Standardized Plans in the Health Care Marketplace: Changing Requirements

Background

For the 2023 coverage year, HealthCare.gov adopted a requirement on participating health insurance insurers to offer standardized plan design (SPD) options to consumers; this requirement will be modified somewhat for 2024 and beyond.1 Such plans apply standardized cost sharing rules to covered benefits. The federal requirement does not apply to SHOP plans sold to small employers; nor does it apply to state-based marketplaces (SBM), though most SBMs also require SPDs.2

One purpose of standardized plans is to simplify and streamline plan comparisons. This year the average HealthCare.gov enrollee faces more than 100 plan options – each with various cost-sharing features (deductibles, copays, and coinsurance) applied differently to different categories of benefits – making it challenging to understand and evaluate plan choices. At least for the SPD options (designated as “easy pricing” plans on HealthCare.gov) consumers can be confident that cost-sharing features will not vary for any given benefit category and can focus on comparing other plan features, such as differences in premiums and provider networks, that they also care about. Federal rules will begin to phase in limits on the number of non-standardized plans that HealthCare.gov insurers can offer next year. Other studies have found that too many health plan choices – for example, more than 30 – confuses and overloads consumers and leads to poor enrollment decisions.3

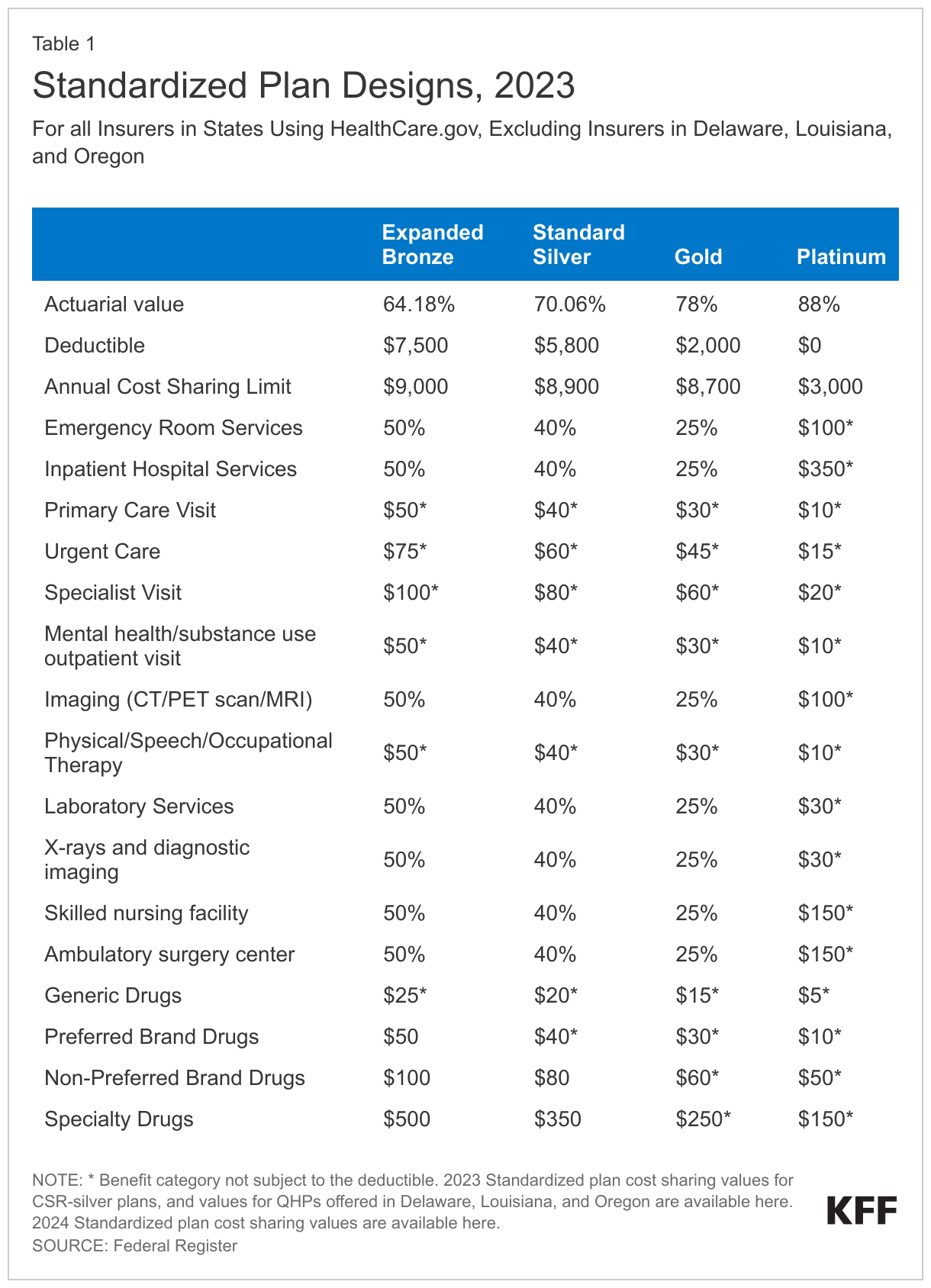

Another purpose of SPDs can be to maximize access to covered services at lower cost sharing. Except when consumers are eligible for cost-sharing subsidies, known as CSR plans, the annual deductibles in marketplace plans are generally quite high.4 This year the average individual annual deductibles in bronze, silver, and gold plans sold on HealthCare.gov are $7,481, $4,890, and $1,650, respectively. All HealthCare.gov SPDs must waive the deductible and instead apply a fixed dollar copay for the following items and services: primary care and specialist office visits, urgent care visits, outpatient visits for mental health and substance use disorder treatment, physical therapy visits, and generic and preferred-brand drugs. Lowering cost sharing for certain services generally means raising cost sharing for others; that is because at each metal level, marketplace plans must achieve a target actuarial value (a measure of the overall level of cost sharing required in a health plan).

Some state-based marketplaces also design SPDs to promote health equity or other population health goals, for example, minimizing cost-sharing for mental health benefits or for services to treat conditions that disproportionately affect underserved populations.

Standardized plans on HealthCare.gov

The 2023 marketplace rule required HealthCare.gov insurers to offer a standardized qualified health plan (QHP) option at every product network type and metal level throughout each service area where they offer non-standardized QHP options. Under federal regulations, a “product” refers to the particular network type an insurer uses to offer the package of covered health benefits, such as a health maintenance organization (HMO) or a preferred provider organization (PPO). Within each product, an insurer may offer multiple “plan” options at each metal level.

Cost sharing values for 2023 SPD plans are shown in Table 1.5 These plans must also use a comprehensive annual deductible that applies to both medical services and outpatient prescription drugs. In addition, CMS requires SPD options to use a 4-tier formulary for outpatient prescription drugs. Generally, tier 1 is for generic drugs, tier 2 is for preferred-brand, tier 3 is for non-preferred brand, and tier 4 is for specialty drugs. CMS proposed to also require plans to assign drugs to formulary tiers in this way. However, this requirement was not adopted in the final 2024 marketplace rule; insurers retain flexibility to assign generic drugs to tiers otherwise designated for brand drugs and vice versa.6

CMS adopted SPD values it determined to be similar to the most popular QHPs in 2021 in terms of deductibles, annual out-of-pocket (OOP) limits, and other cost-sharing parameters so that SPD options would be similar to plans that most consumers were already enrolled in. In addition, CMS sought to maximize the number and types of services that would be covered pre-deductible. Finally, at each metal level, QHPs must have an actuarial value within a de minimis range of the target actuarial value. CMS adopted SPD cost sharing that result in plans with actuarial values near the lower end of the de minimis range.7

How does cost sharing compare in SPD and other plans?

Cost-sharing features vary substantially among the major medical QHPs offered on HealthCare.gov. Here we highlight some differences in cost-sharing designs among silver-level (non-CSR) plans in the federal marketplace.

Annual deductibles: The annual comprehensive deductible for silver SPD options this year is $5,800. By contrast, among 1,674 non-standardized silver plans on HealthCare.gov this year, 1,297 plans have a comprehensive annual deductible that ranges between $0 and $9,050 (with an average of $4,365), while 377 charge a separate annual deductible for outpatient prescription drugs.

Primary care office visits: Silver SPD plans this year waive the annual deductible for all primary care visits and require a flat $40 copay in cost sharing. By contrast, among non-standardized silver plans, primary care office visit copays range from $0 to $105 (with an average of $32). In addition, nearly 500 plans limit the number of primary care office visits in a year that are subject to just a copay; visits beyond the limited number are subject to the annual deductible, and in some of these plans, coinsurance ranging from 10% to 50% may additionally apply.

Outpatient prescription drugs: SPD plans this year apply 4 tiers to the outpatient prescription drug benefit. (In addition, all marketplace plans must include a zero-cost sharing tier for preventive drugs.) Under the silver SPD, the annual deductible is waived for generic and preferred brand drugs with copays of $20 and $40 applied, respectively. Non-preferred brand (tier 3) and specialty drugs (tier 4) are subject to copays of $80 and $350, respectively, after the plan’s annual deductible has been satisfied. Of non-standardized silver plans offered on HealthCare.gov this year, 12% apply 5 or more tiers to the outpatient prescription drug benefit. For drugs on the most expensive tiers in these plans, consumers might be required to pay coinsurance of 40% to 100% or a copay of more than $1,000.

Physical therapy: Silver SPD plans this year waive the annual deductible for physical therapy, speech therapy, and occupational therapy visits and apply a $40 copay. In non-standardized silver plans, physical therapy is often subject to the annual deductible, thereafter a copay (ranging from $5 to $160) or coinsurance (ranging from 5% to 60%) applies.

Inpatient hospital stays: Silver SPD plans this year apply the annual deductible, then 40% coinsurance applies until the patient reaches the annual out-of-pocket (OOP) cost sharing limit of $8,900. In non-standardized silver plans, the annual deductible typically also applies to inpatient hospital care; then coinsurance applies – sometimes 50% or higher. Some non-standardized silver plans apply a per-admission or a per-day copay (ranging from $100 to $3,000) instead of coinsurance.

Numbers of plan options

In 2023, of the 6,126 major medical plans offered to individuals on HealthCare.gov, 1,676 were SPD options and 4,450 were non-standardized. While on average, insurers offer roughly 3 non-standardized plan options for each SPD, some offer many more. Looking just at silver tier HealthCare.gov plans (not including CSR variations), some insurers offered more than 10 non-standardized silver plans for each silver SPD in 2023.8

For the 2024 plan year, CMS will limit insurers to offering no more than 4 non-standardized plan options for each SPD option they offer in a metal level for a given product/network type. This limit on the number of non-standardized plan offerings will be further reduced to 2 for the 2025 plan year and beyond. According to CMS estimates, this change will result in a modest reduction in the weighted average number of plan offerings that consumers face next year, from 113.7 in 2023 to 90.5 in 2024.9

In Appendix Table A, we provide information about silver plan options offered by a single marketplace insurer in one metropolitan area, where the 13 offerings illustrate the considerable complexity of information consumers might need to discern and evaluate as they make plan choices.

Pricing of SPD vs non-standardized plan options

We compared the premiums for SPD options to their non-standardized silver plan counterpart(s) offered by each HealthCare.gov insurer in 2023 by matching the plan service area, the plan type (HMO vs PPO), the provider network ID, and whether the plan covers supplemental adult dental benefits.

For the most part, we observe that insurers tend to charge premiums for SPD options similar to the premium for their lowest-cost non-standardized silver plan counterpart. The 35-year-old-single-adult premium for the silver SPD plan was within $10 per month (higher or lower) compared to the premium of the lowest-cost non-standardized silver plan counterpart 59% of the time in counties where issuers offer both standardized and non-standardized plan counterparts. However, in some cases, insurers set premiums for their silver SPD options that were substantially higher than what they charged for other non-standardized silver plans. For example, one Chicago-area insurer charges a monthly premium for its SPD HMO option that is $47 to $89 higher than for its two corresponding non-standardized HMO plan.10

Given that SPD plans and their non-standardized counterparts cover the same benefits, use the same provider networks, and have the same or nearly the same actuarial values, it is not clear why premiums for otherwise very similar plans would differ so much. However, because premium subsidies are tied to the cost of the second-lowest cost silver plan in an area, it can be difficult for most consumers to afford more costly plan options. As a result, when SPD options cost substantially more than their other non-standardized silver plans, consumers can effectively be discouraged from selecting the SPD.

Standardized plan design in state-based marketplaces

Federal regulations do not require standardized plan designs in state-based marketplaces (SBMs), although 10 of the 18 SBMs require standardized plans this year (CA, CO, CT, DC, ME, MA, NJ, NY, VT, WA). In 4 SBMs (CA, DC, NJ, and VT) only standardized plan designs are offered,11 while 5 SBMs limit the number of non-standardized plans that insurers may offer (CT, ME, MA, NY, and WA.) In addition, Oregon – one of three state-based marketplaces that uses the HealthCare.gov platform – also requires insurers to offer SPD plans.

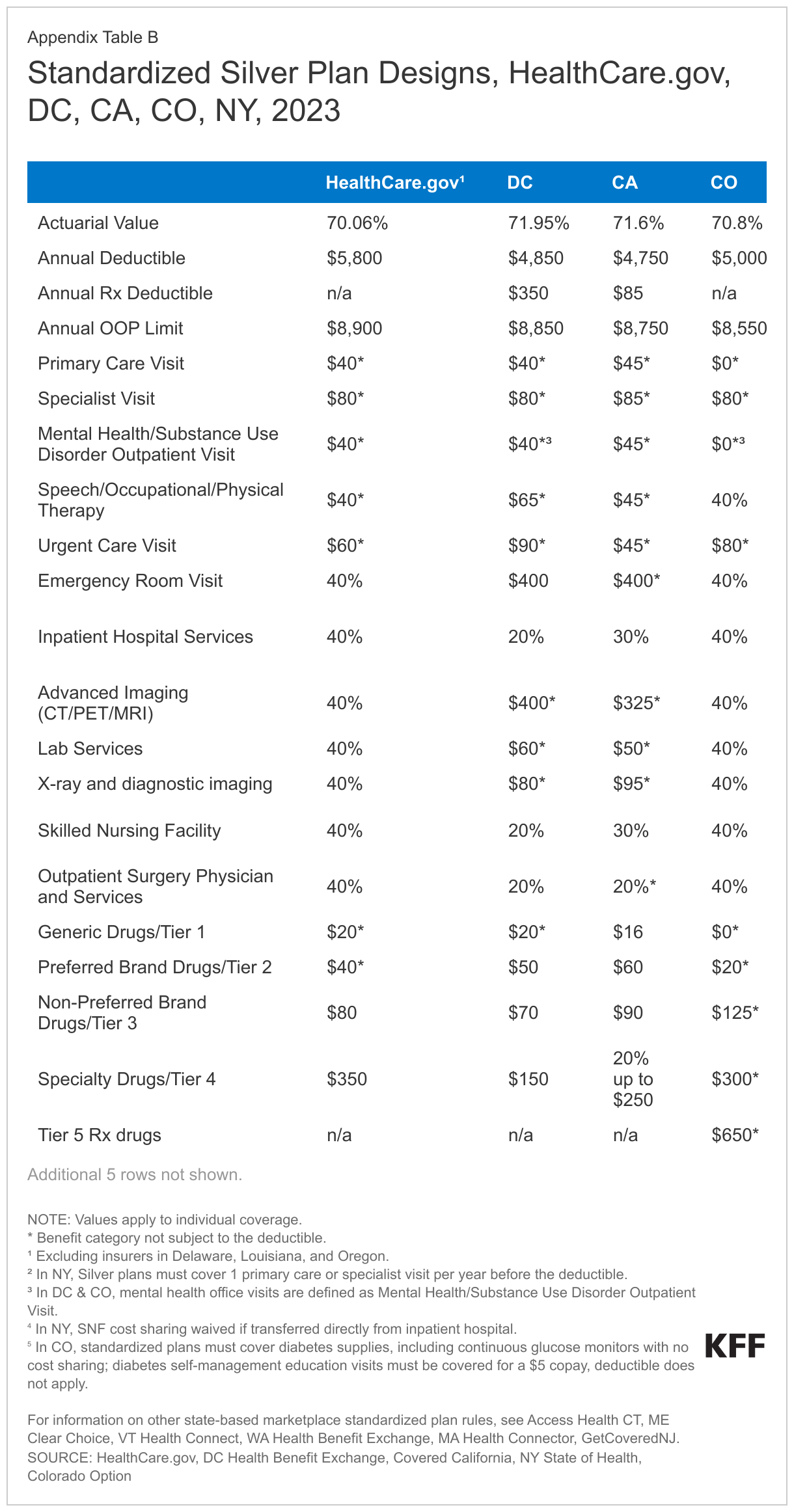

In most of the SBMs, as in HealthCare.gov, the standardized plan design is set to maximize the number and types of services that must be covered pre-deductible. New York takes a different approach, minimizing the annual deductible and applying it to most covered benefits. Under standardized silver plans in NY, for example, the annual deductible is $1,750 – compared to $5,800 in HealthCare.gov SPDs – but it is waived only for one outpatient physician visit annually and for all outpatient prescription medications. Appendix Table B shows SPD cost-sharing features for silver plans in California, New York, Colorado, and the District of Columbia, and links to SPD rules for the other SBMs.

Several SBMs also use the SPD to promote health equity by minimizing cost sharing for services to treat conditions that disproportionately affect racial and ethnic minorities, or to minimize cost sharing for key services for other populations. For example:

- Diabetes – Health plans offered on the marketplace in the District of Columbia must waive all cost sharing for insulin, other medications, supplies and other health services for the management of type 2 diabetes.12 In Colorado, standardized plans impose no cost sharing on diabetes supplies, including continuous glucose monitors, and limit the copay for diabetes self-management education services to $5. Colorado requires all fully insured health plans, including marketplace plans, to cover insulin with a copay of no more than $50.

- Mental health and substance use disorder treatment – Standardized plans at all metal levels in Colorado impose no cost sharing on outpatient visits for mental health and substance use disorder. Starting in 2024, standardized plans in the District of Columbia will waive all cost sharing for outpatient pediatric mental health visits.

- Specialty prescription drugs – At least three SBMs limit cost sharing for other specialty prescription drugs. New York requires standardized silver plans to cover outpatient specialty drugs with a $75 copay and waives the deductible. DC requires SPD plans to have a separate $350 outpatient drug deductible, then limits copays for specialty drugs to $150. California requires a separate $85 outpatient drug deductible, with coinsurance of 20% capped at $250.

- Pediatric benefits – Several SBMs, including California, Connecticut, and DC, waive the annual deductible and limit other cost sharing for certain pediatric dental and vision benefits.

Some state-based marketplaces also publish data on the share of marketplace participants who enroll in standardized plan options. In Colorado, 13% of marketplace enrollees selected the standardized Colorado Option plan the first year it was offered. In Washington, more than 60% of consumers enrolled in a standardized health plan option.

Discussion

As implemented to date, HealthCare.gov’s requirement to offer SPD plans has increased, not decreased, the number of plan choices consumers face. Limits on the number of non-standardized plan options will begin to phase in next year. Though consumers in most areas will continue to face a very large number of plan choices for the foreseeable future, over time the number of plan choices might become more manageable.

Cost-sharing designs in non-standardized plans vary considerably, complicating the task for consumers who want to try to estimate what their out-of-pocket costs might be, even for care they can anticipate needing. Other key plan features, including health plan provider networks and prescription drug formularies, also vary considerably across QHPs and can dramatically impact consumers’ access to and cost for care. Consumers who try to investigate these plan differences face a particularly challenging task as this information can be complex and not very transparent, and their task is made more difficult given the number of plans to investigate.

Beyond trying to simplify plan choices, the SPD can also be a tool to promote other population health goals. For example, last year, Congress considered legislation to limit cost sharing for insulin under Medicare and private health plans to $35 per month. Ultimately the limit was applied only to Medicare; however, states have shown this cost protection could be extended to marketplace enrollees through SPDs. As another example, in its FY 2024 budget, the Administration proposed a requirement on all health plans to cover 3 behavioral health visits and 3 primary care visits annually with no cost sharing. State marketplaces have demonstrated that SPDs can also be used to extend these kinds of protections to marketplace consumers. It remains to be seen if the federal marketplace will further evolve its SPD requirements to promote such health equity and other public health goals.

Appendix Table A

Comparing Silver Plan Options from One HealthCare.gov Insurer in Houston, Texas

Earlier KFF surveys of marketplace enrollees found the monthly premium is named by most people as a very or extremely important factor influencing their plan selection. Even among similarly priced plans, however, there are substantial differences that could affect consumers’ out-of-pocket cost for covered benefits and provider access. In this example, we try to illustrate the amount and complexity of information consumers can face in comparing their marketplace health plan choices.

Residents of Houston, Texas who buy private coverage through HealthCare.gov have a choice of 125 Qualified Health Plans (QHPs) in 2023. Seven insurers together offer 38 bronze, 54 silver, and 33 gold QHPs. (These totals do not include CSR plans.) The table below shows summary information displayed on HealthCare.gov for the 13 silver plans offered by just one insurer. It shows the plan marketing name, unsubsidized monthly premium (for a 35-year-old individual), the type of plan, key cost sharing values, and whether plans include added coverage for adult dental and vision care. Additional details on plan options are also available on HealthCare.gov if consumers click beyond the first plan options screen.

Three of the 13 silver plans offered by this issuer use SPD and 10 use non-standardized cost-sharing designs. The marketing names of these 13 silver plans (Standard, Standard Value, Focused, Focused Value, etc.) signal that the plan choices may involve some key differences, although other than the 3 plans whose names indicate added coverage for adult dental and vision benefits, it is up to the consumer to discern and evaluate what these differences may be.

Price-sensitive consumers might limit consideration to the 4 least expensive plan choices, with monthly premiums ranging from $423.69 to $429.87. Premiums for the other silver plans offered by this issuer exceed $500/month. Though premiums are nearly identical for the 4 cheapest plan options, there are substantial differences in how cost sharing applies to covered benefits.

The cost-sharing structure differs most under the Clear plan, which requires enrollees to pay 100% of allowed charges for all non-preventive services until the annual deductible/OOP maximum is satisfied; thereafter, services are covered 100% for the rest of the plan year.

Relative to the SPD, annual deductibles are $200 and $300 higher under the Complete and Focus plans, and $100 lower under the Virtual Access plan. The annual OOP maximum is lower under all of these non-standardized plans compared to the SPD.

Copays for generic drugs and physician office visits vary somewhat across the SPD and non-standardized plans. The Virtual Access plan name signals that telehealth visits to select primary care physicians under this plan have zero cost sharing, although upon further inspection, all of the silver plan options offered by this issuer provide zero-cost virtual primary care visits.

There are other key cost-sharing differences, though consumers interested in finding this information would need to click further into HealthCare.gov to find it. For example:

- Physical therapy visits are subject to the deductible and 50% coinsurance under all of the non-standardized plans, compared to a $40 copay (pre-deductible) under the SPD.

- Specialty drugs are subject to coinsurance of 40-50% after the deductible under the non-standardized plans, compared to a $350 copay after the deductible in the SPD.

- Hospitalization is subject to the deductible and 50% coinsurance under all of the non-standardized plans, compared to deductible plus 40% coinsurance under the SPD.

- Advanced imaging and durable medical equipment require 50% coinsurance after the deductible under the Focus and Virtual Access plan, vs. 40% after the deductible under the SPD and the Complete plan.

Looking across all plans offered by this issuer, EPO plans generally cost much more than HMO plans. This may be due to differences in the EPO vs HMO provider networks (the CMS plan attribute database shows different network IDs for this issuer’s EPO and HMO plans). However, recognizing and evaluating network differences would be challenging for consumers to explore on their own, and HealthCare.gov offers little help. For QHPs offered in Texas, HealthCare.gov operates a pilot program that provides general descriptive information about the relative breadth of provider networks used by QHPs. However, networks are described only as “smaller than other plans in similar areas” for all plans offered by this issuer, whether HMO or EPO.

Finally, comparing just the 3 SPD silver options offered by this insurer, monthly premiums vary by more than $100 per month. The least expensive (Standard Silver Value) and the most expensive (Standard Virtual Access Basic Silver) are both HMOs, covering the same benefits with the same provider network and cost-sharing structure, making the reason for this 25% price differential unclear. That said, price-sensitive consumers would be unlikely to consider the more expensive SPD based on affordability, alone.

Appendix Table B

For information on other HealthCare.gov and state-based marketplace standardized plan rules, see HealthCare.gov; DC Health Benefit Exchange, Covered California, NY State of Health, Colorado Option, Access Health CT, ME Clear Choice, VT Health Connect, WA Health Benefit Exchange, MA Health Connector, GetCoveredNJ

- Previously, CMS had given HealthCare.gov issuers the option to offer SPDs beginning with the 2017 coverage year. The Trump Administration ended this option, but a federal court ruled that it should be restored. ↩︎

- The requirement to offer SPDs also does not apply to SHOP plans sold to small employers. ↩︎

- See for example, Rose Chu et.al., “Facilitating Consumer Choice: Standardized Plans in Health Insurance Marketplaces, ASPE Office of Health Policy Issue Brief, December 28, 2021. ↩︎

- Nearly half (48%) of all consumers who selected a HealthCare.gov plan during the 2023 open enrollment period receive cost sharing reductions. See https://modern.kff.org/health-reform/state-indicator/marketplace-plan-selections-by-financial-assistance-status-2/?currentTimeframe=0&sortModel=%7B%22colId%22:%22Location%22,%22sort%22:%22asc%22%7D ↩︎

- Note, these cost sharing values apply for QHPs offered in all states using HealthCare.gov except Delaware, Louisiana, and Oregon where, pursuant to state law, somewhat modified SPD cost sharing designs apply. ↩︎

- Although insurers have flexibility in the tiers they assign particular drugs, plans are not supposed to engage in “adverse tiering” by placing all or most drugs to treat a medical condition on a high-cost tier in order to discourage enrollment by individuals with that condition. ↩︎

- For expanded bronze plans, the de minimis range around the target AV of 60% is +5/-2 percentage points. For standard silver (non-CSR) plans, the de minimis range around the target AV of 70% is +2/0 percentage points. For gold and platinum plans, the de minimis range around the target AV of 80% and 90%, respectively, is +2/-2 percentage points. ↩︎

- Source: HealthCare.gov 2023 Plan Attribute File, available at https://www.cms.gov/cciio/resources/data-resources/marketplace-puf ↩︎

- This estimate does not take into account added flexibility that insurers will be allowed to offer separate SPDs – and so additional non-standardized plan options – for plan options that are otherwise identical except for the inclusion of adult dental or vision benefits. In the regulation, CMS provides an example of an insurer that might offer a gold HMO SPD with no added dental or vision benefits, another with added adult dental benefits, a third with adult vision benefits, and a fourth with added adult vision and dental benefits. This insurer would be allowed to offer up to 4 non-standardized gold HMO plans for each of these benefit packages, for a total of 20 plan offerings. CMS did not provide estimates for the number of plan choices HealthCare.gov consumers might face in 2025. ↩︎

- See HealthCare.gov, plan offerings in Cook County Illinois (zip 60614). The full-priced premium for the Blue Precision Silver HMO 706 (easy pricing) plan is $541.29, compared to its non-standardized counterparts, the Blue Precision Silver HMO 206 plan ($452.63), and the Blue Precision Silver HMO 704 plan ($494.32).. ↩︎

- In California, insurers may apply to offer non-standardized plan designs, though none currently do. In New Jersey, insurers may offer non-standardized plans at the catastrophic level only. ↩︎

- In DC, insurers retain some flexibility in their formulary design so that certain brands of insulin, for example, may still be subject to cost sharing. ↩︎