FAQs on Medicare Financing and Trust Fund Solvency

Key Takeaways

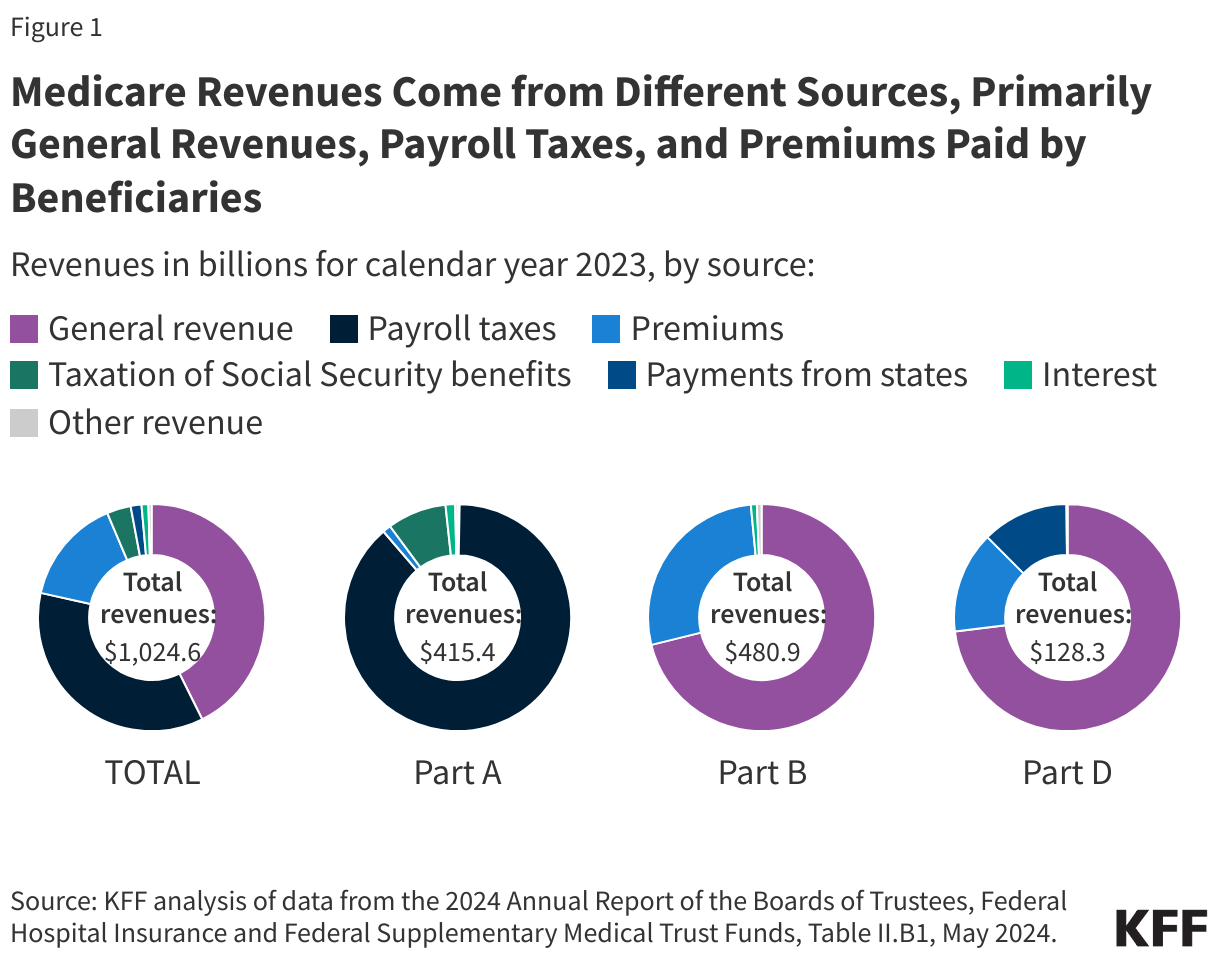

- Funding for Medicare, which totaled $1 trillion in 2023, comes primarily from general revenues (government contributions), payroll tax revenues paid by employers and workers, and premiums paid by beneficiaries.

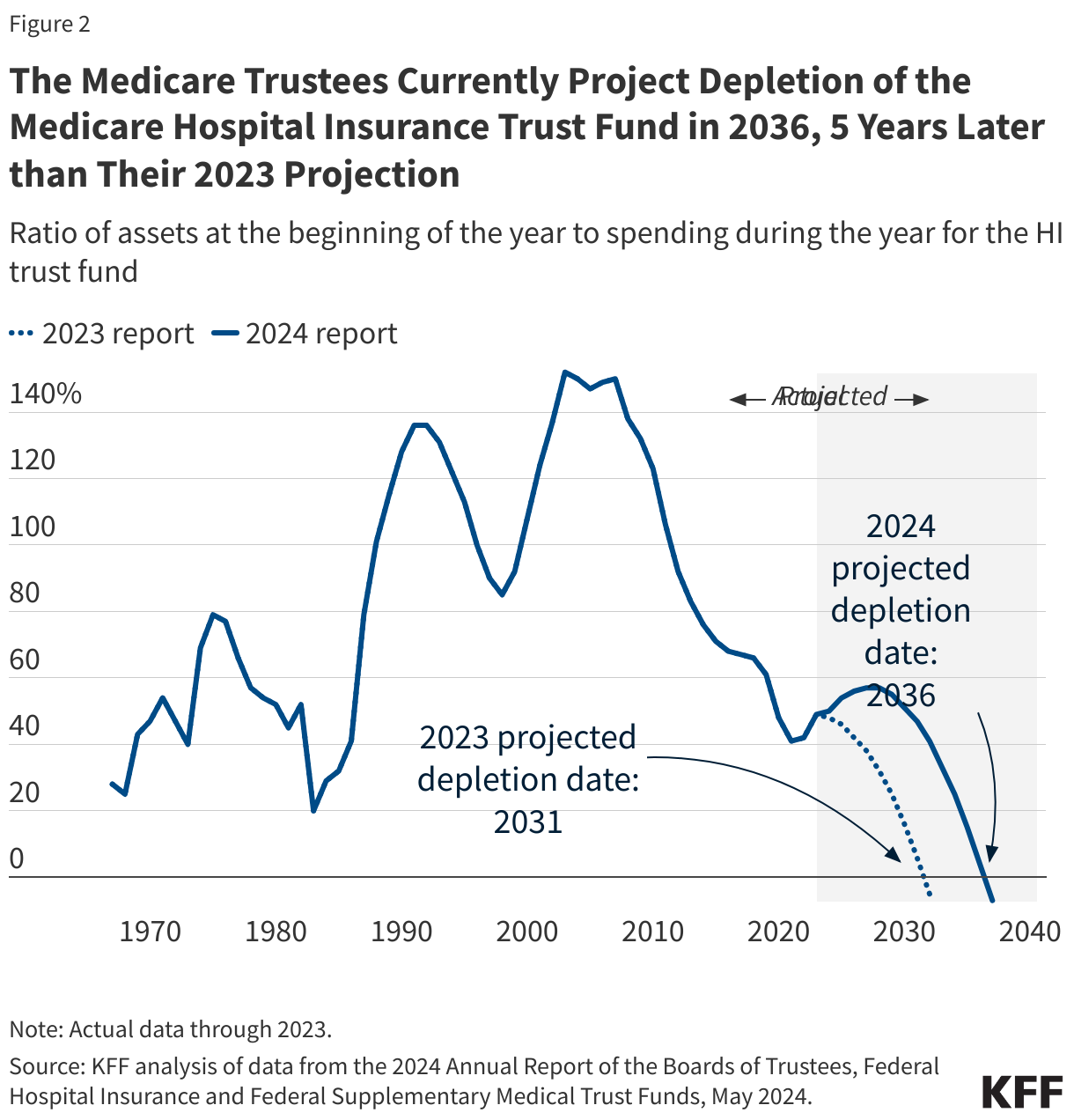

- Based on current projections from the Medicare Board of Trustees’ 2024 report, the Medicare Part A (Hospital Insurance, or HI) trust fund is projected to be depleted in 2036, 12 years from now – an improvement of five years compared to the projected depletion date of 2031 in the previous report due to higher expected revenues and lower projected spending. To date, lawmakers have never allowed the HI trust fund to be fully depleted.

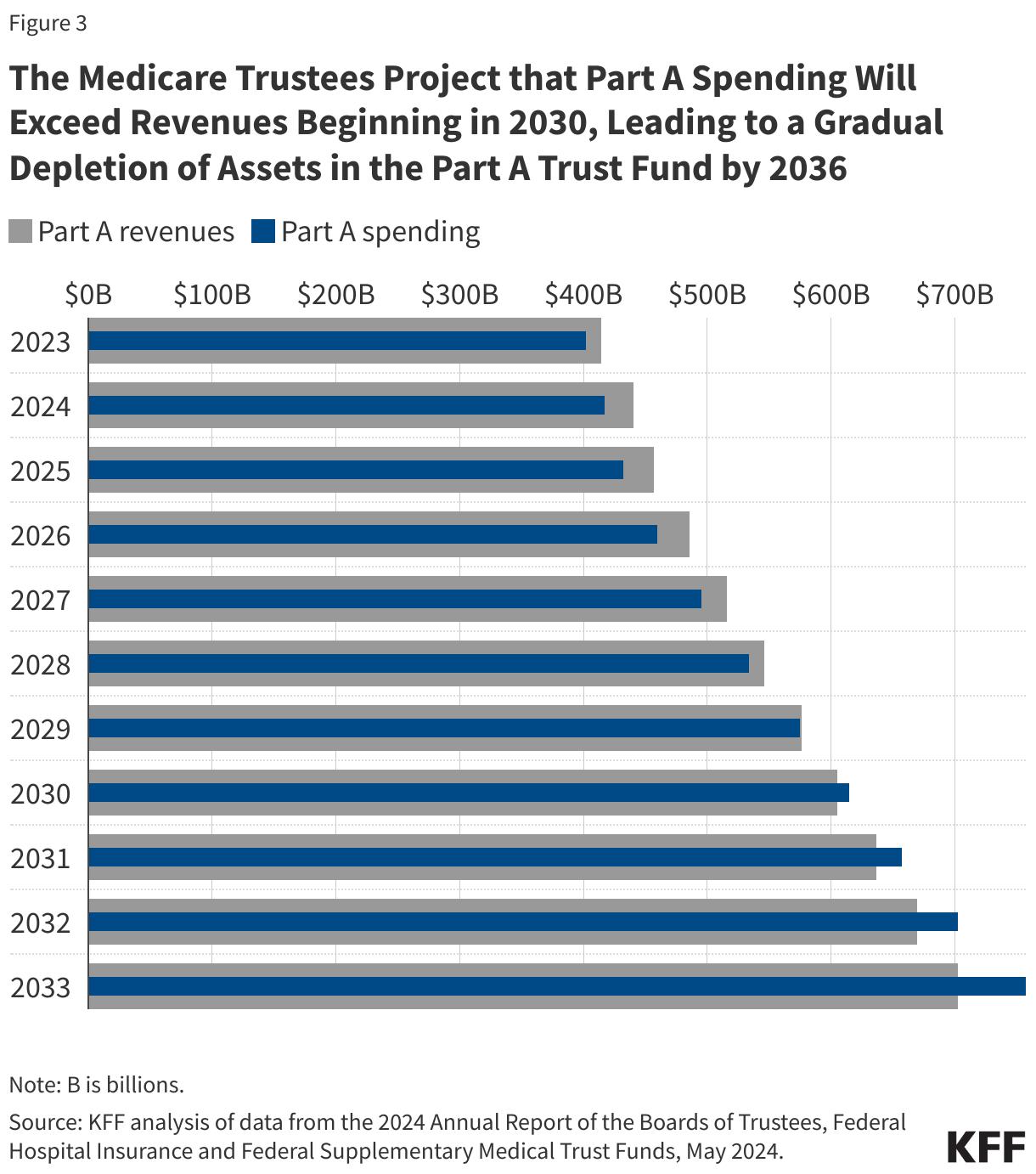

- Total Part A spending is projected to exceed revenues beginning in 2030, which means trust fund reserves will be needed to pay benefits in full. By 2036, there will be insufficient revenues, including reserves, to pay full benefits for the year. Medicare would be able to pay 89% of costs covered under Part A using payroll tax revenues in that year.

- The revenues for Medicare Parts B and D are determined annually to meet expected spending obligations for the coming year, meaning that the Supplementary Medical Insurance, or SMI, trust fund does not face a funding shortfall, in contrast to the HI trust fund. But higher projected spending on Part B and Part D will increase the amount of general revenues and beneficiary premiums required to cover this spending. Altogether, beneficiary premiums and cost sharing for Part B and Part D are estimated to account for 26% of the average Social Security benefit in 2024.

- With rising enrollment in Medicare Advantage, payments to Medicare Advantage plans are rising as a share of Part A and Part B spending, which affects the balance of the HI Trust Fund and Part B premiums. In 2024, MedPAC estimates that the Medicare program will spend 22% more per Medicare Advantage enrollee than for similar beneficiaries in traditional Medicare – an additional $83 billion in total.

- The Medicare trustees estimate that an increase of 0.35% of taxable payroll (increasing the 2.9% payroll tax to 3.25%) or a spending reduction of 8% would bring the HI trust fund into balance over the long term.

Introduction

Medicare, the federal health insurance program for 67 million people ages 65 and over and younger people with long-term disabilities, helps to pay for hospital and physician visits, prescription drugs, and other acute and post-acute care services. In 2023, Medicare benefit payments totaled $839 billion, net of premiums and other offsetting receipts. Accounting for 21% of national health care spending and 12% of the federal budget in 2022, Medicare spending often plays a major role in federal health policy and budget discussions.

In discussions of Medicare’s financial condition, attention frequently centers on one specific measure —the solvency of the Medicare Hospital Insurance (HI) trust fund, out of which Medicare Part A benefits are paid. Based on current projections from the Medicare Board of Trustees in their 2024 report, the HI trust fund is projected to be depleted in 2036, 12 years from now – an improvement of five years compared to the projected depletion date of 2031 in the previous report due to higher expected revenues and lower projected spending.

The HI trust fund depletion date is only one way of measuring Medicare’s financial status and doesn’t present a complete picture of total program spending and revenues, but it does indicate whether there is an imbalance between spending and financing for inpatient hospital and other benefits covered under Medicare Part A. These FAQs answer key questions about Medicare financing and trust fund solvency.

How is Medicare financed?

Funding for Medicare, which totaled $1 trillion in 2023, comes primarily from general revenues (government contributions), payroll tax revenues paid by employers and workers, and premiums paid by beneficiaries (Figure 1). Other sources include taxes on Social Security benefits, payments from states, and interest. The different parts of Medicare are funded in varying ways, and revenue sources dedicated to one part of the program cannot be used to pay for another part.

- Part A, which covers inpatient hospital stays, skilled nursing facility (SNF) stays, some home health visits, and hospice care, is financed primarily through a 2.9% tax on earnings paid by employers and employees (1.45% each). Higher-income taxpayers (more than $200,000 per individual and $250,000 per couple) pay a higher payroll tax on earnings (2.35%). Payroll taxes accounted for 88% of Part A revenue in 2023.

- Part B, which covers physician visits, outpatient services, preventive services, and some home health visits, is financed primarily through a combination of general revenues (71% in 2023) and beneficiary premiums (27%) (and 1% from interest and other sources). Beneficiaries with annual incomes over $103,000 per individual or $206,000 per couple pay a higher, income-related Part B premium reflecting a larger share of total Part B spending, ranging from 35% to 85%. The standard monthly Part B premium in 2024 is $174.70, while the income-related monthly premiums range from $244.60 to $594.

- Part D, which covers outpatient prescription drugs, is financed primarily by general revenues (73%), with additional revenues coming from beneficiary premiums (14%) and state payments for beneficiaries enrolled in both Medicare and Medicaid (12%). Higher-income enrollees pay a larger share of the cost of Part D coverage, as they do for Part B.

The Medicare Advantage program (Part C) is not separately financed. Medicare Advantage plans, such as HMOs and PPOs, cover Part A, Part B, and (typically) Part D benefits. Funds for Part A benefits provided by Medicare Advantage plans are drawn from the Medicare HI trust fund (accounting for 48% of total spending on Part A benefits in 2023). Funds for Part B and Part D benefits are drawn from the Supplementary Medical Insurance (SMI) trust fund. Beneficiaries enrolled in Medicare Advantage plans pay the Part B premium and may pay an additional premium for their plan.

What does Medicare trust fund solvency mean and why does it matter?

The solvency of the Medicare Hospital Insurance (HI) trust fund, out of which Part A benefits are paid, is a common way of measuring Medicare’s financial status, though because it only focuses on the status of Part A, it does not present a complete picture of total program spending. Medicare solvency is measured by the level of reserves in the HI trust fund. In years when annual income to the trust fund exceeds benefits spending, the level of reserves increases, and when annual spending exceeds income, the level of reserves decreases. This matters because when spending exceeds income and the reserves are fully depleted, Medicare will not have sufficient funds to pay hospitals and other providers for all Part A benefits that are provided in a given year. Based on current projections from the Medicare trustees, Part A spending will exceed Part A revenues beginning in 2030.

When are HI trust fund reserves projected to be depleted?

Each year, the Medicare trustees provide an estimate of the year when the HI trust fund reserves are projected to be fully depleted. In the 2024 Medicare Trustees report, the trustees project that reserves in the Part A trust fund will be depleted in 2036, 12 years from now. This is an improvement of five years from the projection in the 2023 Medicare Trustees report, when the depletion date was projected to be 2031 (Figure 2).

In the coming decade, based on current projections from the Medicare trustees, Part A spending will exceed Part A revenues beginning in 2030, leading to a gradual reduction in the level of reserves in the HI trust fund (Figure 3). By 2033, the Medicare trustees project that the HI trust fund will begin the year with $254 billion in reserves, but because spending is projected to exceed revenue by $55 billion that year, the trust fund is expected to end the year with $198 billion in reserves. As Part A spending is projected to continue to exceed Part A revenues in the years that follow, the reserves will be depleted at some point during the year in 2036.

What happens if the reserves in the HI trust fund are fully depleted? Can Medicare go bankrupt?

Medicare cannot go bankrupt or go broke. While some describe Medicare or the Medicare HI trust fund as heading toward bankruptcy or going broke when referring to the depletion of HI trust fund reserves, Medicare will not cease to operate if HI trust fund reserves are fully depleted because revenue will continue flowing into the fund from payroll taxes and other sources.

Based on current projections of trust fund reserve depletion in 2036, Medicare would be able to pay 89% of costs covered under Part A using payroll tax revenues in that year. However, there is no automatic process in place or precedent to determine how to apportion the available funds or how to fill the shortfall.

What factors affect the solvency of the HI trust fund and what explains the improved status in 2024?

The solvency of the Medicare HI trust fund is affected by several factors. In addition to legislative and regulatory changes that affect Part A spending (both utilization of services and payments for services provided by hospitals, skilled nursing facilities, and other providers, and for Part A services covered by Medicare Advantage plans) and revenues, Part A trust fund solvency is affected by:

- the level of growth in the economy, which affects Medicare’s revenue from payroll tax contributions: economic growth that leads to higher employment and wages boosts revenue to the trust fund, while an economic downturn can have the opposite effect,

- overall health care spending trends: higher health care price and cost growth can lead to higher spending for services covered under Medicare Part A that could hasten the depletion date, while moderation in the growth of prices and costs could slow spending growth, and

- demographic trends: this includes the aging of the population, which is leading to increased Medicare enrollment (especially between 2010 and 2030 when the baby boom generation reaches Medicare eligibility age); a declining ratio of workers per beneficiary making payroll tax contributions, which means lower revenue; and other factors, such as fertility rates, disability rates, and immigration.

In the 2024 report, the Medicare trustees attributed the improvement in the financial status of the HI trust fund to a combination of factors:

- Income to the HI trust fund is projected to be higher than in the 2023 report due to higher employment and average wage growth.

- Part A spending is projected to be lower than last year’s estimates due to a policy change to exclude graduate medical education expenses associated with enrollees in Medicare Advantage from the fee-for-service costs used to determine payments to Medicare Advantage plans.

- Projected Part A spending on inpatient and home health services is lower than previously estimated, with more recent spending data informing these projections.

How have the solvency projections of the HI trust fund changed over time?

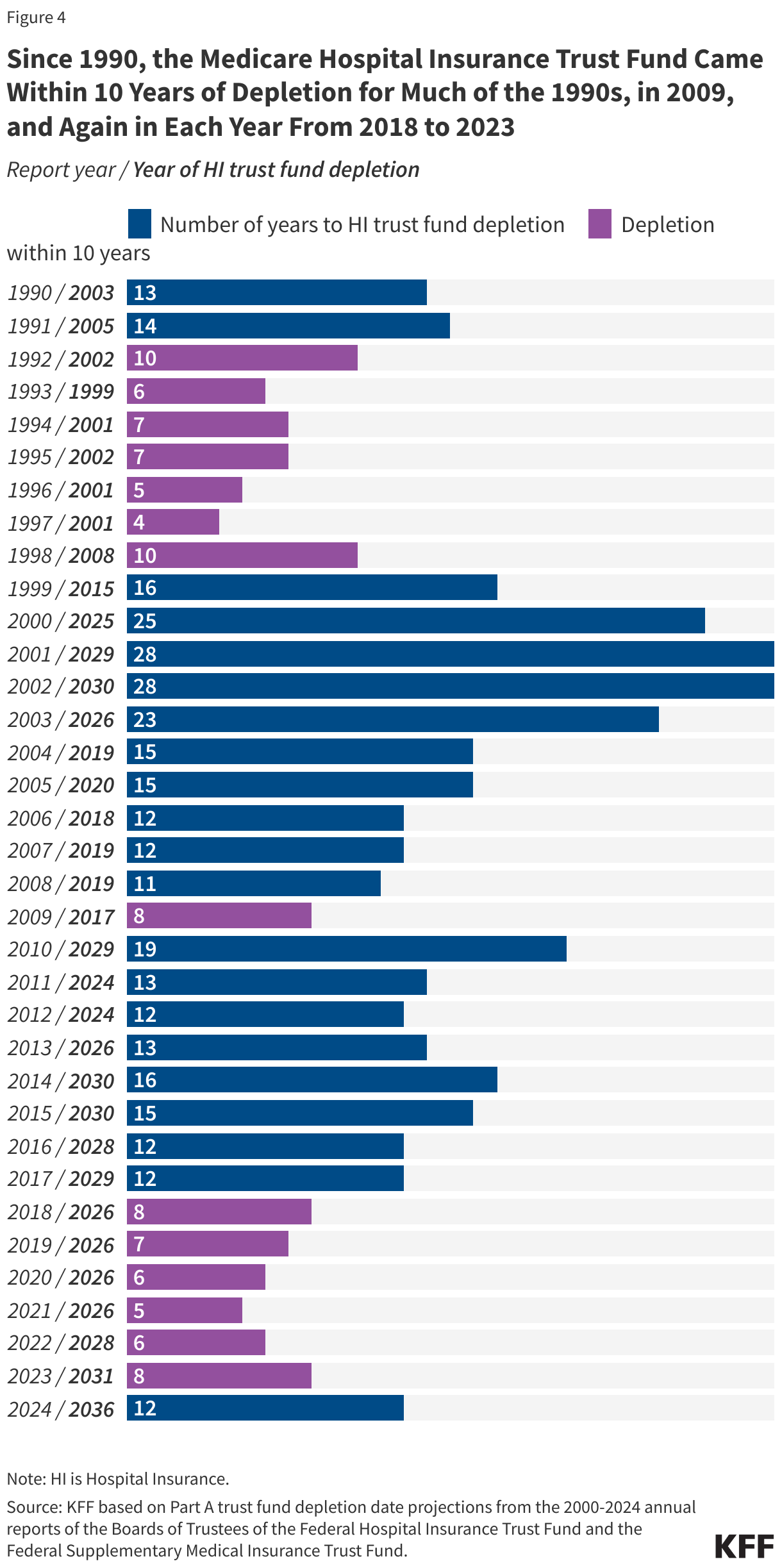

Since 1990, the HI trust fund came within 10 years of depletion for much of the 1990s, in 2009, and again in each year between 2018 and 2023 (Figure 4). To improve the fiscal outlook of the trust fund in the 1990s, Congress enacted legislation to reduce Medicare spending obligations, while policy changes adopted in the Affordable Care Act of 2010 – including reduced Medicare payments to plans and providers and increased revenues – helped to improve the status of the HI trust fund between 2009 and 2010. To date, lawmakers have never allowed the HI trust fund to be fully depleted.

What is the Medicare funding warning and why does it matter?

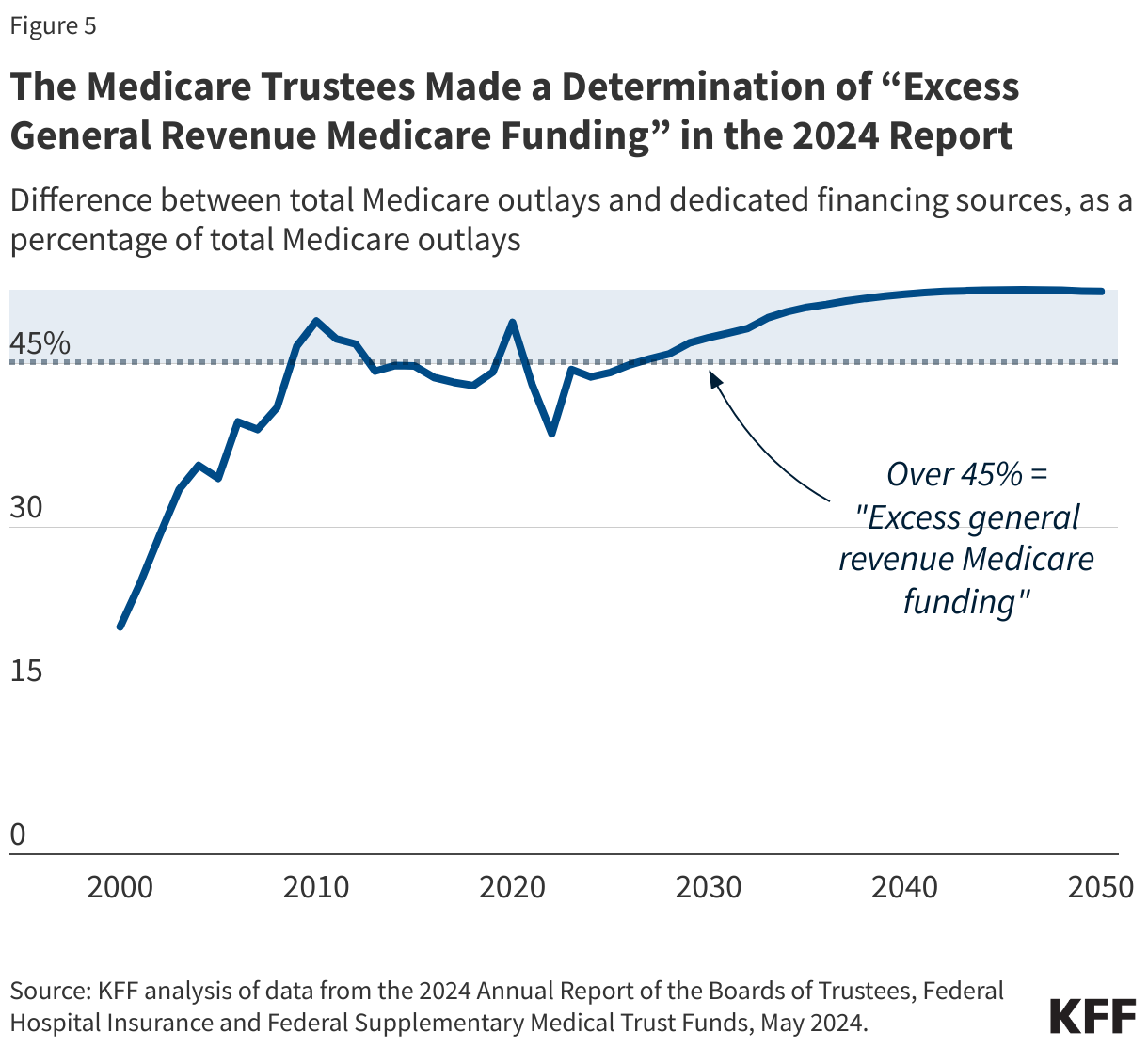

The Medicare Modernization Act of 2003, the law that created the Medicare Part D drug benefit, also included a provision that required the Medicare Trustees to calculate annually whether the difference between total Medicare outlays and specified dedicated financing sources is expected to account for more than 45% of Medicare outlays in the current fiscal year or any of the next six fiscal years. If so, the trustees issue a determination of “excess general revenue Medicare funding,” and making such a determination in two consecutive reports triggers a “Medicare funding warning.”

In their 2024 report, the Medicare Trustees made a determination of “excess general revenue Medicare funding” based on projections of general revenue funding exceeding 45% in the next seven years, and because the same determination was made in the 2023 report, this triggered a “Medicare funding warning” (Figure 5). In fact, the trustees have made a determination of excess general revenue funding for eight years in a row and issued funding warnings for seven years in a row.

While this measure is intended to draw attention to Medicare spending and revenues and the role of government contributions in funding the Medicare program, no automatic changes are made to Medicare if the funding warning is issued. Instead, the President is required to submit legislation to Congress to respond to the warning, and an expedited process is in place for the Congress to consider the President’s proposed legislation. To date, however, only President George W. Bush in 2008 submitted a proposal to Congress in direct response to a Medicare funding warning issued by the Medicare Trustees in 2007, but Congress took no action on that proposal.

Are Medicare Part B and Part D also facing a trust fund shortfall?

The Hospital Insurance trust fund provides financing for only one part of Medicare, so it represents only one part of Medicare’s total financial picture. While Part A is funded primarily by payroll taxes, benefits for Part B physician and other outpatient services and Part D prescription drugs are funded by general revenues (government contributions) and premiums paid for out of separate accounts in the Supplementary Medical Insurance, or SMI, trust fund. The revenues for Medicare Parts B and D are determined annually to meet expected spending obligations for the coming year, meaning that the SMI trust fund does not face a funding shortfall, in contrast to the HI trust fund.

However, higher projected spending for benefits covered under Part B and Part D will increase the amount of general revenues and beneficiary premiums required to cover costs for these parts of the Medicare program in the future. The Medicare trustees project that the standard monthly Part B premium will increase from $174.70 in 2024 to nearly $300 in 2033, accounting for 15% of the average retired worker’s Social Security benefit in 2033, up from 10% in 2024. Altogether, premiums and cost sharing for Part B and Part D are estimated to account for 26% of the average Social Security benefit in 2024.

How do payments to Medicare Advantage plans affect the solvency of the Part A Trust Fund and Part B premium and general revenue spending?

With the rise in Medicare Advantage enrollment, payments to private Medicare Advantage plans account for a growing share of total Medicare spending under Part A and Part B. According to current projections, payments to Medicare Advantage plans are projected to rise as a share of total Part A spending from 48% in 2023 to 54% in 2033, a shift that could impact HI trust fund solvency. Medicare Advantage is also projected to rise as a share of total Part B spending, from 55% in 2023 to 65% in 2033, which could impact both beneficiary premiums and general revenue spending. In 2024, MedPAC estimates that the Medicare program will spend 22% more per Medicare Advantage enrollee than for similar beneficiaries in traditional Medicare – an additional $83 billion in total.

What is the longer-term outlook for Medicare financing and trust fund solvency?

Although current projections show that the short-term solvency outlook for the Medicare HI trust fund has improved, the Medicare program continues to face longer-term financial pressures associated with higher health care costs and an aging population. The Medicare trustees estimate that an increase of 0.35% of taxable payroll (increasing the 2.9% payroll tax to 3.25%) or a spending reduction of 8% would bring the HI trust fund into balance over the long term.

To sustain Medicare for the long run, policymakers may consider adopting broader changes to the program that could include both reductions in payments to providers and plans or reductions in benefits, and additional revenues, such as payroll tax increases or new sources of tax revenue. Evaluating such changes would likely involve careful deliberation about the effects on federal expenditures, the Medicare program’s finances, and beneficiaries, health care providers, and taxpayers.

This work was supported in part by Arnold Ventures. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.