Juliette Cubanski

Juliette Cubanski  Meredith Freed

Meredith Freed  Nancy Ochieng

Nancy Ochieng  Alex Cottrill

Alex Cottrill  Jeannie Fuglesten Biniek

Jeannie Fuglesten Biniek  Tricia Neuman

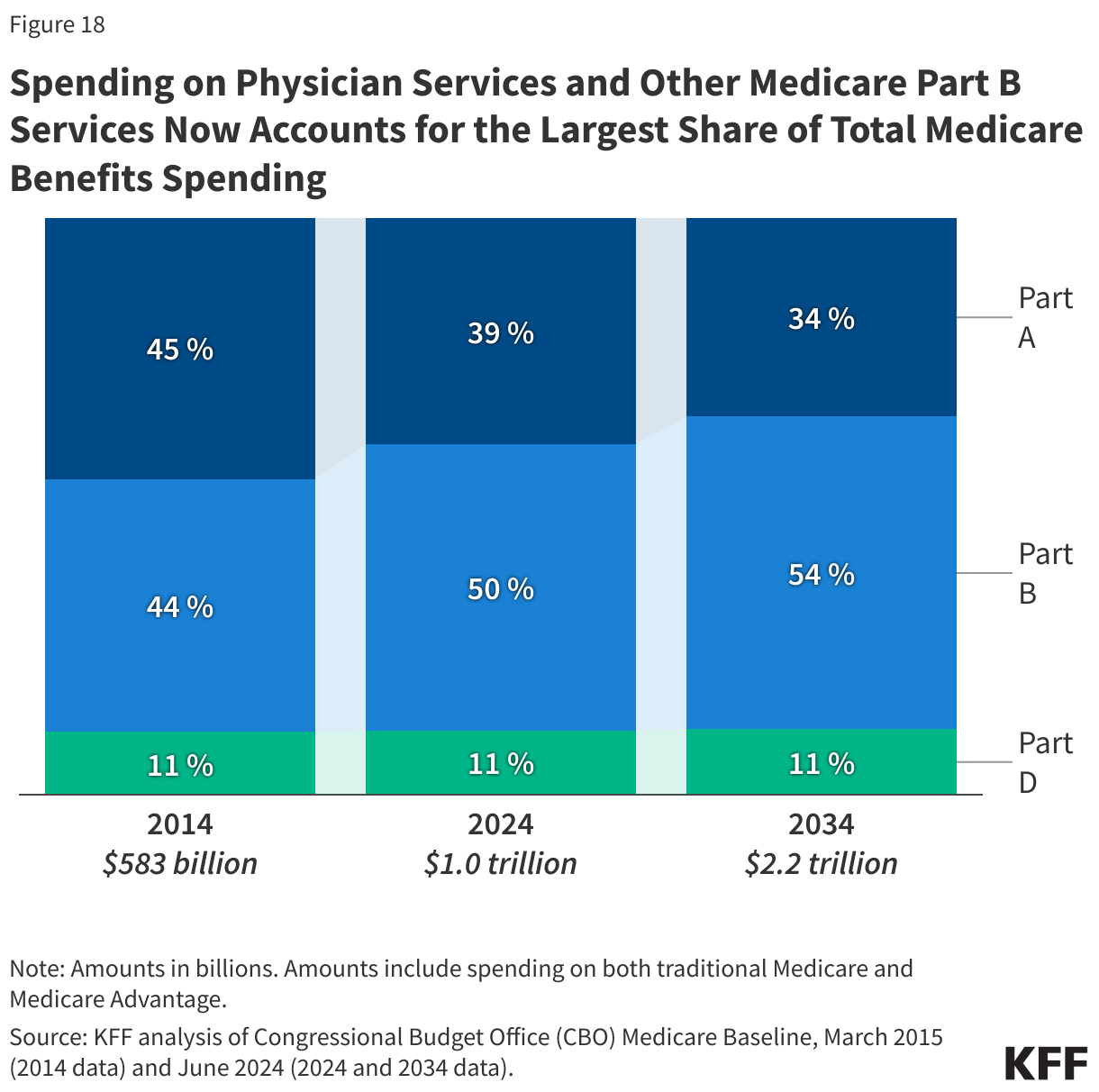

Tricia Neuman Medicare is the federal health insurance program established in 1965 under Title XVIII of the Social Security Act for people age 65 or older, regardless of income or medical history, and later expanded to cover people under age 65 with long-term disabilities. Today, Medicare provides health insurance coverage to 68 million people, including 61 million people age 65 or older and 7 million people under age 65. Medicare covers a comprehensive set of health care services, including hospitalizations, physician visits, and prescription drugs, along with post-acute care, skilled nursing facility care, home health care, hospice, and preventive services. People with Medicare can choose to get coverage under traditional Medicare or Medicare Advantage private plans.

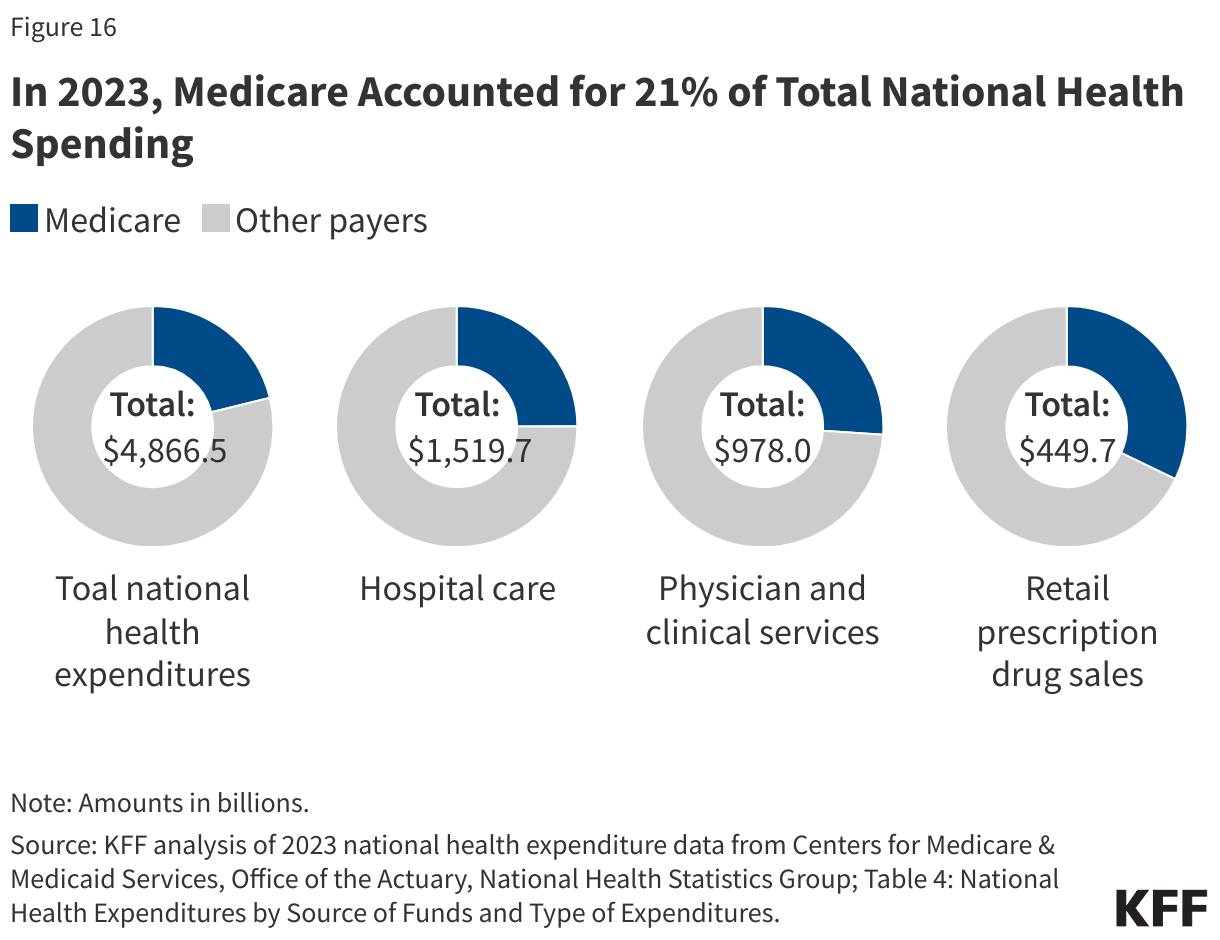

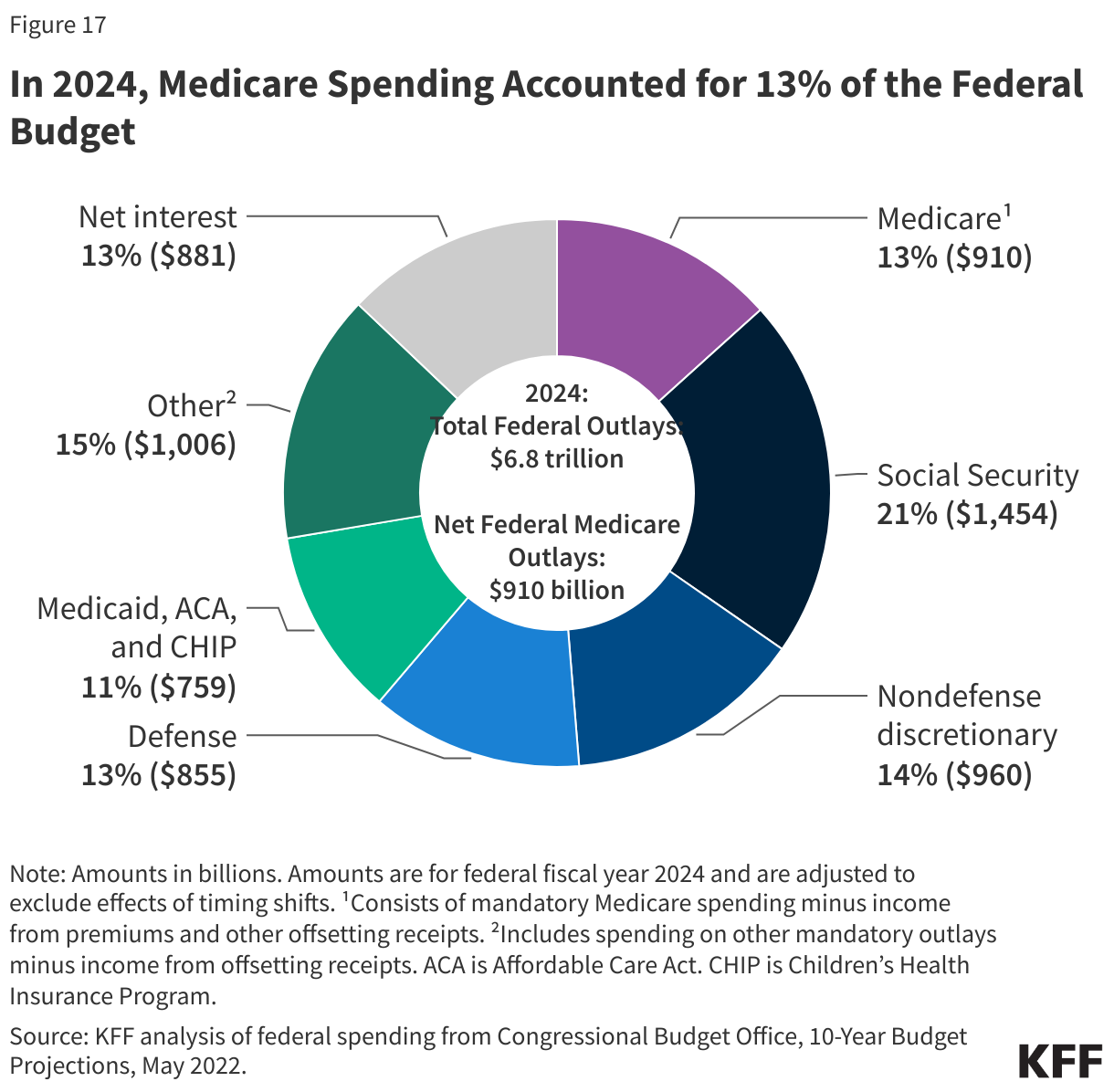

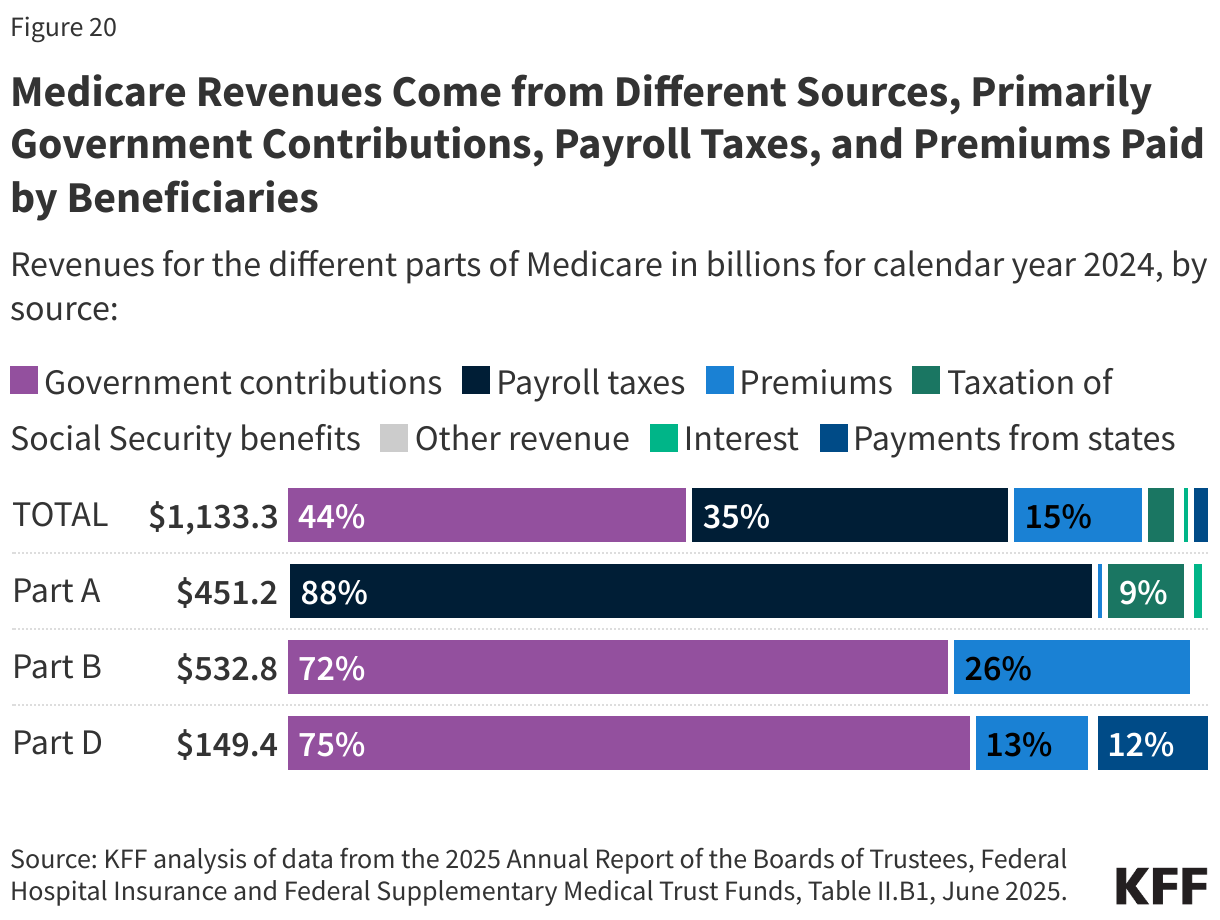

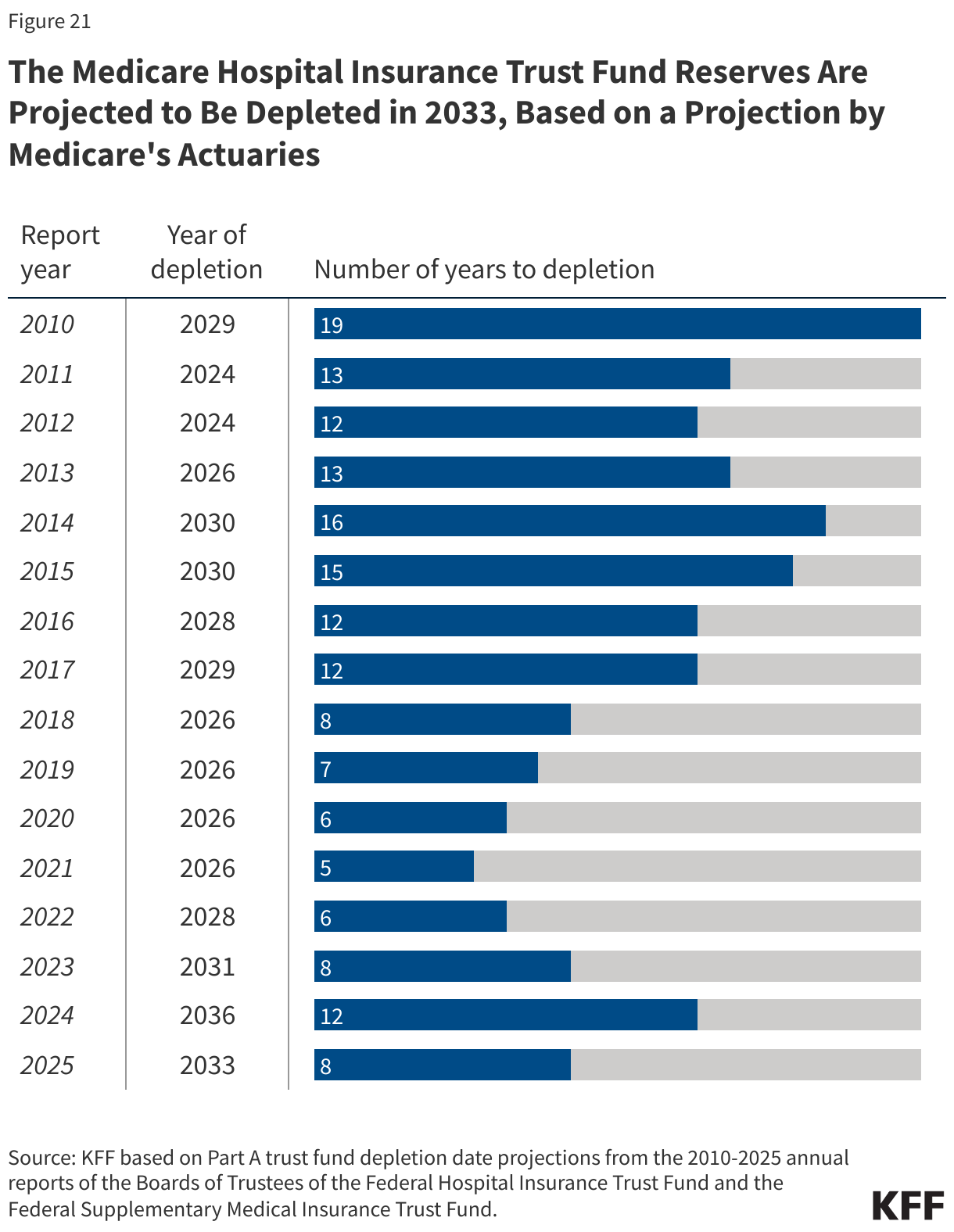

Medicare spending comprised 13.5% of the federal budget in 2024 and 21.2% of national health care spending in 2023. Funding for Medicare comes primarily from government contributions, payroll tax revenues, and premiums paid by beneficiaries. Over the longer term, the Medicare program faces financial pressures associated with higher health care costs, growing enrollment, and an aging population.