Medicare Advantage in 2026: Premiums, Out-of-Pocket Limits, Supplemental Benefits, and Prior Authorization

People with Medicare have the option of receiving their Medicare benefits through the traditional Medicare program administered by the federal government or through a private Medicare Advantage plan, such as an HMO or PPO. In Medicare Advantage, the federal government contracts with private insurers to provide Medicare benefits to enrollees. Medicare pays insurers a set amount per enrollee per month, which varies depending on the county in which the plan is located, the health status of the plan’s enrollees, the plan’s quality star rating, and the plan’s estimated costs of covering Medicare Part A and Part B services.

The plans use the payments from the federal government to pay for Medicare-covered services, and in most cases, to also pay for supplemental benefits and reduced cost sharing, which are attractive to enrollees. Plans are able to offer these additional benefits, often without charging an additional premium for Part D prescription drugs or supplemental benefits, because in 2026, they receive an additional $2,664 per enrollee above their estimated costs of providing Medicare-covered services, according to the Medicare Payment Advisory Commission (MedPAC). This portion of plan payments, also called the rebate, has increased substantially in the last several years, more than doubling since 2018.

Plans are also able to lower costs, which help finance these supplemental benefits, through cost management tools, such as prior authorization requirements and provider networks. Prior authorization requirements are used to assess whether health care services are medically necessary before they are covered to reduce unnecessary costs, though they may also impose barriers to receiving care. Medicare Advantage plans often have a limited network of providers, which can restrict beneficiary choice of physicians and hospitals. More than half of Medicare Advantage beneficiaries are enrolled in HMO plans that typically do not cover out-of-network services.

This brief provides information about Medicare Advantage plans in 2026, including premiums, out-of-pocket limits, supplemental benefits, and prior authorization, as well as trends over time. A companion analysis examines trends in Medicare Advantage enrollment.

Highlights for 2026:

- In 2026, three quarters (75%) of enrollees in individual Medicare Advantage plans with prescription drug coverage pay no premium other than the Medicare Part B premium, which is a selling point for enrollees, particularly those living on modest incomes. The average supplemental premium, including Medicare Advantage enrollees who pay no supplemental premium, is $15 a month. Individual Medicare Advantage plans are available to all beneficiaries with Medicare Part A and Part B, unlike special needs plans (SNPs) or group plans offered to retirees by an employer or union.

- More than 6 in 10 enrollees in individual Medicare Advantage plans with prescription drug coverage are in HMOs (61%), 38% are in local PPOs, and less than 1% are in regional PPOs in 2026. HMOs generally only cover services provided in-network, but tend to have lower supplemental premiums, which were $12 a month, on average, in 2026. PPOs cover services received out-of-network, typically for higher cost sharing, and tend to charge higher supplemental premiums, which were $18 a month, on average, in 2026.

- The average out-of-pocket limit for Medicare Advantage enrollees is $5,421 for in-network services and $9,825 for in-network and out-of-network services combined in 2026. The average out-of-pocket limit for in-network services is higher for PPOs ($6,592) than HMOs ($4,636). Traditional Medicare does not have an out-of-pocket limit, but Medicare Advantage plans are required to cap patient costs.

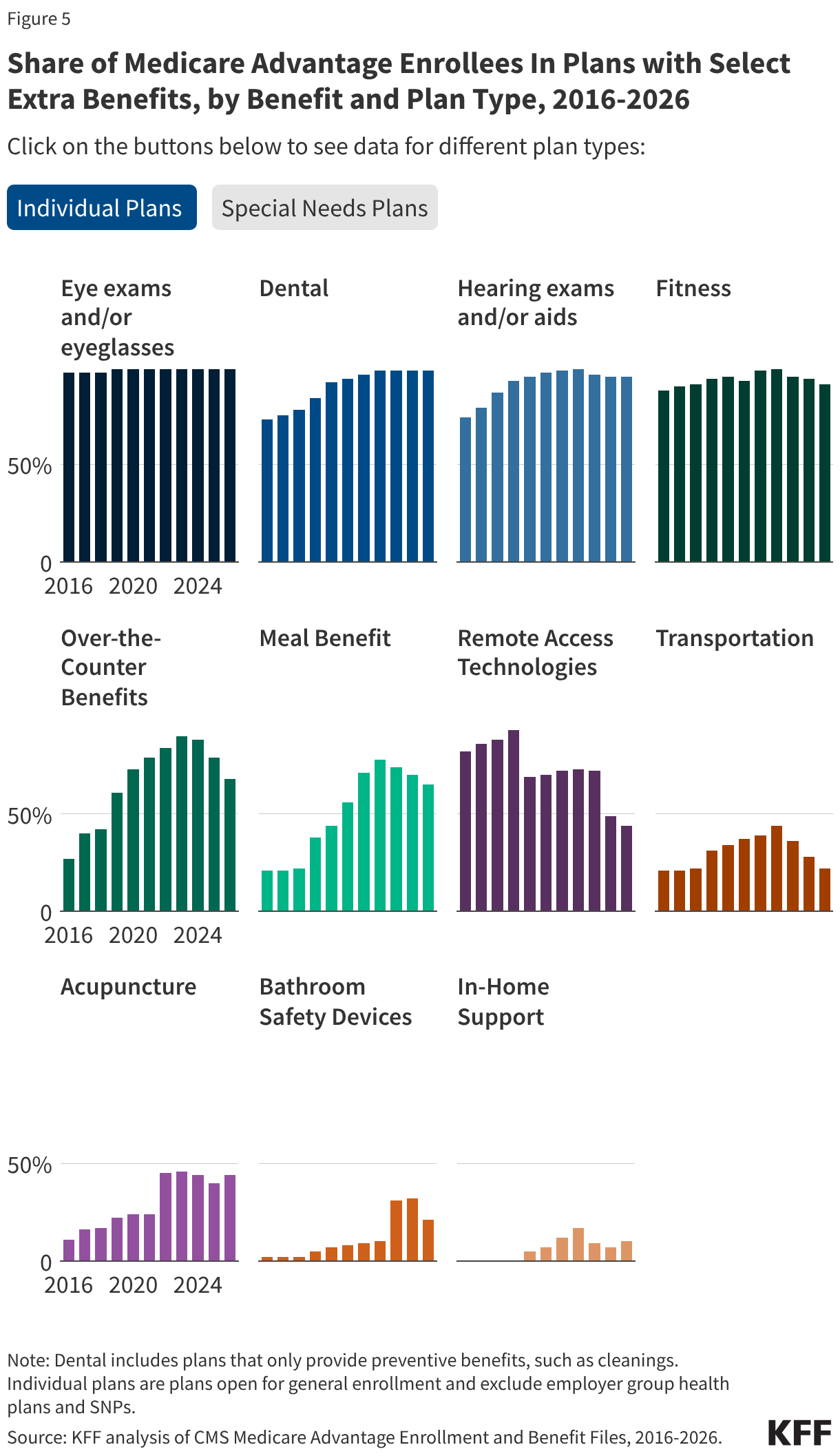

- Most Medicare Advantage enrollees are in plans that offer supplemental benefits not covered by traditional Medicare, such as vision, hearing and dental. From 2025 to 2026, access to dental, vision, and hearing benefits for Medicare Advantage enrollees remained stable. However, there were decreases in the share of individual plan enrollees in plans providing over-the-counter benefits, meal benefits, remote access technologies, transportation benefits, and bathroom safety devices. The share of SNP enrollees in plans that offered in-home support services increased, while the share of SNP enrollees in plans that offered transportation benefits, bathroom safety devices, and remote access technologies decreased.

- About one third of enrollees (31%) are in plans that also reduce the Part B premium ($202.90 per month in 2026), most often by less than $10 a month. Among enrollees in individual Medicare Advantage plans, nearly a third (32%) received a reduction in their Part B premium in 2026, the same as in 2025. Among enrollees in individual plans that offer reduced Part B premiums as a supplemental benefit, 39% are in plans that reduce premiums by less than $10 a month, while about 32% are in plans that reduce Part B premiums by $100 or more per month.

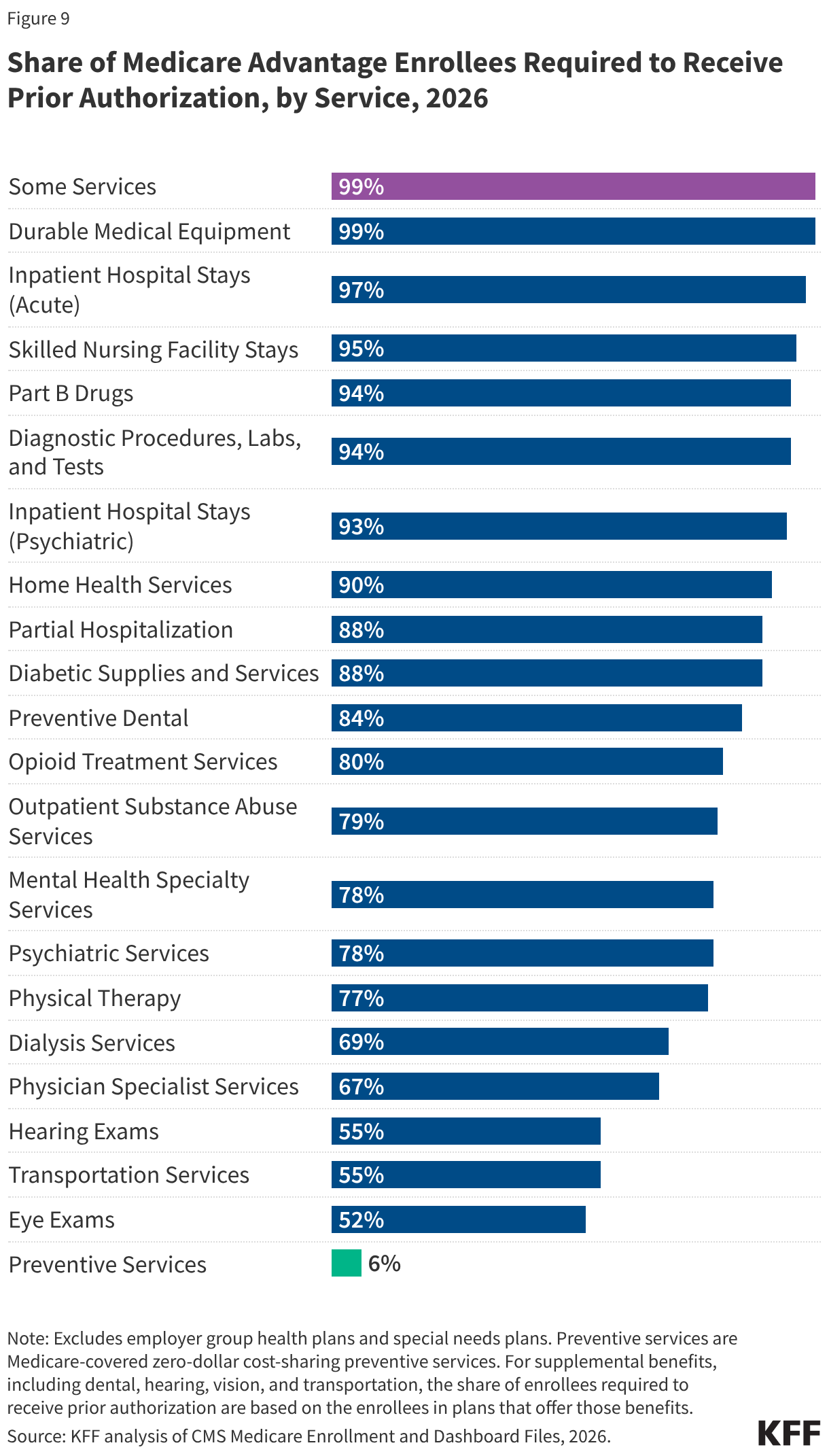

- Nearly all Medicare Advantage enrollees (99%) are in plans that require prior authorization for some services, which is rarely used in traditional Medicare. Prior authorization is most often required for relatively expensive services, such as inpatient hospital stays (acute: 97%; psychiatric: 93%), skilled nursing facility stays (95%), Part B drugs (94%), and home health services (90%) and is rarely required for preventive services (6%).

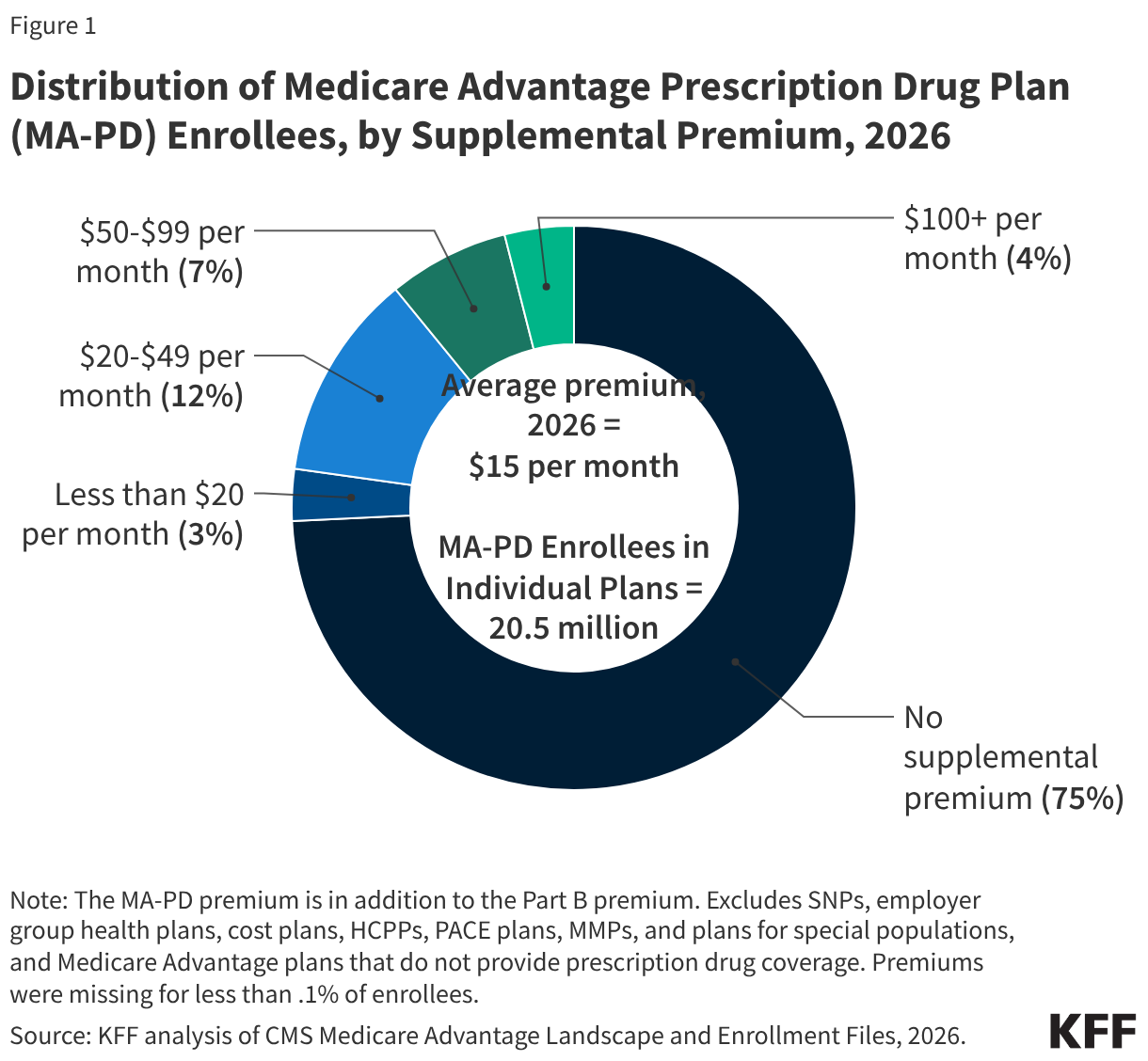

In 2026, three quarters of Medicare Advantage enrollees (75%) are in plans with no premium other than the Part B premium.

In 2026, most people (75%) enrolled in individual Medicare Advantage plans with prescription drug coverage (MA-PDs) pay no premium other than the Medicare Part B premium ($202.90 in 2026) (Figure 1). The MA-PD supplemental premium includes both the cost of Medicare-covered Part A and Part B benefits and Part D prescription drug coverage. In 2026, 96% of Medicare Advantage enrollees in individual plans open for general enrollment are in plans that offer prescription drug coverage.

Altogether, including those who do not pay a supplemental premium, the average enrollment-weighted supplemental premium in 2026 is $15 per month, and averages $8 per month for just the Part D portion of covered benefits, substantially lower than the average premium of $36 for stand-alone prescription drug plans (PDP) in 2026. Higher average PDP premiums compared to the MA-PD drug portion of premiums is due in part to the ability of MA-PD sponsors to use rebate dollars from Medicare payments to lower their Part D premiums. When a plan’s estimated costs for Medicare-covered services are below the maximum amount the federal government will pay private plans in an area (known as the benchmark), the plan retains a portion of the difference, known as the “rebate” (See How Medicare Pays Medicare Advantage Plans: Issues and Policy Options for additional information on how Medicare sets payment rates). According to MedPAC, rebates average nearly $2,400 per enrollee in 2026 for individual plans, with individual plans allocating $600 or 26% of these rebates for Part D benefits, including reducing Part D premiums.

For the 25% of beneficiaries in plans that charge a MA-PD premium (5.0 million), the average premium is $59 per month, and averages $40 for the Part D portion of covered benefits.

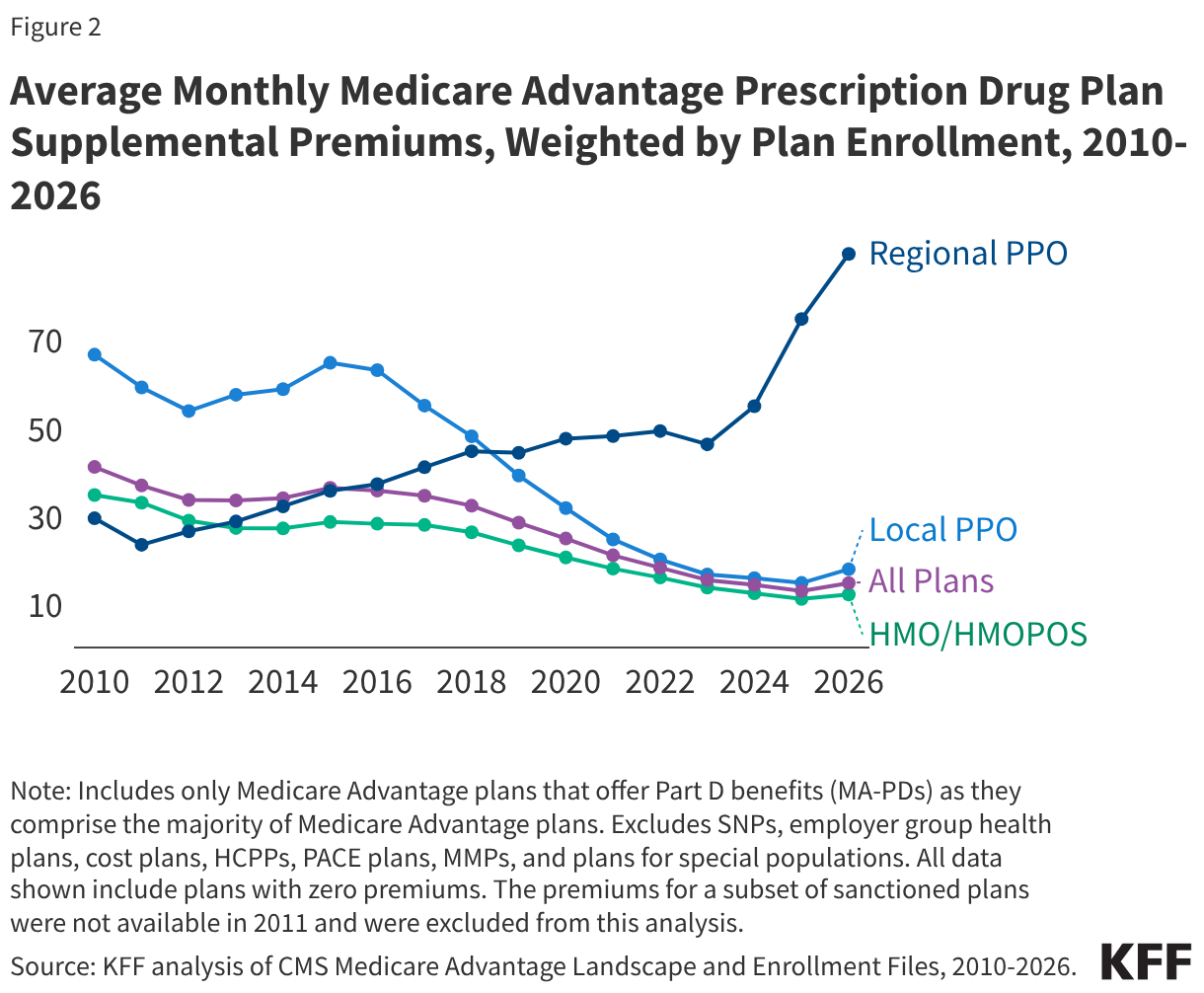

Supplemental premiums paid by Medicare Advantage enrollees steadily declined between 2015 and 2025 but increased slightly in 2026.

Average supplemental MA-PD premiums declined from $36 per month in 2015 to $13 per month in 2025, but increased to $15 per month in 2026 (Figure 2). Average supplemental MA-PD premiums have declined markedly for local PPOs, falling from $65 per month in 2015 to $15 per month in 2025, but increased to $18 per month in 2026. Supplemental premiums for HMOs have also declined steadily from $28 per month in 2015 to $11 per month in 2025, increasing slightly to $12 per month in 2026. Only regional PPOs, which represent a very small and declining share of enrollment, have seen an increase in plan premiums over this time from $36 per month in 2015 to $75 in 2025, increasing again to $89 per month in 2026.

More than 6 in 10 individual Medicare Advantage enrollees in plans with prescription drug coverage are in HMOs (61%), 38% are in local PPOs, and less than 1% are in regional PPOs in 2026. The reduction in supplemental premiums for nearly all plans is driven in part by the decline in supplemental premiums for local PPOs and HMOs, that account for a rising share of enrollment over this time period, as well as the increase in rebates paid by Medicare to these plans.

Since 2015, a rising share of plans estimate that their cost of providing Medicare Part A and Part B services (the “bid”) is below the benchmark, and as plan bids have declined, the rebate portion of plan payments has increased. Additionally, because rebates are adjusted for the health status of enrollees, rebates have increased as risk scores have increased. (A risk score is a measure that reflects an enrollee’s expected health care costs based on their health status and demographic characteristics, with higher risk scores translating to higher payments to plans.) As mentioned above, plans are allocating some of these rebate dollars to lower the Part D portion of the MA-PD premium. According to MedPAC, rebates for individual plans have increased from an average of about $924 per enrollee in 2015 to nearly $2,400 per enrollee in 2026. This trend contributes to greater availability of zero-premium plans, which brings down average premiums.

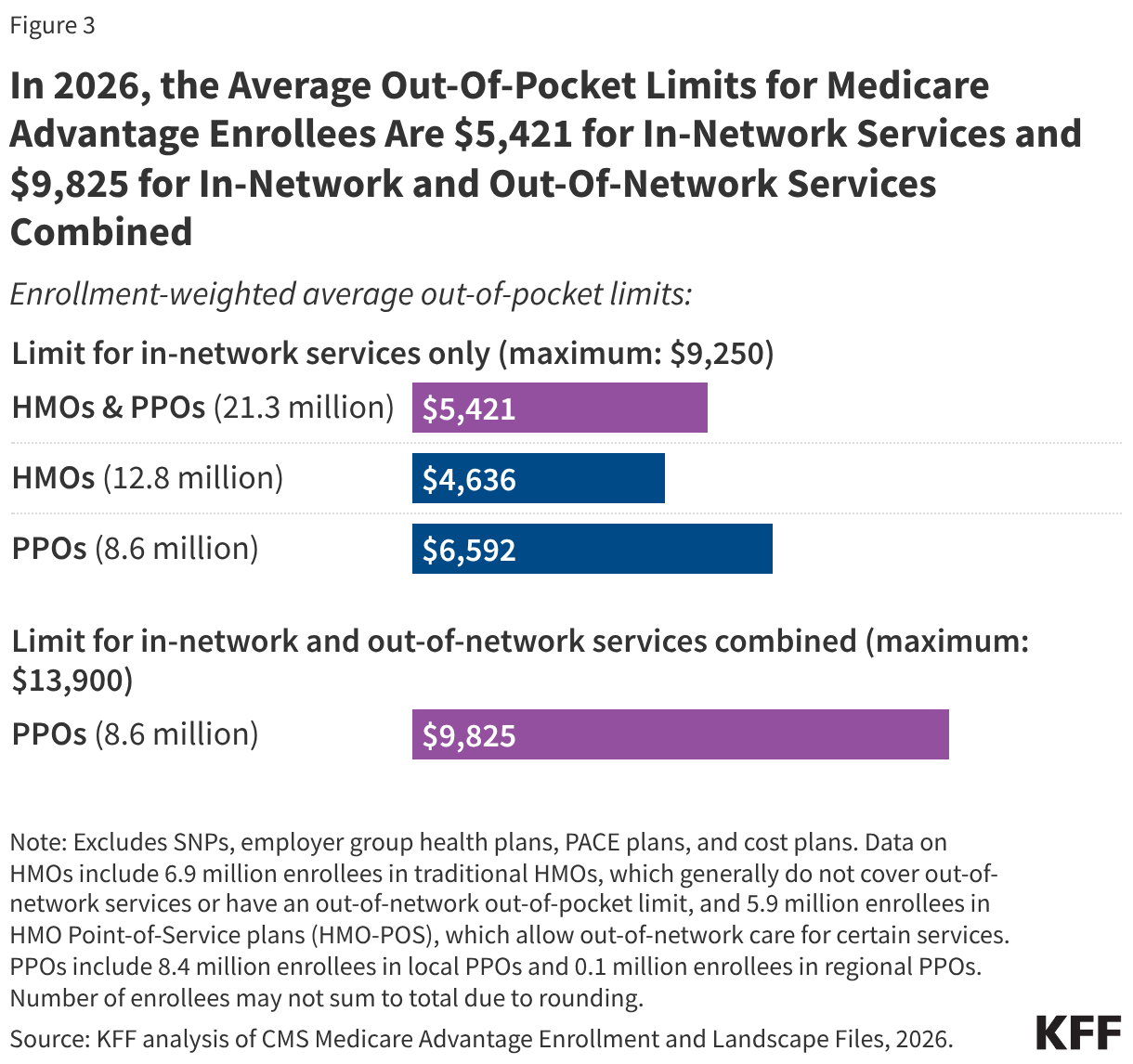

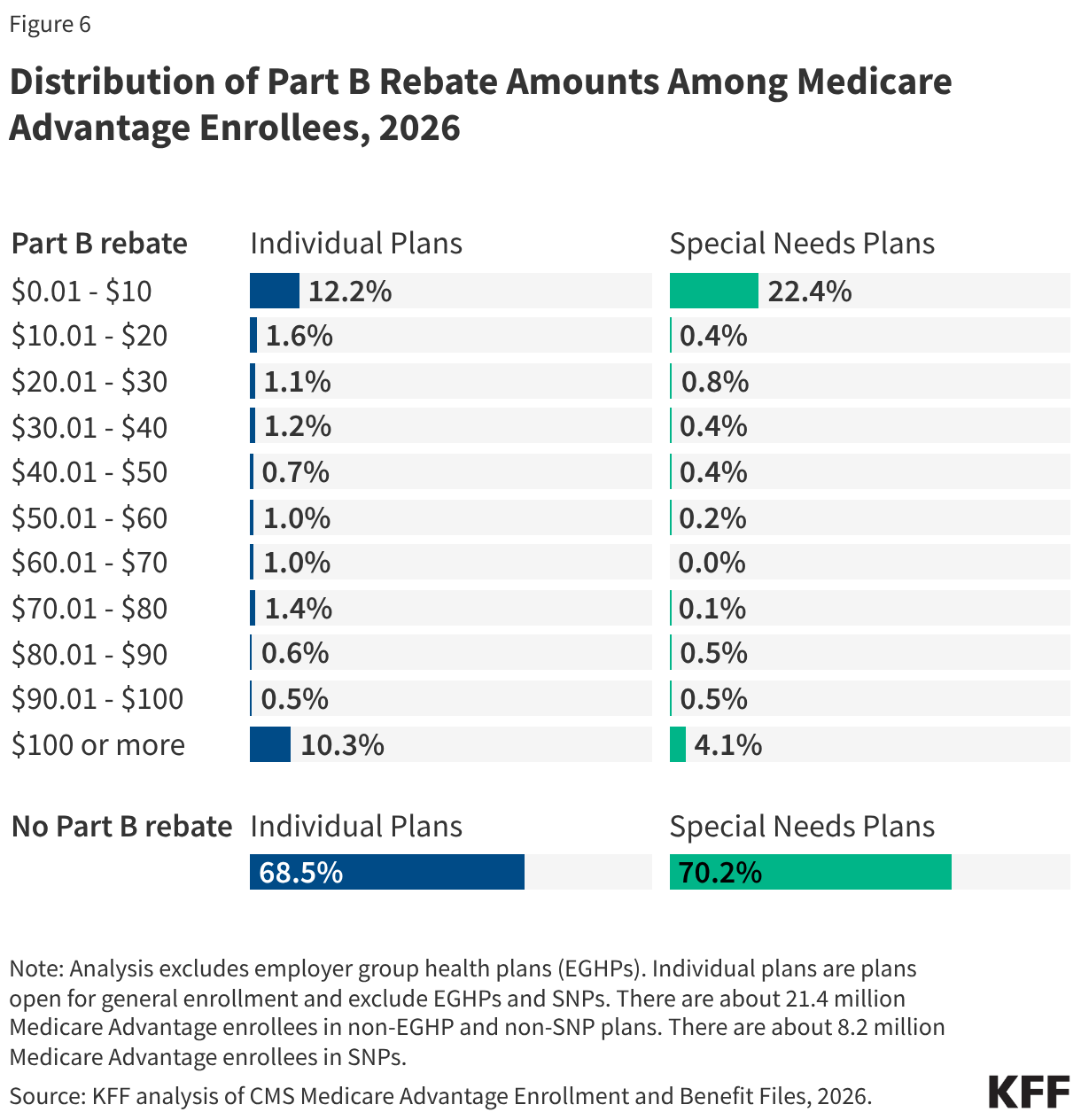

The average out-of-pocket limit for Medicare Advantage enrollees is $5,421 for in-network services and $9,825 for both in-network and out-of-network services (PPOs) in 2026.

Since 2011, federal regulation has required Medicare Advantage plans to provide an out-of-pocket limit for services covered under Parts A and B. In contrast, traditional Medicare does not have an out-of-pocket limit for covered services.

In 2026, the out-of-pocket limit for Medicare Advantage plans may not exceed $9,250 for in-network services and $13,900 for in-network and out-of-network services combined, though plans can offer lower limits than the maximum. These out-of-pocket limits apply to Part A and B services only, and do not apply to Part D spending, which has a separate out-of-pocket limit of $2,100 in 2026. The size of Medicare Advantage provider networks for physicians vary greatly across counties and across plans in the same county, with beneficiaries having access to about half of the physicians available to traditional Medicare beneficiaries in their area, on average.

In 2026, the average out-of-pocket limit for Medicare Advantage enrollees is $5,421 for in-network services, including those enrolled in both HMOs and PPOs. The average out-of-pocket limit both in-network and out-of-network services combined, which applies to just PPOs, is $9,825 (Figure 3).

HMOs generally only cover services provided by in-network, and the average out-of-pocket (in-network) limit is $4,636. Enrollees in HMOs are generally responsible for 100% of costs incurred for out-of-network care, so typically do not have a limit for out-of-network services. These numbers also include about 6 million Medicare Advantage enrollees that are in HMO Point-of-Service plans (HMO-POS), which generally operate the same as HMOs, but give enrollees the option of receiving specified services outside of the HMO plan's provider network, though these services typically cost more than services received in-network and may require prior approval. PPOs cover services delivered by out-of-network providers but charge enrollees higher cost sharing for this care. The average out-of-pocket limit for in-network services for PPOs is $6,592.

Average out-of-pocket limits for in-network services generally declined between 2017 and 2023 but have increased since then, with average limit for in-network services decreasing by nearly $600 from 2017 ($5,253) to 2023 ($4,685), before increasing by about $700 from 2023 to 2026 ($5,421).

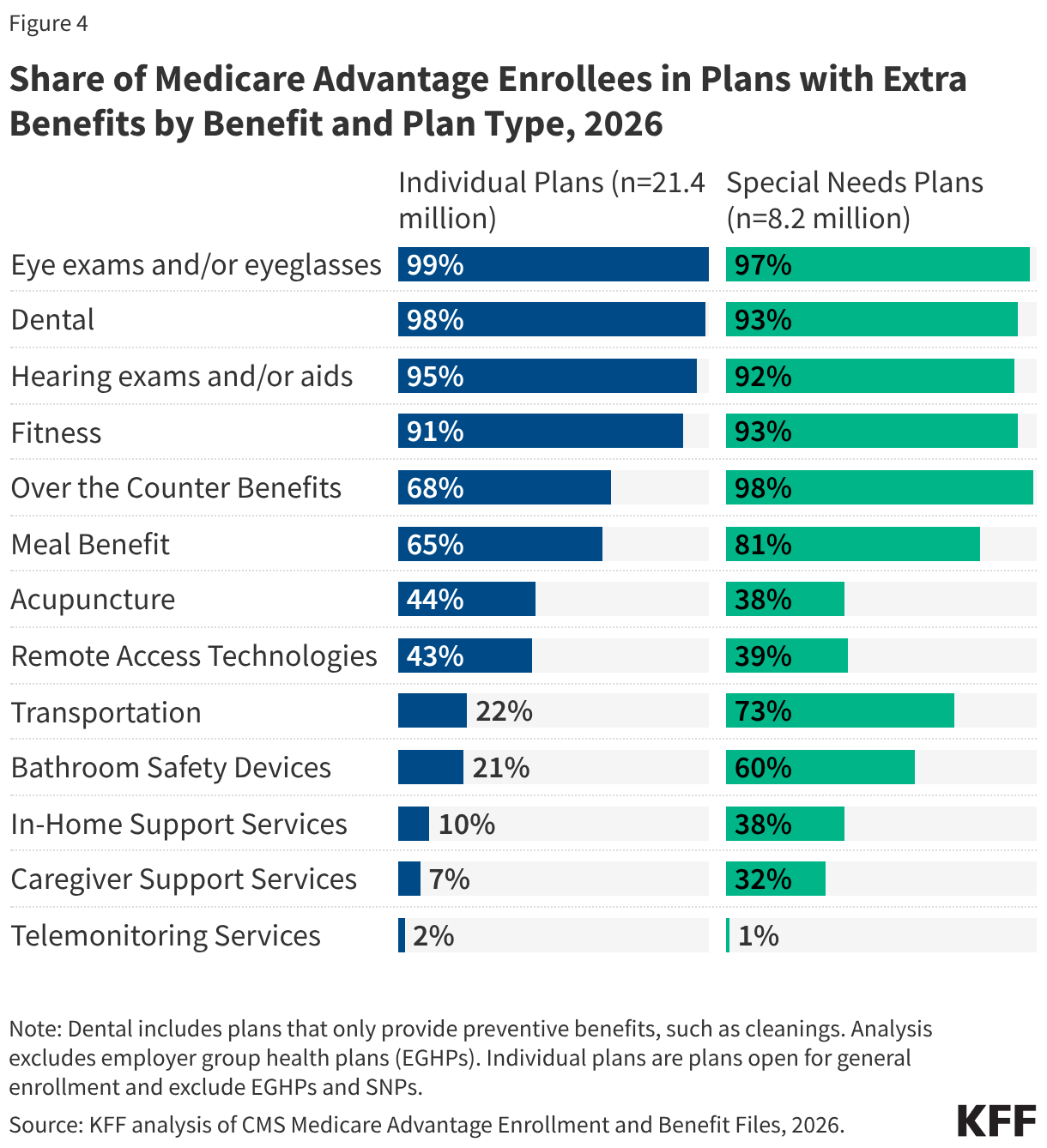

Most Medicare Advantage enrollees, including enrollees in special needs plans (SNPs), are in plans that offer some benefits not covered by traditional Medicare in 2026.

Virtually all enrollees in individual Medicare Advantage plans (those generally available to Medicare beneficiaries) are in plans that offer primarily health related supplemental benefits including eye exams and/or glasses (more than 99%), dental care (98%) hearing exams and/or aids (95%), and a fitness benefit (91%) (Figure 4). Similarly, most enrollees in SNPs are in plans that offer these benefits. However, benefits such as in-home support services are less common for enrollees in both individual plans (10%) and SNPs (38%). This analysis excludes employer-group health plans because employer plans do not submit bids, and available data on supplemental benefits may not be reflective of what employer plans actually offer.

Though these benefits are widely available, the scope of specific services varies. For example, a dental benefit may include preventive services only, such as cleanings or x-rays, or more comprehensive coverage, such as crowns or dentures. Plans also vary in terms of cost sharing for various services and limits on the number of services covered per year, many impose an annual dollar cap on the amount the plan will pay toward covered service, and some have networks of dental providers that beneficiaries must choose from.

SNPs restrict enrollment to beneficiaries with significant or relatively specialized care needs, or who qualify because they are eligible for both Medicare and Medicaid. Enrollees in SNPs have greater access than other Medicare Advantage enrollees to transportation (73% vs 22%), meal benefits (81% vs 65%), bathroom safety devices (60% vs 21%), over-the-counter benefits (98% vs 68%), and in-home support services (38% vs 10%). Enrollees in SNPs who are dually eligible for Medicare and Medicaid may also have access to similar benefits through Medicaid.

It is not known what share of enrollees have used these benefits because data are not yet available.

As of 2020, Medicare Advantage plans have been allowed to include telehealth benefits as part of the basic Medicare Part A and B benefit package – beyond what was allowed under traditional Medicare prior to the public health emergency, which has again been extended to December 31, 2027. Therefore, these benefits are not included in the figure above because their cost is not covered by either rebates or supplemental premiums. Medicare Advantage plans may also offer supplemental telehealth benefits via remote access technologies and/or telemonitoring services, which can be used for those services that do not meet the requirements for coverage under traditional Medicare or the requirements for additional telehealth benefits (such as the requirement of being covered by Medicare Part B when provided in-person). Less than half of enrollees in both individual plans and SNPs are in plans that offer remote access technologies (43% and 39%, respectively), and just 2% of enrollees in individual plans and 1% of enrollees in SNPs have access to telemonitoring services.

Nearly all Medicare Advantage enrollees are in plans that offer vision, dental, and hearing benefits, similar to 2025, while fewer are offered over-the-counter benefits, meals, remote access technologies, transportation, and bathroom safety devices.

In 2026, there were changes to the share of enrollees in plans that offer specific benefits compared to 2025. The same share of enrollees in individual plans are in plans that offer eye exams and/or eyeglasses, dental benefits, and hearing exams and/or aids (Figure 5). However, smaller shares of enrollees are in plans that offer over-the-counter benefits (68% in 2026 vs 79% in 2025), meal benefits (65% in 2026 vs 70% in 2025), remote access technologies (43% in 2026 vs 49% in 2025), transportation benefits (22% in 2026 vs 28% in 2025), and bathroom safety devices (21% in 2026 vs 32% in 2025).

For those in Special Needs Plans (SNPs), similar shares of enrollees are in plans that offer eye exams and/or eyeglasses, dental benefits, and hearing exams and/or aids compared to 2025. Larger shares of SNP enrollees are in plans that offer in home-support services (38% in 2026 vs 11% in 2025). However, smaller shares of SNP enrollees are in plans that offer transportation benefits (73% in 2026 vs 80% in 2025), bathroom safety devices (60% in 2026 vs 68% in 2025), and remote access technologies (39% in 2026 vs 46% in 2025).

Despite concerns that recent changes to Medicare Advantage payment may impact the availability of extra benefits, overall, Medicare Advantage enrollees have not experienced a substantial loss in access to supplemental benefits, particularly dental, vision, hearing, and fitness benefits. However, the availability of some supplemental benefits, such as those mentioned above, has decreased over the last few years, down from a peak in 2023. This analysis also does not account for any changes to the design of benefits, which could make benefits more or less generous, such as changes to eligibility for these benefits, networks of providers, required cost sharing, or the generosity coverage.

Additionally, while CMS collects data on the use and spending for supplemental benefits, these data are not currently available to researchers or consumers. Further, CMS does not collect detailed data on prior authorization requests and denials for these benefits.

Nearly one-third (31%) of enrollees are in plans that offer a rebate against the Part B premium, though the dollar values of the rebates are often small.

In 2026, about one-third (32%) of individual plan enrollees were in plans that offer a Part B rebate, the same as in 2025. Although the Part B rebate is often used in Medicare Advantage marketing (sometimes described as “money back in your Social Security check”), for most enrollees, the dollar value of the rebate is small relative to the $202.90 standard Part B premium in 2026. Among the 6.7 million beneficiaries in an individual Medicare Advantage plan that provides a Part B rebate, 39% (2.6 million) are in plans that offer rebates of less than $10 a month, though about one-third (32%; 2.2 million) are in plans that offer rebates of $100 or more per month. (Figure 6). In other words, about 12% of all Medicare Advantage enrollees in individual plans get $10 a month off their monthly Part B premium, while 10% get $100 or more off their monthly premium.

In 2026, 30% of SNP enrollees were in plans that offer a Part B rebate, down from 44% in 2025. Among all SNP enrollees, 22% are in plans with a rebate of less than $10 a month. Most SNP enrollees are dually eligible for Medicare and Medicaid, and Medicaid pays the Part B premiums on their behalf (except in Puerto Rico). When dually-eligible individuals enroll in a Medicare Advantage plan with a Part B rebate, the state Medicaid program receives the Part B premium rebate payment from the plan (except in Puerto Rico).

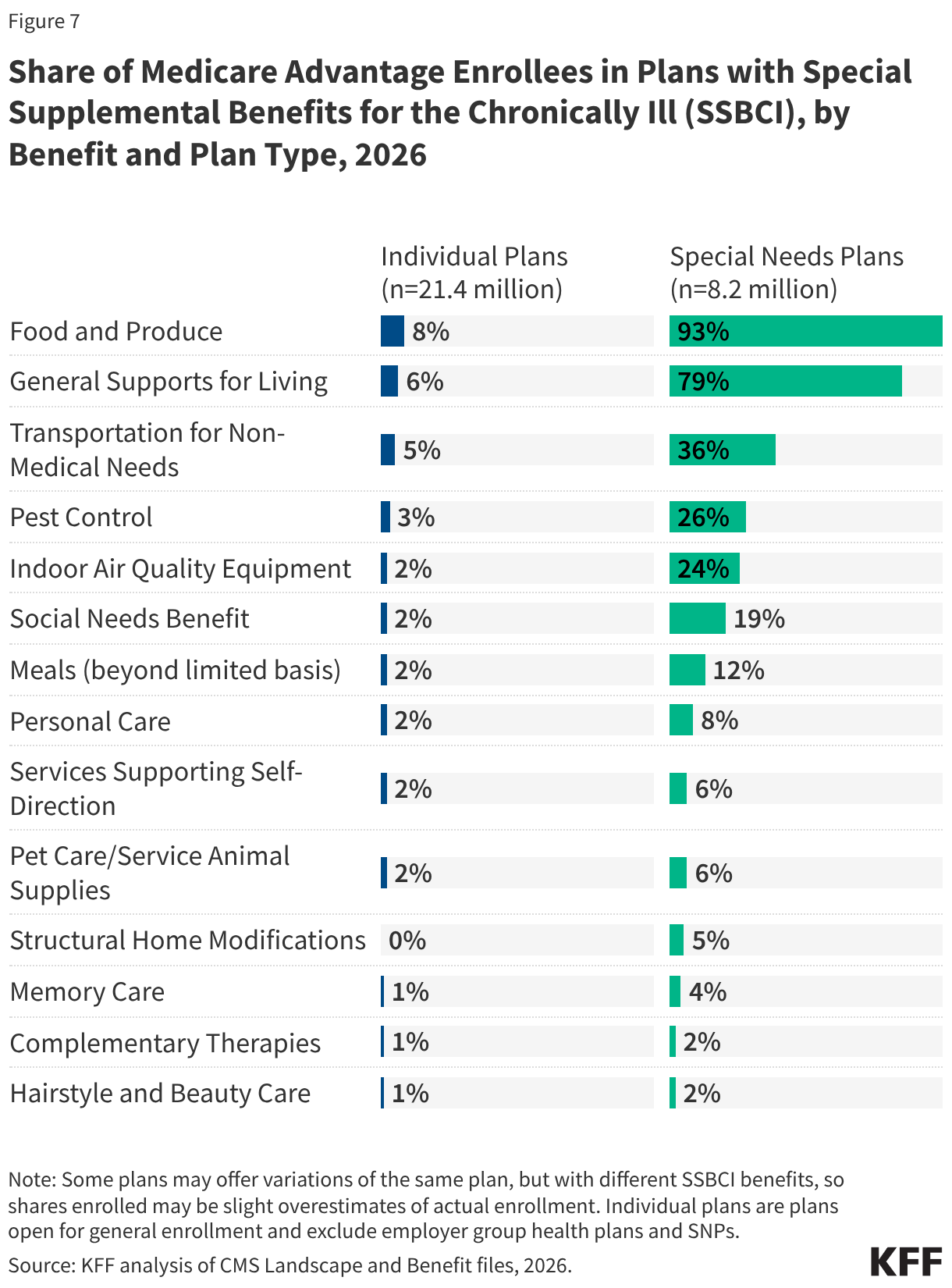

Enrollees in SNPs are more likely to be in plans that offer Special Supplemental Benefits for the Chronically Ill (SSBCI) than other Medicare Advantage enrollees.

Beginning in 2020, Medicare Advantage plans have also been able to offer supplemental benefits that are not primarily health related for chronically ill beneficiaries, known as Special Supplemental Benefits for the Chronically Ill (SSBCI). In addition, Medicare Advantage plans participating in the Value-Based Insurance Design Model (which was discontinued at the end of 2025) also offered these non-primarily health related supplemental benefits to their enrollees, but used different eligibility criteria than required for SSBCI, including offering them based on an enrollee’s socioeconomic status (e.g., LIS eligibility) or whether the enrollee lives in an underserved area. While this analysis provides information on the share of Medicare Advantage enrollees in plans that offer these SSBCI benefits, data on how many beneficiaries use these benefits and how often they use them are not currently available.

In 2026, the share of Medicare Advantage enrollees offered SSBCI is highest for food and produce—8% of individual plan enrollees (1.8 million), and the vast majority (93%) of SNP enrollees (7.6 million) are offered this benefit (Figure 7).

The other SSBCI benefits that are most commonly offered are:

- General supports for living (e.g., housing, utilities) (6% for individual plans vs 79% for SNPs)

- Transportation for non-medical needs (5% for individual plans vs 36% for SNPs)

- Pest control (3% for individual plans vs 26% for SNPs)

- Meals beyond a limited basis (2% for individual plans vs 12% for SNPs)

- A social needs benefit (e.g., community programs)(2% for individual plans vs 19% for SNPs)

- Indoor air quality equipment and services (e.g., air conditioning units)(2% for individual plans vs 24% for SNPs)

- Services supporting self-direction (e.g., power of attorney for health services, financial literacy classes) (2% for individual plans vs 6% for SNPs)

- Complementary therapies (those offered alongside traditional medical treatment) (1% for individual plans vs 2% for SNPs)

- Structural home modifications (0.04% for individual plans vs 5% for SNPs)

In addition to the 10 initially enumerated examples of SSBCI provided by CMS, plans are also able to offer “other” extra benefits specified by the plan, including pet care/service animal supplies (2% in individual plans and 6% for SNPs), personal care (2% in individual plans and 8% for SNPs), memory care (1% in individual plans and 4% for SNPs), and hairstyling and beauty care (1% in individual plans and 2% for SNPs). However, this is not an exhaustive list of additional benefits plans may offer.

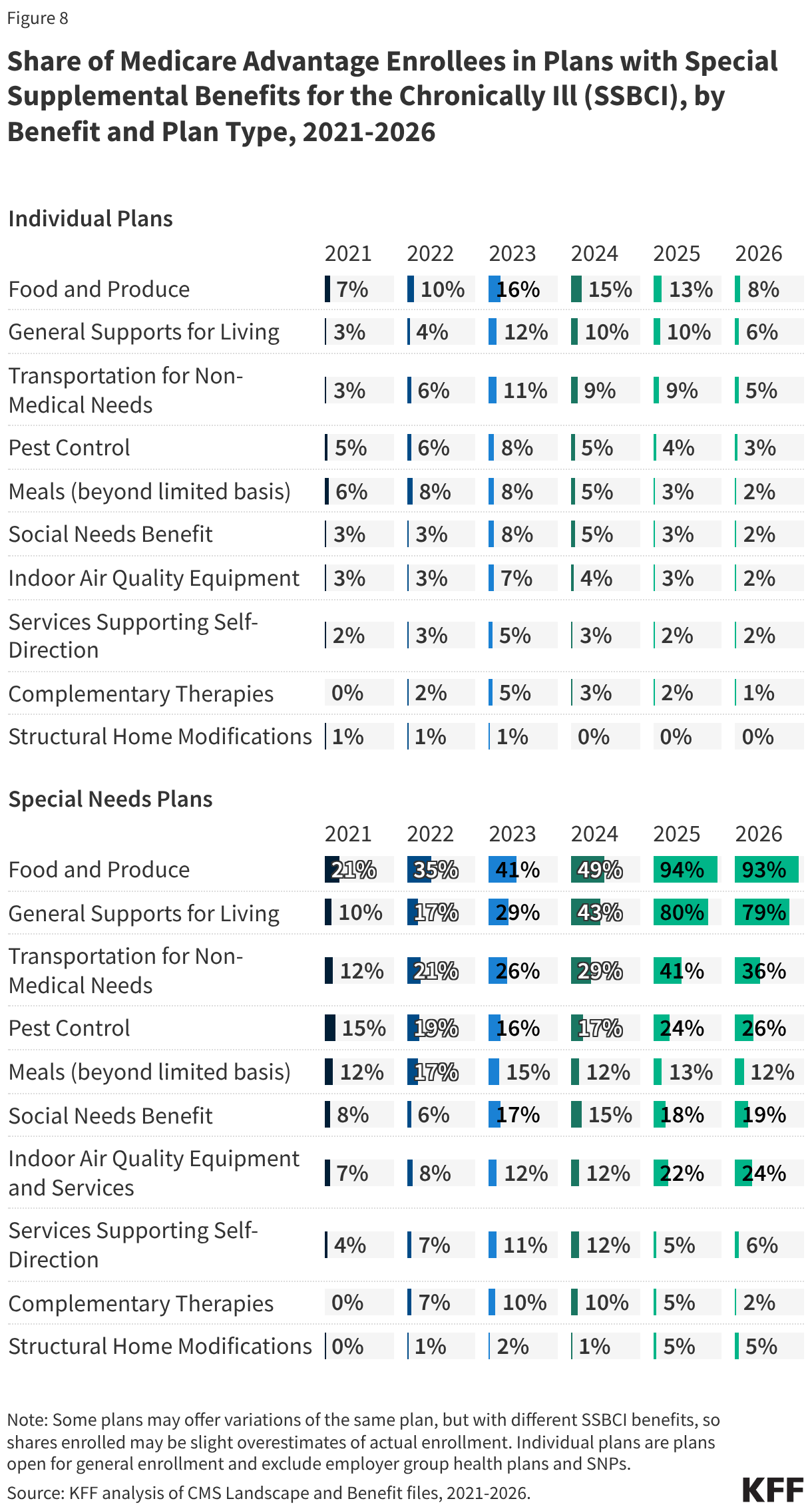

While the share of enrollees with plans that offer some SSBCI benefits has increased since 2021, such as food and produce, growth for other benefits has been much slower.

Though the share of SNP enrollees in plans with food and produce benefits and general supports for living benefits has grown considerably since 2021, the share of enrollment in plans for other SSBCI benefits has grown much more slowly, particularly for enrollees in individual plans (Figure 8). For example, the share of SNP Medicare Advantage enrollees with food and produce benefits has more than quadrupled from 21% in 2021 to 93% in 2026—with the sharpest growth from 2024 (49%) to 2025 (94%)—while for individual plans, food and produce benefits are far less common. The share of enrollees with these benefits increased modestly from 2021 to 2023 (from 7% to 16%) but has declined back to 8% in 2026. For general supports for living benefits, the share of SNP Medicare Advantage enrollees with these benefits has also significantly increased from 10% to 79%—with the sharpest growth from 2024 (43%) to 2025 (80%)—while for individual plans, the share more than tripled to 2025, from 3% to 10%, but has declined back to 6% in 2026.

Like for other supplemental benefits, the scope of services for SSBCI benefits varies. For example, many plans offer a specified dollar amount that enrollees can use toward a variety of benefits, such as food and produce, utility bills, rent assistance, and transportation for non-medical needs, among others. This dollar amount is often loaded onto a flex card or spending card that can be used at participating stores and retailers, which can vary depending on the vendor administering the benefit. Depending on the plan, this may be a monthly allowance that expires at the end of each month or rolls over month to month until the end of the year, when any unused amount expires.

Nearly all Medicare Advantage enrollees are in plans that require prior authorization for many higher-cost services.

Medicare Advantage plans can require enrollees to receive prior authorization before a service will be covered, and nearly all Medicare Advantage enrollees (99%) are in plans that require prior authorization for some services in 2026 (Figure 9). Prior authorization is most often required for relatively expensive services, such as inpatient hospital stays (acute: 97%; psychiatric: 93%), skilled nursing facility stays (95%), Part B drugs (94%), and home health services (90%) and is rarely required for preventive services (6%). Prior authorization is also required for the majority of enrollees for some extra benefits (in plans that offer these benefits), including preventive dental services, and hearing and eye exams.

The number of enrollees in plans that require prior authorization for one or more services stayed around the same from 2025 to 2026. In contrast to Medicare Advantage plans, traditional Medicare does not generally require prior authorization for services and does not require step therapy for Part B drugs. However, the Center for Medicare & Medicaid Innovation (CMMI) is testing a new model, the Wasteful and Inappropriate Service Reduction (WISeR) Model, that uses technologies such as artificial intelligence to apply prior authorization for a limited set of services in six states in traditional Medicare.

In 2024, nearly 53 million prior authorization requests were submitted to Medicare Advantage insurers, with insurers denying 4.1 million or nearly 8% of those requests. While Medicare Advantage insurers are required to publish some data on timeliness and use of prior authorization, information is not currently available on how prior authorization requests, denials, and appeals vary by type of service, plan, or enrollee characteristics because CMS does not collect or report this information.

Methods

This analysis uses data from the Centers for Medicare & Medicaid Services (CMS) Medicare Advantage Enrollment, Benefit and Landscape files for the respective year.

In previous years, KFF had used the term Medicare Advantage to refer to Medicare Advantage plans as well as other types of private plans, including cost plans, PACE plans, and HCPPs. However, since 2022, KFF has excluded cost plans, PACE plans, HCPPs in addition to MMPs. We exclude these other plans as some may have different enrollment requirements than Medicare Advantage plans (e.g., may be available to beneficiaries with only Part B coverage) and in some cases, may be paid differently than Medicare Advantage plans. These exclusions are reflected in both current data as well as data displayed trending back to 2010.

In previous years, KFF’s analysis of average out-of-pocket limits in Medicare Advantage excluded HMOs that are Point-of-Service plans (HMO-POS), which allow out-of-network care for certain services, because they represented a relatively small share of HMO enrollment at the time (e.g., 10% in 2017). However, HMO-POS enrollment has grown substantially and now accounts for nearly half (46%) of HMO enrollment in Medicare Advantage. As a result, these plans are included in the current analysis to better reflect the experience of a substantial share of Medicare Advantage enrollees in HMOs.

Meredith Freed, Jeannie Fuglesten Biniek, and Tricia Neuman are with KFF. Anthony Damico is an independent consultant.