Explaining Health Care Reform: Questions About Health Insurance Subsidies

Health insurance is expensive and can be difficult to afford for people with lower or moderate incomes. In response, the Affordable Care Act (ACA) provides sliding-scale subsidies that lower premiums and insurers offer plans with reduced out-of-pocket (OOP) costs for eligible individuals.

This brief provides an overview of the financial assistance provided under the ACA for people purchasing coverage on their own through health insurance Marketplaces (also called exchanges).

Health Insurance Marketplace Subsidies

There are two types of financial assistance available to Marketplace enrollees. The first type, called the premium tax credit, reduces enrollees’ monthly payments for insurance coverage. The second type of financial assistance, the cost sharing reduction (CSR), reduces enrollees’ deductibles and other out-of-pocket costs when they go to the doctor or have a hospital stay. To receive either type of financial assistance, qualifying individuals and families must enroll in a plan offered through a health insurance Marketplace.

Premium Tax Credit

Premium tax credits can be applied to Marketplace plans in any of four “metal” levels of coverage: bronze, silver, gold, and platinum. Bronze plans tend to have the lowest premiums but have the highest deductibles and other cost sharing, leaving the enrollee to pay more out-of-pocket when they receive covered health care services, while platinum plans have the highest premiums but very low out-of-pocket costs.

Also offered on the Marketplace are catastrophic health plans with even lower premiums and higher cost sharing compared to bronze plans. Catastrophic plans are generally only available to individuals younger than 30, and premium tax credits cannot be applied to these plans.

Who is eligible for the premium tax credit?

To receive a premium tax credit for 2025 coverage, a Marketplace enrollee must meet the following criteria:

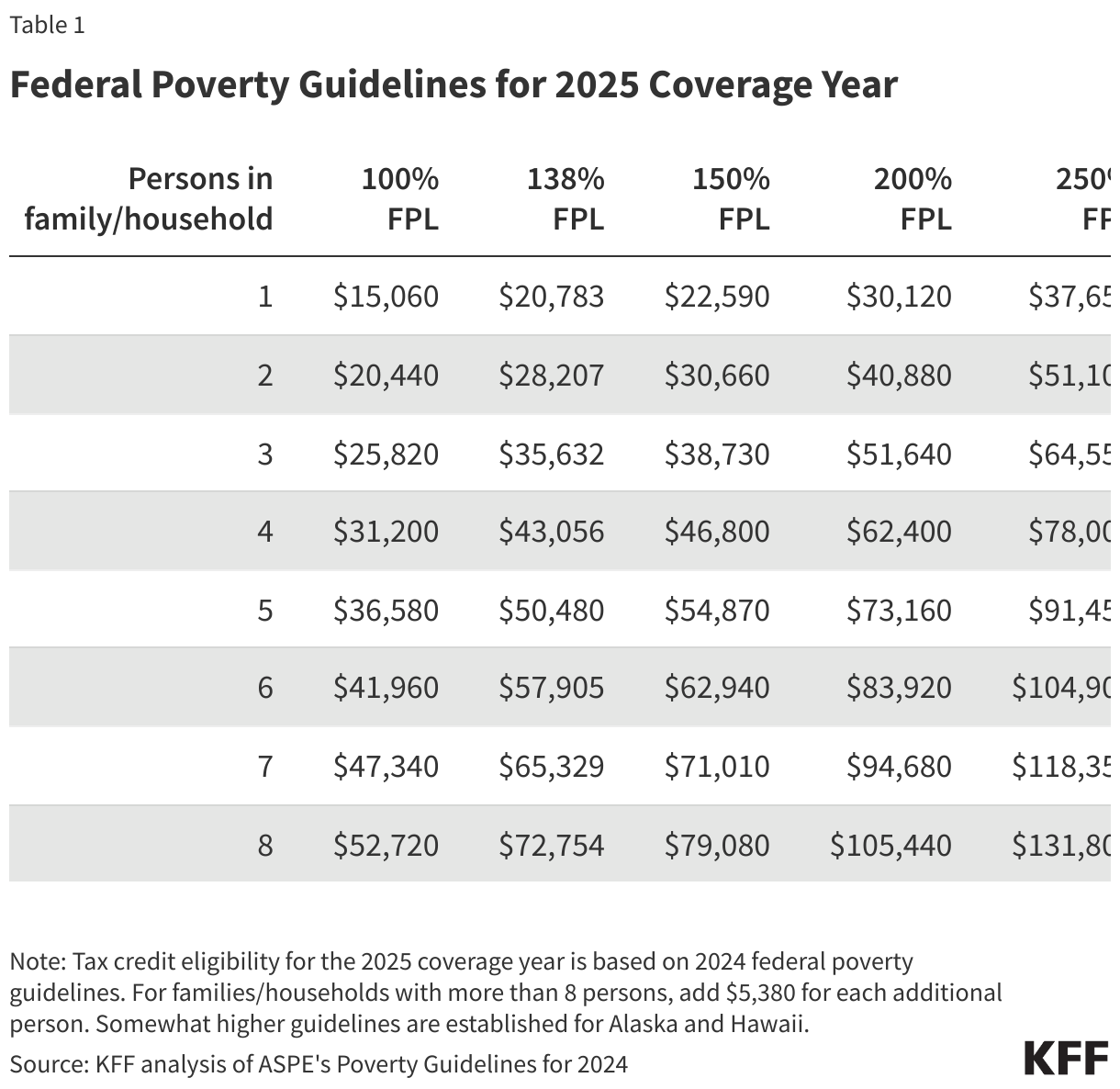

- Have a household income at least equal to the Federal Poverty Level (FPL), which for the 2025 benefit year will be determined based on 2024 poverty guidelines (Table 1).

- Not have access to an employer plan (including a family member’s employer) that both meets minimum value and is considered affordable. For 2025, the threshold that determines if an employer plan is affordable is if the premium is equal to or less than 9.02 percent of one’s household income.

- Not be eligible for coverage through Medicare, Medicaid, or the Children’s Health Insurance Program (CHIP).

- Have U.S. citizenship or proof of legal residency. (Lawfully present immigrants whose household income is below 100 percent FPL can also be eligible for tax subsidies through the Marketplace if they meet all other eligibility requirements.)

- If married, must file taxes jointly.

Income: For the purposes of the premium tax credit, household income is defined as the Modified Adjusted Gross Income (MAGI) of the taxpayer, spouse, and dependents who are required to file a tax return. The MAGI calculation includes income sources such as wages, salary, foreign income, interest, dividends, and Social Security.

Employer coverage: Employer coverage is considered affordable if the required premium contribution is no more than 9.02 percent of household income in 2025. The Marketplace will look at both the required employee contribution for self-only and (if applicable) for family coverage. If the required employee contribution for self-only coverage is affordable, but the required employee contribution is more than 9.02 percent of household income for family coverage, the dependents can purchase subsidized exchange coverage while the employee stays on employer coverage.

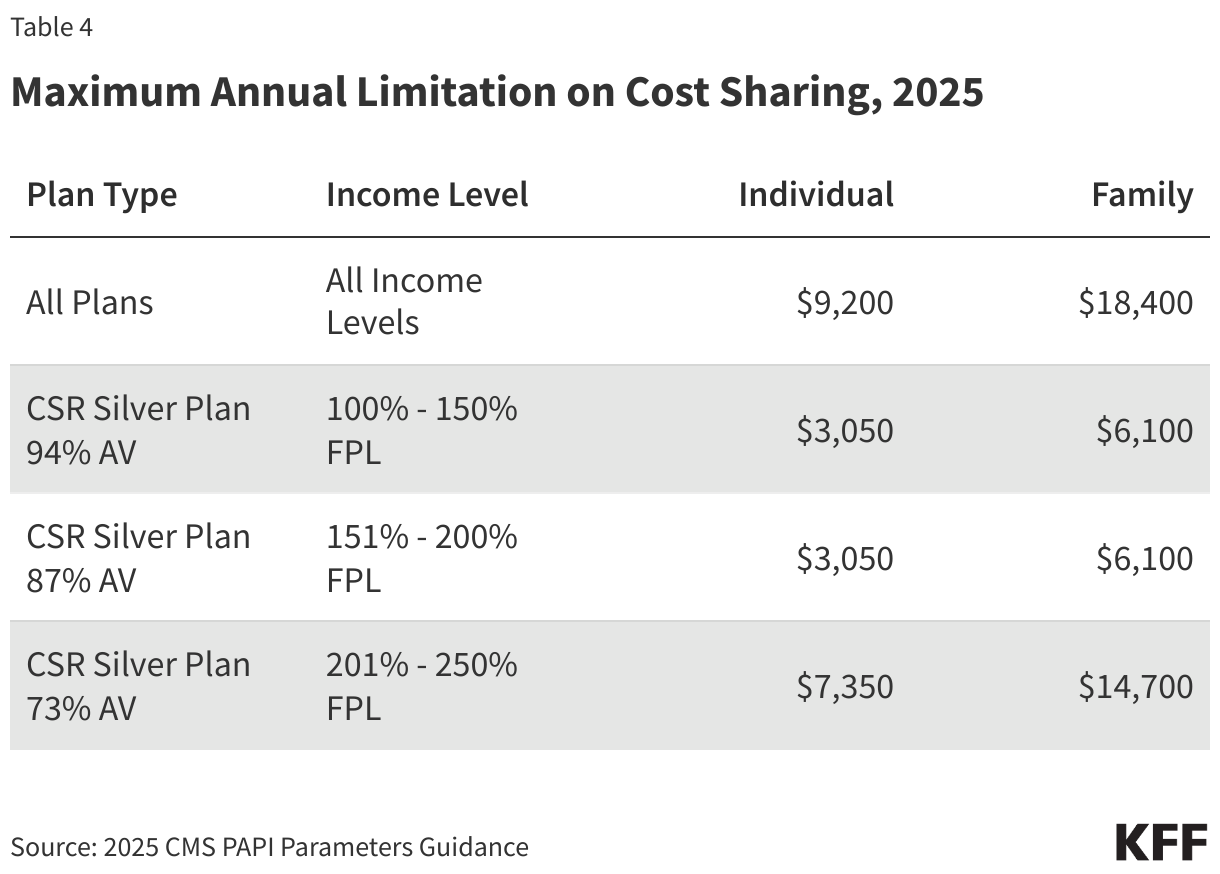

The employer’s coverage must also meet a minimum value standard that requires the plan to provide substantial coverage for physician services and for inpatient hospital care with an actuarial value of at least 60 percent (meaning the plan pays for an average of at least 60 percent of all enrollees’ combined health spending, similar to a bronze plan). The plan must also have an annual OOP limit on cost sharing of no more than $9,200 for self-only coverage and $18,400 for family coverage in 2025.

People who are offered employer-sponsored coverage that fails to meet either the affordability threshold or minimum value requirements can qualify for Marketplace subsidies if they meet the other criteria listed above.

Eligibility for Medicaid: In states that have expanded Medicaid under the ACA, adults earning up to 138 percent FPL are generally eligible for Medicaid and not for Marketplace subsidies. In states that have not adopted Medicaid expansion, adults with income as low as 100 percent FPL can qualify for Marketplace subsidies. However, those with incomes lower than 100 percent FPL are generally not eligible for tax credits or Medicaid unless they meet other state eligibility criteria. KFF estimates that 1.5 million Americans living in non-expansion states fall into this coverage gap.

Certain lawfully present immigrants are exempt from the rule restricting tax credit eligibility for adults below the poverty level. Other federal rules restrict Medicaid eligibility for lawfully present immigrants, other than pregnant women, refugees, and asylees, until they have resided in the U.S. for at least five years. Immigrants who would otherwise be eligible for Medicaid but have not yet completed their five-year waiting period may instead qualify for tax credits through the Marketplace. If an individual in this circumstance has an income below 100 percent of poverty, for the purposes of tax credit eligibility, his or her income will be treated as though it is equal to the poverty level. Exceptions are also made for Deferred Action for Childhood Arrivals (DACA) recipients, who became newly eligible for Marketplace coverage after the Biden-Harris administration passed new regulations in May 2024 expanding the definition of lawfully present to include DACA recipients. Immigrants who are not lawfully present are ineligible to enroll in health insurance through the Marketplace, receive tax credits through the Marketplaces, or enroll in non-emergency Medicaid and CHIP.

What amount of premium tax credit is available?

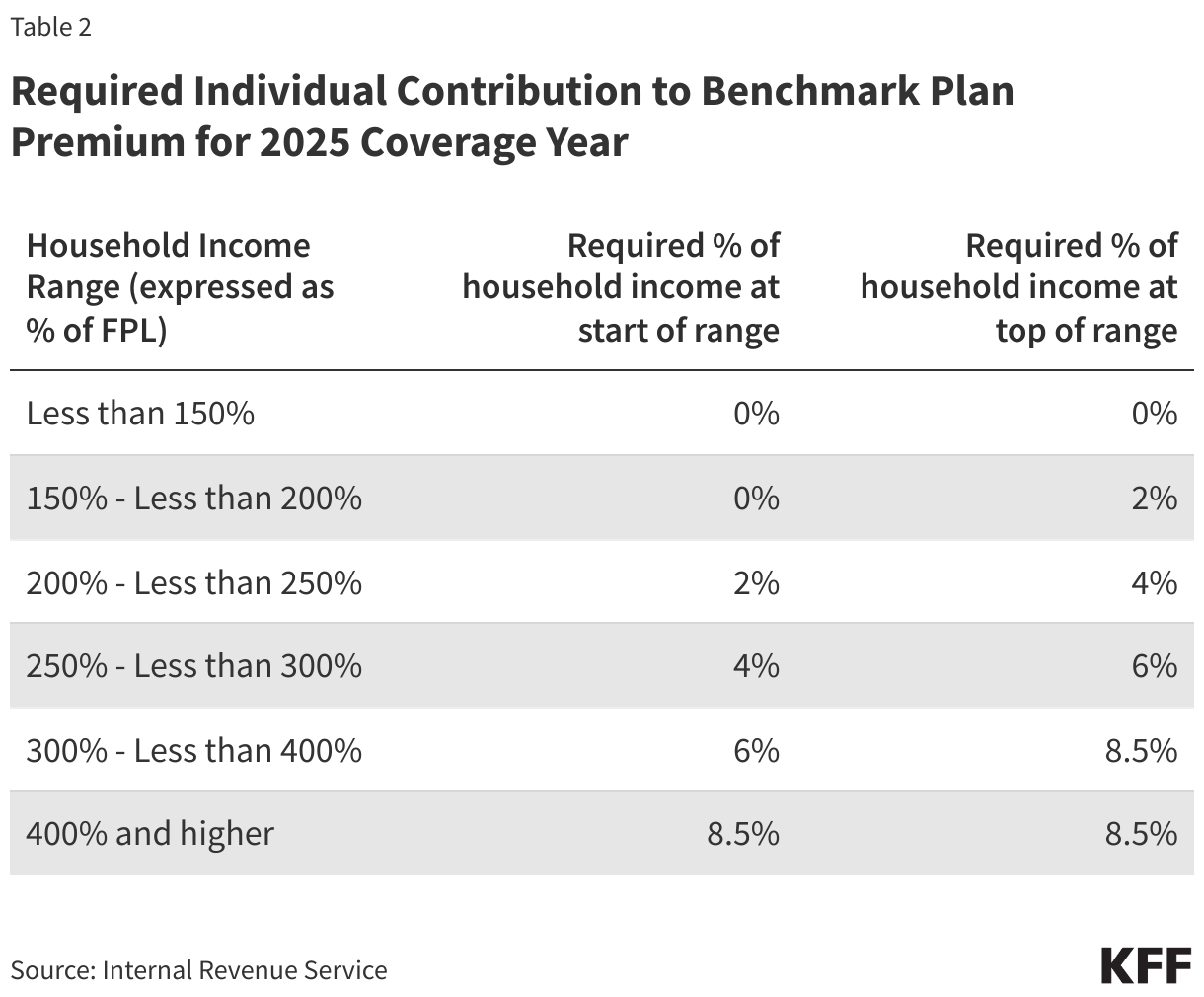

The premium tax credit limits an individual’s contribution toward the premium of the “benchmark” plan, the second-lowest cost silver plan in their Marketplace. This “required individual contribution” is set on a sliding income scale. In 2025, for individuals with income up to 150 percent FPL, the required contribution is zero, while at an income of 400 percent FPL or above, the required contribution is 8.5 percent of household income (Table 2). Individuals making above 400 percent FPL whose required contribution for a benchmark silver premium is greater than the actual cost of a benchmark silver plan relative to their household income would be ineligible for subsidies.

These contribution amounts were set by the American Rescue Plan Act (ARPA) and later temporarily extended by the Inflation Reduction Act (IRA). Prior to the ARPA, the required contribution percentages ranged from about two percent of household income for people with poverty level income to nearly 10 percent of household income for people with income from 300 to 400 percent FPL. In addition, prior to the ARPA, people with incomes above 400 percent FPL were not eligible for premium tax credits.

The amount of tax credit is calculated by subtracting the individual’s required contribution from the actual cost of the “benchmark” plan. So, for example, if the benchmark plan costs $6,000 annually, the required contribution for someone with an income of 150 percent FPL ($22,590 in 2025) is zero, resulting in an annual premium tax credit of $6,000. If that same person’s income equals 250 percent FPL (or $37,650 in 2025), the individual contribution is four percent of $37,650, or $1,506 per year, resulting in an annual premium tax credit of $4,494.

The premium tax credit can then be applied toward any other plan sold through the Marketplace (except Catastrophic coverage). The amount of the tax credit remains the same, so a person who chooses to purchase a plan that is more expensive than the benchmark plan will have to pay the difference in cost. Conversely, if a person chooses a less expensive plan, such as the lowest-cost silver plan or a bronze plan, the tax credit will cover a greater share of that plan’s premium, and possibly even cover the entire cost, leaving the consumer with a zero-premium plan. When the tax credit exceeds the cost of a plan, it lowers the premium to zero and any remaining tax credit amount is unused.

For certain components of a Marketplace plan premium, the premium tax credit will not apply. First, the tax credit cannot be applied to the portion of a person’s premium attributable to covered benefits that are not essential health benefits (EHB). For example, a plan may offer adult dental benefits, which are not currently included in the definition of EHB. In that case, the person would have to pay the portion of the premium attributable to adult dental benefits without financial assistance. In addition, the ACA prohibits applying premium tax credits to the portion of premiums covering “non-Hyde” abortion benefits. Marketplace plans that cover abortion are required to charge a separate $1 monthly premium to cover the cost of this benefit; this means a consumer who is otherwise eligible for a fully subsidized, zero-premium policy would still need to pay $1 per month for a policy that covers abortion benefits. Finally, if the person smokes cigarettes and is charged a higher premium for smoking, the premium tax credit is not applied to the portion of the premium that is the tobacco surcharge.

How do people receive the premium tax credit?

To receive the premium tax credit, people must apply for coverage through the Marketplace and provide information about their age, address, household size, citizenship status, and estimated income for the coming year. After submitting the application, people will receive a determination letting them know the amount of premium tax credit for which they qualify. The consumer then has the option to have the tax credit paid in advance, claim it later when they file their tax return, or some combination of the two options.

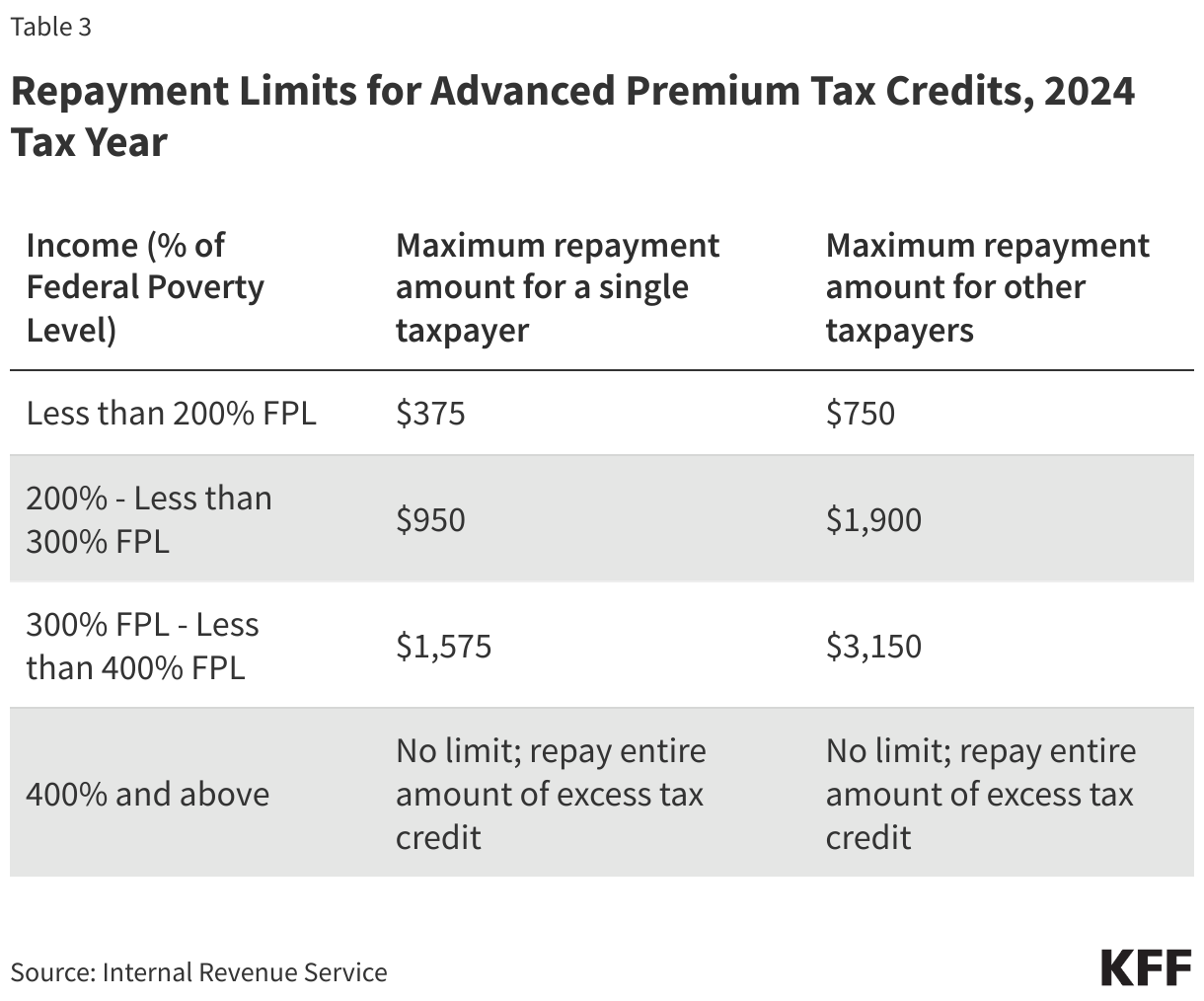

The advanced premium tax credit (APTC) option allows consumers to have 1/12 of their tax credit paid directly to their Marketplace plan insurer each month, reducing the monthly amount the consumer owes. However, because the APTC eligibility determination is based on estimated income, the enrollee is required to reconcile their APTC at tax time the following year, once they know what their actual income was. For people receiving an advanced payment of the premium tax credit in 2025, the reconciliation would occur when they file their 2025 tax return in 2026. If the consumer overestimated their income when they applied, they can receive the unclaimed premium tax credit as a refundable tax credit when they file. If the consumer underestimated their income at the time of application and excess APTC was paid on their behalf during the year, they would have to repay some or all of the excess tax credit when they file. There are maximum repayment limits which vary depending on income, shown in Table 3.

Alternatively, people can opt to pay their entire premium costs each month and wait to receive their tax credit until they file their annual income tax return the following year, although most Marketplace participants cannot afford this option. The premium tax credit is refundable, meaning it is available to qualifying enrollees regardless of whether they otherwise owe any federal income tax. Everyone who receives an APTC in a tax year is required to file a tax return for that year in order to continue receiving financial assistance in the future. People who fail to file and reconcile for two consecutive years will be ineligible for premium tax credits the following year.

Cost Sharing Reduction

The second form of financial assistance available to Marketplace enrollees is a cost sharing reduction. Cost sharing reductions lower enrollees’ out-of-pocket cost due to deductibles, copayments, and coinsurance when they use covered health care services.

Who is eligible for the cost sharing reduction?

People eligible for premium tax credits and have household incomes between 100 to 250 percent of poverty are eligible for cost sharing reductions.

How are cost sharing reductions provided?

Unlike the premium tax credit (which can be applied toward any metal level of coverage), cost sharing reductions (CSR) are only offered through silver plans. For eligible individuals, cost sharing reductions are applied to a silver plan, essentially making deductibles and other cost sharing under that plan more similar to that under a gold or platinum plan. Individuals with income between 100 and 250 percent FPL can continue to apply their premium tax credit to any metal level plan, but they can only receive plans with reduced cost sharing if they pick a silver-level plan.

What amount of cost sharing reductions are available to people?

Cost sharing reductions are determined on a sliding scale based on income. The most generous cost sharing reductions are available for people with income between 100 and 150 percent FPL. For these enrollees, silver plans that otherwise typically have higher cost sharing are modified to be more similar to a platinum plan by substantially reducing the silver plan deductibles, copays, and other cost sharing. For example, in 2024, the average annual deductible under a silver plan was just over $5,000, while the average annual deductible under a platinum plan was $97. Silver plans with the most generous level of cost sharing reductions are sometimes called CSR 94 silver plans (with 94 percent actuarial value, which represents the average share of health spending paid by the health plan, compared to 70 percent actuarial value for a silver plan with no cost sharing reductions).

Somewhat less generous cost sharing reductions are available for people with incomes above 150 and up to 200 percent FPL. These reduce cost sharing under silver plans to 87 percent actuarial value (CSR 87 plans). In 2024, the average annual deductible under a CSR 87 silver plan was about $700.

For people with incomes above 200 and up to 250 percent FPL, cost sharing reductions are available to modestly reduce deductibles and copays to 73 percent actuarial value (sometimes called CSR 73 plans). In 2024, the average annual deductible under a CSR 73 silver plan was about $4,500.

Insurers have flexibility in how they set deductibles and copays to achieve actuarial value benchmarks set by the ACA for Marketplace plans, including CSR plans, so actual deductibles may vary from these averages.

The ACA also requires maximum annual out-of-pocket spending limits on cost sharing under Marketplace plans, with reduced limits for CSR plans. In 2025, the maximum OOP limit will be $9,200 ($18,400 family) for all QHPs with lower maximum OOP limits permitted under cost sharing reduction plans (Table 4).