KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

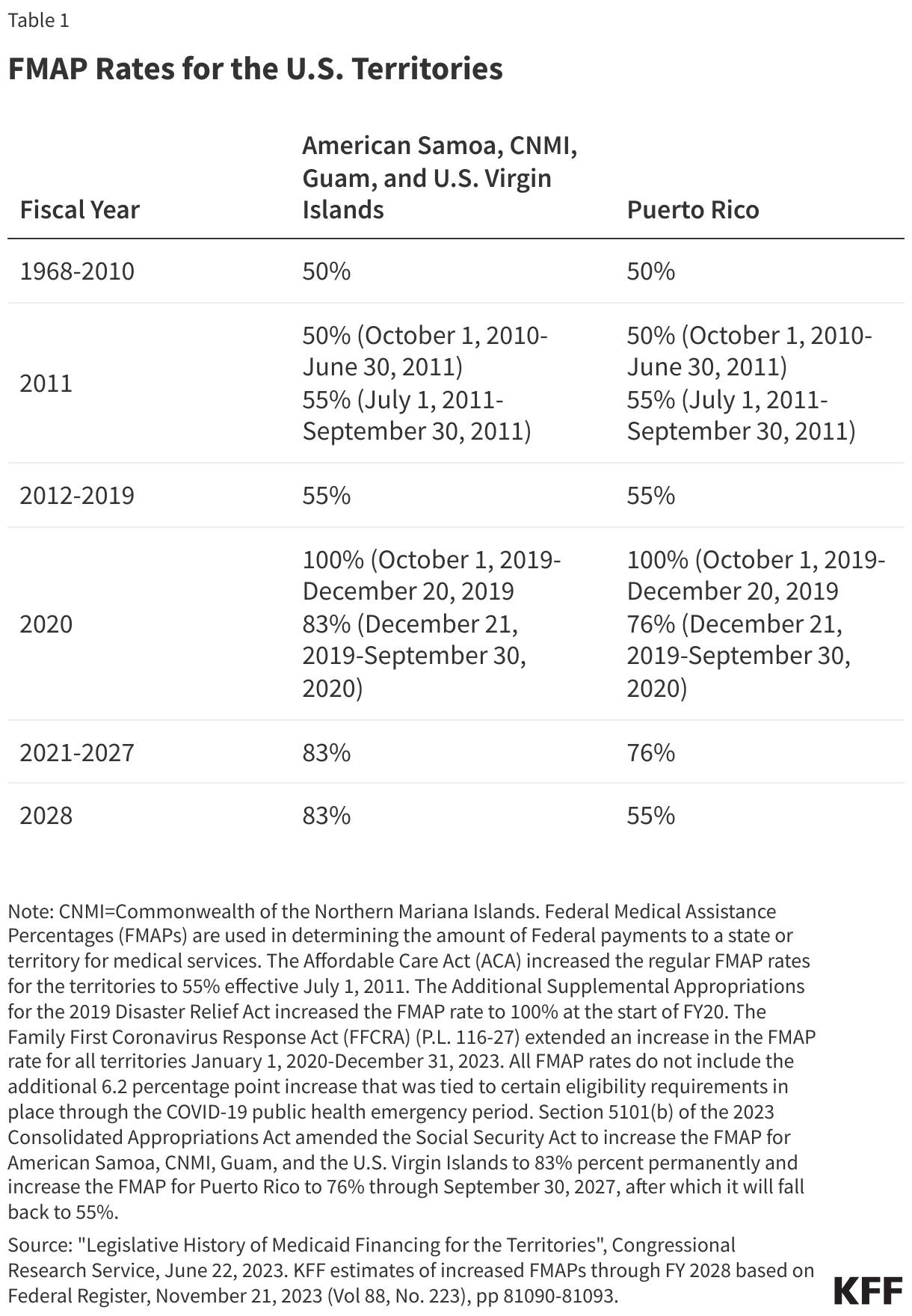

The U.S territories – American Samoa, the Commonwealth of the Northern Mariana Islands (CNMI), Guam, Puerto Rico, and the U.S. Virgin Islands (USVI) – have faced an array of longstanding fiscal and health challenges that were exacerbated by somewhat recent natural disasters and the COVID-19 pandemic. Over 1.7 million people residing in the territories were enrolled in Medicaid in fiscal year (FY) 2023. Medicaid financing in the territories differs from the states due to a statutorily set Federal Medical Assistance Percentage (FMAP) and an annual ceiling in federal funding that has historically resulted in lower levels of funding and often health care coverage and access.

Over time, Congress has provided temporary supplemental federal funding and increases to the FMAP rate in response to emergencies beyond the Medicaid allotments set in statute. Most recently, the Families First Coronavirus Response Act (FFCRA) significantly increased allotments for the territories and the 2023 Consolidated Appropriations Act (CAA) included a permanent statutory increase to 83% (from 55%) for most of the territories’ Medicaid allotments and FMAP rates, except Puerto Rico. In Puerto Rico, the allotments are set in statute through FY 2027, and the FMAP was increased to 76% and set to expire after FY 2027 and return to 55% without legislative action.

While neither candidate has announced detailed policy proposals in the campaign, the outcome of the 2024 election could have implications for the American territories. In a recently released policy fact sheet, Vice President Harris highlights several initiatives to support Puerto Rico, including calling for Congress “to pursue parity and equal access to key federal programs that support health care, nutrition, and other critical needs for low-income families, seniors, and people with disabilities.” In addition, the Biden-Harris administration proposed eliminating Medicaid funding caps for the American territories and bringing FMAP rates in parity with the states in their FY 2025 budget. In contrast, former President Trump previously proposed reducing Medicaid funding for Puerto Rico and has supported proposals to cap and reduce Medicaid financing and the FMAP, which could impact the territories as well. This issue brief provides background on how Medicaid financing differs between U.S. territories and states and the implications of these differences.

How does Medicaid in the territories differ from the states?

Unlike in the 50 states and D.C., annual federal funding for Medicaid in the U.S. territories is subject to a statutory cap and fixed matching rate. Both the capped federal allotment (known as the Section 1108(g) allotment) and the territories’ FMAP are fixed in statute. Annual federal Medicaid funding is set in statute for Puerto Rico for FY 2023 through FY 2027 and increases in the allotments are tied to the medical care component of the Consumer Price Index for All Urban Consumers (CPI-U) for the rest of the territories. This funding arrangement is unlike federal Medicaid funding for states, where federal dollars are uncapped and the FMAP is adjusted annually based on a state’s relative per capita income. In addition, the territories receive Section 1935(e) funding, also known as the Enhanced Allotment Program (EAP), which can be used to provide prescription drug coverage under Medicaid for low-income Medicare beneficiaries who would otherwise be eligible for subsidies under Medicare Part D. Most territories receive funding for Medicaid data systems, and Puerto Rico receives additional funds for physician payment rates and for program integrity through FY 2027.

Medicaid programs in the territories have programmatic differences in coverage and benefits compared to the states. Unlike the states, the territories develop their own measures rather than use federal poverty levels (FPL) to determine eligibility for Medicaid for the population. CNMI and American Samoa operate Medicaid programs under waivers so they are not subject to most program requirements, including flexibility that allows them to waive coverage of any benefits that are mandatory in the states when needed.

What are recent Medicaid financing changes for the Territories?

The 2023 CAA included a permanent statutory increase in territories’ Medicaid FMAP rate, except in Puerto Rico, where the increase will expire at the end of FY 2027. Congress has previously authorized both permanent and supplemental increases in the FMAP rate for the territories broadly and in response to specific emergency events (Table 1). Following the passage of the Affordable Care Act (ACA), the FMAP rate for territories was increased from 50% to 55% in 2011, and at the beginning of FY 2020, during the COVID-19 pandemic, the FMAP was temporarily increased to 100%. For the remainder of FY 2020 through the beginning of FY 2023, Congress increased FMAP rates from 55% to 83% for American Samoa, CNMI, Guam, and USVI and from 55% to 76% for Puerto Rico (with an additional increase of 6.2% if certain maintenance of eligibility requirements were met). With the 2023 CAA, Congress made the temporary FMAP increase to 83% permanent for American Samoa, CNMI, Guam, and the USVI, while authorizing a temporary increase to Puerto Rico’s FMAP to 76% through FY 2027. The law also provides 100% federal funding for qualifying data system improvements for American Samoa, CNMI, Guam, and USVI, up to $20 million for all four of the territories.

In addition to the change in the FMAP rates, annual federal capped funding for the territories increased substantially in FY 2020. The FFCRA increased allotments for each of the territories for FY 2020 and FY 2021 and then CMS used these levels as the new base for FY 2022 and beyond, except for Puerto Rico, where capped amounts are set in statute through FY 2027. The annual capped funding for Puerto Rico will be $3.475 billion for FY 2025, $3.645 billion for FY 2026, and $3.825 billion for FY 2027. After FY 2027, the allotments for Puerto Rico will be calculated from the much lower FY 2019 base without a legislative change.

What are the implications of the Medicaid financing structure in the territories?

The capped federal Medicaid funding structure in the territories contributes to cost shifts to the territories and/or coverage restrictions. Once a territory exhausts its capped federal funds, the territory must use local funds to cover costs of coverage or may suspend or limit services. Historically, all of the territories have reported depleting the capped federal funds before the fourth quarter of the year. Medicaid programs in American Samoa and CNMI have recently suspended or limited a wide range of services for parts of the fiscal year due to funding constraints, despite the recent increases in allotments and FMAP rates.

In the absence of additional statutory changes, annual federal allotments for Medicaid in Puerto Rico will drop and the FMAP rate will drop to 55% in FY 2028. Under the 2023 CAA, Puerto Rico’s annual federal allotment will drop in FY 2028 because it will be re-calculated based on the annual FY 2019 cap adjusted to the medical component of the CPI-U without regard for the additional funding received between FY 2020 and FY 2027, and the FMAP will return to 55% in FY 2028. Both of these changes would result in significant reductions in federal Medicaid funding for Puerto Rico. Beyond adjustments for Puerto Rico, proposals like the Territories Health Equity Act would treat the territories like states for Medicaid funding and eliminate federal funding caps if enacted by Congress.

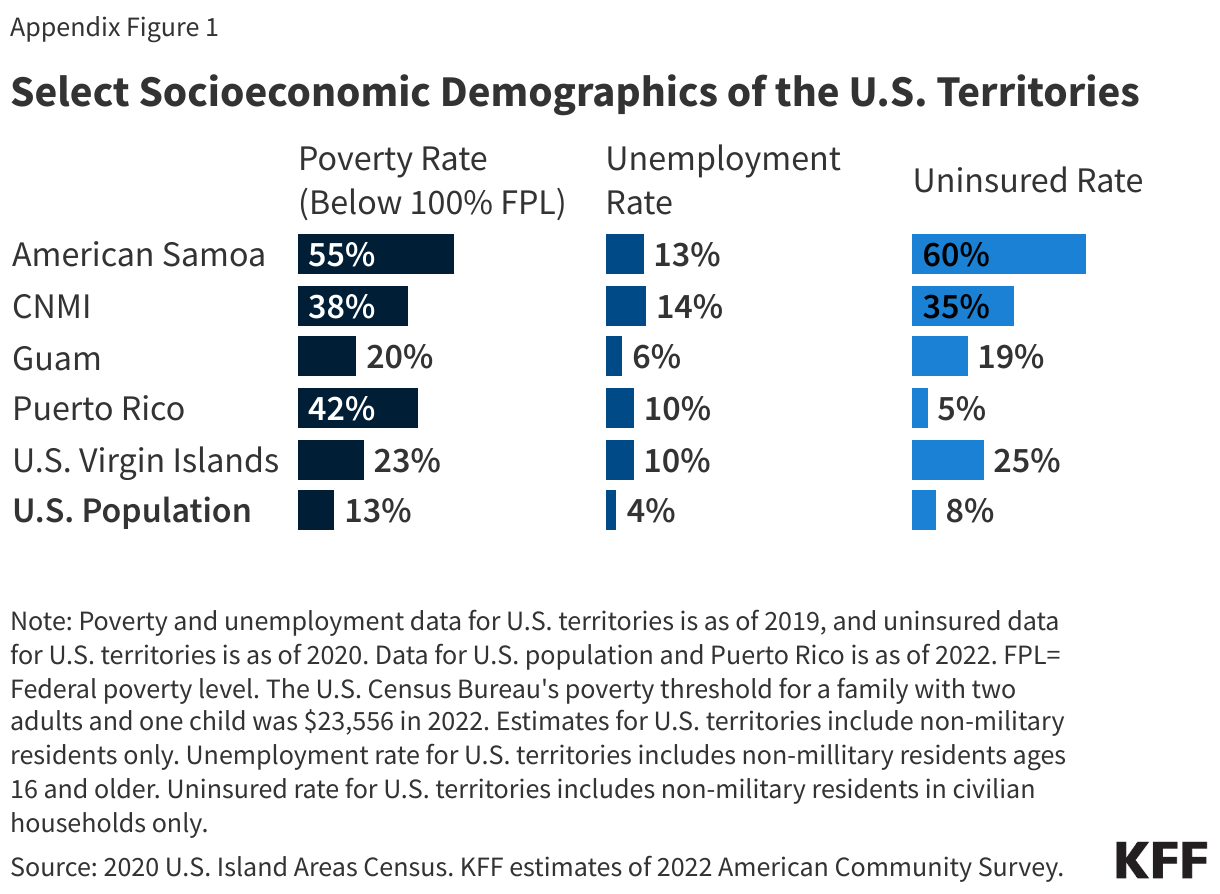

Limits on federal Medicaid funding contribute to increasing challenges for the territories in addressing health care needs of their residents given growing poverty, infrastructure, and environmental challenges. Studies have found that the territories rank worse than the states on health care quality measures and health outcomes. The territories also have higher rates of poverty and unemployment, and all the territories, with the exception of Puerto Rico, also have higher rates of uninsured people than the U.S. population overall (Appendix Figure 1). Limitations in federal data on the American territories, including gaps in federal statistics and Medicaid claims reporting, and limited local public health workforce capacity may reduce government capabilities to understand and address these challenges. The territories have also become increasingly susceptible to natural disasters and environmental hazards due to climate change as well as U.S. colonial and military activity, which can exacerbate population loss due to outmigration and further negatively impact island economies. Recent disaster events in Puerto Rico have also shown how they negatively impact health outcomes and the mental health of residents in the long-term.

NOTE: This brief was updated on November 4, 2024 to incorporate additional information about the role of midwives in maternal and infant care.

Summary

Stark racial disparities in maternal and infant health in the U.S. have persisted for decades despite continued advancements in medical care. The disparate impact of the COVID-19 pandemic for people of color increased attention to health disparities, including the longstanding inequities in maternal and infant health. Additionally, the overturning of Roe v. Wade, increased barriers to abortion and may widen the existing disparities in maternal health. Given these factors, there recently has been increased attention to improving maternal and infant health and reducing disparities in these areas.

This brief provides an overview of racial disparities for selected measures of maternal and infant health, discusses the factors that drive these disparities, and provides an overview of recent efforts to address them. It is based on KFF analysis of publicly available data from CDC WONDER online database, the National Center for Health Statistics (NCHS) National Vital Statistics Reports, and the CDC Pregnancy Mortality Surveillance System. While this brief focuses on racial and ethnic disparities in maternal and infant health, wide disparities also exist across other dimensions, including income, education, age, and other characteristics. For example, there is significant variation in some of these measures across states and disparities between rural and urban communities. Data and research often assume cisgender identities and may not systematically account for people who are transgender and non-binary. In some cases, the data cited in this brief use cisgender labels to align with how measures have been defined in underlying data sources. Key takeaways include:

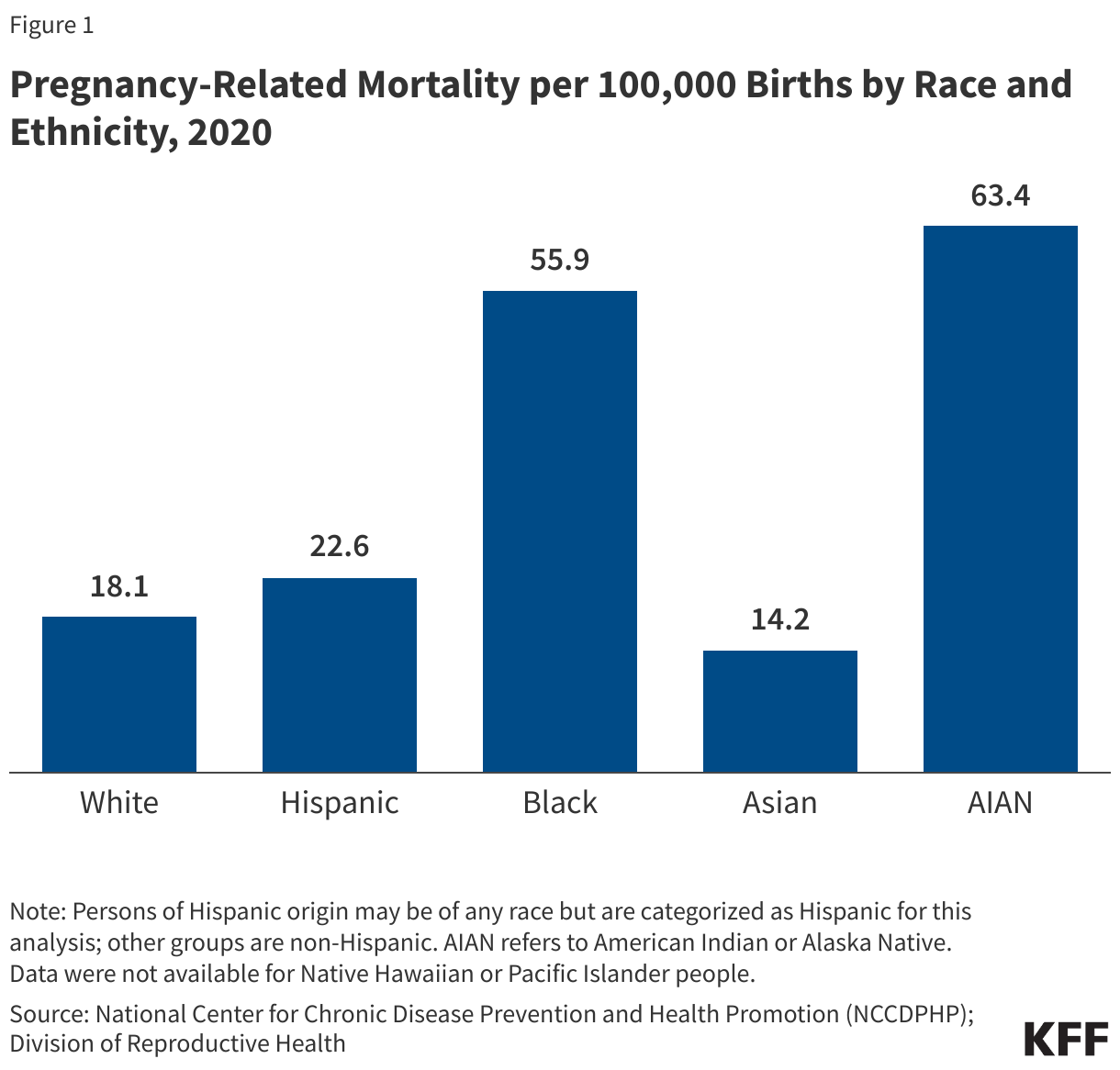

Large racial disparities in maternal and infant health outcomes persist. Pregnancy-related mortality rates among American Indian and Alaska Native (AIAN) and Black women are over three times higher than the rate for White women (63.4 and 55.9 vs. 18.1 per 100,000). Black, AIAN, and Native Hawaiian or Pacific Islander (NHPI) women also have higher shares of preterm births, low birthweight births, or births for which they received late or no prenatal care compared to White women. Infants born to Black, AIAN, and NHPI people have markedly higher mortality rates than those born to White people.

Maternal and infant health disparities reflect broader underlying social and economic inequities that are rooted in racism and discrimination. Differences in health insurance coverage and access to care play a role in driving worse maternal and infant health outcomes for people of color. However, inequities in broader social and economic factors, including income, are primary drivers for maternal and infant health disparities. Moreover, disparities in maternal and infant health persist even when controlling for certain underlying social and economic factors, such as education and income, pointing to the roles racism and discrimination play in driving disparities.

Increased attention to maternal and infant health has contributed to a rise in efforts and resources focused on improving health outcomes and reducing disparities in these areas. These include efforts to expand access to coverage and care, increase access to a broader array of services and providers that support maternal and infant health, diversify the health care workforce, and enhance data collection and reporting. However, addressing social and economic factors that contribute to poorer health outcomes and disparities will also be important. Moreover, the persistence of disparities in maternal health across income and education levels, points to the importance of addressing the roles of racism and discrimination as part of efforts to improve health and advance equity.

Moving forward, legislative and policy efforts and the outcome of the 2024 presidential election could all have important implications for efforts to address racial disparities in maternal and infant health. For example, state variation in access to abortion in the wake of the overturning of Roe v. Wade may exacerbate existing racial disparities in maternal health. Further, differences in records and proposed approaches by Vice President Harris and former President Trump on abortion, reproductive health, and maternal health will likely have different implications for disparities in maternal health going forward.

Racial Disparities in Maternal and Infant Health

Pregnancy-Related Mortality Rates

In 2020, approximately 900 women died in the U.S. from causes related to or worsened by pregnancy. Pregnancy-related deaths are deaths that occur within one year of pregnancy. Approximately one quarter (26%) occur during pregnancy, another quarter (27%) occur during labor or within the first week postpartum, and nearly half (47%) occur one week to one year postpartum, underscoring the importance of access to health care beyond the period of pregnancy. Recent data shows that more than eight out of ten (84%) pregnancy-related deaths are preventable. Although leading causes of pregnancy-related death vary by race and ethnicity, infection (including COVID-19) and cardiovascular conditions are the leading causes of pregnancy-related death among women overall, illustrating the importance of care for chronic conditions on pregnancy-related outcomes. Additional data from detailed maternal mortality reviews in 38 states found mental health conditions to be the overall leading cause of pregnancy-related deaths.

AIAN and Black people are more than three times as likely as White people to experience a pregnancy-related death (63.4 and 55.9 vs. 18.1 per 100,000 live births) in 2020 (Figure 1). Hispanic people also have a higher rate of pregnancy-related deaths compared to White people (22.6 vs. 18.1 per 100,000). The rate for Asian people is lower compared to that of White people (14.2 vs. 18.1 per 100,000). Data from one year were insufficient to identify mortality among NHPI women. However, earlier data showed that NHPI (62.8 per 100,000) people had the highest rates of pregnancy-related mortality across racial and ethnic groups.

Research shows that these disparities increase by age and persist across education and income levels. Data show higher pregnancy-related mortality rates among Black women who completed college education than among White women with the same educational attainment and White women with less than a high school diploma. Similarly, studies find that high income Black women have the same risk of dying in the first year following childbirth as the poorest White women. Other research also shows that Black women are at significantly higher risk for severe maternal morbidity, such as preeclampsia, which is significantly more common than maternal death. Further, AIAN, Black, NHPI, Asian, and Hispanic women have higher rates of admission to the intensive care unit during delivery compared to White women, which is considered a marker for severe maternal morbidity.

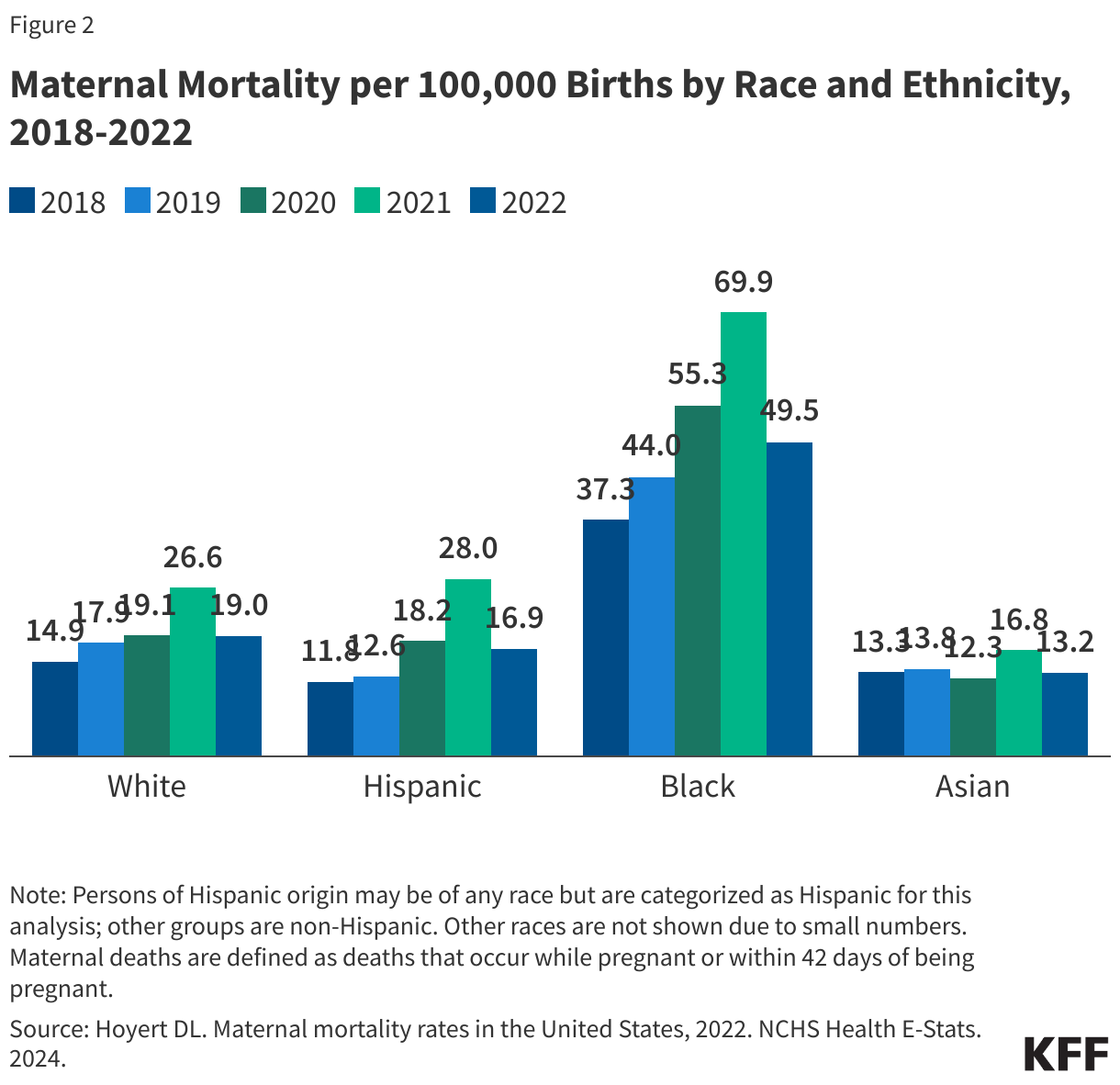

Maternal death rates declined across most racial and ethnic groups between 2021 and 2022 following the large increase in maternal deaths rates due to COVID-19. Maternal mortality and pregnancy-related mortality are similar concepts but maternal mortality is a narrower measure, limited to deaths that occur while pregnant or within 42 days or pregnancy and excluding those due to accidents or acts of violence. However, more recent maternal mortality data are available allowing for examination of trends since COVID-19. Black women had the highest maternal mortality rate across racial and ethnic groups between 2018 and 2022 and also experienced the largest increase during the pandemic (Figure 2). Maternal mortality rates decreased significantly across most racial and ethnic groups between 2021 and 2022. This decline may reflect a return to pre-pandemic levels following the large increase in maternal death rates due to COVID-19 related deaths. Despite this decline, the U.S. has the highest maternal mortality rate among high-income countries and the maternal mortality rate for Black women remained over two and a half times as high as the rate for White women.

Birth Risks and Outcomes

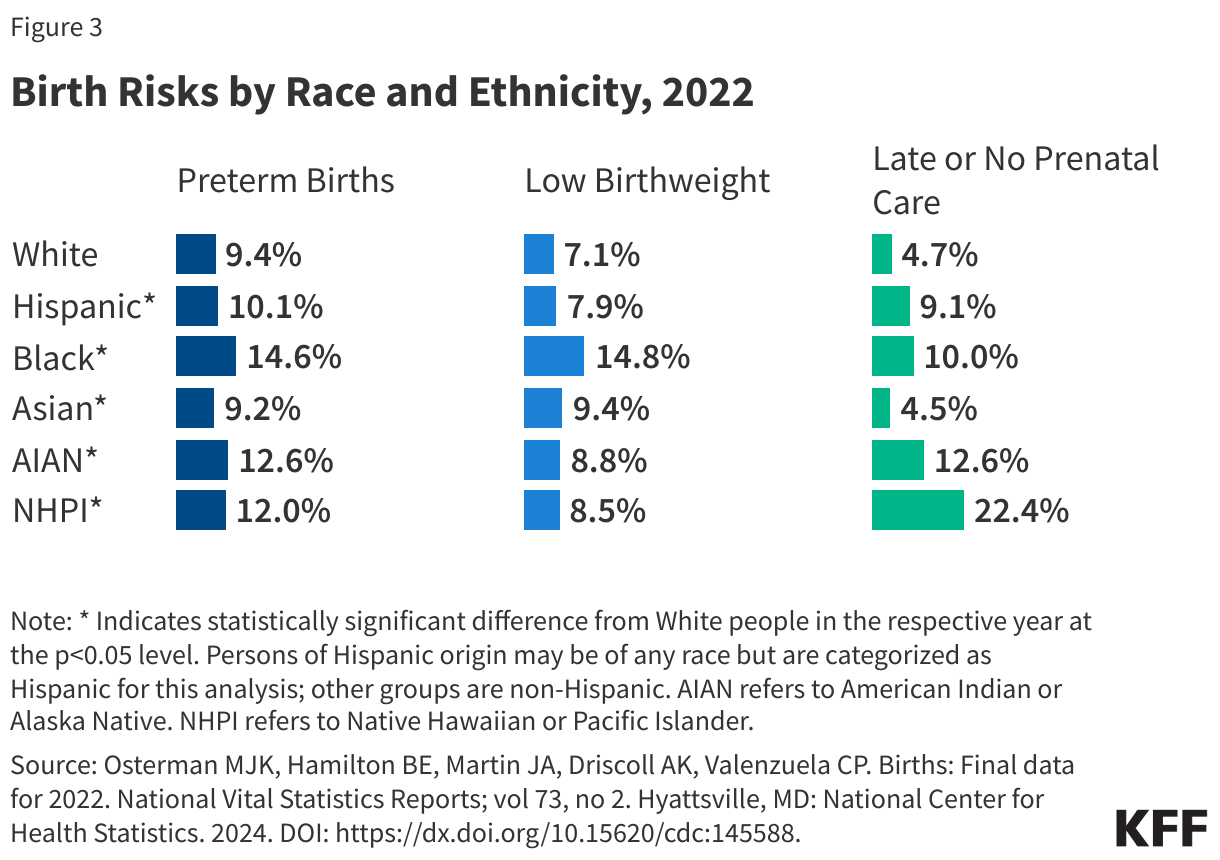

Black, AIAN, and NHPI women are more likely than White women to have certain birth risk factors that contribute to infant mortality and can have long-term consequences for the physical and cognitive health of children. Preterm birth (birth before 37 weeks gestation) and low birthweight (defined as a baby born less than 5.5 pounds) are some of the leading causes for infant mortality. Receiving pregnancy-related care late in a pregnancy (defined as starting in the third trimester) or not receiving any pregnancy-related care at all can also increase the risk of pregnancy complications. Black, AIAN, and NHPI women have higher shares of preterm births, low birthweight births, or births for which they received late or no prenatal care compared to White women (Figure 3). Notably, NHPI women are four times more likely than White women to begin receiving prenatal care in the third trimester or to receive no prenatal care at all (22% vs. 5%). Black women also are nearly twice as likely compared to White women to have a birth with late or no prenatal care compared to White women (10% vs. 5%).

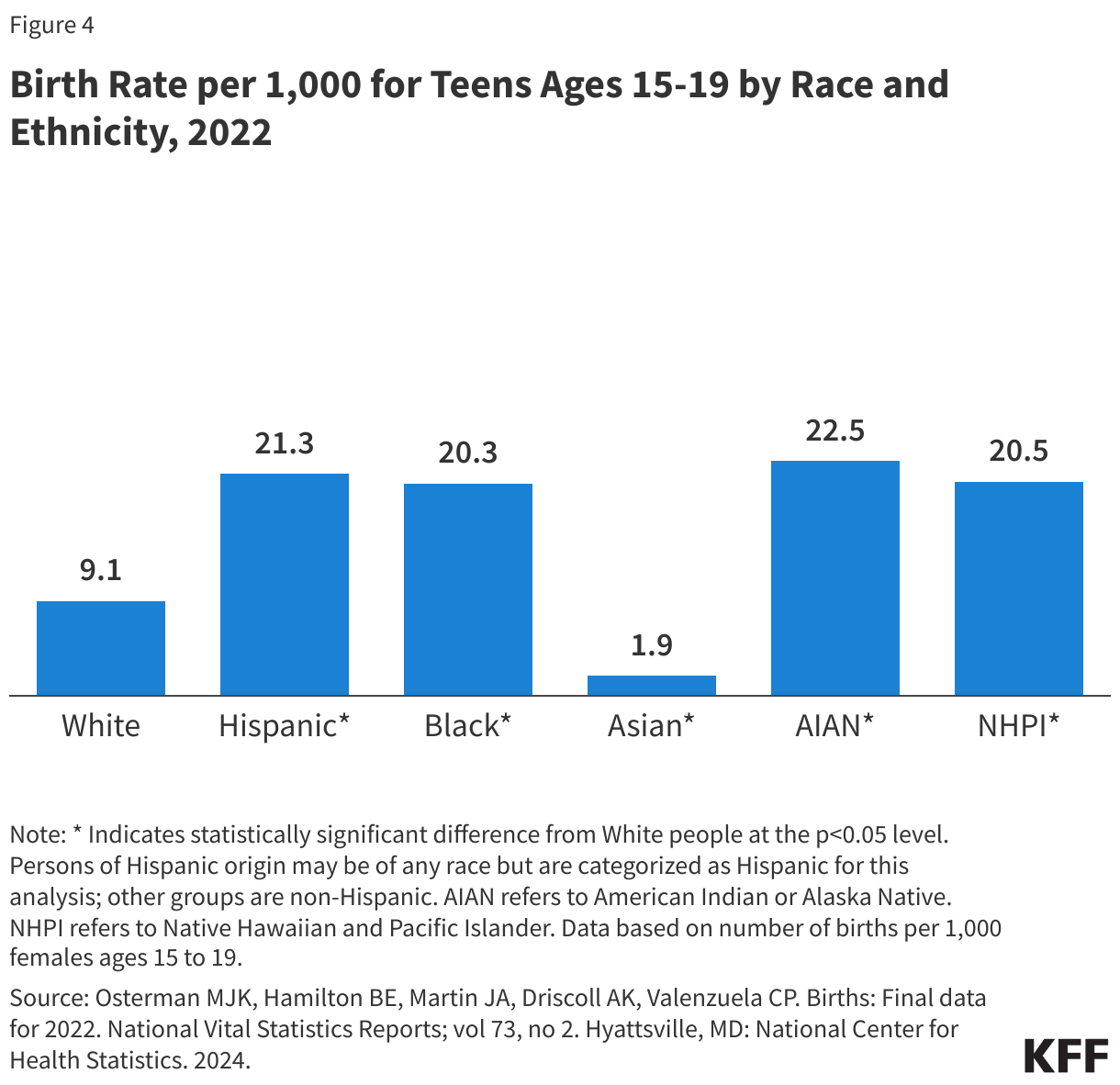

While teen birth rates overall have declined over time, they are higher among Black, Hispanic, AIAN, and NHPI teens compared to their White counterparts (Figure 4). In contrast, the birth rate among Asian teens is lower than the rate for White teens. Many teen pregnancies are unplanned, and pregnant teens may be less likely to receive early and regular prenatal care. Teen pregnancy also is associated with increased risk of complications during pregnancy and delivery, including preterm birth. Teen pregnancy and childbirth can also have social and economic impacts on teen parents and their children, including disrupting educational completion for the parents and lower school achievement for the children. The drivers of teen pregnancy are multi-faceted and include poverty, history of adverse childhood events, and access to comprehensive education and health care services. Research studies have found that increased use of contraception as well as support for comprehensive sex education have helped lower the rate of teen births nationally.

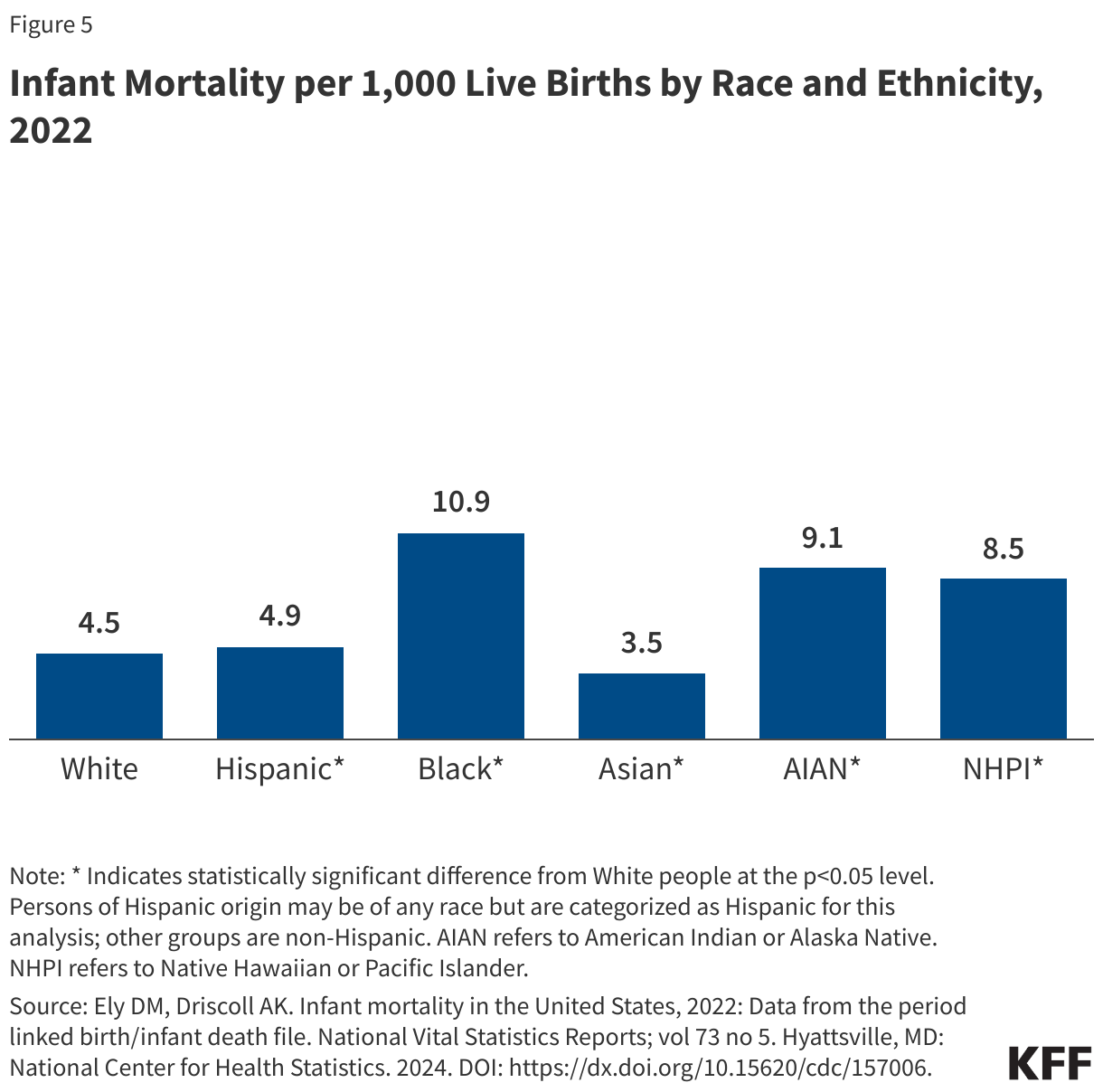

Reflecting these increased risk factors, infants born to AIAN, Hispanic, Black, and NHPI women are at higher risk for mortality compared to those born to White women. Infant mortality is defined as the death of an infant within the first year of life, but most cases occur within the first month after birth. The primary causes of infant mortality are birth defects, preterm birth and low birthweight, sudden infant death syndrome, injuries, and maternal pregnancy complications. Infant mortality rates have declined over time although there was a slight increase between 2021 and 2022 (5.4 vs. 5.6 per 1,000 births, respectively). However, disparities in infant mortality have persisted and sometimes widened for over a century, particularly between Black and White infants. As of 2022, infants born to Black women are over twice as likely to die relative to those born to White women (10.9 vs. 4.5 per 1,000), and the mortality rate for infants born to AIAN and NHPI women (9.1 and 8.5 per 1,000) is nearly twice as high (Figure 5). The mortality rate for infants born to Hispanic mothers is similar to the rate for those born to White women (4.9 vs. 4.5 per 1,000), while infants born to Asian women have a lower mortality rate (3.5 per 1,000). Data also show that fetal death or stillbirths—that is, pregnancy loss after 20-week gestation—are more common among NHPI, Black and AIAN women compared to White and Hispanic women. Moreover, causes of stillbirth vary by race and ethnicity, with higher rates of stillbirth attributed to diabetes and maternal complications among Black women compared to White women.

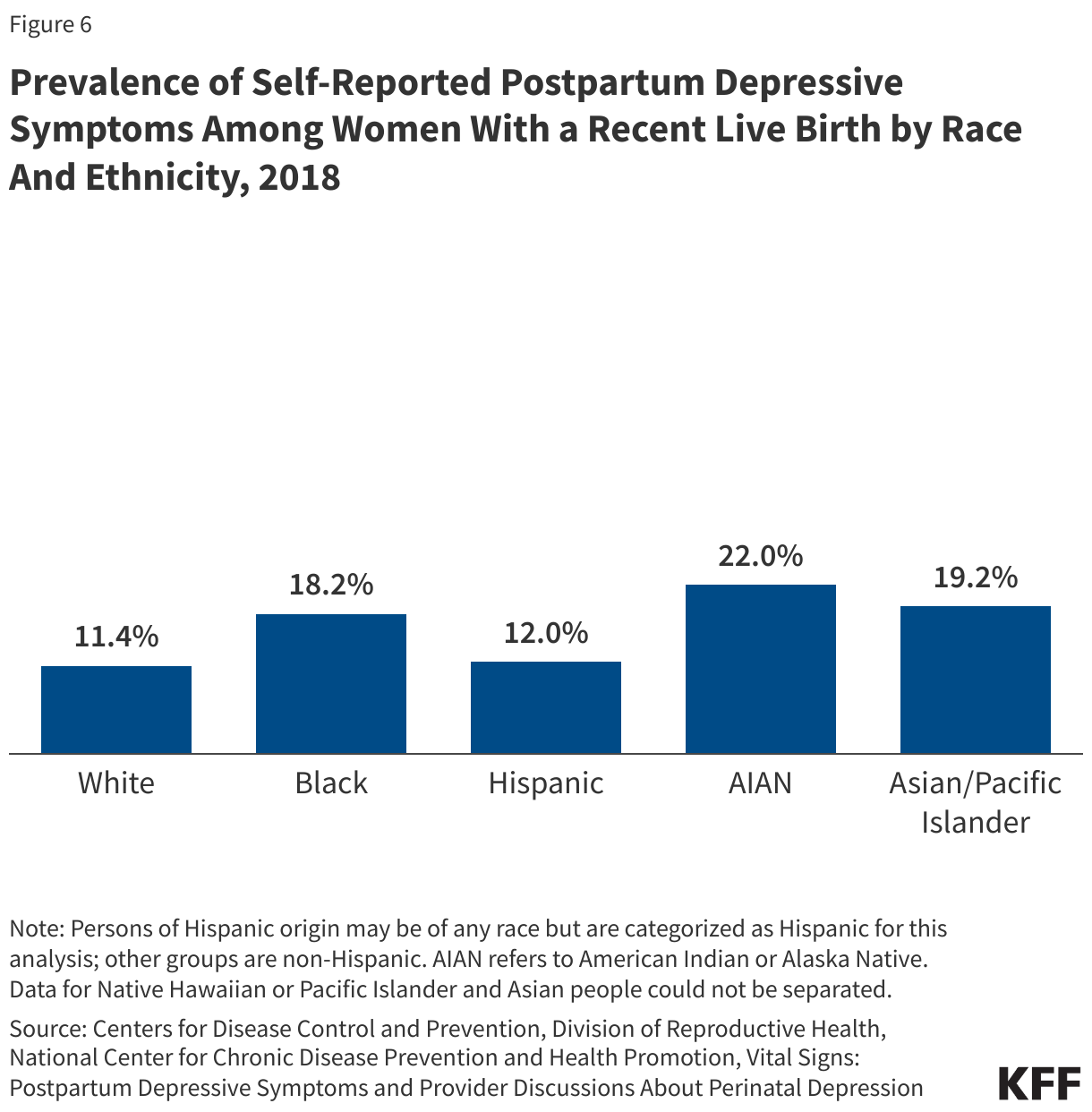

About one in five AIAN, Asian or Pacific Islander, and Black women report symptoms of perinatal depression compared to about one in ten White women (Figure 6). Hispanic women (12%) have similar rates of perinatal depression compared to their White counterparts (11%). Other research shows that the prevalence of postpartum depression has grown dramatically over the course of the past decade increasing from 9.4% in 2010 to 19.3% in 2021, driven by increases among Black and Asian and Pacific Islander women. Women of color experience increased barriers to mental health care and resources, along with racism, trauma and cultural barriers. Research suggests that perinatal mental health conditions are a leading underlying cause of pregnancy-related deaths and that individuals with perinatal depression are also at increased risk of chronic health complications such as hypertension and diabetes. Infants of mothers with depression are more likely to be hospitalized and die within the first year of life.

Factors Driving Disparities in Maternal and Infant Health

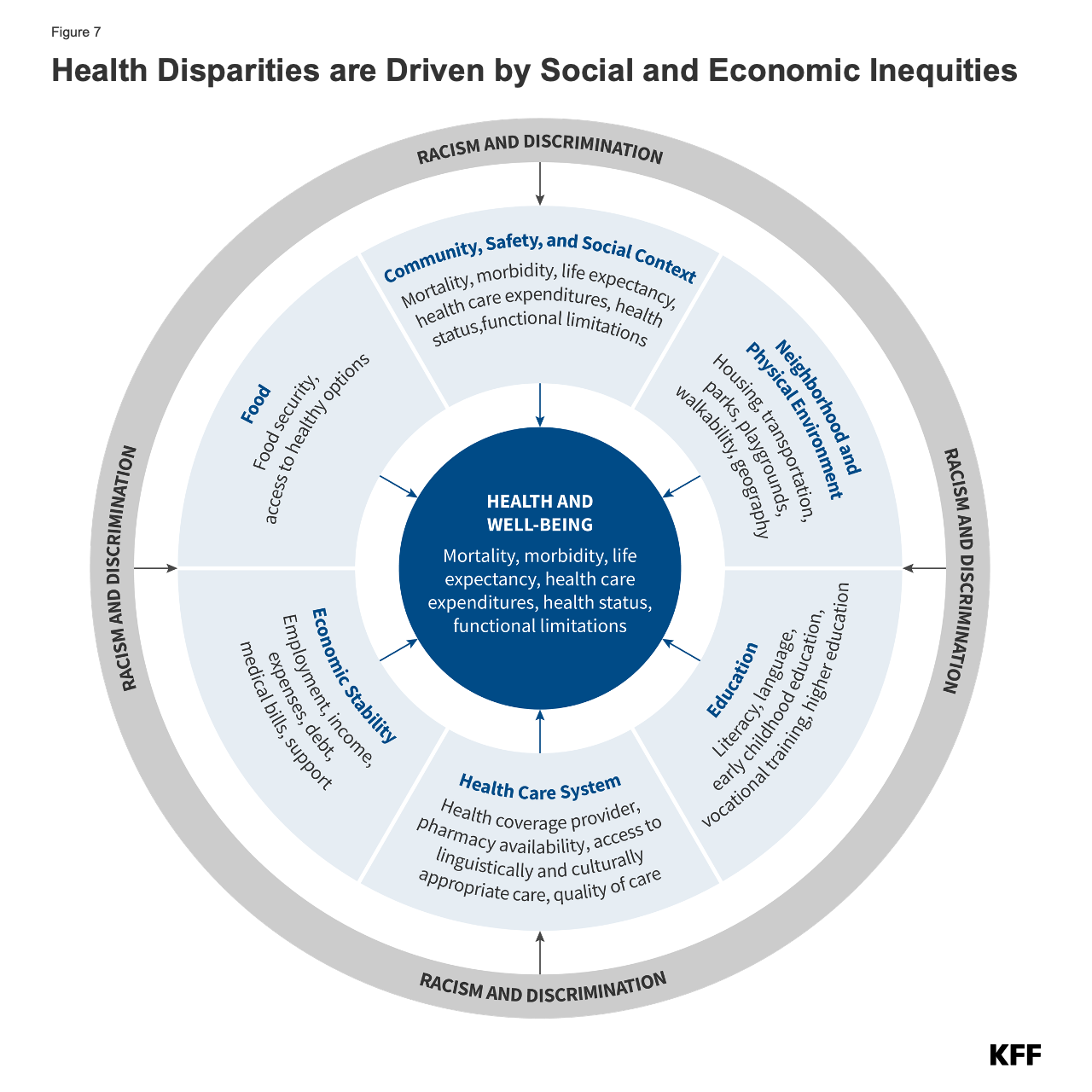

The factors driving disparities in maternal and infant health are complex and multifactorial. They include differences in health insurance coverage and access to care. However, broader social and economic factors and structural and systemic racism and discrimination also play a major role (Figure 7). In maternal and infant health specifically, the intersection of race, gender, poverty, and other social factors shapes individuals’ experiences and outcomes. Recently there has been broader recognition of the principles of reproductive justice, which emphasize the role that the social determinants of health and other factors play in reproductive health for communities of color. Notably, Hispanic women and infants fare similarly to their White counterparts on many measures of maternal and infant health despite experiencing increased access barriers and social and economic challenges typically associated with poorer health outcomes. Research suggests that this finding, sometimes referred to as the Hispanic or Latino health paradox, in part, stems from variation in outcomes among subgroups of Hispanic people by origin, nativity, and race, with better outcomes for some groups, particularly recent immigrants to the U.S. However, the findings still are not fully understood.

Disparities in maternal and infant health, in part, reflect increased barriers to care for people of color. Research shows that coverage before, during, and after pregnancy facilitates access to care that supports healthy pregnancies, as well as positive maternal and infant outcomes after childbirth. Overall, people of color are more likely to be uninsured and face other barriers to care. Medicaid helps to fill these coverage gaps during pregnancy and for children, covering more than two-thirds of births to women who are Black or AIAN. However, AIAN, Hispanic, and Black people are at increased risk of being uninsured prior to their pregnancy, which can affect access to care before pregnancy and timely entry to prenatal care. Beyond health coverage, people of color face other increased barriers to care, including limited access to providers and hospitals and lack of access to culturally and linguistically appropriate care. Several areas of the country, particularly in the South have gaps in obstetrics providers. AIAN women also are more likely to live in communities with lower access to obstetric care. These challenges may be particularly pronounced in rural and medically underserved areas. For example, research suggests that closures of hospitals and obstetric units in rural areas has a disproportionate negative impact on Black infant health.

Research also highlights the role racism and discrimination play in driving racial disparities in maternal and infant health. Research has documented that social and economic factors, racism, and chronic stress contribute to poor maternal and infant health outcomes, including higher rates of perinatal depression and preterm birth among Black women and higher rates of mortality among Black infants. In recent years, research and news reports have raised attention to the effects of provider discrimination during pregnancy and delivery. News reporting and maternal mortality case reviews have called attention to a number of maternal and infant deaths and near misses among women of color where providers did not or were slow to listen to patients. A recent report determined that discrimination, defined as treating someone differently based on the class, group, or category they belong to due to biases, stereotypes, and prejudices, contributed to 30% of pregnancy-related deaths in 2020. In one study, Black and Hispanic women reported the highest rates of mistreatment (such as shouting and scolding, ignoring or refusing requests for help during the course of their pregnancy). Even controlling for insurance status, income, age, and severity of conditions, people of color are less likely to receive routine medical procedures and experience a lower quality of care. A 2023 KFF survey found that about one in five (21%) Black women say they have been treated unfairly by a health care provider or staff because of their racial or ethnic background. A similar share (22%) of Black women who have been pregnant or gave birth in the past ten years say they were refused pain medication they thought they needed.

Efforts to Address Maternal and Infant Health Disparities

Increased awareness and attention to maternal and infant health have contributed to a rise in efforts and resources focused on improving health outcomes and reducing disparities. These include efforts to expand access to coverage and care, increase access to a broader array of services and providers that support maternal and infant health, diversify the health care workforce, and enhance data collection and reporting.

Since the launch of the White House Blueprint for Addressing the Maternal Health Crisis in 2022, there has been a variety of actions and investments across federal agencies to improve maternal health. The Biden-Harris Administration’s Blueprint focuses on increasing coverage for perinatal services, improving data collection and analysis, expanding the maternity workforce, strengthening social supports, and improving patient-provider relations. Federal initiatives have included a pilot project with distribution of newborn supply kits, a $27.5 million program for specialized maternity care training to over 2,000 OB/GYNs, nurses, and other providers. In March 2024, the Biden Administration issued a new Executive Order to advance women’s health research and innovation, including support to fund research to identify warning signs of maternal morbidity and mortality among Special Supplemental Nutrition Program for Women, Infants, and Children (WIC) recipients. The Office of Intergovernmental and External Affairs (IEA) and the March of Dimes have created a public-private partnership, Maternal Health Collaborative to Advance Racial Equity, to improve maternal health outcomes among Black mothers. Additionally, the Biden-Harris Administration recently launched the Expanding Access to Women’s Health grant program, which will provide funding to 14 states and the District of Columbia to address disparities in maternal health outcomes with an emphasis on improving access to reproductive and maternal health coverage and services.

Nearly all states have expanded access to Medicaid coverage during the postpartum period, helping to stabilize coverage. Medicaid covers four in ten births nationally. However, historically, many pregnant women lost coverage at the end of a 60-day postpartum coverage period because eligibility levels are lower for parents than pregnant women in many states, particularly those that have not implemented the ACA Medicaid expansion. The American Rescue Plan Act (ARPA) of 2021 initially provided states a new option to extend postpartum coverage to a full year beginning April 1, 2022. As of August 1, 2024, 47 states, including DC, had implemented a 12-month postpartum coverage extension, with additional states planning to implement the extension. KFF analysis suggests that the coverage extension could prevent hundreds of thousands of enrollees from losing coverage in the months after delivery. Additional actions to expand coverage may also help to reduce disparities, including adoption of the ACA Medicaid expansion in the ten remaining states that have not yet expanded, as nearly six in ten adults in the coverage gap in these states are adults of color, and Medicaid expansion promotes continuity of coverage in the prenatal and postpartum periods.

In addition, many state Medicaid programs have implemented policies, programs, and initiatives to improve maternity care and outcomes. This includes outreach and education to enrollees and providers about maternal health issues; expanding coverage for benefits such as doula care, home visits, and substance use disorder and mental health treatment; and using new payment, delivery, and performance measurement approaches. For example, Ohio’s Comprehensive Maternal Care program aims to develop community connections and culturally aligned supports for women with Medicaid as they and their families navigate pre- and post-natal care. Participating obstetrical practices are required to measure and engage with patients and families to hear firsthand accounts of how access to care, cultural competence, and communication methods affect patient outcomes. Some states also are leveraging managed care contracts to require Medicaid plans to develop an explicit focus on reducing disparities related to maternal and child health .

Implementation of evidence-based best practices may help to improve maternal and infant health outcomes. As part of its maternity care action plan, CMS has launched a “Birthing-Friendly” hospital designation to provide public information on hospitals that have implemented best practices in areas of health care quality, safety, and equity for pregnant and postpartum patients. Currently, more than 2,200 hospitals nationwide have received the “Birthing Friendly” designation, however, some argue that additional quality metrics and efforts are needed to improve the impact and utility of this designation. CMS is also proposing new baseline health and safety requirements for hospitals, including topics related to delivery of care in obstetric units, staffing, and annual training on evidence-based maternal health practice and cultural competencies. Moreover, in 2024, CMS has launched a new effort within its maternal and infant health initiative to focus on maternal mental health, substance use, and hypertension management.

Some states include a focus on equity as part of their Maternal Mortality Review Committee (MMRC). Nearly all states have an MMRC that reviews pregnancy associated deaths and offers recommendations to prevent future deaths. However, state MMRCs vary in how they examine racial disparities, with some specifying identifying and addressing disparities as a key focus. Beginning in 2020, discrimination was added to the list of circumstances surrounding a pregnancy-related death that can be reported by MMRCs. For example, in California, each death is examined through a health equity lens and considerations include how social determinants of health, discrimination, and racism may have contributed to the death. Similarly, Vermontamended the charge of its committee in 2020 to include considerations of disparities and social determinants of health, including race and ethnicity in perinatal death reviews. States also vary in the membership of their committees, with some having requirements related to Tribes and doulas or midwives. Washington, Montana and Arizona are examples of states that have a Native or Tribal Government representative, while Oregon and Louisiana have doula representation, and Vermont and Pennsylvania have midwife representation on their MMRCs.

A variety of efforts are underway to increase workforce diversity and expand access to doula services to improve maternal and infant health outcomes and reduce disparities. Studies have shown that a more diverse healthcare workforce and the use of midwives and doulas may improve birth outcomes. Midwives are an important component of the health care workforce, attending approximately one in ten births in 2021. Midwife-attended births are associated with fewer medical interventions, and there are efforts to grow and diversify the midwifery workforce to help improve maternal health outcomes and reduce mortality and morbidity.

The percent of maternal health physicians and registered nurses that are Hispanic or Black is lower than their share of the female population of childbearing age. The Biden Administration’s Blueprint includes efforts by HRSA to provide scholarships to students from underrepresented communities in health professions and nursing schools to grow and diversify the maternal care workforce.

Expanding access to doula services is another approach to increase diversity and expand the maternal health workforce. Doulas are trained non-clinicians who assist a pregnant person before, during and/or after childbirth by providing physical assistance, labor coaching, emotional support, and postpartum care. People who receive doula support have been found to have shorter labors and lower C-section rates, fewer birth complications, are more likely to initiate breastfeeding, and their infants are less likely to have low birth weights. The HHS FY2025 budget directs $5 million towards growing and diversifying the doula workforce and $5 million towards addressing emerging issues and social determinants of maternal health. Additionally, in recent years, there has been growing interest in expanding coverage of doula services through Medicaid. The MOMNIBUS is federal legislation that has been introduced to address maternal health disparities, and proposes to expand access to coverage of midwife and doula services. Some states are taking steps to include coverage through their state programs. As of early February 2024, 12 states reimburse services provided by doulas under Medicaid (CA, DC, FL, MD, MI, MN, NV, NJ, OK, OR, RI, VA), with two states, Louisiana and Rhode Island, also implementing private coverage of doula services. Some states also are seeking to increase access to these providers by providing patient education about these services, supporting training and credentialing of these providers, and raising reimbursement rates.

Some states are seeking to improve access to culturally responsive maternal and childcare through community engagement and collaboration with community stakeholders. For example, as part of its Birth Equity Project, Washington held listening sessions with Black, immigrant, and Indigenous families and birth workers to understand the challenges to birth equity in the state. In 2021 and 2022, Utah conducted the Embrace Project Study to reduce disparities among NHPI women by providing culturally responsive health services, with a focus on mental health and self-care practices rooted in ancestral NHPI cultural traditions. California has a Black Infant Health Program that includes empowerment-focused group support services and client-centered life planning to improve the health and social conditions for Black women and their families. Arizona hosts a maternal and infant mortality summit which brings together stakeholders to discuss how to improve equity and a Tribal maternal task force that develops a Tribal maternal health strategic plan and provides training about maternal health and family wellness from an Indigenous perspective.

A range of organizations are advocating for more interventions and support to address maternal mental health and substance use issues, major causes of pregnancy-related mortality and morbidity. Some studies have found higher rates of postpartum depression among some pregnant and postpartum women of color, but many mental health conditions are undiagnosed and untreated due to stigma and poor access to treatment. These issues also limit access to services for pregnant and postpartum people with substance use disorders. Additionally, some states have laws that take a punitive approach toward substance use during pregnancy, which may discourage some, particularly people of color, from seeking care. Community-based and provider organizations are calling for a number of policy and structural changes to address these challenges, including broader insurance coverage for behavioral health care, higher reimbursement for existing treatment services, greater education and awareness about screening for mental health and substance use conditions among health care providers and childbearing people. Federal initiatives in this area include the launch of the National Maternal Mental Health Hotline by HRSA to provide support, resources and referrals to new mothers and their families.

Looking Ahead

Improving maternal and infant health is key for preventing unnecessary illness and death and advancing overall population health. Healthy People 2030, which provides 10-year national health objectives, identifies the prevention of pregnancy complications and maternal deaths and improvement of women’s health before, during, and after pregnancy as a public health goal. Further, the National Institutes of Health (NIH) Pathways to Prevention panel recently recommended a “maternal mortality moonshot” with a goal of reducing preventable maternal mortality by 50% and eliminating racial disparities within the next 10 years.

While there are a range of efforts underway to reduce disparities in maternal and infant health, state abortion bans and restrictions may exacerbate poor maternal and infant health outcomes and access to care. Since the Dobbs ruling in June 2022, about half of states have banned abortion or restricted it to early in pregnancy. People of color are disproportionately affected by these bans and restrictions as they are at higher risk for pregnancy-related mortality and morbidity, are more likely to obtain abortions, and more likely to face structural barriers that make it more difficult to travel out of state for an abortion. There are many documented cases of people being forced to continue pregnancies that are endangering their lives because they could not obtain abortion care, and the recent deaths of two pregnant women in Georgia were attributed directly to delays in pregnancy termination. State-level bans and restrictions criminalize clinicians who provide abortion care which also has cascading effects on other aspects of maternity care, and as a result some clinicians are choosing not to practice in these states, potentially widening existing clinician shortages. Research also suggests that rates of infant mortality have increased since the Dobbs ruling.

The outcome of the presidential election also could have important implications for disparities in maternal and infant health. While both candidates have taken actions focused on improving maternal health, former President Trump and Vice President Harris have widely differing records and proposals related to health coverage and health. Vice President Harris has been an outspoken advocate for eliminating maternal health disparities and promoting access to abortion and contraception services in addition to maternity care for all. Trump expresses his support for letting states set their own abortion policy, which can limit the availability of other related services, including maternity care.

Health insurance is expensive and can be difficult to afford for people with lower or moderate incomes. In response, the Affordable Care Act (ACA) provides sliding-scale subsidies that lower premiums and insurers offer plans with reduced out-of-pocket (OOP) costs for eligible individuals.

This brief provides an overview of the financial assistance provided under the ACA for people purchasing coverage on their own through health insurance Marketplaces (also called exchanges).

Health Insurance Marketplace Subsidies

There are two types of financial assistance available to Marketplace enrollees. The first type, called the premium tax credit, reduces enrollees’ monthly payments for insurance coverage. The second type of financial assistance, the cost sharing reduction (CSR), reduces enrollees’ deductibles and other out-of-pocket costs when they go to the doctor or have a hospital stay. To receive either type of financial assistance, qualifying individuals and families must enroll in a plan offered through a health insurance Marketplace.

Premium Tax Credit

Premium tax credits can be applied to Marketplace plans in any of four “metal” levels of coverage: bronze, silver, gold, and platinum. Bronze plans tend to have the lowest premiums but have the highest deductibles and other cost sharing, leaving the enrollee to pay more out-of-pocket when they receive covered health care services, while platinum plans have the highest premiums but very low out-of-pocket costs.

Also offered on the Marketplace are catastrophic health plans with even lower premiums and higher cost sharing compared to bronze plans. Catastrophic plans are generally only available to individuals younger than 30, and premium tax credits cannot be applied to these plans.

Who is eligible for the premium tax credit?

To receive a premium tax credit for 2025 coverage, a Marketplace enrollee must meet the following criteria:

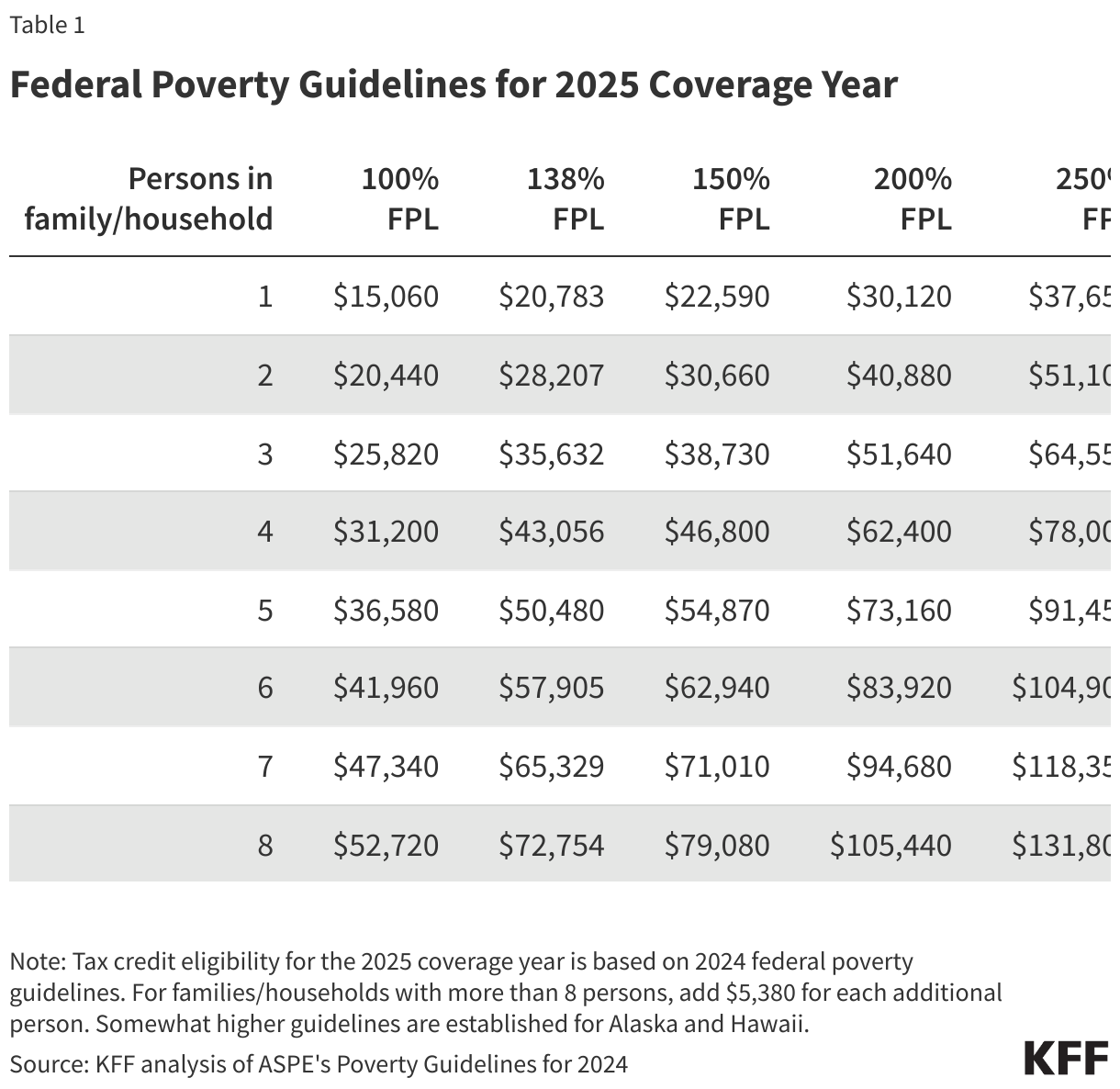

Have a household income at least equal to the Federal Poverty Level (FPL), which for the 2025 benefit year will be determined based on 2024 poverty guidelines (Table 1).

Not have access to an employer plan (including a family member’s employer) that both meets minimum value and is considered affordable. For 2025, the threshold that determines if an employer plan is affordable is if the premium is equal to or less than 9.02 percent of one’s household income.

Not be eligible for coverage through Medicare, Medicaid, or the Children’s Health Insurance Program (CHIP).

Have U.S. citizenship or proof of legal residency. (Lawfully present immigrants whose household income is below 100 percent FPL can also be eligible for tax subsidies through the Marketplace if they meet all other eligibility requirements.)

If married, must file taxes jointly.

Income: For the purposes of the premium tax credit, household income is defined as the Modified Adjusted Gross Income (MAGI) of the taxpayer, spouse, and dependents who are required to file a tax return. The MAGI calculation includes income sources such as wages, salary, foreign income, interest, dividends, and Social Security.

Employer coverage: Employer coverage is considered affordable if the required premium contribution is no more than 9.02 percent of household income in 2025. The Marketplace will look at both the required employee contribution for self-only and (if applicable) for family coverage. If the required employee contribution for self-only coverage is affordable, but the required employee contribution is more than 9.02 percent of household income for family coverage, the dependents can purchase subsidized exchange coverage while the employee stays on employer coverage.

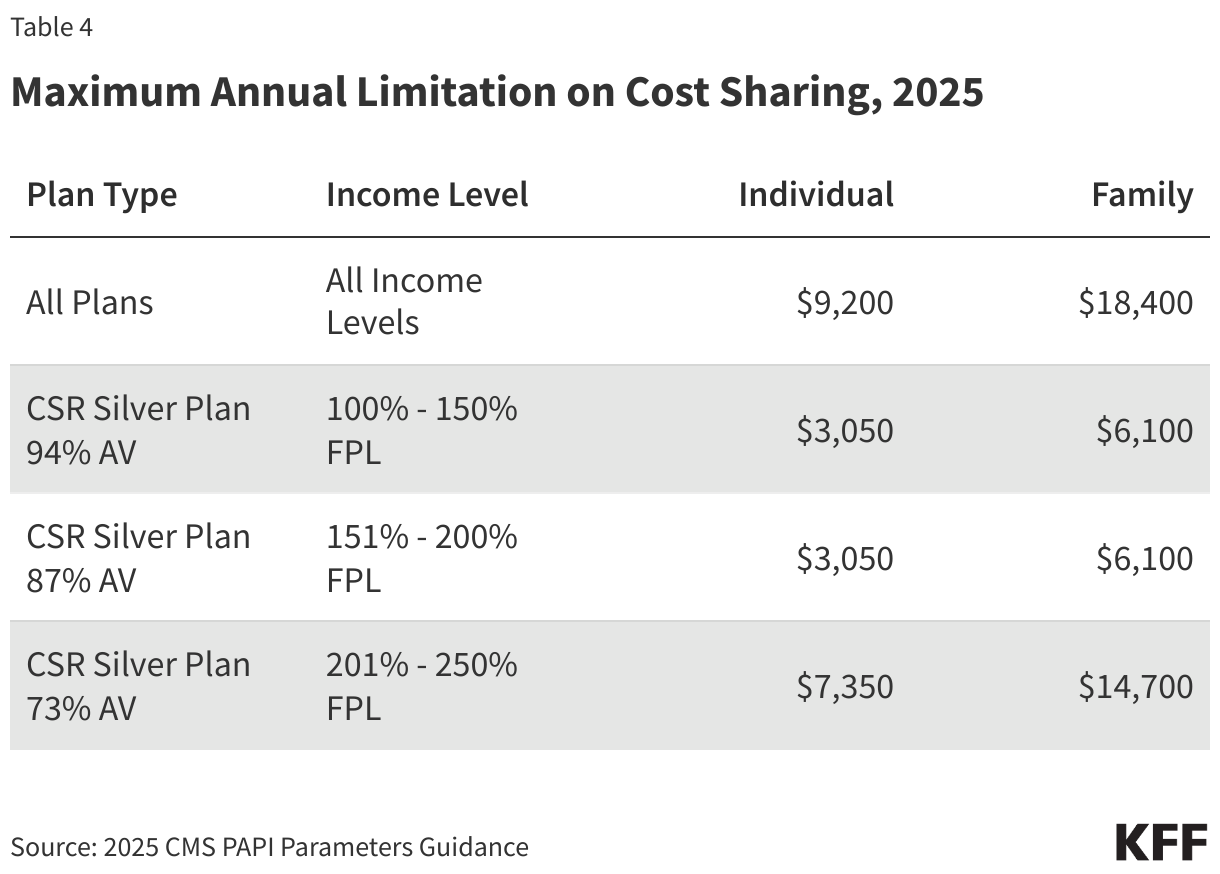

The employer’s coverage must also meet a minimum value standard that requires the plan to provide substantial coverage for physician services and for inpatient hospital care with an actuarial value of at least 60 percent (meaning the plan pays for an average of at least 60 percent of all enrollees’ combined health spending, similar to a bronze plan). The plan must also have an annual OOP limit on cost sharing of no more than $9,200 for self-only coverage and $18,400 for family coverage in 2025.

People who are offered employer-sponsored coverage that fails to meet either the affordability threshold or minimum value requirements can qualify for Marketplace subsidies if they meet the other criteria listed above.

Eligibility for Medicaid: In states that have expanded Medicaid under the ACA, adults earning up to 138 percent FPL are generally eligible for Medicaid and not for Marketplace subsidies. In states that have not adopted Medicaid expansion, adults with income as low as 100 percent FPL can qualify for Marketplace subsidies. However, those with incomes lower than 100 percent FPL are generally not eligible for tax credits or Medicaid unless they meet other state eligibility criteria. KFF estimates that 1.5 million Americans living in non-expansion states fall into this coverage gap.

Certain lawfully present immigrants are exempt from the rule restricting tax credit eligibility for adults below the poverty level. Other federal rules restrict Medicaid eligibility for lawfully present immigrants, other than pregnant women, refugees, and asylees, until they have resided in the U.S. for at least five years. Immigrants who would otherwise be eligible for Medicaid but have not yet completed their five-year waiting period may instead qualify for tax credits through the Marketplace. If an individual in this circumstance has an income below 100 percent of poverty, for the purposes of tax credit eligibility, his or her income will be treated as though it is equal to the poverty level. Exceptions are also made for Deferred Action for Childhood Arrivals (DACA) recipients, who became newly eligible for Marketplace coverage after the Biden-Harris administration passed new regulations in May 2024 expanding the definition of lawfully present to include DACA recipients. Immigrants who are not lawfully present are ineligible to enroll in health insurance through the Marketplace, receive tax credits through the Marketplaces, or enroll in non-emergency Medicaid and CHIP.

What amount of premium tax credit is available?

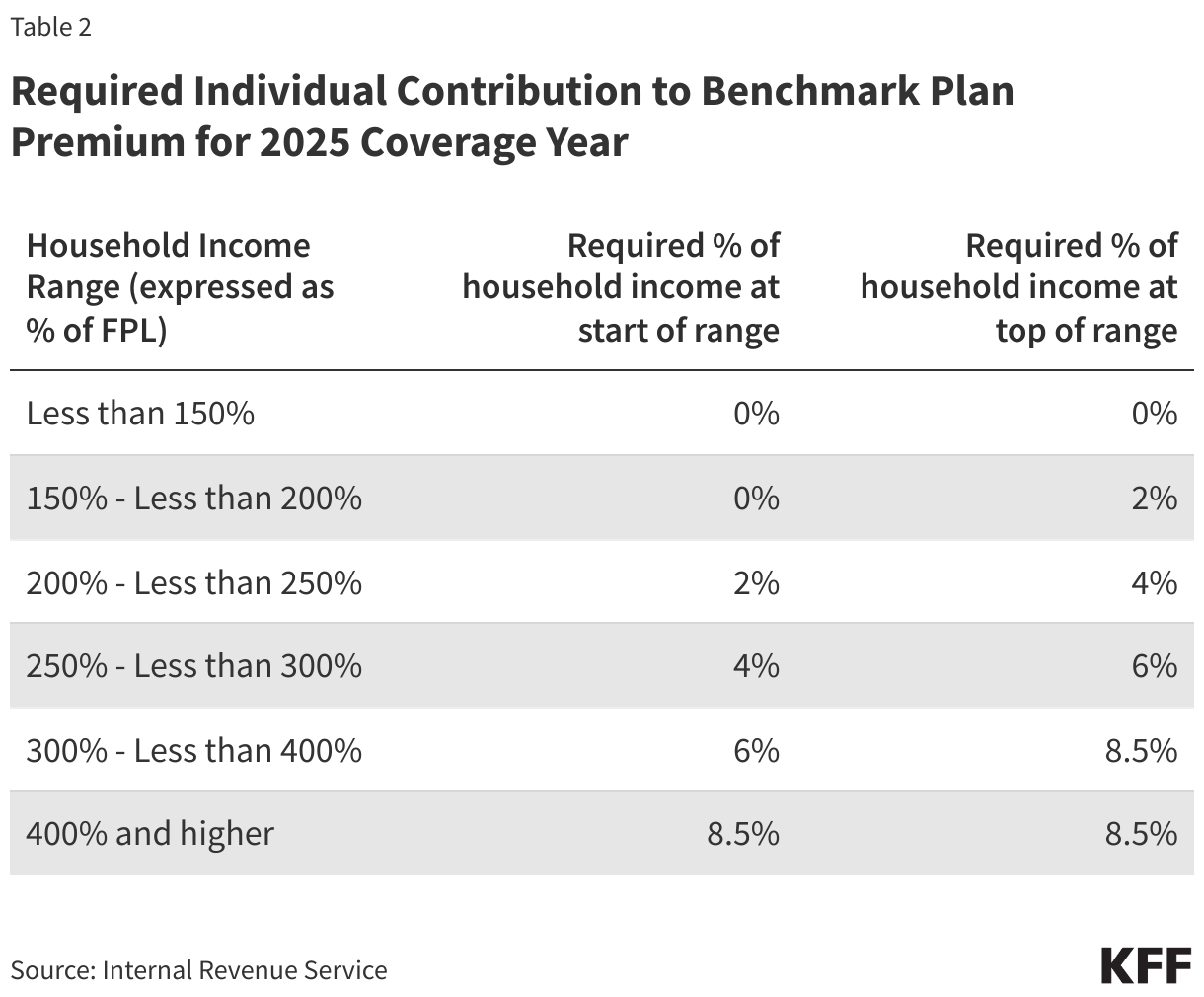

The premium tax credit limits an individual’s contribution toward the premium of the “benchmark” plan, the second-lowest cost silver plan in their Marketplace. This “required individual contribution” is set on a sliding income scale. In 2025, for individuals with income up to 150 percent FPL, the required contribution is zero, while at an income of 400 percent FPL or above, the required contribution is 8.5 percent of household income (Table 2). Individuals making above 400 percent FPL whose required contribution for a benchmark silver premium is greater than the actual cost of a benchmark silver plan relative to their household income would be ineligible for subsidies.

These contribution amounts were set by the American Rescue Plan Act (ARPA) and later temporarily extended by the Inflation Reduction Act (IRA). Prior to the ARPA, the required contribution percentages ranged from about two percent of household income for people with poverty level income to nearly 10 percent of household income for people with income from 300 to 400 percent FPL. In addition, prior to the ARPA, people with incomes above 400 percent FPL were not eligible for premium tax credits.

The amount of tax credit is calculated by subtracting the individual’s required contribution from the actual cost of the “benchmark” plan. So, for example, if the benchmark plan costs $6,000 annually, the required contribution for someone with an income of 150 percent FPL ($22,590 in 2025) is zero, resulting in an annual premium tax credit of $6,000. If that same person’s income equals 250 percent FPL (or $37,650 in 2025), the individual contribution is four percent of $37,650, or $1,506 per year, resulting in an annual premium tax credit of $4,494.

The premium tax credit can then be applied toward any other plan sold through the Marketplace (except Catastrophic coverage). The amount of the tax credit remains the same, so a person who chooses to purchase a plan that is more expensive than the benchmark plan will have to pay the difference in cost. Conversely, if a person chooses a less expensive plan, such as the lowest-cost silver plan or a bronze plan, the tax credit will cover a greater share of that plan’s premium, and possibly even cover the entire cost, leaving the consumer with a zero-premium plan. When the tax credit exceeds the cost of a plan, it lowers the premium to zero and any remaining tax credit amount is unused.

For certain components of a Marketplace plan premium, the premium tax credit will not apply. First, the tax credit cannot be applied to the portion of a person’s premium attributable to covered benefits that are not essential health benefits (EHB). For example, a plan may offer adult dental benefits, which are not currently included in the definition of EHB. In that case, the person would have to pay the portion of the premium attributable to adult dental benefits without financial assistance. In addition, the ACA prohibits applying premium tax credits to the portion of premiums covering “non-Hyde” abortion benefits. Marketplace plans that cover abortion are required to charge a separate $1 monthly premium to cover the cost of this benefit; this means a consumer who is otherwise eligible for a fully subsidized, zero-premium policy would still need to pay $1 per month for a policy that covers abortion benefits. Finally, if the person smokes cigarettes and is charged a higher premium for smoking, the premium tax credit is not applied to the portion of the premium that is the tobacco surcharge.

How do people receive the premium tax credit?

To receive the premium tax credit, people must apply for coverage through the Marketplace and provide information about their age, address, household size, citizenship status, and estimated income for the coming year. After submitting the application, people will receive a determination letting them know the amount of premium tax credit for which they qualify. The consumer then has the option to have the tax credit paid in advance, claim it later when they file their tax return, or some combination of the two options.

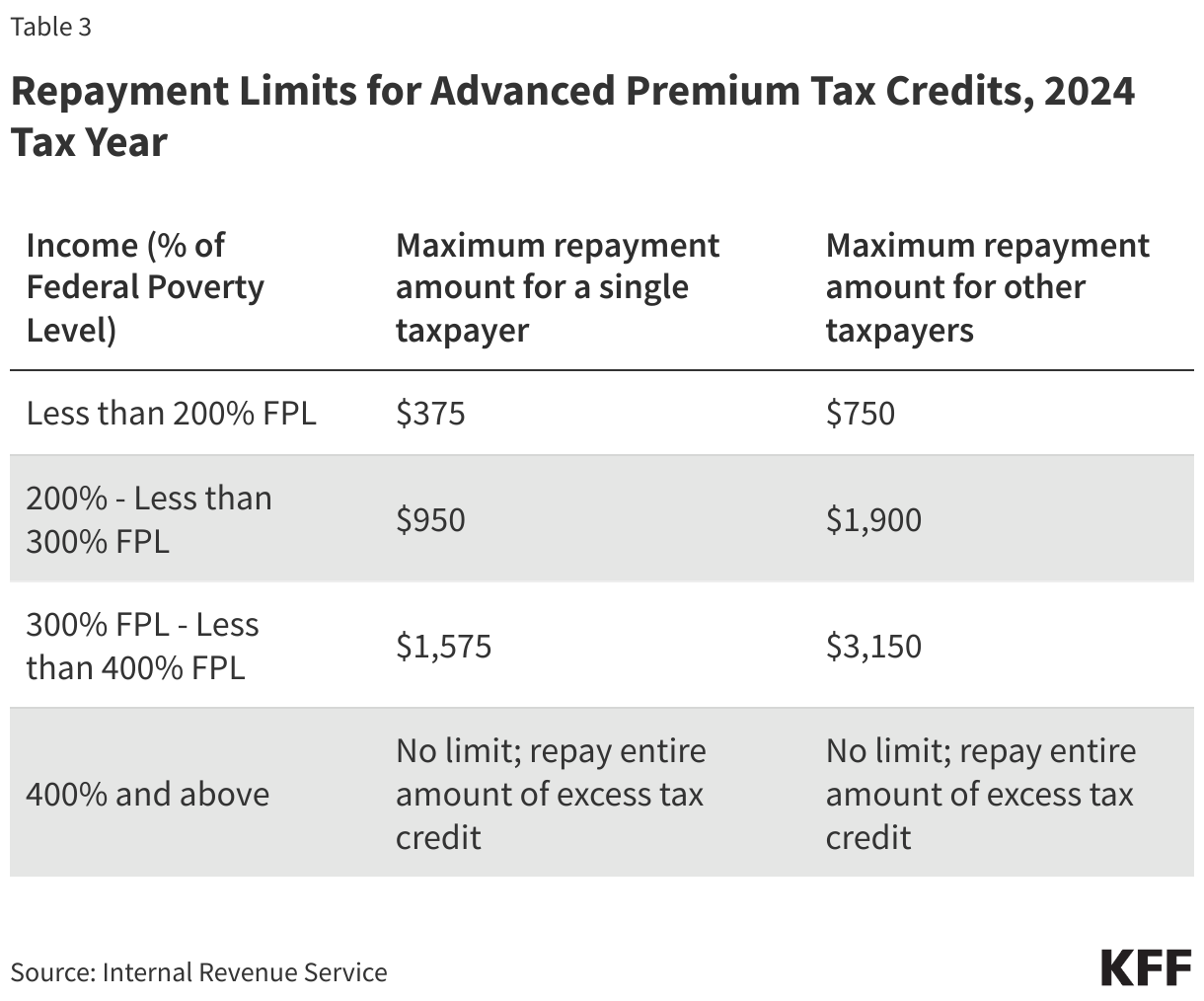

The advanced premium tax credit (APTC) option allows consumers to have 1/12 of their tax credit paid directly to their Marketplace plan insurer each month, reducing the monthly amount the consumer owes. However, because the APTC eligibility determination is based on estimated income, the enrollee is required to reconcile their APTC at tax time the following year, once they know what their actual income was. For people receiving an advanced payment of the premium tax credit in 2025, the reconciliation would occur when they file their 2025 tax return in 2026. If the consumer overestimated their income when they applied, they can receive the unclaimed premium tax credit as a refundable tax credit when they file. If the consumer underestimated their income at the time of application and excess APTC was paid on their behalf during the year, they would have to repay some or all of the excess tax credit when they file. There are maximum repayment limits which vary depending on income, shown in Table 3.

Alternatively, people can opt to pay their entire premium costs each month and wait to receive their tax credit until they file their annual income tax return the following year, although most Marketplace participants cannot afford this option. The premium tax credit is refundable, meaning it is available to qualifying enrollees regardless of whether they otherwise owe any federal income tax. Everyone who receives an APTC in a tax year is required to file a tax return for that year in order to continue receiving financial assistance in the future. People who fail to file and reconcile for two consecutive years will be ineligible for premium tax credits the following year.

Cost Sharing Reduction

The second form of financial assistance available to Marketplace enrollees is a cost sharing reduction. Cost sharing reductions lower enrollees’ out-of-pocket cost due to deductibles, copayments, and coinsurance when they use covered health care services.

Who is eligible for the cost sharing reduction?

People eligible for premium tax credits and have household incomes between 100 to 250 percent of poverty are eligible for cost sharing reductions.

How are cost sharing reductions provided?

Unlike the premium tax credit (which can be applied toward any metal level of coverage), cost sharing reductions (CSR) are only offered through silver plans. For eligible individuals, cost sharing reductions are applied to a silver plan, essentially making deductibles and other cost sharing under that plan more similar to that under a gold or platinum plan. Individuals with income between 100 and 250 percent FPL can continue to apply their premium tax credit to any metal level plan, but they can only receive plans with reduced cost sharing if they pick a silver-level plan.

What amount of cost sharing reductions are available to people?

Cost sharing reductions are determined on a sliding scale based on income. The most generous cost sharing reductions are available for people with income between 100 and 150 percent FPL. For these enrollees, silver plans that otherwise typically have higher cost sharing are modified to be more similar to a platinum plan by substantially reducing the silver plan deductibles, copays, and other cost sharing. For example, in 2024, the average annual deductible under a silver plan was just over $5,000, while the average annual deductible under a platinum plan was $97. Silver plans with the most generous level of cost sharing reductions are sometimes called CSR 94 silver plans (with 94 percent actuarial value, which represents the average share of health spending paid by the health plan, compared to 70 percent actuarial value for a silver plan with no cost sharing reductions).

Somewhat less generous cost sharing reductions are available for people with incomes above 150 and up to 200 percent FPL. These reduce cost sharing under silver plans to 87 percent actuarial value (CSR 87 plans). In 2024, the average annual deductible under a CSR 87 silver plan was about $700.

For people with incomes above 200 and up to 250 percent FPL, cost sharing reductions are available to modestly reduce deductibles and copays to 73 percent actuarial value (sometimes called CSR 73 plans). In 2024, the average annual deductible under a CSR 73 silver plan was about $4,500.

Insurers have flexibility in how they set deductibles and copays to achieve actuarial value benchmarks set by the ACA for Marketplace plans, including CSR plans, so actual deductibles may vary from these averages.

The ACA also requires maximum annual out-of-pocket spending limits on cost sharing under Marketplace plans, with reduced limits for CSR plans. In 2025, the maximum OOP limit will be $9,200 ($18,400 family) for all QHPs with lower maximum OOP limits permitted under cost sharing reduction plans (Table 4).

This brief was updated on October 24, 2024 to incorporate updates to Medicare and Medicaid administrative data.

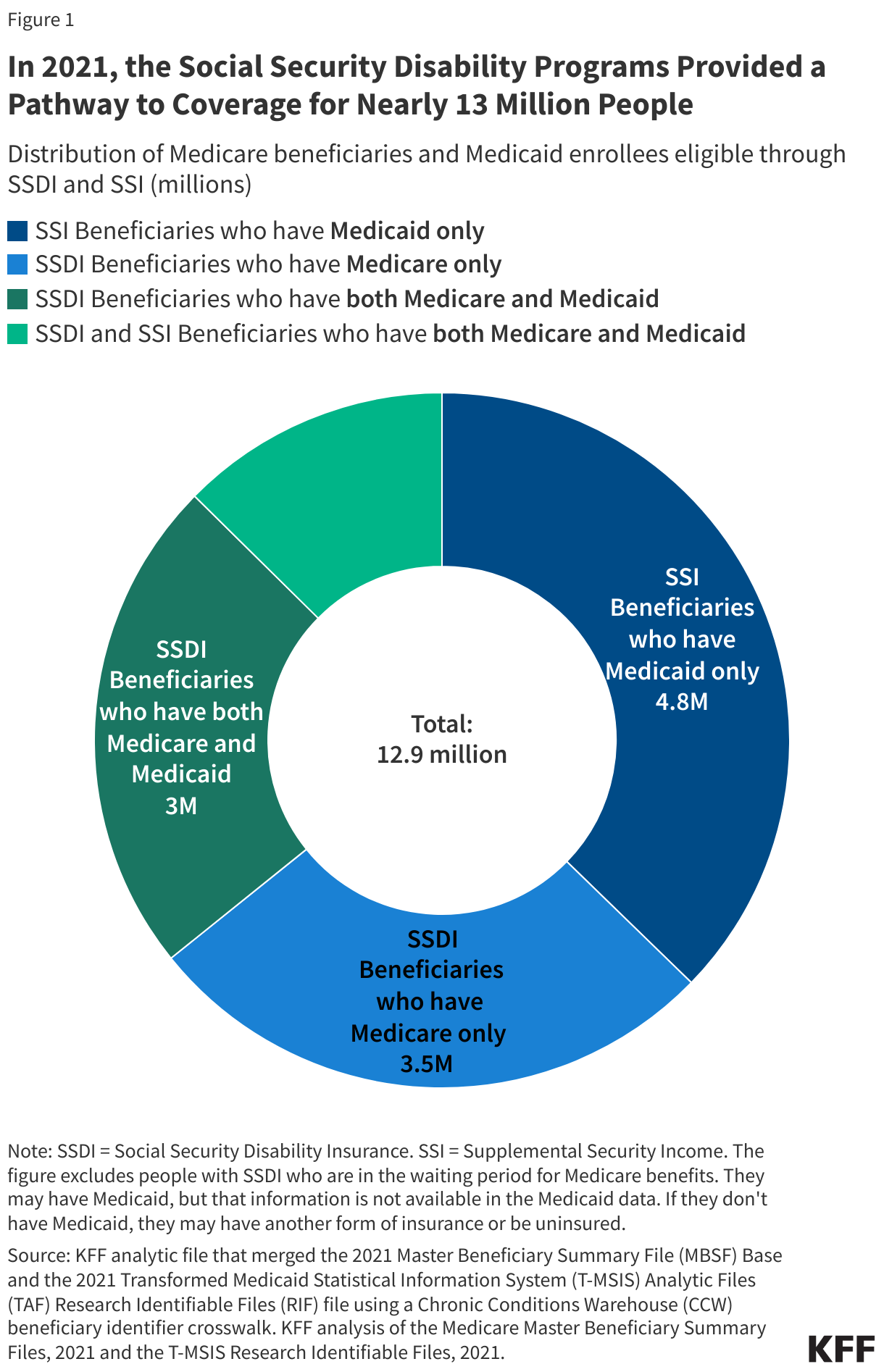

In 2021, 13 million people under age 65 received income from the Social Security disability programs, Social Security Disability Insurance (SSDI) and Supplemental Security Income (SSI), which provide monthly income to people who are unable to work on account of a disability. A less-commonly appreciated benefit of qualifying for Social Security disability programs is the connection to health insurance coverage through Medicare or Medicaid. In most states, SSI beneficiaries automatically qualify for and receive Medicaid coverage, while SSDI beneficiaries qualify for Medicare after receiving disability benefits for at least two years. Many who receive benefits from the SSDI and SSI programs also qualify for both Medicare and Medicaid, known as dual-eligible individuals.

This analysis examines enrollment in disability programs and characteristics of enrollees from 2002-2022 Social Security Administration data and related health coverage through the Medicare and Medicaid programs using data from the Centers for Medicare and Medicaid Services for 2021, the most recent year of data available. (See methods for details.) State-level data about the disability programs are also available on KFF’s State Health Facts.

Key Takeaways

In 2021, 12.9 million people were eligible for Medicare or Medicaid because they received disability benefits from either SSDI or SSI. Of that total, 4.6 million, or more than one-third (35%), qualified for health coverage under both Medicare and Medicaid (dual-eligible individuals). Another 4.8 million SSI beneficiaries had Medicaid coverage only and 3.5 million SSDI beneficiaries had Medicare coverage only.

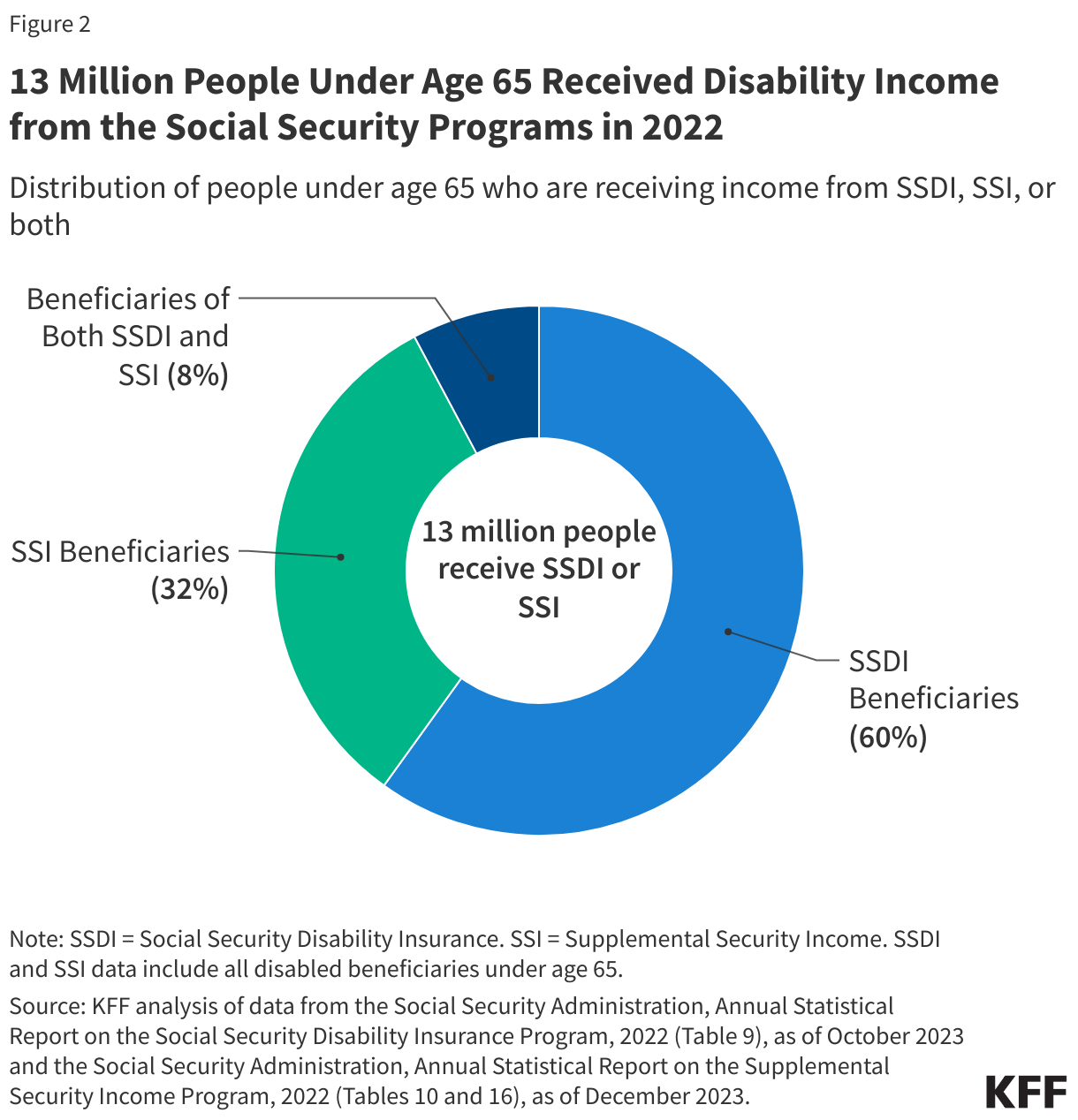

A total of 13.0 million people under age 65, including working-age adults and children, received disability benefits in 2022, including 7.8 million people who received income from SSDI, 4.2 million who received income from SSI, and 1 million who received income from both programs.

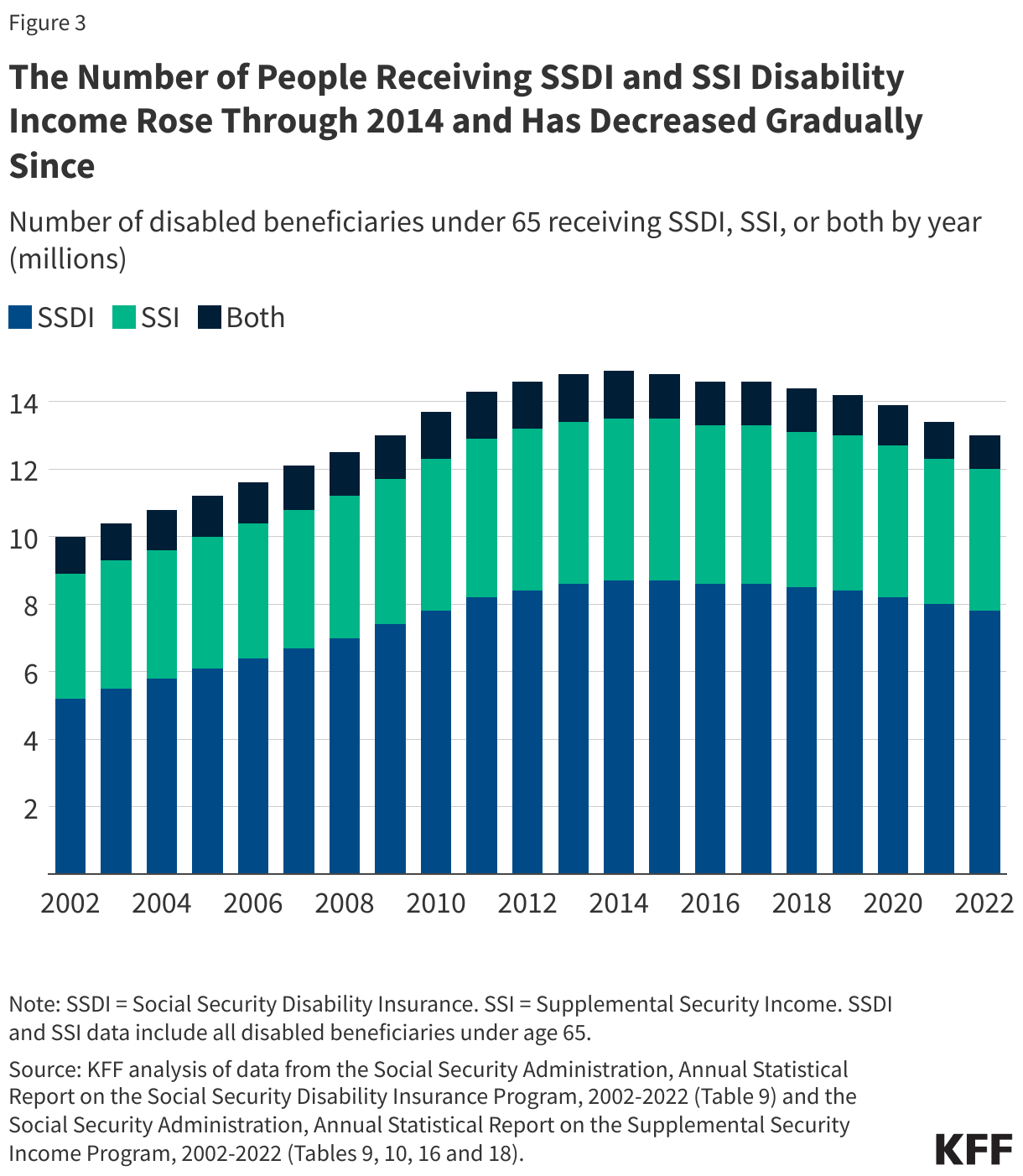

Enrollment of working-age adults in both the SSDI and SSI programs has decreased since 2014, reflecting the changing demographics of the U.S. population, the economy, and other factors that have reduced the number of new beneficiaries, including in more recent years, the lasting effects of Social Security office closures during the COVID-19 pandemic. The decline in SSDI enrollment has also meant a decline in the number of Medicare beneficiaries under age 65 who qualify due to disability.

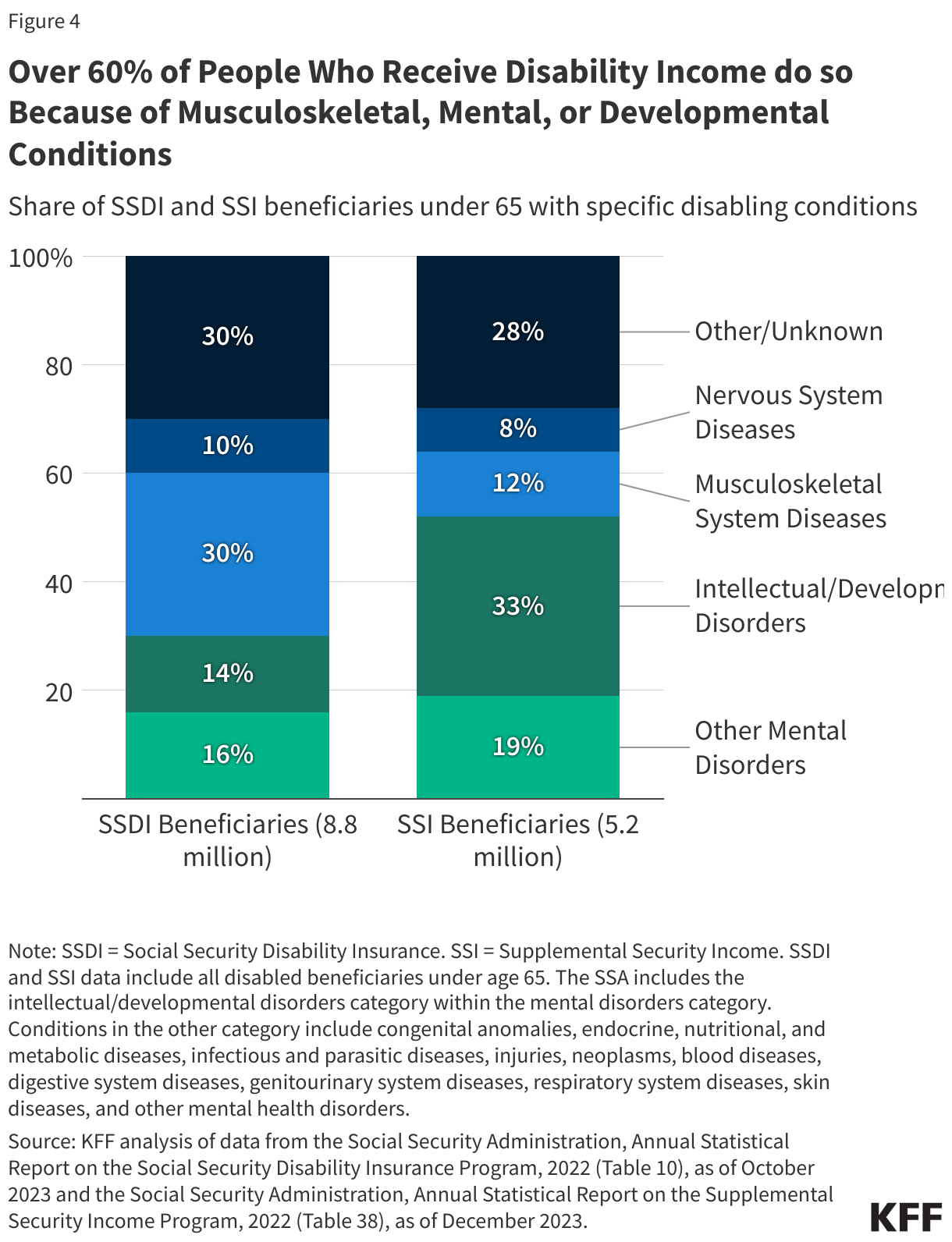

Mental disorders—which include intellectual and developmental disorders and other mental disorders—comprise the largest percentage of disabling conditions across both programs. In the SSDI program, musculoskeletal conditions are the most common disabling conditions among disabled beneficiaries (30%), followed by other mental disorders (16%) and intellectual/developmental disorders (14%). For SSI beneficiaries, intellectual and developmental disorders are the most common disabling conditions (33%), followed by other mental disorders (19%) and musculoskeletal disorders (12%).

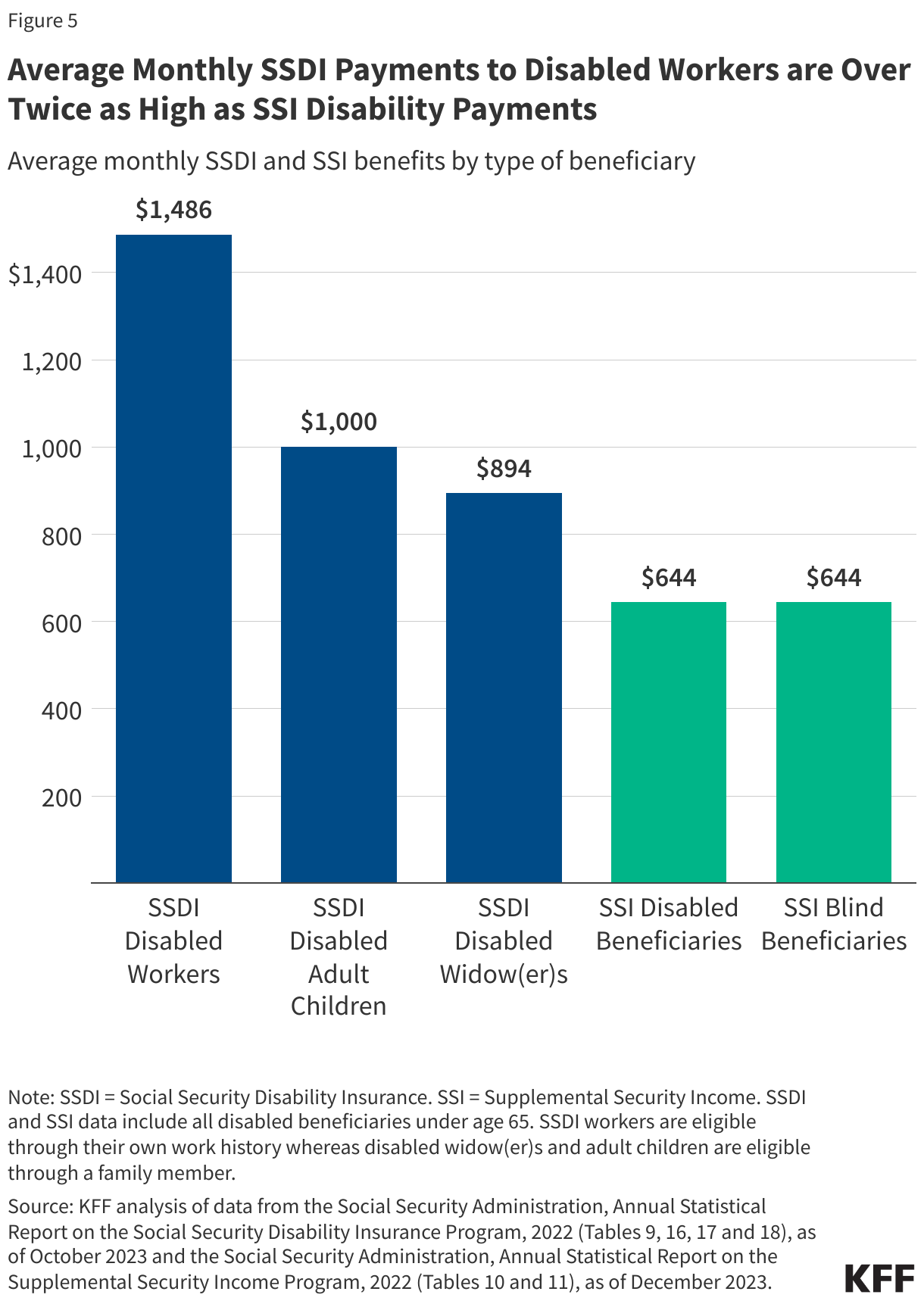

The average monthly benefit in 2022 was more than twice as large for disabled workers in the SSDI program (nearly $1,500 per month) than disabled beneficiaries in the SSI program (nearly $650 per month).

How many people under age 65 qualify for Medicaid and Medicare through the Social Security disability programs?

In 2021, 12.9 million people who received benefits through the Social Security disability programs qualified to receive coverage from Medicare, Medicaid, or both programs on account of their eligibility for disability benefits (Figure 1). While 61% of working age adults and nearly half of children had health coverage through an employer in 2022, employment-based coverage is much less common among people with disabilities, who are less likely to work. As a result, the Social Security disability programs – Social Security Disability Insurance (SSDI) and Supplemental Security Income (SSI) (see Box 1) – play an important role in helping people with disabilities access health insurance coverage through the Medicaid or Medicare programs, with some people with disabilities qualifying for health coverage under both Medicare and Medicaid (known as dual-eligible individuals).

Of the 12.9 million people with disabilities who have coverage from Medicare, Medicaid, or both based on their eligibility for disability programs, a total of 4.6 million, or more than one-third (35%), are dual-eligible individuals. Overall, the overall group includes:

4.8 million SSI beneficiaries who have Medicaid only;

3.5 million SSDI beneficiaries who have Medicare only;

3.0 million SSDI beneficiaries who have both Medicare and Medicaid; and

1.6 million beneficiaries receiving both SSDI and SSI, who have both Medicare (through SSDI) and Medicaid (through SSI).

Although most people qualify for Medicare based on age when they turn 65, people under age 65 may become eligible for Medicare if they have received SSDI payments for 24 months. In 2021, 8.3 million people under the age of 65 were eligible for Medicare because of a disabling condition. Nearly all (8.1 million) were eligible through SSDI, and 0.2 million were eligible because they had End-Stage Renal Disease (ESRD) but did not receive SSDI. SSDI beneficiaries often must wait 5 months for SSDI payments after the onset of benefits, followed by a two-year waiting period between receipt of SSDI benefits and Medicare eligibility, referred to as the “Medicare waiting period.” It is unknown how many people are currently in the waiting period or what their health insurance coverage is during this period. Because of the length of the SSDI application process and the fact that SSDI eligibility is retroactive, applicants may complete some or all of the waiting period prior to receiving SSDI benefits, but many experience gaps in coverage during this time too. (Those under age 65 who qualify for Medicare based on having ESRD or Amyotrophic Lateral Sclerosis (ALS) do not have to wait 24 months for their Medicare benefits to start because they are not required to qualify for SSDI first.)

According to KFF analysis, although majorities of people with Medicare of all ages rate Medicare positively, people under age 65 with disabilities are less likely than older beneficiaries to give positive ratings to Medicare and some features of it, such as the quality and availability of providers. Medicare beneficiaries under age 65 with disabilities have also reported worse access to care, more cost concerns, and lower satisfaction with care than those age 65 or older. The lower ratings by people under 65 with disabilities may possibly be related to their different pathways to Medicare eligibility and because the program was originally designed to cover older adults, with coverage for younger people with disabilities added later. Also, because a larger share of people with Medicare under 65 with disabilities report that they are in fair or poor physical and mental health and have severe chronic conditions compared to people age 65 or older, those under 65 with disabilities may be more likely to have multiple encounters with the health care system during the year and encounter problems when they do.

States must generally provide Medicaid to people who receive SSI. In 2021, 6.5 million people were eligible for Medicaid through the SSI disability program. If states do not want to use the SSI eligibility criteria, they can use more restrictive rules so long as the rules are no more restrictive than what the state had in place in 1972 when the SSI program was established. There are currently 8 states using their own criteria, known as the 209(b) states: Connecticut, Hawaii, Illinois, Minnesota, Missouri, New Hampshire, North Dakota, and Virginia.

Box 1: What are the Differences Between SSDI and SSI?

Social Security Disability Insurance (SSDI) and Supplemental Security Income (SSI) are federal programs administered by the Social Security Administration (SSA), but they differ in terms of how people qualify, the benefits they receive, and how they are financed. Both programs require adults under age 65 to have a qualifying disability, but SSI also includes qualifying disability criteria for children.

How do people qualify for SSDI and SSI? To qualify for SSDI, enrollees must have a sufficient work history, which varies by age but generally requires ten years of employment at least five of which were within the past decade. Some individuals with a disability can qualify based on a relative’s work history including:

Spouses of disabled workers (and divorced spouses if the marriage lasted for at least 10 years) if they have a child in their care or if they are at least 63 years old; and

Children of disabled workers if they are under age 18, 18 years old but still in high school, or are adults who have disabilities that started under the age of 22.

SSI is a means-tested program in which eligibility is based on an assessment of income and resources. To qualify, SSI enrollees must have low incomes, limited assets, and either be over age 64 or have a qualifying disability. Unlike SSDI, SSI is available to people regardless of their work history. The SSA redetermines eligibility and benefit amounts for SSI beneficiaries every 1 to 6 years or when a change that affects eligibility or payment is reported.

What benefits do people receive and how are the programs financed? Under both programs, the federal government pays monthly benefits to people who meet the eligibility criteria, and 45 states add supplemental payments for some SSI recipients. Maximum monthly benefits for SSI are legislatively established and updated annually to reflect inflation. Monthly benefits for SSDI reflect the payments workers made into the program through payroll taxes and are updated annually based on the growth in average wages. There are no state supplemental payments for SSDI. People can receive both SSDI and SSI if the income from SSDI is less than the maximum SSI payment. In those cases, SSI can cover the difference between the SSDI income amount and the maximum SSI.

How many people under age 65 receive income from Social Security disability programs?

Among the 268 million people under age 65 in the U.S., 5% or 13 million people received income from SSDI, SSI, or both programs in 2022. More than half (60%, or 8 million) of Social Security disability program beneficiaries under 65 exclusively receive SSDI income, and nearly a third (32%, or 4 million) receive only SSI, while over 1 million people received benefits from both programs (Figure 2).

How has enrollment in the Social Security disability programs changed over time?

Enrollment of working-age adults in the Social Security disability programs increased from the early 2000s through 2014 but has been declining since (Figure 3). Enrollment of people under age 65 in SSDI and SSI has decreased from 14.9 million beneficiaries in 2014 to 13.0 million beneficiaries in 2022. Enrollment trends in the disability programs reflect the demographics of the U.S. population, the economy, and other factors. Program size depends in part on the size of the labor force, and some of the decreased participation in recent years reflects the baby boomers entering their retirement years. For the SSDI program, participation also requires people to meet past employment requirements and lower labor force participation means fewer people can meet those requirements. Research has also found lower application and award rates for “contingent workers,” which includes independent contractors, consultants, and those in temporary, on-call, and gig economy jobs, who make up an increasing share of the workforce. Lower SSDI enrollment over the past decade also likely reflects fewer applications stemming from the end of routinely-mailed social security statements in 2011.

More stringent disability determinations could also contribute to the lower enrollment. Between 1999 and 2019, the percentage of applicants who were approved to receive benefits (the “award rate”) declined for both disability programs: from 56% to 29% for SSDI and from 44% to 34% in 2021 for SSI. Lower award rates mean that even if a similar number of people apply, fewer people will enroll and receive benefits.

The decline in SSDI enrollment has meant fewer people under age 65 qualifying for Medicare due to having a long-term disability. The total number of Medicare beneficiaries under age 65 with disabilities (excluding those who qualify based on having end-stage renal disease) has declined since 2016, both in terms of the total number and the share of overall Medicare enrollment, based on Medicare enrollment data from the Centers for Medicare & Medicaid Services. In 2016, there were 8.6 million Medicare beneficiaries under age 65, or 16% of all beneficiaries, decreasing to 7.2 million in 2023, or 11% of the total.

The same trend is not observed in Medicaid because people have more options for qualifying for Medicaid than they do Medicare. Between 2014 and 2022, most states adopted Medicaid expansions under the Affordable Care Act, which provided another mechanism for adults under age 65 to qualify for Medicaid and spurred enrollment growth. Enrollment also grew between 2020 and 2023 because of the COVID-19 continuous enrollment period, a three-year period during which Medicaid eligibility disenrollments were paused.

Historically, economic downturns led to increases in SSDI and SSI enrollment, but notably, there was no enrollment surge during the economic downturn associated with the COVID-19 pandemic. In fact, the enrollment decline accelerated during the COVID-19 pandemic, when Social Security offices were closed for 2 years, likely further reducing the number of applicants. Office closures also contributed to a backlog of cases that is causing people to wait longer for eligibility decisions: Social Security data show that the average review time for initial applications increased from 4 months or less before the pandemic to nearly 8 months in 2023. Similar trends occurred for applications that were reconsidered after an initial denial.

The application for Social Security disability benefits can be a lengthy and complicated process, spanning months, if not years. A chart visualizing the steps to disability determinations in 2022 by the National Organization of Social Security Claimants’ Representatives shows that 62% of the 1.8 million applicants in 2022 were denied at the initial application, but that hundreds of thousands pursued reconsiderations and subsequent legal proceedings to establish eligibility. A 2022 study by the National Bureau of Economic Research found that legal representation did not affect the likelihood of a successful SSDI outcome but reduced the time it took for approval by nearly one year. The challenge with demonstrating eligibility is in proving that one has a disabling condition that makes substantive employment impossible.

The Biden-Harris Administration’s proposed FY 2025 budget includes a $1.3 billion (9%) increase to the Social Security Administration’s budget from FY 2023 to 2025 to improve customer service across field offices, disability determination, and teleservice, and reduce wait times. The Biden-Harris Administration also supports using the budget increase to advance equity and accessibility. The new funding would support simplifying the SSI application process, broadening access to Social Security programs especially for unserved populations, and preventing overpayments. The Social Security Administration would also use the funding to continue improving information technology systems to make accessing services and communication with staff easier both online and via phone.

What are the most common conditions that qualify people for Social Security disability benefits?

For both SSDI and SSI, musculoskeletal system diseases and mental disorders are the most common conditions that qualify people for disability benefits (Figure 4). Both Social Security disability programs use a strict definition of disability when assessing eligibility, which limits how many people with disabilities ultimately qualify for SSDI or SSI payments. The Social Security Administration defines disability for adults as the inability to engage in any “substantial gainful activity” because of one or more medically determinable physical or mental disabilities that are either expected to result in death or have lasted or are expected to last for a continuous period of at least 12 months. Substantial gainful activity describes a level of work that involves doing significant physical or mental activities or a combination of both. For children to qualify as disabled, they must be under 18 and have one or more physical or mental impairments which result in marked and severe functional limitations and the impairment must have lasted or be expected to last for at least 12 months or be expected to result in death.

Over the past two decades, musculoskeletal system diseases and mental disorders (including both intellectual and developmental disorders and other mental disorders) have accounted for the largest shares of disability determinations, and in 2022, these conditions combined account for 60% of disability determinations among SSDI beneficiaries and 64% among SSI beneficiaries. The most common conditions for SSDI beneficiaries are musculoskeletal system diseases, which include non-healing or complex fractures, abnormalities of major joints, and disorders of the spine. The most common conditions for SSI beneficiaries are intellectual/developmental disorders which include autism spectrum disorders and neurocognitive disorders. Other mental disorders include depressive, bipolar, and related conditions and schizophrenia spectrum and other psychotic disorders.

How much do Social Security disability program beneficiaries receive in monthly benefits?

SSDI beneficiaries receive average monthly benefits that are over twice as large as what SSI beneficiaries receive, with monthly SSDI payments for disabled workers averaging nearly $1,500 per month, compared with roughly $650 per month for people receiving SSI benefits (Figure 5). Family members of SSDI workers receive lower monthly benefits, on average: just under $900 for widowers and $1,000 for adult children. The monthly payment from SSDI is calculated using a statutory formula that accounts for people’s earnings and is designed to pay higher benefits to people with higher earnings but to replace a larger percentage of earnings for people with lower earnings. In 2022, SSDI benefits ranged from less than $600 to more than $3,000 each month. The maximum SSI benefit is set by Congress and in 2022 was $841 per month for an individual ($943 in 2024) and $1,261 for a couple ($1,415 in 2024). If people have non-SSI income, their SSI benefits are reduced by the amount of countable income.

Many beneficiaries are now facing benefit reductions on account of prior overpayments by the Social Security Administration, as reported by KFF Health News, but the Biden-Harris Administration is taking steps to limit the effects of benefit reductions. Each year, more than 2 million beneficiaries have been receiving notices that their disability benefits were overpaid and are being asked to repay the specific amounts within 30 days or have their monthly disability benefits reduced. In many cases, those payments had been made years earlier without the recipients’ knowledge. There have been overpayments in both programs, but they are more common in SSI because SSI eligibility and payment amounts change when recipients experience changes in income and assets.

From April through June 2024, new overpayment policies went into effect to address those benefit reductions, including:

Limiting the amount that can be withheld from a recipient’s monthly disability benefits (to adjust for overpayments) to no more than 10% of the recipient’s monthly benefits for SSI recipients and either 10% or $10 for SSDI recipients (whichever is greater), rather than withholding the entire amount,

Increasing the amount of time for recipients to repay the overpayment,

Making overpayment notices easier to understand,

Simplifying the waiver application for beneficiaries who meet repayment exemption criteria, and

Holding the Social Security Administration responsible for providing proof of overpayment rather than the beneficiary.

This work was supported in part by Arnold Ventures. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

Methods

Included Areas: The analysis includes data from the 50 states and Washington D.C. (excluding enrollees in the territories and foreign countries).

Included Beneficiaries: Beneficiaries of Social Security disability programs who are under age 65.

Disability Programs: Data on the Social Security disability programs come from the Annual Statistical Report on the Social Security Disability Insurance Program, 2002-2022; and the Supplemental Security Income Annual Statistical Report, 2002-2022. The numbers in the issue brief come from the online appendix tables.

Medicare and Medicaid Enrollment: Data are from a KFF analytic file that merged the Centers for Medicare & Medicaid Services Chronic Conditions Data Warehouse 2021 research-identifiable Master Beneficiary Summary File (MBSF) Base and the 2021 Transformed Medicaid Statistical Information System (T-MSIS) Analytic Files (TAF) Research Identifiable Files (RIF) file using a Chronic Conditions Warehouse (CCW) beneficiary identifier crosswalk. The numbers include all Medicare enrollees who were currently eligible for Medicare on the basis of disability using ENTLMT_RSN_ORIG with values of 1, 3 and under 65 using AGE_AT_END_REF_YR in 2021, and all Medicaid enrollees who were currently eligible for Medicaid on the basis of SSI enrollment using the monthly ELGBLTY_GRP_CD with values of 11-22, 37, 38, 40, 41 and under 65 using AGE in 2021. People with records in both the Medicare and Medicaid data were categorized as dual-eligible beneficiaries.

Limitations: The estimates for SSDI and SSI enrollment are not comparable to the estimates of SSI and SSDI enrollees with Medicare and Medicaid coverage in 2021 for several reasons:

The data come from different sources and years.

The SSDI and SSI numbers are in the month of December whereas the Medicare and Medicaid numbers are people who were ever enrolled during the year.

Some people who are eligible for Medicare or Medicaid in a given month because of SSDI or SSI may not be receiving benefits from those programs in that month, particularly, if they are enrolled in certain programs designed to help people with disabilities work. This may be especially true between the years of 2020 and 2023 because states did not disenroll people during that time period on account of a continuous enrollment provision.