What to Watch in the 2024 ACA Open Enrollment

With the start of the 2024 Affordable Care Act open enrollment, the Marketplaces have been operating for a full decade and are heading into their eleventh year. This year’s open enrollment season will last from November 1, 2023 to January 16, 2024 in most states and longer in some state-based marketplaces. (Due to the federal holiday on January 15, state marketplaces are allowed to extend the deadline for Open Enrollment to January 16.) Even after a decade of operation, there continue to be changes in these markets. Here’s what to watch in 2024:

- Unsubsidized premiums in the ACA Marketplaces are rising due in part to inflation. Premiums are rising by an average of 5% in 2024 for the second-lowest cost silver plan (the benchmark against which subsidies are calculated). Premiums for the lowest cost bronze plans (the least expensive plans on the Marketplaces) are similarly rising 6%. (State-level data are available here). An earlier KFF analysis of premium rate filings found the primary drivers of premium growth heading into 2024 are rising prices paid to health care providers, driven in part by inflation in the rest of the economy, and a rebound in utilization coming out of the pandemic. However, other factors like the reduced use of COVID-related care are having a downward effect on premiums. Although unsubsidized premiums are rising, the Inflation Reduction Act’s temporary enhancement of subsidies continues to make the vast majority of Marketplace shoppers eligible for financial help with the cost of coverage. These subsidies cap how much enrollees must spend on a benchmark silver plan premium as a share of their household income, meaning that most enrollees will be sheltered from the increases in the sticker price of the premium.

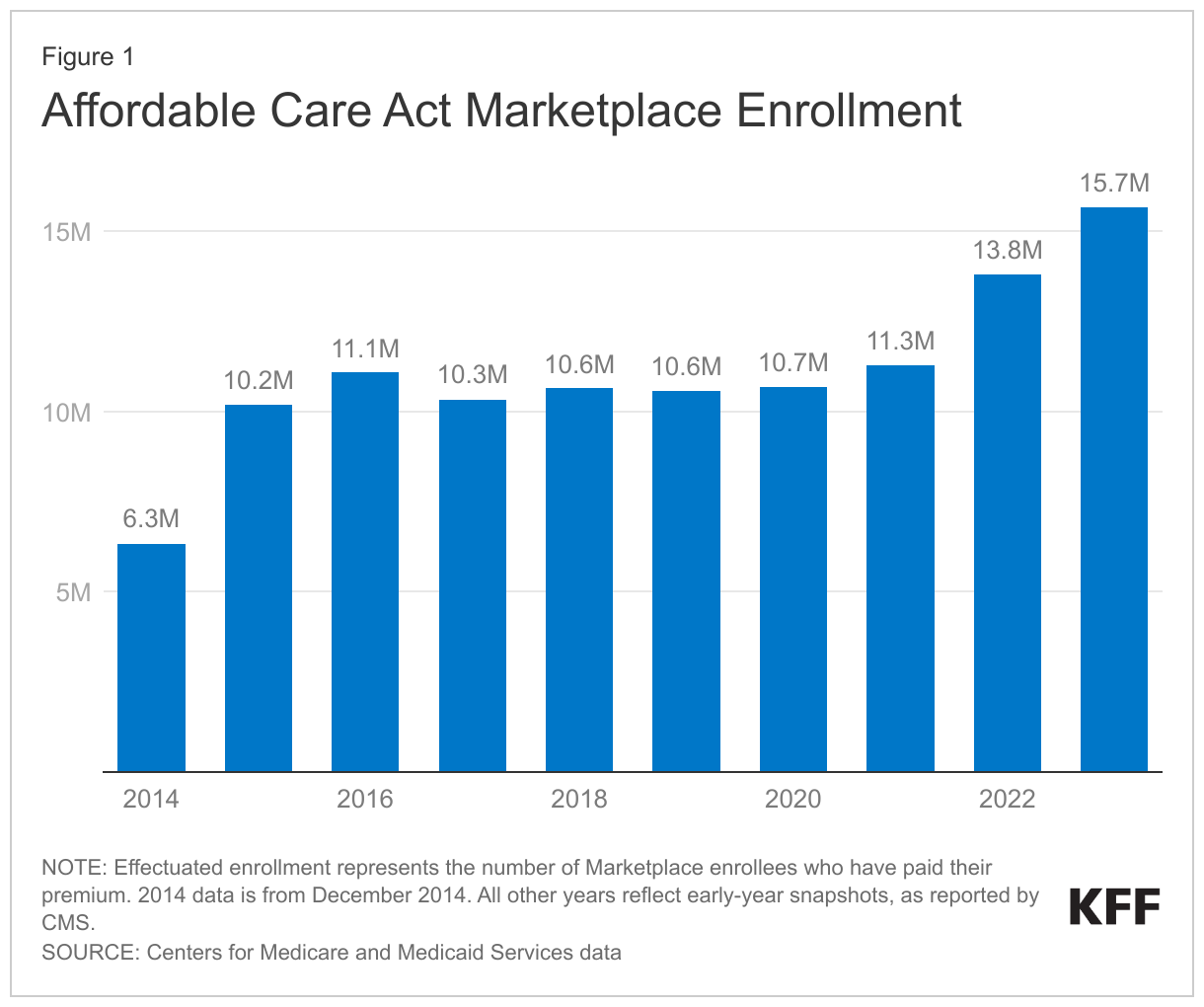

- 2024 could be another record-setting year for enrollment. The number of people who enrolled in Marketplace coverage earlier this year reached 15.7 million, surpassing prior record-setting years in 2021 and 2022. During the pandemic, state Medicaid programs suspended annual renewal requirements for Medicaid and kept everyone continuously enrolled. Now, states are resuming renewal requirements and will end Medicaid coverage if people are no longer eligible or if they do not complete renewal forms (sometimes called “procedural reasons”). So far this year, more than 9.5 million adults and children have been disenrolled from Medicaid and CHIP, mostly due to procedural reasons, and millions more will likely be disenrolled in the coming months. Some may find themselves eligible for Marketplace subsidies, further boosting enrollment in the coming year, though there may be challenges in ensuring people losing Medicaid are aware of their options for coverage through the Marketplaces.

- Insurer participation in 2024 will be more robust than in recent years. There are more insurers entering new markets than there are plans exiting from the Marketplace. Notably, Oscar Health is withdrawing from the California individual insurance market after profits fell short of expectations. Cigna is also exiting from Kansas’s and Missouri’s markets. At the same time, other insurers are entering several states, such as California, Colorado, Delaware, Indiana, Maryland, Nevada, New Jersey, New Mexico, Oklahoma, Pennsylvania, South Carolina, Utah and Wisconsin.

- State-level policy changes will affect what coverage some residents are eligible for, how much it costs, and how they sign up. For example, Virginia plans to start using its own enrollment platform with the 2024 open enrollment cycle, rather than relying on the federal Healthcare.gov platform. California will begin offering additional cost-sharing reduction subsidies that eliminate deductibles and lower other out-of-pocket expenses for about 4 in 10 Covered California enrollees. Massachusetts is increasing the income limit for additional state subsidies. Washington is allowing undocumented immigrants to enroll in Marketplace plans with state income-based subsidies starting in 2024. And North Carolina will expand Medicaid starting December 1, 2023, to residents with incomes up to 138% of the poverty level. Some low-income people enrolled in Marketplace plans in North Carolina will move to Medicaid.

- A new auto-reenrollment policy on Healthcare.gov will save some consumers money on their deductibles. People who are enrolled in Marketplace plans now and who do not act during Open Enrollment to renew or change their coverage will, in many cases, be automatically reenrolled by the Marketplace on December 16 so coverage will continue in 2024. In the past, people were usually automatically re-enrolled in the same plan. This year, the federal Marketplace (healthcare.gov) will first check to see if people currently enrolled in bronze plans have income at or below 250% of the federal poverty level, which would make them eligible for a cost-sharing reduction, or CSR, plan. If these individuals do not act by December 15 to select another plan or renew their bronze plan coverage for 2024, the Marketplace will automatically re-enroll them in a silver level plan offered by the same insurer and with the same provider network if the premium for that silver plan (taking into account APTC) will be the same or lower than their bronze plan. Deductibles and other cost sharing in silver CSR plans are much lower than in bronze plans. Those who are automatically re-enrolled in this way but want to select a different plan will still have until the end of Open Enrollment (January 15, 2024) to make a change.

- Marketplace shoppers will have extra time to submit proof of income. Marketplaces automatically check trusted data sources (such as the IRS and Social Security) to verify the income of enrollees. If the Marketplace cannot verify the income on a given application, the applicant may be asked to submit more documentation. Until this year, the Marketplace has given people 90 days to submit requested documentation, but regulators noticed many people were missing this deadline. Starting this fall, Marketplace shoppers will be given an automatic 60-day extension (for a total of 150 days) to submit documentation of their income. This change applies to all Marketplaces, including those run by states. Coverage will continue during this period, but financial assistance may be reduced or terminated if the requested documentation is not received by the deadline.

- Young adults turning 26 in 2024 will have until the next open enrollment to move off of their parents’ Marketplace plans. Private health plans must permit young adults the option of remaining covered as a dependent under their parent’s policy until they turn age 26. Starting in 2024, though, federal Marketplace health plans will officially not be allowed to terminate coverage for young adult dependents mid-year on their 26th birthday. Instead, they will have to continue the dependent coverage through the end of the calendar year. The federal Marketplace has already been keeping these individuals on the plan until the end of the year, and then automatically enrolling them in their own exchange coverage the following year, but this rule codifies that practice.

- Some people will have a chance to sign up or change plans outside of the open enrollment window. In states that use Healthcare.gov, the federal government is making changes to some special enrollment periods (SEPs) that allow certain people to sign up for coverage outside of the Open Enrollment period. Generally, state-based marketplaces can also offer these and other SEPs but don’t have to. These special enrollment periods differ depending on the qualifying reason:

Medicaid disenrollment: Under a new, temporary “Medicaid Unwinding Special Enrollment Period” people losing Medicaid between March 31, 2023 and July 31, 2024 can apply to the Marketplace, check the box attesting to the fact that they lost Medicaid or CHIP, and select a new plan within 60 days of applying for Marketplace coverage. In the long-run an additional, permanent change was made to extend the amount of time people disenrolled from Medicaid have to sign up for Marketplace coverage, from 60 days following loss of Medicaid to at least 90 days. In addition, like last year, people with low incomes will still be able to sign up for Marketplace coverage or change plans throughout the year. This “low-income special enrollment period (SEP)” is available to people in HealthCare.gov states who are eligible for premium tax credits and whose 2024 income will be no more than 150% of the federal poverty level ($21,870 for a single person, $37,290 for a family of 3). Coverage will begin the first day of the following month.

Natural disasters: People recently affected by natural disasters, such as the Maui wildfires, are eligible for an exceptional circumstances SEP that will give them more time to apply for Marketplace coverage. To be eligible they must live in or have moved away from an area designated by the Federal Emergency Management Association (FEMA) as eligible for individual or public assistance.

Loss of other coverage SEP: People who lose other coverage, such as job-based plans or Medicaid, are eligible for a special enrollment period to join the Marketplace, and people who anticipate loss of other coverage are eligible to apply for Marketplace coverage up to 60 days in advance of the date current coverage will end. In the past, when people applied for this coverage loss SEP in advance, new marketplace coverage would take effect on the first day of the month after current coverage ends. However, sometimes, current coverage ends in the middle of a month, leaving a gap in coverage of several days or weeks. Starting in 2024, to avoid this gap in coverage, people applying in advance for the coverage loss SEP can ask to have marketplace coverage take effect on the first day of the month that current coverage ends.

Pandemic: During the Public Health Emergency (PHE), every county in the USA had a FEMA designation that made people eligible for the exceptional circumstances SEP due to COVID. However, since the PHE has ended, this COVID SEP is no longer available.

- Tax credit recipients must again file tax returns to maintain eligibility for subsidies. It has long been the case that people who receive advanced premium tax credits (APTC) in a year must file their federal tax return the following spring in order to continue receiving an APTC. This “file and reconcile” requirement was temporarily waived during the pandemic, but it is back in force with a change. Now people who fail to file and reconcile for two consecutive years will be ineligible for APTC the following year.