Medicaid and State Financing: What to Watch in Upcoming State Budget Debates

Note: To learn how how state fiscal conditions could affect state budget debates and Medicaid policy changes in 2026, read our latest issue brief.

State legislatures are currently gathering to develop new budgets for state fiscal year (FY) 2025. Heading into this budget cycle, state fiscal conditions are shifting, with state revenues starting to decline following steep revenue growth during the pandemic. While states reported favorable fiscal conditions in KFF’s recent budget survey, they noted uncertainty in their fiscal outlooks in the years ahead. At the same time, federal pandemic-era supports to state financing are expiring, requiring adjustments to state spending to maintain balanced budgets. Even though national economic indicators remain strong, pandemic-related supports for households have also expired and families are still struggling to cover costs from record inflation during the pandemic. This will all affect the development of state budgets going forward, including for Medicaid programs which are a large expenditure item as well as revenue source for states.

This issue brief examines trends in state fiscal conditions and discusses how state budgets and macroeconomic conditions may affect individuals and state Medicaid programs. Thirty-three states and DC will be adopting FY 2025 budgets this year; the other 17 states enacted biennial budgets last year, though some of these states may adopt a supplemental budget for FY 2025. The state budget cycle in most states runs from July to June, and Governor’s typically release their budget proposals by January followed by a convening of the legislature to finalize and enact a budget.

What are state fiscal conditions in FY 2024 and looking ahead to FY 2025?

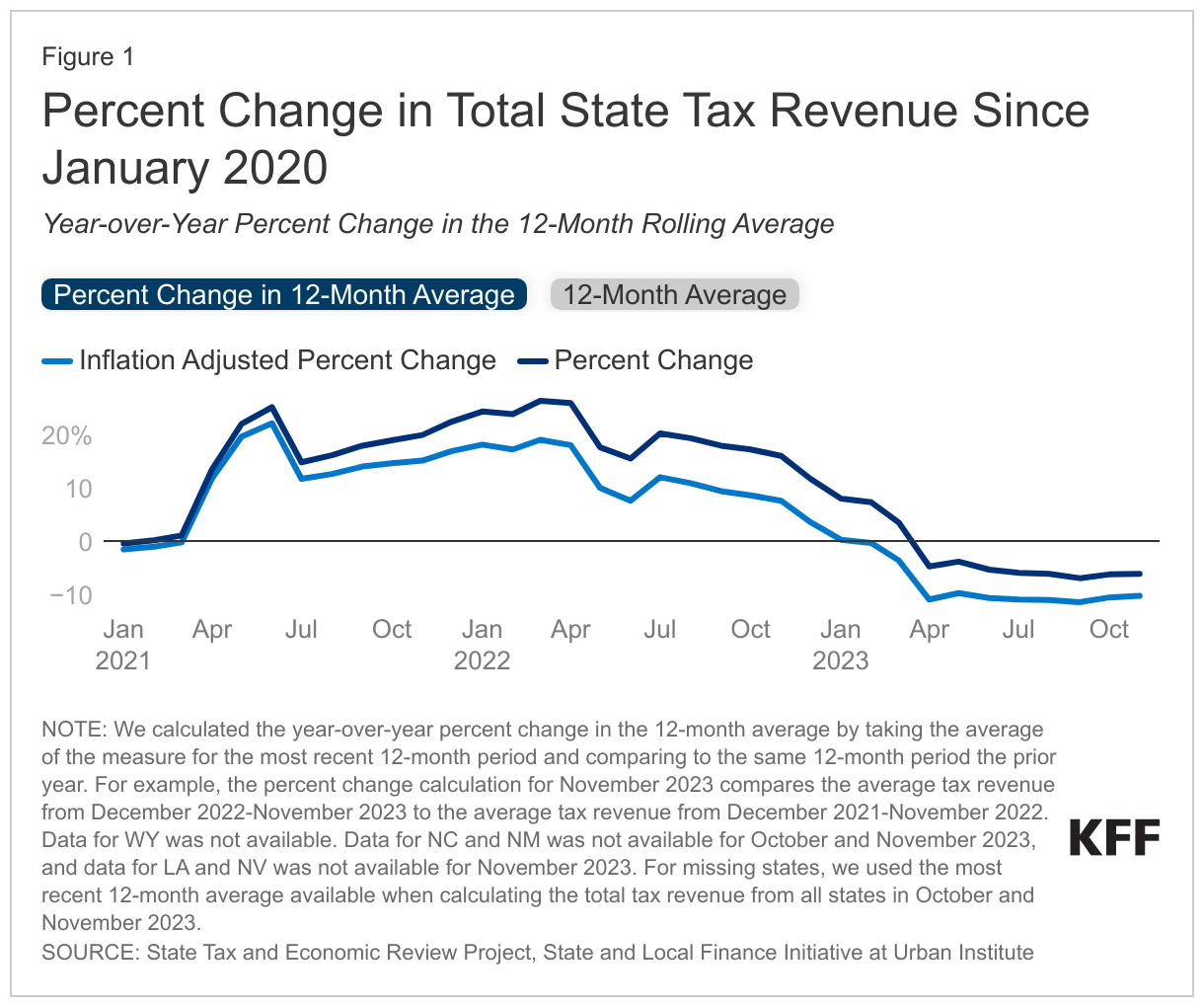

State tax revenues are beginning to decline following years of strong growth (Figure 1). Most states saw strong revenue collections in FY 2021 and FY 2022, with revenue growth in the double digits collectively across states. Many states took the opportunity to make one time investments, enact tax cuts, build reserves, and pay down debts, with rainy day funds reaching historic levels. These favorable state fiscal conditions, combined with federal fiscal relief, mitigated the need for the widespread state spending cuts that occurred in prior recessions. While revenues remained higher than pre-pandemic levels as of November 2023, revenue growth has slowed and started to decline as a result of a number of factors, including state tax cuts. Although there was variation across revenue type and across states, changes in large states like California and New York have a substantial impact on the overall changes.

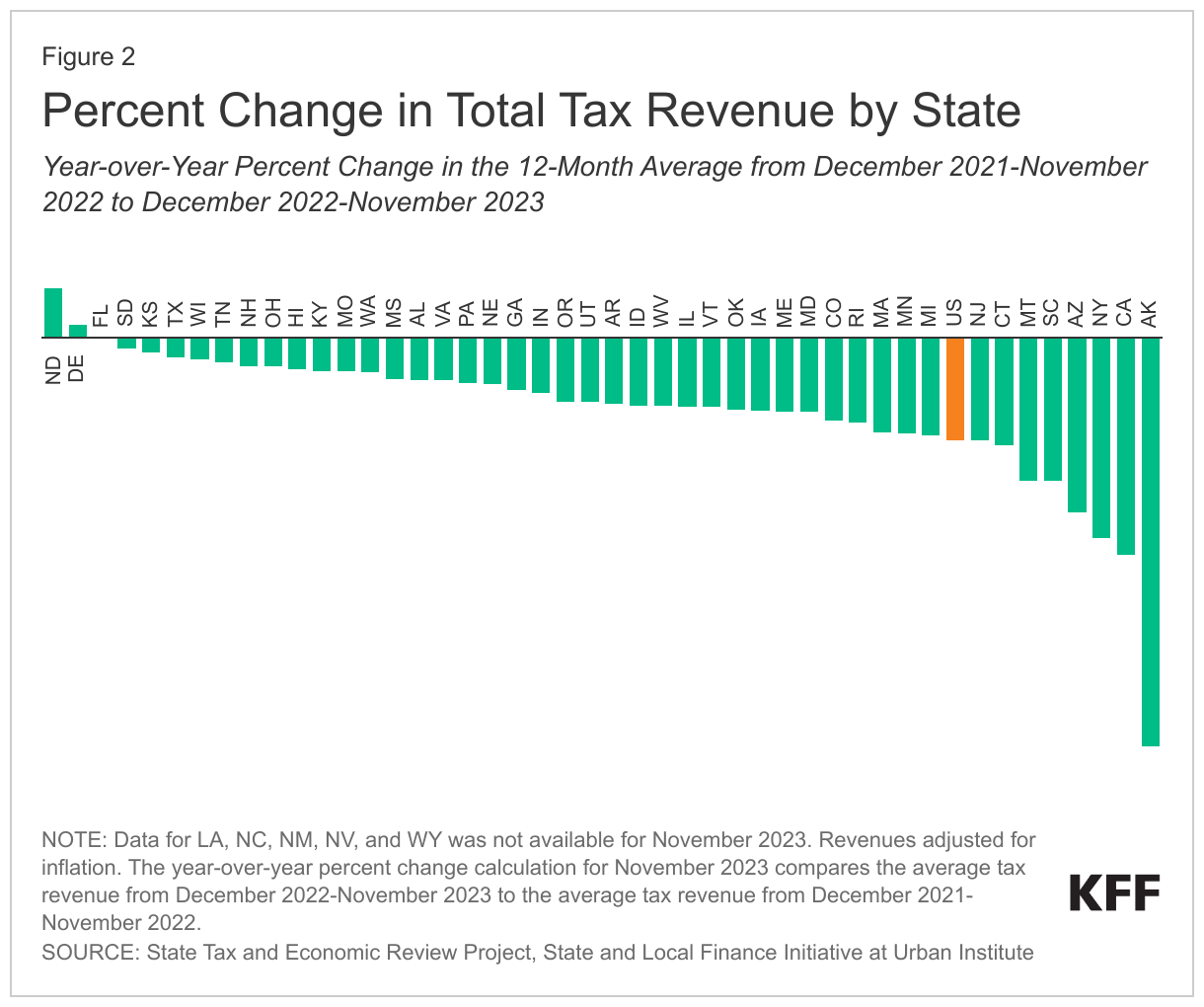

State revenue changes vary across states and revenue sources depending on state policy decisions and state characteristics such as tax structure and industry reliance. Almost all states with available data saw a decline in their average total tax revenue for the most recent 12 months (December 2022-November 2023) compared to the 12 months prior, though the declines ranged widely from -0.1% in Florida to -40.7% in Alaska (Figure 2). States are also experiencing revenue declines across all tax revenue types, including personal income tax, corporate income tax, and sales tax, though personal income taxes have seen the largest decline. This is largely attributable to state income tax rate cuts, as well as stock market losses in 2022 (though the market rebounded in 2023). Revenue from capital gains taxes have also declined and there has been a reduction in initial public offerings in states like California. Thirty states made cuts to income taxes in 2022 or 2023, and additional states provided other temporary tax relief such as tax credits, tax holidays, or rebates. Sales tax revenues are also weakening as consumer patterns have shifted away from purchasing taxable goods and overall decreases in consumption.

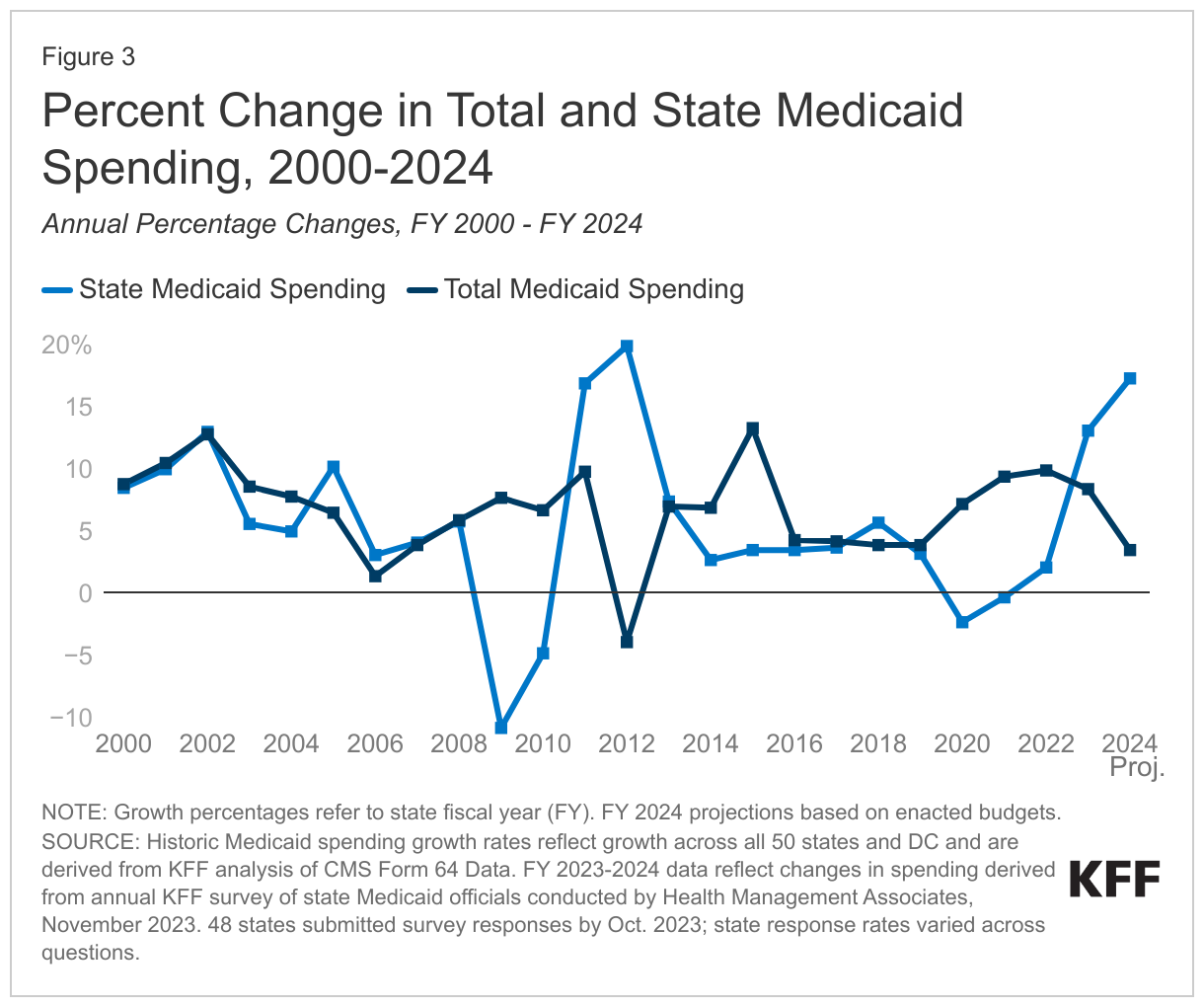

At the same time, pandemic-era federal funding for states has also expired or is expiring, including the phase out of the Medicaid enhanced federal funds at the end of 2023. For a three-year period following the onset of the COVID-19 pandemic, states provided continuous Medicaid enrollment in exchange for an increase in the federal share of Medicaid spending (known as the Federal Medical Assistance Percentage or “FMAP”), which kept state Medicaid spending below pre-pandemic levels. However, states are now in the process of “unwinding” the continuous enrollment provision, and the enhanced FMAP expired in December 2023, resulting in expectations of a temporary, sharp increase in state spending similar to what happened when fiscal relief provided during the Great recession expired (Figure 3). Other federal fiscal relief for states is also expired or has expired, including the enhanced federal matching funds for HCBS implemented as part of the American Rescue Plan Act (ARPA.)

How are people experiencing economic conditions?

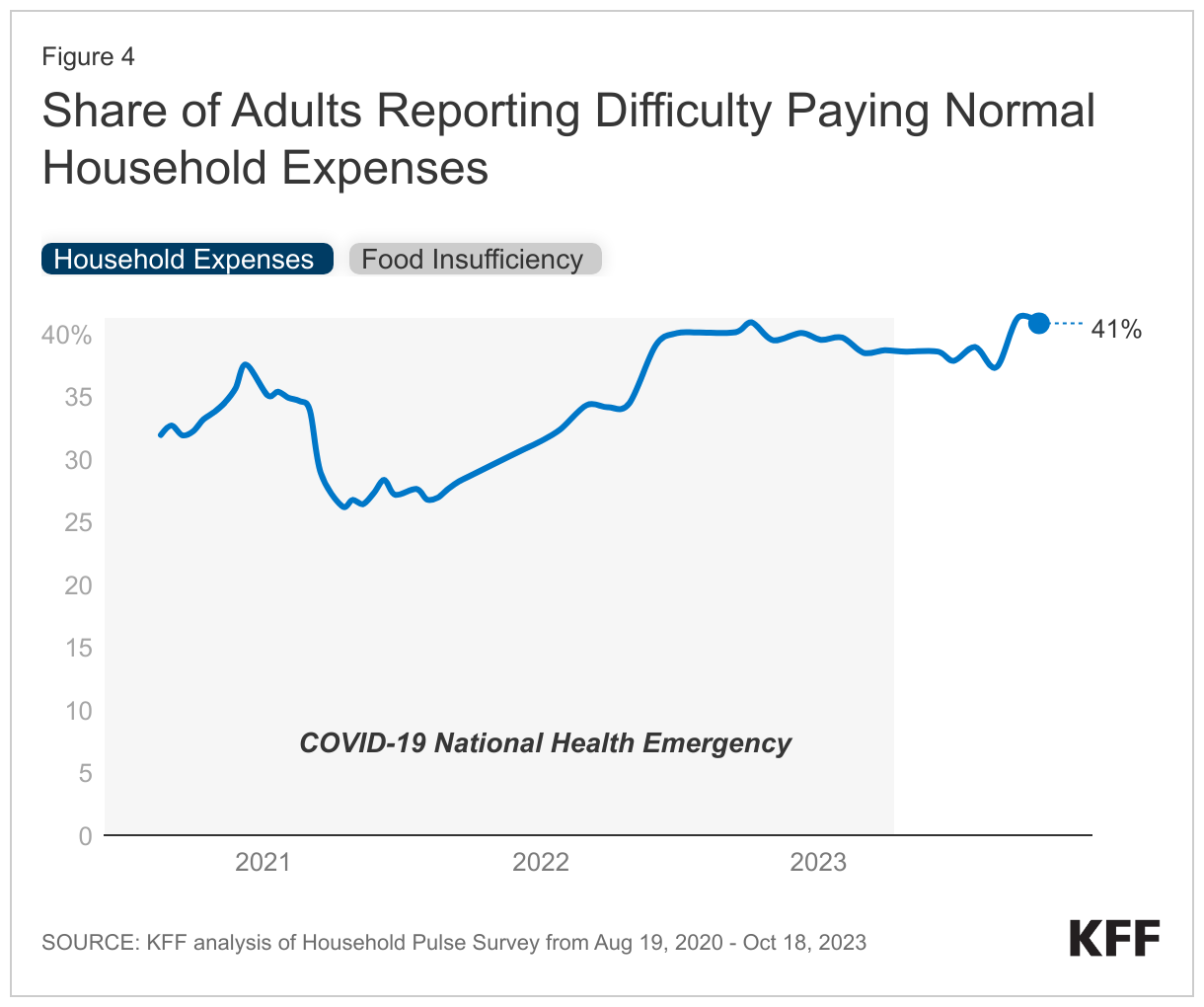

At the same time states are beginning to contend with weakening fiscal conditions, some U.S. households are experiencing increases in financial hardships despite positive economic indicators (Figure 4.) The unemployment rate was 3.7% in November 2023 and has remained below 5% since September 2021. In addition, the rates of inflation have slowed and wages have increased. Despite these positive economic indicators, many Americans have a negative view of the economy that is somewhat difficult to understand. Part of the reason for these negative views includes high prices that remain much higher than before the pandemic. Also, pandemic-era relief initiatives for families — such as the expanded Child Tax Credit (CTC) and expanded Supplemental Nutrition Assistance Program (SNAP) benefits — expired, and student loan payments have restarted. After rising initially with the onset of the pandemic and then declining as the economy improved and pandemic aid was dispersed, the share of households with food insecurity and difficulty paying expenses has increased. KFF analysis of the Household Pulse Survey finds that 41% of household in October 2023 found it somewhat or very difficult to pay household expenses, up from a low of 26% in April 2021, and 13% of households could sometimes or often not afford enough to eat — up from a low of 8% in August 2021. Congress has reached a tentative bipartisan agreement to expand the CTC, and the Biden Administration has taken several actions to provide student debt relief, which could help families currently struggling with the high cost of living.

Amid increases in financial hardships for individuals, millions have recently been disenrolled from Medicaid due to the unwinding of the Medicaid continuous enrollment provision. Almost three-quarters of disenrollments so far have been for paperwork or procedural reasons, raising concerns that many people who remain eligible for Medicaid may be losing coverage and becoming uninsured. People without insurance coverage have lower access to care and are less likely to receive preventive care and needed services compared with people who are insured. Uninsured people are more likely to delay or forgo care due to costs and often face unaffordable medical bills when they do seek care. In a recent KFF focus group report participants noted that losing Medicaid results in substantial out of pocket costs and would be “devastating” to lose access to prescriptions and treatments for themselves or their children. Recent KFF polling shows that with less than one year until the 2024 election, inflation and the affordability of health care are the dominant issues that voters want candidates to be discussing. As many families continue to struggle with finances and/or health coverage, state policymakers will have to balance funding for public aid with stricter budgetary constraints.

How might the state fiscal outlook affect Medicaid Programs and Enrollees?

For the remainder of FY 2024, the unwinding of the continuous enrollment provision and enhanced FMAP will be dominant factors affecting Medicaid enrollment and spending. Declines in enrollment will contribute to lower overall Medicaid spending growth while the expiration of the enhanced federal matching funds will increase state Medicaid spending. Heading into FY 2025, considerable uncertainty remains about overall Medicaid enrollment as well as the acuity of members that will remain on the program after the unwinding.

In FY 2025, unwinding will be less of a factor driving changes in Medicaid enrollment and spending; however, state revenue declines may dampen enthusiasm for ongoing investments in Medicaid and could prompt spending reductions. Fewer financial resources will have implications for states’ ability to continue to support increases in reimbursement rates and expansions in benefits that have been made in recent years. Due to strong fiscal conditions and federal pandemic-era aid, an annual KFF report on state Medicaid budgets found that states were upping reimbursement rates to address workforce shortages, particularly for long-term services and supports (LTSS.) States have also prioritized improving access to care, especially for behavioral health services and rural areas. States have to keep their budgets balanced, and — as budgets get tighter — it’s uncertain whether states will continue to make expansions, focus more heavily on cost containment initiatives, or potentially consider cuts to the program. As a result of the federal matching structure, states seeking to save state dollars in Medicaid would need to make larger programmatic cuts and would lose federal Medicaid funding. Governor’s proposed budgets and legislative debate about the budget will reveal different approaches to how states manage any budget challenges.