KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

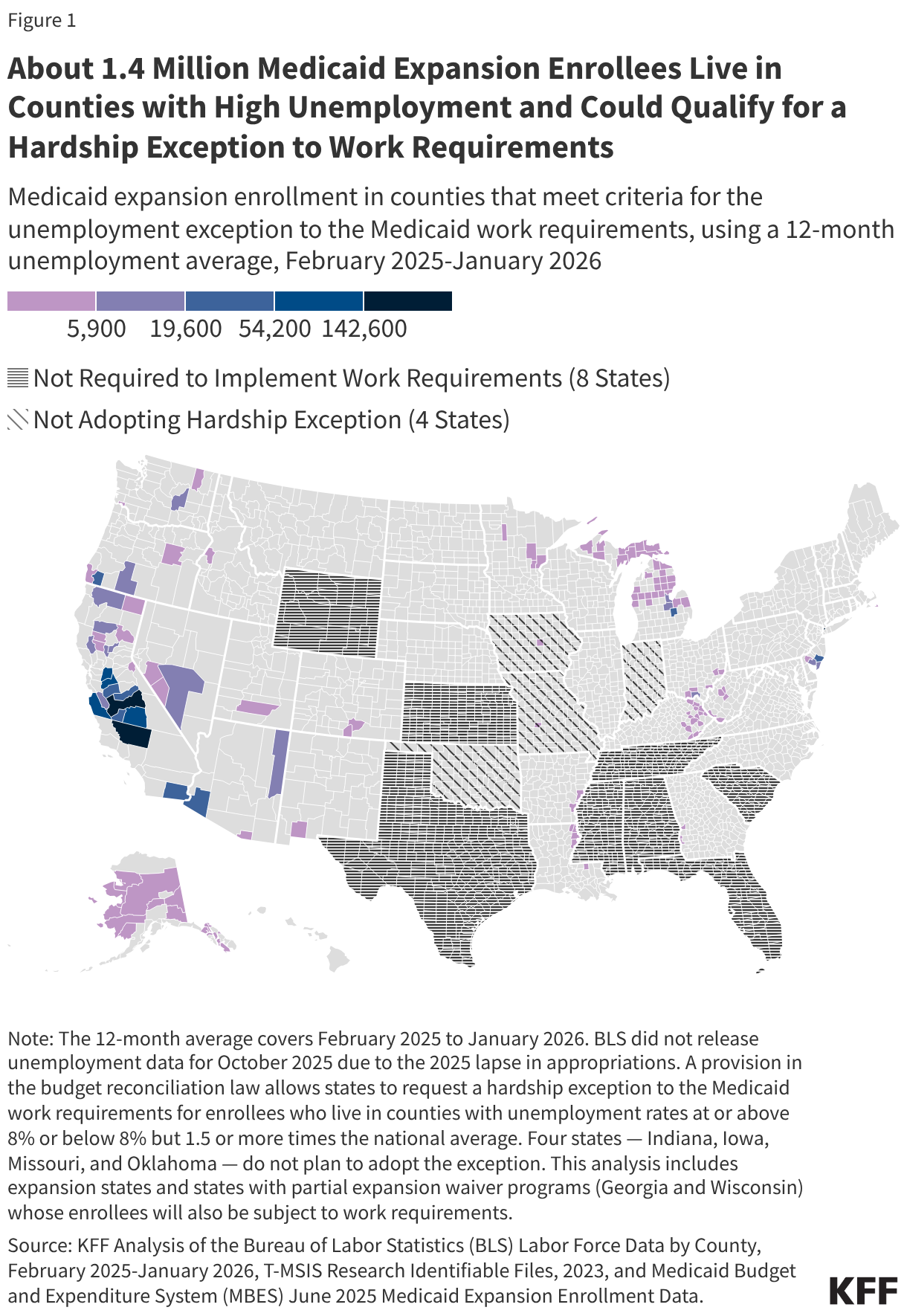

The 2025 reconciliation law will—for the first time—require adults who are enrolled in Medicaid though the Affordable Care Act (ACA) expansion, along with those in partial expansion waiver programs in Georgia and Wisconsin, to meet work requirements or qualify for an exemption as a condition of eligibility starting in January 2027 in most states.

States may adopt an optional hardship exception to Medicaid work requirements for individuals living in counties with unemployment rates at or above 8%, or at least 1.5 times the national average unemployment rate. A recent KFF survey found that most states plan to adopt this exception, which will exempt both Medicaid applicants and enrollees in counties with unemployment rates that meet the specified thresholds. However, four states, Indiana, Iowa, Missouri, and Oklahoma, do not plan to adopt the exception.

An update to a previous KFF analysis of county unemployment rates, using 12-month average unemployment rates from February 2025 through January 2026, and county-level Medicaid expansion enrollment estimates that:

1.4 million expansion enrollees, or 7.5% of expansion enrollees, live in counties that meet the high unemployment threshold and may qualify for the hardship exception in the 27 states that plan to adopt the exception and in the 12 states that had not made a decision on adoption at the time of the KFF survey.

Among the states that are planning to adopt or may adopt the exception, 133 counties in 22 states meet the high unemployment thresholds, representing 7% of counties in expansion states and states with partial expansion waiver programs. No counties meet the thresholds in 16 states, and DC does not meet the thresholds.

Nine in ten expansion enrollees who are in counties that meet the high unemployment criteria and could be exempt from the work requirements live in five states—California, New York, Michigan, New Jersey, and Oregon.

Among the states that do not plan to adopt the hardship exception, two counties in Iowa and Missouri meet the high unemployment thresholds, and approximately 3,300 expansion enrollees in those counties may have qualified for the high unemployment hardship exception if the states had decided to adopt the exception. In Indiana and Oklahoma, there are no counties that meet the thresholds.

Nebraska began enforcing work requirements on May 1, 2026, the first state to implement the new requirements. Although the state indicated it would adopt the high unemployment hardship exception, no counties in the state currently meet the thresholds.

States are waiting for federal guidance on how to implement this hardship exception, including what data will be used to identify counties that meet the thresholds and what additional information states must submit. This analysis uses the most recent available county-level unemployment data from Bureau of Labor Statistics (BLS) and is consistent with the methods used to determine whether any counties qualify for the high unemployment exemption waiver from SNAP work requirements. However, the guidance, which CMS is expected to release in early June, may require a different method.

KFF’s interactive Medicaid work requirements tracker includes new county-level unemployment data by state, showing which counties meet the high unemployment thresholds and how many expansion enrollees in those counties may be exempt from work requirements.

The President’s Emergency Plan for AIDS Relief (PEPFAR) has been and continues to be subject to a range of Congressional reporting requirements. These include enduring (ongoing) requirements as well as time-bound requirements, through both PEPFAR’s authorizations as well as appropriations legislation in some years.

This document provides a list of reporting requirements identified in PEPFAR’s authorizing legislation over time as well as other key legislation. Table 1 includes current requirements and requests. Table 2 includes past requirements and requests that are no longer in effect. While this document lists most such requirements, it may not be exhaustive.1

There are other requirements [such as those that are not specific to PEPFAR established under the Foreign Aid Transparency and Accountability Act (FATAA) of 2016, for example, which includes more general reporting requirements; and some in appropriations legislation, along with accompanying congressional reports and explanatory statements, over the more than 20 years of PEPFAR] that are not included in this analysis. ↩︎

Note: The map in this brief will be updated regularly to include new federal actions about potential Medicaid fraud and new state responses. The brief was last updated on May 15, 2026.

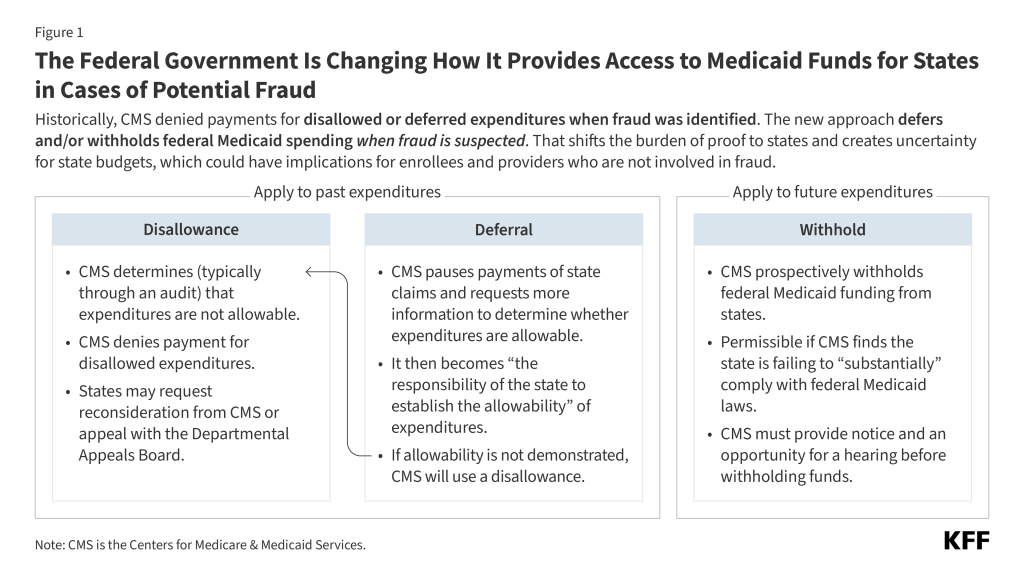

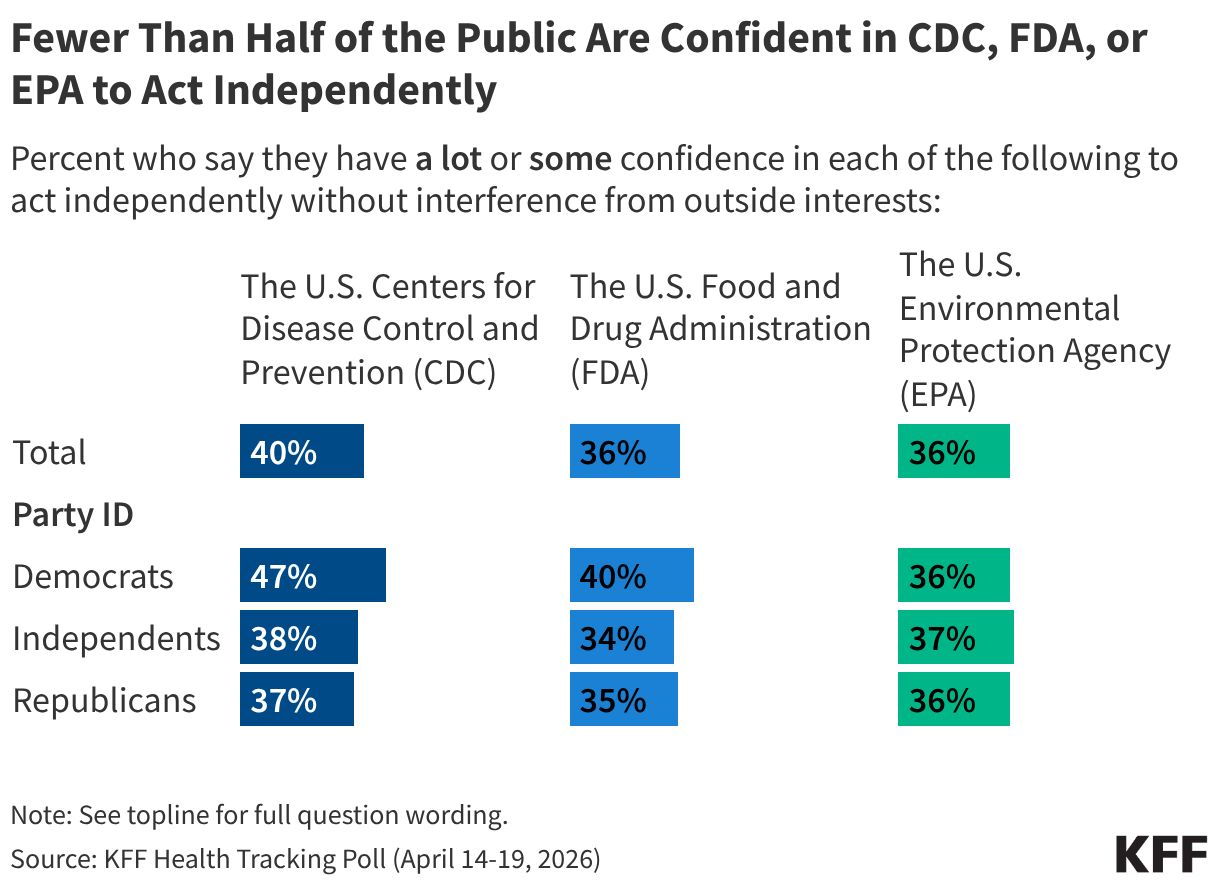

The current administration is placing a new emphasis on potential fraud in Medicaid with its Comprehensive Regulations to Uncover Suspicious Healthcare (CRUSH) initiative. The Centers for Medicare and Medicaid Services (CMS’) started the new initiative in Medicaid focusing on Minnesota and three other states with Democratic governors (California, Maine, and New York) while the House Committee on Energy and Commerce sent requests for information to 11 states. CMS has historically partnered with states to identify and resolve issues of fraud, waste, and abuse, and denied the federal share of Medicaid spending when fraud has been identified by an audit, investigation, or reported by the state. However, CMS has recently announced a new approach to fraud that will rely more heavily on options to prevent spending federal funds in cases of potential fraud, which could have broad implications for states and enrollees. This issue brief explains the new approach. Key findings include:

CMS’ historic practice has relied on disallowing federal Medicaid payments when fraud is identified (typically through an audit), a process that may take several years to implement.

CMS’ new approach to potential fraud involves potentially pausing or withholding federal Medicaid payments when fraud is suspected (Figure 1). This approach differs from prior approaches because, if implemented, it could have more immediate consequences, place a much larger share of federal spending at risk (including spending that pays for services uninvolved in fraud), and proactively shift the burden of proof to states to obtain federal funds.

While all approaches aim to limit future fraudulent payments using tools such as corrective action plans, the new approach to federal Medicaid spending when fraud is suspected creates uncertainty for state budgets and could have implications for Medicaid enrollees and providers who are not involved in fraud.

What is a disallowance?

The federal and state governments share responsibility for financing Medicaid, and states draw on federal funds to pay health care providers and health plans for providing health care to enrollees. The federal government makes quarterly grant awards to states to cover the federal share of Medicaid spending. Awards reflect states’ estimated expenditures for the upcoming quarter and adjustments from prior quarters’ expenses. Adjustments reflect various considerations such as:

Instances where states’ estimated expenditures are higher or lower than actual expenditures

Changes to accounting practices or federal matching rates

Reductions in payment resulting from claims where fraud has been identified

Publicly-available data on Medicaid expenditures show the total amount of adjustments each year, reflecting the net impact of all various factors, and do not specifically identify adjustments due to disallowances and deferrals.

Historically, CMS has used disallowances to deny federal matching funds for state Medicaid expenditures that have already occurred and are later determined to be not allowable. There is limited information available about the frequency and scope of Medicaid disallowances, but an older report by the Government Accountability Office (GAO) suggests that they were not infrequent between 2014 and 2017.Upon receiving a disallowance notice, states may request that CMS reconsider the decision and provide additional information to CMS to demonstrate that the expenditures were allowable or accept the disallowance and resolve it directly with CMS. In all cases, once CMS has issued a disallowance, “the state has the burden of documenting the allowability” of the expenditures to overturn the disallowance. When states request a reconsideration, CMS has 60 days to decide, although this timeline may take longer if CMS requests additional information from the state.

States may appeal the disallowance decisions to a Departmental Appeals Board, but the state still has the burden of proof for documenting the allowability of expenditures and the process may take years to resolve. States are not required to request a reconsideration before appealing the disallowance. More information is publicly available for cases where states do appeal the decisions than for cases where they settle or request a reconsideration. In such cases, data about the decisions of the Department Appeals Board are available online through the Department’s website. Between 2020 and 2025, the Departmental Appeals Board has issued 12 Medicaid disallowance rulings (with 6 rulings being an appeal of a prior case). In all 6 new rulings, there were on average 15 years between the oldest year of disputed expenditures and the final ruling, highlighting how long it takes to resolve these cases (see Figure 2 for an example from Texas). All cases were decided in favor of CMS, but that may reflect the fact that CMS has historically used disallowances only in cases where fraud is well-established.

The amount of disputed disallowances where the Departmental Appeals Board issued a ruling between 2020 and 2025 ranged from less than $500,000 to almost $200 million, but these amounts reflect differences in the number of years and scope of services within the disallowed claims. Some of the largest disallowances to be upheld involve disproportionate share hospital (DSH) payments.

The largest disallowance ruling between 2020 and 2025 was $195.7 million in a case involving Michigan’s DSH payments between 2001-2009. In that instance, CMS in 2018 determined that the state had made DSH payments to a small number of hospitals that were ineligible to receive them. The Departmental Appeals Board ruling was in 2024.

The second largest disallowance ruling between 2020 and 2025 was for more than $97 million in a case where Florida made DSH payments between 2006-2013 in excess of the limits established for specific hospitals (CMS first issued this disallowance in 2016 and the Departmental Appeals Board ruling was in 2021).

Figure 2

What is a deferral?

With deferrals, CMS pauses payment for state Medicaid expenditures that have already ocurred and requires the state to provide additional information demonstrating that expenditures are “allowable.” Deferrals are usually initiated by the federal government and may be used to pause federal funding while the state and federal governments work out the details of a disallowance, and in cases where fraud, waste, or abuse has been identified and the state and federal governments are gauging the extent of the issue. In the past, deferrals were used as temporary measures that pause funding until CMS either reimburses the expenditures or issues a disallowance. Deferral notices must specify the reason for the deferral and include a request for all documents and materials that CMS believes are necessary to determine whether the expenses are allowable. After the notice is sent, the loss of federal funds occurs immediately.

After receiving a deferral notice from CMS, states have 60 days to provide all requested documents and materials unless they request an additional 60-day extension. CMS usually begins document review within 30 days but may request different formats or additional materials from the state. States have 15 days to submit additional materials and if they do not meet that deadline, CMS disallows the expenses. Once all documents are available, CMS has 90 days to review and determine whether expenditures are allowable. If CMS determines expenditures are not allowable, the disallowance process begins, offering the state the opportunity to request a reconsideration and appeal to the Departmental Appeals Board.

Deferrals are receiving new attention after the administration announced that it would temporarily defer $259 million in federal Medicaid payments to Minnesota for expenditures incurred in quarter 4 of in fiscal year (FY) 2025, an unprecedentedly large amount. In the announcement, CMS noted that it may continue to defer federal payments for either additional quarters in 2025 or future quarters in 2026, and that similar announcements for other states would likely be coming soon. As of March 25, 2026, 4 additional states have received formal letters from CMS requesting information about program integrity, and 11 states have received formal letters from the House Committee on Energy and Commerce (Figure 3).

What is a withhold?

In January 2026, CMS notified Minnesota that pending the outcome of a hearing, it would begin withholding $515 million in quarterly federal Medicaid payments moving forward, a process that has seldom been used in prior years. Withholding funds has been referred to as the “compliance process” because it is only permissible in cases where the state is failing to comply with Medicaid law. Prior use of withholding has been limited. When CMS has considered withholding as a compliance tool in the past, it announced withholdings that were at most between 1 and 10 percent of the federal share of Medicaid spending for specific services (in most cases, the administrative costs states incurred to implement their Medicaid programs). Prior CMS communication notifying states of possible withholdings appear to have been used when states incorrectly restrictedeligibility or benefits, thus failing to comply with minimum requirements regarding access to coverage or eligibility. Minnesota’s case is different because of the scope of the proposed withholding and because the proposed withholding would be to address potential future fraud, rather than state policies that restrict Medicaid eligibility or benefits. The announced level of withholding would have represented nearly 20% of the federal share of Minnesota’s spending on an annual basis.

To withhold federal Medicaid funds, CMS must first provide states with the opportunity for an administrative hearing, and withholding generally ends when CMS is satisfied with states’ resolution of the issue. Withholdings may reflect issues with states’ Medicaid approved plans or with states’ implementation of the plans. Because CMS has authority to approve states’ plans, most issues arise regarding implementation of the plan and are resolved using a corrective action plan. Corrective action plans may also be used to address other types of issues in Medicaid (such as payment error rates or eligibility re-determinations). In general, the plans include a narrative of steps states are planning to take to address issues related to proper implementation of the Medicaid program. On January 13, 2026, Minnesota requested a hearing about the withholding and on January 30, 2026, Minnesota submitted a revised corrective action plan to CMS. On March 20, 2026, CMS accepted Minnesota's revised corrective action plan. Successful completion of the corrective actions outlined in the plan will resolve the threat of withholding.

What are the implications of new reliance on deferrals and withholds?

The new approach to federal Medicaid spending when fraud is suspected creates uncertainty for state budgets, particularly given the magnitude of federal funding at stake and the time it takes to resolve administrative disputes. Unlike the federal government, states must generally operate balanced budgets, which is one reason states are able to draw down matching funds to finance ongoing expenditures. If withholding is implemented, the loss of federal funds could make it difficult for states to maintain current programs while details of the cases are being sorted out. More extensive use of deferrals could have similar, but more immediate, destabilizing effects on states’ budgets because they reduce the amount of federal funds available to states for several months, and the state has no option to request reconsideration or appeal until a disallowance is issued. Increasing the use of deferrals so that it applies to entire categories of services where fraud is suspected but not established would also place a new administrative burden on states to demonstrate the allowability of expenditures. Other approaches to addressing suspected fraud, waste, and abuse remain available to CMS. The National Association of Medicaid Directors (NAMD) has suggested the following actions to help states to address fraud waste, and abuse in Medicaid:

Help states identify federal materials about best practices such as recommendations and provider enrollment self-assessments;

Create rapid methods to share information about provider disqualifications between Medicare, the Veterans' Health Administration, and Medicaid;

Respond more quickly to fraud reports from state attorneys general and the Medicaid Fraud Control Units;

Strengthen procedural pathways for states and CMS to work collaboratively on Corrective Action Plans to enhance adherence to provider requirements while maintaining access to Medicaid benefits;

Conducting additional analysis of Medicaid data through the Center for Program Integrity;

Strengthening federal data sources and their interoperability; and

Providing technical assistance to state officials and staff.

New uncertainty about the availability of federal funding could have implications for Medicaid enrollees and providers who are not involved in fraud. If states have inadequate funding to maintain existing Medicaid services, they may face difficult decisions regarding how to limit Medicaid spending. In general, states can reduce Medicaid spending by decreasing payment rates for providers, covering fewer services, or enrolling fewer people. Such actions could affect enrollees and providers who are not using or providing services in which fraud is suspected. There will also be additional disruptions for providers who lawfully provide Medicaid services where fraud is suspected because of new administrative burdens associated with increased audits, delayed payments, and other administrative practices.

CMS’ new approach to addressing cases of suspected fraud may exacerbate administrative and financial challenges states face as they implement the 2025 reconciliation law. The 2025 reconciliation law made historic reductions in federal funding for Medicaid and created new administrative requirements for states, particularly those that must implement work requirements for enrollees eligible for Medicaid through the Affordable Care Act Medicaid expansion. As states work to implement those changes and adjust to changes in federal financing, the new approach to fraud creates additional administrative requirements and potential new reductions in federal funding. Combined, these changes may have more significant implications for states’ ability to maintain existing levels of Medicaid payment rates, coverage, and eligibility.

The American Association of Public Opinion Research (AAPOR) last night recognized KFF’s Mollyann Brodie, Ph.D., with the AAPOR Award for Distinguished Achievement for her outstanding leadership and contributions to the field of public opinion research over three decades.

The award honors Dr. Brodie, a KFF executive vice president and executive director of KFF’s Public Opinion and Survey Research, for leading KFF’s polling team as it has built a body of work “that has become the nation’s definitive source for public opinion on health — earning the confidence of policymakers, journalists, and the public alike.”

The association notes Dr. Brodie’s role in developing the KFF Health Tracking Poll, which has documented the arc of the public’s opinions on and experiences with the Affordable Care Act and provided a record of how sweeping legislation affects ordinary Americans, and the KFF COVID-19 Vaccine Monitor, which became a critical resource for understanding the public’s views, access, uptake, and concerns about emerging vaccines. “In each case, her vision produced research that went beyond poll numbers to tell the broader story of how Americans experienced major changes in health and health care,” AAPOR noted in its award citation.

AAPOR also praised Dr. Brodie’s commitment to inclusion for women and other underrepresented groups, both in her work at KFF and as a leader within the association. The association notes her role in developing methodologically innovative surveys of working-class Americans, transgender adults, Hurricane Katrina evacuees, and rural communities — populations whose voices too rarely get elevated in other nationally representative polls.

In addition, KFF’s Surveys of Immigrants received the 2026 AAPOR Inclusive Voices Award, which recognizes work examining complex challenges related to underrepresented populations.

The multi-year initiative, including surveys conducted in partnership with The New York Times and The Los Angeles Times, is the only large-scale, nationally representative probability-based survey of immigrants in the United States in decades. Through innovative multi-frame, multilingual, and multi-mode methods, the surveys succeeded in amplifying the voices of groups often excluded from survey research, such as undocumented immigrants and those with limited English proficiency.

“We started our polling program when we started KFF in the early 1990s, but it made the jump to light speed after Molly arrived. These awards recognize her expertise and vision, and how effective we’ve been in coordinating our polling under Molly’s leadership with our equally tremendous capacity in policy research and journalism,” said Dr. Drew Altman, Founding President and CEO, KFF.

At KFF, Dr. Brodie works closely with Senior Vice President and Director of Public Opinion and Survey Research Liz Hamel, Director of Survey Methodology Dr. Ashley Kirzinger, and Dr. Altman, in addition to the policy research team led by Executive Vice President Larry Levitt, and journalists at KFF Health News. She also helped develop KFF’s polling partnerships with major news organizations, including The New York Times and The Washington Post. Dr. Brodie and Mr. Levitt are the executive team who work with Dr. Altman to oversee all of KFF’s program directions, finances, and operations.

The awards were presented last night at AAPOR’s 81st annual conference in Los Angeles.

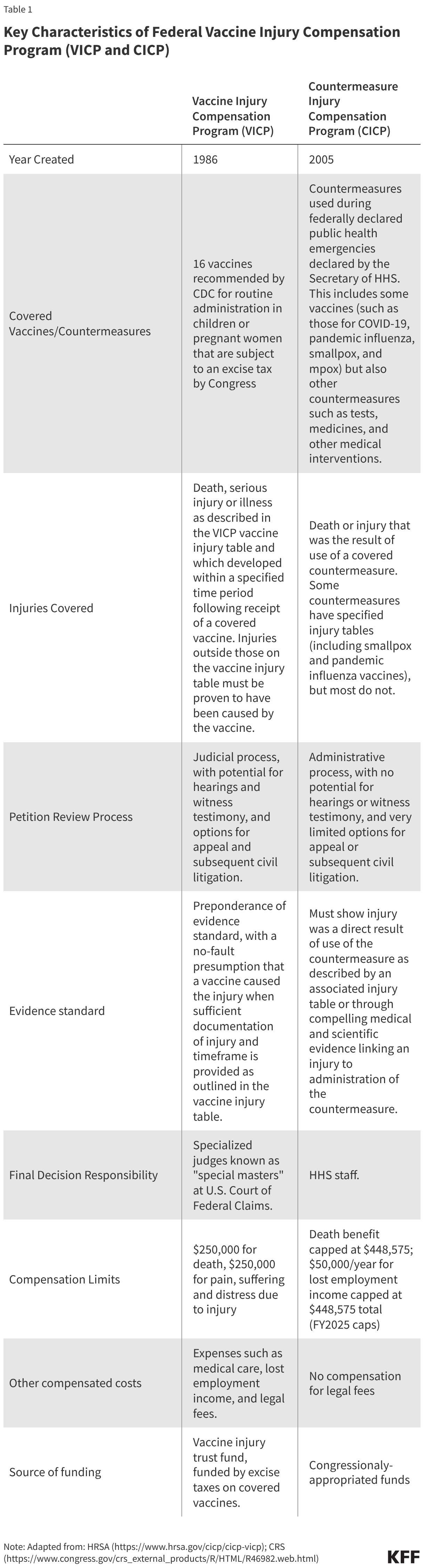

For decades, the federal government has overseen two key vaccine injury compensation programs: the National Vaccine Injury Compensation Program (VICP) and the Countermeasures Injury Compensation Program (CICP). The VICP and CICP are designed to help maintain vaccine access while also recognizing that vaccine injuries can occur and those affected by such injuries should be compensated. However, over time, the demands on, and challenges faced by, these programs have grown. Recently, they have become targets of criticism from members of the Trump administration, including the Secretary of Health and Human Services (HHS) Robert F. Kennedy Jr. ,who said (without evidence) in 2025 that VICP had “devolved into a morass of inefficiency, favoritism, and outright corruption” and that he would lead an effort to overhaul it. Some lawmakers and external groups have called to replace or end these programs while others have suggested keeping them intact but adopting policy changes that could help modernize them and make them more effective. Some have raised concerns that making drastic changes to vaccine injury compensation programs could undermine the U.S. vaccine market and, more generally, confidence in vaccines.

To provide background and context on this topic, this brief summarizes the history and rationale for these programs and their key elements, analyzes publicly available information on claims and compensation under the programs, and discusses key policy issues they currently face. The programs, while both having been created as alternatives to civil courts, vary significantly in their structures, processed, vaccines covered, and compensation rates and amounts, among other factors.

Origins and Rationales for VICP and CICP

VICP and CICP were both created as alternative pathways to civil courts to allow individuals to seek compensation for vaccine-related injuries and address vaccine safety while also addressing concerns about vaccine supply in the U.S. Prior to the existence of these programs, there were times when vaccine manufacturers faced a large volume of lawsuits linked to rising public concerns about vaccine safety, which threatened to drive vaccine makers from the market and led them to raise their prices, affecting access to vaccines.

VICP, created by Congress in 1986, was designed as a legal pathway separate from traditional civil courts through which individuals can seek compensation for potential vaccine injuries directly from the federal government. VICP was created by Congress following a wave of public concern regarding vaccine safety in the late 1970s and 1980s that was fueled, in part, by sensationalizedtelevision programs on the topic of vaccine injuries in children. There had been a surge in lawsuits in the civil court system filed against health care practitioners and vaccine makers. Facing rising legal costs, some vaccine manufacturers chose to exit the vaccine market and those that remained raised their prices, which threatened the market for childhood vaccines in the U.S. In response, Congress passed the 1986 National Childhood Vaccine Injury Act (NCVIA) that, among other things, established the VICP. It was intended to help stabilize the vaccine market, preserve public confidence in immunization, while also providing a less adversarial and more streamlined pathway for families to submit claims and receive compensation payments for vaccine injuries compared to civil litigation. The act created the process by which vaccines could be added to VICP coverage and created the VICP trust fund, which funded the program using excise taxes placed by Congress on each of the vaccines covered under VICP. Congress has made several statutory changes and additions to VICP since 1988, including the 1993 Omnibus Budget Reconciliation Act that allowed for rapid inclusion of new U.S. Centers for Disease Control and Prevention or CDC-recommended vaccines into VICP once Congress enacted the excise tax on that vaccine, and the 21st Century Cures Act from 2016 that added vaccines recommended for pregnant women to VICP and explicitly included injuries to children in utero as eligible for VICP compensation.

CICP was created by Congress in 2005 to allow individuals to seek compensation for injuries that may have occurred from use of medical countermeasures (such as vaccines) during a public health emergency (as distinct from routine use addressed under VICP). It was established as part of the Public Readiness and Emergency Preparedness (PREP) Act, at a time of heightened national security concerns following the September 11, 2001 attacks, anthrax mailings, and the threat of an influenza pandemic. The PREP Act was meant to address concerns that in a public health emergency, such as a bioterrorist attack or a naturally occurring outbreak, private companies might be reluctant to develop and manufacture vaccines, drugs, and other medical countermeasures because of liability risks they could face from use of those products during an emergency. As part of a broader strategy incentivizing rapid development and deployment of countermeasures, the PREP Act offered immunity from liability to manufacturers and distributors of these products, and created the CICP as the federal compensation mechanism for injuries that may occur through use of these products.

Vaccines and Injuries Covered, and Processes for Review and Compensation

While both VICP and CICP are designed to be more efficient and streamlined mechanisms compared to civil courts for vaccine injury compensation cases, they are distinct in terms of which vaccines are covered and how claims are submitted, reviewed, and adjudicated (see Table 1 for a comparison of key characteristics of these programs).

VICP

There are currently 16 vaccine types covered under the VICP program. By statute, VICP covers FDA approved vaccines used in the U.S. that are 1) recommended by the CDC for “routine administration” to children or pregnant women, 2) subject by Congress to the VICP excise tax, and, 3) added to the official VICP vaccine injury table by the Secretary of HHS. When first passed in 1986, VICP covered 6 vaccines, a number that has grown to 16 existing vaccines, including the components of common childhood vaccines such as DPT, MMR, and polio as well as child and adult vaccines such as seasonal influenza. The VICP also covers “any new vaccine” recommended by CDC, subject to an excise tax and issued a notice of coverage by the Secretary of HHS.

The vaccine injury table is a key VICP document listing vaccine types and injuries compensable by VICP. The table lists and explains injuries presumed to be caused by vaccines and the time periods in which the first symptom of these injuries must occur after receiving the vaccine. The current table lists 14 compensable injuries across the 16 vaccine types, with most injuries associated with one or a few vaccine types only. For example, “chronic arthritis” is listed as a potential injury associated only with rubella-containing vaccines, and “vaccine-strain polio infection” is only associated with oral polio vaccine. Others are associated with multiple vaccine types, such as “shoulder injury” and “vasovagal syncope” (i.e. a drop in blood pressure and heart rate), which are each listed for 15 vaccine types.

VICP claims are submitted to HHS and the U.S. Court of Federal Claims and reviewed through a judicial process overseen by the Office of Special Masters. An individual (or legal representative) must first file a petition with the U.S. Court of Federal Claims “Office of Special Masters” which handles VICP cases. “Special Masters” are specialized officers of the court who function similarly to a judge. Upon receipt, each claim is assigned to one of eight Special Masters and initially reviewed by specialized HHS staff for compliance with VICP submission requirements. Documentation to support an injury claim must be provided, and typically only injuries listed on the vaccine injury table are eligible for compensation. For injuries not on the table, a petitioner must prove, through medical documentation and/or expert opinion, that the vaccine in fact caused the alleged injury. VICP typically pays petitioners’ legal fees, even if the claim is eventually unsuccessful.

Special Masters issue a ruling on compensation based on a “preponderance of evidence” standard. VICP is designed as a no-fault system, meaning petitioners do not need to prove negligence on the part of vaccine makers or health care practitioners. With sufficient documentation of an injury matching a condition and fitting the timetable listed on the vaccine injury table, it is usually presumed that the vaccine caused the injury. In some cases, additional information is needed such as expert testimony or medical research findings to support injury claims, and evaluating evidence may require hearings with witnesses.

Petitioners can accept or reject a compensation decision, with the option for appeal. If a ruling is made in favor of a petitioner, the Special Master determines the level of compensation, which a petitioner can accept or reject. If the claim is denied, the petitioner can seek review by a judge of the Court of Federal Claims and potentially appeal further to the U.S. Court of Appeals. If the claimant moves through all appeals and is still denied compensation, then they may have the right to subsequently file a suit in civil court (with some limitations).

The Secretary of HHS can modify the VICP vaccine injury table, though changes must abide by a statutory process including external expert review and a public comment period. The Secretary of HHS has the explicit authority to modify the vaccine table, though any changes are subject to a process outlined in statute (42 U.S.C. § 300aa-14) and federal regulations (Code of Federal Regulations (CFR) Part 100), including referred to an external expert advisory body known as the Advisory Commission on Childhood Vaccines (ACCV), which has at least 90 days to review suggested changes. In addition, HHS must follow Administrative Procedures Act (APA) guidelines, including publishing a Notice of Proposed Rulemaking (NPRM) in the Federal Register and a 180-day public comment period. Adding a new vaccine to the vaccine injury table requires that new vaccine to be recommended for routine use by CDC, and for Congress to apply an excise tax on that vaccine, before HHS can publish a notice of coverage and submit related changes to the vaccine injury table.

The VICP vaccine injury table has rarely been updated; its last major revision was in 2017. At that time, “Shoulder Injury Related to Vaccine Administration, or SIRVA was added. HHS proposed adding this to the Table, submitted it to ACCV for input, and in 2015 published the related NPRM. In 2017 HHS issued the final ruling after reviewing and responding to public comments, as required under APA.

CICP

CICP covers countermeasures used in federally declared public health emergencies, which has included COVID-19 vaccines, as well as vaccines for pandemic influenza, smallpox, and mpox. By statute, covered countermeasures are those that the Secretary of HHS specifically lists in the declarations issued under the PREP Act for each health emergency. Currently, there are 10 such declarations in effect covering countermeasures against health emergencies, including Anthrax, Ebola, Marburg, pandemic influenza, mpox, and COVID-19.

CICP claims are reviewed through an administrative process by HHS staff, rather than a judicial process. Individuals submit a request to the Health Resources and Services Administration (HRSA) within HHS, which administers CICP. Filings must include sufficient medical records and other documentation linking the countermeasure and the individual’s claimed injury. In contrast to VICP, there no judges or hearings under CICP. Instead, claims are reviewed internally by HHS medical and legal staff. CICP does not pay petitioners’ legal fees.

CICP does not have a single “injury table” reference for covered countermeasures, with claims typically requiring individualized, case-by case review. Some declared health emergencies – including smallpox and pandemic influenza – have a specified countermeasure injury table, but most do not (COVID-19 countermeasures, for example, do not have an injury table). Therefore, most claims require individualized scientific review and case-by-case considerations. To receive compensation, a petitioner must show “serious physical injury was sustained as the result of the use of a covered countermeasure,” which is a higher evidentiary standard compared to VICP.

CICP decisions leave little room for appeal. HRSA issues a written determination on whether the injury is eligible for compensation under CICP and, if found eligible, how much compensation is awarded. If found ineligible, a petitioner can request reconsideration, but further review is still handled internally, with no process for formal legal appeal. In most cases, individuals who have pursued compensation through CICP cannot go on to pursue lawsuits in civil court against manufacturers or providers for covered countermeasures.

The HHS Secretary has broad authority to make changes to countermeasures and injuries covered under CICP. The PREP Act provides the HHS Secretary more discretion and imposes fewer regulatory requirements on the process to make changes to injuries covered by CICP, compared to VICP. The Secretary can determine which countermeasures are covered and which injuries are presumed to be compensable under the CICP, and there is no statutory requirements for advisory committees or public comment periods for changes to these policies.

Historical Data on Petitions and Compensation Decisions

The number of petitions submitted to VICP and CICP has varied over time, and both programs have seen large increases in petitions in certain years driven by different factors, such as a surge in CICP claims related to COVID-9 vaccines starting in 2021 (COVID-19 claims comprise most CICP petitions at this point). Overall, VICP provides compensation for a much greater share of its petitions compared to CICP (48% compared to less than 1% for COVID-19 vaccine petitions), largely reflecting the differences between the programs. Still, given the large number of vaccines administered in the U.S., very few petitions or claims in either program are found to be compensable relative to vaccines received (1.89 VICP compensable petitions per million vaccine doses and 0.14 compensable CICP claims per million COVID-19 vaccine doses).

VICP

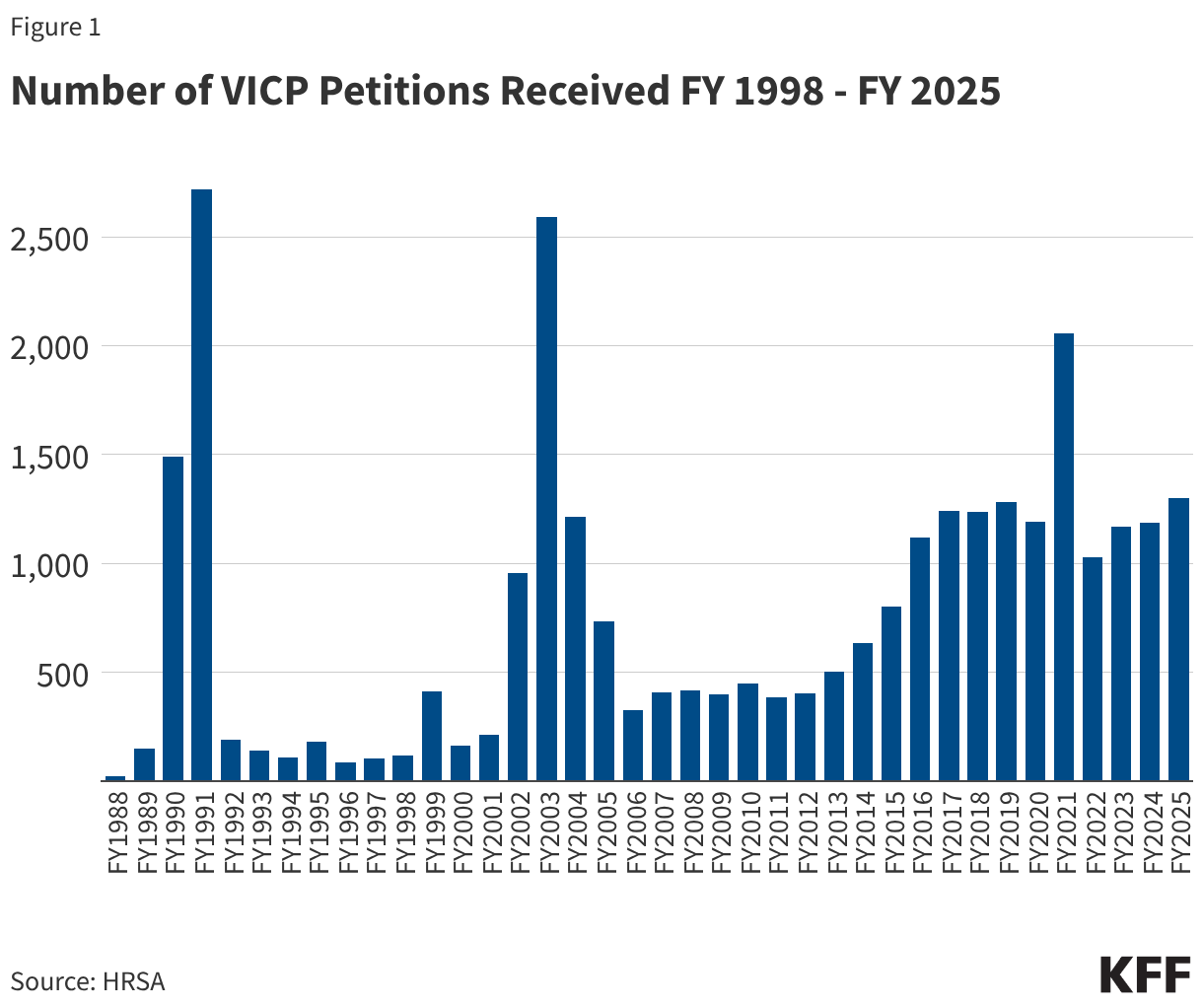

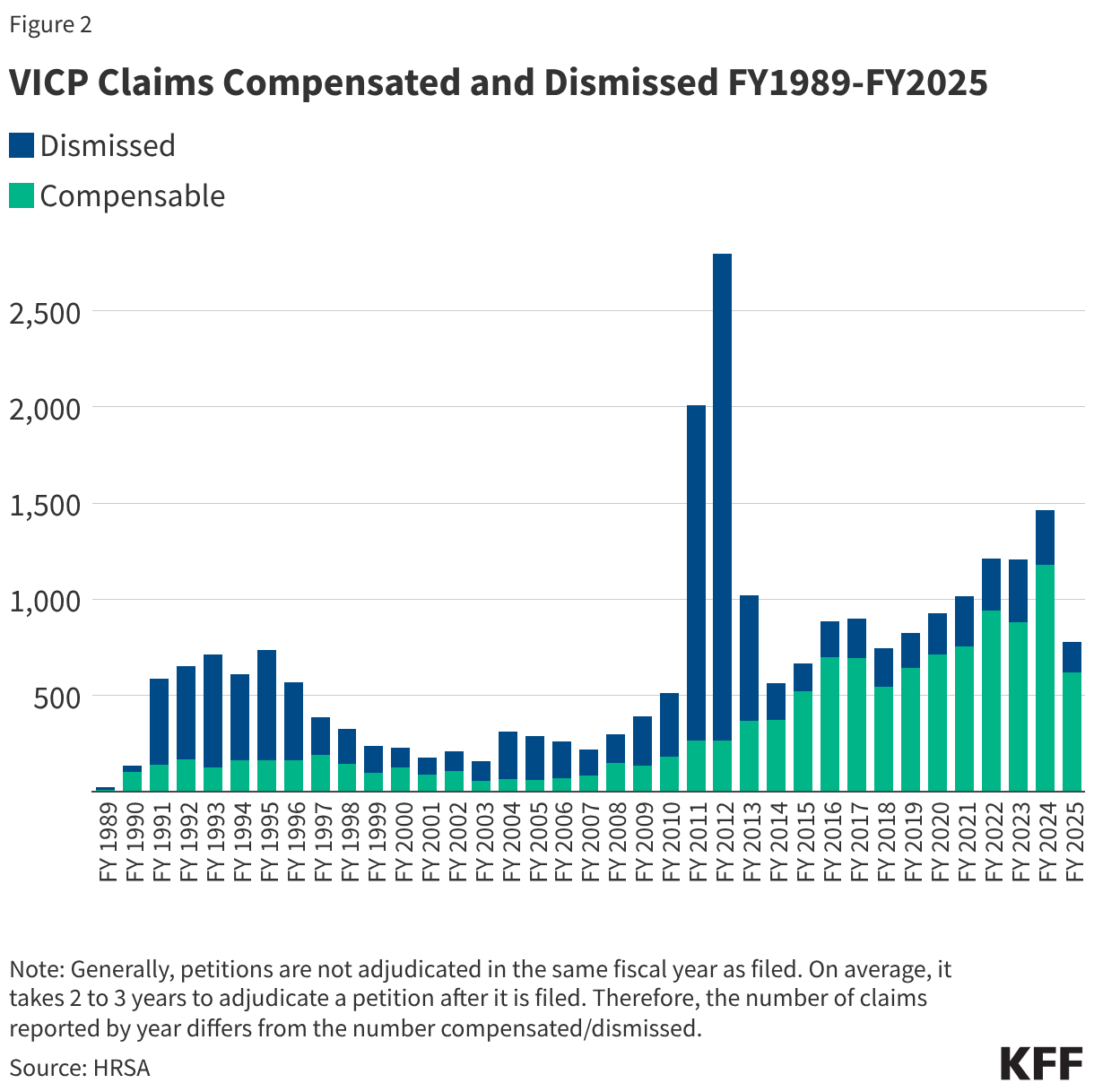

From FY 1988 through FY 2025, VICP received a total of 28,673 petitions. The annual number of petitions has varied over time, including notable surges in some years (see Figure 1). Surges occurred in FY 1990 and FY 1991 (1,492 and 2,718 VICP petitions were filed, respectively) due to a large increase in claims stemming from parental concerns about injuries caused by DPT vaccines. There was also a surge a decade later, primarily reflecting a wave of public concern about MMR vaccine after reports (later found to be false) that the vaccine could be linked to autism.1 Since FY 2014, there has been a general increase in the number of petitions filed, with the average number growing from 466/year during the FY 2005-FY 2014 period to 1,238/year during FY 2015-FY 2025. This increase may be linked to policy changes that expanded the scope of the vaccine injury table, such as the inclusion of “Shoulder Injury Related to Vaccine Injury (SIRVA),” which was formally added in 2017.

25,026 VICP petitions (87% of all 28,673 petitions received) have been adjudicated through FY2025, with 12,019 (48%) found to be compensable and 13,007 (52%) dismissed. As shown in Figure 2, the share of compensable injuries has generally increased in recent years compared to earlier periods of the program, with 77% of petitions found compensable between FY 2016-FY 2025 compared to 28% of petitions in the prior 10-year period (FY2006-FY2015). This again may be partially attributed to increasing scope of the vaccine injury table. The notable spike in claims dismissed in FY 2011-FY 2012 was a result of the resolution of the Omnibus Autism Proceedings allowing a backlog of claims related to autism as a vaccine injury to be processed and dismissed when the program found no credible evidence that vaccines were the cause of autism.2

The number of VICP claims and compensation adjudications represents a tiny fraction of the number of vaccines distributed in the U.S. According to HRSA and CDC data, from January 1, 2006 to December 31, 2024 there were 5.65 billion doses of VICP-covered vaccines distributed in the U.S.. During this same period, there were 14,409 VICP petitions filed, or 2.6 VICP petitions per million doses distributed. Of these, 10,633, or 1.89 petitions per million doses, were found to be compensable.

CICP

Between FY 2010 and FY 2026 (through March 1, 2026) CICP received a total of 14,733 claimsfor covered countermeasures. CICP reports it has reached a decision on 7,423 (50%) of those claims, finding 135 (1.8%) were eligible for compensation. The remainder are still being processed.

The majority of CICP petitions received were related to COVID-19 vaccines (10,981 or 75% of all petitions filed). CICP has reached a decision on 6,827 (62%) of these. Overall, 95 (0.9%) of COVID-19 vaccine claims been found eligible for compensation through CICP. With over 670 million doses COVID-19 vaccines administered in the U.S. between December 2020 and May 2023, that translates into approximately 16 petitions filed per million doses administered, and 0.14 compensation-eligible claims per million doses.

Relatively few non-COVID-19 vaccine countermeasure claims have been filed through CICP. For example, CICP reports 29 compensation payments were made related to the 2009 H1N1 vaccine (after approximately 90 million doses were administered in the U.S., translating to about 0.3 compensation payments per million doses administered). One CICP compensation payment was reported related to the smallpox vaccine, though CICP reports that 8 petitions related to the mpox vaccine and 2 additional claims related to the smallpox vaccine have been filed and are still being processed.

Publicly available information about CICP claims and compensation is limited compared to VICP. In contrast to VICP, CICP does not report petitions received or claims processed by year and does not publicly release details on the rationale for compensation decisions.

Funding and Expenditures

These two programs have different funding sources, with VICP funded through a trust fund holding revenues collected from the excise taxes and CICP funded through the annually-appropriated funds provided to HHS/HRSA. Compensation award amounts through VICP, while variable, have averaged between $500,000 and $1 million for most of the program with some recent declines.. In contrast, most awards (75%) through CICP are for amounts under $10,000, though there have been a few very large individual payments exceeding $1 million.

VICP

VICP is funded through revenues collected from an excise tax placed by Congress on every dose of each vaccine covered under VICP produced in the U.S.. The excise tax is paid into a Vaccine Injury Compensation Trust Fund overseen by the U.S. Treasury. The Trust Fund also generates revenue from investing its assets. Treasury uses Trust Fund resources to make payments and transfers to government agencies responsible for administering VICP including the Department of Justice, the U.S. Court of Appeals, and HHS/HRSA.

Over time, the VICP trust fund has grown as its annual revenues typically exceed expenses. The U.S. Treasury reports that as of September 30, 2025 the VICP trust fund held $4.66 billion. In FY 2025, $363 million was added to the trust fund (including $131 million from excise taxes, $169 million from interest on investments, and $63 million in refunds from current and prior year authority). VICP expenses totaled $314 million in FY 2025, which were primarily for compensation payments but also administrative and other costs.

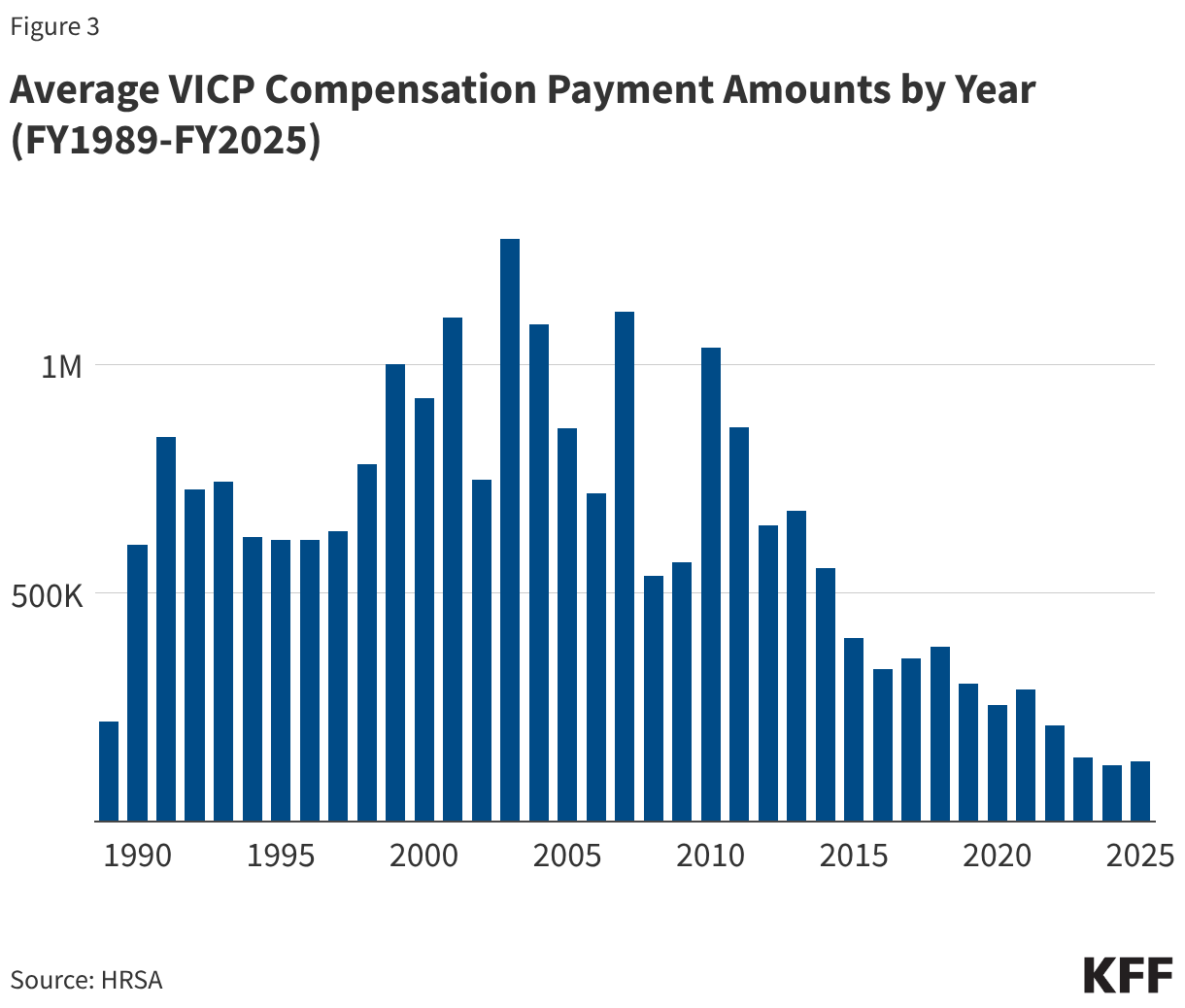

12,409 VICP compensation payments have been awarded between FY1989 and FY2025 totaling $4.89 billion (see Figure 3). Since the early 2010s, the average amount of compensation has generally declined, and has remained below $500,000 since FY 2015, likely a reflection of the expansion of the vaccine injury table to include milder injuries such as SIRVA (which entail comparatively lower payments relaive to other injuries).

CICP

There is no specific tax or dedicated funding source for CICP compensation payments, as there is for VICP. CICP funding comes from annual Congressional appropriations to HRSA rather than an excise tax. Through the PREP Act Congress created a “Covered Countermeasures Process Fund (CCPF)” to be administered by HRSA for CICP purposes, though little information is available on how much funding – if any – is currently held in the CCPF. At times Congress has provided emergency appropriations (such as the CARES Act during the COVID-19 response) that allowed, but did not require, HHS to direct funds to the CCPF.

Several large single payments comprise the majority of all compensation provided by CICP since 2010. There is only limited information about CICP expenditures, which includes the number and amounts of CICP compensation payments that have been made since FY2010. According to this data, CICP has paid compensation for 81 claims totaling more than $13 million. Most of the this total comes from a few very large single compensation payment amounts – for example there are reported payments of $5.9 million (related to thrombotic thrombocytopenia syndrome injury linked to COVID-19 vaccination), $2.3 million, and $1.8 million (the latter two related to Guillain-Barre Syndrome injury linked to 2009 H1N1 pandemic influenza vaccines). Of the 81 claims that received compensation, 11 (14%) were for amounts over $100,000, 10 (12%) were for amounts between $10,000 and $100,000, and 60 (74%) were for amounts under $10,000.

There are significant caseload, backlog, and capacity constraints in both programs. As noted above, there has been a growing number of petitions filed for each these programs over the last few years. However, the staffing and resources allocated to the programs have not matched this growth. For example, the VICP is limited by statute to eight special masters, with each now facing a larger caseload. The CICP has faced a surge of claims related to COVID-19 vaccines since 2021. The growing burden of claims and limited set of resources has contributed to long case review times and delays in issuing decisions and settlements.

The question of how best to address COVID-19 vaccine injuries has been an ongoing issue, particularly now that the COVID-19 public health emergency has ended. Under current law, COVID-19 vaccines are still covered under the CICP through the end of 2029. However, because CICP was created to address smaller scale deployments of medical countermeasures during a health emergency, rather than national-level responses to pandemics that extend over years, it has faced limitations in taking on COVID-19 vaccine injuries. Available compensation is generally lower compared to VICP, and the standard of proof for non-table injuries is higher. Even though the deployment of COVID-19 vaccines began as an emergency countermeasure during a national health emergency, these vaccines have become integrated into routine vaccinations and are recommended by CDC for broad segments of the U.S. population. For that reason, some health policy experts, lawyers, and politicians have advocated for including COVID-19 vaccines under VICP rather than CICP.

Politicization of vaccines and strains on scientific credibility threaten confidence in and stability of these programs. As views about vaccines have become more politicized, vaccine injury compensation programs have become a frequent target of partisan criticism. There is a striking partisan divide on the benefits and risks of COVID-19 vaccines, for example, with Republicans seeing those vaccines as causing more harm and arguing for more injury compensation as a result, compared to Democrats. This has also played out in actions taken by the Trump administration, such as seeking to narrow recommendations for several childhood vaccines and calling into question vaccine safety. On VICP, the Secretary of HHS Kennedy has argued that the program is too restrictive and the number and scope of vaccine injuries covered should be expanded to include conditions such as autism, though there is no credible evidence that vaccination causes autism, and the VICP itself reviewed available evidence on autism and vaccines during the Omnibus Autism Proceedings in the early 2000s and found no scientific evidence to support the link. Secretary Kennedy has also said that VICP has become a “morass of inefficiency, favoritism, and outright corruption.” Advocates linked to Secretary Kennedy have argued for expanding the VICP injury table to cover as many as 300 additional conditions they claim are injuries linked to vaccines. Others have raised concerns that adding injuries without sufficient scientific evidence to do so threatens the credibility of these programs and could even lead to insolvency if the scope of covered “injuries” expands to highly prevalent conditions like autism.

Updating legislation and regulations on compensation payment rules and related policies is politically challenging. A frequent criticism of these programs is that compensation payments were set when the programs were first created and have not been updated over time to reflect new developments and are not indexed to inflation. VICP, for example, has the same $250,000 cap on compensation for injuries or death that was in place when the program was established in 1988. However, making changes to these rules would require that Congress amend the underlying legislation, and doing so has proven politically challenging (changes were last made in 2016 through the “21st Century Cures Act”). There have been multiple legislative proposals introduced to update and modernize the vaccine injury compensation systems legislation but none has advanced. For example, the Vaccine Injury Compensation Modernization Act (H.R. 5142), which was last introduced in 2022-2023, proposed changes such as: increasing the number and tenure of special masters, requiring a formal plan to eliminate backlog, moving COVID-19 vaccines from CICP to VICP, increasing compensation caps and indexing payments to inflation, and increasing transparency and reporting requirements. Another proposal, recognizing that CICP has been inundated with claims for COVID-19 vaccines even though the program was designed with a smaller scale in mind, would replace that program with a “pandemic injury compensation system” that would be pre-funded, scalable, and automatically activated during a public health emergency. However, these bills have not advanced.

Endnotes

Due to the increased public concern about a potential vaccination-autism link and the large number of related claims filed, VICP established a special program in 2002 called the Omnibus Autism Proceeding, which evaluated several hypotheses for vaccine-autism links, ultimately finding that there was no causal relationship. No scientific evidence has shown autism to be linked to childhood vaccines, therefore autism is not included as an injury in the VICP vaccine injury table. ↩︎

Due to the increased public concern about a potential vaccination-autism link and the large number of related claims filed, VICP established a special program in 2002 called the Omnibus Autism Proceeding, which evaluated several hypotheses for vaccine-autism links, ultimately finding that there was no causal relationship. No scientific evidence has shown autism to be linked to childhood vaccines, therefore autism is not included as an injury in the VICP vaccine injury table. ↩︎

This analysis, originally published on June 17, 2025, was updated to note that changes to the final legislation that became law reduced the number of low-income Medicare beneficiaries who would be affected. CBO did not provide a detailed analysis of the impact, but based on available information the number is likely somewhat lower.

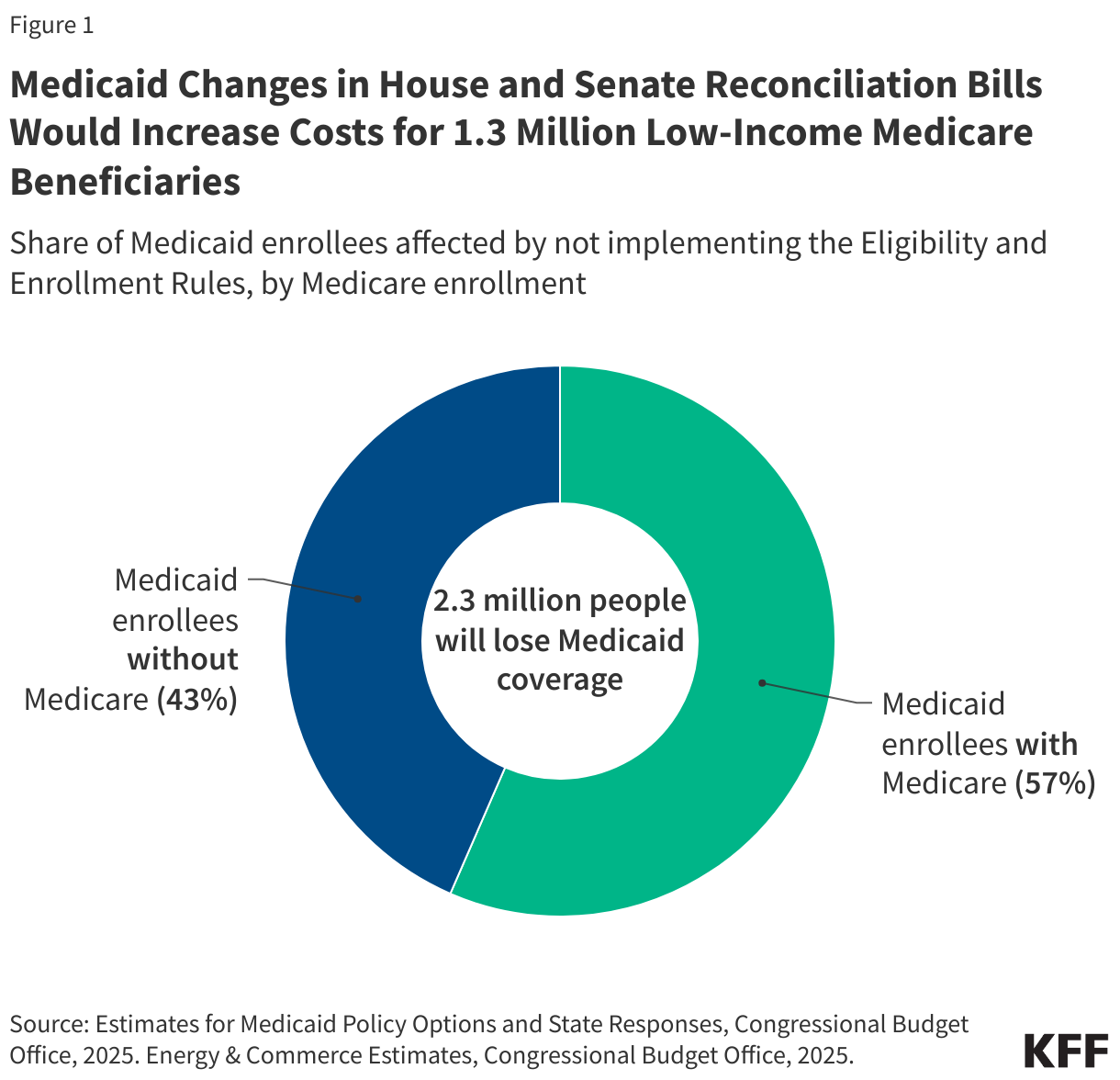

On May 22, the House passed a reconciliation bill, the One Big Beautiful Bill Act, which would partially pay to extend expiring tax cuts by cutting Medicaid. The Congressional Budget Office (CBO) estimates that the bill would reduce federal Medicaid spending by $793 billion over ten years and 10.3 million fewer people would be enrolled in Medicaid in 2034, including 1.3 million people with Medicare, otherwise known as “dual-eligible individuals”. The loss of Medicaid coverage for Medicare beneficiaries stems from delaying implementation of two rules that aimed to streamline the enrollment process and make it easier for people to maintain Medicaid coverage by reducing administrative barriers. Dual-eligible individuals would be disproportionately impacted by these provisions, comprising nearly 60% of the 2.3 million Medicaid enrollees who are estimated to lose coverage as a result of delaying these rules under the House reconciliation bill (Figure 1). Instead of placing a moratorium on implementation of the rules, the recently released Senate reconciliation language would prohibit nearly all of the provisions in the rules from ever being implemented.

Dual-eligible individuals have low incomes and modest savings. The 1.3 million people that would no longer have Medicaid if the eligibility and enrollment rules were not implemented would retain their primary health insurance coverage under Medicare, but lose Medicaid coverage of Medicare premiums, and in most cases, cost sharing, which are provided through Medicare Savings Programs (MSPs) administered by state Medicaid programs. Many would also lose coverage of Medicaid benefits that supplement their Medicare coverage, such as long-term care, dental services, and non-emergency medical transportation.

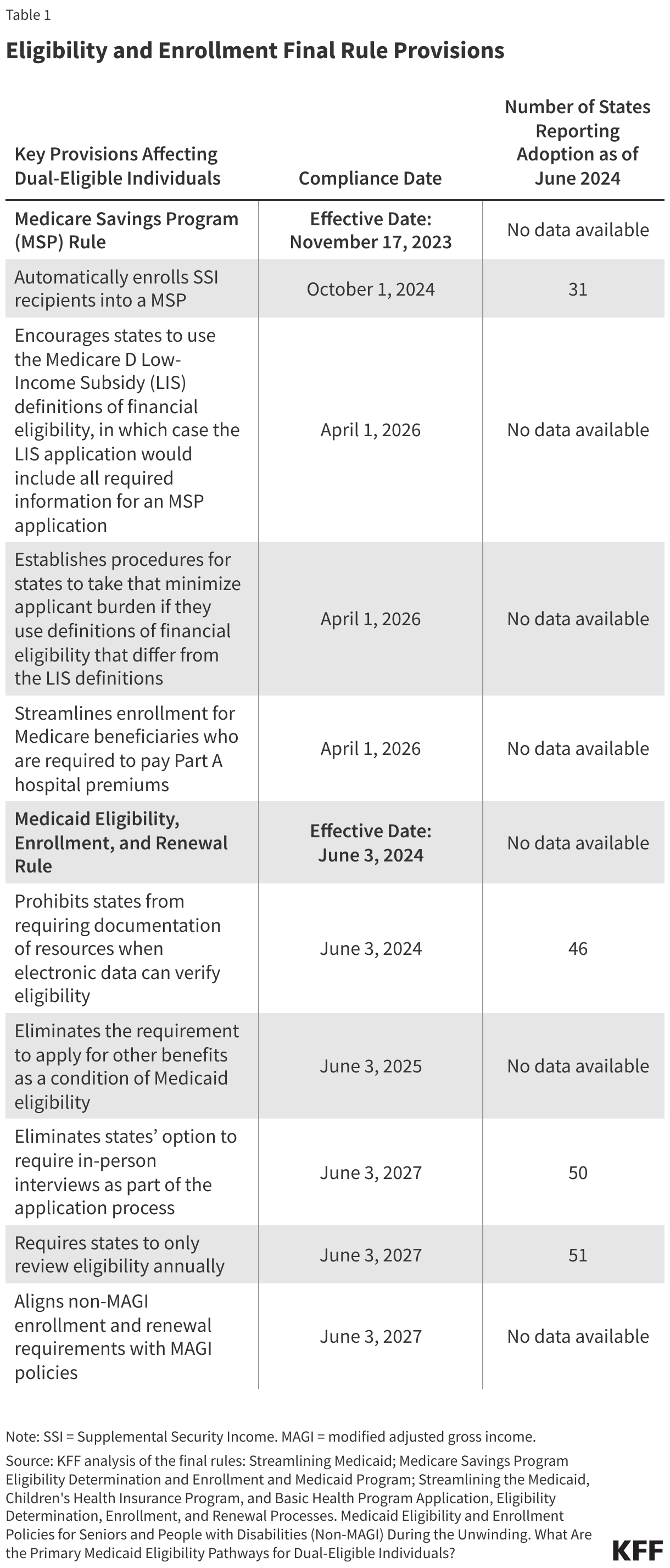

The loss of Medicaid coverage for Medicare beneficiaries stems from provisions in the House bill that would delay implementation of two Biden administration rules until 2035. The two rules that would be delayed under the House reconciliation bill were intended to make it easier for people to enroll in and maintain Medicaid coverage by minimizing administrative burden in the following ways.

One rule aimed to reduce barriers to enrollment in the Medicare Savings Programs (MSPs), under which Medicaid pays Medicare premiums, and in most cases, cost sharing for low-income Medicare beneficiaries. Among other changes, the rule would automatically enroll Medicare beneficiaries with Supplemental Security Income (SSI) into the MSPs and would more closely align the MSP application to the application for Medicare’s Part D prescription drug Low-Income Subsidy (LIS).

The second rule would more broadly streamline application, enrollment, and renewal processes in Medicaid. Among the changes most relevant for dual-eligible individuals are new requirements for states to assist applicants with procuring appropriate documentation to validate income and assets, a requirement to renew Medicaid coverage only once per year, and a prohibition on requiring in-person interviews as part of the application process

CBO estimates that delaying these two rules would reduce federal spending by $167 billion over 10 years, making this the second largest source of cuts to federal Medicaid spending in the bill. Illustrating why administrative burdens may make it hard for dual-eligible individuals to maintain Medicaid, prior KFF research finds that among people who newly become eligible for both Medicare and Medicaid, 28% lose Medicaid coverage within the first year despite living on fixed incomes.

Although states have already implemented some of the rules’ provisions (Table 1), if the rules are delayed, it is expected that further implementation will cease and states may resume some practices that were prohibited under the rules. For example, 38 states report sending pre-populated renewal forms to Medicaid enrollees who qualify because they are ages 65 and older or have a disability, a practice they may discontinue if the rules are delayed. Alternatively, it’s possible that some states will reinstate requirements for applicants to submit paper documentation or report for in-person interviews. In a few cases, states will be required to reinstate application requirements or be prohibited from using more streamlined application processes.

Losing Medicaid coverage would substantially increase out-of-pocket costs for low-income Medicare beneficiaries. Because Medicare beneficiaries who qualify for Medicaid typically have very low incomes and little to no savings, the loss of Medicaid payment for the costs of Medicare’s premiums and cost sharing could make their Medicare coverage unaffordable. For example, the first rule would automatically enroll low-income Medicare beneficiaries who receive Supplemental Security Income (SSI) into a MSP. Without the MSP, such people must pay 20% of the $967 SSI monthly benefits for the $185 Medicare Part B monthly premium in 2025. (In order to qualify for SSI, individuals must have low incomes, limited assets, and either be over age 64 or have a qualifying disability.) This same individual would have additional out-of-pocket costs if they went to the doctor or were admitted to the hospital. Those additional out-of-pocket costs could discourage low-income beneficiaries from using health care and is the reason for CBO’s estimate that delaying implementation of the rules would reduce Medicare spending by $11 billion over 10 years.

Additionally, some of the 1.3 million Medicare beneficiaries expected to lose Medicaid under the House reconciliation bill may also lose subsidies that help pay for prescription drug premiums and cost sharing. Medicare beneficiaries with Medicaid are automatically enrolled in the Medicare Part D Low-Income Subsidy (LIS), which provides assistance with Part D prescription drug premiums and cost sharing. Illustrating the connection between Medicaid enrollment and LIS coverage, between December 2024 and January 2025, the number of LIS recipients decreased by 1 million, following Medicaid disenrollments that stemmed from the unwinding of the Medicaid continuous enrollment provision. Before the decline, LIS enrollment had been slowly but steadily growing over time.

This work was supported in part by Arnold Ventures. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

Medicaid is the primary program providing comprehensive coverage of health care to about 80 million low-income people in the U.S. Medicaid is an insurance program, not a population health system. It can only fund services for eligible individuals. The public health system in the U.S. is decentralized, with most authorities and programs delegated to the state and local levels. State and local public health agencies are responsible for protecting community health through surveillance, disease prevention, and policy development and enforcement. Local health departments frequently focus on service delivery (immunizations, screenings, maternal health, environmental health) and community outreach to address local health needs. Public health serves entire communities, not just insured individuals.

Medicaid agencies and state/local public health agencies work to advance the health of their communities, often with similar priorities serving common populations. However, there is often a lack of strong and sustained partnerships between Medicaid and public health agencies. Strengthening collaboration between Medicaid and public health could improve safety net services, help coordinate and leverage resources and financing, improve intervention targeting and outreach, and reduce system fragmentation.

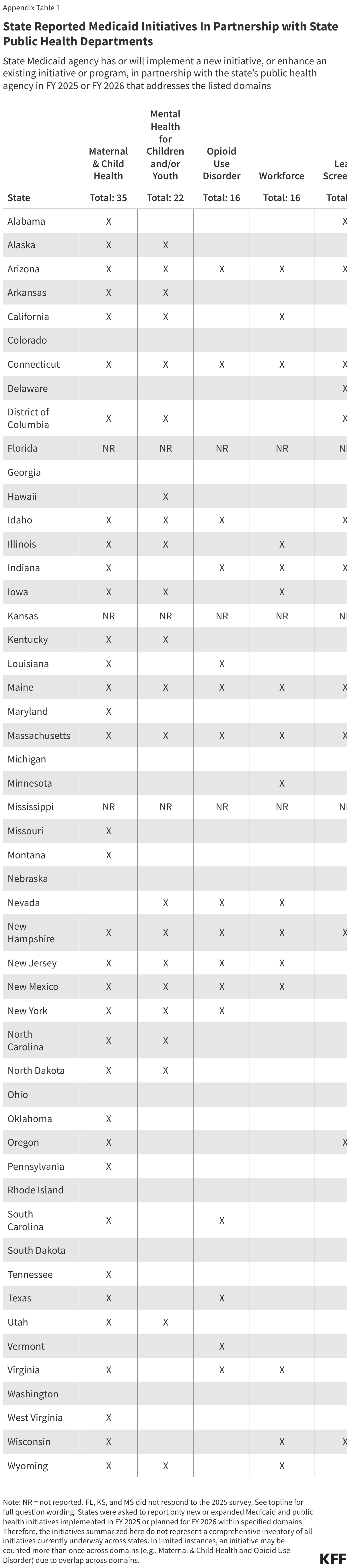

To improve understanding of Medicaid and Public Health agency partnerships, the 25th annual Medicaid budget survey, conducted by KFF and Health Management Associates (HMA) in collaboration with the National Association of Medicaid Directors (NAMD), asked state Medicaid directors about new or enhanced initiatives involving public health implemented in FY 2025 or planned for FY 2026 across the following domains. (The survey did not capture the full scope of established Medicaid and Public Health agency partnerships across states, including initiatives implemented or expanded before FY 2025 – FY 2026, nor all activity within these domains as states select which efforts to report.)

More than three quarters of responding states1 reported at least one new or expanded initiative implemented in FY 2025 or planned for FY 2026 (see Appendix), with maternal and child health and behavioral health emerging as areas of focus for newly implemented or expanded Medicaid and Public Health initiatives. Initiatives frequently fell into common areas, including data sharing, rural-focused initiatives, initiatives to improve access, and workforce initiatives.

Findings

States were asked to report only new or expanded Medicaid and Public Health initiatives implemented in FY 2025 or planned for FY 2026 under specific domains. Therefore, initiatives summarized and reported here do not represent a comprehensive look at all initiatives currently in place across states. State counts are not identified in the sections below, as open-ended questions often lead to underreporting. See Appendix for additional (high-level) state-by-state detail.

To track common themes across domains, state responses have been summarized (at a high-level) under the following subheadings, as applicable: “data sharing,” “rural,” “workforce,” “access,” and “other.” State examples are included in text boxes under each domain. While the survey asked about workforce initiatives separately, “workforce” also emerged as a theme applicable to other domains. These initiatives are only summarized once (e.g., do not appear under the separate “workforce” domain if they also fell under another domain).

Maternal & Child Health

Conception through early childhood represents an important period for intervention to promote long-term health and other outcomes. More than one in four Medicaid/CHIP enrollees is a female in their reproductive years. Medicaid is the primary payer for about 41% of all births and provides coverage for 37% of all children in the U.S. Public health agencies often oversee maternal and child health surveillance, prevention, and early childhood initiatives to improve outcomes and reduce gaps in health outcomes and access.

States reported new or expanded maternal and child health initiatives in the following areas:

Data sharing. States reported cross-agency data sharing initiatives to strengthen maternal and child health surveillance.

Rural. States reported collaborative efforts to address rural maternal health needs, as individuals in rural areas face access challenges (lack of local obstetric services) and geographic barriers.

Workforce. Statesmentioned collaborating with public health agencies to certify and support community health workers (CHW), including doulas and other perinatal providers.

Access.

Transforming Maternal Health Model. States reported collaborating with public health agencies on implementing CMS’s Transforming Maternal Health Model (TMaH), identifying collaboration as important to developing strategies to direct resources / interventions to high-need communities. CMS’s TMaH model supports state Medicaid agencies in implementing evidence-based strategies to expand access to maternal care, integrate behavioral health and social determinants of health, and ensure care continuity in the postpartum period.2

Coverage expansions. States pointed to expansion of Medicaid coverage of maternal and child health services, such as doula and lactation services. Some described partnering with public health agencies to inform coverage expansions through shared data and collaborative program design.

MH/SUD expansions. States highlighted initiatives to integrate and/or expand mental health (MH) and/or substance use disorder (SUD) services for pregnant and parenting populations, including home visiting services for pregnant and postpartum individuals.

Other.

Interagency workgroups. States described leveraging interagency workgroups and committees to facilitate coordination and to advance maternal and child health priorities, including improving outcomes and addressing complex factors (e.g., social needs) that a single agency can’t solve alone.

Box 1: State Examples of Maternal and Infant Health Initiatives

Data Sharing:

The OklahomaMedicaid Birth Certificate Linkage Project is supported by an interagency agreement between the Oklahoma Health Care Authority (the state agency that administers the Medicaid program) and the Oklahoma State Department of Health. The project links vital records (birth certificate) data to Medicaid data to provide a more complete picture of pregnancy and birth outcomes of Medicaid enrollees.

Rural:

As part of a two-year HRSA-funded Maternity Care Deserts Policy Academy run by the National Academy for State Health Policy (NASHP), Kentucky Medicaid is working with the state’s Department of Public Health to identify maternity care deserts in the state and to develop solutions to connect pregnant individuals to care. (Maternity care deserts are places with no hospitals or birth centers offering obstetric care and no obstetric providers.) The Kentucky Perinatal Quality Collaborative and other state organizations are also involved.

Workforce:

Massachusetts reported providing training and technical assistance to MassHealth (Medicaid) providers to support maternal health initiatives, including efforts to strengthen care coordination and outreach and to support implementation of state maternal health legislation (enacted in 2024) that aims to expand access to midwifery, birth centers, doulas, and postpartum home visiting services.

Access:

California’s Department of Health Care Services was awarded $17 million in federal funding to implement CMS’s Transforming Maternal Health Model in five counties in the Central Valley. The model will provide funding to transform three key areas: access to care, infrastructure, and workforce; quality improvement and safety; and whole person care delivery (i.e., customized care to meet an individual’s unique needs). The Department of Health Care Services will work with managed care plans, providers, community-based organizations, and other partners to implement the model and to ensure alignment with the state’s Birthing Care Pathway initiative, a broader statewide effort to improve maternity care and outcomes.

To improve maternal health outcomes, Illinoisadded doula and lactation support services (without requiring physician referral) to its Medicaid coverage. The Department of Public Health supported the coverage expansion, highlighting differences in maternal health outcomes by race and ethnicity in the state.

Louisiana reported the state Department of Health launched Project M.O.M. (Maternal Overdose Mortality) in May 2025. Project M.O.M. aims to reduce pregnancy-associated opioid overdose deaths through early identification and treatment of substance use disorder during pregnancy. The project will convene hospital and community partners and aims to align managed care plans and health care providers to improve access to care and treatment coordination.

Montana Medicaid is partnering with state public health to implement targeted case management and evidence-based home visiting for pregnant and postpartum individuals and parents of children ages 0-5 who meet high-risk criteria, including mental health/SUD criteria.

Other:

Arizona reported that its Medicaid agency will continue to strengthen its relationship with the state Department of Health Services through ongoing participation in health-focused workgroups and committees, including the Maternal Mortality Review Committee, Congenital Syphilis Collaborative, Perinatal and Infant Health Committee, Home Visiting Workgroup, among other groups and committees.

Children/Youth Mental Health

Early childhood and adolescence are important developmental periods that can influence long-term health. In recent years, there have been growing concerns about children’s mental health and well-being. Medicaid provides health coverage for 37% of children in the U.S. and plays a significant role in funding school-based behavioral health services. Nearly one in five students attending public schools in the U.S. use school-based mental health services, underscoring how schools serve as an important access point for youth mental health treatment. Public health agencies may be involved in assessing the status of statewide and community early childhood mental health, developing policy and programming for youth and caregivers, encouraging participation in mental health programs, and partnering to maintain school-based behavioral health services.

States reported new or expanded children/youth mental health initiatives in the following areas:

Workforce. States reported working with public health agencies to connect PCPs to psychiatrist consultations, including initiatives specifically targeting rural areas.

Access. Statesreported collaborating with public health agencies on maintaining and increasing access to school-based services, which offer a convenient setting for delivering health services to students (overcoming transportation and other barriers), including mental health services.

Box 2: State Examples of Children/Youth Health Initiatives

Workforce:

Kentucky’s Medicaid agency reported working with the Kentucky Department of Public Health on “KY MARK,” an initiative that helps PCPs better manage children’s mental health issues by partnering with University systems to connect primary care providers to child psychiatrists. The program aims to help PCPs develop the skills to treat/manage mental and behavioral health needs.

Access:

Massachusetts’ Medicaid agency reported working with the state Department of Health on implementing school-based services and on conducting outreach. The Department of Health operates school-based health centers that provide comprehensive primary care and behavioral health services. The state’s Medicaid program covers these services for Medicaid eligible youth.

New Hampshire reported cross-agency work to strengthen the system of care for children with behavioral health needs, aiming to create a comprehensive, coordinated network of behavioral health services and supports for children and families.

Opioid Use Disorder (OUD)

Opioids were involved in over 79,000 deaths in 2023. The opioid epidemic’s impact remains widespread, with nearly three in ten adults (29%) reporting in a 2023 KFF poll that they or a family member experienced an opioid addiction. Medicaid is the primary source of coverage for adults with opioid use disorder (OUD), covering nearly half of all adults with OUD, over two-thirds of those receiving outpatient OUD treatment, and more than half of those receiving medication-based treatment. Public health departments have worked to reduce opioid overdoses through harm reduction strategies (e.g., naloxone distribution, fentanyl test strip distribution, syringe services) and data surveillance. The Centers for Disease Control (CDC) funds state and local health departments for drug overdose surveillance through its Overdose Data to Action (OD2A) program.

States reported new or expanded OUD initiatives in the following areas:

Data sharing. States reported engaging public health partners in strategic planning and data sharing initiatives (e.g., matching Medicaid records with OUD data) to understand state and local OUD impacts and prevent future OUD deaths.

Access. States reported initiatives focused on addressing opioid use disorder among pregnant and parenting populations. These initiatives have been captured and discussed under the “Maternal & Child Health” domain above.

Box 3: State Examples of Opioid Use Disorder Initiatives

Data Sharing:

Arizona reported data sharing with the public health agency’s drug overdose fatality review committee that works across state agencies to determine how system changes may help prevent overdose deaths.

DC reported matching and sharing Medicaid records with OUD death data to engage public health partners in strategic planning.

Lead Screening

Exposure to lead can seriously harm a child’s health, including damage to the brain and nervous system, which may lead to slow growth and development, learning and behavior problems, and hearing and speech problems. The federal government has estimated that more than half of children with elevated blood lead levels are eligible for Medicaid. Federal law requires that all children enrolled in Medicaid receive blood lead screening tests at age 12 months and 24 months. In addition, children between 36 and 72 months with no record of a previous blood lead screening test must receive one. While Medicaid cannot be used to abate or for remediation of environmental damage, states are required to provide medically necessary diagnostic and treatment services for children identified with elevated blood lead levels. Medicaid programs can leverage public health expertise in outreach, education, surveillance, and data analysis, strengthening identification of populations at risk of lead exposure and expanding the reach and effectiveness of Medicaid services.

States reported new or expanded lead screening initiatives in the following areas:

Data sharing. States described maintaining data-sharing agreements with public health agencies to monitor lead screening rates, close care gaps, and better coordinate interventions.

Other. States reported working with public health agencies to develop lead screening guidance for providers and/or managed care plans.

Box 4: State Examples of Lead Screening Initiatives

Data Sharing:

Maine‘s Medicaid and public health agencies share blood lead level testing data and coordinate technical assistance and communications to PCPs to increase blood lead testing rates. The Medicaid agency incorporated blood lead testing into an alternative payment model for primary care services (called Primary Care Plus) that emphasizes primary care quality and incentivizes providers to improve testing, screenings, and immunizations, including blood lead testing for children enrolled in Medicaid.

Other:

Arizona reported that its Medicaid agency works closely with the state Department of Health’s elevated blood lead level program to increase screening rates, identify children with elevated blood lead levels, and provide information to managed care plans for follow-up testing and treatment.

DC reported its Healthy Homes Program and Childhood Lead Poisoning Prevention Program moved from its Department of Energy & Environment to the DC Department of Health, streamlining efforts in risk mitigation from lead poisoning, asthma, and pest infestation, providing comprehensive home assessments and case management in one place, ensuring a closer link between environmental housing factors and direct public health intervention.

Wisconsin reported that public health staff are routinely included in Medicaid agency meetings with managed care plans to help identify potential quality improvement activities, including activities related to lead screening and environmental intervention.

Infectious Disease

Infectious diseases threaten public health, causing morbidity, mortality, and economic disruption. Recent outbreaks of vaccine-preventable and emerging diseases highlight the need for coordinated prevention, surveillance, and response efforts. States are required to provide comprehensive preventive care to children through the EPSDT benefit. States are required by (federal) law to cover certain preventive services for adults eligible under the ACA’s Medicaid expansion. Medicaid plays a key role in disease prevention by facilitating access to vaccines for children, adolescents, and adults. CMS and the Centers for Disease Control and Prevention (CDC) jointly run the Vaccines for Children program, which provides vaccines to Medicaid and CHIP-enrolled youth. State and local public health agencies lead disease surveillance, outbreak response, and vaccine administration. They provide guidance, education, and outreach to high-risk populations, coordinating with Medicaid to ensure prevention efforts reach eligible individuals

States reported new or expanded infectious disease initiatives in the following areas:

Data sharing. States reported collaborating with state public health agencies on disease-specific efforts (e.g., sharing and analyzing HIV data to guide outbreak response and enhance access to care) as well as broader data sharing initiatives with public health agencies to improve coordination and population health monitoring.

Workforce. States reported collaborative initiatives, including training and service coordination, to strengthen the local response capacity of public health teams and clinical providers.

Access. States highlighted cross-agency efforts aimed at maintaining vaccine access and aligning coverage policy with public health recommendations.

Box 5: State Examples of Infectious Disease Initiatives

Data Sharing:

DC’s Medicaid agency shared data with DC Health to support continuity of care for individuals with HIV following implementation of Medicaid eligibility policy changes effective January 1, 2026 that resulted in coverage changes for certain adults.

The North Carolina Division of Public Health’s Immunization Registry is collaborating with the state’s Health Information Exchange (HealthConnex) to draw patient immunization data into the registry. This integration allows providers to access a consolidated record of immunizations administered across the state, regardless of where the vaccines were given.

Workforce:

Maine’s Medicaid agency reported working closely with the Public Health agency on HIV outbreak response to coordinate services and training for local response teams and providers.

Workforce

Health care provider shortages can reduce access to care and lead to poor health outcomes. Provider shortages are a particular challenge in low-income and rural communities. Community health workers (CHWs), doulas, and other community-linked providers, often play a role in bridging gaps in care, connecting individuals to services, and addressing health related social needs. Medicaid provides coverage for eligible enrollees by reimbursing providers directly for services or paying managed care plans to deliver services. Public health agencies provide significant safety net clinical care, operating at the state and local level and often bridging gaps in care for underserved populations, including the uninsured.

States reported new or expanded workforce initiatives in the following areas:

Rural. States reported collaboration on workforce initiatives spurred by the introduction of the Rural Health Transformation Program, introduced by the 2025 reconciliation law. This program (also referred to as the “Rural Health Fund”) provides $50 billion in funding for state grants that can be used to support rural areas in a variety of ways, including to pay for health care services, expand the rural health workforce, promote care interventions, and provide technical assistance with system transformation. However, over time reductions in funding to Medicaid (due to reconciliation law) are likely to exceed funding from the Rural Health Fund.

Other.