KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

On April 2nd, the Supreme Court of the United States will hear oral arguments in Medina v. Planned Parenthood South Atlantic. The case addresses whether Medicaid beneficiaries can seek relief in federal court to enforce Medicaid’s “free-choice of provider provision,” which allows Medicaid beneficiaries to seek care from any provider that is qualified and willing to participate in the program. While the case focuses on this specific question, it has its origins in broader efforts by anti-abortion policymakers to exclude Planned Parenthood clinics from the Medicaid program and, ultimately, eliminate all federal payments to Planned Parenthood centers. In this brief, we describe the case, the Medicaid policies underlying it, and potential implications for Medicaid beneficiaries’ access to reproductive health services.

What is the case in front of the Supreme Court about?

The Supreme Court’s review of this case is limited to one question: Can a Medicaid beneficiary bring a civil action to enforce the Medicaid Act’s free choice of provider? This question is similar to one that the Court decided in 2023 (Health and Hospital Corp of Marion County v. Talevski ) when it ruled (7-2) that patients do have a private right of action to enforce certain conditions that federal Medicaid law imposes on states and health care providers. However, the current case involves a different provision of federal law relating to free choice of provider under the Medicaid Act. Planned Parenthood and the individual beneficiary who has brought this case take the position that Medicaid beneficiaries meet the requirements to sue in order to enforce the free choice of provider provision. The Trump administration has weighed in on the side of South Carolina, contending that Medicaid beneficiaries should not be permitted to bring an action to enforce this provision.

In 2018, South Carolina’s Governor McMaster (R) issued an executive order prohibiting any clinic that provides abortion care from participating in the state’s Medicaid program. The order states that the state funds used to reimburse providers could be used to indirectly subsidize abortion care even though Medicaid only pays for non-abortion family planning services. The executive order had a direct impact on the Planned Parenthood clinics that offer abortion services in the state (South Carolina limits abortion to up to six weeks of pregnancy) but also offer enrollees other Medicaid-covered services including contraceptive care and STI screening and treatment. The state has historically reimbursed these providers for the non-abortion medical care they provide to Medicaid enrollees just like it pays for all other medical care. The federal Hyde Amendment bans the use of federal funds (including Medicaid) from being used to pay for abortions unless the pregnancy is a result of rape or incest or endangers the life of the pregnant person.

States operate Medicaid programs under federal guidance, and one of the federal provisions of the Medicaid law is known as free choice of provider. This provision states that “A State plan for medical assistance must… provide that any individual eligible for medical assistance… may obtain such assistance from any institution, agency, community pharmacy, or person, qualified to perform the service or services required… who undertakes to provide him such services.” Additionally, because many states require Medicaid beneficiaries to enroll in managed care, limiting their care to a defined network of providers, federal law states that beneficiaries may seek care from any Medicaid provider for family planning services specifically, even those outside the plan network.

The larger context for this case involves how a state determines who is a qualified provider, even though the Supreme Court is more narrowly focusing on private right of action. The statute does not define the word “qualified,” but longstanding federal regulations, recognize states’ authority to “set reasonable standards relating to the qualifications of providers.” The final lines of the regulation say that States need not provide payments to providers with certain felony convictions. The regulations and a separate provision contemplate that “[i]n addition to any other authority, a State may exclude” any provider from Medicaid for certain reasons “for which the Secretary could exclude” the provider from participating in Medicaid.

In 2016, in a “Dear Medicaid Director letter” issued during the Obama administration, CMS wrote that states have the authority to set standards that providers must meet, but to disqualify a willing provider, the state must have a legitimate reason such as concerns about the fitness of the provider to meet the standards or evidence of fraud. It went on to say that states cannot target a specific provider and “The failure of a state to apply otherwise reasonable standards in an evenhanded manner may suggest such targeting.” CMS went on to say that “states may not deny qualification to family planning providers…solely because they separately provide…abortion or another service that the state does not approve of.” This letter was rescinded by the Trump administration in 2018. Whether it be through the Courts or through administrative actions, this issue will likely continue to be debated and legally challenged for the foreseeable future.

The Supreme Court, however, is only considering whether Medicaid beneficiaries have the right to bring a case to enforce their right to choose their provider. The Court is not considering whether South Carolina acted properly when it excluded Planned Parenthood from its Medicaid program, deeming them “unqualified” because they provide abortion services as well as other reproductive health care services. If the Supreme Court finds that Medicaid beneficiaries have the right to bring an action to enforce their right to choose any provider, the case will then go back down to the district court to determine whether South Carolina acted within its authority to exclude Planned Parenthood as a nonqualified provider. If the Supreme Court rules that Medicaid beneficiaries do not have a private right of action, then Planned Parenthood itself could appeal South Carolina’s decision that found them to be an unqualified provider.

How have courts ruled about private right of action for Medicaid beneficiaries in other cases?

A civil rights statute, Section 1983, has long provided a mechanism for individuals to enforce the rights provided to them under federal programs, including Medicaid. There is a long history of litigation related to private enforcement of the Medicaid Act. While courts have affirmed the authority for individuals to use Section 1983 to protect Medicaid rights, the Supreme Court has issued decisions that have narrowed this authority. Currently there is a three-pronged test (pursuant to the cases Blessing v Freestone (1997), Gonzaga University v. Doe (2002), and Health & Hosp. Corp of Marion County v. Talevski (2023)) based on legal precedent that courts use to evaluate whether a federal law establishes an enforceable right:

whether the plaintiff is an intended beneficiary of the statute;

whether the plaintiff’s asserted interests are specific enough to be enforced; and

whether the statute imposes a binding obligation on the State.

In Talevski, the most recent Supreme Court case to consider this right, the high court reaffirmed the holdings in Gonzaga that a statutory provision is enforceable under Section 1983 when the provision is “phrased in terms of the persons benefits” and contains “right-creating individual centric language with an unmistakable focus on the benefited class.”

Federal circuit courts havegenerally upheld private enforcement of rights for Medicaid enrollees. Before the Supreme Court Talevski ruling in 2023, there was a split among circuit court rulings. In 2019 there were four circuit court opinions that all ruled in favor of beneficiaries’ right to enforce Medicaid provisions. However, in 2020, three of four circuit court decisions did not rule in favor of Medicaid enrollees, including one decision from the 5th Circuit Court of Appeals which ruled in favor of Texas’ decision to exclude Planned Parenthood. Until the Medina case, the Supreme Court had previously refused to review multiple cases in which Planned Parenthood patients were found to have an enforceable right. An earlier version of the Medina case, Planned Parenthood South Atlantic v. Baker, went up to the Supreme Court but was denied review. This is the first time the current configuration of the Supreme Court will hear a case involving Planned Parenthood.

While this case is narrowly focused on whether Medicaid beneficiaries have the right to sue to enforce their right to choose any willing, qualified provider, the Supreme Court’s decision will have implications for the many states wishing to exclude providers, such as Planned Parenthood, based on abortion politics and not based on clinical qualifications to provide medical services. If Medicaid beneficiaries cannot bring an action to enforce the free choice of provider provision, then states will have greater latitude to exclude providers, such as Planned Parenthood, based on political objections.

What does this case mean for Medicaid beneficiaries?

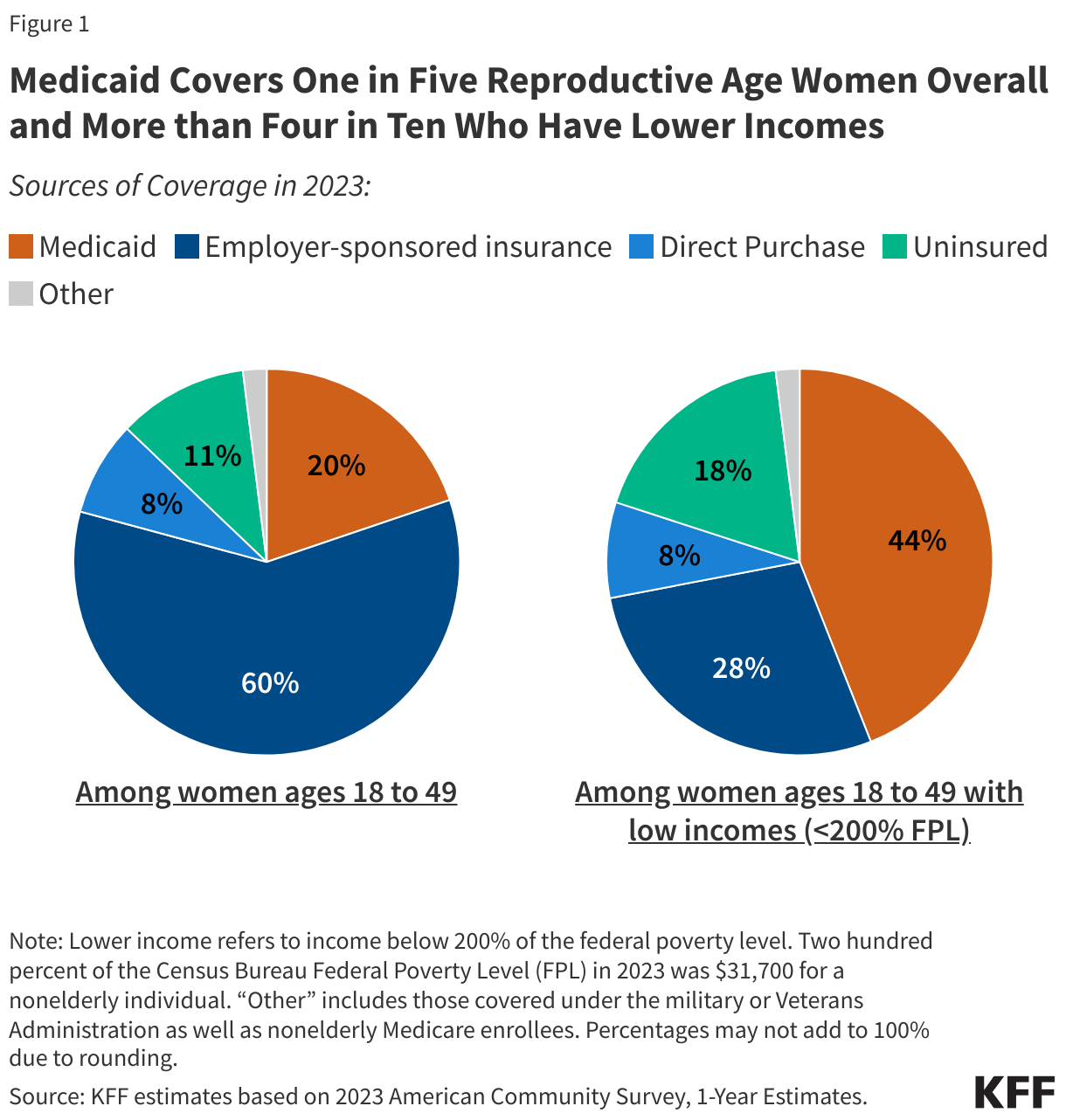

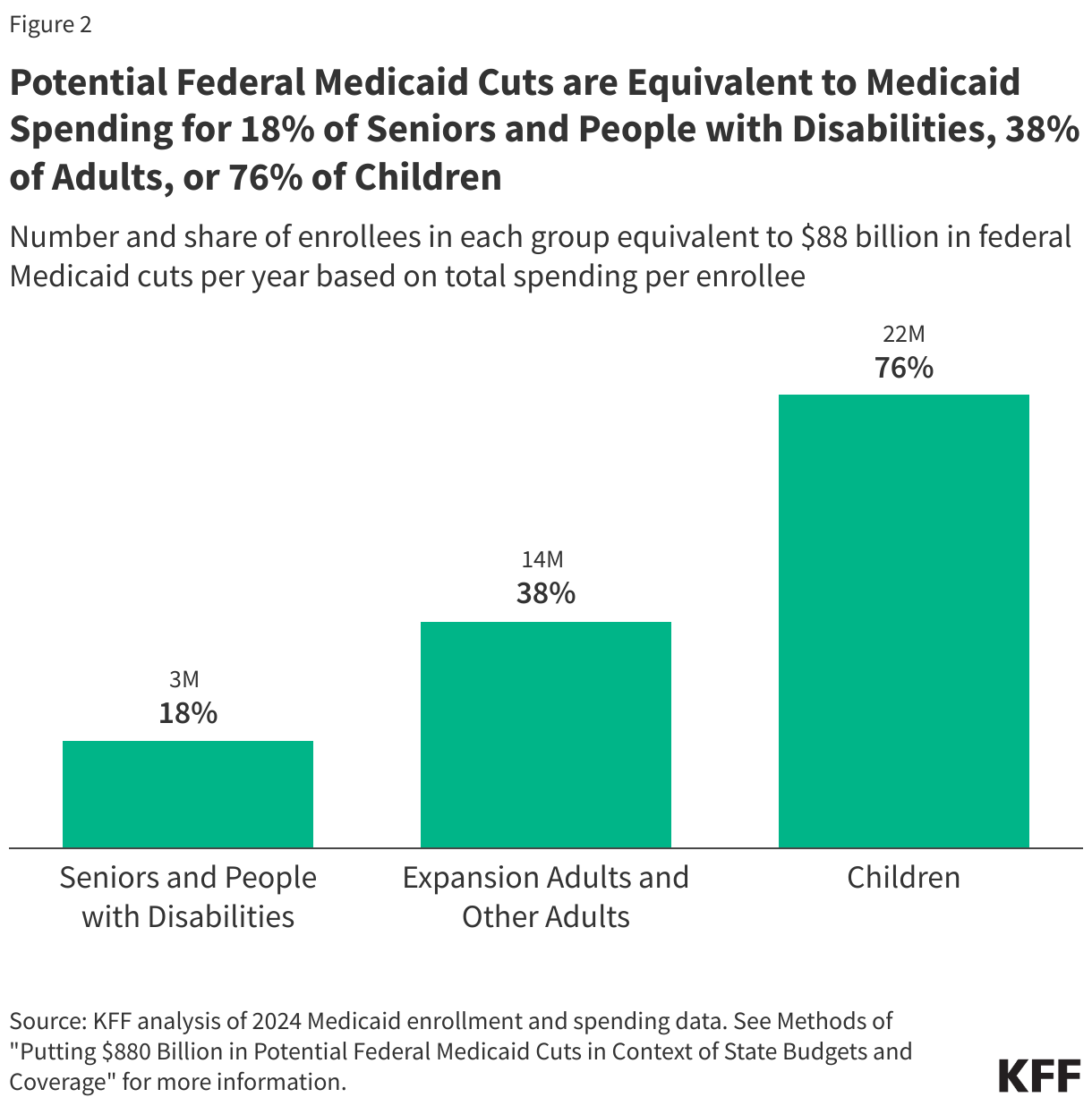

This case has the potential to curtail low-income individuals’ access to preventive reproductive health care in South Carolina and potentially in many states in the nation. The Medicaid program covers one in five reproductive age women and is the largest source of coverage for women with low incomes, covering over four in ten (Figure 1). All state Medicaid programs must cover family planning services, which includes contraceptive care plus a range of related services such as physical exams, cancer screenings, pregnancy testing and counseling, and screenings for other conditions. Medicaid is an essential source of financing for safety-net clinics and is widely considered to be the largest single public payer of family planning services. KFF research has found that specialty reproductive health care clinics such as Planned Parenthood centers offer a broader range of services to their patients compared to non-specialized clinics.

Other states are likely to follow suit if the Court rules in South Carolina’s favor. In fact, several other states, such as Texas, Arkansas, Indiana, and Missouri have tried to keep Planned Parenthood clinics out of their Medicaid networks, and while some of these efforts were blocked by CMS and courts because they violate the free choice of provider requirements, there have been exceptions. Federal courts upheld Arkansas and Texas decisions excluding Planned Parenthood from their Medicaid programs. South Carolina filed a waiver application to CMS during the first Trump Administration to exclude Planned Parenthood clinics from their Medicaid program, and Tennessee also has a similar waiver pending. No action has been taken to date on these waivers.

Blocking Planned Parenthood from receiving Medicaid reimbursements or other public funds has been shown to reduce low-income women’s access to contraceptives. In 2013, Texas replaced its Medicaid family planning program with a 100% state funded program that excluded Planned Parenthood as a participating provider. Following the policy change, there was a sizable drop in Medicaid claims for long-acting contraceptives such as IUDs or implants, and injectable contraceptives and an increase in Medicaid-funded births.

What is next?

The federal Solicitor General was granted approval to participate in oral arguments and has taken the position of South Carolina in this case. The Supreme Court will hear oral arguments on April 2nd and is expected to issue a ruling by the end of the term in June 2025.

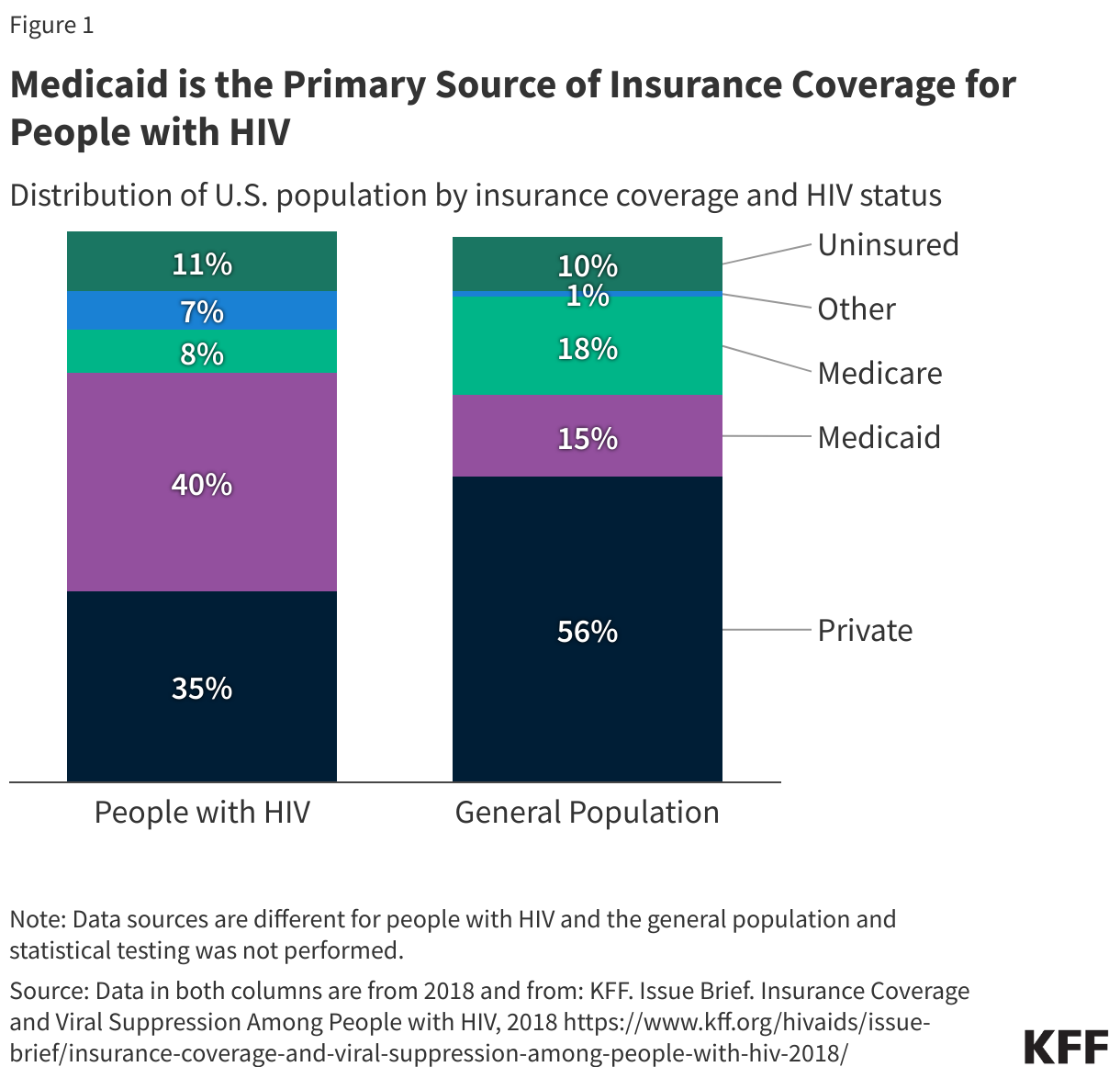

Medicaid is the primary source of insurance coverage for people with HIV, playing a key role in financing HIV care and prevention efforts. Despite the importance of Medicaid for people with HIV, they represent a very small share of program enrollees overall (less than one-half of a percent). Most Medicaid enrollees with HIV qualify for the program through the Affordable Care Act (ACA)’s Medicaid expansion and disability-related pathways.

Policy proposals being considered by Congress to reduce federal spending for the Medicaid program could have negative implications for people with HIV and those at risk. It is unclear what specific policies might be implemented to achieve federal reductions and a range of options are being considered, but reductions in federal Medicaid funding would shift costs to states and could result in coverage losses, reduction in benefits, cost-shifting to HIV safety-net programs, and/or reductions in payment rates to providers, if states do not offset federal dollars. Policies imposing Medicaid work requirements, which could happen through the Congressional budget process or via waiver approvals, would impact people with HIV as well, likely leading to coverage losses. Coverage losses among people with HIV would likely increase demand on the nation’s HIV safety-net program, the Ryan White Program (which could also face cuts in Congress though the program’s funding has already not kept pace with inflation or growing need). Loss of Medicaid coverage could result in interruptions in HIV care and treatment, which could lead to increased morbidity and mortality as well as HIV transmission.

1. Medicaid is the primary source of insurance coverage for people with HIV.

Medicaid is the single largest source of coverage for adults with HIV in the U.S., with four in ten estimated to be covered by the program (40%). By comparison, only 15% of adults in the general population have Medicaid coverage (Figure 1). Medicaid has helped to provide HIV care since the HIV epidemic began in the early 1980s. Coverage and benefits have grown over time as people with HIV are living longer, new infections continue to occur, and due to the Medicaid program’s expansion under the Affordable Care Act (ACA). Higher rates of Medicaid coverage reflect the fact that people with HIV have lower-incomes (33% of adults with HIV have incomes below 100% FPL compared to 11% of adults overall). Additionally, a large share of people with HIV have a disability (42%) and one in four (25%) people with HIV on Medicaid are dually eligible for Medicare, compared to 14% of enrollees without HIV.

2. Medicaid is the primary payer for HIV care and treatment

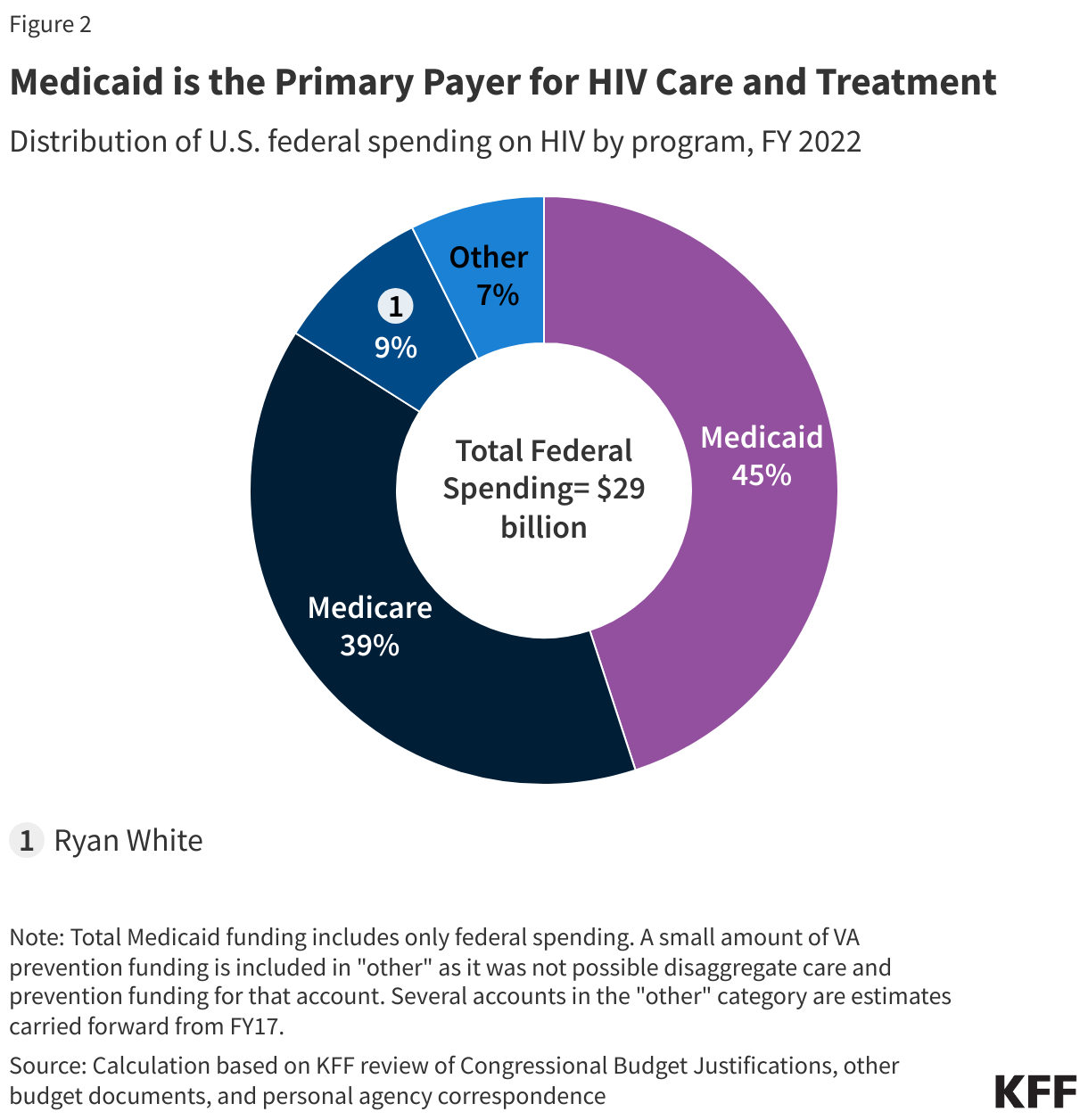

While Medicaid spending on people with HIV is a small share of all Medicaid spending, it accounts for an estimated 45% of all federal spending on HIV care and is the largest source of public financing for HIV care in the U.S, followed by Medicare. Still, in FY 2022, CMS estimates federal Medicaid spending on HIV represented less than 2% of total federal Medicaid spending. In addition, states also contribute to Medicaid spending on HIV (Medicaid is jointly financed by state and federal governments). Medicaid spending on HIV has increased over time, reflecting growing numbers of enrollees with HIV and the rising costs of care and treatment. In this way, it differs from the Ryan White Program, which is dependent on Congressional appropriations and funding levels do not automatically adjust to meet the needs of a growing population and increasing medical costs.

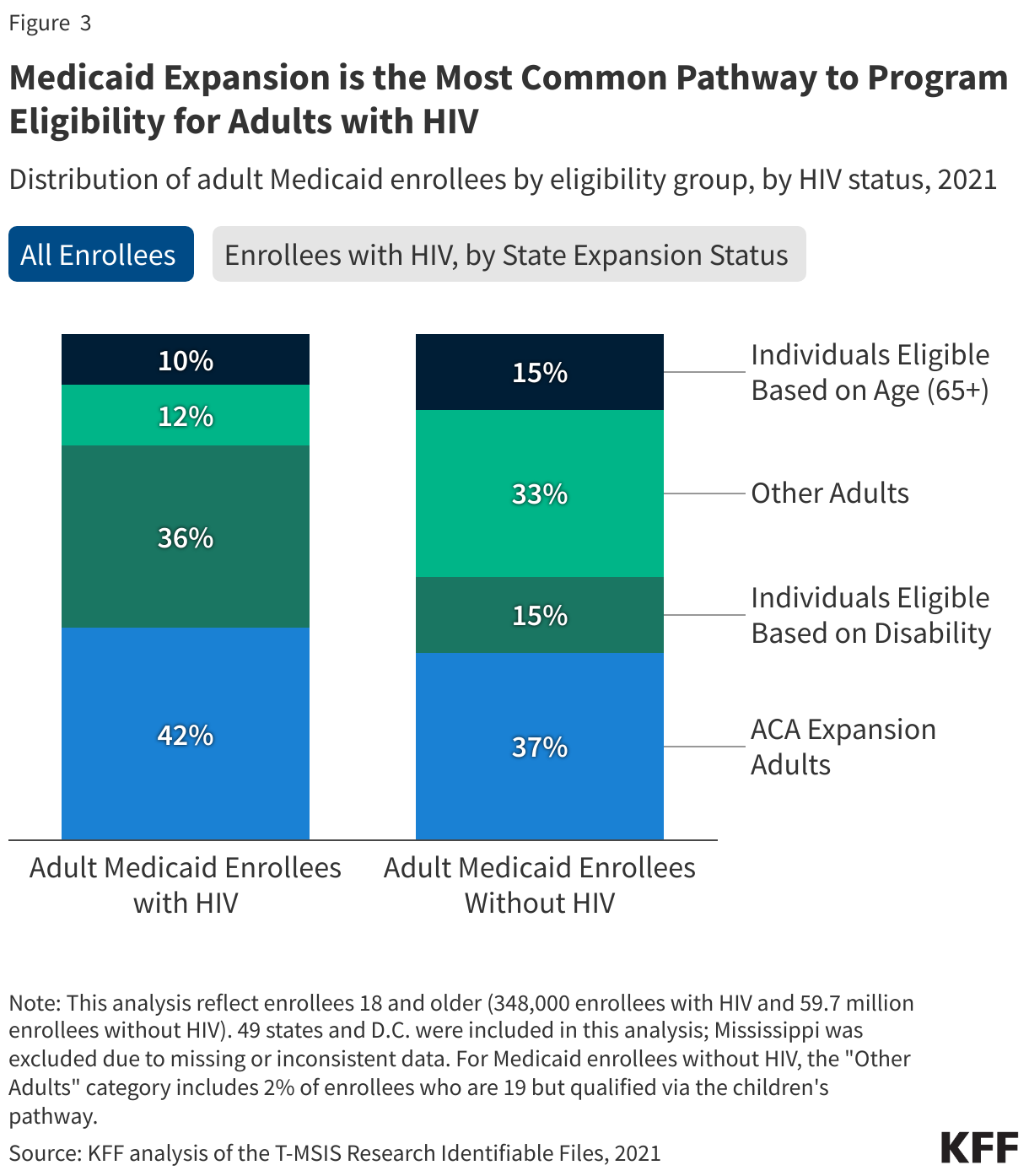

3. Medicaid expansion is the most common pathway to program eligibility for people with HIV.

Over four in ten (42%) Medicaid enrollees with HIV have coverage through the ACA’s Medicaid expansion, making it the primary pathway to Medicaid eligibility for this population. In Medicaid expansion states, over half (51%) of adults with HIV have coverage through the expansion. This pathway was created under the ACA to provide coverage to low-income adults on the basis of income without other categorical requirements like disability or pregnancy. Individuals with HIV who qualify through the expansion pathway may be able to access early treatment that could help stave off disability and significantly improve health outcomes. However, not all states offer the expansion pathway and today over one-third (35%) of people with HIV live in one of ten states that has not opted to expand Medicaid. Medicaid enrollees with HIV continue to enroll through the disability pathway at much higher rates than those without HIV (36% v 15%) and it remains the primary entry point to coverage for adults with HIV in non-expansion states, two-thirds (66%) of whom have disability- related coverage (compared to 30% in expansion states).

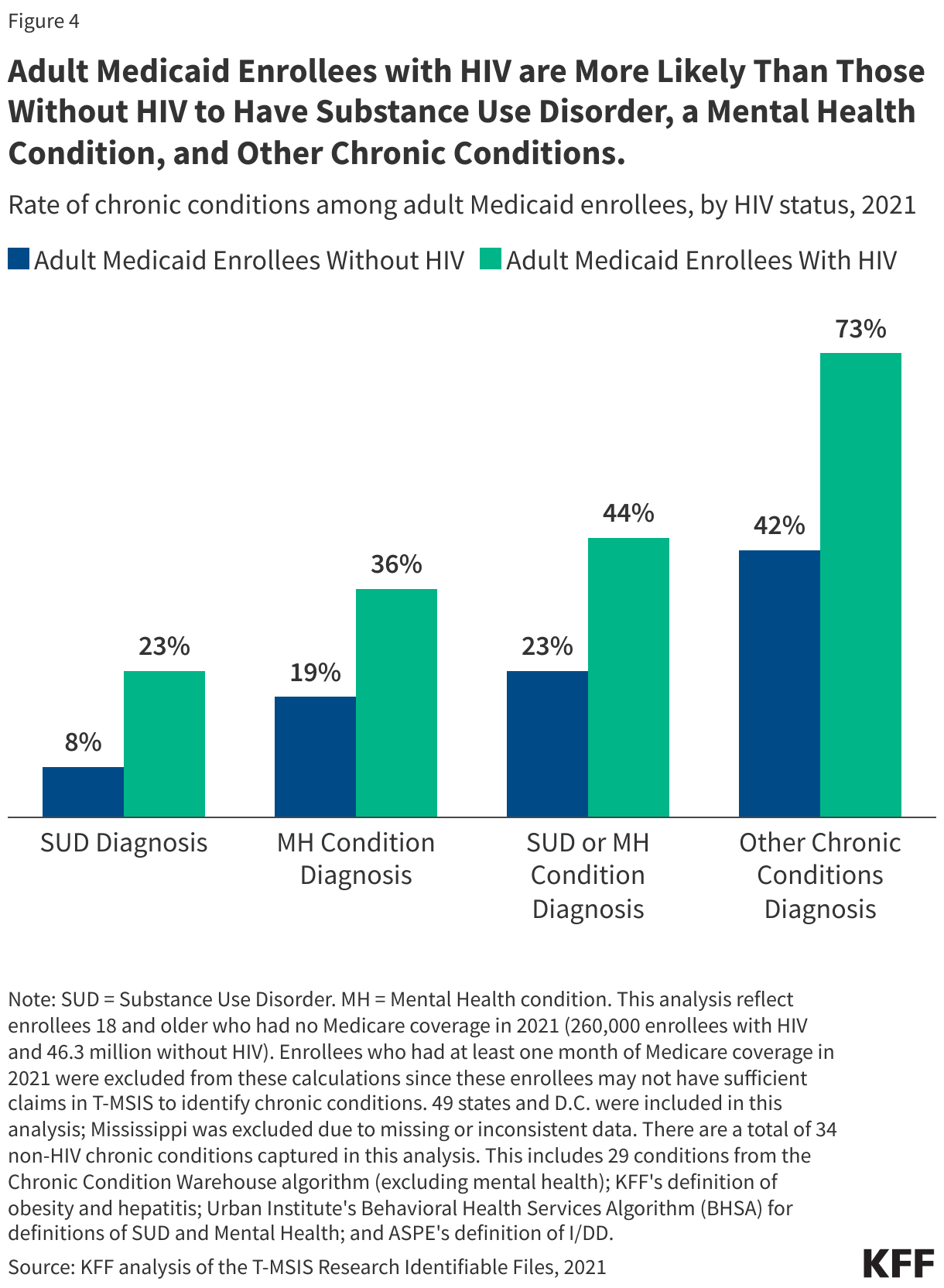

4. Medicaid enrollees with HIV are more likely to have substance use disorders, mental health conditions, and other chronic conditions relative to those without HIV.

Medicaid enrollees with HIV experience comorbidities at higher rates than those without HIV, including those related to mental health and substance use disorders. Nearly three-quarters (73%) of Medicaid enrollees with HIV have one of 34 other chronic conditions, compared to 42% of enrollees without HIV (see Figure 4 notes for details). Enrollees with HIV are more than twice as likely to be medically complex than enrollees without HIV, with about one-third (32%) having three or more chronic conditions in addition to HIV, compared to 13% of enrollees without HIV (data not shown). Adult enrollees with HIV are also twice as likely to have either a substance use disorder or mental health condition diagnosis (44% v 23%) compared to those without HIV. Enrollees with HIV are nearly ten times more likely than enrollees without HIV to have a hepatitis diagnosis. However, likely reflecting curative treatments now available, that share has declined from 14% of enrollees in 2013 to 6% in 2021 (data not shown). These differences between enrollees with HIV and without HIV likely reflect a range of both medical and social factors that combine to increase the risk and prevalence of these co-occurring conditions.

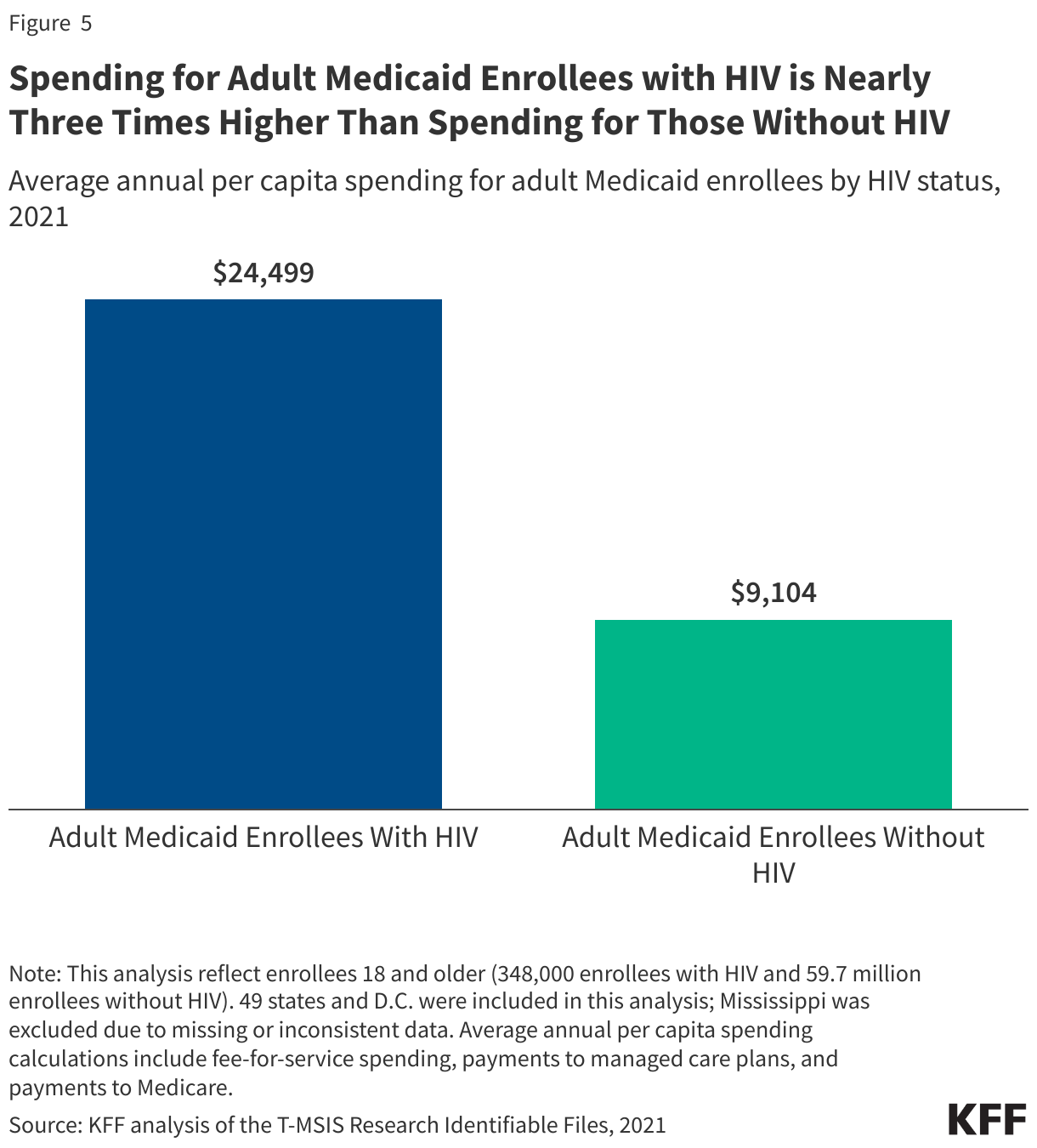

5. Spending for Medicaid enrollees with HIV is nearly three times higher than spending for those without HIV.

Spending on people with HIV enrolled in Medicaid is substantially higher than on those without HIV, reflecting higher health needs and costs of care. Average Medicaid spending per adult enrollee with HIV was about $24,000 in 2021, nearly three times that of adult Medicaid enrollees without HIV (about $9,000 per enrollee). While spending on enrollees with HIV was higher across all spending categories, the difference was especially marked in the drug/treatment category reflecting the relatively high cost of HIV medications (though notably, the drug spending data reflects pre-rebate amounts). Still, because people with HIV represent less than one-half of a percent of Medicaid enrollees overall, the net impact on Medicaid spending is small (less than 2%, see point 2 above).

Methods

Medicaid Claims Data: Figures 3-5 in this analysis use the 2021 T-MSIS Research Identifiable Demographic-Eligibility and Claims Files (T-MSIS data) to identify Medicaid enrollees with HIV.

Identifying HIV in Medicaid Claims Data: Enrollees with HIV were flagged if they had a relevant ICD 9 or ICD 10 code, any drug claims for a single tablet regiment (STR), or two or more other non-STR ARVs. A list of diagnosis and drug codes that were used for this analysis are available upon request.

Enrollee Inclusion Criteria: Enrollees were included if they were ages 18 or older and had at least one month of Medicaid coverage. Figure 4, which identifies rates of chronic conditions among those with and without HIV, also excludes those who had at least one month of Medicare coverage. These enrollees were excluded from these calculations since they may not have had sufficient claims in T-MSIS to identify chronic conditions.

State Inclusion Criteria in Medicaid Claims Data: To assess the usability of states’ data, the analysis examined quality assessments from the DQ Atlas for service users in the “Other Services” and Drug files for 2021. 49 states and D.C. were included in this analysis. Mississippi was excluded since it received an “Unusable” rating on these measures.

Defining Chronic Conditions (Figure 4): This analysis used the CCW algorithm for identifying chronic conditions (updated in 2020), excluding its definition for mental illness, which was pulled from a different source. This analysis also included in its definition of chronic conditions substance use disorder, mental illness, obesity, hepatitis C, and intellectual and developmental disabilities (ASPE definition).

Calculating Spending (Figure 5): Average annual per capita spending calculations include fee-for-service spending, payments to managed care plans, and payments to Medicare.Spending was calculated by summing the total spending of all claims per enrollee in the T-MSIS claims files and manually adds Medicare premiums for those who are also enrolled in Medicare. Estimates here do not include prescription drug rebates and most supplemental payments to providers.

Medicare, the federal health insurance program for people ages 65 and older and people under 65 with long-term disabilities, covers 68 million people and represents 15% of all federal spending – nearly $1 trillion dollars in 2024. The Medicare program has more than 1.4 million providers and more than 20 different payment systems. Due to the complexity and size of the program, Medicare faces risk of improper payments and some vulnerability to fraud, waste, and abuse, though many actions have been taken over the years to reduce improper payments in the program and to root out fraud.

Strengthening program integrity and tackling fraud, waste, and abuse in Medicare, as well as in other government programs, has been a priority across prior administrations. During President Obama’s administration, President Trump’s first term and during President Biden’s administration, the Department of Health and Human Services (HHS) budgets included proposals to improve program integrity, including for Medicare and Medicaid, reduce improper payments for these and other programs, and provide additional funding to combat fraud, waste, and abuse.

CMS, primarily through the Center for Program Integrity (CPI), plays a key role in efforts to promote program integrity in Medicare. In addition, the HHS Office of Inspector General (HHS OIG), often in collaboration with the Department of Justice (DOJ) and other agencies, monitors and combats fraud, waste, and abuse to improve the efficiency of Medicare by conducting audits, evaluations, and investigations, and carrying out enforcement actions, which in some instances have resulted in criminal or civil penalties. Despite the HHS Inspector General playing a key role in providing oversight of program integrity efforts for Medicare and other HHS programs, President Trump fired the HHS Inspector General and several other Inspectors General just days after taking office for his second term.

This brief explains fraud, waste, abuse, and improper payments in Medicare and describes actions to ensure Medicare program integrity.

Fraud, waste, abuse, and improper payments are often used interchangeably but have distinct meanings in the context of Medicare.

Improper payments. Improper payments are defined in law as “any payment that should not have been made or that was made in an incorrect amount, including an overpayment or underpayment, under a statutory, contractual, administrative, or other legally applicable requirement; and includes: any payment to an ineligible recipient; any payment for an ineligible good or service; any duplicate payment; any payment for a good or service not received, except for those payments where authorized by law; and any payment that does not account for credit for applicable discounts.”

Improper payments in the Medicare program, both overpayments and underpayments, can result from fraud, waste, and abuse as well as errors. For example, improper payments can be due to documentation mistakes or omissions, such as missing signatures, which may occur with otherwise appropriate claims and payments.

Fraud. According to CMS, Medicare fraud occurs when a provider knowingly submits false information to the federal government to receive Medicare payments. Medicare fraud can include knowingly billing for a higher level of complexity of services than the level that was actually provided, knowingly billing for services not provided, including falsifying records of providing such services, and knowingly ordering medically unnecessary items or services. Committing Medicare fraud is illegal and may lead to imprisonment, fines, and penalties. There are no estimates of how much Medicare specifically loses to fraud.

One recent example of Medicare fraud involved a $17 million Medicare hospice fraud committed against the federal government, in which an individual plead guilty to health care fraud, aggravated identity theft, and money laundering. In this case, the individual engaged in a scheme to operate a series of sham hospice companies and submitted fraudulent claims to Medicare for services that were not medically necessary and not provided, including for people who were not terminally ill and those who never received care from those sham hospices. Another example is a provider who was found guilty of health care fraud and other charges, who submitted over $24 million in fraudulent claims to Medicare, involving kickbacks and bribes for authorizing medically unnecessary cancer genetic lab tests, lengthy office visits that were never provided to patients, and medically unnecessary orthotic braces.

Abuse. According to CMS, abuse occurs when providers or suppliers perform actions that directly or indirectly result in unnecessary costs to the Medicare program. Abuse includes any practice that does not meet professionally recognized standards. Examples of abuse are billing for unnecessary medical services, charging excessively for services or supplies, or upcoding claims, which is when a provider uses an inaccurate billing code for a medical procedure that increases reimbursement. As CMS explains, “the difference between “fraud” and “abuse” depends on specific facts, circumstances, intent, and knowledge,” but fraudulent activity can be characterized by its intentional nature leading to some “unauthorized benefit.” Ultimately, CMS notes that providers who engage in abusive billing practices, like upcoding, or fraudulent activity, like charging for services that were not delivered, can be subject to civil and criminal penalties.

Waste. CMS defines waste as the overuse or misuse of resources that directly or indirectly result in unnecessary costs to the Medicare program. Examples of waste include conducting excessive office visits, prescribing more medications than necessary, and ordering excessive or duplicative laboratory tests. As one recent example, Medicare spending on expensive “skin substitute” products used for wound care increased from $1.6 billion in 2022 to over $10 billion in 2024, although according to research conducted for CMS, the efficacy of many of these products has not been studied. While the distinction between waste and abuse is not always clear, both result in unnecessary costs to the Medicare program.

CMS’s formal definition of waste differs from other views of waste, which may include value judgements of how the government should or should not be spending taxpayer money. As one example of this, MedPAC, an independent agency that advises Congress about Medicare payment, estimates the federal government pays insurers 20% more for Medicare Advantage enrollees than it pays for similar people in traditional Medicare, which amounts to $84 billion in additional annual spending in 2025 alone. Some might argue that this extra spending is wasteful while others might argue it adds value to the Medicare program by providing extra benefits to Medicare Advantage enrollees.

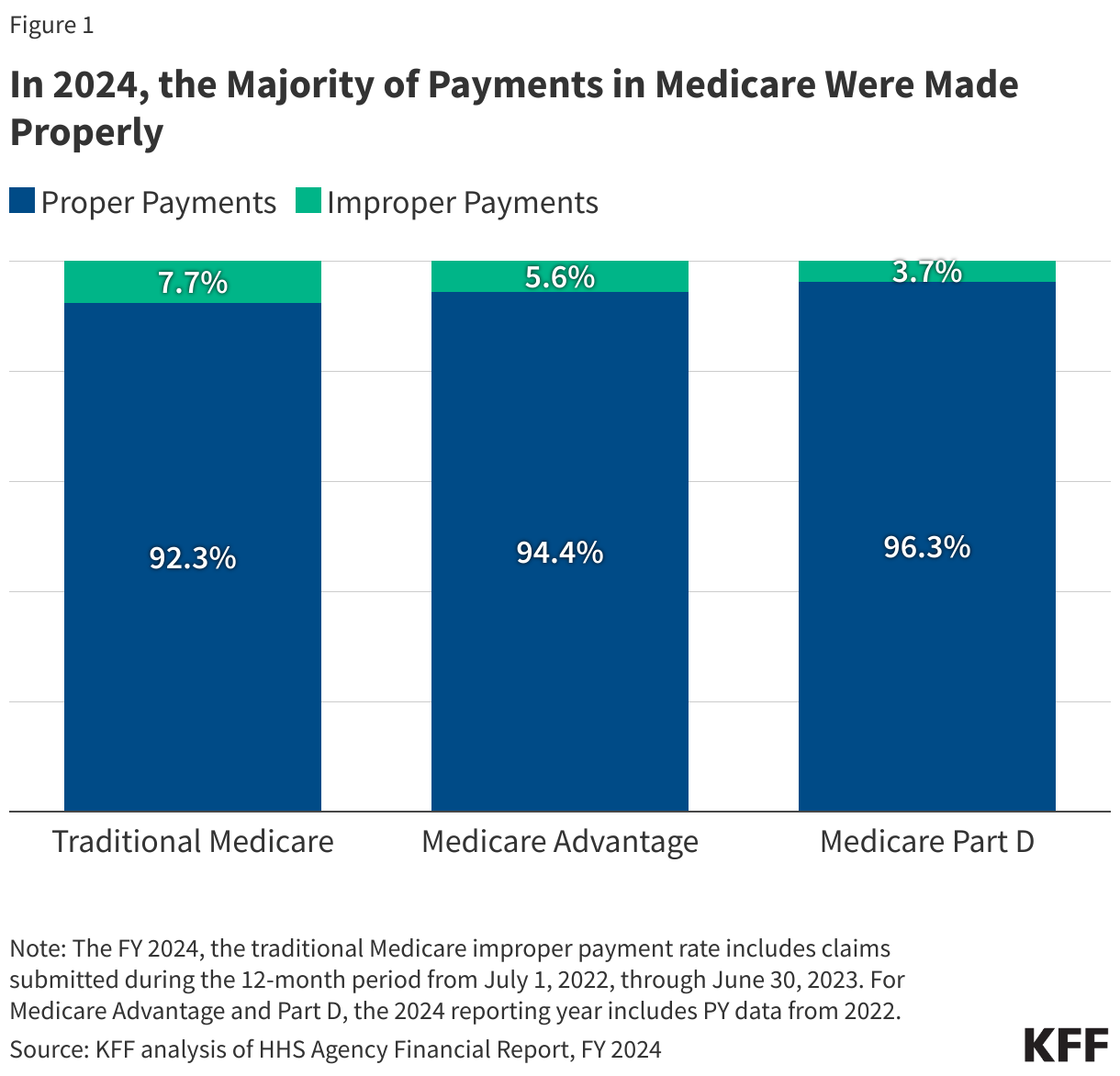

The vast majority of Medicare payments are made properly, although improper payments are an ongoing concern.

The Trump administration recently cited an estimate of $140 billion in improper payments made by CMS in 2024, but based on the amounts derived from each part of Medicare (as described below), improper payments for the Medicare program totaled substantially less – $54.3 billion in 2024, according to GAO. Even across all CMS programs – Medicare, Medicaid, CHIP, and the Affordable Care Act Health Insurance Exchange Advance Payments of the Premium Tax Credit (APTC) programs, the total amount of improper payments is less than the total cited by the administration – totaling $87.1 billion in 2024, according to CMS. Government-wide, 16 federal agencies across 68 programs, reported improper payments of $162 billion in 2024, a decrease of $74 billion from 2023, according to GAO. Again, estimates of improper payments described here are not the same as estimates of fraud.

CMS relies on three approaches to measure improper payments for traditional Medicare, Medicare Advantage, and Medicare Part D using different statistical methods for each:

The Comprehensive Error Rate Testing (CERT) program measures the improper payment rate in traditional Medicare. To determine if claims were paid properly, the CERT program reviews a random sample of traditional Medicare claims – approximately 37,500 claims in 2024.

In 2024, traditional Medicare paid an estimated 92.34% of claims properly, representing $382.02 billion in proper federal payments. The traditional Medicare improper payment rate was 7.66% (or $31.70 billion in federal payments) in 2024.

In 2024, Medicare Advantage paid an estimated 94.39% of claims properly, representing $320.87 billion in proper federal payments. The Medicare Advantage improper payment rate was 5.61% (or $19.07 billion in federal payments) in 2024. (These estimates of improper payments in Medicare Advantage do not include estimates of higher spending in Medicare Advantage compared to traditional Medicare for similar beneficiaries as discussed above, which are often referred to as “overpayments”).

In 2024, Medicare Part D paid an estimated 96.30% of claims properly, representing $92.95 billion in proper federal payments. The Medicare Part D improper payment rate was 3.70% (or $3.58 billion in federal payments) in 2024.

The rate of improper payments for traditional Medicare has decreased over time from 12.7% in FY2014 to 7.66% in FY2024. (Similar trends are not included for Medicare Advantage and Part D due to methodological changes in the calculation of the estimates over time.) While improper payment rates for traditional Medicare have generally declined, the overall amount of improper payments have increased as Medicare spending has increased over this period. Improper payments both negatively impact beneficiaries and reduce the solvency of the Medicare Hospital Insurance (Part A) Trust Fund, which is projected to be depleted in 2036.

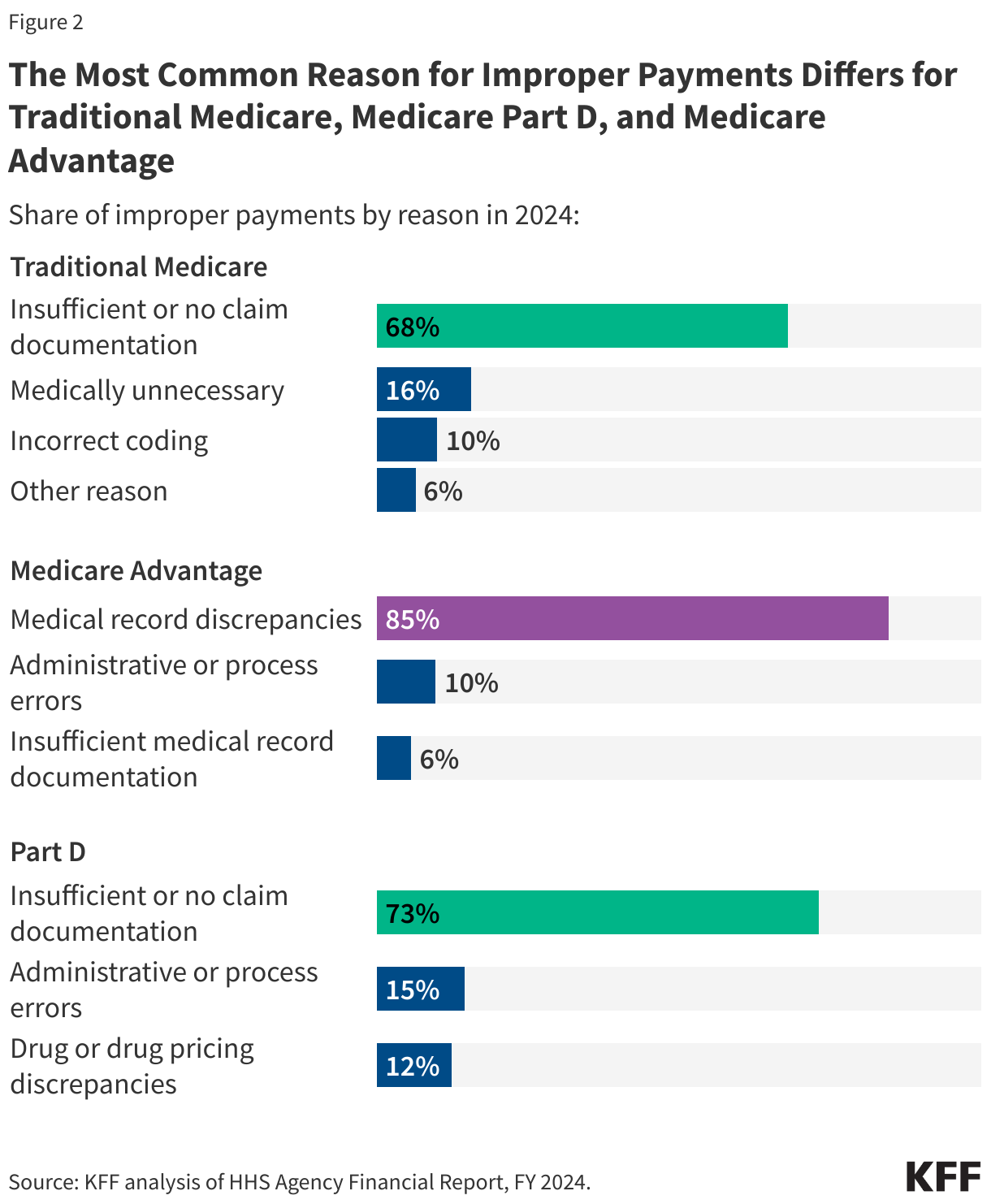

The primary reason for improper payments differs for traditional Medicare, Medicare Part D and Medicare Advantage.

In traditional Medicare, insufficient or no documentation was the most common reason for improper payments, accounting for 68% of improper payments, similar to Medicare Part D (73%), while for Medicare Advantage, medical record discrepancies accounted for 85% of all improper payments (Figure 2).

In 2024, the most common reason for improper payments in traditional Medicare was insufficient or no documentation (68%), followed by claims being medically unnecessary (16%), incorrect coding (10%), and other reasons (6%). Similarly, for Medicare Part D, insufficient or no documentation (73%) was the main reason for improper payments, followed by administrative or process errors (15%) and drug or drug pricing discrepancies (12%). The primary reason for Medicare Advantage improper payments is medical record discrepancies, accounting for 85% of all improper payments, followed by administrative or process errors (10%) and insufficient documentation (6%). According to CMS, improper payments due to medical record discrepancies result when medical record documentation submitted by a Medicare Advantage plan does not support payments received by the plan.

The differences in the main drivers of improper payments in traditional Medicare, Medicare Part D and Medicare Advantage reflect in part how improper payments are calculated – for traditional Medicare, CERT evaluates claims submitted by providers, and for Part D, the Part D IPM evaluates errors in payments for prescription drug claims, while for Medicare Advantage, the Part C IPM evaluates whether submitted diagnoses codes for which Medicare Advantage plans received payment are supported by enrollees’ medical records. Improper payments can result in either overpayments (monetary loss) or underpayments (non-monetary loss).

CMS is responsible for many program integrity activities, including conducting audits to identify and recover Medicare improper payments.

The CMS Center for Program Integrity (CPI) primarily implements the Medicare Integrity Program, which is responsible for helping to protect Medicare against fraud, waste, and abuse for various parts of the Medicare program. Program integrity activities within CMS resulted in estimated Medicare savings of $14.9 billion in FY 2023 and produced a substantial return on investment (ROI) – for every $1 spent on program integrity efforts, Medicare saved $8.30.

Among the many program integrity activities conducted by CMS to root out fraud, waste, abuse, and address improper payments in traditional Medicare and Medicare Advantage, audits are an important tool, including the Medicare Fee for Service Recovery Audit Program and the Medicare Advantage Risk Adjustment Data Validation audits.

The Medicare Fee for Service Recovery Audit Program. The Medicare Fee for Service (FFS) Recovery Audit Program’s mission is to identify and correct Medicare improper payments made on claims of health care services provided to traditional Medicare beneficiaries and recover those improper payments. In FY 2023, Recovery Audit Contractors (RACs) identified $353 million in overpayments and recovered $273 million. Recovery audits are distinct from CERT audits in that they seek to both identify and recover improper payments, while the CERT audits provide a national estimate of improper payments in traditional Medicare.

Medicare Advantage Risk Adjustment Data Validation (RADV) audits. Medicare Advantage RADV audits have similar objectives to the Medicare Fee for Service Recovery Audit Program and are the primary way CMS identifies and collects improper payments in Medicare Advantage. As part of RADV audits, CMS confirms that diagnoses submitted by Medicare Advantage organizations for risk adjustment are supported by enrollees’ medical records. Medicare Advantage organizations are held financially accountable when data submitted for risk adjustment purposes do not align with program rules. If Medicare Advantage organizations do not agree with the audit results, they may appeal these medical record review determinations. RADV audits, conducted by the CPI, seek to both identify and recover improper payments from Medicare Advantage plans, while Part C IPM audits provide a national estimate of improper payments in Medicare Advantage.

In 2023, the Biden Administration finalized a rule, which was proposed in 2018 during the first Trump administration, to make adjustments to the RADV program. One of the major elements of the finalized rule was the decision to extrapolate payments, which is a technique widely used in traditional Medicare and other audits, to estimate values, such as overpayments, based on a statistically random sample that would apply to the entire Medicare Advantage contract. The final rule extrapolates contract-level findings for audits starting in payment year 2018. In September 2023, Humana sued the government over its methodology and a federal judge denied dismissal of the case in June 2024, but the final outcome of the case is still pending.

The HHS OIG, DOJ, and other agencies play a major role in combatting Medicare fraud, waste, abuse and improper payments.

The HHS OIG, established through legislation in 1976, has played a major role in monitoring and combating fraud, waste and abuse to improve the efficiency of Medicare and other HHS programs, with the majority of its resources going to oversight of Medicare and Medicaid. The HHS OIG has a variety of responsibilities including conducting and supervising audits, investigations, and evaluations relating to HHS programs; identifying systemic weaknesses that give rise to opportunities for fraud and abuse and making recommendations to prevent them from reoccurring; leading and coordinating activities to prevent and detect fraud and abuse; and imposing administrative sanctions against providers of health care under Medicare and Medicaid who commit certain prohibited acts. The HHS OIG also operates a fraud hotline where it accepts tips and complaints related to potential fraud, waste, and abuse in HHS programs.

As the number of beneficiaries enrolled in Medicare Advantage has increased, the HHS OIG has focused more of its efforts on addressing the risks of fraud, waste, and abuse in Medicare Advantage and has developed a strategic plan for its oversight. One of its main priorities is ensuring that payments to Medicare Advantage plans are accurate. Similar to the RADV audits mentioned above that are conducted by CMS, the HHS OIG regularly audits Medicare Advantage organizations to review the accuracy of diagnosis codes since some diagnoses are at higher risk of being miscoded, resulting in overpayments to these organizations. For example, two of OIG’s recentaudits released in December 2024, found that Medicare Advantage plans had submitted diagnosis codes that did not comply with federal requirements, resulting in millions of dollars in estimated overpayments, though both plans disputed OIG’s findings and recommendations. HHS OIG audits do not represent final determinations and CMS officials ultimately determine whether the agency will seek to recoup overpayments in these instances.

The HHS OIG has also examined the use of health risk assessments (HRAs) and chart reviews in Medicare Advantage, producingmultiplereports on how these activities can increase risk scores and drive billions of dollars in additional payments to Medicare Advantage plans. As mentioned above, MedPAC estimates the federal government pays more for Medicare Advantage enrollees than it pays for similar people in traditional Medicare, at a cost of $84 billion in 2025 – $40 billion of which can be attributed to coding differences that increase payments to Medicare Advantage plans.

The HHS OIG often collaborates with the DOJ to fulfill its duties. OIG works with DOJ, under the joint direction of the Attorney General and the Secretary of Health and Human Services (HHS), to operate the Health Care Fraud and Abuse Control (HCFAC) Program, which was established in 1996 as part of the Health Insurance Portability and Accountability Act of 1996 (HIPAA) by the Clinton administration. The Program is tasked with coordinating federal, state, and local law enforcement efforts relating to health care fraud for Medicare, Medicaid, and other health care programs, conducting investigations and audits relating to the delivery of and payment for health care, and enforcing remedies for fraud.

The DOJ and U.S. Attorneys carry out enforcement actions against those suspected of engaging in Medicare fraud, including bringing criminal and civil cases to stop ongoing fraud, deter future fraud, and recover funds wrongfully taken through fraud and false claims. In FY 2023, 476 defendants were convicted of health care fraud-related crimes, which includes but is not limited to Medicare. In its annual report on the Health Care Fraud and Abuse Control Program, the OIG highlighted significant criminal and civil investigations for Medicare and other federal health care programs including in the areas of ambulances, diagnostic testing, durable medical equipment, home health providers, hospice, and medical devices, among others.

The DOJ has also been involved in civil cases regarding Medicare Advantage insurers, often in relation to allegations of false diagnosis codes submitted to inflate Medicare payments to plans through the risk adjustment system. For example, the Justice Department is litigating actions against UnitedHealthGroup, Elevance Health, and KaiserPermanente regarding the accuracy of their diagnosis data used for risk adjustment. In September 2023, Cigna paid $172 million dollars to the federal government in order to resolve False Claims Act allegations that it provided inaccurate data on patients’ diagnoses to inflate payments, though there was no determination of liability.

During FY 2023, efforts by the Health Care Fraud and Abuse Control Program for Medicare, Medicaid, and other government programs resulted in recoveries of $3.4 billion, of which the Medicare Trust Funds received close to $1 billion. The ROI for the HCFAC program from 2021 to 2023 is $2.80 returned for every $1.00 expended toward addressing fraud and abuse.

The GAO, which examines how taxpayer dollars are spent and provides Congress and federal agencies with information to help the government save money and work more efficiently, has undertaken a series of studies looking at these issues in the Medicare and Medicaid programs. A recent report from GAO found that while CMS has implemented numerous GAO recommendations to reduce improper payments in Medicare (as well as Medicaid), there are additional opportunities to improve program integrity in these programs and save billions of dollars. GAO also annually publishes a high-risk series that identifies government operations vulnerable to fraud, waste, and abuse, and Medicare has been on this list since 1990 due to the size and complexity of the program. In addition, in 2015, GAO established a framework to manage fraud frisk in federal programs, which CMS uses for implementing its Medicare integrity programs.

This work was supported in part by Arnold Ventures. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

From understanding health insurance terminology like “deductibles” and “copays” to deciphering the contents of a bill, consumers can face various barriers when trying to understand the costs associated with their health insurance coverage. This lack of understanding may contribute to frustration and cost-related problems and can have far-reaching effects on consumer health and finances. The KFF 2023 Survey of Consumer Experiences with Health Insurance (“KFF Consumer Survey”) found that 27% of insured adults reported that their health insurance paid less than they expected for a bill they received from a doctor, hospital, or lab in the past twelve months, the biggest cost-related problem consumers reported experiencing. Efforts to make cost information more readily available and easy to understand could help reduce some of these problems.

The first brief of this two-part series on navigating health insurance complexities and consumer protections focused on how consumers understand what their health insurance covers, what they do when coverage is denied, and what federal protections exist to ensure that the information available to them and coverage determinations are fair, accurate, and timely. This second brief focuses on KFF Consumer Survey findings about consumers’ understanding of health insurance costs and examines existing federal protections that seek to address barriers to understanding the cost of coverage and care, such as price transparency, self-service price estimator tools, and simplifying cost-sharing designs.

KFF Consumer Survey Findings: Consumer Understanding of Costs Associated With Health Coverage

The KFF Consumer Survey included a nationally representative sample of 3,605 U.S. adults ages 18 and older with health insurance. The survey asked consumers how well they understand costs associated with their health coverage, cost-related health insurance terminology, and the difficulty level of comparing cost-related insurance options such as premiums and deductibles.

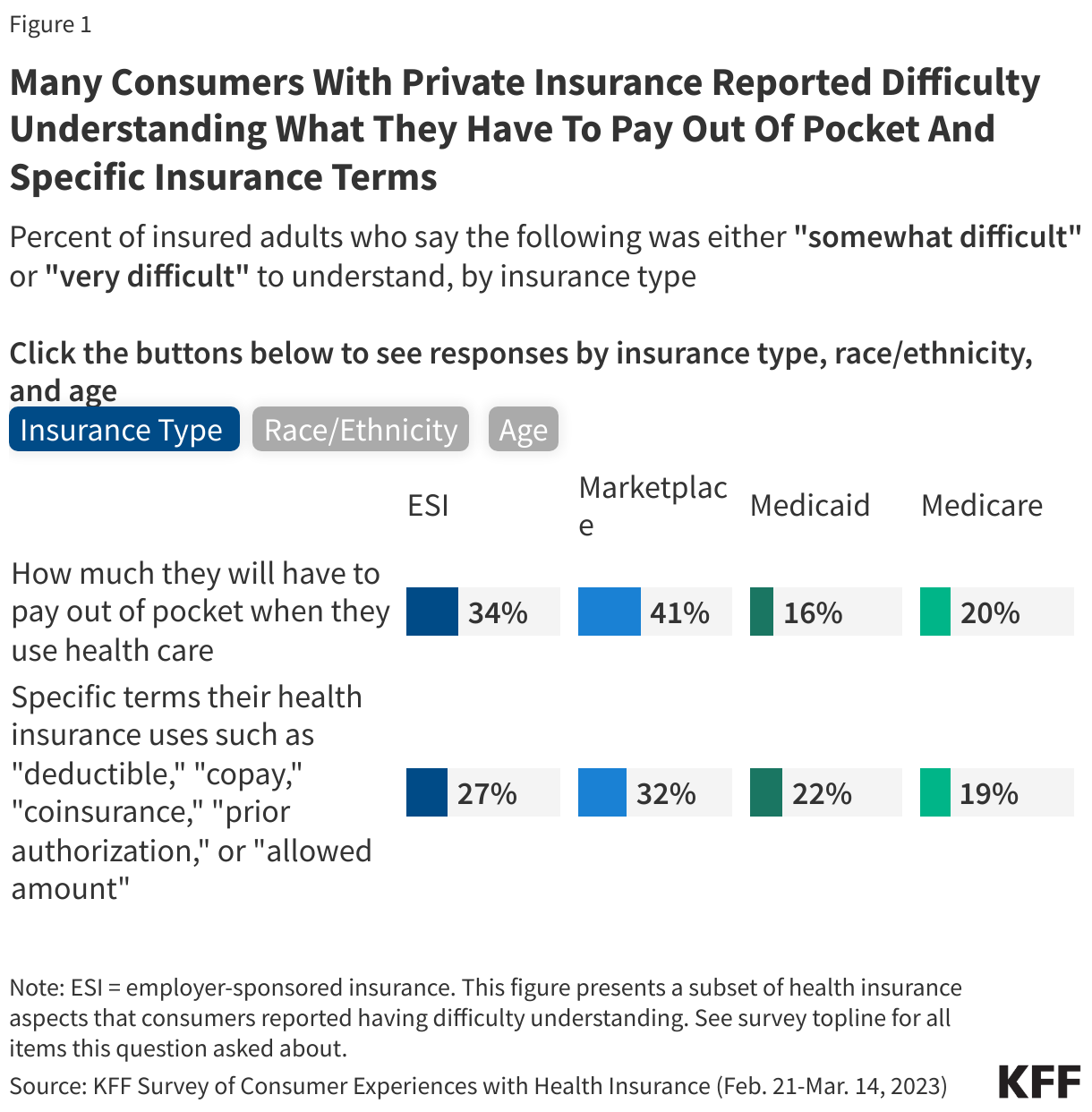

Three out of ten adults (30%) said that it was somewhat or very difficult to understand how much they would have to pay out-of-pocket when they use their health insurance. Marketplace (41%) and ESI (34%) enrollees were more likely to report this difficulty compared to Medicaid (16%) and Medicare (20%) enrollees (Figure 1). Insured White (30%) and Hispanic (32%) adults were more likely to report that it was somewhat or very difficult to understand how much they will have to pay out of pocket when they use health insurance compared to Black adults (23%). Additionally, insured adults ages 18-29 (35%), 30-49 (35%) and 50-64 (30%) were all more likely to report that it was somewhat or very difficult to know how much they will have to pay out of pocket when they use health insurance compared to those ages 65 and older (18%).

One-quarter (25%) of insured adults said that it was somewhat or very difficult to understand specific terms that their health insurance uses such as “deductible,” “copay,” “coinsurance,” “prior authorization,” or “allowed amount.” Those with Marketplace coverage (32%) and ESI (27%) were more likely to report that it was somewhat or very difficult to understand these terms compared to those with Medicaid (22%) and Medicare (19%) (Figure 1). Furthermore, Hispanic adults (31%) were also more likely to report difficulty in understanding these terms compared to White (23%) or Black (22%) adults. Insured adults between the ages of 18-29 (29%), 30-49 (30%), and 50-64 (25%) were all more likely to report difficulty in understanding these insurance terms compared to those ages 65 and older (17%).

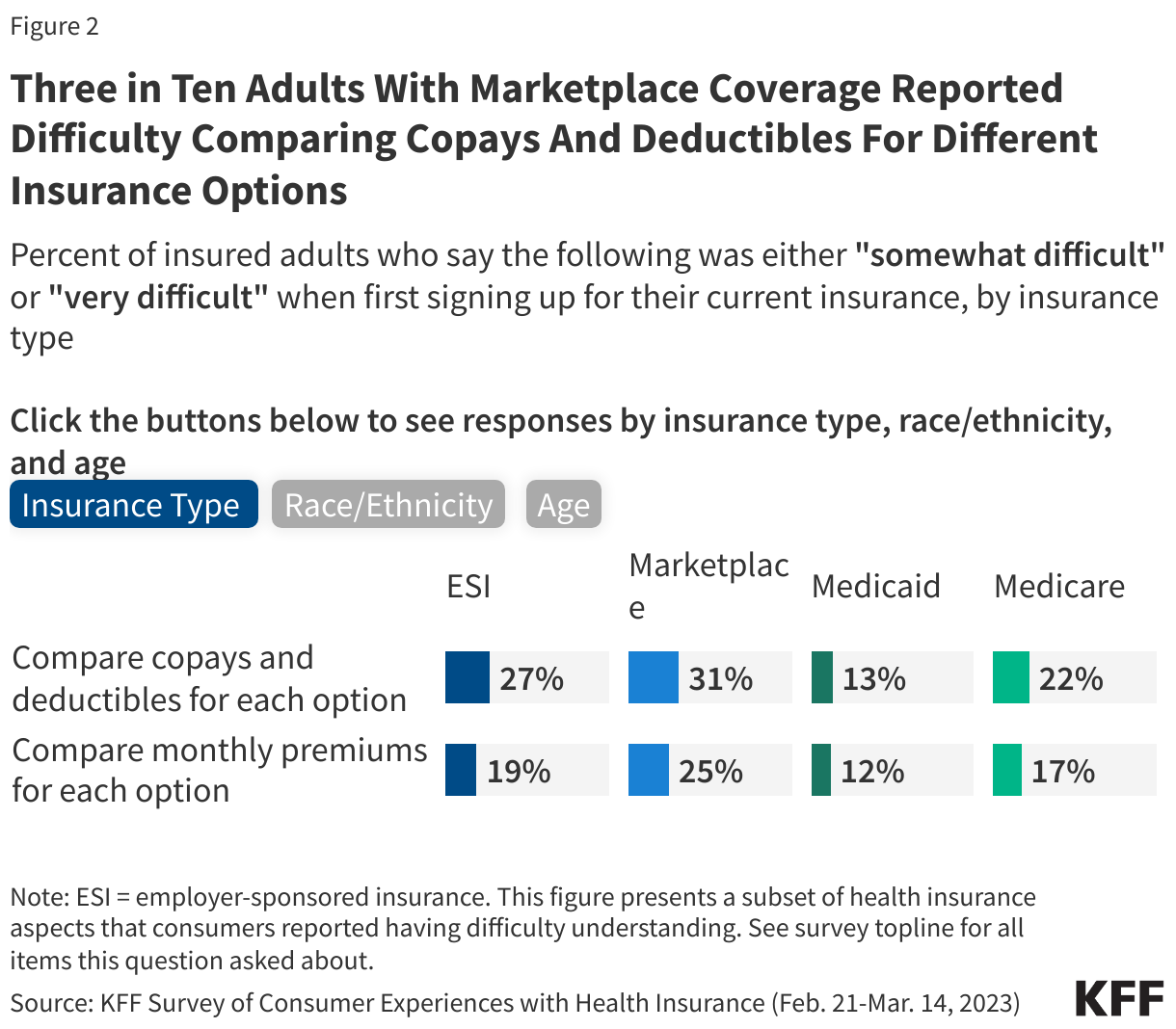

One in four (25%) insured adults reported that it was somewhat or very difficult to compare the copays and deductibles for each plan option. Those with ESI (27%) and Marketplace (31%) coverage were more likely to report having this problem compared to those with Medicaid (13%) or Medicare (22%) (Figure 2). A larger share of insured White (24%) and Hispanic (27%) adults reported difficulty comparing the copays and deductibles for each option than Black (19%) adults. Additionally, insured adults ages 18-29 (28%) and those ages 30-49 (27%) were more likely to report that it was somewhat or very difficult to compare the copays and deductibles for each option compared to those ages 65 and older (21%).

About one in five (19%) insured adults reported that it was somewhat or very difficult to compare the monthly premiums for each coverage option. Those with Marketplace coverage (25%) were more likely to report having this issue compared to those with ESI (19%), Medicaid (12%), or Medicare (17%) (Figure 2). Insured Hispanic adults (22%) were more likely to report difficulty comparing the plan premiums than White (17%) adults. Insured adults ages 18-29 (24%), 30-49 (20%), and 50-64 (19%) were all more likely to report that it was somewhat or very difficult to compare the monthly premium for each option compared to those ages 65 and older (13%).

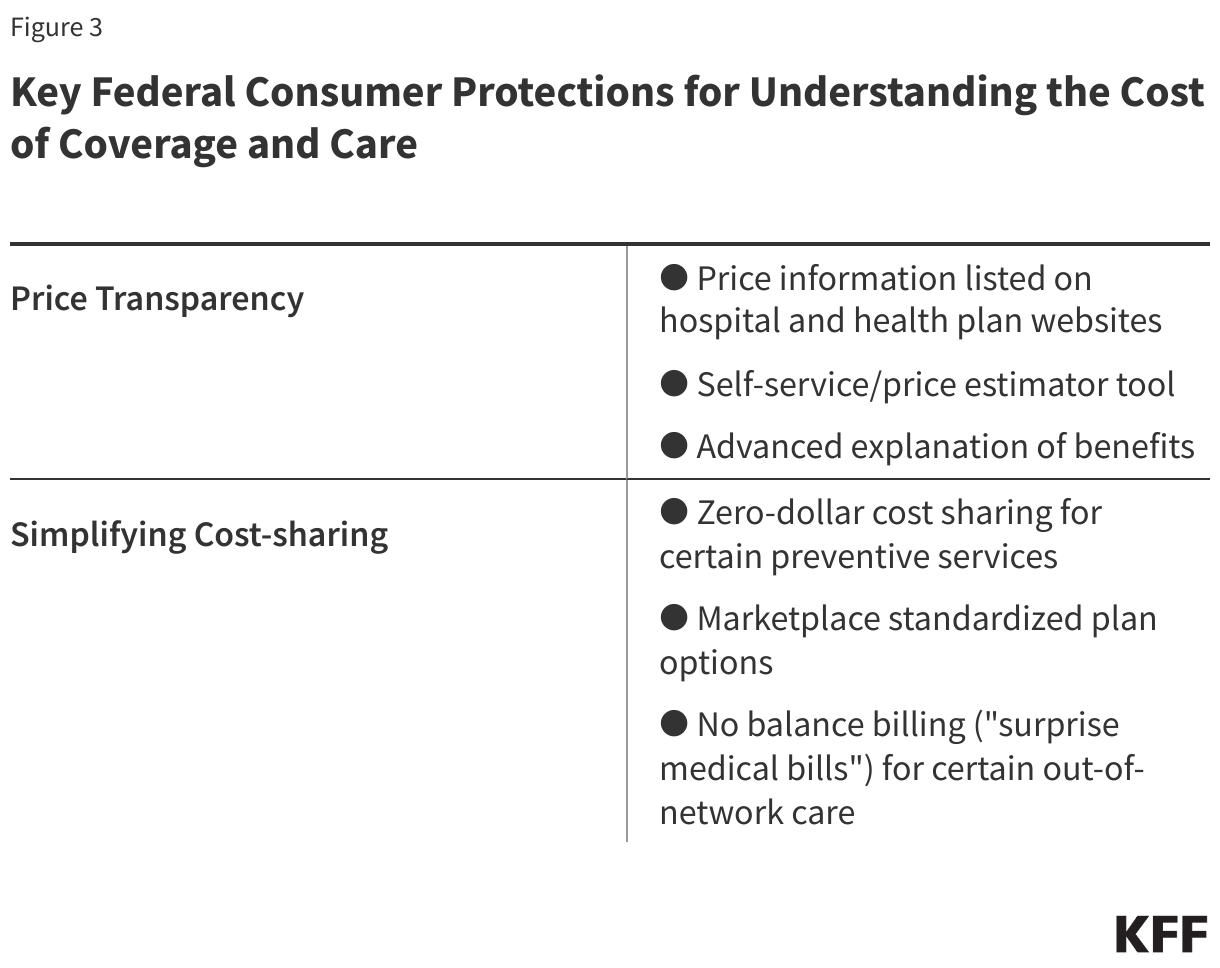

Federal Consumer Protections that Seek to Address Barriers to Understanding the Cost of Coverage and Care

The KFF Consumer Survey indicates that many consumers have gaps in understanding what they will have to pay for the services they need before they receive care. Federal reforms related to health insurance costs aim to simplify and standardize cost sharing, set guidelines for the coverage of certain health benefits, and promote price transparency. Some of these changes may enable consumers with private coverage to better understand their coverage options and out-of-pocket obligations for covered benefits. This section focuses primarily on federal protections for individuals with private health insurance (individual and employer-sponsored), though public programs like Medicare and Medicaid have established many consumer protections as well.

Providing Consumers with Cost Specific Information: Price Transparency

Federal reforms to private insurance aim to increase price transparency and promote competition among hospitals and among insurers, reduce health care costs, encourage patients to price-shop at different facilities by providing an estimate of patient out-of-pocket costs for a health care service or prescription drug, and help consumers make better plan selections. Reforms would allow consumers to look for price information about a service in at least three ways:

Search listed pricing information available on hospital and plan websites: Most hospitals in the U.S. are required to establish, update annually, and make public on the internet a comprehensive machine-readable file containing a list of their “standard charges” for all items and services that they provide. Standard charges are the regular rates established by hospitals for items and services. Standard charges alone are generally of less value to insured consumers when determining their out-of-pocket costs than the “allowed amount,” which is the maximum amount a specific health plan will pay for a covered benefit. This hospital price transparency requirement was included in the Affordable Care Act (ACA), with more extensive federal regulations (incorporating additional forms of pricing, including allowed amounts) issued in 2019 and effective in 2021. Separate federal price transparency standards require employer-sponsored plans and insurers to post on a publicly accessible internet site three machine-readable files disclosing different forms of pricing information specific to each plan: in-network provider-negotiated rates, historical out-of-network allowed amounts (the maximum amount a plan will pay for a covered health service received from an out-of-network provider), and prescription drug rates. Health plans and insurers must update these machine-readable files at least monthly and clearly state when it was last updated. This “Transparency in Coverage” requirement was created by 2020 regulations interpreting a provision in the ACA related to consumer transparency. These postings have been required since 2022, although full implementation of the prescription drug reporting was delayed.

The information posted to date under these two requirements is anything but consumer-friendly, as experts have noted their own problems evaluating the data. Data scientists and other researchers have reported finding this information overwhelming and sometimes inaccurate and difficult to decipher. As third-party entities aggregate this data to assist employer plans to make purchasing decisions and public policy researchers to evaluate costs, consumers themselves likely have limited ability to use the raw data on their own. There are few studies of the consumer experience with this machine-readabledata, especially whether they know it is available, and their ability to understand and use it.

Use a self-service or price estimator tool: In an effort to alleviate the complexity and possible confusion that was perhaps anticipated by policymakers when requiring the posting of large amounts of data in digital files, federal rules also require that more “consumer-friendly” tools be available so that consumers can obtain information about out-of-pocket costs before they get a service or drug. Under the hospital transparency regulation, hospitals must also compile and display online a “consumer-friendly” list of at least 300 “shoppable” services (e.g., having a baby, getting a hip replacement), including 70 services specified by the Centers for Medicare & Medicaid Services (CMS) and any additional procedures chosen by the hospital. The list must include a plain language description of each procedure, discounted cash prices, payer-specific (i.e., private insurers, Medicare, Medicaid) negotiated prices, and de-identified minimum and maximum negotiated prices for all third-party payers for an item or service. As an alternative to this “consumer-friendly” list, a hospital can instead create and maintain an online price estimator tool that:

Provides estimates for at least 300 shoppable services (including the 70 CMS-required services).

Is displayed on the hospital website for easy access (i.e., does not require payment or the creation of an account to use the estimator tool); and

Allows consumers to obtain an estimate of the amount they will be expected to pay the hospital for the shoppable service before they receive it.

The Transparency in Coverage regulation requires plans and insurers to provide cost-sharing information via an internet self-service tool that consumers can use to obtain personalized out-of-pocket estimates for in- and out-of-network health care items and services (including prescription drugs and medical equipment). Plans and insurers must make other information—such as the negotiated rate for a service, and whether the service is subject to prior authorization—available through a billing code or service description search. This rule was fully effective in 2024.

In addition, in 2020 Congress passed and President Trump signed the Consolidated Appropriations Act (CAA), which required plans and insurers to make a “price comparison tool” available on the internet, in paper form, and by telephone. Since this tool is similar to the Transparency in Coverage self-service tool, federal agencies state in guidance that they have deferred enforcement of this CAA price comparison tool requirement.

Review an Explanation of Benefits before care is received (Advanced Explanation of Benefits (AEOB)): In addition to the transparency initiatives above, Congress also included in the CAA another transparency-related protection—the Advanced Explanation of Benefits—to help consumers better understand their expected out-of-pocket cost for a service before they receive it so they can budget and/or compare cost to other providers. This was part of the No Surprises Act, a group of consumer protections included as part of the CAA.

When scheduling care or upon request health care providers and facilities must provide a personalized good faith estimate of the provider’s expected charges to the consumer’s employer plan or insurer. The plan or insurer must then use this information to create an Advanced Explanation of Benefits for the consumer that includes standard Explanation of Benefits information such as the provider’s expected charge, what the plan expects to pay, and the amount the consumer is expected to pay.

Implementation of this provision of the law has been challenging, according to CMS, as it will require coordination between providers and plans, and likely the development and testing of a single industry-wide electronic interchange standard. The agencies involved had convened an industry working group as well as consumer testing with prototype Advanced Explanation of Benefits. The rule’s 2022 effective date has been delayed.

Although the Advanced Explanation of Benefits has not yet been implemented, providers and facilities must provide a good faith estimate to uninsured and self-pay patients upon request or in advance of a scheduled service, within a specified timeframe. If the final bill is $400 or more above the good faith estimate, consumers may be able to dispute the bill through a patient-provider dispute resolution process. Eligible consumers may submit a complaint to CMS if the provider did not give the patient a good faith estimate or if the provider does not honor a dispute resolution in the patient’s favor.

Simplifying Cost Sharing and Other Consumer Out-of-Pocket Payments to Limit Cost and Address Complexity

The ACA ushered in new federal requirements to limit out-of-pocket spending for consumers with private insurance, with protections that set parameters for the design of certain health plan options and limited cost sharing so that it is the same whether the consumer has employer coverage or other private coverage on- or off- Marketplace. Marketplace plans have gone further through standardized plan options. The No Surprises Act’s reforms address balanced billing, eliminating it for certain services. All look to make costs more understandable and predictable for patients. These protections include:

Maximum out-of-pocket limit: All non-grandfathered private plans are required to set an annual cap on cost sharing for essential health benefits received in-network. These dollar limits are adjusted each year. For the 2025 plan year, the maximum out-of-pocket limit is $9,200 for self-only coverage and $18,400 for family coverage. Once a consumer reaches the maximum out-of-pocket limit, the insurer is required to cover 100% of the cost of essential health benefit services received in-network for the remainder of the plan year.

Ban on annual and lifetime dollar limits: All private plans, including grandfathered plans, are prohibited from imposing annual or lifetime dollar limits on coverage for essential health benefits, whether for in-network or out-of-network services. An annual dollar limit refers to the maximum amount an insurer would pay for covered benefits within a given year, whereas a lifetime dollar limit is the total dollar amount that a health plan would pay for as long as a consumer was enrolled in the plan. Prior to the passage of the ACA, an estimated 70 million people in large employer plans, 25 million in small employer plans, and 10 million with individual coverage had lifetime limits on their health coverage.

Zero-dollar cost sharing for certainpreventive services: Under the ACA, all private, non-grandfathered plans must cover a range of preventive services and not apply cost sharing, including:

Evidence-based screenings and counseling for adults recommended by the U.S. Preventive Services Task Force (USPSTF) with an “A” or “B” rating such as cancer screenings, prenatal care, and medications that help prevent heart disease

Routine immunizations for adults and children recommended by the Centers for Disease Control and Prevention’s Advisory Committee on Immunization Practices such as influenza, measles, and COVID-19

Preventive care for infants, children, and adolescents recommended by Health Resources and Services Administration’s (HRSA) Bright Futures Program such as well-child visits, autism screening, and fluoride supplements

Additional preventive services for women as recommended by HRSA’s Women’s Preventive Services Initiative such as contraception, breast cancer screening, and breastfeeding supplies and support

Marketplace standardized plan options: Plans in the Marketplace are separated into categories — Bronze, Silver, Gold, or Platinum — based on the amount of cost sharing they require. In general, plans with lower cost sharing have higher premiums, and vice versa. For example, Bronze plans have the highest cost sharing but lower premiums, and Platinum plans have the lowest cost sharing but higher premiums. There can be substantial variation in plan details, even within the same insurer (e.g., premiums, provider networks, covered benefits, plan network types).

Standardized plan designs (also known as “easy pricing”) were created to simplify and streamline plan comparison and selection offered on the federally facilitated Marketplace (FFM), state-based exchanges using the federal platform (SBE-FPs), and some state-based Marketplaces (SBMs) by applying the same deductibles, copays, coinsurance, and out-of-pocket maximums to each category of essential health benefits across all Easy Price plans in the same metal level. For example, in 2025, the annual deductible for covered services under all Gold level Easy Price plans is $1,500, regardless of insurer. By contrast, other non-standardized Gold level plans might have different deductible and copay amounts.

Standardized plan design options were also designed to improve affordability by covering certain services before the deductible is met. All Easy Price plans must waive the deductible and instead apply a fixed dollar copay (e.g., $30 for a Gold Easy Price plan) for the following items and services: primary care and specialist office visits, urgent care visits, outpatient visits for mental health and substance use disorder treatment, physical therapy visits, and generic and preferred-brand drugs.

Not all Marketplace plans are standardized, though Marketplace plans must offer a standardized plan option at every product network type, metal level, and throughout each service area where they offer non-standardized plan options. Insurers can still choose to offer non-standardized plan options in the individual market but are limited to two plan options per product network type (i.e., HMO, PPO, EPO, POS) for plan year 2025.

Research has shown that having too many choices can confuse consumers and lead to them choosing suboptimal coverage. As implemented to date, HealthCare.gov’s requirement to offer standardized plan options may have increased, not decreased, the number of plan choices consumers face. Though consumers in most areas will continue to have a large number of plan choices for the foreseeable future, over time, that number may become more manageable.

Prohibition on balance billing for certain out-of-network care: Also known as “surprise medical bills,” balance billing can occur in medical emergencies, when insured patients are not necessarily able to choose an in-network hospital or provider as well as in non-emergencies when patients inadvertently receive care from an out-of-network provider at an in-network facility. In these cases, patients can be liable for the balance bill from the provider plus any cost sharing under their health plan. As of 2022, many of these types of balance bills are now prohibited under the No Surprises Act. The No Surprises Act generally protects patients with individual and employer-sponsored insurance by:

Requiring private health plans to cover these out-of-network claims and apply in-network cost sharing for certain covered benefits.

Prohibiting out-of-network providers, facilities, and providers of air ambulance services from billing patients more than in-network cost sharing for certain out-of-network care.

Requiring providers and facilities to provide patients with written notice explaining surprise billing protections, who to contact for concerns about potential violations, and how they can waive billing protections if they choose to do so.

Looking Forward

Consumer understanding of their coverage costs can play a significant role in seeking needed health care. One study found that lower health literacy scores were associated with consumers delaying or forgoing preventive care due to perceived health care costs. While better consumer education and outreach can help, the inherently complicated and profit-driven insurance and health care system includes few incentives to provide consumers with individualized and impartial assistance. However, several existing consumer protections, if implemented and enforced, as well as a broader health policy focus on how to improve the consumer experience, could make a difference.

Focus on price transparency: Despite a deregulatory agenda and recent cuts to agency staff, the Trump administration has directed the agencies to better enforce price transparency regulations. However, these machine-readable files with lists of prices and procedure codes currently have limited value to help consumers directly without an impartial analysis of the data and user-friendly vehicles to describe the information. Price estimators, also required as part of the Transparency in Coverage rule, have the potential to have more value to patients. However, while consumers may want an estimate of their expected out-of-pocket costs for a covered benefit, their awareness of the existence of these estimator tools and the likelihood of using them will influence how effective the regulation is at achieving its aims. Research conducted before and after its implementation showed mixed results on the consumer experience using these tools and their effectiveness in lowering out-of-pocket costs and health care costs overall. There is also concern that consumers will conflate high-cost with high-value care when price estimator tools do not incorporate quality metrics, potentially leading to higher health care spending. In an era of rapid developments in digital technology and artificial intelligence, ways to improve, consumer test, and standardize these tools and encourage their use may be one area of future focus.

Spotlight on cost-sharing protections: Getting renewed attention in the coming months and years are standardized cost-sharing designs that have or have the potential to provide more transparency and predictability about out-of-pocket costs for consumers. The U.S. Supreme Court will decide a case that could end free coverage of certain preventive care services recommended by the U.S. Preventive Services Task Force. A decision in that case is expected later this year. Consumers also await implementation of the Advanced Explanation of Benefits, as a key tool for patients to get cost information upfront. The coordination between plans and providers required for this initiative could go a long way to help patients often caught in the middle between plans and providers not working with each other in the best interest of consumers.

Finally, look for more attention to prescription drug costs and a cost-sharing protection that has been in place across all private insurance for over a decade, the maximum out-of-pocket limit, or cost-sharing limit. Many people who take certain high-cost medications receive financial assistance from drug manufacturers to offset their out-of-pocket costs. In recent years, private plans (excluding those offered to federal workers) have increasingly applied copay accumulators and copay maximizers when an enrollee receives this manufacturer assistance. Under these types of adjustment programs, the amount of financial assistance an enrollee receives does not count toward an enrollee’s out-of-pocket obligations, including the maximum out-of-pocket limit. Research has found that there is little transparency in how these programs operate and research has demonstrated that consumers are not always aware that their health plan contains these features. After a court challenge and a recent change in essential health benefit regulations, the federal government might be poised to confirm and clarify that cost sharing includes amounts received from pharmacy financial assistance programs and that plans must count those amounts toward the maximum out-of-pocket limit.

Continuing state-level initiatives to improve cost transparency: State-level initiatives that aim to improve cost transparency and help prevent medical debt could play a larger role if federal enforcement and regulations concerning consumer protections are stalled. New York, for example, enacted a bill in 2024 that bans a common provider practice, requiring patients to agree to cover the costs of a bill that their insurer does not cover before services are rendered (referred to as a “consent-to-bill” form) and requiring providers have a discussion with their patients about costs of services before signing this form. Although the state has indefinitely delayed full implementation of this law, the requirement for providers to discuss costs with the patient before asking them to sign the consent-to-bill form would still apply.

States continue wide-ranging activity to address high prescription drug costs in private insurance as public concern about high prescription drug costscontinues to mount. For example, pharmacy benefit manager (PBM) practices have been criticized for driving up prices and for being shrouded in secrecy. In response, many states have passed laws that aim to improve PBM transparency and reporting requirements, prohibit PBM policies that prevent pharmacists from telling patients when a lower-cost option might be available, and prohibit PBMs from steering enrollees to PBM-owned pharmacies, among others. Whether these laws apply to all private insurance, including self-insured private employer plans, is an open question.

This work was supported in part by a grant from the Robert Wood Johnson Foundation. The views and analysis contained here do not necessarily reflect the views of the Foundation. KFF maintains full editorial control over all of its policy analysis, polling, and journalism.

This volume features findings on beliefs about bird flu from KFF’s latest Tracking Poll on Health Information and Trust, as well as the false promotion of vitamin A as a preventative for measles. The Monitor also shares developments in content moderation on social media and how a study about mental health after gender-affirming care is misrepresented to make false claims about health care for transgender and non-binary people. Additionally, this volume explores when people prefer to use an AI chatbot, instead of a person, for health information.

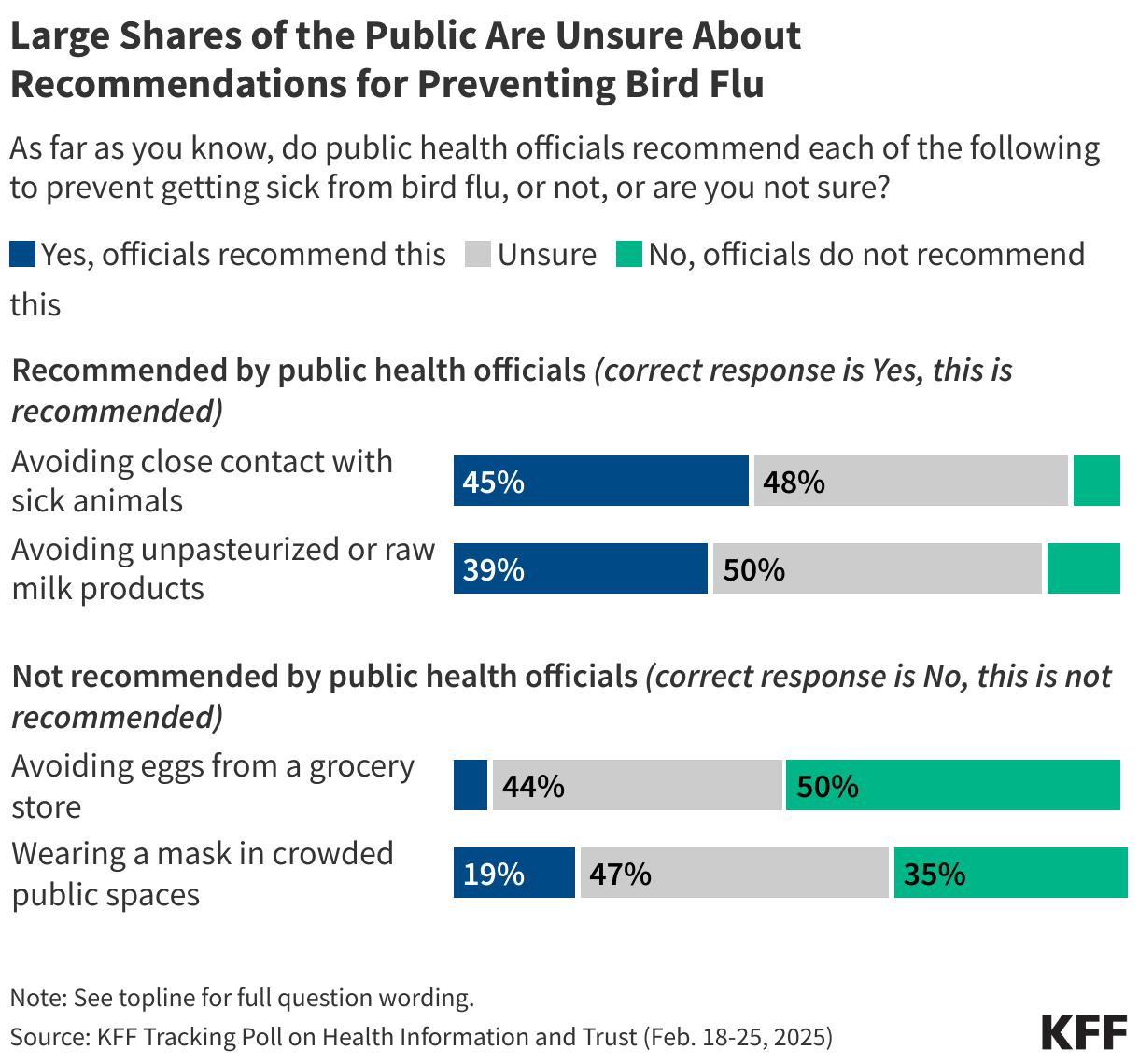

Featured: Latest KFF Poll Finds Many Are Unaware of Current Public Health Recommendations on Bird Flu

KFF’s latest Tracking Poll on Health Information and Trust finds that large shares of the public are unaware or unsure of what precautions are currently recommended by the CDC to protect individuals from bird flu. Fewer than half of adults are aware that public health officials recommend avoiding close contact with sick animals (45%) and avoiding unpasteurized or raw milk products (39%), with most adults saying they are either unsure or incorrectly saying these actions are not currently recommended. Half of the public is aware that public health agencies are not recommending avoiding eggs from a grocery store for bird flu prevention, while about one-third (35%) are aware that wearing a mask in crowded spaces is not currently recommended for bird flu prevention.

The survey also found notable partisan gaps when it comes to trust in the CDC for bird flu information. Fewer than half of Republicans (42%) say they trust the CDC at least a “fair amount” to provide reliable information about bird flu, compared to larger shares of independents (61%) and Democrats (72%) who expressed trust. This partisan divide on trust in the CDC is consistent with KFF’s past polling showing divisions in trust in the agency on health issues in recent years, but represents a shift from the start of the COVID-19 pandemic when at least eight in ten adults across partisans expressed trust in the CDC to provide information on coronavirus.

Recent Developments

False Claims about Vitamin A for Measles Prevention as Outbreak Grows

Natalya Maisheva / Getty Images

A measles outbreak in Texas and other states continues to grow, with cases quickly rising and multiple deaths reported. According to the Centers for Disease Control (CDC), two doses of the measles, mumps, and rubella (MMR) vaccine are 97% effective in preventing measles. However, growing concerns about vaccine safety have contributed to declining vaccination rates, exacerbating the outbreak. According to the Texas Department of State Health Services, only five patients diagnosed with measles in the current outbreak are known to have received at least one dose of the vaccine, although the department notes that some patients may have been vaccinated after exposure to reduce the risk of severe illness.

Alongside growing vaccine hesitancy, some are turning to nutrition as an alternative prevention method. One emerging narrative promotes vitamin A and other nutritional supplements as an effective way to prevent and treat measles. On March 4, a prominent organization that spreads false claims about vaccine safety shared a post on X stating that the CDC’s website now recommends vitamin A treatment for children who are hospitalized with severe measles. While the CDC has updated its measles guidance, it recommends vitamin A treatment only in a hospital setting and under a doctor’s supervision. Some comments advocated for the MMR vaccine and correctly warned that too much vitamin A without medical supervision may cause both short-term and long-term health complications, others falsely suggested that giving children high doses of vitamin A is a safe and effective way to prevent measles.

Vaccine opponents who promote this claim often cite research showing that vitamin A deficiency—which is rare in the U.S.—can increase the risk of death from measles and other infections to falsely suggest that vitamin A prevents measles. The World Health Organization recommends vitamin A along with vaccination for children at risk of vitamin A deficiency in countries where vitamin A deficiency is common, but it cannot prevent measles infection and long-term, repeated use can carry risks, including liver damage. Even a single large dose of vitamin A can cause nausea, vomiting, blurred vision, and dizziness.

The claims gained traction when Department of Health and Human Services (HHS) Secretary Robert F. Kennedy Jr. published an op-ed for Fox News where he acknowledged that vaccines prevent measles, but also wrote that “good nutrition remains a best defense against most chronic and infectious illnesses.” In an interview with Fox News, Kennedy said that doctors in Texas were giving cod liver oil, which is high in vitamin A, to their patients and “getting very, very good results.” He has since falsely claimed that the MMR vaccine causes the measles-like illnesses, including encephalitis, and leads to deaths every year. However, there are only three published reports of encephalitis among those who are vaccinated, and a study from the CDC’s Immunization Safety Office found no causal link between the MMR vaccine and death.

Social Media Health Content Moderation Under Scrutiny While FTC Launches Investigation

KFF / Unsplash

Meta is facing renewed criticism for restricting posts about abortion pills on Instagram and Facebook, with some accounts becoming undiscoverable in search results (“shadow banned”) or suspended entirely. Meta told The New York Times that it may have removed these posts or accounts if they violate the company’s policies on pharmaceutical sales, but reproductive health groups argue that these actions limit access to health information following the Supreme Court’s decision to overturn Roe v. Wade. Meta has recently pledged to scale back its fact-checking in an effort to uphold free speech, but these recent actions have led some, including U.S. Senator Ruben Gallego, to question whether Meta’s commitment to free speech applies equally to all issues.

Recent policy actions may further shape how health information is moderated online. In February, the Federal Trade Commission (FTC) launched an investigation into potential censorship by technology platforms, inviting public comments from users who have been “banned, shadow banned, demonetized, or otherwise censored.” As of March 11, more than 1,200 comments had been submitted, with some users reporting past removals of COVID-19 posts. In 2024, the Supreme Court reviewed the Biden administration’s role in moderating social media content on topics like COVID-19 and vaccines, but ruled that the plaintiffs did not have standing to bring the case. The FTC investigation follows an executive order from the Trump administration aimed at ending federal involvement in content moderation, while examining past efforts to curb health misinformation. While the executive order opposes censorship, other actions by the Trump administration have been accused of promoting it, including efforts to restrict information on gender equity.

Study on Transgender Mental Health Misrepresented to Discredit Gender-Affirming Care

A new study on the mental health of transgender people after gender-affirming surgery is being misrepresented to claim that gender-affirming care causes poor health outcomes. The retrospective study, published in the Journal of Sexual Medicine, found that transgender adults who had gender-affirming surgery were more likely to report negative mental health outcomes than transgender adults who did not have surgery. However, the authors do not attribute this effect to the surgery, stating instead that these findings may reflect: that individuals receiving gender-affirming surgery experience higher levels of baseline psychological distress compared to those who do not, provider charting practices that are more likely to record gender dysphoria prior to surgery and other mental health diagnoses after surgery, or that those individuals receiving surgery interact with the health care system more often and therefore have more opportunities for mental health diagnoses to be charted.

Transgender people often experience depression and anxiety due to minority stress, including enduring ongoing experiences of stigma and discrimination, even after transitioning. Discrimination in health care settings can further limit access to mental health care and contribute to systemic distrust. A 2023 KFF-Washington Post poll found that a majority of transgender adults (64%) have been verbally attacked because of their gender or sexual identity, while about three in ten trans adults said they had to teach a doctor about trans people to get appropriate care or had a doctor refuse to acknowledge their preferred gender identity. However, the poll also found that eight in ten (78%) trans adults say that living as a gender different from the one assigned to them at birth has made them “more satisfied” with their lives.

On X, a podcast host and author with approximately 4.8 million followers shared a screenshot of an article about the study and misinterpreted it to allege that gender-affirming surgery worsens mental health. As of March 11, the post received about 45,000 likes, 17,000 reposts, and 2,400 comments. Other X users, including commenters on the post, correctly noted that stigma may contribute to trans people experiencing ongoing mental health symptoms before and after surgery and that the study did not account for undiagnosed mental health outcomes before surgery. Some cited previous research showing that gender-affirming surgery is associated with improved mental health and noted that regret rates for gender-affirming procedures are significantly lower than those for other types of surgeries. More broadly, studies have found positive associations between gender-affirming care and mental health.

AI & Emerging Technology

Study Finds People Prefer Chatbots When Embarrassed, But Humans When Angry

d3sign / Getty Images