10 Things to Know About Medicaid Managed Care

Key Facts

Introduction

Managed care is the dominant delivery system for people enrolled in Medicaid. The latest national Medicaid managed care enrollment data (from 2024) show 78% of Medicaid beneficiaries were enrolled in comprehensive managed care organizations (MCOs). While managed care is the dominant Medicaid delivery system, states decide which populations and services to include in managed care arrangements, which leads to considerable variation across states. Additionally, while state requirements for Medicaid managed care plans can be tracked, plans have flexibility in certain areas, including in setting provider payment rates, and plans may choose to offer additional benefits beyond those required by the state.

States and plans faced considerable rate setting uncertainty after millions of people were disenrolled during the “unwinding” of the pandemic-era Medicaid continuous enrollment provision. Many states sought federal approval to adjust rates to address shifts in utilization and acuity—as people who used fewer services than average were disenrolled, leaving a group with higher health risk and spending. Looking ahead, states expect the 2025 federal budget reconciliation law will create additional managed care plan rate setting challenges as the Medicaid provisions impacting enrollment and spending (e.g., program financing changes, work requirements, and more frequent eligibility redeterminations) roll out over the next several years. Federal Medicaid spending cuts, coupled with a more tenuous fiscal climate (at the state-level), will have implications for states and enrollees as well as plans and providers. In this context, this brief describes 10 themes related to the use of comprehensive, risk-based managed care in the Medicaid program.

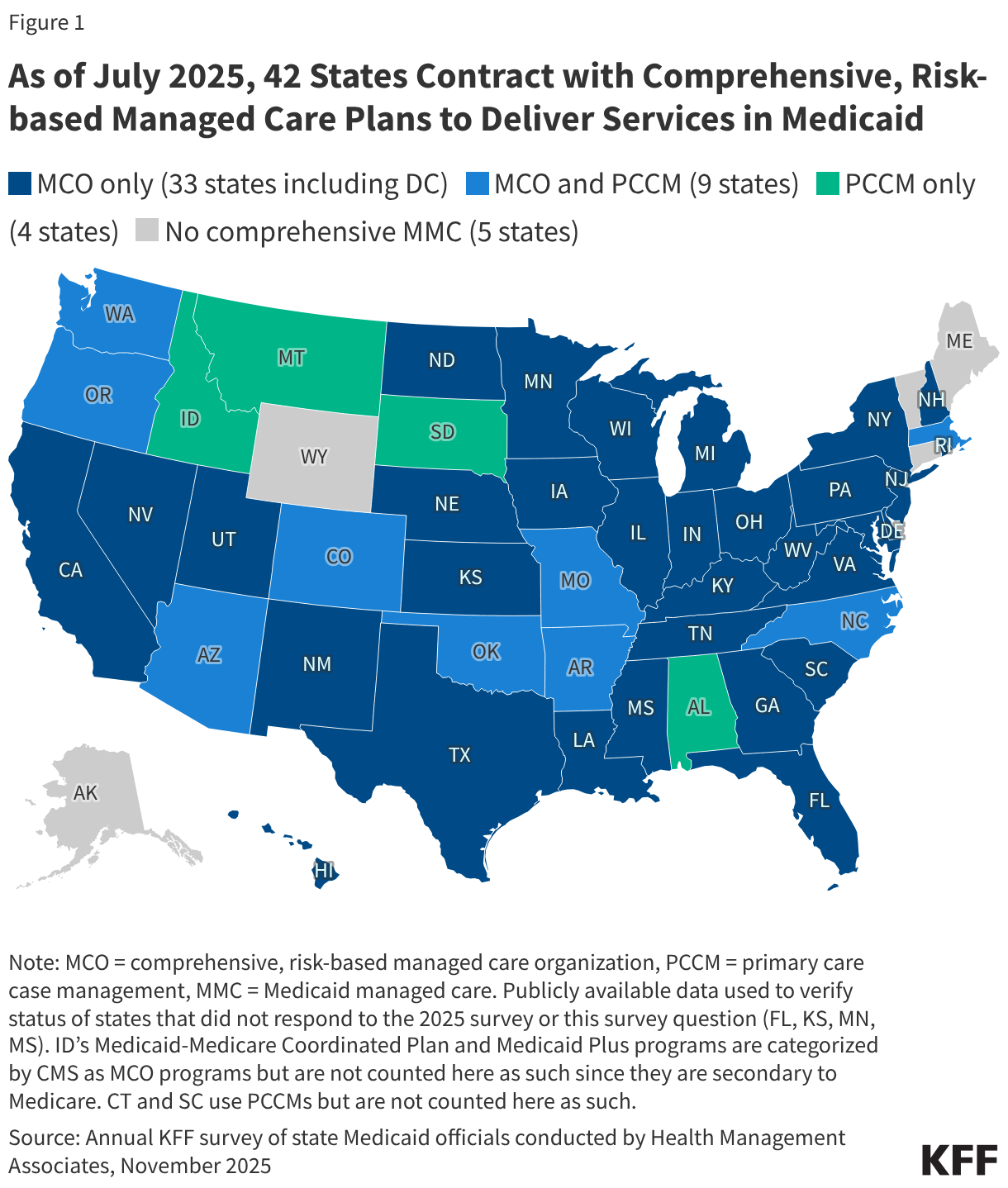

1. Capitated managed care is the dominant way in which states deliver services to Medicaid enrollees.

States design and administer their own Medicaid programs within federal rules. States determine how they will deliver and pay for care for Medicaid beneficiaries. Nearly all states have some form of managed care in place – comprehensive risk-based managed care (i.e., contracts with MCOs) and/or primary care case management (PCCM) programs.1, 2 As of July 2025, 42 states (including DC) contract with comprehensive, risk-based managed care plans to provide care to at least some of their Medicaid beneficiaries (Figure 1). Oklahoma is the latest state to be included in this count, having implemented capitated, comprehensive Medicaid managed care (for most children and adults) on April 1, 2024. Following the passage of state legislation, Idaho ended its PCCM program effective January 1, 2026 and expects to implement comprehensive MCOs in January 2030. Medicaid MCOs provide comprehensive acute care (i.e., most physician and hospital services) and, in some cases, long-term care to Medicaid beneficiaries and are paid a set per member per month payment for these services. For more than three decades, states have increased their reliance on managed care delivery systems with the aim of improving access to certain services, enhancing care coordination and management, and making future costs more predictable. While the shift to MCOs has increased budget predictability for states, the evidence about the impact of managed care on access to care and costs is both limited and mixed.3,4,5

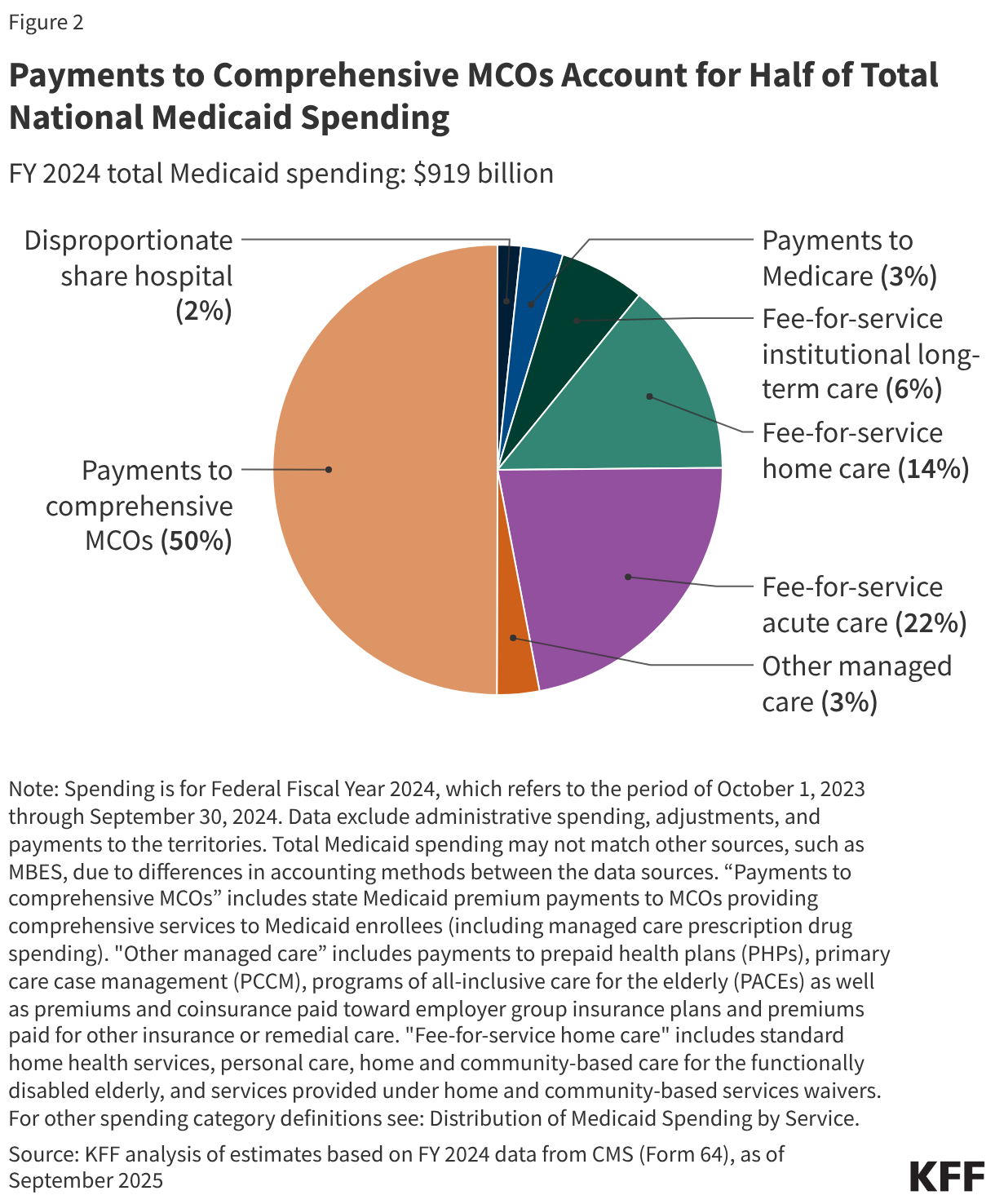

2. In FY 2024, payments to comprehensive risk-based MCOs accounted for half of Medicaid spending.

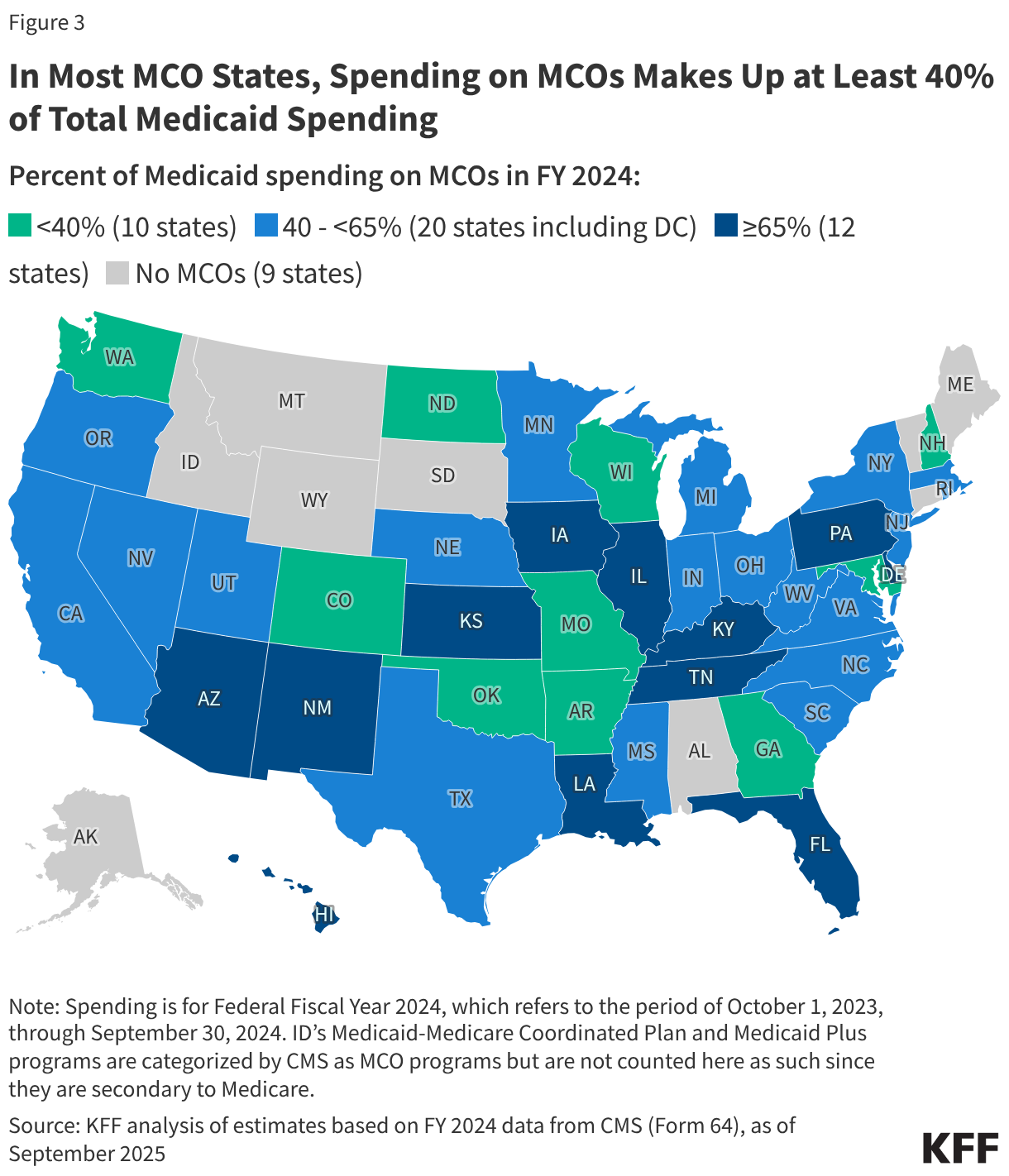

In FY 2024, state and federal spending on Medicaid services totaled $919 billion. Payments made to MCOs accounted for about 50% of total Medicaid spending (Figure 2). The share of Medicaid spending on MCOs varies by state, but about three-quarters of MCO states directed at least 40% of total Medicaid dollars to payments to MCOs (Figure 3). State-to-state variation reflects many factors, including the proportion of the state Medicaid population enrolled in MCOs, the health profile of the Medicaid population, whether high-risk/high-cost beneficiaries (e.g., people with disabilities, dual-eligible beneficiaries) are included in or excluded from MCO enrollment, and whether long-term care services are included in MCO contracts. As states continue to expand Medicaid managed care to include higher-need, higher-cost beneficiaries, expensive long-term care, and adults eligible for Medicaid under the Affordable Care Act (ACA), the share of Medicaid dollars going to MCOs could continue to increase.

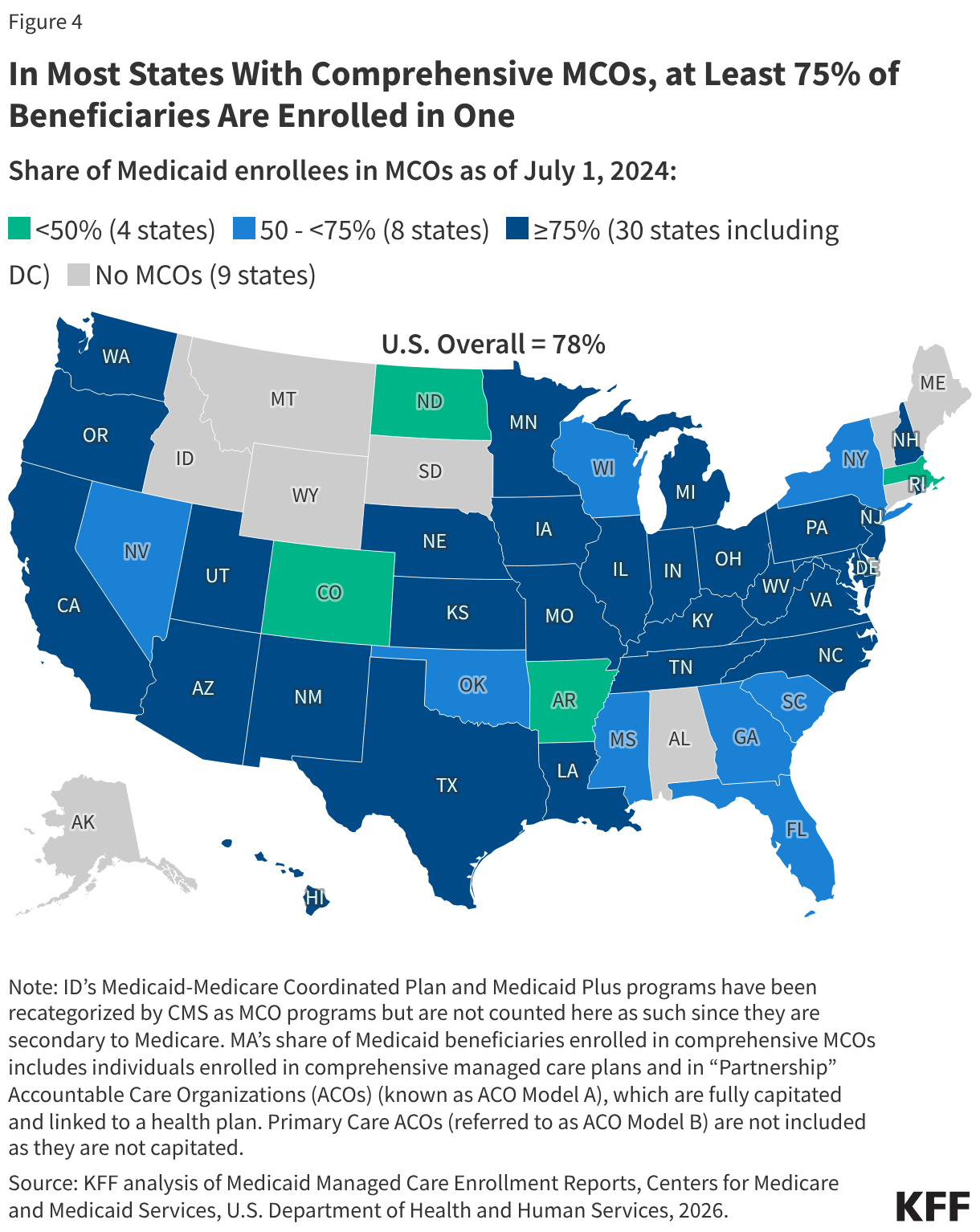

3. Over three-quarters (78%) of all Medicaid beneficiaries received their care through comprehensive risk-based MCOs.

As of July 1, 2024, over 66 million Medicaid enrollees, or 78% of all Medicaid enrollees, received their care through risk-based MCOs. Thirty MCO states covered at least 75% of Medicaid beneficiaries in MCOs (Figure 4).

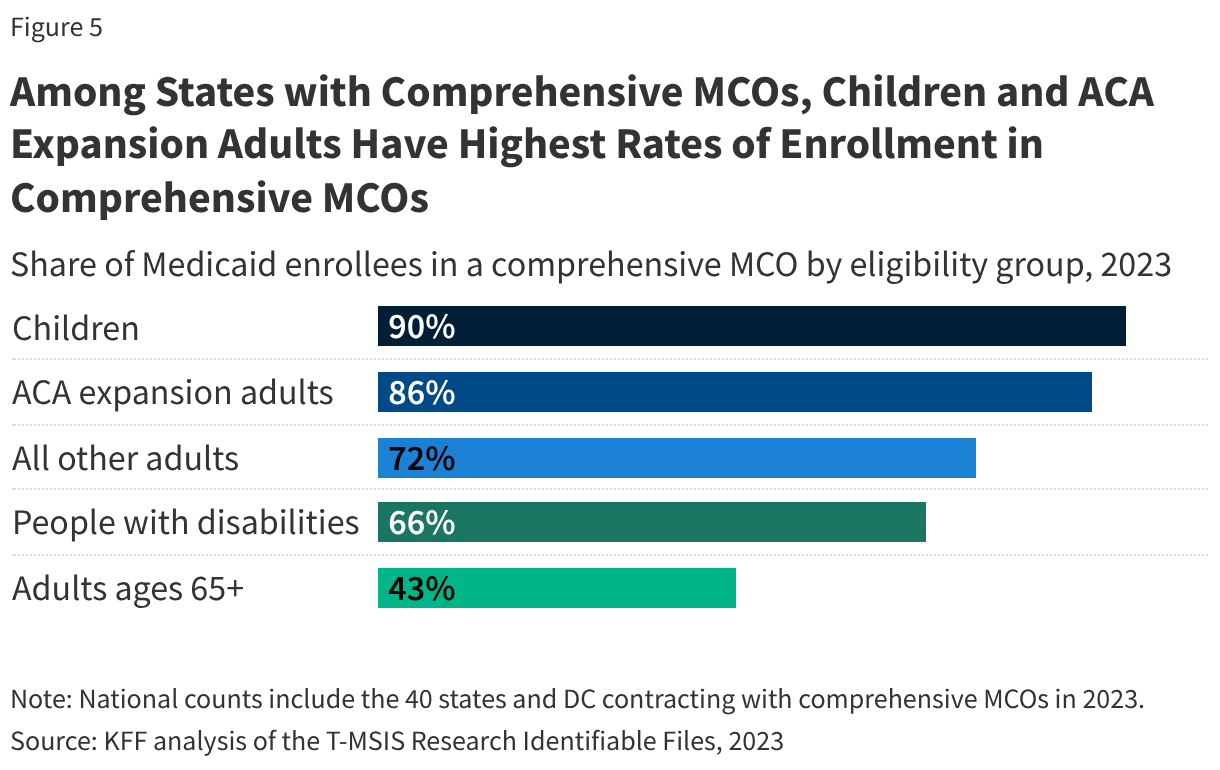

4. Children and adults are groups most likely to be enrolled in MCOs.

Among states that contract with comprehensive Medicaid MCOs, children and ACA expansion adults are the most likely to be enrolled in comprehensive MCOs (90% and 86%, respectively) (Figure 5). Nearly three quarters (72%) of “other adults” (e.g., parents and pregnant individuals) were enrolled in comprehensive MCOs (in 2023). People eligible for Medicaid through a disability pathway and adults ages 65+ are less likely to be enrolled in comprehensive MCOs, although states have been moving to include these groups in MCOs over time.

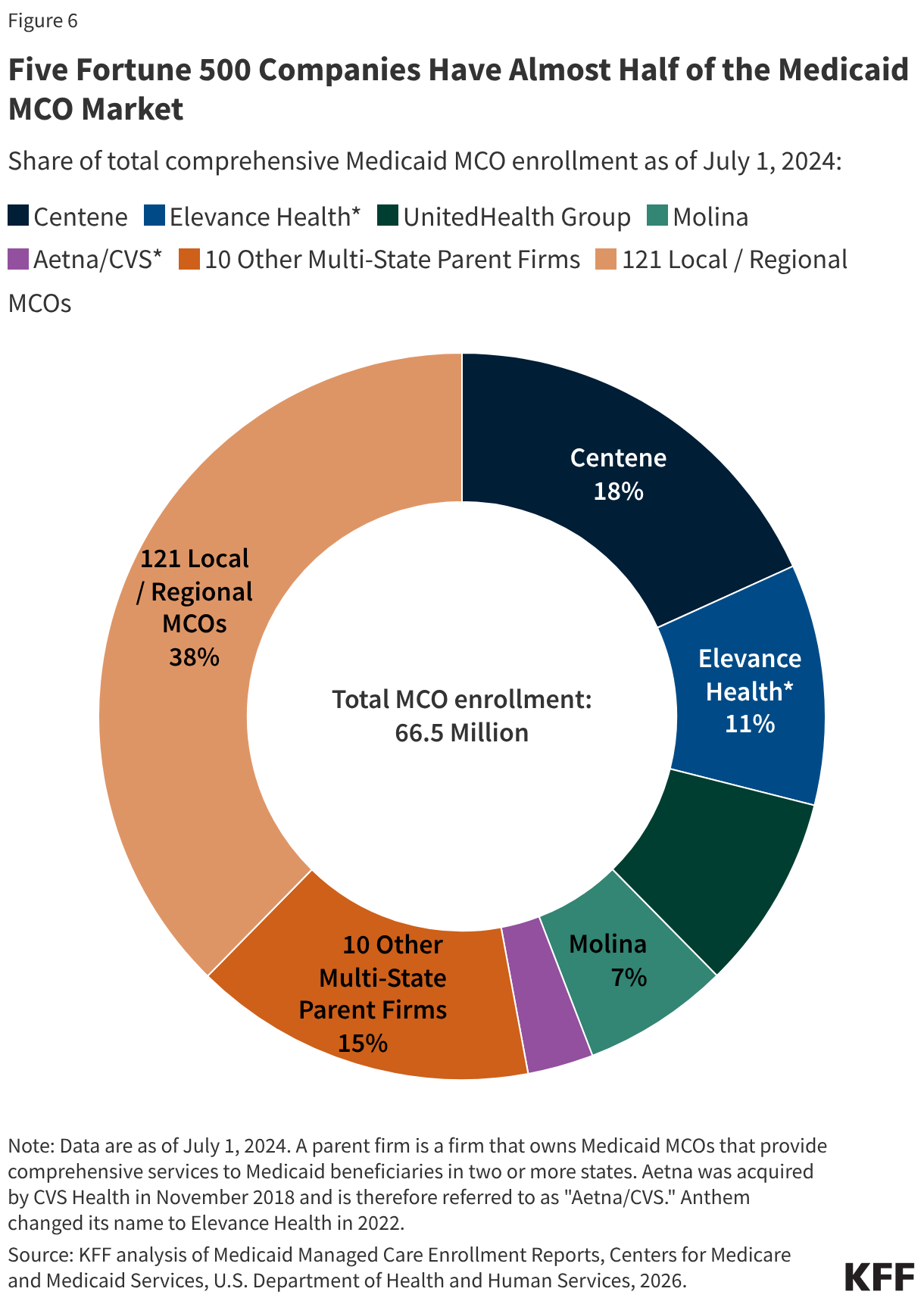

5. Five publicly traded firms account for almost half of MCO enrollment.

States contracted with a total of 291 Medicaid MCOs as of July 2024. MCOs represent a mix of private for-profit, private non-profit, and government plans. As of July 2024, a total of 15 firms operated Medicaid MCOs in two or more states (called “parent” firms), and these firms accounted for over 62% of enrollment in 2024 (Figure 6). Of the 15 parent firms, six are publicly traded, for-profit firms while the remaining nine are non-profit companies. Five firms – Centene, UnitedHealth Group, Elevance (formerly Anthem), Molina, and Aetna/CVS – account for 47% of all Medicaid MCO enrollment (Figure 6). All five are publicly traded companies ranked in the Fortune 500, and four are ranked in the top 100.

6. States make decisions about which services to carve in and out of MCO contracts.

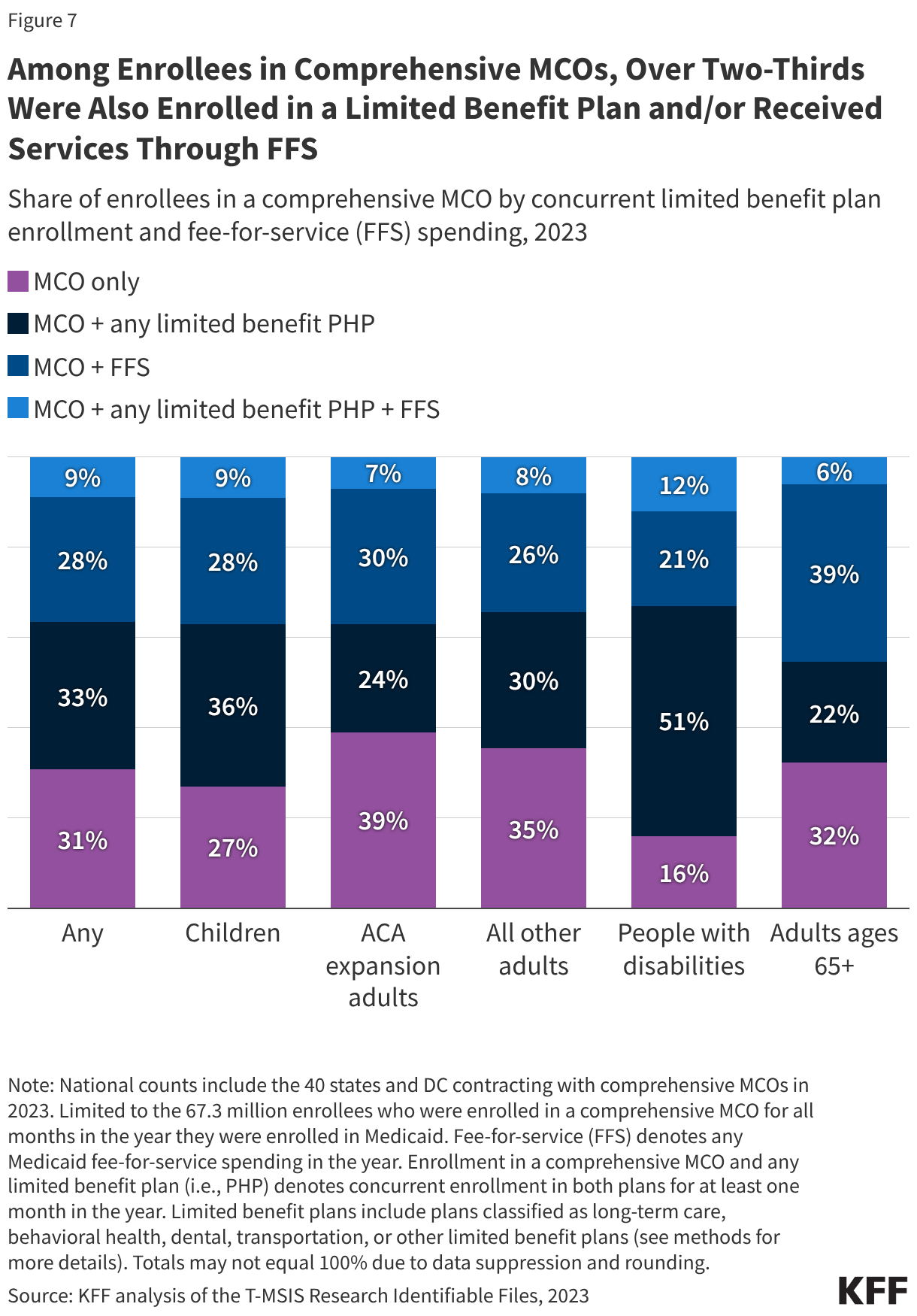

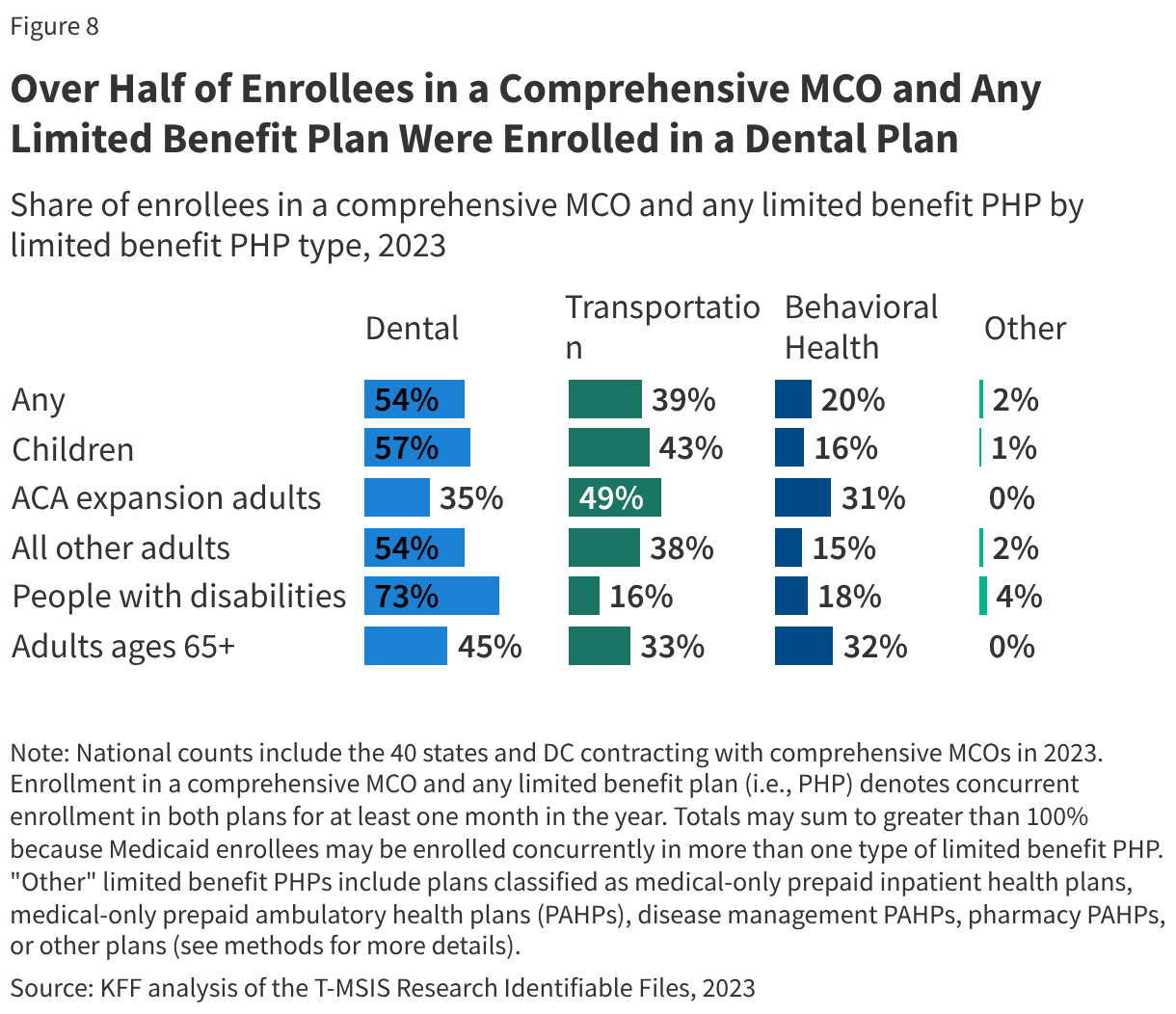

Although MCOs provide comprehensive services to beneficiaries, states may carve specific services out of MCO contracts to fee-for-service systems or limited benefit plans. Services frequently carved out include dental, non-emergency medical transportation (NEMT), and behavioral health. Among those enrolled in comprehensive MCOs, over two-thirds were also enrolled in at least one limited benefit prepaid health plan (PHP) and/or received fee-for-service (FFS) care outside of their MCO in 2023 (Figure 7). People with disabilities (enrolled in an MCO) are most likely to also be enrolled in a limited benefit plan(s) and/or receive FFS care. Individuals enrolled in multiple plans (i.e., MCO + limited benefit PHP(s)) or delivery systems (i.e., MCO + FFS) may have to juggle multiple complex systems, with differing rules. Among MCO enrollees also enrolled in at least one limited benefit plan, over half were enrolled in a dental plan (Figure 8). (Note that while EPSDT requires states to provide comprehensive dental services for children, dental benefits are optional for adults. State Medicaid programs are required to provide necessary transportation for enrollees to and from providers (referred to as “non-emergency medical transportation” or “NEMT”).)

7. Each year, states develop MCO capitation rates that must be actuarially sound and may include risk mitigation strategies.

MCOs are at financial risk for services covered under their contracts, receiving a per member per month “capitation” payment for these services. While plans set rates in the commercial and Medicare Advantage markets, Medicaid managed care rates are developed by states and their actuaries and reviewed and approved by CMS. Capitation rates must be actuarially sound6 and are applied prospectively, typically for a 12-month rating period, regardless of changes in health care costs or utilization. States may use a variety of risk mitigation tools to ensure payments are not too high or too low, including risk sharing arrangements, risk and acuity adjustments, or medical loss ratios (MLR) remittance requirements. States may also incorporate quality metrics into the ongoing monitoring of their programs, including linking financial incentives (e.g., performance bonuses or withholds) to quality measures.

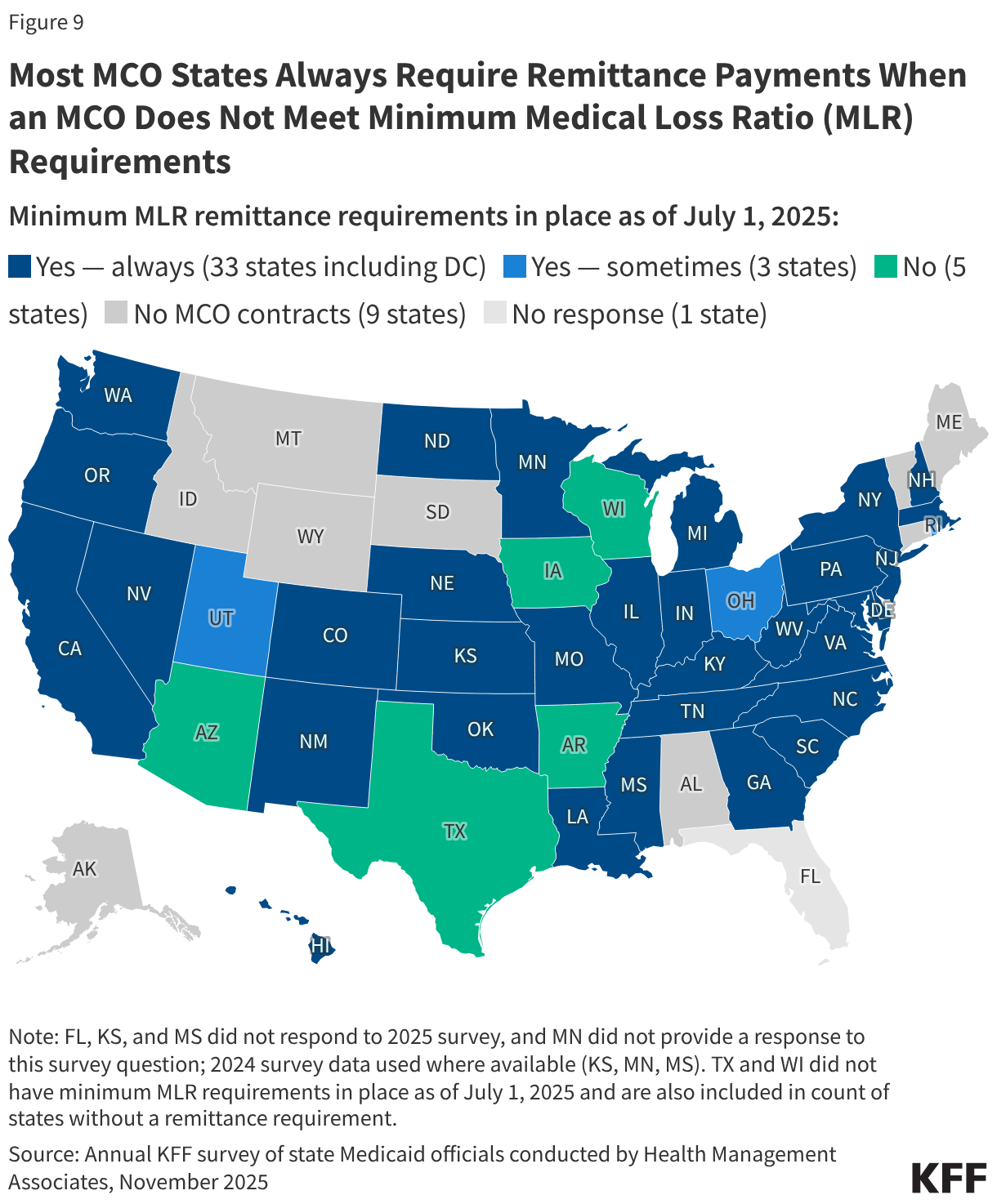

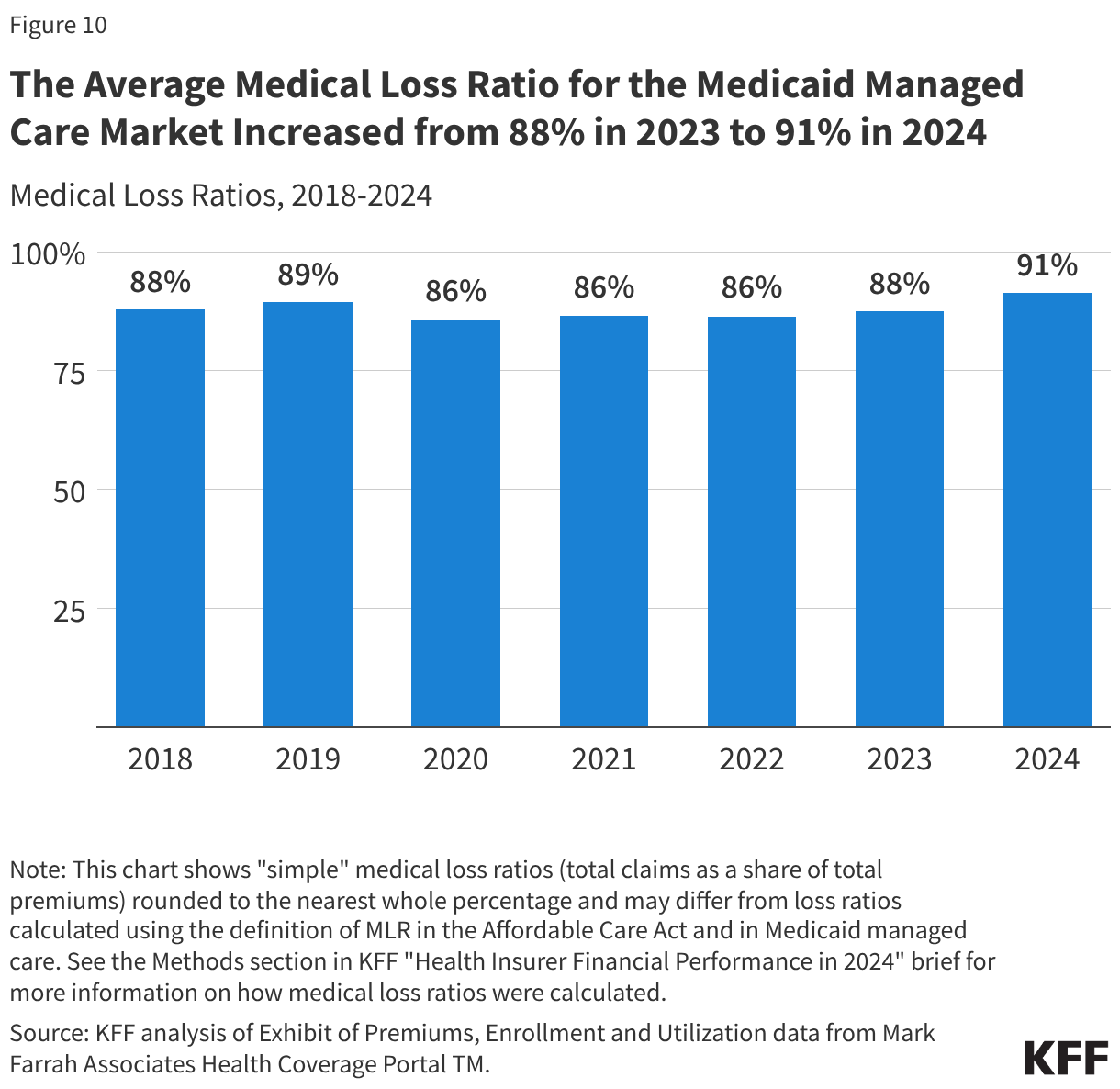

To limit the amount that plans can spend on administration and keep as profit, states are required to develop capitation rates for Medicaid to achieve an MLR of at least 85% in the rate year;7 however, there is no federal requirement for Medicaid plans to pay remittances to the state if they fail to meet the MLR standard.8 As of July 2025, 33 MCO states reported they always require remittance payments when an MCO does not meet state minimum MLR requirements, while three states indicated they sometimes require MCOs to pay remittances (Figure 9). Analysis of National Association of Insurance Commissioners (NAIC) data for the Medicaid managed care market show that average loss ratios (in aggregate across plans) increased from 88% in 2023 to 91% in 2024 (Figure 10) (the highest Medicaid managed care average loss ratio observed in the past decade – data not fully shown).

When significant enrollment, utilization, cost, and acuity changes began to emerge early in the COVID-19 public health emergency, CMS allowed states to modify managed care contracts, and many states implemented COVID-19 related “risk corridors” (where states and health plans agree to share profit or losses), allowing for the recoupment of funds. States and plans faced another period of heightened rate setting uncertainty when the continuous enrollment provision expired on March 31, 2023. During the “unwinding” of the pandemic-era Medicaid continuous enrollment provision, millions of people were disenrolled. Higher member risk and utilization patterns began to emerge by late 2023, and many states sought federal approval to adjust rates to address these shifts. The 2025 federal budget reconciliation law is expected to create rate setting challenges for states as the Medicaid provisions impacting enrollment and spending (e.g., work requirements, more frequent eligibility redeterminations, and provider tax and state directed payment (SDP) caps and reductions) roll out over the next several years.

8. Changes to federal state directed payment rules may impact provider payments.

States are generally prohibited from contractually directing how a managed care plan pays its providers.9 Subject to CMS approval, however, states may implement certain “state directed payments” (SDPs) that require managed care plans to adopt minimum or maximum provider payment fee schedules, provide uniform dollar or percentage increases to providers (above base payment rates), or implement value-based payment (VBP) arrangements.10,11,12 Many states that contract with MCOs use SDPs to make uniform rate increases that are like FFS supplemental payments. Since SDPs were introduced in 2016, they have become a core component of reimbursement for many providers. Significant changes to state directed payment rules recently enacted through the 2025 federal budget reconciliation law and through the 2024 CMS Managed Care rule are expected to affect Medicaid provider payment rates.

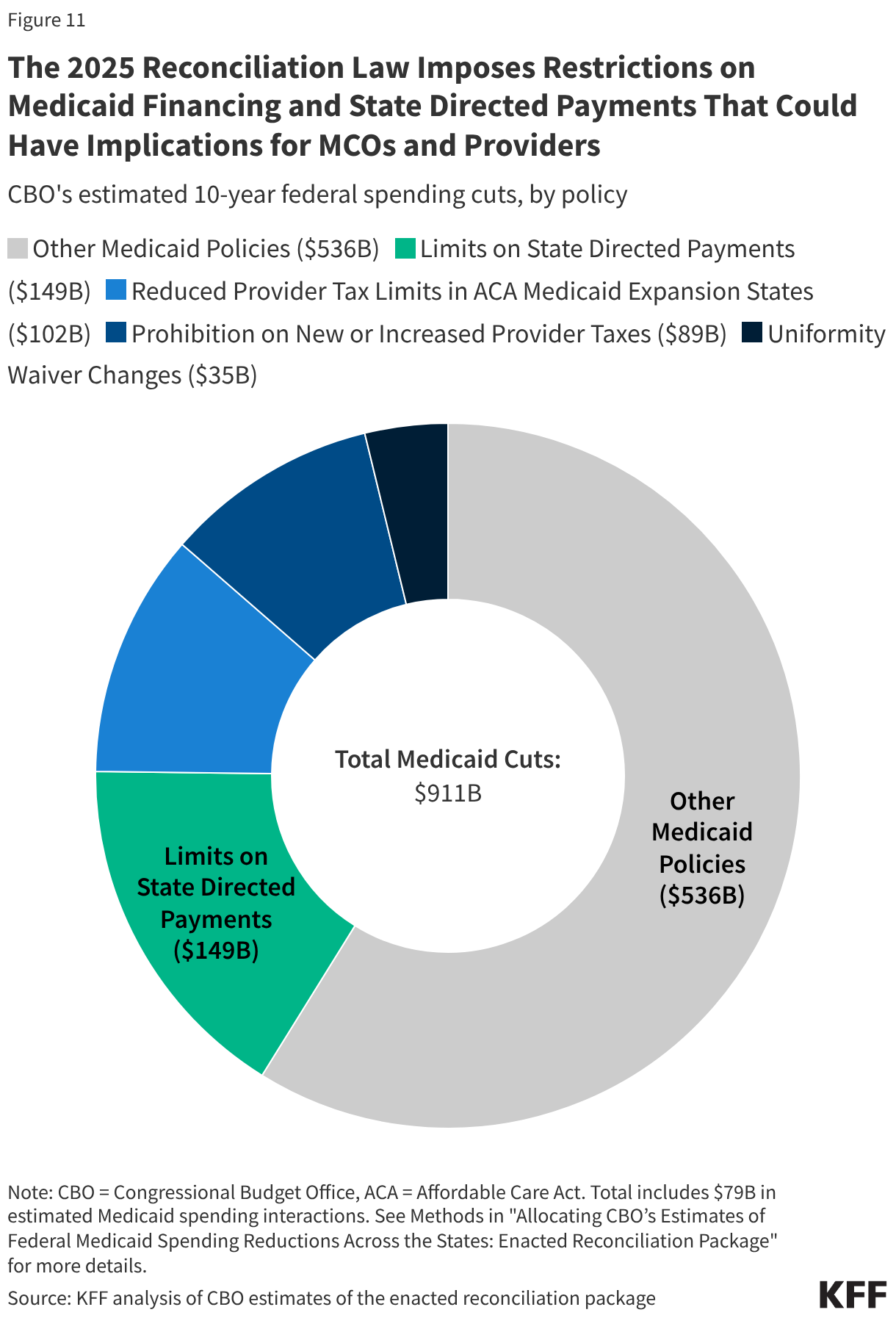

The reconciliation law directs HHS to revise SDP regulations to cap the total payment rate for inpatient and outpatient hospital services, nursing facility services, and professional services at academic medical centers at 100% of the total published Medicare payment rate for states that have adopted the Medicaid expansion and at 110%13 of the total published Medicare payment rate for states that have not adopted the expansion. (Under previous rules, payments were capped at 100% of average commercial rates.14) Certain SDPs are initially grandfathered15 but will be reduced by ten percentage points each year (starting January 1, 2028) until they reach the allowable Medicare-related payment limit. The Congressional Budget Office (CBO) estimated revising the payment limit for state directed payments will result in $149 billion in federal savings over ten years (Figure 11). The 2025 reconciliation law also imposes significant new restrictions on states’ ability to generate Medicaid provider tax revenue, estimated to result in $226 billion in federal savings (Figure 11). In KFF’s 2025 Medicaid budget survey, states noted the new provider tax changes could result in significant state budget impacts as well as reductions in provider payment rates and state directed payments, which are often funded by provider taxes.

In addition to the 2025 reconciliation law changes, beginning in July 2027, the 2024 Medicaid Managed Care rule requires states to incorporate all SDPs through capitation rate setting adjustments instead of using “separate payment terms,” which provide payments outside of base capitation rates.16 The change moves these payments from predictable, separate payments to more complex, risk-based arrangements, which may reduce states’ ability to target reimbursement for specific provider types. CMS eliminated separate payment terms due to concerns that these separate payments undermine the risk-based nature of managed care and are frequently driven by the financing of the non-federal share. MACPAC analysis found that over half of SDP arrangements approved between February 2023 and August 2024 were incorporated through separate payment terms.

9. CMS finalized rules to strengthen access standards, but the future of the rules is uncertain.

In 2024, the Biden administration finalized major Medicaid regulations designed to promote quality of care and advance access to care for Medicaid enrollees. The Managed Care rule strengthens standards for timely access to care, including through the establishment of national maximum wait time standards for certain “routine” appointments, and states’ monitoring and enforcement efforts. These rules are complex and set to be implemented over several years. It remains uncertain whether the Trump administration will seek to roll back or revise provisions included in the 2024 managed care final rules.

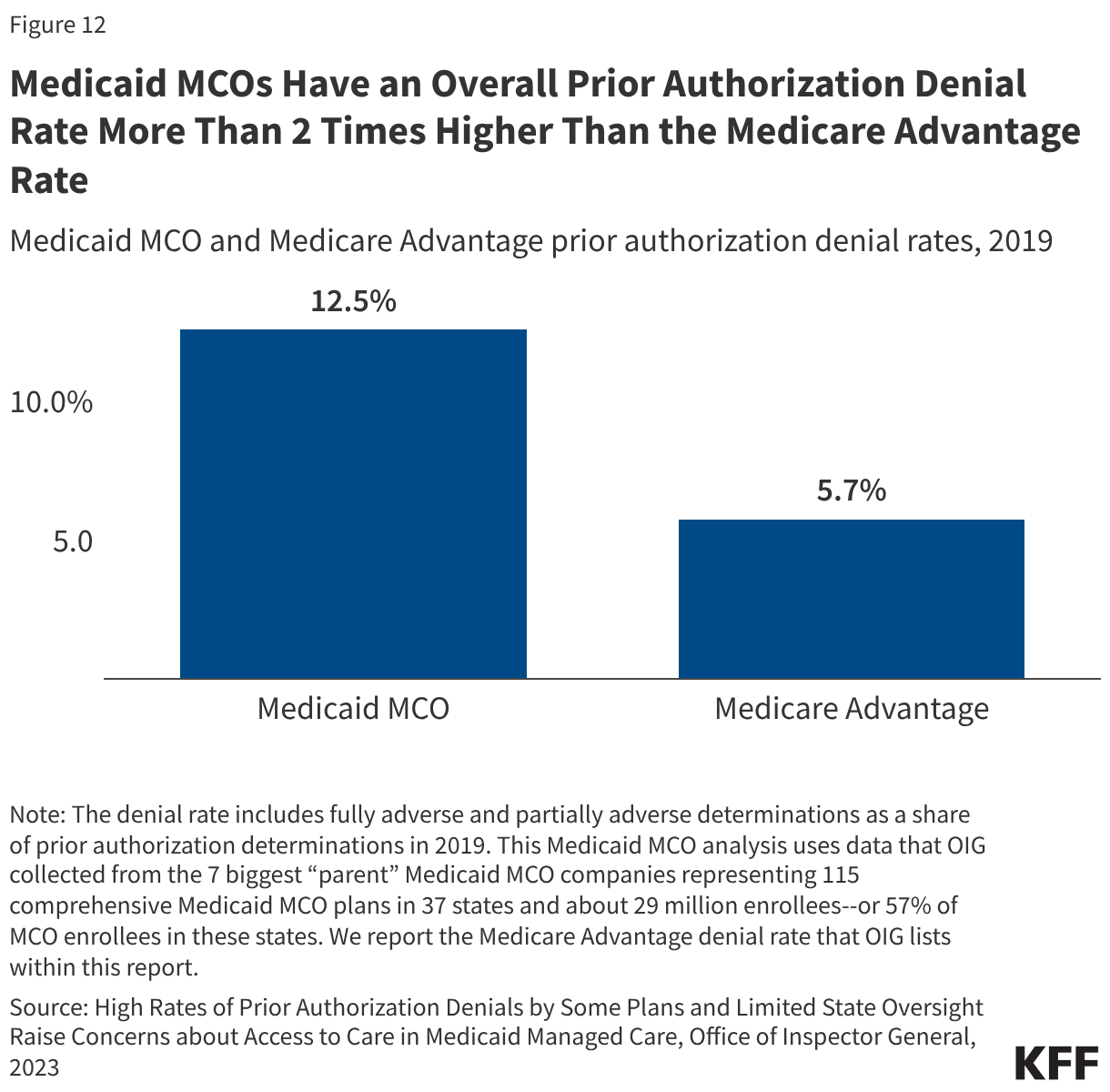

In 2024, CMS also finalized a rule focused on improving the prior authorization process including reducing approval wait times and improving transparency. A July 2023 OIG report found that Medicaid MCOs had an overall prior authorization denial rate of 12.5%–more than 2 times higher than the Medicare Advantage rate (Figure 12), raising concerns about prior authorization and access in Medicaid managed care. OIG recommendations (to CMS) included strengthening state monitoring of denials and appeals. MACPAC has highlighted similar concerns, making recommendations in the March 2024 Report to Congress focused on improving the appeals process and enhancing monitoring and oversight of MCOs. Beginning in June 2026, states will be required to report plan-level prior authorization data to CMS, including the total number prior authorization requests, denial and approval rates, the percentage of standard prior authorization requests that were approved after appeal, and average and median decision times as part of managed care annual program reports (see additional discussion below).

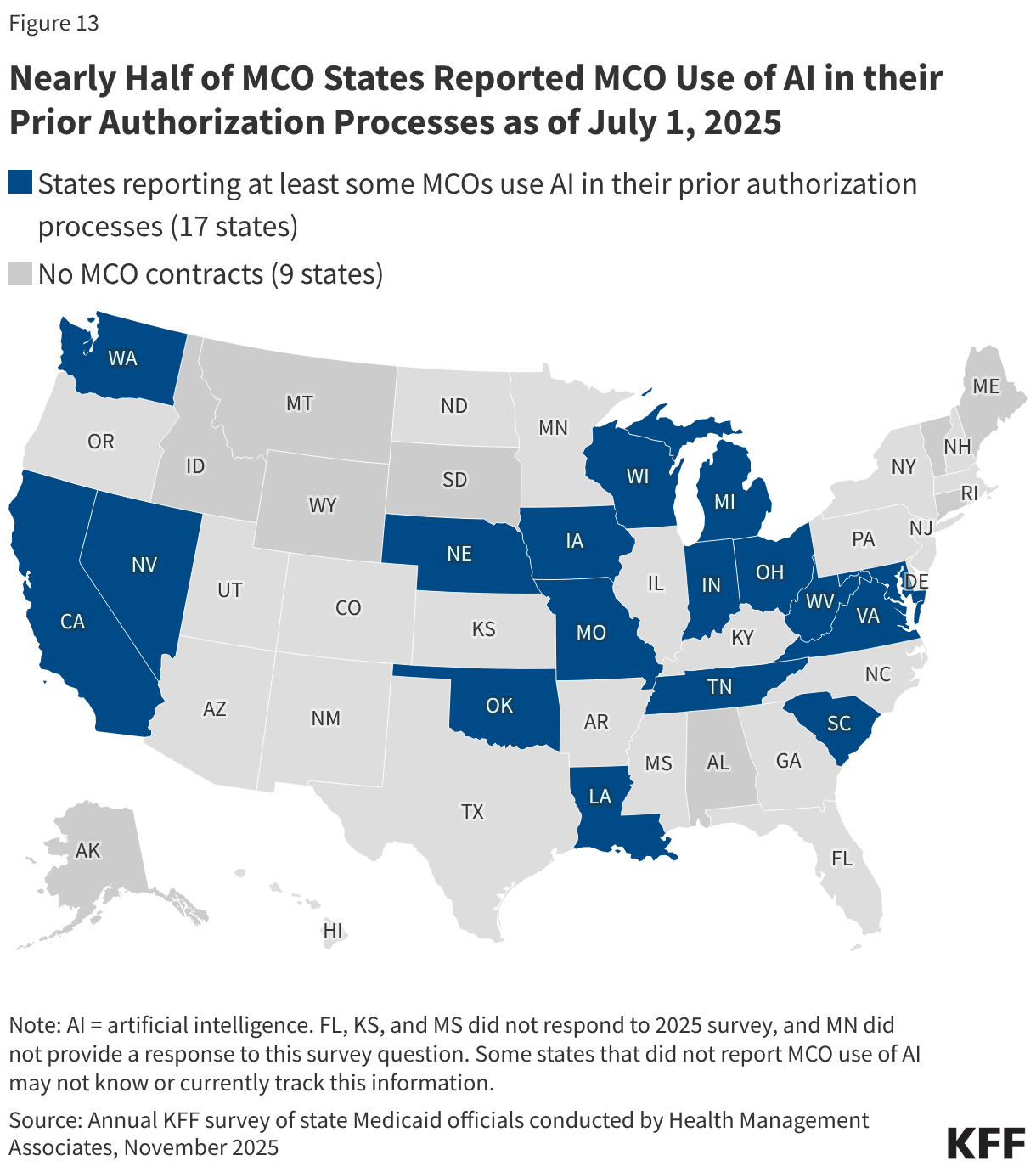

While health insurers are increasingly using AI to automate parts of the prior authorization process, there is limited information available about its use and impact within Medicaid managed care. MACPAC found that while there are potential benefits of automation in prior authorization such as administrative efficiencies and faster processing times, it may also pose potential risks or challenges depending on how it is administered and monitored. In the absence of comprehensive federal policy governing AI use and oversight in prior authorization, some states have taken steps to regulate or monitor use of AI by health plans. A 2025 KFF survey of state Medicaid directors found less than one-quarter of states reported requiring MCOs to disclose the use of AI in prior authorization processes as of July 1, 2025, although nearly half of MCO states reported knowledge of at least some of their contracted MCOs using AI in their prior authorization processes (Figure 13). Several states reported implementing new or expanded oversight activities or adopting other safeguards in FY 2025 or 2026 to support appropriate use of AI in MCO prior authorization processes.

10. In recent years, CMS has taken steps to improve managed care program monitoring and transparency.

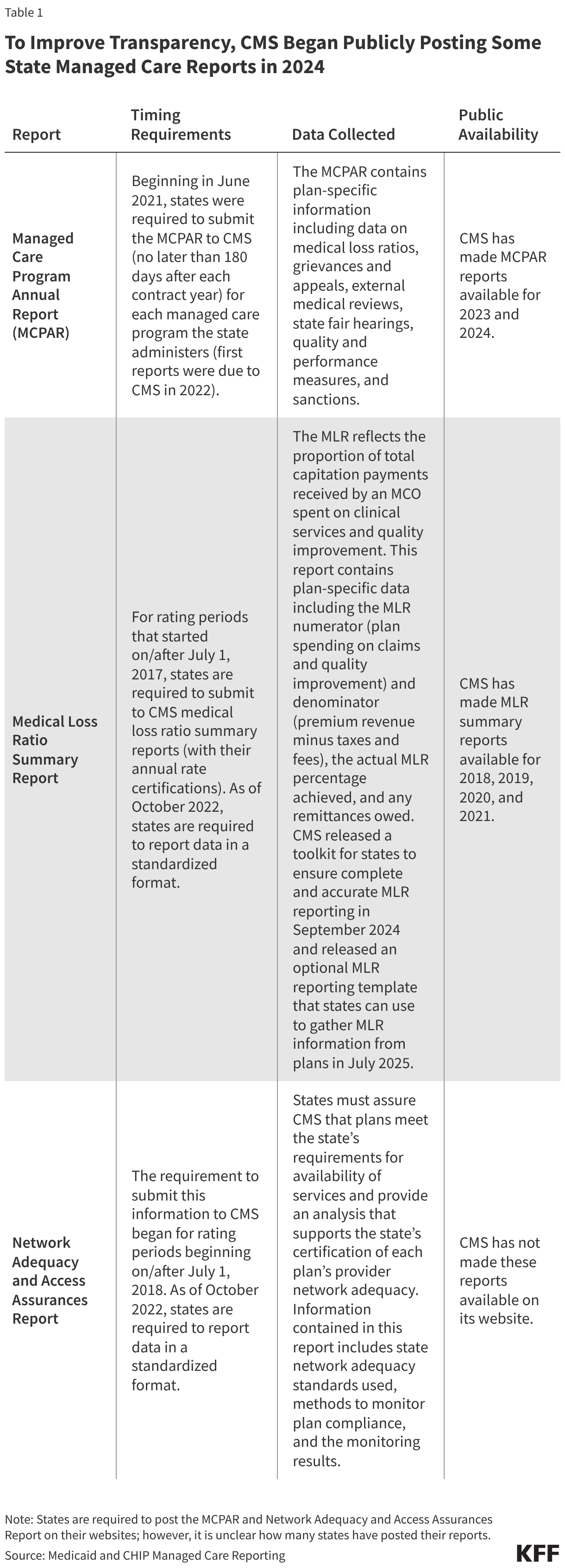

The 2016 Medicaid managed care final rule created new managed care reporting requirements for states. CMS, under the Biden administration, developed standard reporting templates (Table 1) and a variety of toolkits and released a series of informational bulletins (2021, 2022, 2023, 2024) to help states improve their monitoring and oversight of managed care programs. Transparency has the potential to promote accountability. To improve transparency, CMS began publicly posting the Managed Care Program Annual Report (MCPAR) and the MLR Summary Reports on Medicaid.gov in 2024. Posting data relating to the performance of individual MCOs may allow for comparison within and across states. However, limitations and challenges may exist.

Managed care rules finalized in 2024 include provisions aimed at further strengthening managed care transparency and monitoring, though the fate of these rules remains uncertain. In March 2026, the Trump administration released an informational bulletin to aid states’ monitoring and oversight of managed care. CMS indicated it has implemented managed care oversight reviews that will leverage data collected from standardized reporting tools (e.g., MCPARs, network adequacy and access reports, and MLR summary reports). While CMS has continued to post state-submitted MCPAR and MLR summary reports on Medicaid.gov, it has also updated MCPAR requirements to remove certain questions related to access and network adequacy and plan-level MLR percentage reporting. These changes were introduced to reduce state burden and duplication with the separate network adequacy and access report and the MLR summary report; however, removing certain access and network adequacy questions may also reduce transparency as state network adequacy and access reports are not currently posted on Medicaid.gov. While the MLR Summary Reports are posted on Medicaid.gov, in the future, individuals will need to access the MLR Summary Reports separately to obtain plan-level MLR reporting information (as it will no longer be available in MCPAR reports).

This work was supported in part by Arnold Ventures. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

Methods

Medicaid Managed Care Plan Enrollment by Eligibility Group

This section provides information on the methods used in the analysis of Medicaid managed care plan enrollment by eligibility group (Figures 5, 7, and 8).

Data: This analysis uses data available from the 2023 T-MSIS Research Identifiable Demographic-Eligibility and Claims Files to identify enrollment in Medicaid managed care plans.

Medicaid enrollee inclusion criteria: Individuals were included if they had at least one month of Medicaid enrollment in 2023. This analysis identified Medicaid enrollment in a month (MM) in 2023 when CHIP_CD_01- CHIP_CD_12 equals 1 or, if missing CHIP_CD, when ELGBLTY_GRP_CD_01- ELGBLTY_GRP_CD_12 equals 1-60 or 69-75. Eligibility groups are defined using the most recent non-missing eligibility group in the calendar year (ELGBLTY_GRP_CD_LTST) and a person’s age as follows:

- Seniors: Enrollees age 65 and older.

- People with Disabilities: Enrollees under age 65 who are reported as eligible because of disability.

- Adults: Enrollees ages 19 to 64 who are not eligible because of disability or newly eligible for Medicaid by the ACA Medicaid expansion.

- Children: Enrollees ages 18 and younger who are not eligible because of disability.

- ACA Expansion Adults: Enrollees ages 19 to 64 who were made newly eligible for Medicaid by the ACA Medicaid expansion.

State inclusion criteria: To assess the usability of states’ data, the analysis examined quality assessments from the DQ Atlas for enrollment in managed care and payments to comprehensive managed care plans and compared enrollment in comprehensive managed care with the Medicaid Managed care enrollment report:

- This analysis excluded 10 states with no comprehensive Medicaid managed care plans in 2023 (Alabama, Alaska, Connecticut, Idaho, Maine, Montana, Oklahoma, South Dakota, Vermont, and Wyoming).

- Among states with Medicaid managed care, the analysis excluded states that had both a “Unclassified/ Unusable” DQ Atlas assessment and more than 50% difference between the number of individuals enrolled in managed care in T-MSIS and the number reported in the Medicaid managed care enrollment report.

- No states were excluded based on those criteria in 2023, leaving the other 40 states and D.C. (hereafter, treated as a state) which contract with comprehensive MCOs in the main analysis. Enrollees were assigned a state based on their T-MSIS STATE_CD.

Identifying enrollment in Medicaid managed care plans: To determine enrollment in plans in 2023, individuals were assigned as enrolled in any plans from the list MC_PLAN_ID_01_MM-MC_PLAN_ID_16_MM from the Managed Care Participation segment of the T-MSIS eligibility file. To determine enrollment in comprehensive MCOs, enrollment was limited to plans from the list MC_PLAN_ID_01_MM-MC_PLAN_ID_16_MM from the Managed Care Participation segment of the T-MSIS eligibility file which also have a positive capitated payment to a plan on behalf of the enrollee in the month (MM) in the T-MSIS Other Services (OT) file. This analysis calculated positive capitated payment to a plan on behalf of the enrollee in a month by summing the MDCD_PD_AMT for claims with CLM_TYPE_CD equal to ”2” (Medicaid or Medicaid-expansion Capitated Payment) having a SRVC_END_DT in the month in 2023. Capitated payments were attributed to a specific plan using the MC_PLAN_ID from the OT file.

Identifying Medicaid managed care plan types: This analysis used the Managed Care Participation segment of the T-MSIS eligibility file to map each plan as identified by its MC_PLAN_ID and STATE_CD to its plan type using the associated MC_PLAN_TYPE_CD. In cases where the plan as identified by MC_PLAN_ID and STATE_CD had more than one associated MC_PLAN_TYPE_CD in the Managed Care Participation segment of the T-MSIS eligibility file, the MC_PLAN_TYPE_CD with the largest number of enrollees in that plan was selected. This virtually always matches the MC_PLAN_TYPE_CD from the TAF Annual Managed Care Plan (APL).

KFF created indicator variables to assign the more detailed plan types into the following larger categories. Note that plan types are not mutually exclusive. For example, while there are no plans in 2023 have a MC_PLAN_TYPE_CD of 19 (Individual is enrolled in Long-Term Services and Supports (LTSS) and Mental Health (MH) PIHP), plans of this plan type would fall under both behavioral health and long-term care. KFF grouped the more detailed plan types into the following larger categories:

- Comprehensive managed care: having a MC_PLAN_TYPE_CD with values of 01 (Comprehensive managed care) or 04 (Health Insuring Organization).

- Program of All-Inclusive Care for the Elderly (PACE): having a MC_PLAN_TYPE_CD with values of 17 (PACE).

- Long-term care: having a MC_PLAN_TYPE_CD with values of 07 (Long Term Care Services and Supports (LTSS) PIHP) or 19 (Individual is enrolled in Long-Term Services and Supports (LTSS) and Mental Health (MH) PIHP).

- Behavioral health: having a MC_PLAN_TYPE_CD with values of 08 (Mental Health (MH) PIHP), 09 (Mental Health (MH) PAHP), 10 (Substance Use Disorders (SUD) PIHP), 11 (Substance Use Disorders (SUD) PAHP), 12 (Mental Health (MH) and Substance Use Disorders (SUD) PIHP), 13 (Mental Health (MH) and Substance Use Disorders (SUD) PAHP), or 19 (Individual is enrolled in Long-Term Services and Supports (LTSS) and Mental Health (MH) PIHP).

- Dental: having a MC_PLAN_TYPE_CD with values of 14 (Dental PAHP).

- Transportation: having a MC_PLAN_TYPE_CD with values of 15 (Transportation PAHP).

- Other limited benefit: having a MC_PLAN_TYPE_CD with values of 05 (Medical-only Prepaid Inpatient Health Plan (PIHP)), 06 (Medical-only Prepaid Ambulatory Health Plan (PAHP)), 16 (Disease Management PAHP), 18 (Pharmacy PAHP), or 20 (Other).

- Any limited benefit: having a MC_PLAN_TYPE_CD with values defined above as long-term care, behavioral health, dental, transportation, or other limited benefit.

- Primary care case management (PCCM): having a MC_PLAN_TYPE_CD with values of 02 (Traditional Primary Care Case Management (PCCM) Provider arrangement), or 03 (Enhanced PCCM Provider arrangement).

Managed long-term care (LTC) limited benefit plans: Using the definitions above, in 2023, virtually zero enrollees in long-term care limited benefit plans were concurrently enrolled in a comprehensive MCO. The likely reason there are no enrollees in comprehensive MCOs and limited benefit LTC plans is that most enrollees in limited benefit LTC plans also have Medicare. For such people (“dual-eligible individuals”), Medicaid covers medical acute and post-acute care, including skilled nursing facility services and home health care. Medicaid wraps around Medicare coverage by paying Medicare premiums and in most cases, cost sharing. Most people with Medicare and Medicaid (“dual-eligible individuals”) also are eligible for Medicaid benefits that are not otherwise covered by Medicare, including long-term care, vision, and dental. It is unlikely that many dual-eligible individuals who are enrolled in LTC plans would also use many benefits provided through a comprehensive MCO.

Endnotes

- PCCM is a managed fee-for-service (FFS) based system in which beneficiaries are enrolled with a primary care provider who is paid a small monthly fee to provide case management services in addition to primary care. ↩︎

- While MCOs are the predominant form of Medicaid managed care, millions of other beneficiaries receive at least some Medicaid services, such as behavioral health or dental care, through limited-benefit risk-based plans, known as prepaid inpatient health plans (PIHPs) and prepaid ambulatory health plans (PAHPs). ↩︎

- Sparer M. 2012. Medicaid managed care: costs, access, and quality of care. Res. Synth. Rep. 23, Robert Wood Johnson Found., Princeton, NJ ↩︎

- Daniel Franco Montoya, Puneet Kaur Chehal, and E. Kathleen Adams, “Medicaid Managed Care’s Effects on Costs, Access, and Quality: An Update,” Annual Review of Public Health 41:1 (2020):537-549 ↩︎

- Medicaid and CHIP Payment and Access Commission (MACPAC), “Managed care’s effect on outcomes,” (Washington, DC: MACPAC, 2018), https://www.macpac.gov/subtopic/managed-cares-effect-on-outcomes/ ↩︎

- Federal regulations require actuarially sound capitation rates that are “projected to provide for all reasonable, appropriate, and attainable costs that are required under the terms of the contract and for the operation of the MCO, PIHP, or PAHP for the time period and the population covered under the terms of the contract . . .” 42 CFR §438.4(a) ↩︎

- The 85% minimum MLR is the same standard that applies to Medicare Advantage and private large group plans. ↩︎

- The 2024 Consolidated Appropriations Act included a financial incentive to encourage certain states to collect remittances from Medicaid MCOs that do not meet minimum MLR requirements. ↩︎

- 42 CFR Sections 438.6(c) and 438.60. ↩︎

- Permissible under 42 CFR Section 438.6(c). ↩︎

- In creating state directed payments (in 2016), CMS aimed to help states ensure access to adequate provider networks and to increase use of VBP arrangements. ↩︎

- State directed payments must meet federal requirements (e.g., must be tied to utilization and delivery of services, be distributed equally to specified providers, and not be conditioned on participation in intergovernmental transfer (IGT) agreements) (42 CFR §438.6(c)). ↩︎

- For states that newly adopt the ACA Medicaid expansion after enactment, the cap at 100% of the Medicare payment rate applies at the time coverage is implemented even for SDPs that had prior approval. ↩︎

- The managed care rules finalized in 2024 permitted states to pay hospitals and nursing facilities at the average commercial payment rate (ACR) when using directed payments, (higher than the Medicare payment ceiling used for other Medicaid FFS supplemental payments). ↩︎

- Specifies that the grandfathering clause only applies to SDPs in rating periods occurring 180 business days before or after enactment of the bill (July 4, 2025) and that (1) for rural hospitals, states received approval or made a “good faith effort” to receive approval prior to enactment of the bill; (2) for all other providers, states received approval or made a “good faith effort” to receive approval prior to May 1, 2025; or (3) states applied for approval prior to enactment of the bill. ↩︎

- “Separate payment terms are a type of payment method that provides a fixed amount of directed payment funding outside of the base capitation rate. States often use separate payment terms to make large uniform rate increases…Under the 2024 managed care rule, separate payment terms will be eliminated effective for the first rating period beginning on or after July 9, 2027, and all directed payment arrangements will henceforth be required to be incorporated through capitation rate adjustments. CMS eliminated separate payment terms due to concerns that payment streams separate from capitation rates undermine the risk-based nature of managed care and are often driven by the underlying financing of the non-federal share.” Medicaid and CHIP Payment And Access Commission, “Directed Payments in Medicaid Managed Care,” October 2024 Issue Brief, p.6, https://www.macpac.gov/wp-content/uploads/2024/10/Directed-Payments-in-Medicaid-Managed-Care.pdf. ↩︎