Jared Ortaliza

Jared Ortaliza  Matt McGough

Matt McGough  Cynthia Cox

Cynthia Cox On March 23, 2010, President Obama signed the Affordable Care Act (ACA) into law, marking a significant overhaul of the U.S. health care system. Prior to the ACA, high rates of uninsurance were prevalent due to unaffordability and exclusions based on preexisting conditions. Additionally, some insured people faced extremely high out-of-pocket (OOP) costs and coverage limits. The ACA aimed to address these issues, though it did not eliminate all of them.

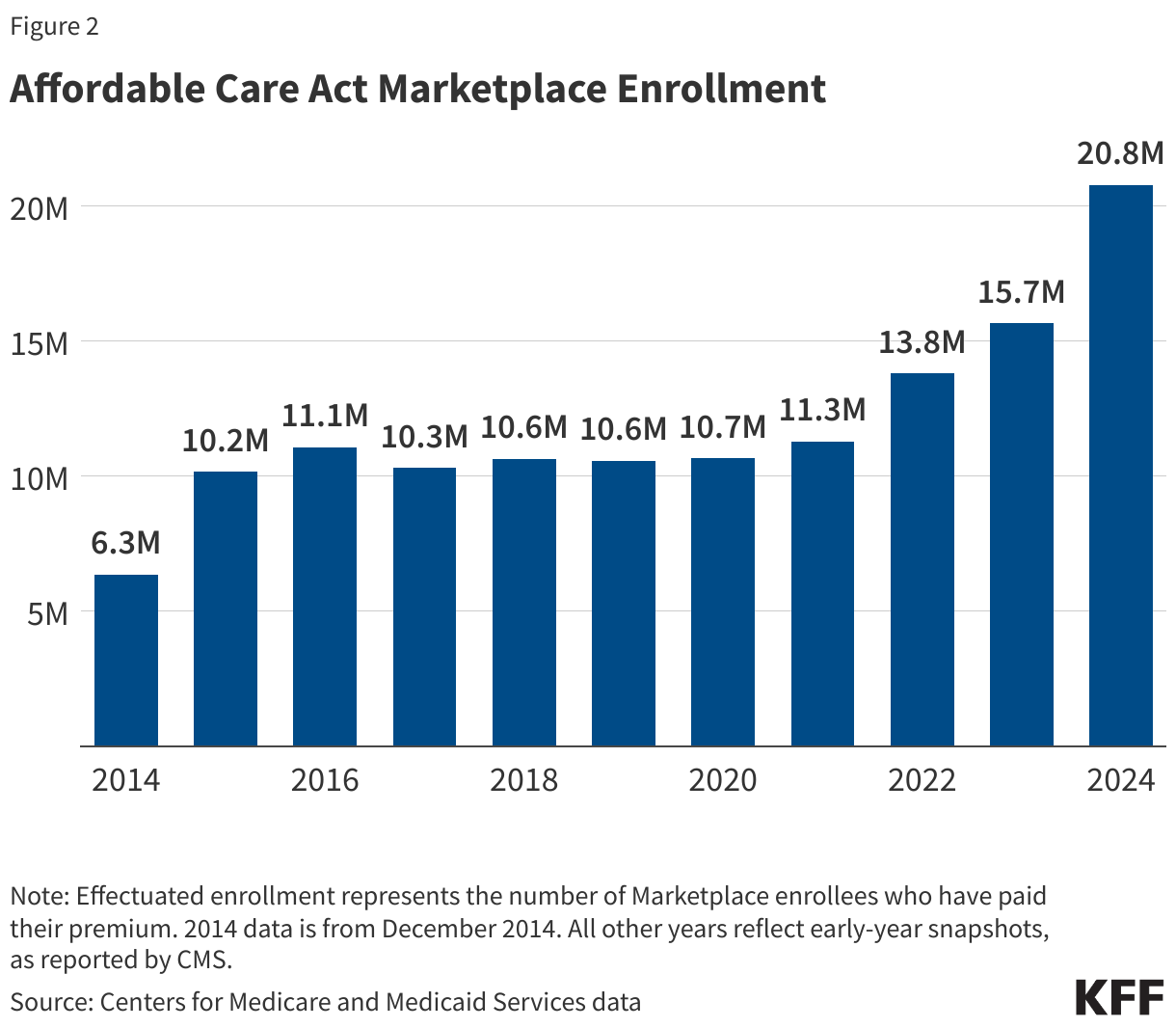

The ACA affects virtually all aspects of the health system, including insurers, providers, state governments, employers, taxpayers, and consumers. The law built on the existing health insurance system, making changes to Medicare, Medicaid, and employer-sponsored coverage. A fundamental change was the introduction of regulated health insurance exchange markets, or Marketplaces, which offer financial assistance for ACA-compliant coverage to those without traditional insurance sources. This chapter has a special focus on these Marketplaces that are integral to the ACA’s framework.