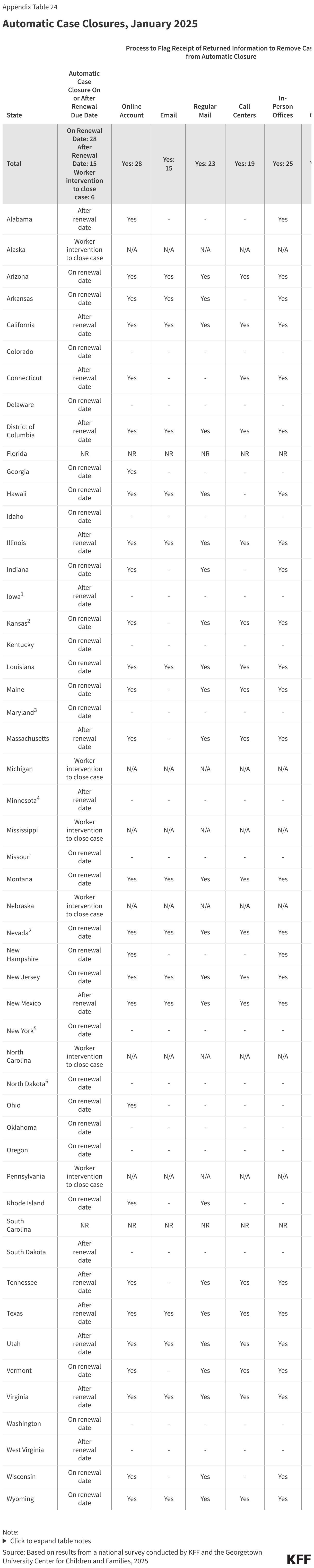

Most state eligibility systems automatically close cases on or shortly after the renewal date. Auto-closures are used by states to automate the disenrollment process for enrollees whose renewal or other missing information has not been received by the end of the renewal period. Over half of states (28) close the case on the eligibility end date, while auto-closures occur shortly after the end date in 15 states (Figure 4). In the remaining six states, workers must manually close cases. Auto-closures avoid keeping a case open past the end of an eligibility period and prevent unnecessary capitation payments in MCO states. However, if states experience delays in processing documents received by mail or fax or uploaded through online accounts and mobile apps, enrollees can be disenrolled despite submitting required documents on time. To avoid unnecessary terminations, 33 of the 43 states that automatically close cases have implemented routine processes to flag the receipt of documents through one or more modes and exclude those cases from an auto-closure.

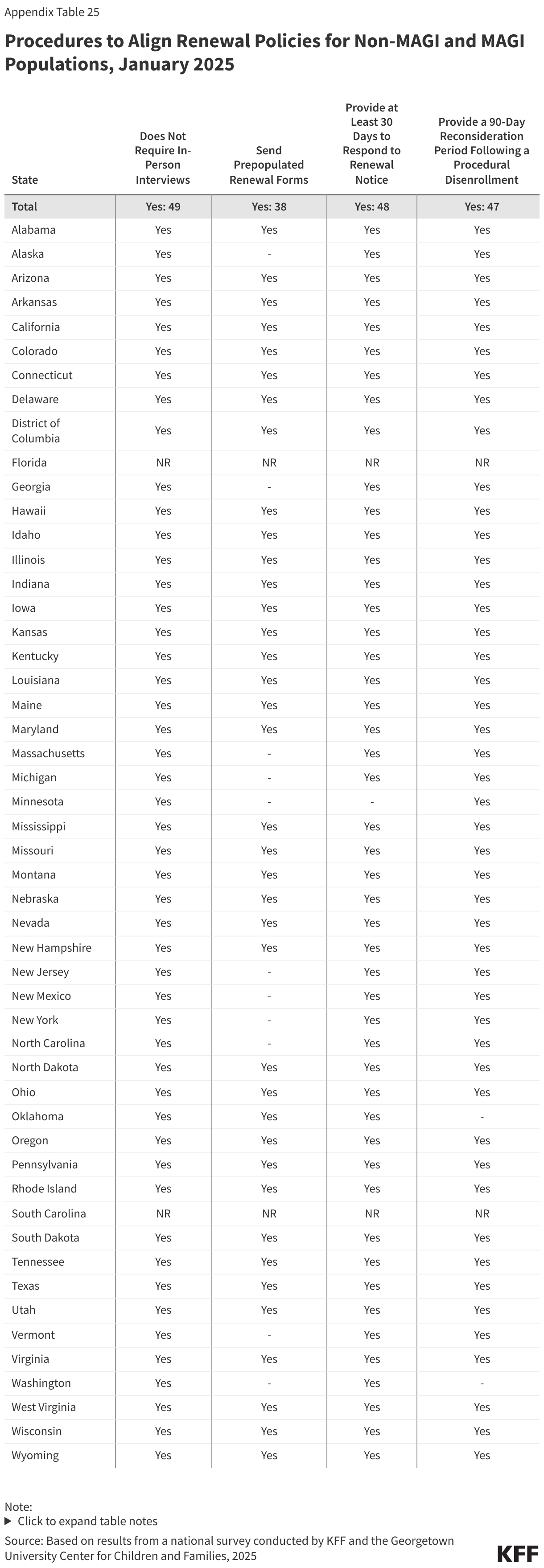

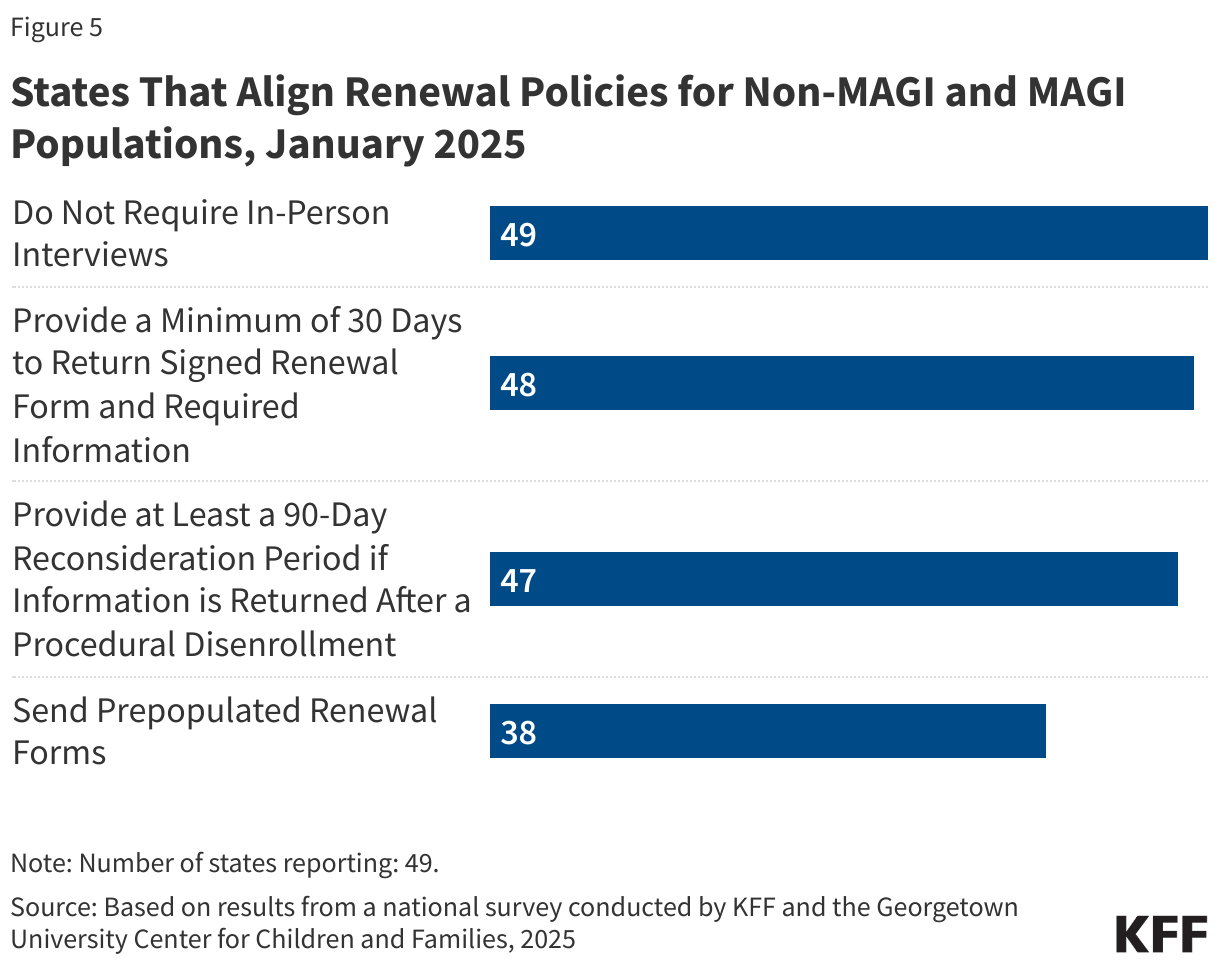

States are expediting alignment of renewal policies for seniors and people with disabilities (non-MAGI groups) with those in place across MAGI groups. No reporting state requires in-person interviews; most states allow at least 30 days for all enrollees to respond to renewal requests (48 states) and provide a 90-day reconsideration period for both MAGI and non-MAGI enrollees (47 states). However, only 38 states send a pre-populated renewal form to non-MAGI enrollees (Figure 5). Aligning processes not only removes barriers to enrollment for seniors and people with disabilities but also makes it easier to program eligibility systems, train workers, and explain the rules to applicants and enrollees. The E&E rule requires states to align these policies by June 2027.

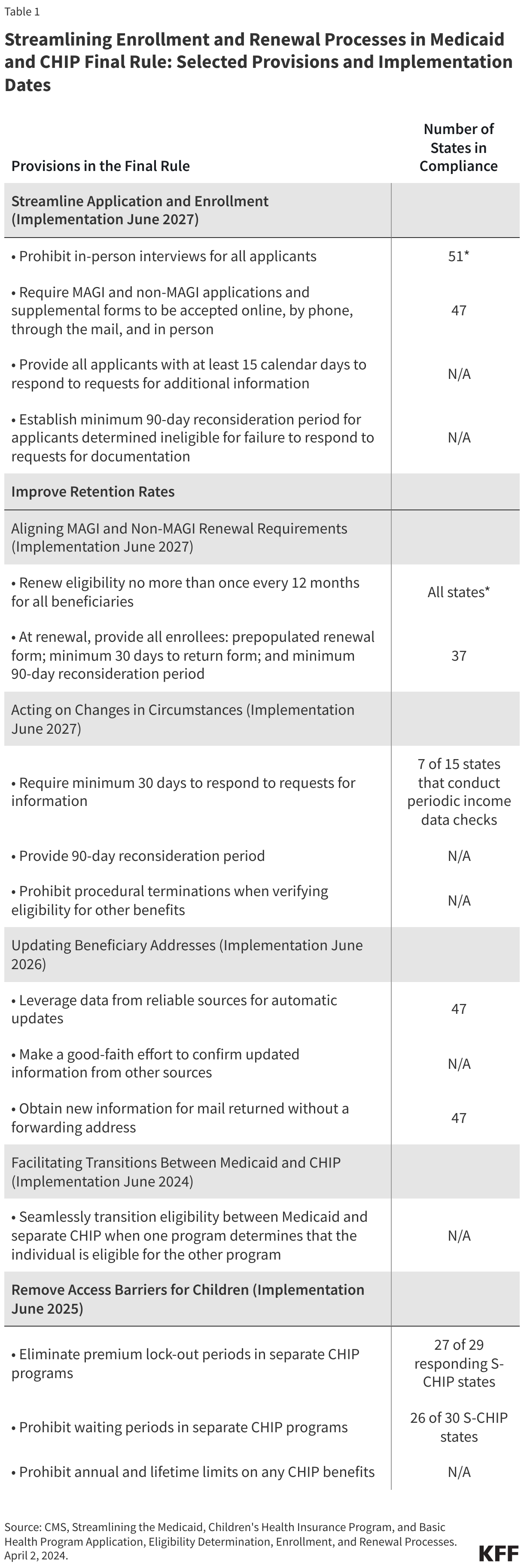

Streamlining Enrollment and Renewal Processes in Medicaid and CHIP Final Rule: Select Provisions, Implementation Dates, and Number of States Already in Compliance

On April 2, 2024, the CMS published the second part of a two-part final E&E rule that simplifies the eligibility and enrollment processes for Medicaid, the Children’s Health Insurance Program (CHIP), and the Basic Health Program (BHP). The rule streamlines application and enrollment processes, aligns renewal policies for all Medicaid enrollees, facilitates transitions between programs, and eliminates certain barriers in CHIP. Deadlines for states to implement vary across provisions, but many states are already in compliance with certain provisions.

In the table below, select provisions in the final rule include those for which there was a question on the survey that provided information on state policies.

Updating Contact information and handling returned mail

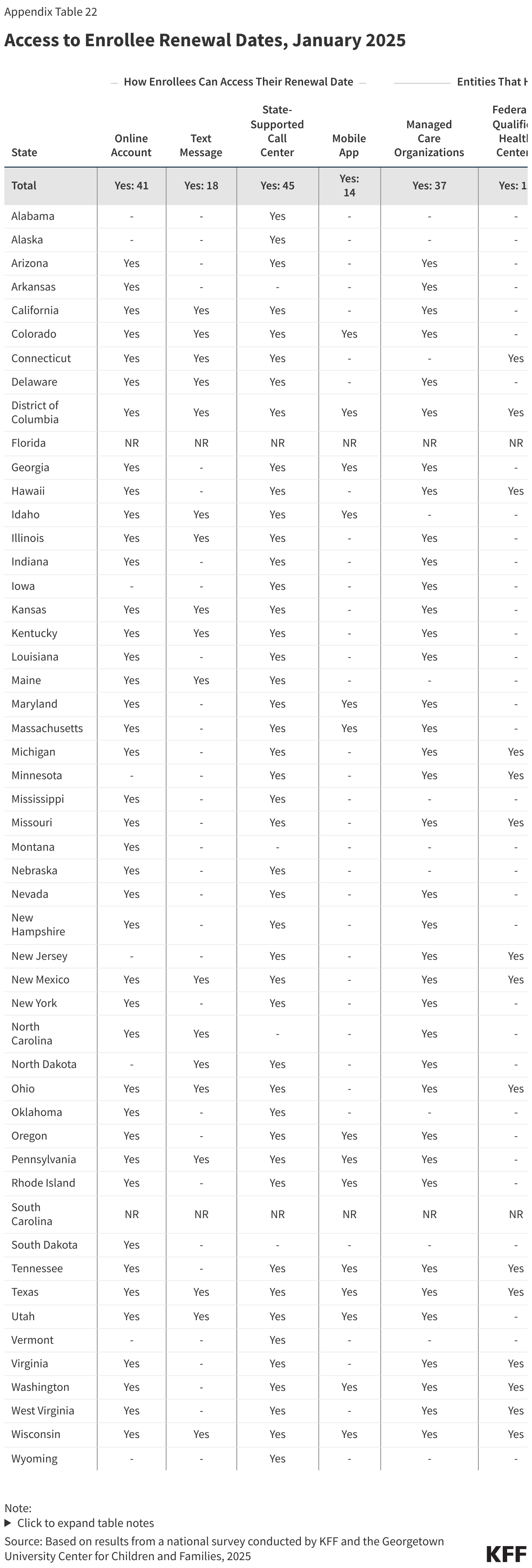

During the unwinding, states implemented new processes to update mailing addresses, reducing the cost and administrative burden of handling returned mail. Returned mail has been a longstanding and costly problem in Medicaid. States offer multiple ways for enrollees to update their contact information, including through their online account (45 states) or mobile app (11 states), through a simple online change of address form (27 states), and/or by calling a dedicated phone number or option on the state’s interactive voice response system (13 states). States also proactively conduct data matches with the USPS National Change of Address (NCOA) database (27 states) and accept updates to mailing addresses from reliable sources (40 states), including managed care organizations and navigators/assisters (Figure 6). The final E&E rule requires states to accept and act on address updates provided by specific reliable sources by December 2025.

Nearly all states follow up on returned mail by checking available data sources or attempting to contact the enrollee, continuing strategies deployed during the unwinding. One third of states (17) check the USPS NCOA database and 35 states check SNAP/TANF for updated contact information when mail is returned, and all but two reporting states (47) attempt to reach the enrollee by phone, email, or text (Figure 6). The final E&E rule requires states, by December 2025, to make a good faith effort to contact enrollees using different communication modes when mail is returned without an in-state forwarding address. Mail returned with an in-state forwarding order is considered a reliable source that does not require redundant verification and can be automatically updated.

Changes in Circumstances

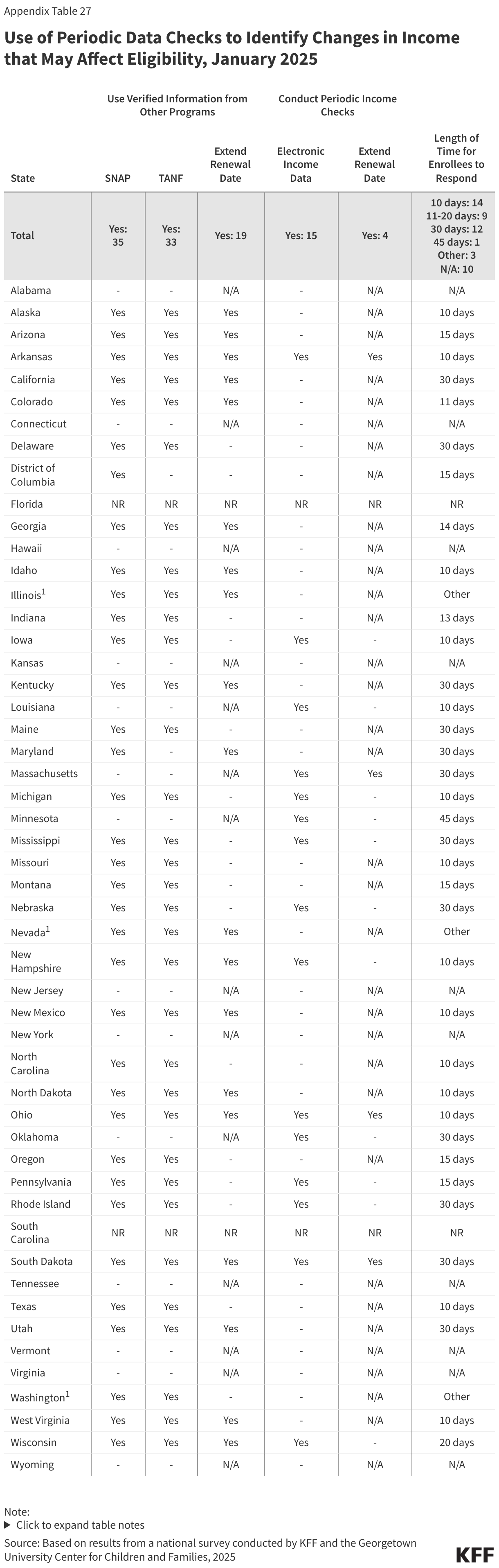

As they return to routine operations, most states use information from SNAP and TANF and/or periodically check other data sources to identify and act on potential changes in eligibility between renewals. States are required to follow up on reported changes that potentially affect eligibility and give individuals an opportunity to respond before taking adverse action. Over two-thirds (35) of states use verified information from SNAP or TANF to identify changes that may affect Medicaid eligibility (Figure 7). Fifteen states periodically check other external data sources, including quarterly wage and unemployment data, and 11 states do both. If information from the other programs confirms ongoing eligibility, 19 states extend the renewal date by 12 months; four states do the same if external income data sources confirm ongoing eligibility. When documentation from the enrollees is required to avoid termination, 14 states give enrollees only 10 days to respond. Periodic data checks and insufficient response times can exacerbate churn particularly given regular mail disruptions and delays.

Systems and Online Tools

The 49 reporting states operate a total of 64 eligibility systems. While 35 states operate a single eligibility system, 13 states operate two systems, and one state operates three systems. Over two-thirds of state systems (44 of 64) are at least ten years old.

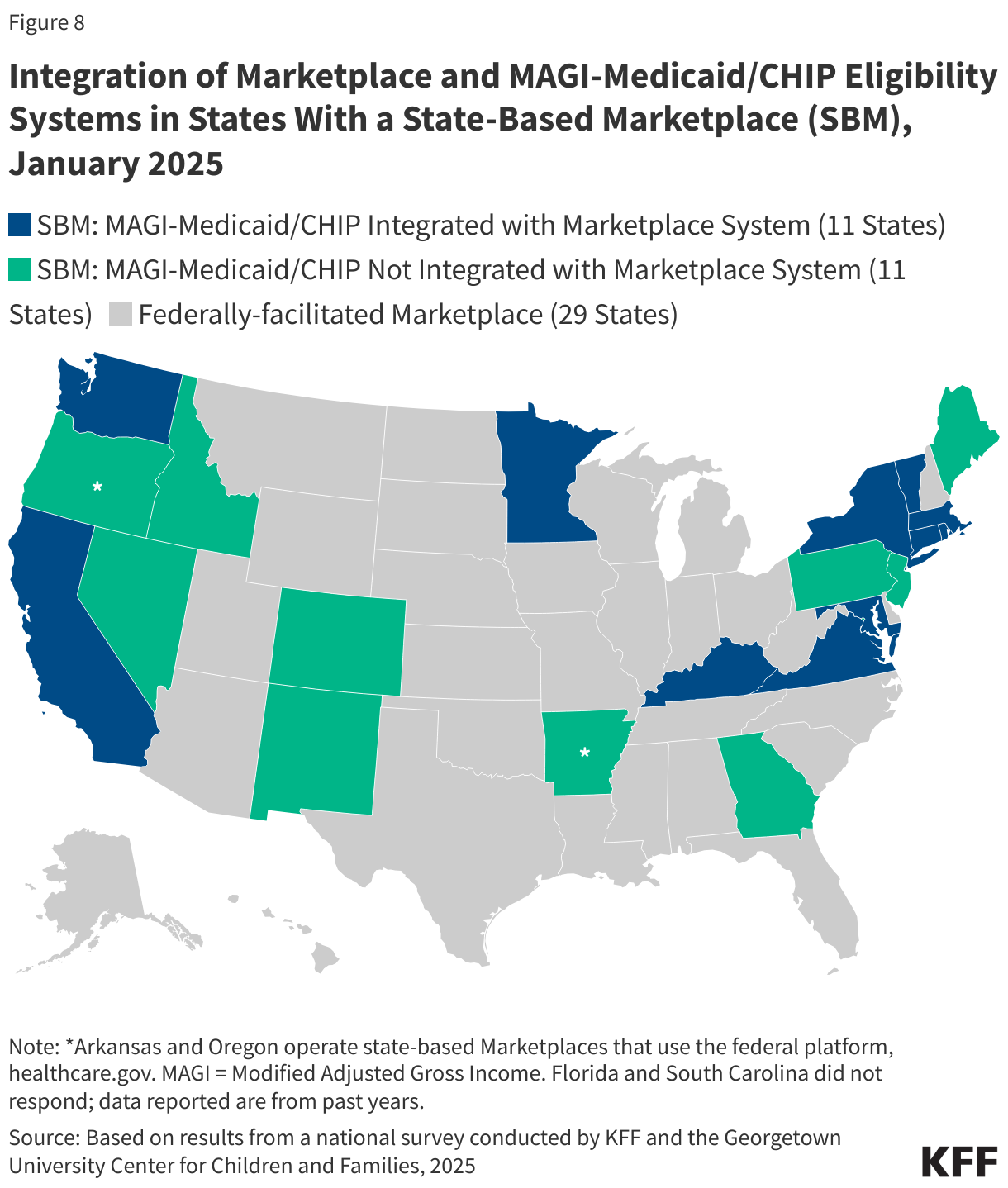

Over half of states that operate their own Marketplace eligibility systems (11 of 20 SBM states) have integrated eligibility for MAGI Medicaid into their SBM systems (Figure 8). The remaining nine SBM states as well as the two SBM states that use the Federally-facilitated Marketplace (FFM) have separate eligibility systems for determining eligibility for MAGI Medicaid and CHIP. Of the 29 reporting states that rely on the Federally-facilitated Marketplace (FFM) for all marketplace functions, 9 allow the FFM to determine Medicaid eligibility while the FFM assesses eligibility in 20 states.

Many states have integrated Medicaid systems that determine eligibility for both MAGI Medicaid and CHIP and non-MAGI Medicaid as well as non-health programs including SNAP, TANF and childcare subsidies. Of the 38 reporting states that have Medicaid eligibility systems that are not integrated with the SBM, 34 have systems that also determine eligibility for non-MAGI Medicaid; 24 states have integrated SNAP and TANF eligibility; and 13 states have systems that also determine eligibility for child care subsidies (Figure 9).

States have developed online tools, including multi-benefit applications, online accounts, and mobile apps to make it easier for people to apply for, renew, and manage their Medicaid coverage. All states have an online application, and most states have multi-benefit applications that incorporate non-MAGI Medicaid (40 states), SNAP (31 states); TANF (29 states); and childcare subsidy (18 states). Medicaid applications in 15 states allow individuals to apply for premium tax credits, all are SBM states. With one exception, all reporting states have an online account that enables people to apply for or renew their coverage, report changes in circumstances, view notices, or upload verification documents. Eight states have also created mobile apps through which people can submit a MAGI-based Medicaid application. These mobile apps also include many of the same features for managing Medicaid coverage as online accounts but are specifically designed to function well on smartphones and tablets. An additional six states report having a mobile app that allows users to manage their coverage but does not include application functionality (Figure 10).

States vary in their approaches to online account security and resetting passwords. Over half the states (29) require identity verification to set up an online account while 30 states use multi-factor authentication for one or more actions. Multi-factor authentication is required to set up the account in 26 states, reset passwords in 24 states, and every time the account is accessed in 15 states (Figure 11). Remembering passwords to access accounts can be challenging, especially when the accounts are not accessed frequently. Most states (41) offer at least two ways for online account users to reset passwords. Most often users can request a link be sent via email or text (41 states) or by answering security questions (33 states). Individuals in most states (30 states) may contact the Medicaid call center for a password reset, but it is the only way to reset a password in one state.

About a quarter of states are using artificial intelligence (AI) to support consumer assistance. States use AI to answer consumer questions on the website (12 states), during the application (6 states) and renewal (7 states) processes, and on using online accounts (8 states) (Figure 12). A couple of states also use chatbots to update contact information and collect information on newborns. A smaller number of states (5) report using AI to assist with eligibility and enrollment processes, including by using bots to read information from certain documents submitted by MAGI applicants and to assist with reviewing non-MAGI ex parte renewals and other case renewals.

Eligibility and Enrollment Policies

Eligibility Policies

While child eligibility remains the highest for all MAGI eligibility groups, the median eligibility limit for pregnancy coverage in Medicaid and CHIP increased from 210% to 213% of the federal poverty level (FPL) with eligibility expansions in two states. In 2025, the median child eligibility remained unchanged at 255% FPL, or $67,957 for a family of three. Alaska and Washington expanded pregnancy eligibility and Colorado adopted the From Conception to End of Pregnancy (FCEP) CHIP option in 2025, becoming the 25th state to adopt this coverage. Since 2023, five states (Alaska, Nevada, North Dakota, Tennessee, and Washington) have increased pregnancy eligibility levels, but one state (Iowa) is seeking approval to reduce pregnancy income eligibility from 380% FPL to 215% FPL.

In states that have not implemented Medicaid expansion, median eligibility for parents is 33% FPL (Figure 13). Half of the ten non-expansion states base eligibility for parents on dollar thresholds that are not routinely updated and erode over time with inflation. Among non-expansion states, only Wisconsin covers adults without dependent children. Through a section 1115 waiver, Georgia provides coverage to parents who do not qualify for section 1931 parent eligibility and childless adults with incomes up to 100% FPL with initial and continued enrollment conditioned on meeting work requirements. Non-expansion states have lower median eligibility levels for all MAGI Medicaid groups compared to expansion states, including for children (234% FPL in non-expansion states compared to 266% FPL in expansion states); for pregnancy coverage (203% FPL compared to 213% FPL), and for parents (33% FPL compared to 138% FPL).

Two-thirds of states cover lawfully-residing immigrant children and pregnant individuals. Thirty-eight states use federal funds authorized under the Immigrant Child Health Insurance Act (ICHIA) to cover lawfully-residing children in both Medicaid and CHIP without requiring the 5-year waiting period. Thirty-two states also provide pregnancy coverage for lawfully-residing immigrant individuals without the 5-year wait.

Enrollment Policies

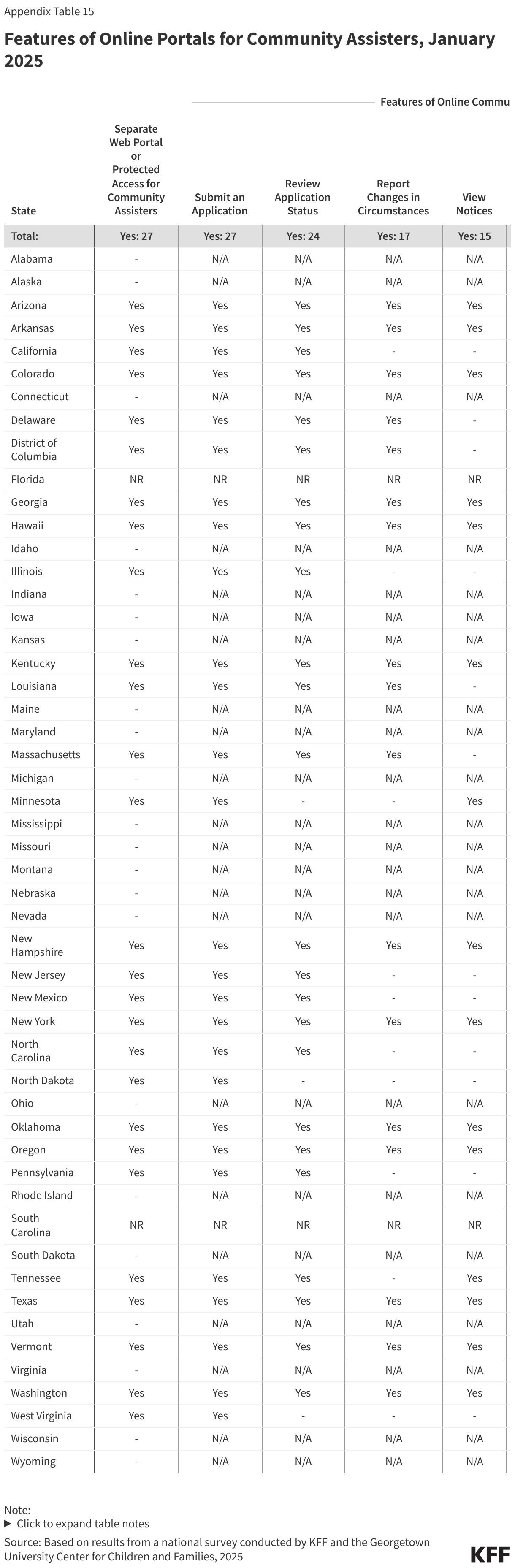

Just over half of states have a separate web portal or protected access to the application portal for certain entities to assist individuals in enrolling and managing their account (Figure 14). The entities authorized to use the portals include health care providers (community health centers, hospitals, and pharmacists), community-based organizations, navigators and application assisters, and MCOs. In all 27 states with portals, authorized assisters can submit facilitated applications; they also have access to many of the features available in online accounts to help individuals report changes and stay enrolled. Seventeen states provide financial support to authorized assisters, primarily through grants and contracts.

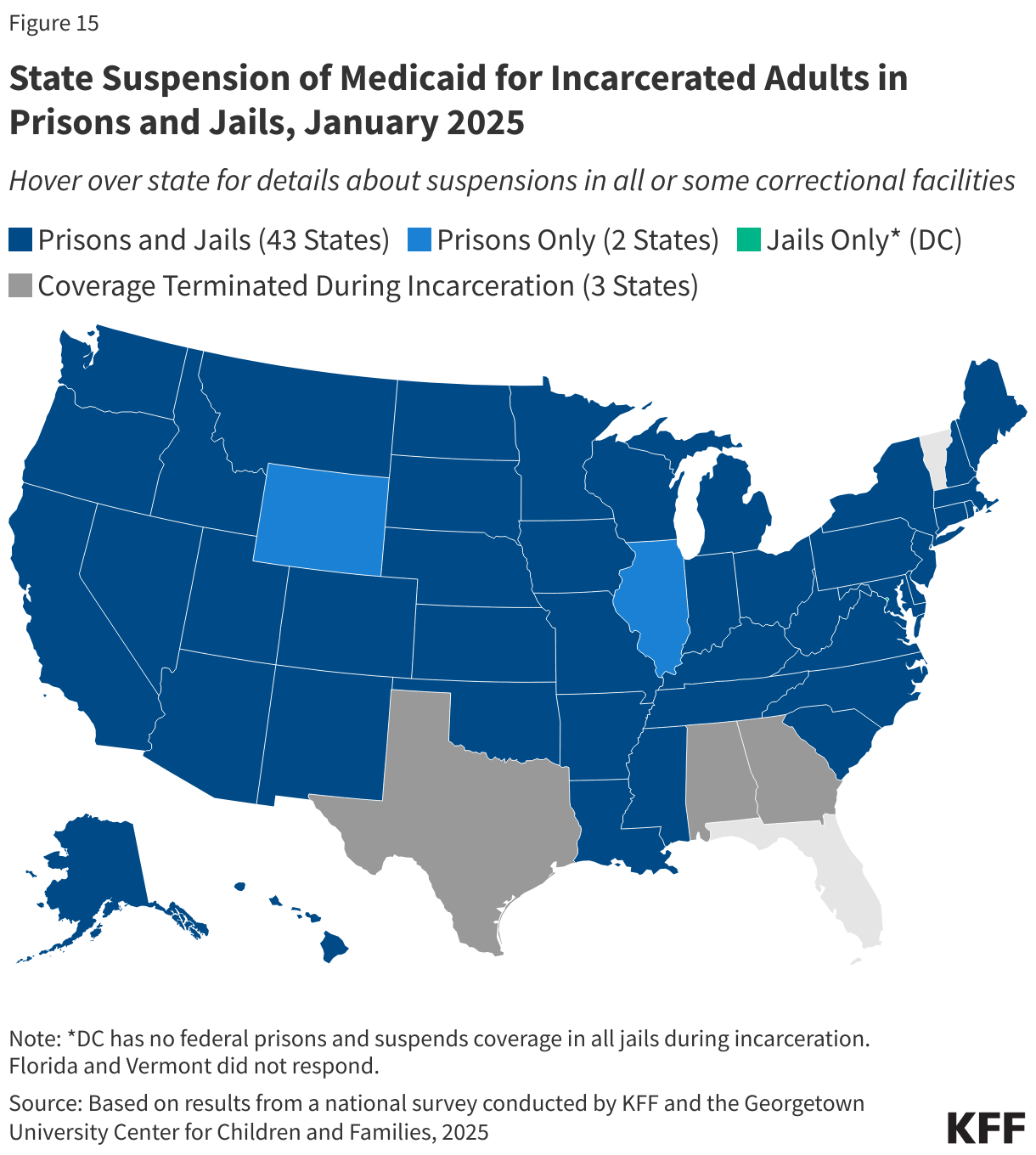

Most states suspend, rather than terminate, Medicaid eligibility for adults during incarceration. Although benefits during incarceration are limited to in-patient hospital stays, 46 states suspend Medicaid coverage when an adult is incarcerated (Figure 15). Nearly all of these states suspend coverage in prisons and jails (43 states) while two states suspend coverage in prisons only, and the District of Columbia, which does not operate any prisons, only suspends coverage in jails. Twelve states employ an automated process for suspending coverage while 5 states use a combination of automated and manual processes. Currently 25 states use only a manual process, and 3 states use some other process, but many states indicated they are working to build automated data interfaces. The Consolidated Appropriations Act, 2023 requires all states to suspend rather than terminate Medicaid coverage when people are incarcerated beginning in 2026. Suspended eligibility makes it easier for states to reactivate reimbursement for inpatient services and take advantage of reentry waiver opportunities. A growing number of states are using reentry waivers to provide access to prescription drugs and mental health and substance use disorder services prior to release to facilitate the transition back into the community and to reduce recidivism.

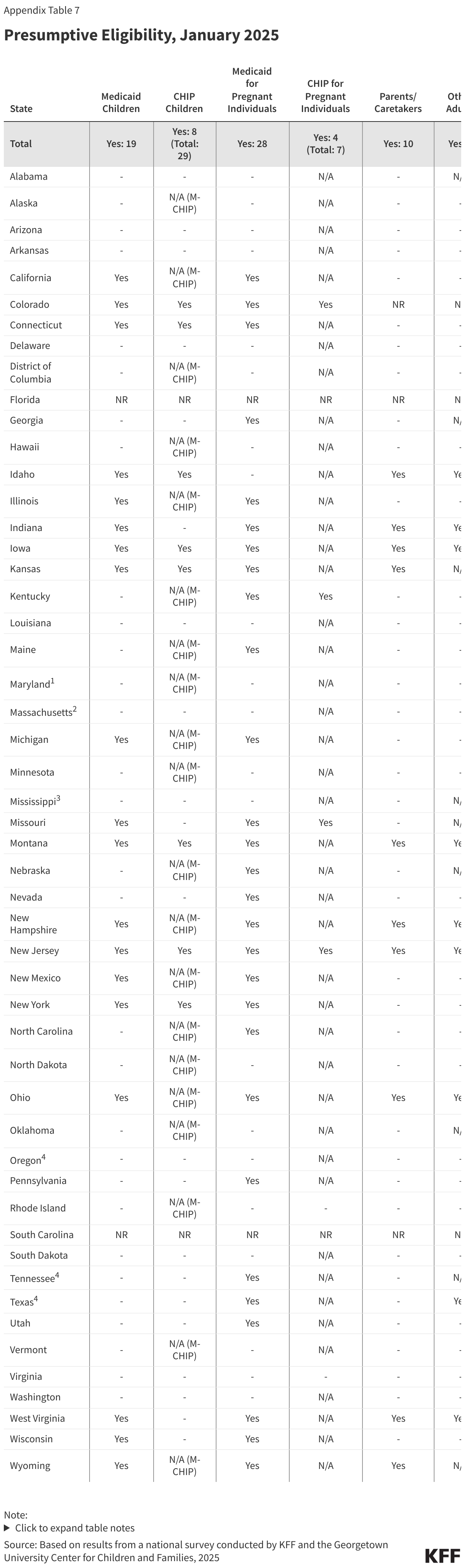

States use presumptive eligibility to expedite enrollment primarily for children and pregnant people. More than half of states authorize qualified entities to screen for eligibility and make a presumptive eligibility (PE) determination to temporarily enroll the individual while the regular application is being processed. PE is a long-standing state policy option designed to expedite immediate access to needed health care services. Twenty-eight states have implemented PE for pregnant people while 19 states have adopted PE for children in Medicaid and 8 use PE for children in their separate CHIP program (Figure 16). PE is used for other adult populations in 17 states and for former foster youth in 9 states. States have flexibility in selecting which types of entities are authorized to make PE determinations. However, all states must also allow hospitals to make presumptive determinations for all populations if the hospital elects to do so.

Fewer states (8) use Express Lane Eligibility (ELE) to automatically enroll and/or renew Medicaid eligibility based on data and eligibility findings from other public benefit programs. ELE policy is limited to children unless a state receives waiver authority to include parents; two states (Massachusetts and Maryland) use ELE to renew coverage for parents to facilitate renewal for the family (Table 2). Information from SNAP is most commonly used for ELE, but some states use information from other programs, including TANF, WIC, and state tax data. ELE can be particularly useful in states without eligibility systems that are integrated with non-health programs by eliminating duplication of data collection and verification processes used by other programs.

Most states have eliminated waiting periods in separate CHIP programs. Only four states continue to require children to be uninsured for a certain period before they can enroll in CHIP, down from 13 states with waiting periods in 2020. Three states require a waiting period of 90 days and one has a waiting period of 2 months. Two of the states plan to phase out the waiting periods by July 2025. All states are required to phase out waiting periods by June 2025, based on new requirements in the E&E rule.

Eighteen states currently charge premiums for children; two of those states impose a lockout period of up to 90 days if premiums are unpaid (Figure 17). Two states (Utah and Delaware) permanently eliminated CHIP premiums in 2024, while Georgia reinstated CHIP premiums after pausing them during the COVID pandemic. Premiums are suspended temporarily or indefinitely in Arizona and Vermont. States may not charge premiums in Medicaid or M-CHIP programs for children with incomes below 150% FPL, but separate CHIP programs may impose premiums on children with household incomes at or above 133% FPL. Premiums can be charged on a monthly, quarterly, or annual basis (also known as an enrollment fee) and can be family-based or per-child, with or without a family cap. The maximum premium or enrollment fee amount for one child ranges from $15 in Idaho to $192 in Missouri, with some states varying premiums based on income. If premiums are unpaid in Kansas or Louisiana, children are locked out of coverage at the end of their 12-month continuous eligibility period for a period of 90 days or until the premium is paid. States are required to phase out nonpayment lockouts by June 2025, based on new requirements in the E&E rule.

Appendix Tables