President Trump has said he will not cut Medicare benefits. At the same time, key figures within the administration, policymakers, and some conservative groups have previously expressed support for boosting the role of Medicare Advantage within the Medicare program, which could include changing the Medicare enrollment process, making Medicare Advantage the default enrollment option rather than traditional Medicare. Under current law, people who sign up for Medicare Parts A and B are automatically enrolled in traditional Medicare, unless they affirmatively choose to enroll in a Medicare Advantage plan. In contrast, under a Medicare Advantage default enrollment approach, unless Medicare beneficiaries make an affirmative choice to enroll in either traditional Medicare or a specific Medicare Advantage plan, they would be automatically enrolled into a Medicare Advantage plan, with the option to switch plans or enroll in traditional Medicare.

This brief considers how default enrollment into Medicare Advantage might work, potential challenges with this approach, and implications for beneficiaries, insurers, providers, agents and brokers, and the federal budget.

How would default enrollment into Medicare Advantage differ from the current enrollment process?

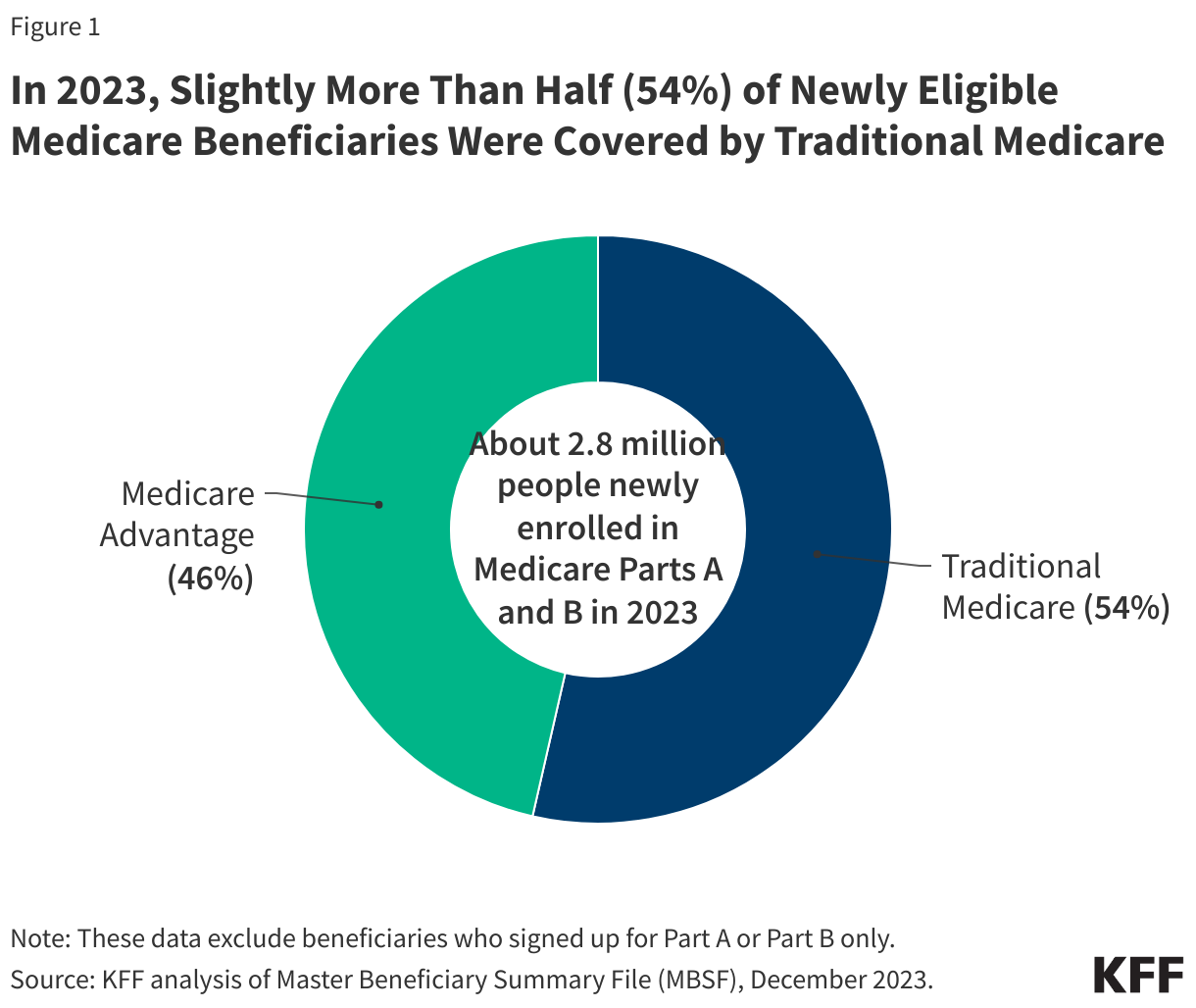

In general, when eligible people first enroll in Medicare during their Initial Enrollment Period (IEP), they can sign up for Medicare Part A and Part B. Once enrolled, new Medicare beneficiaries have the option to get their benefits under traditional Medicare or a private Medicare Advantage plan. New Medicare beneficiaries are automatically covered under traditional Medicare unless they choose to enroll in a Medicare Advantage plan in their area. In 2025, beneficiaries have a choice of 34 Medicare Advantage plans with prescription drug coverage, on average.

In 2023, about 2.8 million beneficiaries newly enrolled in Medicare, with slightly more than half (54%) or 1.5 million people covered by traditional Medicare and slightly less than half (46%) or 1.3 million enrolling in Medicare Advantage (Figure 1). For those covered by traditional Medicare when they newly enrolled in Medicare, it is possible that they made a change to their coverage and switched to a Medicare Advantage plan after their initial enrollment period. Defaulting individuals into a Medicare Advantage plan would be a change in the way most new Medicare beneficiaries get their coverage.

In contrast to the current approach, some have proposed to enroll newly eligible beneficiaries in Medicare Advantage by default, rather than traditional Medicare. Proposals vary in the level of detail, but in general, this process would involve assigning individuals to a specific Medicare Advantage plan based on certain criteria, such as patient-provider relationships or plan attributes, as discussed below.

Default options have been used across a variety of fields, including in the areas of retirement savings, organ donations, and electricity pricing programs. In these instances, defaulting people into certain programs with the option to opt out have shown to have a powerful effect on people’s choices, often resulting in a large share of people accepting the default option. In an analysis of default enrollment into Medicare Part D plans for certain low-income beneficiaries (as discussed in more detail below), the authors found that only 16% of individuals opted out of the plan they were randomly defaulted into and actively selected a new plan. The evidence on the impact of default enrollment on individual choices is one of the reasons proponents have put forward this approach for Medicare Advantage.

There are a number of questions about proposals to default beneficiaries into Medicare Advantage plans, along with tradeoffs, such as:

- What criteria would be used to assign new Medicare beneficiaries to a specific Medicare Advantage plan offered in their area, and how would the assignment to a private plan affect the continuity of care between patients and their doctors (due to provider networks), the ability of beneficiaries to access drugs prescribed by their doctors (due to variations in plan formularies) or timely access to services (due to prior authorization requirements)?

- Would the new system take into account special considerations such as whether the new Medicare beneficiary has a disability, is covered under both Medicare and Medicaid, or has a condition that requires access to specific medical providers or health care facilities within proximity to their home?

- What information would be provided to beneficiaries who are default enrolled into a Medicare Advantage plan about other Medicare coverage options that are available to them, including other Medicare Advantage plans or traditional Medicare and stand-alone Part D prescription drug plans in their area? How much time would beneficiaries be given to make a change before being locked in until the next annual open enrollment period?

- Will beneficiaries who wish to switch out of the Medicare Advantage plan in which they were enrolled and switch to traditional Medicare be provided a special enrollment period for Medigap, without pre-existing condition exclusions, if they choose to switch beyond the current 12-month “trial period” for people switching from Medicare Advantage to traditional Medicare regardless of the duration of their enrollment in Medicare Advantage?

- How would this approach impact insurers that offer Medicare Advantage plans? Would insurers have the option to opt out of the default enrollment system and continue to enroll new Medicare beneficiaries? What would be the impact on insurance brokers?

- What would be the impact of default Medicare Advantage enrollment on Medicare spending? While some claim this approach could achieve savings, the increase in Medicare Advantage enrollment that results from default enrollment would likely increase Medicare spending (and Part B premiums paid by all beneficiaries), without a change in current payment methodology. The Medicare Payment Advisory Commission (MedPAC) has consistently found that Medicare pays more for people enrolled in Medicare Advantage than for similar beneficiaries in traditional Medicare.

How would the government assign individuals to Medicare Advantage plans?

One of the main policy considerations for proposals that would default beneficiaries into specific Medicare Advantage plans is how the government would make this assignment. This is particularly challenging because plans vary across an array of features, including premiums, cost sharing for services, provider networks, drug coverage, plan quality (star ratings), extra benefits, and the frequency with which they impose prior authorization requirements and issue denials.

There are a number of different approaches that could be considered to implement default enrollment into Medicare Advantage:

- Random assignment. The government could randomly assign new Medicare beneficiaries to one of the plans offered in their area. This would ensure more even distribution of enrollment across plans, without benefiting one plan (or insurer) over another. However, random assignment would not take into account any plan features that might matter to individual beneficiaries, such as premiums, cost sharing, the scope of extra benefits, existing relationships with providers, drugs taken by the individual, or quality ratings.

- CMS currently uses random assignment for certain beneficiaries with LIS, a process which is intended to ensure a generally even distribution of beneficiaries among benchmark (premium-free) plans and to minimize selection bias for plans. However, this process does not match an individual’s prescription drugs with the list of drugs covered by plans, as opposed to a more targeted approach (“intelligent assignment” or “person-centered” assignment, which has been proposed by some advocates and policymakers) tries to align beneficiary needs with plan features. The possibility for greater discordance between an individual’s medical care needs and circumstances would likely arise with a random approach to default enrollment in Medicare Advantage plans, which would encompass more domains than just prescription drugs, such as continuity of coverage with primary care providers.

- Preserve existing relationships with physicians, specialists and other health care providers. Some proposals would assign patients to plans based on their relationship with a primary care provider or a specific specialist. Being able to see preferred providers in-network is one of the plan elements that is a top priority for beneficiaries. However, this process might not be able to take into account relationships with all providers and may not account for relationships with providers that are most consequential to beneficiaries (e.g., for some beneficiaries it might be their primary care physician while for others it might be a certain specialty care physician). If there are also only one or two insurers offering plans in a certain area, any existing provider relationships may not be able to be prioritized at all if providers are not in plan networks. This process would also require a way to identify relationships with providers for individuals who are not yet covered by Medicare, which could prove challenging.

- Challenges with preserving existing provider relationships for beneficiaries automatically assigned to plans were evident as part of the Financial Alignment Initiative (FAI) for beneficiaries enrolled in both Medicare and Medicaid. As part of this demonstration, states were required to try to assign enrollees to plans based on the individual’s most frequently utilized providers and medical facilities to best meet the individual’s current needs and circumstances. To do this, states could use the most recent 12 months of Medicare and Medicaid claims data, though this data was not always available. Beneficiaries automatically assigned to plans were able to opt-out, however, and there were high-opt out rates among beneficiaries, due to a number of factors, including enrollees being satisfied with existing care and not seeing the benefit of being in one of the demonstration plans and resistance from providers who refused to participate in the plan’s network and encouraged their patients not to participate. In California, for example, after the first evaluation of the demonstration, only about 50 percent of beneficiaries in the demonstration plans were able to retain their primary care providers, and those beneficiaries who were not able to maintain existing relationships with providers were more dissatisfied with the new plans. Similar issues could arise for Medicare Advantage default enrollment if the assignment process is not able to adequately match beneficiaries with their current providers.

- Zero-dollar premiums (other than the Part B premium). Some proposals would assign beneficiaries to plans with a zero-dollar premium. Using this approach would prioritize a plan parameter that is often cited as a top reason for selecting a Medicare Advantage plan, making it very meaningful to potential enrollees. There are a small share of beneficiaries who do not have access to a plan with a zero-dollar premium – about 325,000 people in 2025 – and in those situations, assignment could be based on the lowest premium available in the area. However, nearly all beneficiaries (99%) have access to a Medicare Advantage plan with drug coverage with no additional monthly premium. Depending on the area, this plan parameter may not be enough to differentiate among plans.

- Star ratings. Some proposals would base assignment on plan quality, placing Medicare beneficiaries in plans with star ratings of 4 or higher. According to CMS, 40% of Medicare Advantage plans with prescription drug coverage earned a star rating of 4 of higher for their 2025 rating, with 62% of Medicare Advantage enrollees currently in plans that will have stars of 4 or higher in 2025. Similar to zero-dollar premium plans, depending on the area, using the quality rating measure alone may not be enough to differentiate among plans. Further, MedPAC has recommended replacing the quality-bonus program which assigns stars because it asserts that this system does not provide a reliable indicator of quality, and Medicare focus groups have shown that few beneficiaries consider quality ratings when choosing a plan, so this approach alone may not adequately match enrollees with plans that meet their preferences.

- Drug coverage. Individuals could be assigned to plans based on the drugs they take and whether those drugs are on the plan formulary. While coverage of prescription drugs is an important part of plan selection, implementing this kind of approach could prove challenging since it would require, at a minimum, identifying the list of prescription drugs used by people not yet covered by Medicare and could result in assigning people to plans that cover some but not all of their medications.Challenges in implementing this kind of approach have been apparent in the case of the LIS random assignment process, which has been used since the program’s beginning in 2006. Advocates and policymakers have called for using intelligent assignment or beneficiary-centered assignment instead of the current LIS random assignment process to minimize potential disruptions in access to specific medications for beneficiaries who become eligible for LIS. This approach would take into account enrollees’ current prescriptions and pharmacies. CMS previously considered modifying the current assignment process for LIS enrollees but did not implement any changes.

- Preserve existing relationships with insurers. Assignment could be based on maintaining a relationship with an insurer based on the plan an individual was enrolled in before enrolling in Medicare. Medicare focus groups have shown that some beneficiaries choose their Medicare Advantage plan based on prior relationships with insurers because they feel comfortable with them. Continuing a plan with the same insurer could potentially preserve some relationships with providers or may be more likely to cover the drugs beneficiaries already take, but commercial plans may have different networks than Medicare plans, and provider networks change from year to year, as do formularies. It might also be difficult to identify insurance coverage for individuals prior to their enrolling in Medicare and in some areas, it may not be an option to continue coverage from a specific insurer if they do not sponsor Medicare Advantage plans.

- Lowest cost plan. Assignment could also be based on the “lowest cost plan” offered in an area. If a goal of default enrollment into Medicare Advantage is to save money for the Medicare program, assigning beneficiaries to plans with the lowest “bid” to provide Medicare Part A and B services at the lowest cost in a specific area may be a way to achieve this. It could also encourage competition among insurers to provide care most efficiently. However, it might also mean enrollees assigned to the lowest-bid plan in an area end up with a less generous set of supplemental benefits, a more narrow network of providers, face higher cost-sharing requirements, or are subject to more utilization review requirements, than other available plans if a plan is trying to cut costs to be the lowest cost option.

What are the implications for beneficiaries, insurers, providers, and agents and brokers?

Beneficiaries. Proponents of default enrollment into Medicare Advantage observe that this approach would provide more individuals with access to benefits beyond those covered by traditional Medicare, such as dental, vision, and hearing benefits, lower cost sharing and an out-of-pocket limit. Beneficiaries would have access to all Medicare-covered and extra benefits, without needing a separate Part D plan or separate supplemental policy, such as Medigap, and Medicare Advantage plans have potential to provide better coordinated care than traditional Medicare.

At the same time, people who are newly eligible for Medicare may not be aware of the differences between traditional Medicare and Medicare Advantage and might accept default enrollment into a Medicare Advantage plan without understanding the potential implications. For example, while Medicare Advantage potentially offers coverage at lower costs with extra benefits not available in traditional Medicare, there are tradeoffs with Medicare Advantage plans, including more limited provider networks compared to traditional Medicare as well as the potential for denials or delays in care related to the use of prior authorization in Medicare Advantage. Default enrollment could also result in more enrollees experiencing cost-related problems than would be encountered by beneficiaries with traditional Medicare and other types of supplemental coverage, such as Medigap. Furthermore, only a small share of Medicare beneficiaries compare plans, meaning that once enrolled in a plan, beneficiaries are unlikely to review their coverage options, potentially leaving them in a plan that does not best meet their individual needs and preferences.

There are also tradeoffs and complications involved with the process of defaulting beneficiaries into Medicare Advantage plans, though the effects would vary on key policy decisions, such as the criteria used by the government to assign beneficiaries to specific Medicare Advantage plans, as discussed above. For example, if beneficiaries are assigned to a plan that does not have one or more of their doctors in network, the assignment could disrupt existing patient-provider relationships, which could be a particular concern for patients with serious medical conditions. Default enrollment algorithms may also not take into account beneficiaries’ health care needs and preferences, such as specific drugs on a formulary.

Insurers. Depending on how a default enrollment approach was structured, it would have implications for insurers, which could result in the realignment of the market in ways that would benefit some insurers but be negative for others. For example, if the assignment process gave priority to a previous insurer relationship, such as through a former employer, this could favor certain insurers who also offer private commercial insurance and disadvantage insurers who have a smaller presence in commercial insurance markets. A previous insurer relationship could also benefit insurers who have a strong presence in both Medicaid and Medicare, as millions of people on Medicaid ultimately become eligible for Medicare. If assignment was prioritized on certain metrics, such as preserving existing provider relationships, quality or premiums, this could favor established insurers who are more dominant in certain areas, rather than smaller insurers and newer entrants to the Medicare Advantage market. Conversely, a random assignment process could be more equitable in terms of allocating beneficiaries to all types of insurers. Some consideration would need to be given to the distribution of new beneficiaries if some insurers offered more plans than others, which would increase their share of new enrollees. Overall, most of these approaches would likely have adverse effects on insurers that have historically relied more heavily on brokers and marketing to attract new enrollees when they first sign up for Medicare.

Providers and Health Systems. Providers are likely to be impacted by a change in default enrollment for newly eligible Medicare beneficiaries. Recent news reports have indicated that some providers and health systems have dropped certain Medicare Advantage plans from their networks or are no longer taking Medicare Advantage altogether, due to what they claim are burdensome prior authorization requirements, slow payments from plans, and denied claims. Some health systems have also questioned whether they can afford to have Medicare Advantage plans in their networks based on reimbursement from these plans. For example, a recent study found that Medicare Advantage plans reimburse rural hospitals at just 90.6% of traditional Medicare rates on a cost basis. Further expansion of Medicare Advantage enrollment under a default enrollment approach could exacerbate tensions between providers and Medicare Advantage plans, which could disrupt access to care for both current and new Medicare Advantage enrollees.

Agents and Brokers. About one in three Medicare Advantage enrollees rely on insurance agents and brokers to help them select their Medicare Advantage coverage. Agents are paid a commission for signing up Medicare beneficiaries to plans and also receive compensation if enrollees renew their plan. Currently, for beneficiaries who do not select a Medicare Advantage plan and are default enrolled into traditional Medicare, agents do not play a role in their Medicare Parts A or B coverage, though they may help them select Part D prescription drug coverage and a Medigap supplemental policy. If instead new Medicare beneficiaries largely relied on a default enrollment system that auto-assigned them to a Medicare Advantage plan, rather than using an agent or broker to help them choose a plan, this change could disrupt business practices and revenues for insurance agents and brokers.

What are potential implications for the federal budget?

In 2025, MedPAC found that Medicare pays 20% more for enrollees in Medicare Advantage than it would cost to cover them in traditional Medicare, a total of $84 billion dollars in additional spending in 2025 alone. In the absence of any changes to Medicare Advantage payment policy to reduce expenditures, a default enrollment approach into Medicare Advantage would likely increase annual Medicare spending above currently projected levels. One study on default enrollment into Medicare Advantage estimates that federal outlays could increase by $189 billion to $269 billion over 10 years under different scenarios. This higher spending would affect taxpayers and beneficiaries themselves. Already, Medicare Advantage spending increases Part B premiums for all enrollees, including those not on Medicare Advantage, at a cost of $13 billion in 2025. Higher spending on benefits, including under Part B, would increase the amount of government contributions and beneficiary premiums required to cover this part of the program, so Part B premiums would likely further increase under this approach.

How could default enrollment into Medicare Advantage be adopted?

The Trump administration could take different approaches to implement a Medicare Advantage default enrollment system, including testing a model for default enrollment through the Center for Medicare and Medicaid Innovation (CMMI or Innovation Center), using Section 402 demonstration authority, or pursuing legislation through Congress.

CMMI. One approach would be testing a model through CMMI. As part of CMMI’s statutory requirements, the goal of a model must be reducing program spending while preserving or enhancing the quality of care or improving quality of care without increasing spending. Under CMMI rules, the Secretary has the authority to waive Medicare and other program requirements in order to develop and conduct these models, and this authority is not limited to reimbursement or payment related changes (in contrast to the Secretary’s waiver authority for Section 402 demonstrations, as discussed below). The testing, evaluation and expansion of CMMI models are also specifically exempted from the Paperwork Reduction Act, and specific features of models are not subject to administrative or judicial review. Implementing a model through CMMI would not require Congressional approval.

Some important questions that may arise when designing this model include (1) how to design a model that does not increase spending; (2) whether the model would require mandatory or voluntary participation; (3) whether it would be tested in certain regions or nationwide, and (4) whether it would apply broadly or to defined subgroups of the Medicare population, such as beneficiaries with both Medicare and Medicaid coverage (dual-eligible individuals).

Section 402. Another approach would be using Section 402 demonstration authority, which provides broad authority to the HHS Secretary to develop and implement demonstration projects to test new Medicare payment methodologies, and allows the Secretary to waive compliance with certain Medicare requirements only as long as they relate “to reimbursement or payment on the basis of reasonable cost, or (in the case of physicians) on the basis of reasonable charge.” While budget neutrality is not specified in statute or regulation, according to CMS’ Medicare Waiver Demonstration Application, “Medicare-waiver-only demonstrations must be budget neutral. Budget neutrality means that the expected costs under the demonstration cannot be more than the expected costs were the demonstration not to occur.” Although most demonstrations have generally conformed to the administrative practice of budget neutrality, there have been exceptions. Section 402 demonstrations also have typically been subject to certain types of review such as requirements under the Paperwork Reduction Act and administrative or judicial review. Similar to a CMMI model, a Section 402 demonstration does not have to be initiated or approved by Congress.

Legislation. Policymakers could also enact legislation to modify current law to make Medicare Advantage the default enrollment option, rather than traditional Medicare. While there is bipartisan support for Medicare Advantage, some policymakers have raised concerns recently about specific elements of the program, such as the Medicare Advantage payment system, as well as the use of prior authorization, leading to denials and delays in care. Traditional Medicare also continues to serve a larger share of beneficiaries in rural areas than Medicare Advantage. These issues might dampen support for legislative changes to the current Medicare enrollment process.

This work was supported in part by Arnold Ventures. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.