Medicare Advantage 2024 Spotlight: First Look

Data Note

This analysis, originally published on Nov. 8, 2023, has been updated to reflect that CalOptima Health OneCare is not a new entrant in the Medicare Advantage market and that Orange County Health Authority and Imperial Health Plan of California are not exiting insurers.

Over the last decade, Medicare Advantage, the private plan alternative to traditional Medicare, has taken on a prominent role in the Medicare program. In 2023, nearly 31 million Medicare beneficiaries are enrolled in a Medicare Advantage plan, more than half, or 51%, of the eligible Medicare population. This brief provides an overview of the Medicare Advantage plans that are available for 2024 and key trends over time. (A separate overview of the 2024 Medicare Part D marketplace is also available.)

Medicare Advantage Highlights for 2024

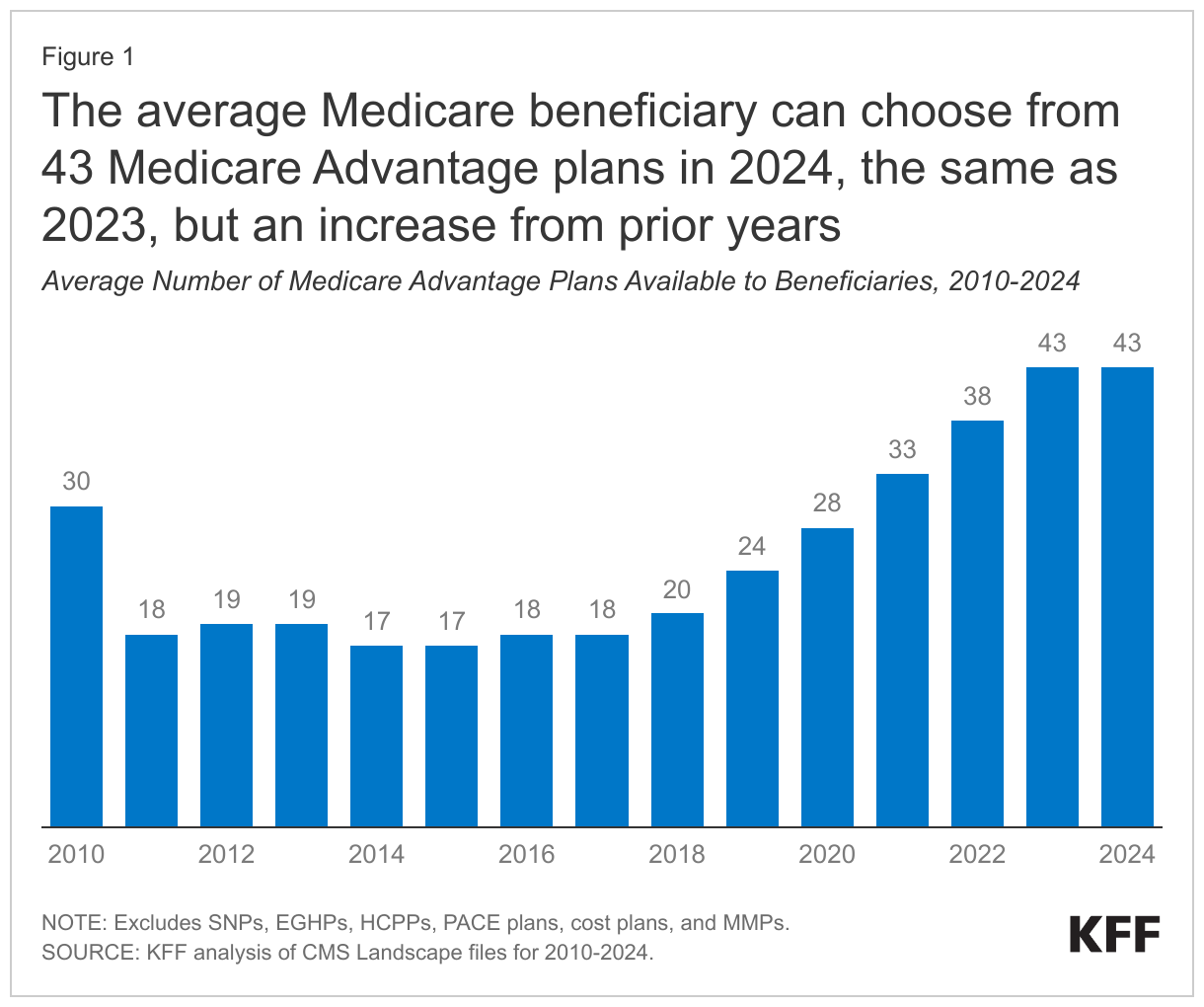

- The average Medicare beneficiary has access to 43 Medicare Advantage plans in 2024, the same as in 2023, but more than double the number of plans offered in 2018.

- HMOs account for more than half of all Medicare Advantage plans nationwide (56% in 2024) but are declining as a share of total, while local PPOs are rising as a share of all plans (42% in 2024).

- The number of D-SNPs (for dually-eligible beneficiaries) has increased substantially over the past five years, nearly doubling from 465 dual SNPs in 2019 to 851 dual SNPs in 2024.

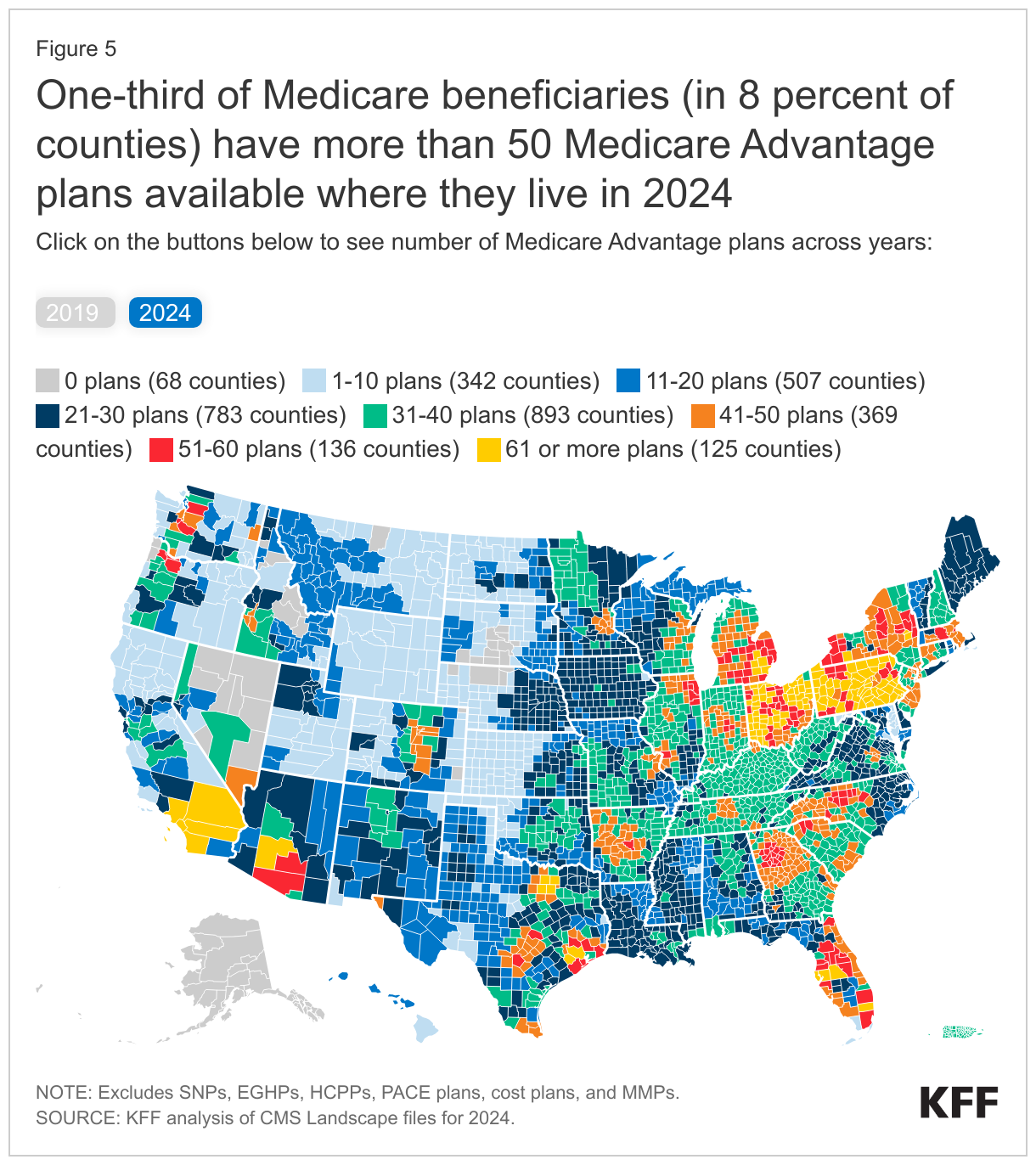

- One-third of Medicare beneficiaries live in a county with more than 50 Medicare Advantage plans available in 2024, up from 1 percent in 2019. Less than 1 percent of beneficiaries live in a county with fewer than four Medicare Advantage plans available.

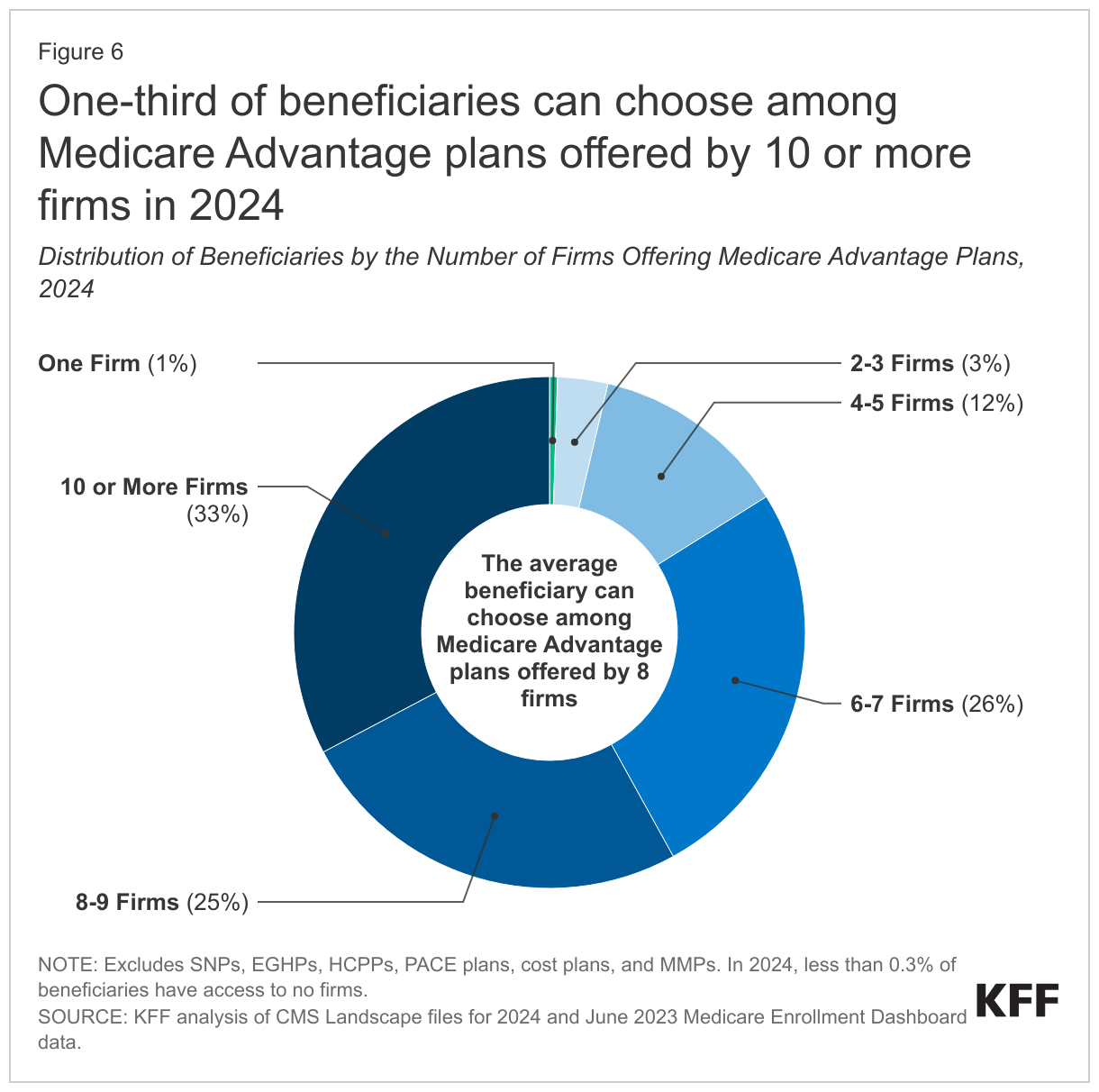

- The average Medicare beneficiary can choose among plans offered by 8 firms in 2024, one fewer than in 2023. Three new insurers entered the Medicare Advantage market in 2024, two of which offer SNPs, while twelve firms exited the market in 2024, principally due to low or no enrollment.

- Humana and UnitedHealthcare plans are available in most counties in 2024 (90% and 87%, respectively). Most major insurers are also expanding into new counties, with CVS Health expanding in the largest number of counties in 2024.

- Two thirds of all MA-PDs (66%) will charge no premium (other than the Part B premium) in 2024, the same as in 2023. In addition, 19% of Medicare Advantage plans will offer some reduction in the Part B premium in 2024, similar to 2023.

- Most Medicare Advantage plans are offering extra benefits, such as vision, dental and hearing as they have in previous years. Most Medicare Advantage plans are not offering Special Supplemental Benefits for the Chronically Ill, which are extra benefits available to a subset of a plan’s enrollees, that are not primarily health related, and are specifically for chronically ill beneficiaries. However, more SNP plans than individual plans generally offer these benefits, particularly food and produce (60.0% in SNPs compared to 13.9% in individual plans).

Plan Offerings in 2024

Number of Plans

Number of Plans Available to Beneficiaries. For 2024, the average Medicare beneficiary has access to 43 Medicare Advantage plans, the same as 2023, but more than double the average number available in 2018, and the largest number of options available over the period we examined, which goes back to 2010 (Figure 1). These numbers exclude employer or union-sponsored group plans, Special Needs Plans (SNPs), PACE plans, cost plans, and Medicare-Medicaid plans (MMPs) that are only available to select populations.

Of the 43 Medicare Advantage plans available for individual enrollment, 36 of the plans include prescription drug coverage (MA-PDs), on average.

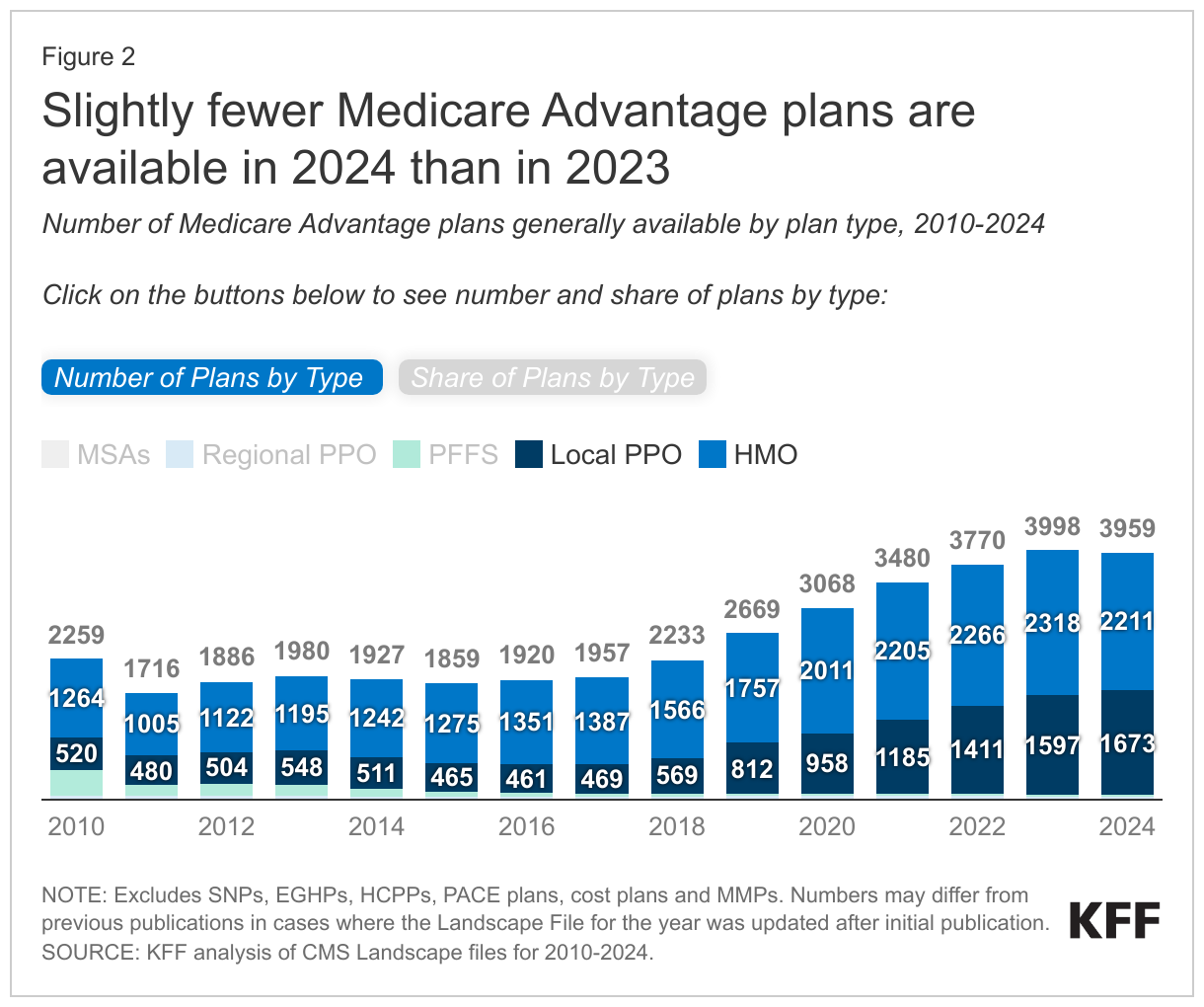

Total Number of Plans. In total, 3,959 Medicare Advantage plans are available nationwide for individual enrollment in 2024 – a slight decrease in the number of plans (1% decrease; 39 fewer plans) offered in 2023. However, it is the second largest number of plans available over the period we examined, which goes back to 2010 (Figure 2; Appendix Table 1).

HMOs account for more than half (56%) of all Medicare Advantage plans offered in 2024 but have declined as a share of all Medicare Advantage plans since 2017 (71% of plans), while local PPOs are rising as a share of all plans. During this period, the availability of local PPOs has increased from 24% in 2017 to 42% in 2024. The share of regional PPOs has slowly declined from around 3% of plans offered in 2017 to 1% in 2024.

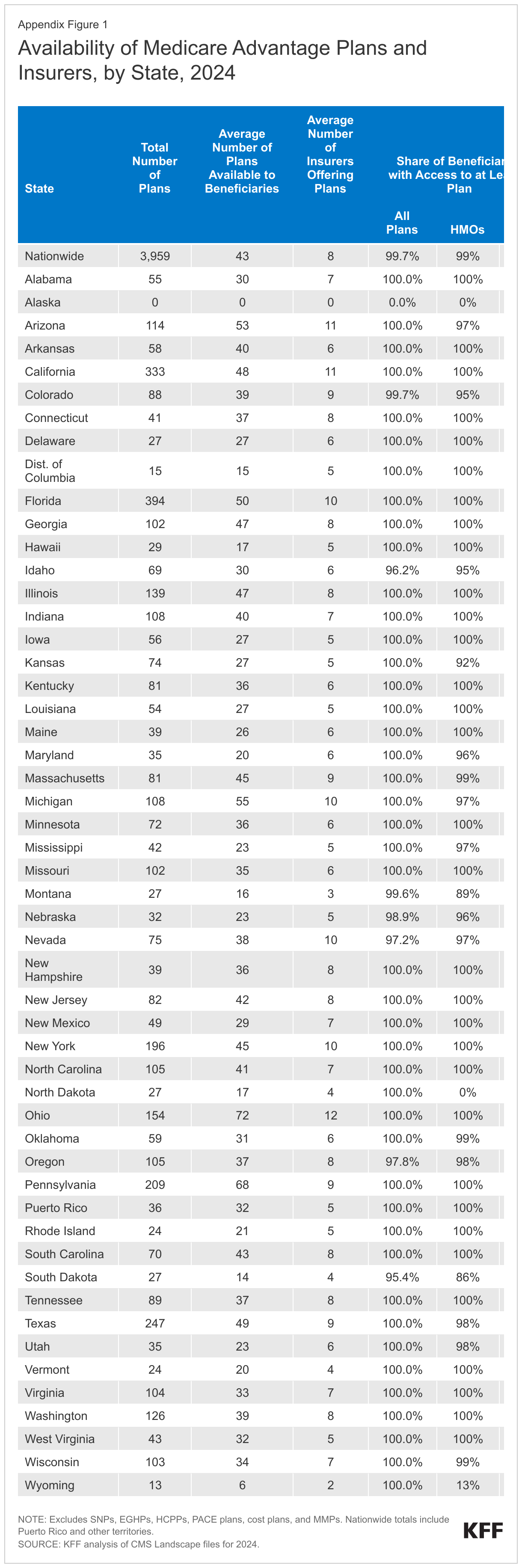

The decline in number of plans varies across states and counties, with the preponderance of the decline occurring in Alabama (20 fewer plans), Illinois (18 fewer plans), and Texas (16 fewer plans) (data not shown), though beneficiaries in Alabama still have a choice of 30 plans on average (down from 32 in 2023), while beneficiaries in Illinois have a choice of 47 plans on average and beneficiaries in Texas have a choice of 49 plans (both down 2 from 2023). Unlike in 2022 and 2023 where two plan options were offered in Alaska, in 2024, there are no plans offered. While there has been an overall decline in the number of plans offered, Colorado has 18 more plans available for 2024 than in 2023. In the remaining states, the number of plans either stayed the same or the growth or decline in plans was 13 or fewer.

While many employers and unions also offer Medicare Advantage plans to their retirees, no information about these 2024 plan offerings is made available by CMS to the public during the Medicare open enrollment period because these plans are administered separately and may have enrollment periods that do not align with the Medicare open enrollment period.

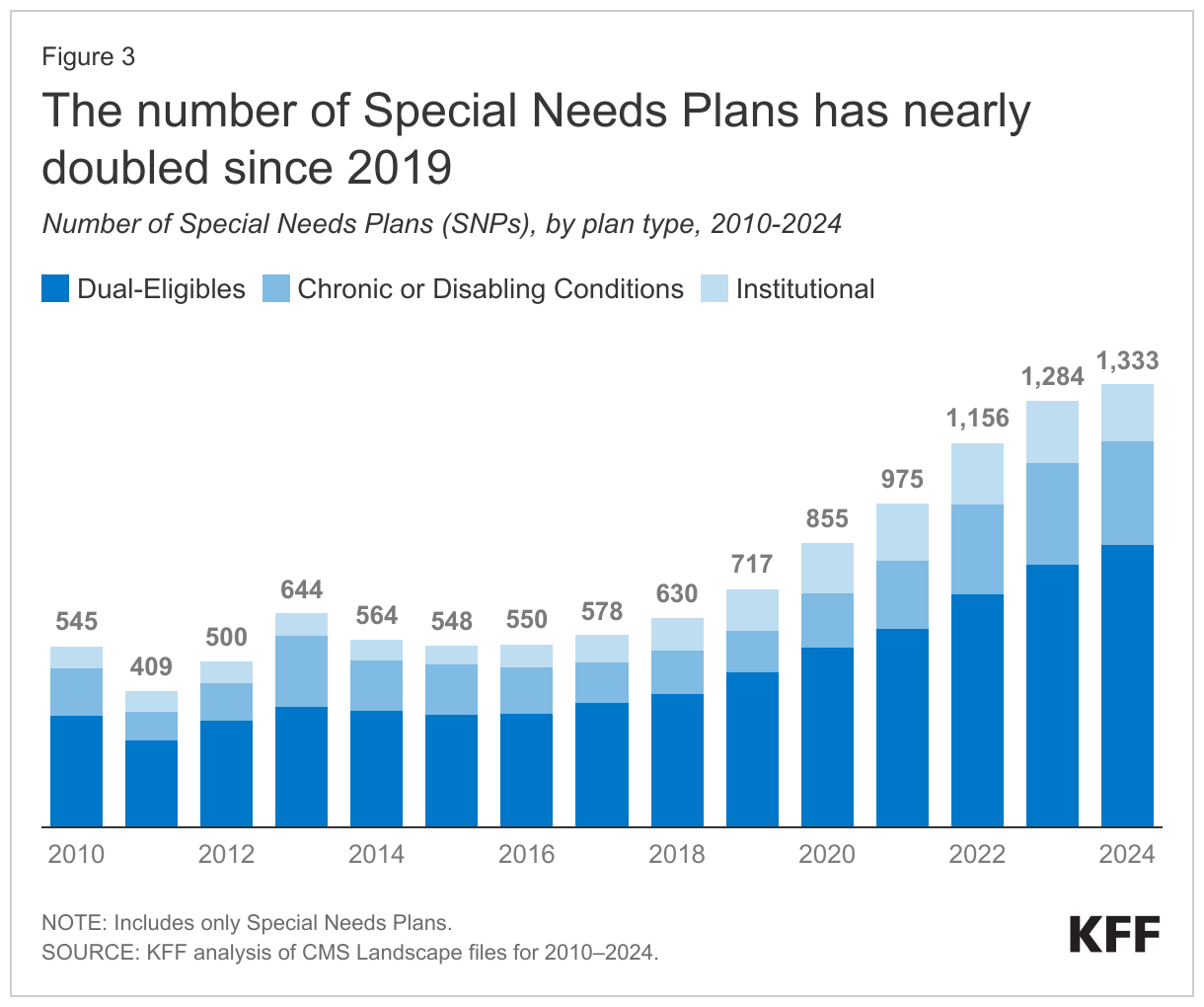

Special Needs Plans (SNPs). In 2024, 1,333 SNPs will be offered nationwide, a 4 percent increase between 2023 and 2024 (Figure 3).

D-SNPs. Nearly two-thirds of SNPs (64%) are designed for people dually eligible for Medicare and Medicaid (D-SNPs). The number of D-SNPs has increased substantially over the past five years, increasing from 465 dual SNPs in 2019 to 851 dual SNPs in 2024, suggesting insurers continue to be drawn to this high-need population.

I-SNPs. The number of SNPs for people who require an institutional-level of care (I-SNPs) nearly doubled from 97 plans in 2018 to 189 plans in 2023, before dropping modestly to 173 plans for 2024. I-SNPs may be attractive to insurers because they tend to have much lower marketing costs than other plan types since they are often the only available option for people who require an institutional level-of-care, such as those who have been in nursing homes for an extended period of time. In 2023, about 100,000 Medicare beneficiaries are enrolled in I-SNPs.

C-SNPs. The number of SNPs offered for people with chronic conditions (C-SNPs) is very similar to 2023 (309 plans in 2024 vs 306 in 2023), more than doubling from 2019 (127 plans). Most C-SNPs focus on people with diabetes, heart disease, or lung conditions, as has been the case since the inception of C-SNPs. For 2024, one firm is offering a C-SNP for people with dementia (compared to two firms in 2023) in four states (California, Florida, Michigan, Virginia). No firms are offering C-SNPs for people with mental health conditions (compared to two firms in 2023), and only one firm is offering a C-SNP for people with HIV/AIDS, the same as 2023. Eight firms are offering C-SNPs for people with end-stage renal disease (up one from 2023).

Variation in the Number of Medicare Advantage Plans, by Geographic Area. Medicare beneficiaries living in metropolitan areas – counties with at least 50,000 people – can choose from 47 Medicare Advantage plans in 2024 on average, substantially more than beneficiaries living in rural or micropolitan areas. Beneficiaries in rural areas – counties with less than 10,000 people – can choose from an average of 27 plans, while beneficiaries in micropolitan areas (10,000 to 50,000 people) can choose from an average of 32 plans.

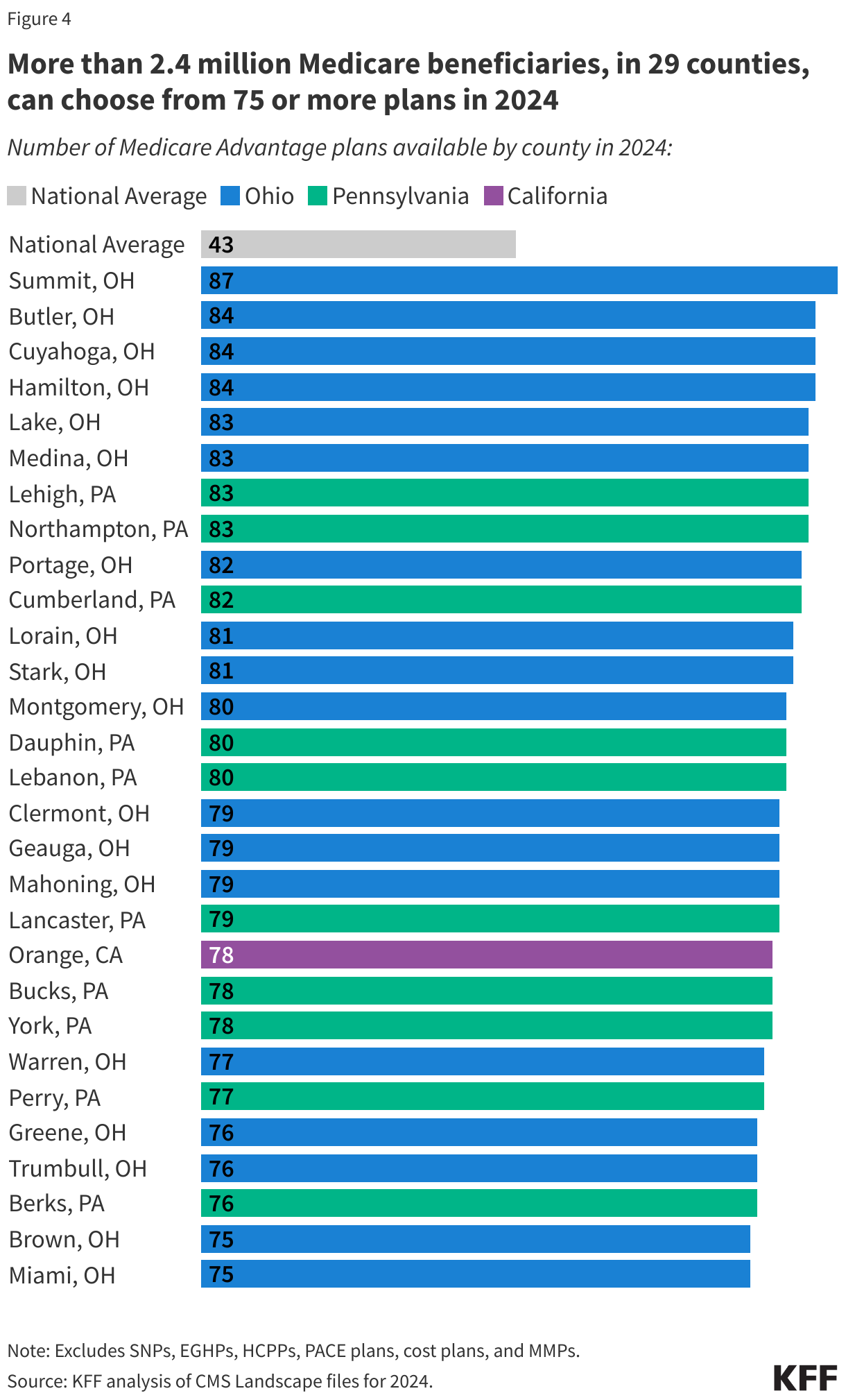

More than 2.4 million beneficiaries in 29 counties can choose from 75 or more Medicare Advantage plans. Similar to the last two years, the counties with the most plan options are predominantly in Ohio and Pennsylvania. In Ohio, for example, beneficiaries can choose from 80 or more Medicare Advantage plans in 10 counties, including Hamilton County (Cincinnati) and Cuyahoga County (Cleveland). Beneficiaries in Summit County, Ohio (Akron) can choose from 87 Medicare Advantage plans – the most offerings of any county in the US. Beneficiaries living in five counties in Pennsylvania can also choose from 80 or more plans. In California, beneficiaries in Orange County can choose from 78 plans (Figure 4).

In 2024, one-third of Medicare beneficiaries (33%) (in 8 percent of counties), can choose from more than 50 Medicare Advantage plans where they live (Figure 5).

The share of Medicare beneficiaries with a choice of at least 50 Medicare Advantage plans has increased from 1% in 2019 to 33% in 2024.

Unlike in 2022 and 2023, there are no Medicare Advantage plans being offered in any county in Alaska in 2024, which includes about 94,000 beneficiaries. In 2024, less than 1 percent of beneficiaries live in a county with fewer than four Medicare Advantage plans available. Additionally, no Medicare Advantage plans are available in territories other than Puerto Rico.

Access to Medicare Advantage Plans, by Plan Type. As in recent years, virtually all Medicare beneficiaries (99.7%) have access to a Medicare Advantage plan as an alternative to traditional Medicare, including almost all beneficiaries in metropolitan areas (99.9%) and the vast majority of beneficiaries in micropolitan (99.5%) and rural areas (98.4%). In micropolitan and rural counties, a smaller share of beneficiaries have access to HMOs (93% in micropolitan counties and 96% in rural counties versus over 99% in metropolitan counties) or local PPOs (98% in micropolitan counties and 96% in rural counties versus 99% in metropolitan counties), while a slightly larger share of beneficiaries in non-metropolitan counties have access to regional PPOs (77% in both micropolitan and rural counties versus 73% in metropolitan counties).

Number of Firms

The average Medicare beneficiary is able to choose from plans offered by 8 firms in 2024, one fewer than in 2023 and 2022 (Figure 6). Despite most beneficiaries having access to plans operated by several different firms, enrollment is concentrated in plans operated by UnitedHealthcare and Humana, and together UnitedHealthcare and Humana account for nearly half (47%) of Medicare Advantage enrollment in 2023.

One-third of beneficiaries (33%), in 211 counties, are able to choose from plans offered by 10 or more firms or other sponsors. Fifteen firms are offering Medicare Advantage plans in Butler and Hamilton counties in Ohio, and 14 firms are offering Medicare Advantage plans in 12 counties: 6 in Ohio, 5 in California, and 1 in Arizona (Maricopa). In contrast, 4 percent of beneficiaries live in a county where one to three firms offer Medicare Advantage plans (528 counties). Further, in 130 counties, most of which are rural counties with relatively few Medicare beneficiaries (less than 1 percent of total), only one firm will offer Medicare Advantage plans in 2024.

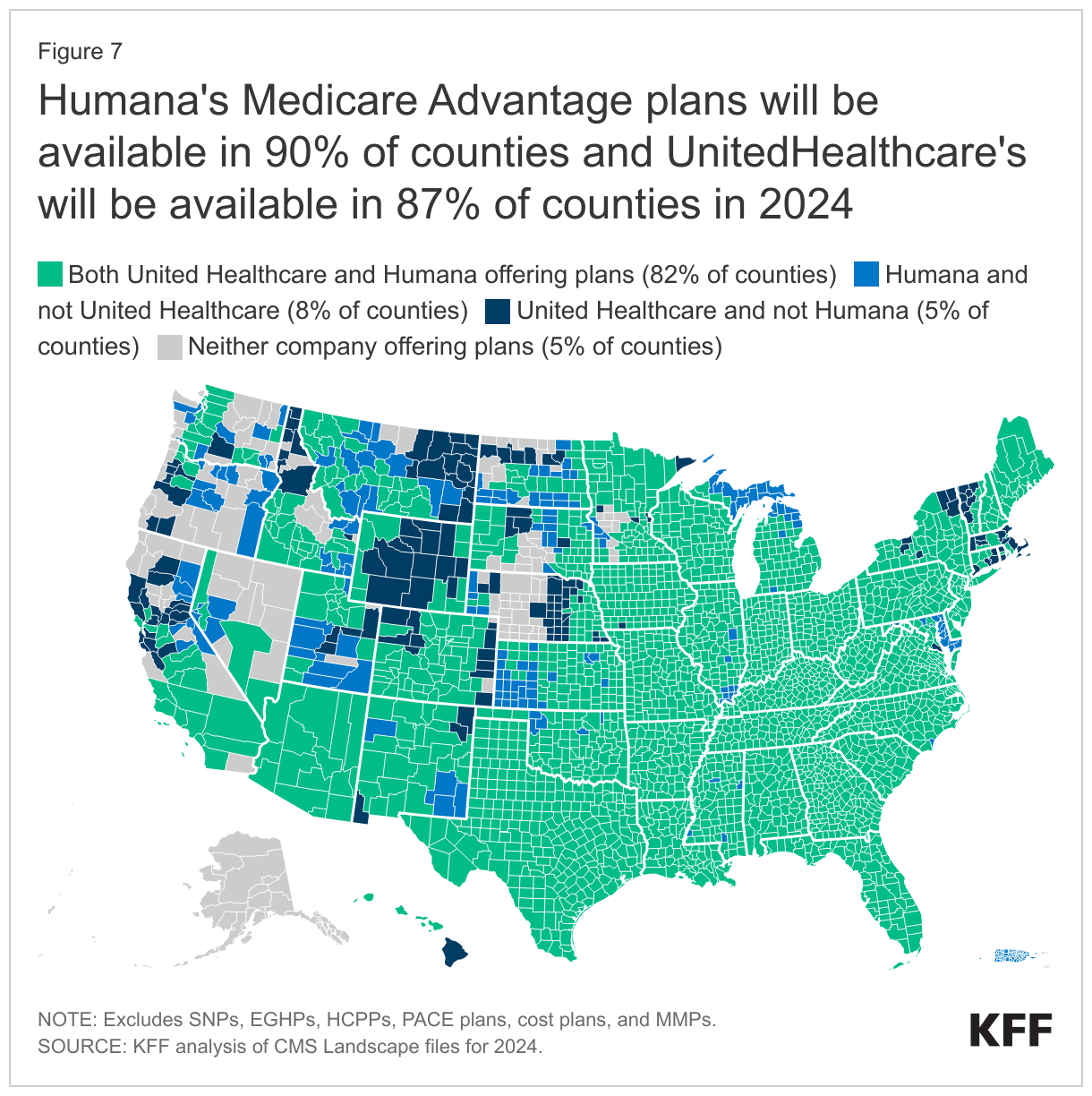

Availability of Plans by Firm and County. UnitedHealthcare and Humana, the two firms with the most Medicare Advantage enrollees in 2023, have large footprints across the country, offering plans in most counties. Humana is offering plans in 90 percent of counties and UnitedHealthcare is offering plans in 87 percent of counties in 2024, roughly the same as in 2023 (Figure 7).

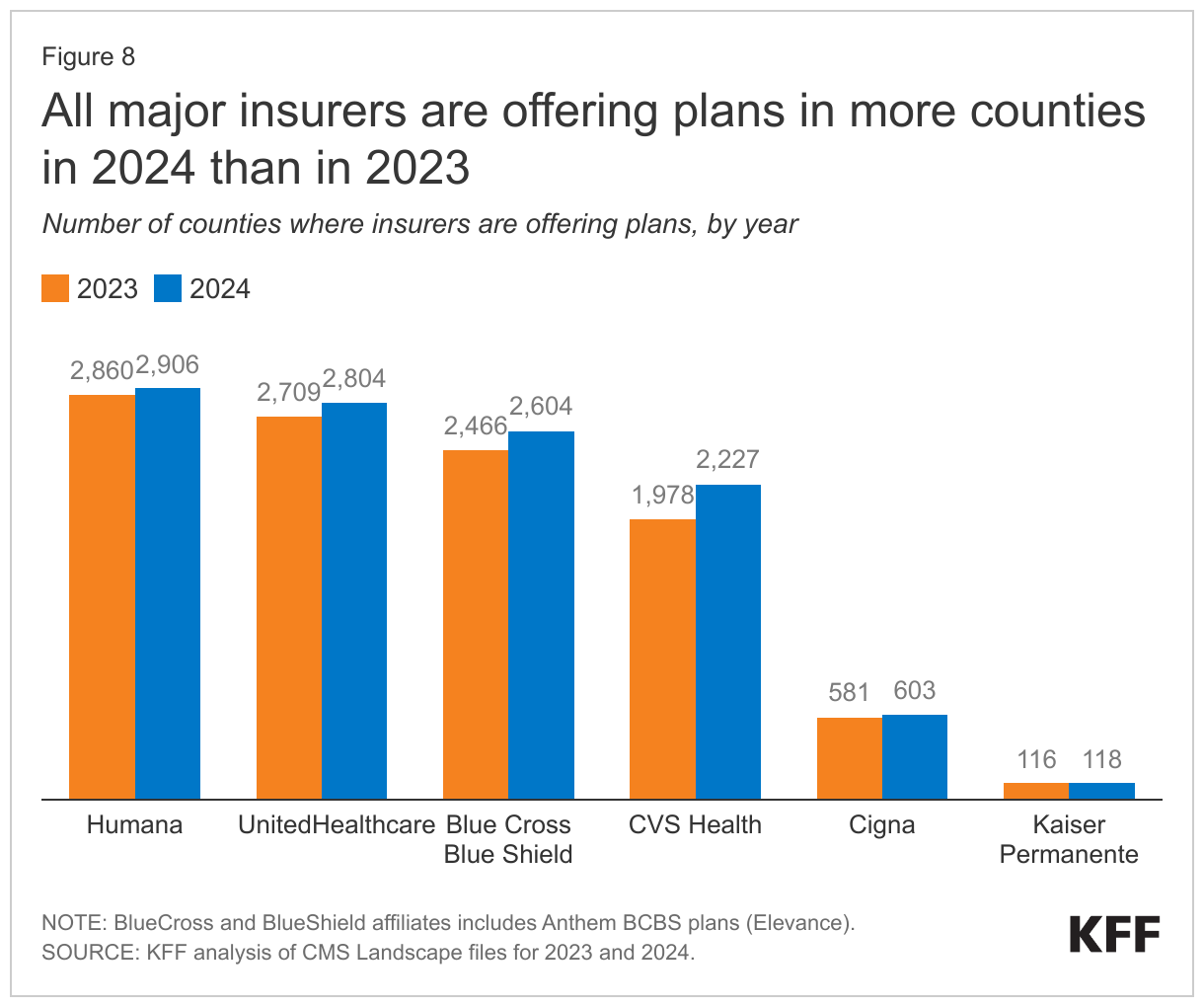

Most major insurers are also expanding into new counties, with CVS Health expanding in the largest number of counties in 2024 – an increase of 249 counties from 2023 (2,227 counties overall) (Figure 8).

Blue Cross Blue Shield Affiliates are offering plans in 2,604 counties in 2024, an increase of 138 counties from 2023. UnitedHealthcare is offering plans in 2,804 counties in 2024, an increase of 95 counties from 2023, while Humana is offering plans in 2,906 counties in 2024, an increase of 46 counties from 2023. Cigna is offering plans in 603 counties, an increase of 22 counties, and Centene is offering plans in 1,748 counties, an increase of 9 counties; Kaiser Permanente is offering plans in 118 counties, an increase of 2 counties.

Multiple Plan Offerings by Firms in the Same County. Many Medicare Advantage firms are also offering more than one plan option in each county. In 1,276 counties (accounting for 59% of beneficiaries), at least one firm is offering 10 or more plans for individual enrollment. For example, in Bucks and Delaware counties in Pennsylvania, four firms are offering 10 or more plans (Humana, UnitedHealthcare, Blue Cross Blue Shield Affiliates, and CVS Health). In 92 counties, two firms are offering 10 or more plans, and in 28 counties, three firms are offering 10 or more plans.

Blue Cross Blue Shield Affiliates and Humana are offering the most plan options in individual counties. BCBS Affiliates are offering 19 different plan options in seven counties, 17 plan options in 9 counties, and 16 plans in 5 counties. Humana is offering 18 Medicare Advantage plans in three counties, 17 plan options in 1 county, and 16 plan options in 35 counties.

New Market Entrants and Exits

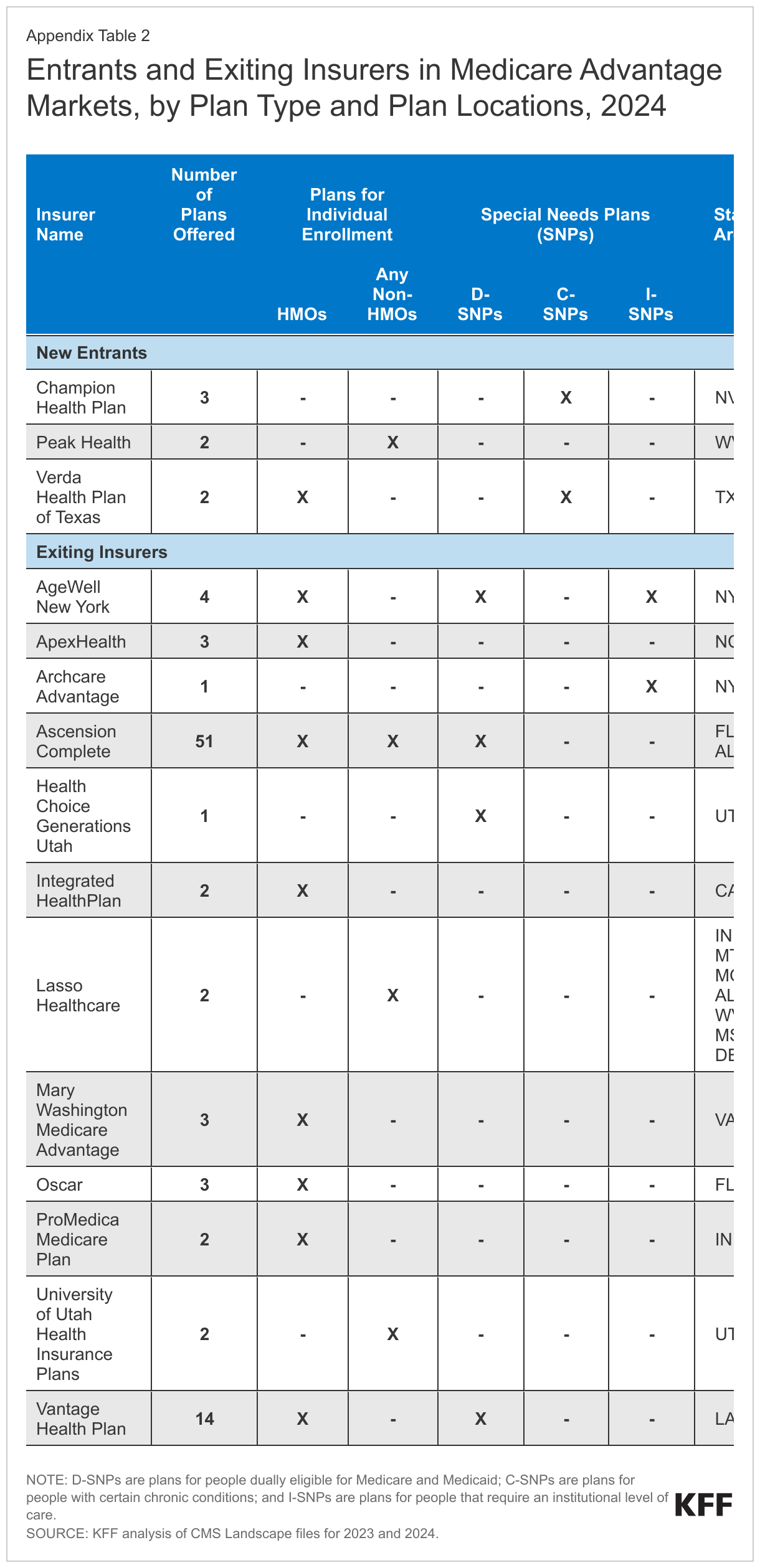

In 2024, three firms (Champion Health Plan, Peak Health, and Verda Health Plan of Texas) entered the market for the first time, while twelve firms exited the market. One new entrant has two new plans available for general enrollment in West Virginia. Two firms are offering C-SNP plans, for people with select chronic conditions in California, Nevada, and Texas. collectively accounting for about 12 percent of the growth in SNPs (Appendix Table 2).

In the last few years, more firms have introduced plans that are either co-branded or are in partnership with another company. For example, in 2024, Alignment Health is offering four plans co-branded with Instacart in 13 counties in California and Nevada. These plans will offer groceries to qualifying beneficiaries with chronic conditions. UnitedHealthcare has partnered with Walgreens over the last few years to offer plans, while Alignment Health has a new partnership with Walgreens for 2024. UnitedHealthcare’s plans with Walgreens in 2024 are available in California, Georgia, Illinois, Missouri, Nevada, Texas, Utah, and Wisconsin, while Alignment Health’s plans with Walgreens in 2024 are offered in Arizona, California, Florida and Texas. Other companies with a partnership that are offering plans in 2024 include Select Health and Kroger and Alignment Health and Rite Aid, though this is not an exhaustive list.

Twelve firms that participated in the Medicare Advantage market in 2023 are not offering plans in 2024. Five of the fourteen firms had low enrollment in 2023 (less than 3,500 enrollees) while five firms either had no enrollment or enrollment of less than 11 people in 2023, one of which was a Medicare Medical Savings Account (MSA) operating in many states. Two of the firms with slightly higher enrollment had contracts taken over by other insurers.

Premiums

The vast majority of Medicare Advantage plans for individual enrollment (89%) will include prescription drug coverage (MA-PDs), and the share of MA-PDs that charge no premium (other than the Part B premium) is 66% in 2024, the same as in 2023. In addition, 19% of Medicare Advantage plans will offer some reduction in the Part B premium in 2024, similar to the share in 2023. Nearly all beneficiaries (99%) have access to a MA-PD with no additional monthly premium in 2024, the same as in 2023 (99%).

In 2023, 73% of enrollees in MA-PD plans pay no premium other than the Medicare Part B premium of $164.90 per month. Based on enrollment in March 2023, 10% of enrollees pay at least $50 a month, including 3% who pay $100 or more. CMS announced that the average monthly plan premium among all Medicare Advantage enrollees in 2024, including those who pay no premium for their Medicare Advantage plan, is expected to be $18.50 a month. In 2023, 10 percent of Medicare Advantage enrollees are in a plan that offered some reduction in Medicare Part B premiums.

Extra Benefits

Medicare Advantage plans may provide extra benefits that are not available in traditional Medicare, are considered “primarily health related,” and can use rebate dollars (including bonus payments) to help cover the cost of these extra benefits. Beginning in 2019, CMS expanded the definition of “primarily health related” to allow Medicare Advantage plans to offer additional supplemental benefits. Medicare Advantage plans may also restrict the availability of these extra benefits to certain subgroups of beneficiaries, such as those with diabetes or congestive heart failure, making different benefits available to different enrollees.

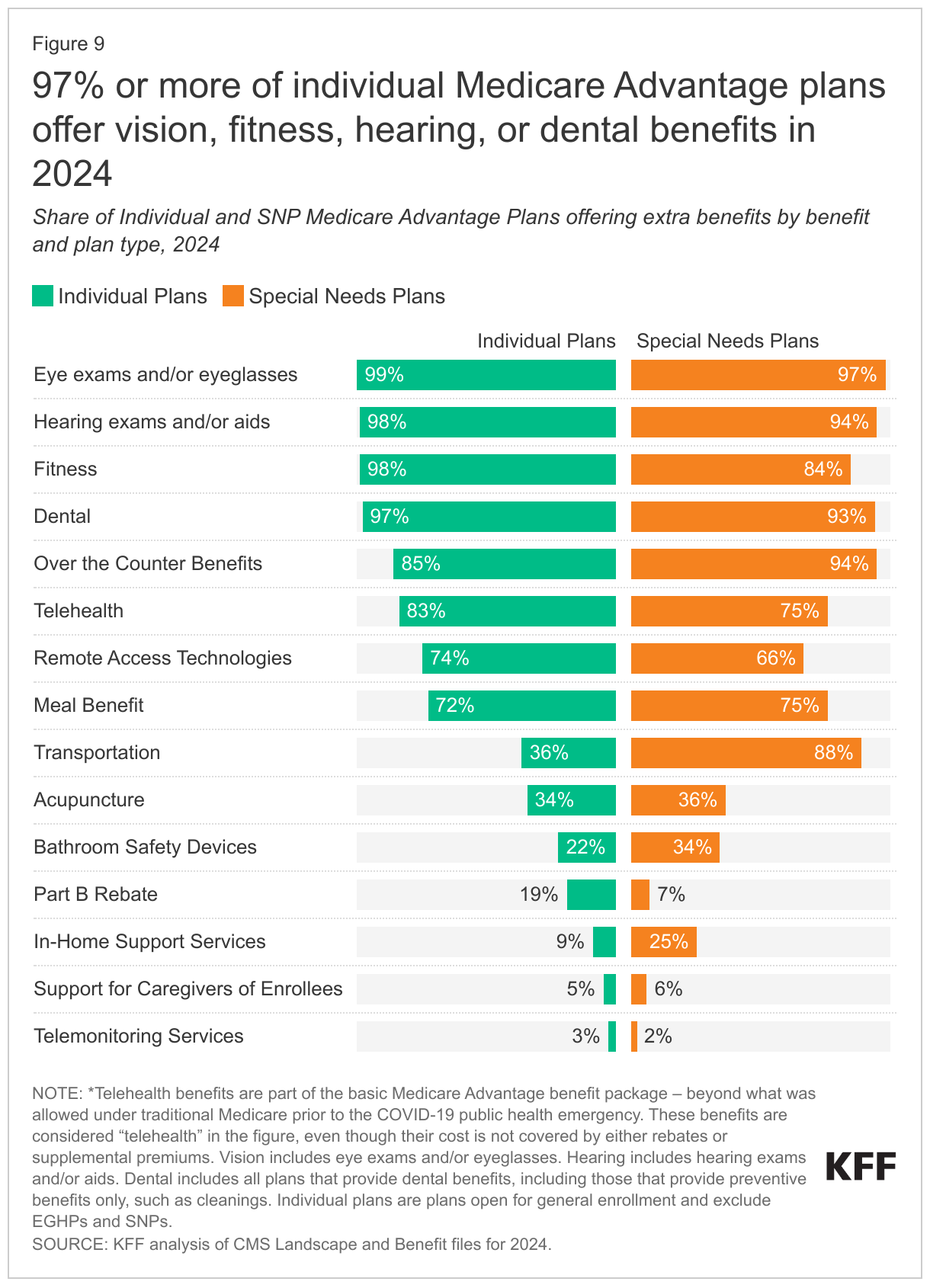

Availability of Extra Benefits in Plans for General Enrollment. In 2024, 97% or more individual plans offer some vision, fitness, hearing or dental benefits (Figure 9). Though these benefits are widely available, the scope of coverage for these services varies. For example, a dental benefit may include cleanings and preventive care or more comprehensive coverage, and often is subject to an annual dollar cap on the amount covered by the plan. Plans are not required to report data about utilization of these benefits or associated costs, so it is not clear the extent to which supplemental benefits are used by enrollees.

As of 2020, Medicare Advantage plans have been allowed to include telehealth benefits as part of the basic benefit package – beyond what was allowed under traditional Medicare prior to the COVID-19 public health emergency. These benefits are shown in the figure above, even though their costs are built into the bid, and are not covered by either rebates or supplemental premiums. Additionally, Medicare Advantage plans may offer supplemental telehealth benefits via remote access technologies and/or telemonitoring services, which can be used for those services that do not meet the requirements for coverage under traditional Medicare or the requirements for the telehealth benefits as part of the basic benefit package (such as the requirement of being covered by Medicare Part B when provided in-person). The majority (83%) of Medicare Advantage plans are offering telehealth in 2024, but a decline from 2023, when 97% of plans offered these benefits.

Other extra benefits that are frequently offered for 2024, similar to the share of plans offering these benefits in 2023, include over the counter items, such as adhesive or elastic bandages (85%), remote access technologies (74%), meal benefits, such as meal delivery (72%), acupuncture (34%), support for caregivers of enrollees (5%), and telemonitoring services (3%). A little more than a third of plans offer transportation benefits for medical needs (36%), down from 43% in 2023, about two in ten plans (22%) offer access to bathroom safety devices, up from 10% in 2023, and nine percent offer in-home support services, down from 14% in 2023. This is not an exhaustive list of extra benefits that plans offer, and plans may provide other services such as home-based palliative care, therapeutic massage, and adult day health services, among others.

Access to Medicare Advantage Plans with Extra Benefits. Virtually all Medicare beneficiaries live in a county where at least one Medicare Advantage plan available for general enrollment (excluding SNPs) has some extra benefits not covered by traditional Medicare, with over 99% having access to at least one or more plans with dental, fitness, vision, and hearing benefits for 2024. The vast majority of beneficiaries also have access to one or more plans that offer telehealth benefits (over 99%), over the counter items (over 99%), a meal benefit (over 99%), remote access technologies (99%), acupuncture (99%), bathroom safety devices (97%), transportation assistance (96%) but fewer have access to one or more plans that offer in-home support services (72%), caregiver support (44%), or telemonitoring services (20%) .

Availability of Extra Benefits in Special Needs Plans. SNPs are designed to serve a disproportionately high-need population, and a somewhat larger percentage of SNPs than plans for other Medicare beneficiaries provide their enrollees over the counter benefits (94%; up from 86% in 2023), transportation benefits for medical needs (88%; the same as 2023), bathroom safety devices (34%; up from 14% in 2023), and in-home support services (25%; down from 34% in 2023). Similar to plans available for general enrollment, a relatively small share of SNPs offer support for caregivers (6%) or telemonitoring services (2%).

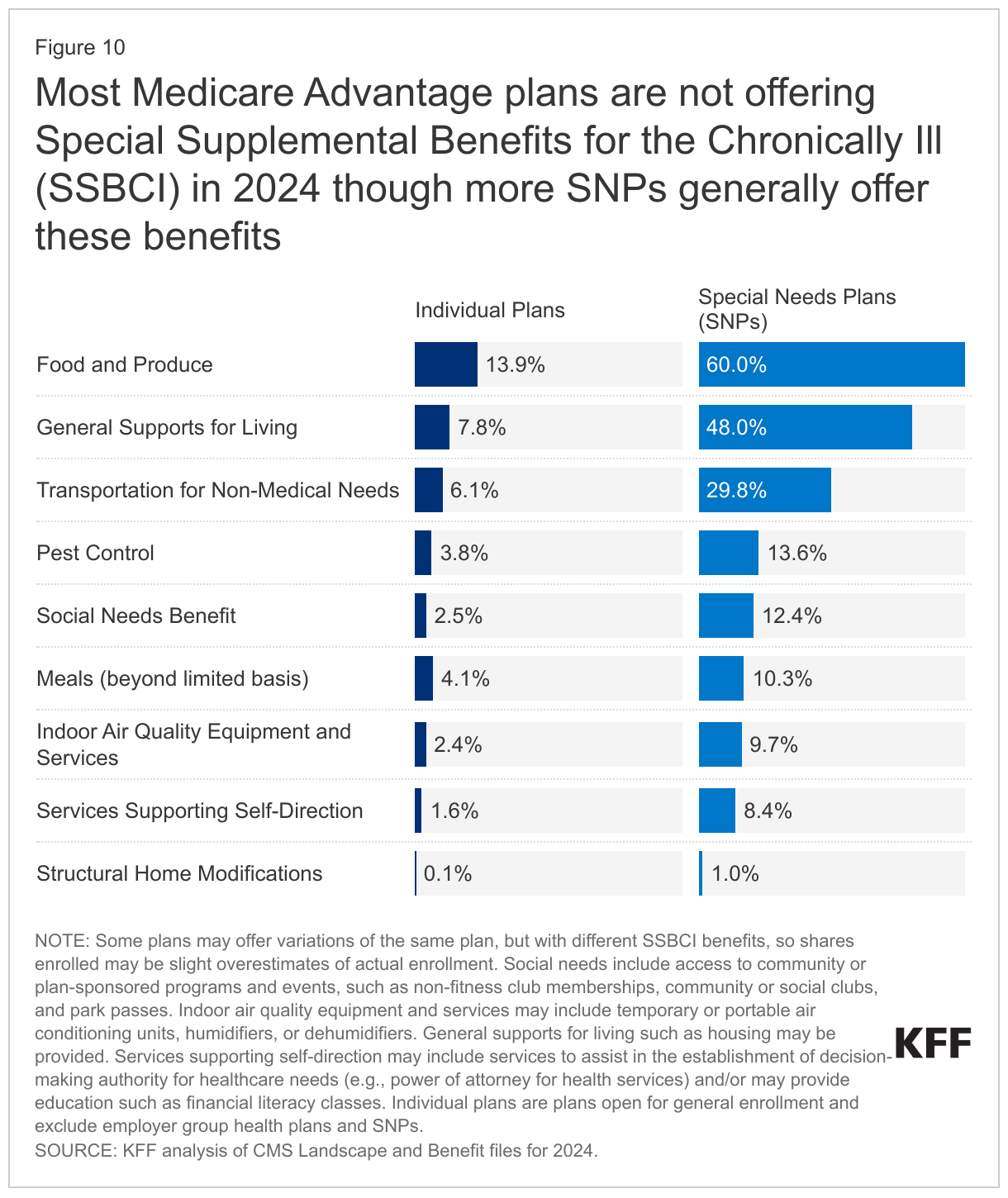

Availability of Special Supplemental Benefits for the Chronically Ill (SSBCI). Beginning in 2020, Medicare Advantage plans have also been able to offer extra benefits to a subset of a plan's enrollees, that are not primarily health related and are specifically for chronically ill beneficiaries, known as Special Supplemental Benefits for the Chronically Ill (SSBCI). Most individual and SNP Medicare Advantage plans still do not offer these benefits, though more SNP plans generally offer these benefits, particularly food and produce. SSBCI benefits offered in 2024 include food and produce (13.9% for individual plans and 60.0% for SNPs), general supports for living (e.g., housing, utilities) (7.8% in individual plans and 48.0% for SNPs), transportation for non-medical needs (6.1% for individual plans and 29.8% for SNPs), and pest control (3.8% for individual plans and 13.6% for SNPs) (Figure 10).

Discussion

The average Medicare beneficiary has a choice of 43 plans in 2024, the same as in 2023, offered by an average of 8 insurers, one less than in 2023. Medicare Advantage plans can be attractive to beneficiaries because they typically offer extra benefits, such as dental, vision and hearing, often for no additional premium, with the trade-off of more restrictive provider networks and greater use of cost management tools, such as prior authorization. The sheer number of plans presents both opportunities (to shop for better coverage) and challenges (to decipher potentially important differences across plans) although a minority of Medicare Advantage enrollees compare plans during the open enrollment period. Insurers have been drawn to the Medicare Advantage market because it is profitable relative to other health insurance markets, and this comes at a cost to Medicare, in that Medicare currently pays Medicare Advantage 106% of traditional Medicare costs, on average, according to MedPAC. As enrollment continues to climb, it will be increasingly important to assess how well Medicare Advantage is serving beneficiaries in terms of costs, quality, benefits and patient outcomes, as well as how well Medicare’s current payment methodology for Medicare Advantage is working to hold down beneficiary costs and Medicare spending.

Meredith Freed, Jeannie Fuglesten Biniek, and Tricia Neuman are with KFF. Anthony Damico is an independent consultant.

Methods

This analysis focuses on the Medicare Advantage marketplace in 2024 and trends over time. The analysis includes nearly 31 million enrollees in Medicare Advantage plans in 2023.

Data on Medicare Advantage plan availability, enrollment, and premiums were collected from a set of data files released by the Centers for Medicare & Medicaid Services (CMS):

- Medicare Advantage plan landscape files, released each fall prior to the annual enrollment period

- Medicare Advantage plan and premium files, released each fall

- Medicare Advantage plan crosswalk files, released each fall

- Medicare Advantage contract/plan/state/county level enrollment files, released on a monthly basis

- Medicare Advantage plan benefit package files, released quarterly

- Medicare Enrollment Dashboard files, released on a monthly basis

In previous years, KFF had calculated the share of Medicare beneficiaries enrolled in Medicare Advantage by including Medicare beneficiaries with either Part A and/or B coverage. We modified our approach in 2022 to estimate the share enrolled among beneficiaries eligible for Medicare Advantage who have both Medicare Part A and Medicare B. These changes are reflected in all data displayed trending back to 2010.

Additionally, in previous years, KFF had used the term Medicare Advantage to refer to Medicare Advantage plans as well as other types of private plans, including cost plans, PACE plans, and HCPPs. However, cost plans, PACE plans, HCPPs are excluded from this analysis in addition to MMPs. These exclusions are reflected in all data displayed trending back to 2010.

KFF’s plan counts may be lower than those reported by CMS and others because KFF uses overall plan counts and not plan segments. Segments generally permit a Medicare Advantage organization to offer the “same” local plan, but may vary supplemental benefits, premium and cost sharing in different service areas (generally non-overlapping counties).

Appendix