How the Pandemic Continues to Shape Medicaid Priorities: Results from an Annual Medicaid Budget Survey for State Fiscal Years 2022 and 2023

Overview

This annual Medicaid budget survey report highlights certain policies in place in state Medicaid programs in state fiscal year (FY) 2022 and policy changes implemented or planned for FY 2023. The findings are drawn from the 22nd annual budget survey of Medicaid officials conducted by the Kaiser Family Foundation (KFF) and Health Management Associates (HMA), in collaboration with the National Association of Medicaid Directors (NAMD).

Medicaid budget survey reports from prior years are available in our archives.

NEWS RELEASE

- A news release announcing the publication of the 2022 Medicaid Budget Survey is available.

EXECUTIVE SUMMARY

- The Executive Summary provides an overview of the 2022 survey results and is available under the Executive Summary.

FULL REPORT

- The complete 2022 Medicaid Budget Survey Report is available under the Report. The Report contains 8 separate sections. Users can view each section separately or download a full Report PDF from the right side of the page.

SPENDING & ENROLLMENT BRIEF

- This companion issue brief provides an overview of Medicaid spending and enrollment growth with a focus on FY 2022 and FY 2023.

WEB BRIEFING

- A recording of an October 25 web briefing highlighting key findings from the 2022 report will be available.

ADDITIONAL BRIEFS

- Additional briefs using 2022 Medicaid budget survey data are published separately:

- State Policies for Expanding Medicaid Coverage of Community Health Worker (CHW) Services

- Strategies to Manage Unwinding Uncertainty for Medicaid Managed Care Plans: Medical Loss Ratios, Risk Corridors, and Rate Amendments

- Medicaid Arrangements to Coordinate Medicare and Medicaid for Dual-Eligible Individuals

- Medicaid Managed Care Network Adequacy & Access: Current Standards and Proposed Changes

BEHAVIORAL HEALTH SUPPLEMENTAL SURVEY

- In 2022, KFF and HMA also fielded a survey on Medicaid behavioral health (mental health and substance use disorder) benefits and other policy. Results from this supplemental survey are published in a series of briefs:

- Telehealth Delivery of Behavioral Health Care in Medicaid: Findings from a Survey of State Medicaid Programs

- A Look at Strategies to Address Behavioral Health Workforce Shortages: Findings from a Survey of State Medicaid Programs

- Leveraging Medicaid for School-Based Behavioral Health Services: Findings from a Survey of State Medicaid Programs

- Medicaid Coverage of Behavioral Health Services in 2022: Findings from a Survey of State Medicaid Programs

- For state-by-state detail, see: Medicaid Behavioral Health Services Data Collection

- How do States Deliver, Administer, and Integrate Behavioral Health Care? Findings from a Survey of State Medicaid Programs

- Behavioral Health Crisis Response: Findings from a Survey of State Medicaid Programs

Executive Summary

The COVID-19 pandemic has profoundly affected Medicaid program spending, enrollment, and policy, challenging state Medicaid agencies, providers, and enrollees in a variety of ways. Serving nearly 90 million low-income Americans and accounting for one-sixth of health care spending (and half of long-term care spending) and a large share of state budgets, Medicaid is a key part of the overall health care system and has had a significant role in COVID-19 response efforts. While the end date of the federal public health emergency (PHE) is currently unknown, state Medicaid programs are preparing for the unwinding of policies in place during the PHE. The PHE is currently set to end in mid-January, and the Biden Administration has indicated it will provide states with 60-day notice before it ends (i.e., in mid-November if the PHE is not extended again). The duration of the PHE will affect a range of emergency policy options in place as well as a 6.2 percentage point increase in the federal match rate (“FMAP”)1 available if states meet certain “maintenance of eligibility” requirements included in the Families First Coronavirus Response Act (FFCRA).

This report highlights certain policies in place in state Medicaid programs in state fiscal year (FY) 2022 and policy changes implemented or planned for FY 2023, which began on July 1, 2022 for most states.2 The findings are drawn from the 22nd annual budget survey of Medicaid officials in all 50 states and the District of Columbia conducted by the Kaiser Family Foundation (KFF) and Health Management Associates (HMA), in collaboration with the National Association of Medicaid Directors (NAMD). Overall, 49 states responded to this year’s survey, although response rates for specific questions varied.3 States completed this survey in mid-summer of 2022, as COVID-19 deaths started to rise after a low in April 2022, due to the highly transmissible Omicron variant, waning vaccine immunity, and relatively low booster uptake.

Key Take-Aways

- States are focusing on both longstanding issues and new priorities, including new and expanded initiatives to improve equity and reduce health disparities, maintain access to telehealth, improve behavioral health access and supports, and address workforce challenges. States also continue to respond to pandemic-related health concerns such as increasing vaccination and booster rates and the utilization of preventive care services.

- States continue to manage and advance complex delivery system and information system procurements to drive improved quality and health outcomes.

- At the same time, states are also preparing for the unwinding of the federal public health emergency and the return to normal operations.

Heading into FY 2023, most states were in a strong fiscal position, but many identified uncertainty in their longer term fiscal outlook due to economic factors including slowing revenue growth, rising inflation, and wage pressures driven by workforce shortages. Also, the outcomes of gubernatorial elections in nearly three-quarters of states (36 states) in November 2022 could have implications for state Medicaid policies and for Medicaid enrollees.

Summary of Findings

Key findings across the six sections of this report include:

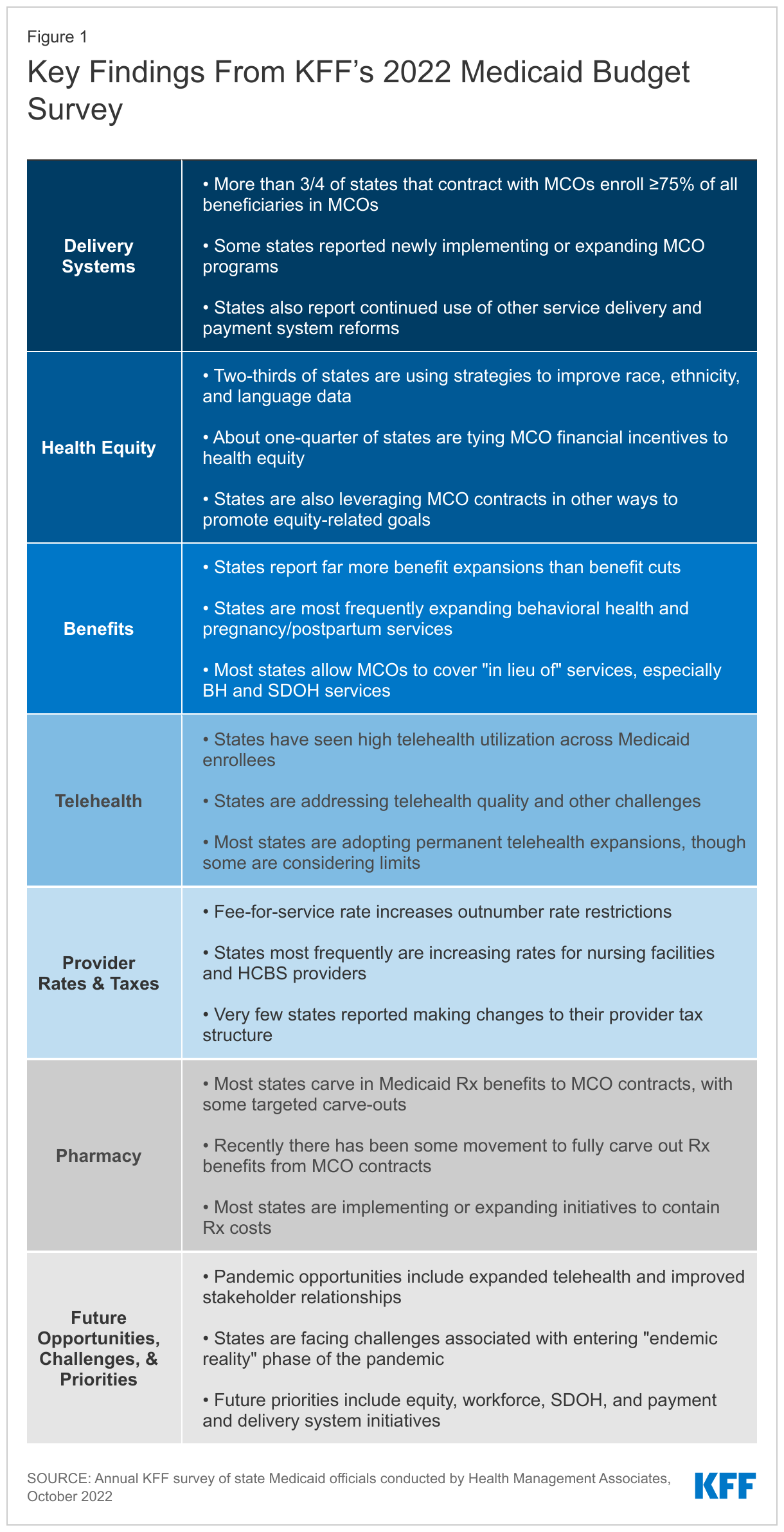

- Delivery Systems. Capitated managed care remains the predominant delivery system for Medicaid in most states. More than three-quarters of states that contract with MCOs reported that 75% or more of their Medicaid beneficiaries were enrolled in MCOs as of July 1, 2022. In FY 2022, North Carolina implemented its first MCO program. Missouri implemented the ACA Medicaid expansion in October 2021, enrolling all expansion adults in Medicaid MCOs. Although not counted in this year’s report, Oklahoma expects to implement capitated, comprehensive Medicaid managed care in FY 2024. In addition to expanding the use of risk-based, comprehensive managed care, state Medicaid programs have expanded their use of other service delivery and payment system reforms (e.g., patient centered medical homes (PCMHs), accountable care organizations (ACOs), etc.) in recent years.

- Health Equity. The COVID-19 pandemic has highlighted and exacerbated longstanding racial and ethnic disparities in health and health care. Over the past few years, the federal government and many states have identified advancing health equity as an important priority for the Medicaid program. High-quality, comprehensive data are essential for identifying and addressing health disparities and measuring progress over time. However, inadequate, incomplete, and inconsistent demographic data, particularly race and ethnicity data, is a longstanding challenge across many areas of health care, including in state Medicaid and CHIP programs (as these data must remain optional for enrollees to report). Two-thirds of states reported using at least one strategy to improve race, ethnicity, and language (REL) data completeness. States also reported MCO financial quality incentives (e.g., performance bonuses, withholds, or value-based state directed payments) tied to health equity-related performance goals and other MCO contract requirements to advance health equity, such as requiring MCOs to achieve the NCQA Distinction in Multicultural Health Care.

- Benefits. The number of states reporting new benefits and benefit enhancements greatly outpaced the number of states reporting benefit cuts and limitations in FY 2022 and FY 2023. In particular, states are focused on service expansions across the behavioral health care continuum, including programming for youth, physical and behavioral health care integration, and crisis services. States are also focused on expansions of pregnancy and postpartum services, often alongside eligibility changes to extend the postpartum period to 12 months (as allowed under the American Rescue Plan Act). Other areas of benefit expansion include preventive services; dental services (including the addition of comprehensive adult dental services); and services to address social determinants of health (SDOH), such as housing-related supports. Also, most states that contract with MCOs reported allowing MCOs to use “in lieu of” authority to cover certain services, especially behavioral health services such as coverage for nonelderly adults in “institutions for mental disease” (IMDs). Additionally, nearly one-third of states permitting ILOS reported that allowable ILOS include services to address SDOH, such as food and housing needs.

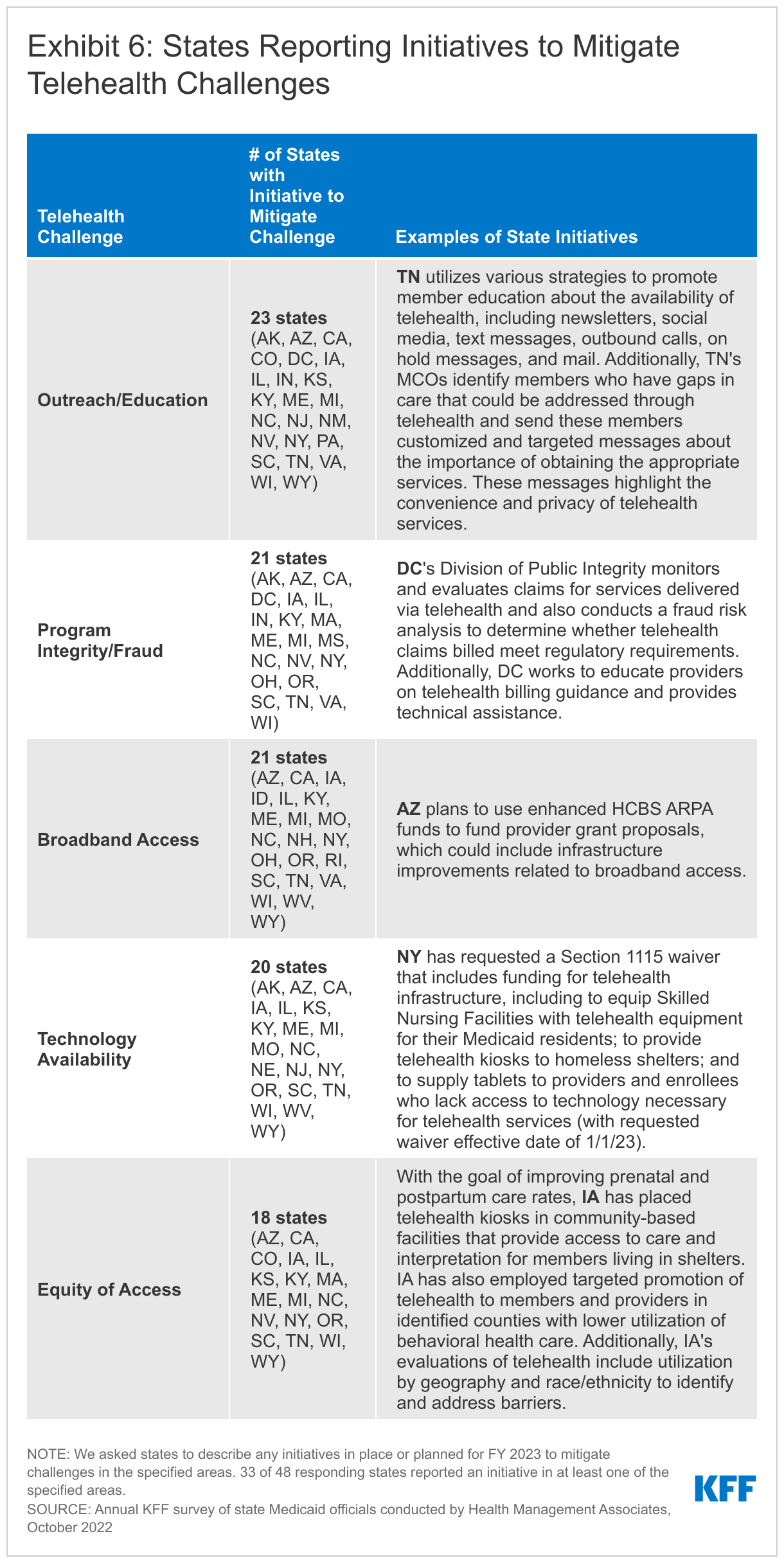

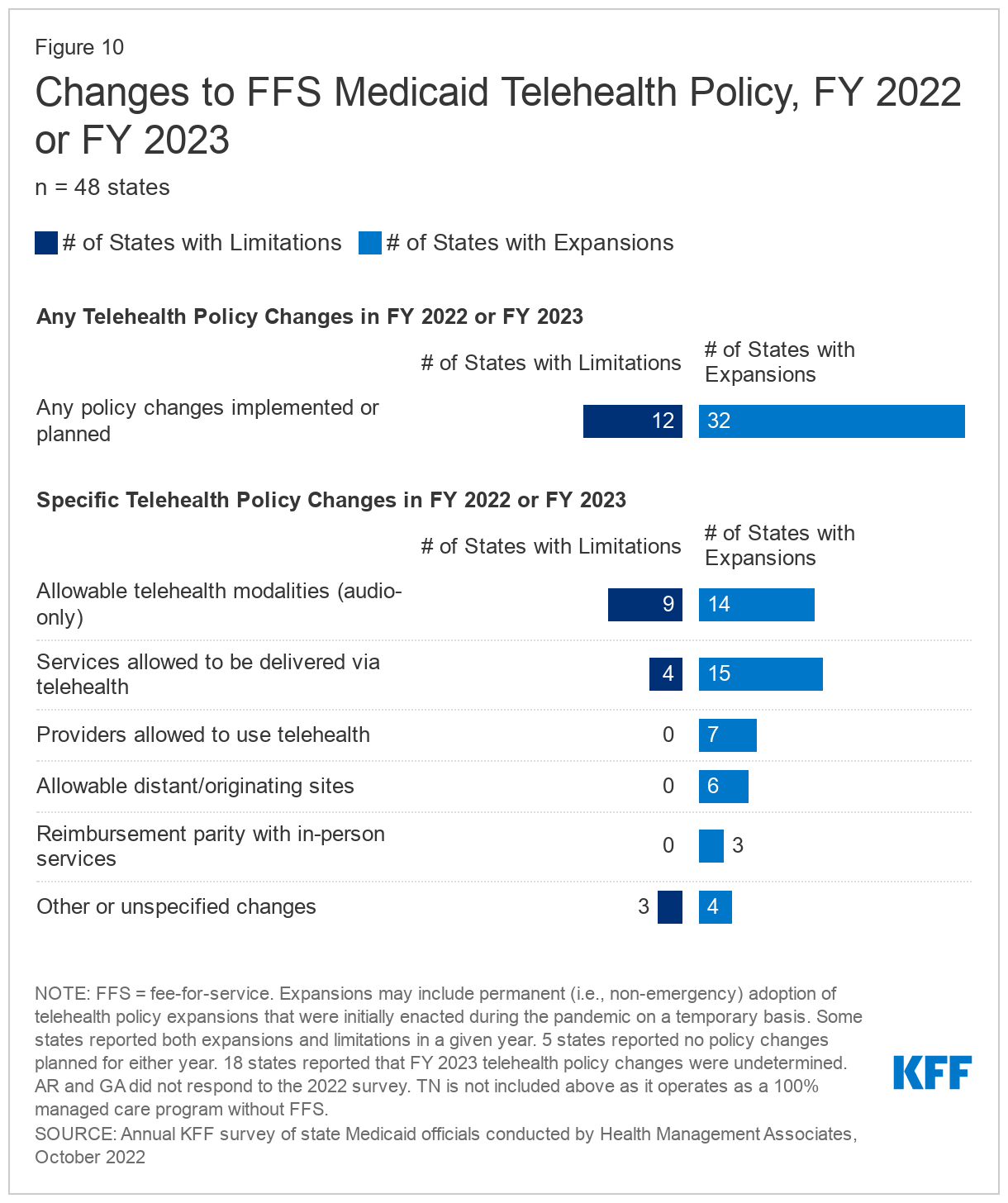

- Telehealth. Many states noted that expanded use of telehealth was a positive outcome of the COVID-19 pandemic that increased access to care. In particular, nearly all responding states added or expanded audio-only telehealth coverage in response to the pandemic. States have seen high utilization of telehealth across populations of Medicaid enrollees (e.g., ACA expansion adults, children, and individuals with disabilities), especially for behavioral health care. Most states have implemented or are planning initiatives to assess telehealth quality, though many states report ongoing considerations and uncertainty over how to effectively evaluate quality. States also report actions to address other telehealth challenges, including access to technology and broadband, program integrity, outreach and education, and equity. Most states have or plan to adopt permanent Medicaid telehealth expansions that will remain in place even after the pandemic, though some are considering guardrails on such policies. Looking ahead, key issues that may influence future Medicaid telehealth policy decisions include analysis of data, state legislation and federal guidance, and cost concerns.

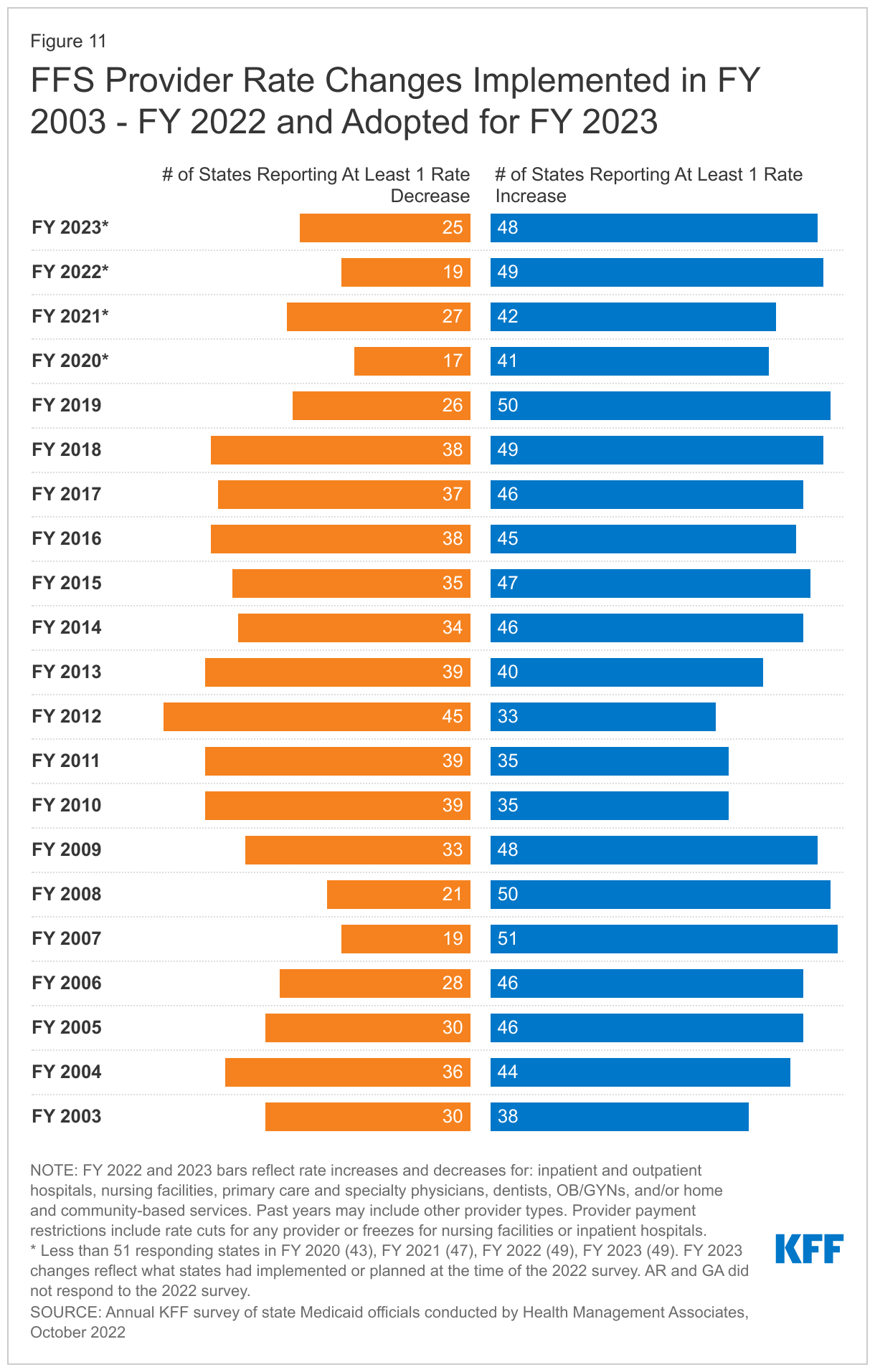

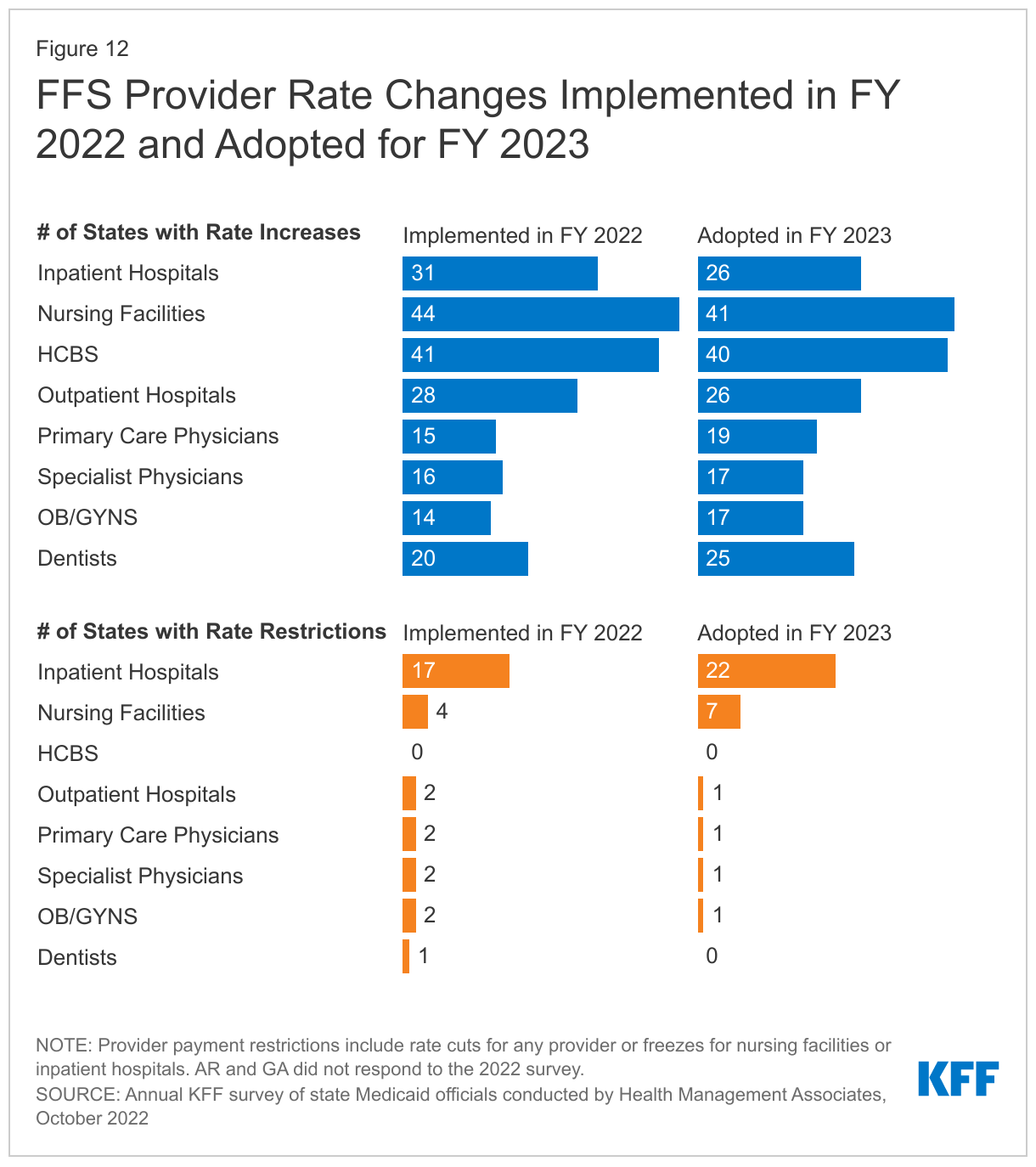

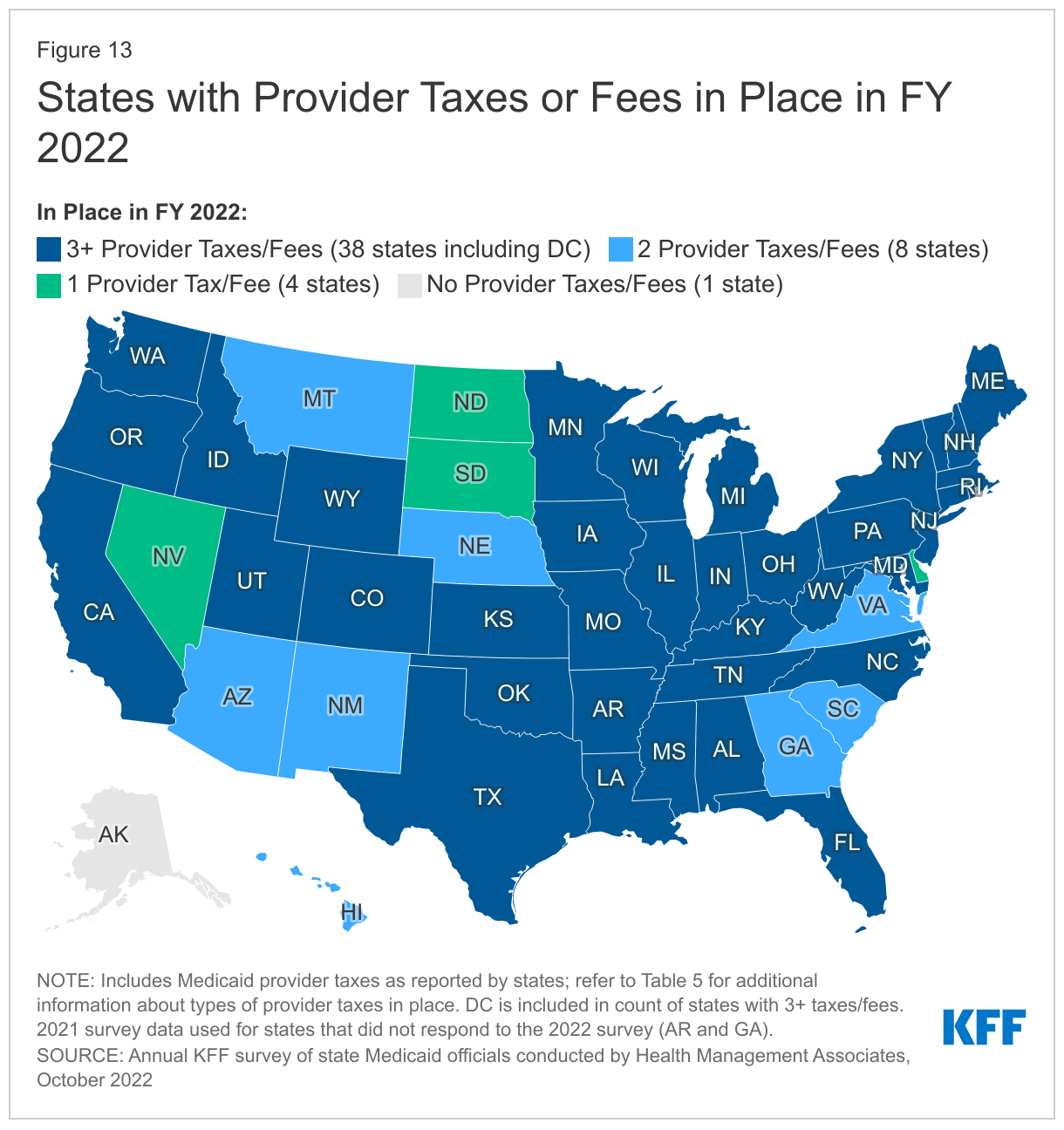

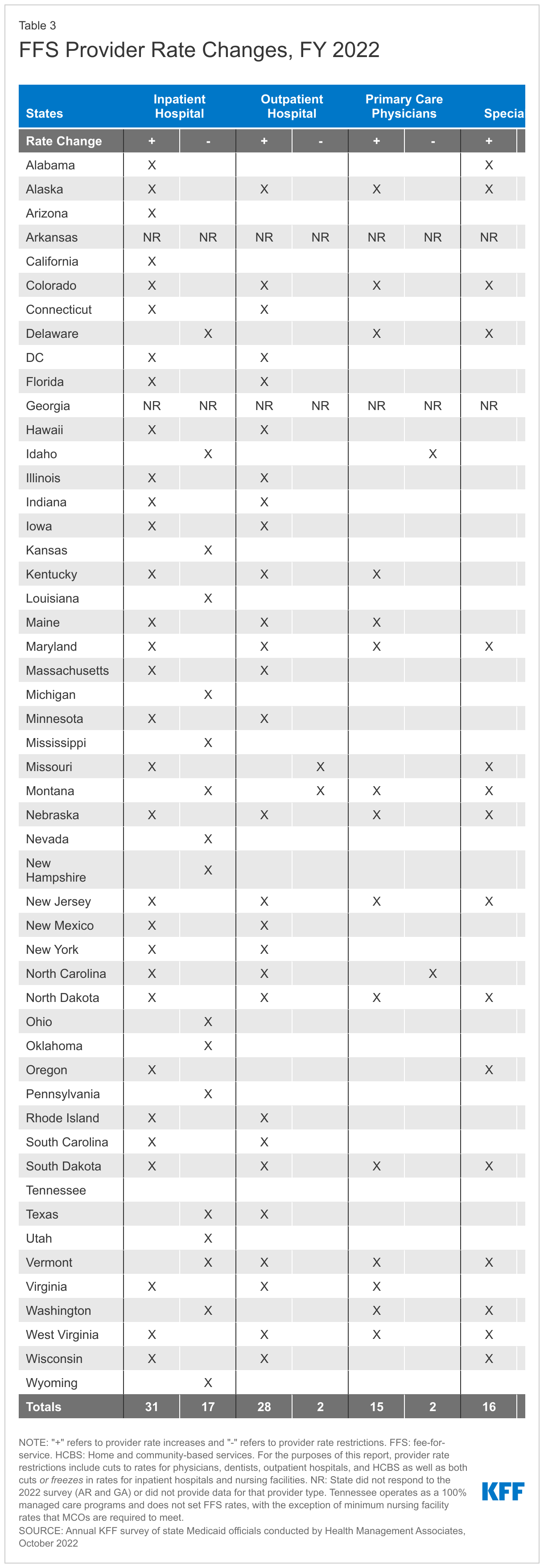

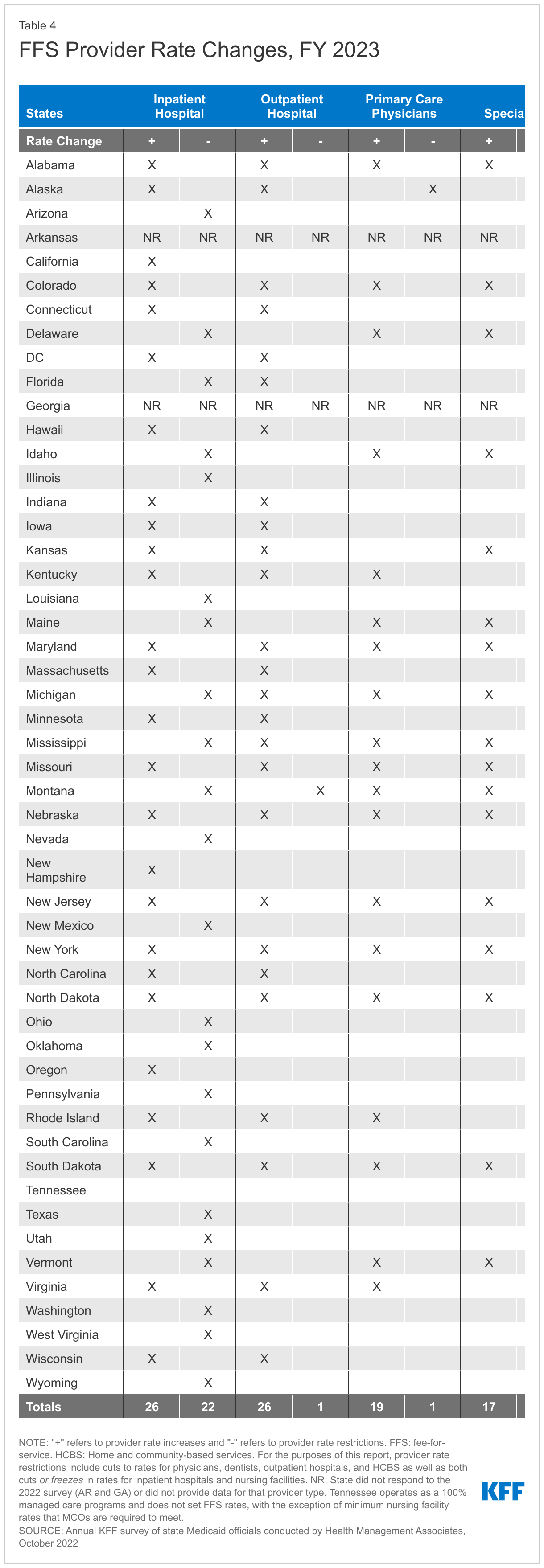

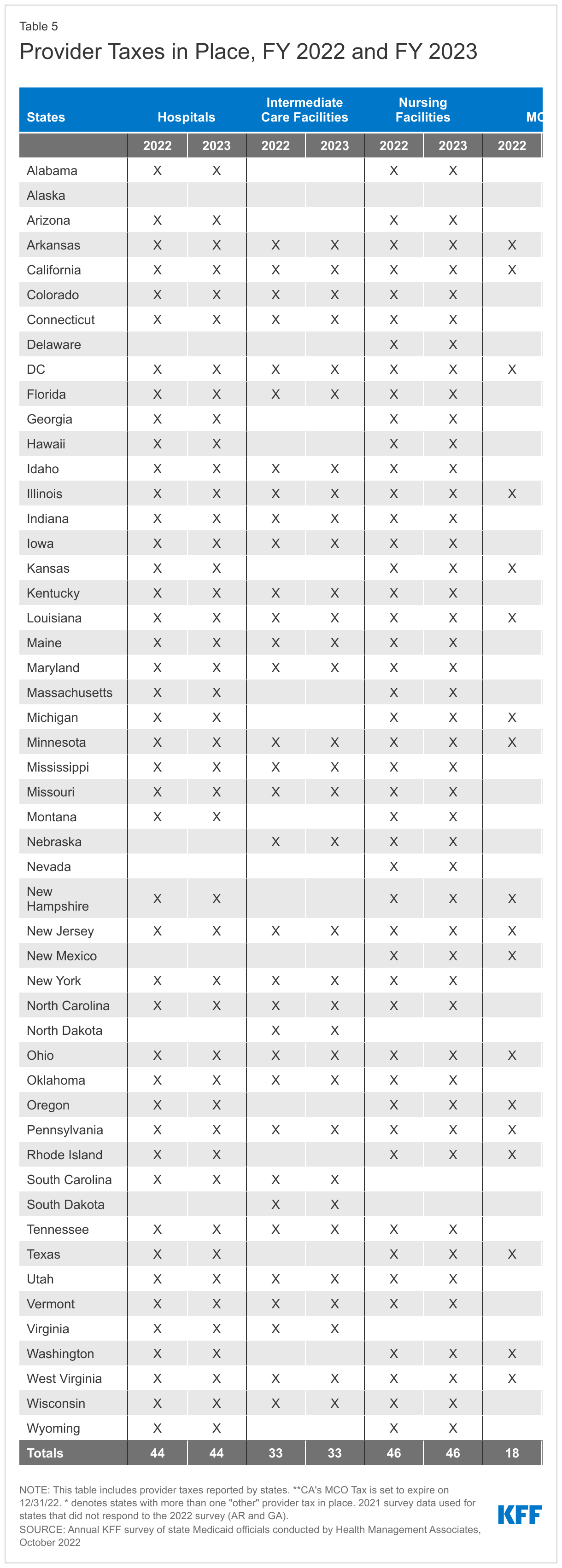

- Provider Rates and Taxes. Reported fee-for-service (FFS) rate increases outnumbered rate restrictions in FY 2022 and FY 2023. States reported rate increases for nursing facilities and home and community-based services (HCBS) providers more often than other provider categories. Several states reported comprehensive rate reform analyses impacting multiple provider types had been completed or were underway. Many states noted that worsening inflation and workforce shortages driving higher labor costs were resulting in growing calls from providers and others for rate increases. Some states noted, however, that their FY 2023 budgets do not account for current inflation levels, as they were introduced in late calendar year 2021 and early 2022 before inflation began to dramatically accelerate, but that inflation remains a concern looking ahead. Provider taxes continue to be an important source of Medicaid financing, with very few states making significant changes to their provider tax structure. Taxes on ambulance providers represent the most common type of “other” taxes implemented by states, and the new taxes planned for FY 2023 will increase the number of states with ambulance taxes to 13.

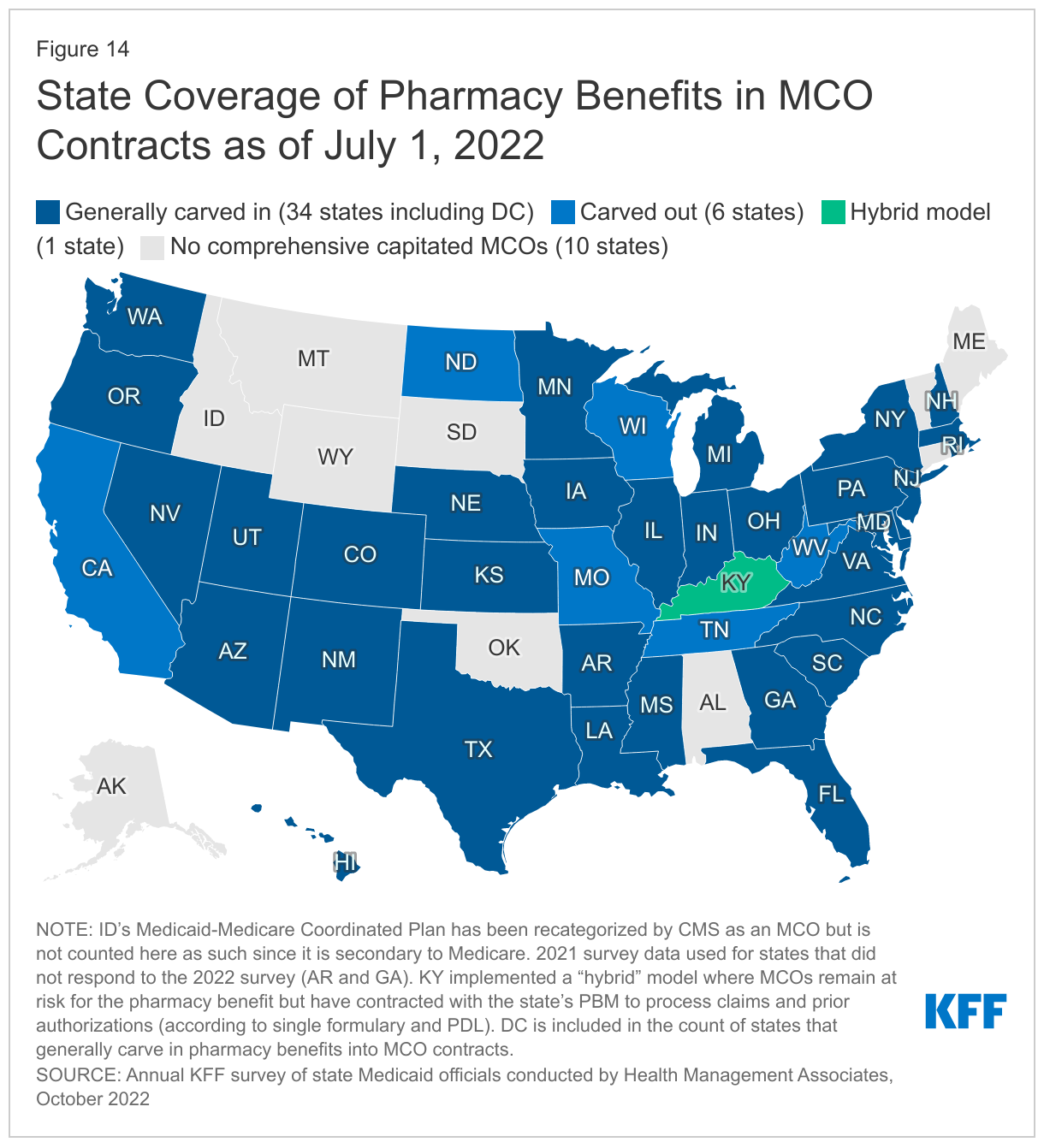

- Pharmacy. The administration of the Medicaid pharmacy benefit has evolved over time to include delivery of these benefits through MCOs and increased reliance on pharmacy benefit managers (PBMs). While most states that contract with MCOs carve in Medicaid pharmacy benefits to MCO contracts, some states “carve out” prescription drug coverage from managed care. As of January 1, 2022, California carved the pharmacy benefit out of managed care, becoming the latest state to implement a full pharmacy carve out. Two states (New York and Ohio) report plans to carve out pharmacy from MCO contracts in state fiscal year FY 2023 or later. Other states are moving to require MCOs to contract with a single PBM designated by the state. Many states are implementing or expanding initiatives to contain prescription drug costs. Seven states reported value-based arrangements (VBAs) in place with one or more drug manufacturers as of July 1, 2022, and 16 additional states are considering opportunities or are developing and executing plans to implement a VBA arrangement in FY 2023 or later. Many states reported reforms aimed at spread pricing and the role of PBMs in administering Medicaid pharmacy benefits.

Looking Ahead

As states anticipate a new “endemic reality” phase of the pandemic, they are considering future operations within the context of the significant pandemic-related impacts on enrollees’ health and wellbeing and on the health care workforce. Many states note that the pandemic has resulted in both opportunities and challenges and has shaped ongoing Medicaid priorities.

- Opportunities. The pandemic presented states with opportunities to expand access for enrollees via telehealth, improve relationships with stakeholders, and focus on data collection improvements. One state commented that telehealth was the “silver lining” of the pandemic. States also noted that the pandemic had resulted in improved relationships and engagement with enrollees, providers, plans, and/or other state and federal agencies. States mentioned that the pandemic had highlighted the importance of obtaining better and more timely data, and that improved data collection and stratification would help to identify and address health disparities.

- Challenges. States are facing challenges related to planning and preparing for the COVID-19 PHE unwinding and associated with entering an “endemic reality” phase of the pandemic. Many states mentioned the immense administrative challenges of restarting redeterminations, particularly workforce needs, as well as the challenge of making permanent or unwinding other emergency authorities in place. Even after the end of the PHE, states will still face pandemic-generated concerns such as the need to increase utilization of preventive care services in addition to vaccinations and boosters.

- Priorities. Looking ahead, states are focused on addressing health inequities that the pandemic had exposed and often exacerbated. States are also prioritizing access and outcomes for specific populations or service categories, including behavioral health, long-term services and supports, and maternal and child health. States are also addressing health care workforce challenges, especially related to behavioral health and HCBS providers. Many states also continue to focus on payment and delivery system initiatives and operations, including value-based purchasing and MCO procurements. Many states are prioritizing IT systems projects, which also support other program objectives. Finally, many states reported a focus on addressing social determinants of health to improve health outcomes.

AcknowledgementsPulling together this report is a substantial effort, and the final product represents contributions from many people. The combined analytic team from KFF and Health Management Associates (HMA) would like to thank the state Medicaid directors and staff who participated in this effort. In a time of limited resources and challenging workloads, we truly appreciate the time and effort provided by these dedicated public servants to complete the survey and respond to our follow-up questions. Their work made this report possible. We also thank the leadership and staff at the National Association of Medicaid Directors (NAMD) for their collaboration on this survey. We offer special thanks to Jim McEvoy and Kraig Gazley at HMA who developed and managed the survey database and whose work is invaluable to us.

Introduction

The COVID-19 pandemic public health emergency (PHE), in place for more than two and a half years at the time of this report, has had profound impacts on the ongoing operations of state Medicaid programs, requiring states to rapidly adapt to meet the changing needs of Medicaid enrollees and providers. Nationwide, Medicaid provided health insurance coverage to about one in four Americans in 2020 and accounted for nearly one-sixth of all U.S. health care expenditures in 2020.4 Total Medicaid/CHIP enrollment grew to 89.4 million in June 2022, an increase of 18.2 million (25.6%) from February 2020, right before the pandemic, when enrollment began to steadily increase. Beginning early in the pandemic, states and the federal government implemented numerous Medicaid emergency authorities to enhance state capacity to respond to the emerging public health and economic crises. In addition, Congress authorized changes to Medicaid through the Families First Coronavirus Response Act (FFCRA) and Coronavirus Aid, Relief, and Economic Security (CARES) Act, including a 6.2 percentage point increase in federal Medicaid matching funds (FMAP) (retroactive to January 1, 2020). This “enhanced FMAP” is available to states that meet “maintenance of eligibility” (MOE) conditions which ensure continued coverage for current enrollees as well as coverage of coronavirus testing and treatment. All of these changes (the emergency policy actions, the fiscal relief, and the MOE) are tied to the duration of the PHE. The PHE is currently set to end in mid-January, and the Biden Administration has indicated it will provide states with 60-day notice before it ends (i.e., in mid-November if the PHE is not extended again).

When the PHE ends, states will begin processing redeterminations and millions of people could lose coverage if they are no longer eligible or face administrative barriers despite remaining eligible.5 Current CMS guidance indicates states must initiate all renewals and other outstanding eligibility actions within 12 months after the PHE ends. Medicaid emergency authorities related to the PHE expire at different times, but states can choose to continue some of these changes even after the PHE ends. Some unwinding of PHE emergency authorities is already completed or underway. The temporary 6.2 percentage point increase in federal matching funds will expire at the end of the quarter in which the PHE ends.

This report draws upon findings from the 22nd annual budget survey of Medicaid officials in all 50 states and the District of Columbia conducted by KFF and Health Management Associates (HMA), in collaboration with the National Association of Medicaid Directors (NAMD). (Previous reports are archived here.) This year’s KFF/HMA Medicaid budget survey was conducted from June through September 2022 via a survey sent to each state Medicaid director in June 2022 and then a follow-up telephone interview. Overall, 49 states responded by September 2022,6 although response rates for specific questions varied. The District of Columbia is counted as a state for the purposes of this report. Given differences in the financing structure of their programs, the U.S. territories were not included in this analysis. The survey instrument is included as an appendix to this report.

This report examines Medicaid policies in place or implemented in FY 2022, policy changes implemented at the beginning of FY 2023, and policy changes for which a definite decision has been made to implement in FY 2023 (which began for most states on July 1).7 Policies adopted for the upcoming year are occasionally delayed or not implemented for reasons related to legal, fiscal, administrative, systems, or political considerations, or due to CMS approval delays. Key findings, along with state-by-state tables, are included in the following sections:

Delivery Systems

Context

For more than two decades, states have increased their reliance on managed care delivery systems to improve access and outcomes, enhance care management and care coordination, and better control costs. State managed care contracts vary widely, for example, in the populations required to enroll, the services covered (or “carved in”), and the quality and performance incentives and penalties employed. Most states contract with risk-based managed care organizations (MCOs) that cover a comprehensive set of benefits (acute care services and sometimes long-term services and supports), but many also contract with limited benefit prepaid health plans (PHPs) that offer a narrow set of services such as dental care, non-emergency medical transportation, or behavioral health services. Managed care plans are at financial risk for the services covered under their contracts and receive a per member per month "capitation" payment for these services. A minority of states operate primary care case management (PCCM) programs which retain fee-for-service (FFS) reimbursements to providers but enroll beneficiaries with a primary care provider who is paid a small monthly fee to provide case management services in addition to primary care.

Enrollment in Medicaid MCOs has grown since the start of the pandemic, tracking with overall growth in Medicaid enrollment. After the PHE ends, state Medicaid agencies will need to complete a large number of eligibility and enrollment tasks and actions, including processing renewals, redeterminations, and post-enrollment verifications. Medicaid MCOs may be well positioned to assist states in conducting outreach and providing support to enrollees who will need to navigate eligibility renewals or redeterminations. CMS guidance for state Medicaid agencies on the resumption of normal operations also includes strategies for working with managed care plans to promote continuity of coverage when the PHE’s continuous coverage requirement ends.

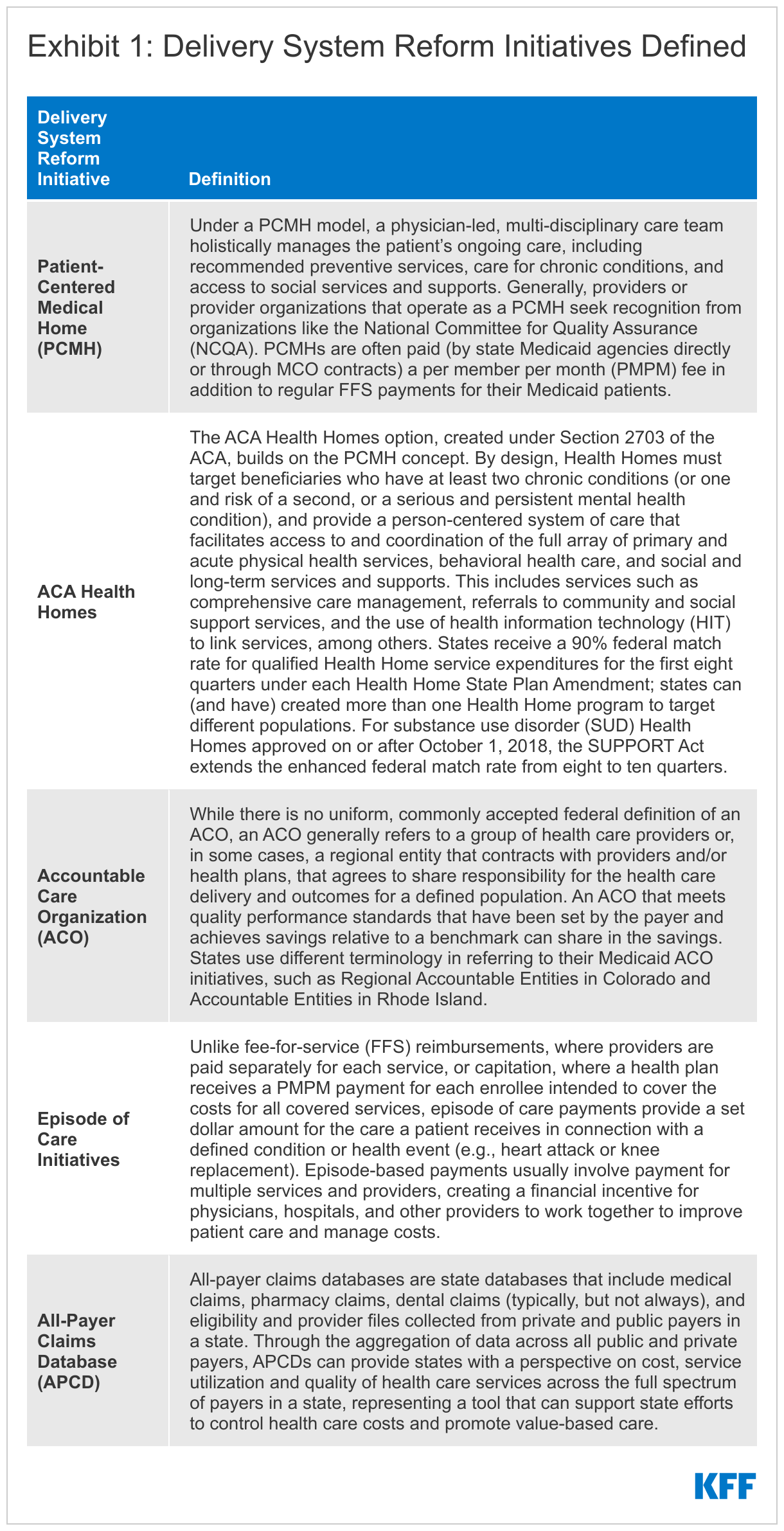

In addition to managed care, state Medicaid programs also use an array of other service delivery and payment system reforms. There is interest among public and private payers alike in restructuring delivery systems to be more integrated and patient-centered and to help achieve better outcomes and lower costs. Common delivery and payment reform models used by state Medicaid programs include patient-centered medical homes (PCMHs), ACA Health Homes, accountable care organizations (ACOs), and episodes of care. Some models may be implemented in Medicaid fee-for-service delivery systems while other payment and delivery system reform models are implemented through managed care. Although the literature is not conclusive regarding the impact of these initiatives and more research is needed, states have seen successes and many models have evolved over time in response to state experience and evaluation findings.8 ,9 ,10 ,11 ,12

Uncertainty and disruptions caused by the COVID-19 pandemic, including lack of stability in utilization patterns, labor shortages, provider capacity, and the appropriateness of pre-pandemic performance measures, among other factors, have affected (and may continue to affect) how states can advance delivery system and payment reform initiatives as well as efforts to monitor and incentivize MCO and provider performance. Additionally, when the continuous enrollment requirement ends and states resume renewals and redeterminations, millions of people could lose coverage if they are no longer eligible or are unable to navigate administrative barriers despite remaining eligible. As a result, Medicaid MCOs may see the overall acuity of their membership increase, with implications for per member utilization and costs, and also the return of member churn (i.e., the temporary loss of coverage in which enrollees disenroll and then re-enroll within a short period of time) which can lead to care disruptions.

This section provides information about:

- Managed care models

- Populations covered by risk-based managed care

- Managed care changes

- Other state-contracted delivery systems or initiatives

Findings

Managed Care Models

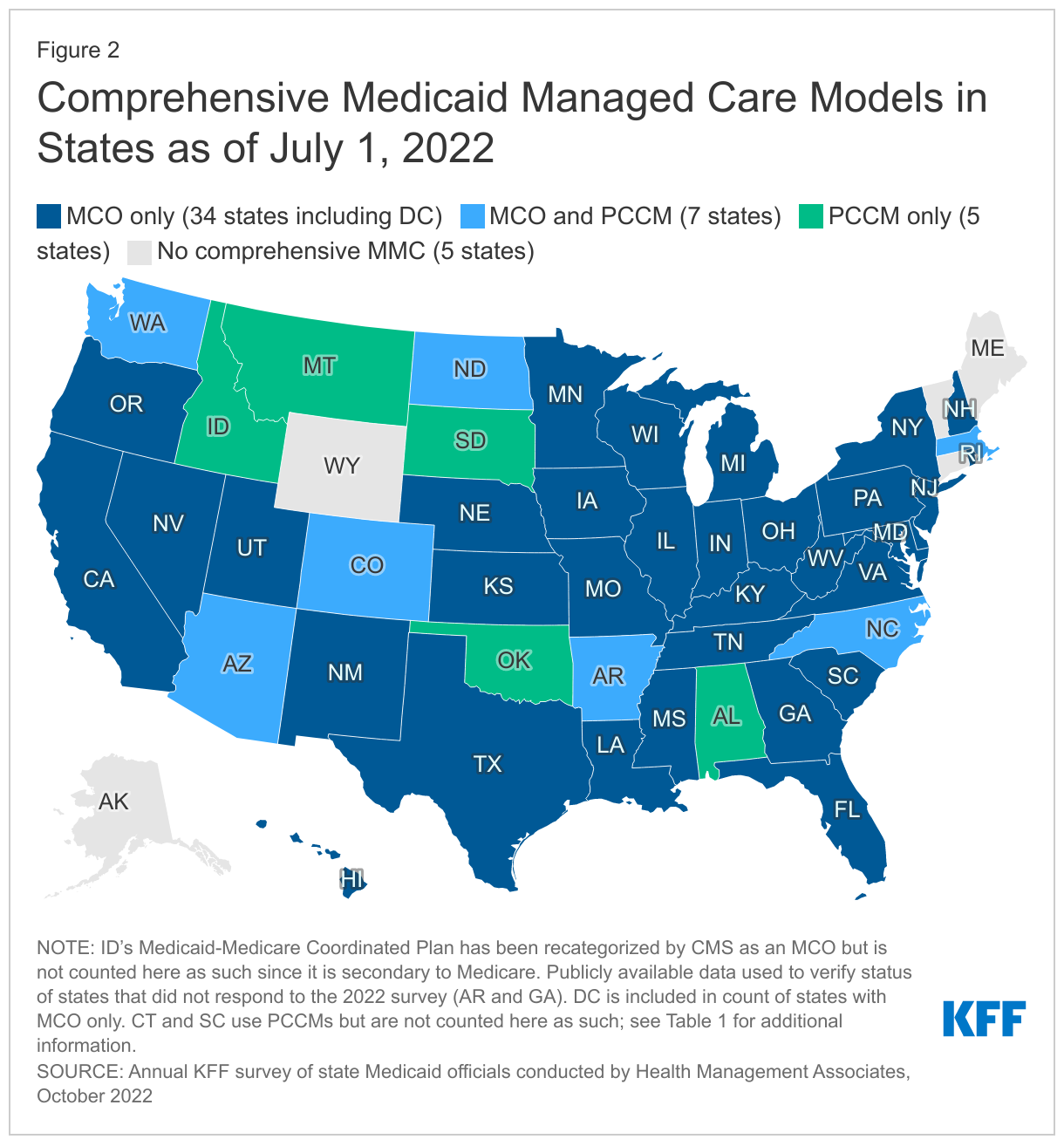

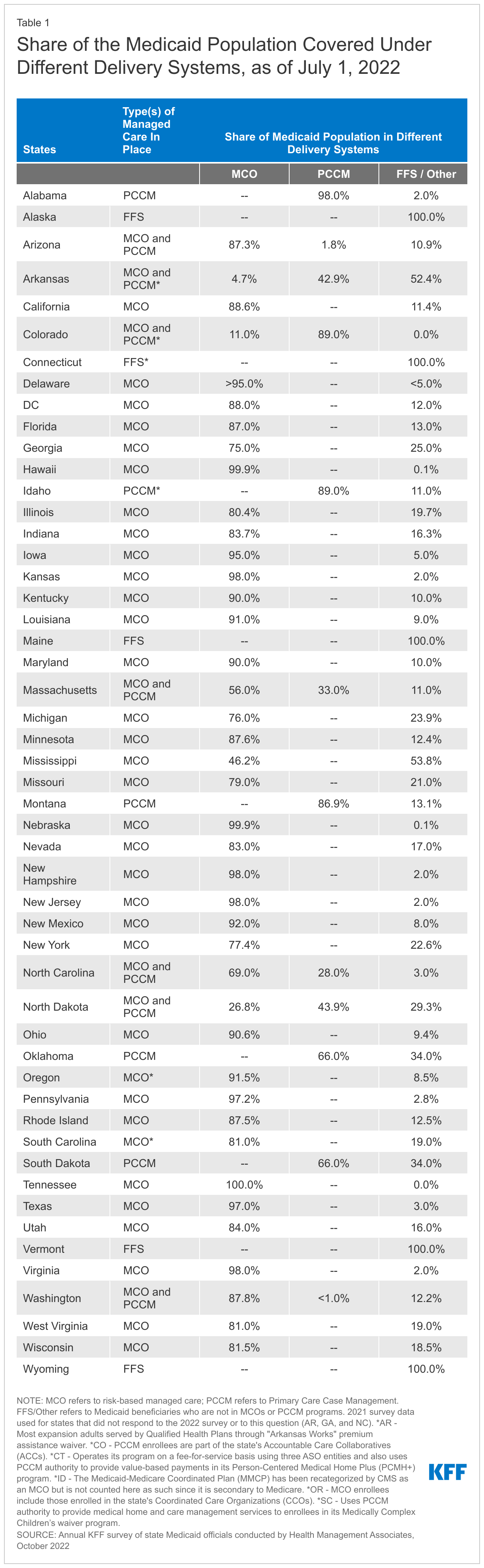

Capitated managed care remains the predominant delivery system for Medicaid in most states. As of July 2022, all states except five – Alaska, Connecticut,13 Maine, Vermont,14 and Wyoming – had some form of managed care (MCOs and/or PCCM) in place. As of July 2022, 41 states15 were contracting with MCOs (unchanged from 2021), and only two of these states (Colorado and Nevada) did not offer MCOs statewide. Twelve states16 reported operating a PCCM program, one fewer than reported in 2021 (as Maine ended its PCCM program in FY 2022).17 Although not counted in this year’s report, following the passage of SB 1337 in May 2022, Oklahoma expects to implement capitated, comprehensive Medicaid managed care in FY 2024 (as of October 1, 2023),18 ,19 and release an RFP to procure MCO vendors in the fall of 2022.

Of the 46 states that operate some form of comprehensive managed care (MCOs and/or PCCM), 34 states operate MCOs only, five states operate PCCM programs only,20 and seven states operate both MCOs and a PCCM program (Figure 2 and Table 1). In total, 27 states21 were contracting with one or more PHPs to provide Medicaid benefits including behavioral health care, dental care, vision care, non-emergency medical transportation (NEMT), or long-term services and supports (LTSS).

Populations Covered by Risk-Based Managed Care

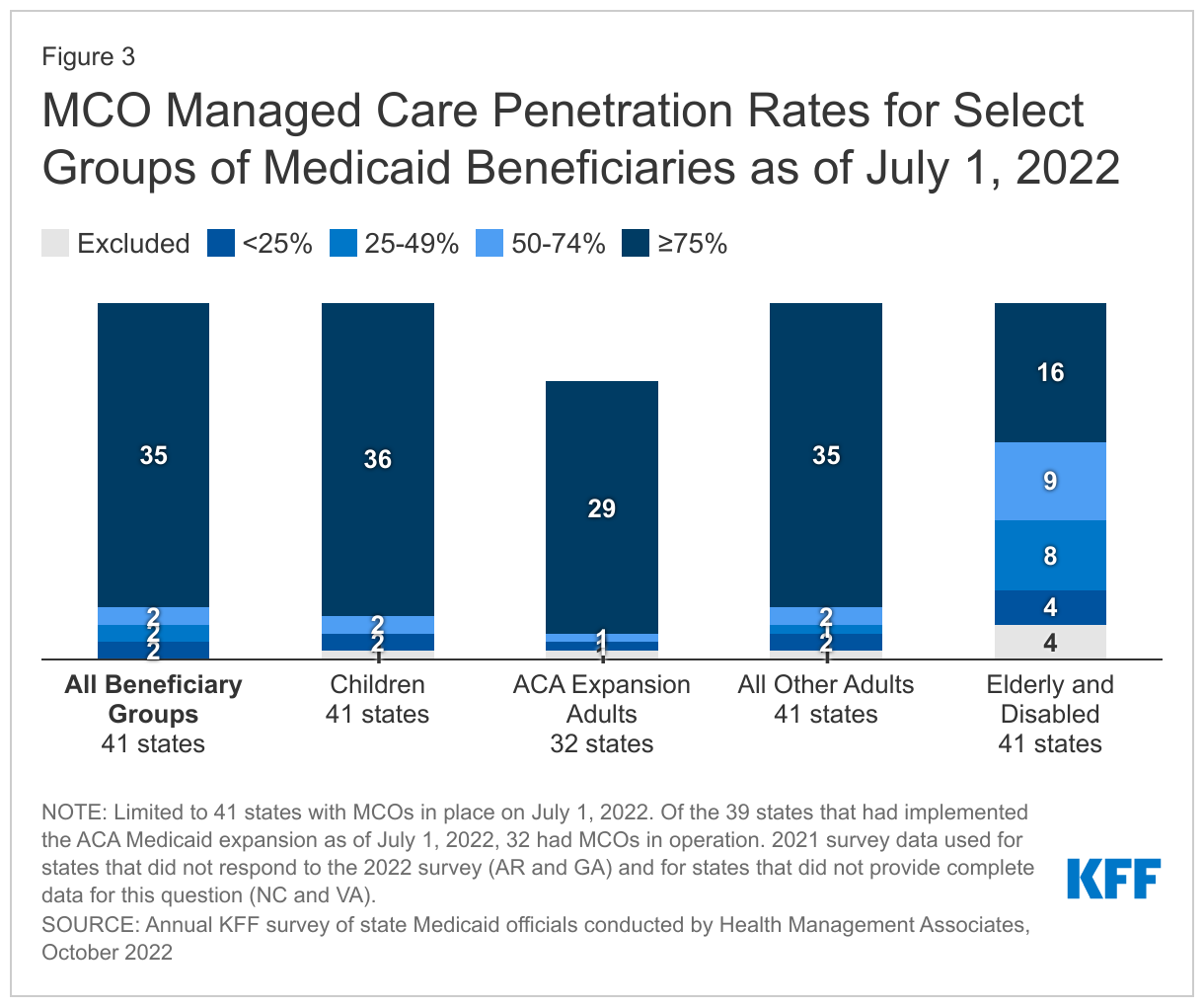

The vast majority of states that contract with MCOs (35 of 41) reported that 75% or more of their Medicaid beneficiaries were enrolled in MCOs as of July 1, 2022, a decrease of one state22 compared to the 2021 survey and includes the ten states with the largest total Medicaid enrollment (Figure 3 and Table 1). These ten states account for over half of all Medicaid beneficiaries across the country.23

Children and adults, particularly those enrolled through the ACA Medicaid expansion, are much more likely to be enrolled in an MCO than elderly Medicaid beneficiaries or persons with disabilities. Thirty-six of the 41 MCO states reported covering 75% or more of all children through MCOs.24 Of the 39 states that had implemented the ACA Medicaid expansion as of July 1, 2022, 32 were using MCOs to cover newly eligible adults. The large majority of these states (29 states) covered more than 75% of beneficiaries in this group through capitated managed care. Thirty-five of the 41 MCO states reported covering 75% or more of low-income adults in pre-ACA expansion groups (e.g., parents, pregnant women) through MCOs. In contrast, the elderly and people with disabilities were the group least likely to be covered through managed care contracts, with only 16 of the 41 MCO states reporting coverage of 75% or more such enrollees through MCOs (Figure 3).

Managed Care Changes

A number of states reported a variety of managed care changes made in FY 2022 or planned for FY 2023. Notable changes included the following:

- North Carolina implemented its first MCO program. On July 1, 2021, North Carolina launched new MCO “Standard Plans,” offering integrated physical and behavioral health services statewide, with mandatory enrollment for most population groups.25 Over 1.7 million Medicaid beneficiaries were enrolled in Standard Plans as of September 2022.26 North Carolina will launch “Tailored Plans” on December 1, 2022, offering integrated services to enrollees with significant behavioral health needs and intellectual/developmental disabilities (I/DD).27

- Five states (California, Missouri, Nevada, New Jersey, and New York) reported expanding mandatory MCO enrollment for targeted populations. Missouri implemented the ACA Medicaid expansion in October 2021 (with coverage retroactive to July 1, 2021) enrolling all expansion adults in Medicaid MCOs. The California Advancing and Innovating Medi-Cal (CalAIM) initiative includes mandatory enrollment of multiple populations into managed care in both FY 2022 and FY 2023.28 In FY 2023, dual eligible beneficiaries across the state will be required to enroll in managed care. Currently, mandatory enrollment of dual eligibles is limited to certain California counties.29 ,30 Effective January 1, 2022, Nevada is no longer allowing enrollees with a seriously mentally ill (SMI) determination to disenroll from managed care. New Jersey expanded managed care for acute care and LTSS to nursing home residents, who were previously grandfathered and allowed to remain in FFS after the state first transitioned to managed long-term services and supports (MLTSS). New York began mandatory MCO enrollment of children and youth in direct placement foster care in New York City and children and youth placed in foster care in the care of Voluntary Foster Care Agencies statewide in July 2021.31

- Two states (Missouri and Ohio) reported introducing specialized managed care programs for children with complex needs. Missouri awarded a specialty plan contract to consolidate state care and custody enrollees into one health plan. On July 1, 2022, Missouri launched a new specialty health plan, called Show Me Healthy Kids, to provide coverage to youth in Department of Social Services custody, former foster children, and for individuals receiving adoption assistance payments. The specialized managed care plan was awarded to Home State Health (Centene).32 On July 1, 2022, Ohio introduced a specialized managed care program for youth with complex behavioral health and multisystem needs. OhioRISE (Resilience through Integrated Systems and Excellence), a prepaid inpatient health plan (PIHP), creates access to new in-home and community-based services for children with complex behavioral health challenges.33 OhioRISE also includes a 1915(c) waiver component which aims to prevent institutionalization and keep families supported in the community.

- Three states (California, Nevada, and Tennessee) indicated that they were carving in certain long-term services and supports into their managed care programs. California will be carving in institutional long term care in to MCO contracts in all counties in 2023, making coverage for these services consistent across California.34 Tennessee plans to incorporate Intermediate Care Facility (ICF) Services as well as home and community based LTSS services for people with intellectual and developmental disabilities into its MCO contract in FY 2023. Finally, Nevada extended the number of days its plans must cover nursing facility services from 45 to 180 days in its MCO contracts effective January 2022.

- Three states (California, District of Columbia, and Ohio) reported carving out specific benefits from managed care contracts. California and Ohio – reported carving out pharmacy services in FY 2022 or FY 2023, respectively. The District of Columbia carved out emergency medical transportation from its MCO contracts in FY 2022.

- Four states (Maine, North Carolina, Oregon, and Washington) reported changes to their PCCM programs. Maine ended its PCCM program, moving to a new value-based approach to support primary care. On July 1, 2022, Maine launched a single, integrated initiative called Primary Care Plus (aligned with the Center for Medicare and Medicaid Innovation’s (CMMI’s) Primary Care First multi-payer initiative). Primary Care Plus aims to move away from a fee-for-service payment system toward population-based payments tied to cost- and quality-related outcomes.35 North Carolina launched a new PCCM option in July 2021 available only to Indian Health Service (IHS) eligible beneficiaries associated with the Eastern Band of Cherokee Indians in select counties in the western part of the state.36 Oregon reported plans to implement an Indian PCCM program in FY 2023. Washington is planning to implement a tribal PCCM entity program in FY 2023 and released a draft SPA for comment in May 2022.37 This program will expand options for Indian health care providers (IHCPs) interested in providing primary case management services. It is like the current PCCM program available to IHCPs but with a larger, more defined list of provider responsibilities.

- Several states also reported efforts to streamline managed care programs. In FY 2023, Virginia plans to implement Cardinal Care, merging the state’s two existing managed care programs: Medallion 4.0 (serving children, pregnant individuals, and adults) and Commonwealth Coordinated Care Plus (CCC Plus) (serving seniors, children and adults with disabilities, and individuals who require LTSS).38 ,39 The six MCOs currently serving members statewide in Medallion 4.0 and CCC Plus will continue to do so under Cardinal Care. Mississippi and Ohio report that in FY 2023 they are centralizing credentialing processes for providers in MCO networks at the state level to reduce the administrative burden on Medicaid providers. In addition, Ohio plans to implement a fiscal intermediary in FY 2023 requiring all provider claims and prior authorization requests to go through the fiscal intermediary rather than through individual MCOs.40

Other State-Contracted Delivery Systems or Initiatives

In addition to expanding the use of risk-based, comprehensive managed care, state Medicaid programs have expanded their use of other service delivery and payment system reforms in recent years. State Medicaid programs utilize a range of delivery and payment reform; however, there is wide state variation in Medicaid health care delivery and payment systems, as states design and combine service delivery models and payment approaches in different ways.

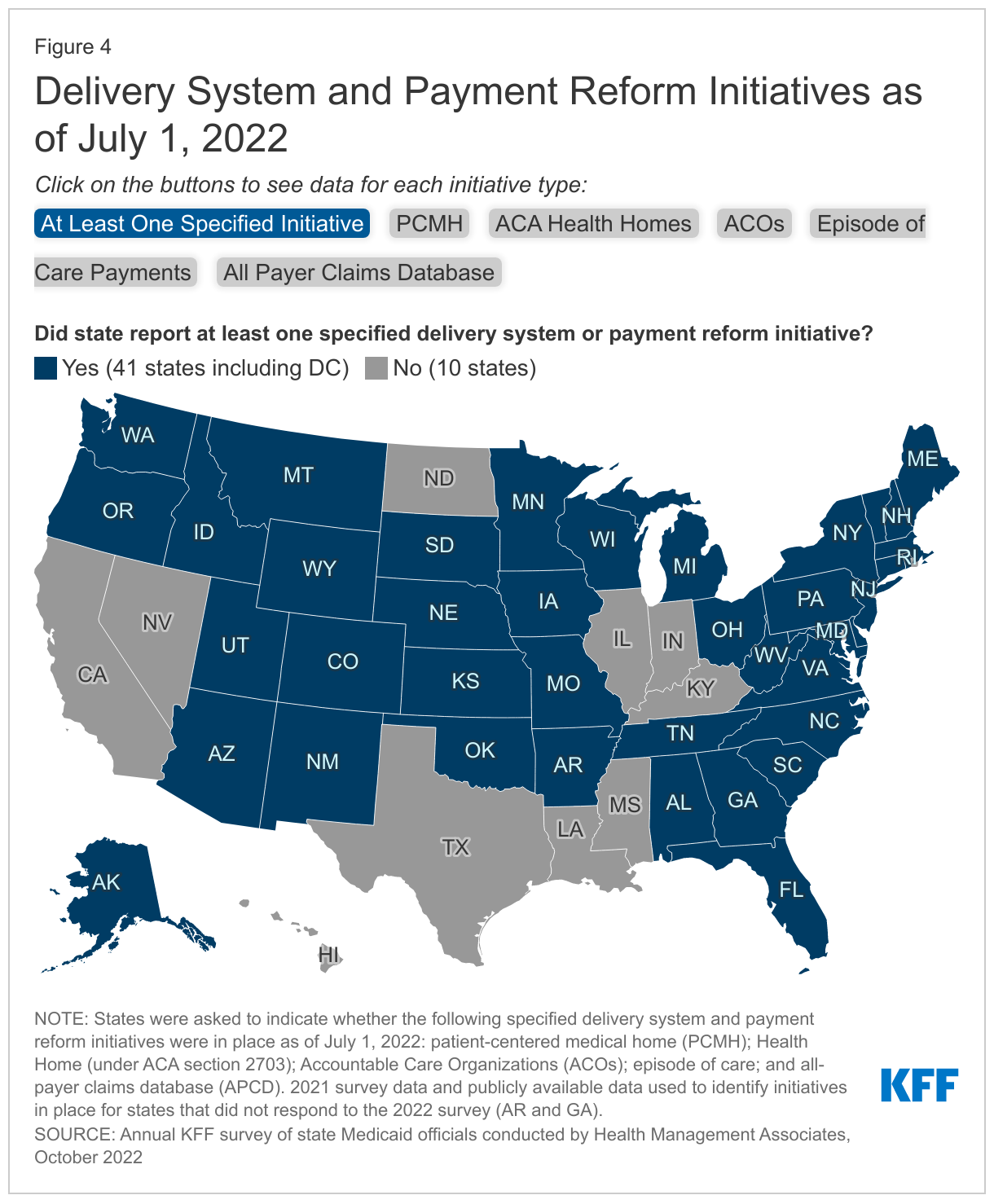

The vast majority of states (41 of 51) had at least one specified delivery system and payment reform initiative41 designed to address Medicaid cost and quality in place as of July 2022 and nearly half (24 of 51) had multiple initiatives in place (Figure 4).42 These initiatives are defined in Exhibit 1. Three states (New York, Rhode Island, and Vermont) had implemented initiatives in all five specified areas. For example, Vermont is participating in an All-Payer ACO Model with CMS; has in place a multi-payer advanced primary care initiative, including PCMH and community health teams through the state’s Blueprint for Health; has a “Hub and Spoke” Health Home model for people experiencing opioid dependence; has episodic payments for its residential substance use disorder (SUD) program; and has a mature all-payer claims data base (APCD). Total states with each initiative include:

- Patient-Centered Medical Home – 26 states43

- ACA Health Homes – 20 states

- All-Payer Claims Database (APCD) – 18 states

- Accountable Care Organization – 11 states

- Episode of Care – 9 states

Many of these delivery system and payment reform initiatives are longstanding and have been in place for many years. Although the survey did not ask for details regarding each initiative, several states identified changes to initiatives as well as plans to implement in the near future. For example, in FY 2022 California transitioned from its former ACA Health Home program to an “Enhanced Care Management” managed care benefit available statewide. This initiative is part of a framework for broad-based delivery system, program, and payment reform across the Medi-Cal program, called California Advancing and Innovating Medi-Cal (CalAIM).44 Also in FY 2022, Maine replaced its PCMH and PCCM programs with the new “Primary Care Plus” program, an integrated care model that provides monthly payments to eligible primary care providers that vary by practice characteristics and are risk adjusted and performance-based. Although Nevada does not currently have an APCD in place, one was approved for implementation in the 2021 legislative session with an anticipated go-live date of January 2023. Several other states including California, Indiana, Oklahoma, and West Virginia indicated an APCD is planned or currently under development.

Health Equity

Context

The COVID-19 pandemic has highlighted and exacerbated longstanding racial and ethnic disparities in health and health care. Prior to the pandemic, people of color fared worse than White people across many measures of health and health care, reflecting inequities within the health care system as well as across broader social and economic factors that drive health (often referred to as social determinants of health or social drivers of health) that are rooted in racism and discrimination. As a major source of health coverage for people of color, Medicaid programs can help to address health disparities. Over the past few years, the federal government and many states have identified advancing health equity as an important priority for the Medicaid program. In November 2021, CMS published its strategic vision for Medicaid and CHIP which identified equity and reducing health disparities as key focus areas, emphasizing Section 1115 demonstration waivers can help foster improved quality and equity.

High-quality, comprehensive data are essential for identifying and addressing health disparities and measuring progress over time. For example, during the COVID-19 pandemic, disaggregated demographic data were crucial to identifying disparities and implementing policy solutions. Unfortunately, inadequate, incomplete, and inconsistent demographic data, particularly race and ethnicity data, is a longstanding challenge across many areas of health care, including in state Medicaid and CHIP programs. For example, a Medicaid and CHIP Payment and Access Commission (MACPAC) analysis of 2018 Medicaid administrative data found high rates of missing or unknown race and ethnicity data and conflicts with key benchmark data.

Federal Medicaid managed care regulations also require states that contract with managed care plans to develop and publicly post quality strategies that include plans to reduce health care disparities. To further these quality strategies, states develop access and quality standards within federal guidelines that MCOs are required to meet. Some state MCO contracts incorporate requirements to advance health equity, such as requiring MCOs to achieve the NCQA Distinction in Multicultural Health Care,45 and states may also tie MCO financial quality incentives (e.g., performance bonuses, withholds, or value-based state directed payments) to health equity-related performance goals. States must also require MCOs to implement performance improvement projects (PIPs) to examine access to and quality of care, and these projects often include analysis of health disparities.

This section provides information about:

- Improving Medicaid race, ethnicity, and language (REL) data collection

- Financial incentives (FFS and MCO) tied to health equity-related performance goals

- Other MCO health equity requirements

- Performance improvement projects (PIPs) focused on health disparities

Findings

Improving Medicaid Race, Ethnicity, and Language (REL) Data Collection

Although all Medicaid agencies ask applicants to self-report their race and ethnicity, it is not mandatory for applicants to do so. During Medicaid eligibility determinations (and redeterminations), race and ethnicity are not considered, and data not being used in Medicaid determinations must remain optional for applicants to report. While states must inform applicants that submitting race/ethnicity data is optional, this can lead to missing data, particularly if the instructions and rationale for providing race/ethnicity data are unclear, if the applicant has concerns or questions about how the data may be used, or if the applicant does not feel he or she fits into the options provided. Race and ethnicity categories on Medicaid applications vary considerably across states. An audit of state Medicaid enrollment applications conducted by the State Health Access Data Assistance Center (SHADAC) revealed substantial variation in the number and type of race/ethnicity categories used by states, ranging from 5 to 37 race categories and 2 to 8 ethnicity categories. States vary in the amount of race/ethnicity data they report as unknown or missing. A December 2021 analysis by CMS found that in 14 states, more than 20 percent of race/ethnicity data was missing. State Medicaid programs can implement a variety of strategies to enhance or improve REL data collection. On this year’s survey, we asked states whether specified strategies were in place (as of July 1, 2022) to improve the completeness of REL data.

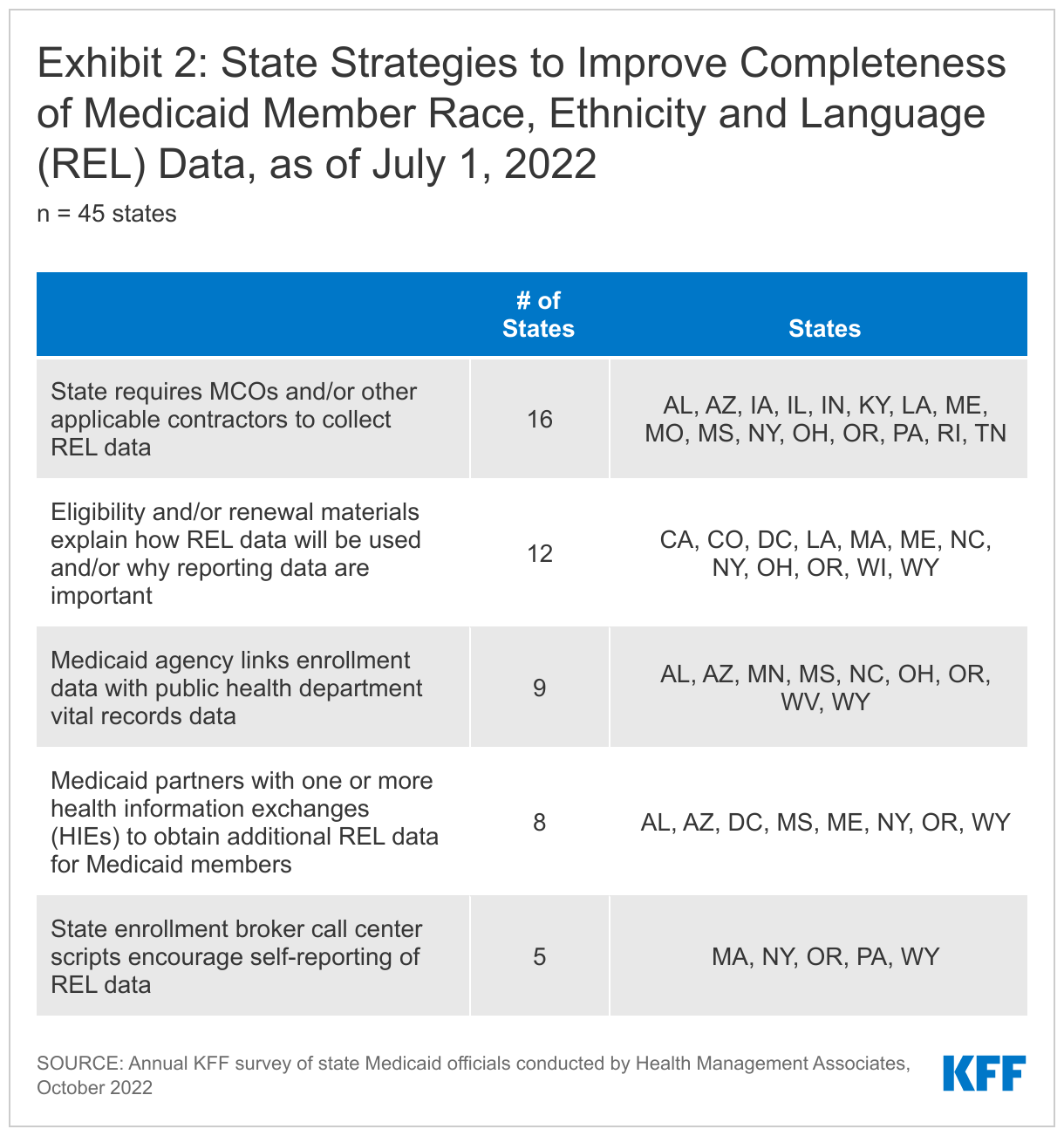

Over half of the states that responded to this question (25 of 45) reported using at least one specified strategy to improve race, ethnicity, and language (REL) data completeness (Exhibit 2). Over one-third of responding states (16 of 45) reported requiring MCOs and other applicable contractors to collect REL data. About one-quarter of responding states (12 of 45) reported that eligibility, renewal materials, and/or applications explain how REL data will be used and/or why reporting these data are important. About the same number of responding states reported linking Medicaid enrollment data with public health department vital records data (9 of 45) and partnering with one or more health information exchanges (HIEs) to obtain additional REL data for Medicaid enrollees (8 of 45). Several states identified issues with data systems and lack of integration between systems as barriers.

Eighteen states reported “other” strategies to improve Medicaid REL data.46 For example:

- Multiple states (Alaska, Colorado, Minnesota, Ohio, and Oregon) reported using data from alternate sources, such as administrative records from other agencies or third-party databases, to populate missing REL values. Washington state reported developing a new eligibility infrastructure that would integrate data across systems to improve data quality.

- Several states mentioned changes made to the Medicaid application to improve REL data including translating the application into other languages (Oklahoma), adding disability questions and gender identity and modality questions (Oregon), changing the phrasing of REL data questions (South Carolina), allowing applicants to provide more detailed race and ethnicity information (Wisconsin), and implementing, or planning to implement, “opt-out” options for race and ethnicity questions (Maryland and Louisiana).

- Two states (Arizona and Connecticut) reported that health equity-related committees or task forces within their state governments were developing recommendations related to REL data collection and disaggregation.

- Massachusetts, through its approved MassHealth Section 1115 demonstration waiver, will financially incentivize ACOs and ACO-participating hospitals to provide complete data on race, ethnicity, language, disability, sexual orientation and gender identity (RELD SOGI) starting in FY 2023. The state is working to update enrollment platforms to clarify and add questions related to RELD SOGI and modify downstream systems accordingly.

- South Carolina reported using training to emphasize the value of REL data collection with its eligibility staff.

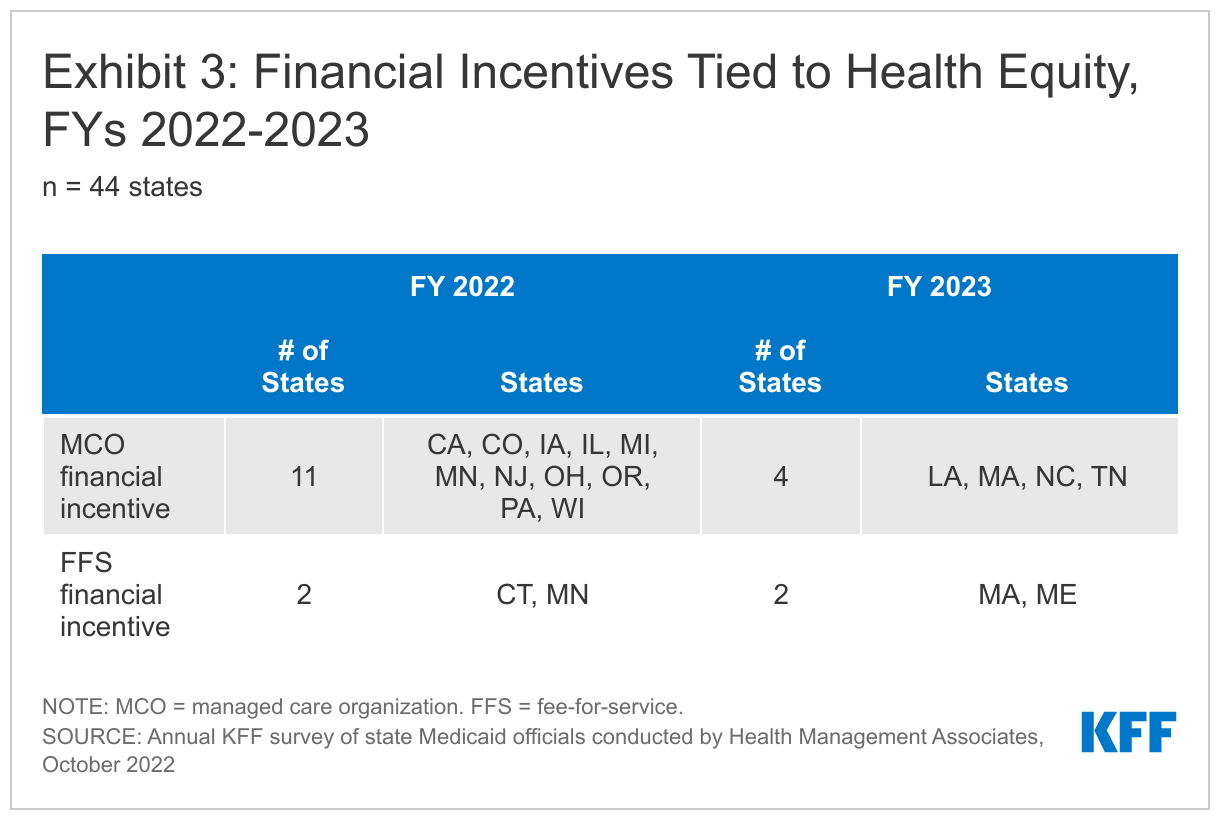

Financial Incentives Tied to Health Equity-Related Performance Goals

States use an array of financial incentives to improve quality including linking performance bonuses or penalties, capitation withholds, or value-based state-directed payments to quality measures. States implement financial incentives across delivery systems (fee-for-service and managed care). On this year’s survey, we asked states if they had an MCO financial quality incentive or FFS financial incentive for providers tied to a health equity-related performance goal (e.g., reducing disparities by race/ethnicity, gender, disability status, etc.) in place in FY 2022 or planned for FY 2023.

About one-quarter of responding states (12 of 44) reported at least one financial incentive tied to health equity in place in FY 2022 (Exhibit 3). The vast majority of these incentives were in place in managed care arrangements (11 of 13). Only two states (Connecticut and Minnesota), reported a FFS financial incentive in FY 2022. Five additional states report plans to implement financial incentives linked to health equity in FY 2023. Within managed care arrangements, states most commonly reported linking (or planning to link) capitation withholds, pay for performance incentives, and/or state-directed provider payments to health equity-related quality measures. Three states (Ohio, Oregon, and Wisconsin) reported implementing MCO incentive funding focused on reducing disparities in COVID-19 vaccination rates. Two states with FFS incentives (in place or planned) (Massachusetts and Minnesota) reported health equity incentives for ACOs.

Other notable state examples include:

- California’s Quality Incentive Pool (QIP) program is a managed care directed payment program for California’s public health care systems (i.e., designated public hospitals and district/municipal public hospitals) that ties payments to performance on designated quality measures. The QIP program explicitly incorporates two Improving Health Equity (IHE) metrics, one of which is required for the larger public hospitals. The IHE measure allows hospitals to report a disparity-sensitive measure on a priority population selected by each hospital. Hospitals are also required to stratify by race/ethnicity for up to five designated measures on an informational basis.47 Additionally, in 2023, the state plans to adjust base capitation rates in counties with more than one plan based on plan performance on select quality measures. Performance on health equity will be incorporated once race and ethnicity stratifications are available.

- Connecticut has had an obstetrics pay for performance program in place for six years that targets birthing people at risk for adverse outcomes, including Black and birthing people of color. In FY 2023, the state plans to launch a maternity payment bundle where financial incentives will be tied to health equity outcomes. The state will include doulas and breastfeeding supports to remedy disparities in maternal and birth outcomes for historically marginalized groups including Black and birthing people of color and those with substance use disorders.

- In Massachusetts, one of the key goals for MassHealth’s next Section 1115 demonstration period is to advance health equity, with a focus on initiatives addressing health-related social needs and specific disparities. MassHealth intends to implement health equity incentives for ACOs and acute care hospitals to improve social risk factor data collection, increase reporting of quality metrics stratified by social risk factors to identify disparities, and then actually close gaps in the identified disparities.

- In both FY 2022 and FY 2023, a portion of Michigan’s MCO capitation withhold pay for performance payments (P4P) is based on health equity Healthcare Effectiveness Data and Information Set (HEDIS) measure performance (30%) and performance on shared metrics that address health equity in the care management that MCOs provide in coordination with behavioral health prepaid inpatient health plans (PIHPs) (15%). In FY 2022, there are 10 HEDIS measures that are part of the health equity measures (comparing people of color to the White population).

- New Jersey reported implementing a perinatal episode of care three-year pilot to test a new alternative payment model for prenatal, labor, and postpartum services statewide. The pilot requires participating providers to complete a Health Equity Action Plan and includes reporting of a provider's quality metrics broken down by the member's race/ethnicity.

- Pennsylvania’s MCO P4P program incentivizes reductions in racial disparities for specific quality measures, including rates of hypertension, diabetes, and prenatal care.

Other MCO Health Equity Requirements

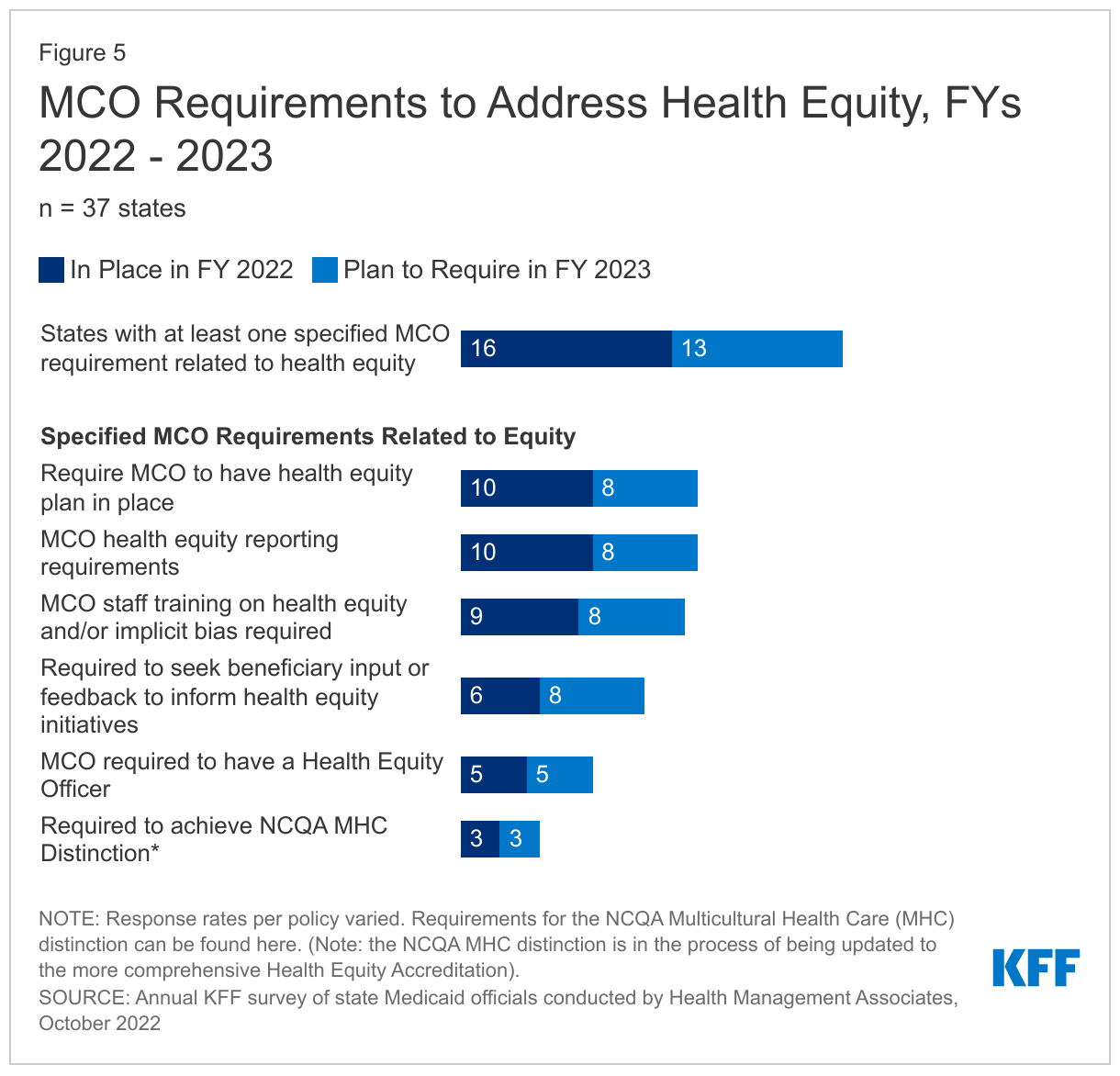

In addition to implementing financial incentives tied to health equity-related performance goals, states can leverage managed care contracts in other ways to promote health equity-related goals. For example, states can require MCOs to achieve national standards for culturally competent care, conduct staff training on health equity and/or implicit bias, develop new positions related to health equity, report racial disparities data, incorporate enrollee feedback, among other requirements. On this year’s survey, we asked states that contract with MCOs about whether certain MCO contract requirements related to health equity were in place in FY 2022 or planned for implementation in FY 2023.

Nearly one-half of responding MCO states (16 of 37) reported at least one specified health equity MCO requirement in place in FY 2022 (Figure 5). In FY 2022, similar numbers of states (about one-quarter) reported requiring MCOs to have a health equity plan in place (10 of 37), meet health equity reporting requirements (10 of 37), and train staff on health equity and/or implicit bias (9 of 37). Fewer states reported requiring MCOs to seek beneficiary input or feedback to inform health equity initiatives (6 of 37), have a health equity officer (5 of 37), and achieve NCQA’s Distinction in Multicultural Health Care (MHC) (3 of 37).48 Among states with at least one requirement in place in FY 2022, half (8 of 16) reported requiring three or more specified initiatives in place (data not shown). The number of MCO states with at least one specified health equity MCO requirement in place is expected to grow significantly in FY 2023, from 16 to 25 states. A few other states reported that though equity-related requirements for MCOs are not planned for FY 2023, they are actively considering or planning to adopt these requirements in the future.

Although states were not asked to describe MCO requirements related to health equity (in place or planned), several states provided additional details including:

- Michigan requires MCOs to implement diversity, equity, and inclusion (DEI) assessment and training programs that are evidence-based and comprehensive. The programs must assess all organizational personnel, policies, and practices and include at least one implicit bias training workshop in 2022 for all personnel. MCOs must also report certain HEDIS measures by race and this data is used by the Department of Health and Human Services in its annual Medicaid Health Equity Project.

- Nevada encourages, but does not require, NCQA MHC distinction as a way of building a strong cultural competency program. Health equity is a component of the required MCO Population Health Program, which must address racial and ethnic disparities, and the required Population Health Program Manager position includes health equity responsibilities. As part of population health program reporting, MCOs must submit an annual population health strategy.

- Oregon requires MCOs to develop a health equity plan and provide updates and progress reports every year. In addition, MCOs must develop a yearly organization-wide training plan on health equity fundamentals which may include training offerings for provider networks. MCOs are also asked to report on training plan progress every year.

Performance Improvement Projects (PIPs) Focused on Health Disparities

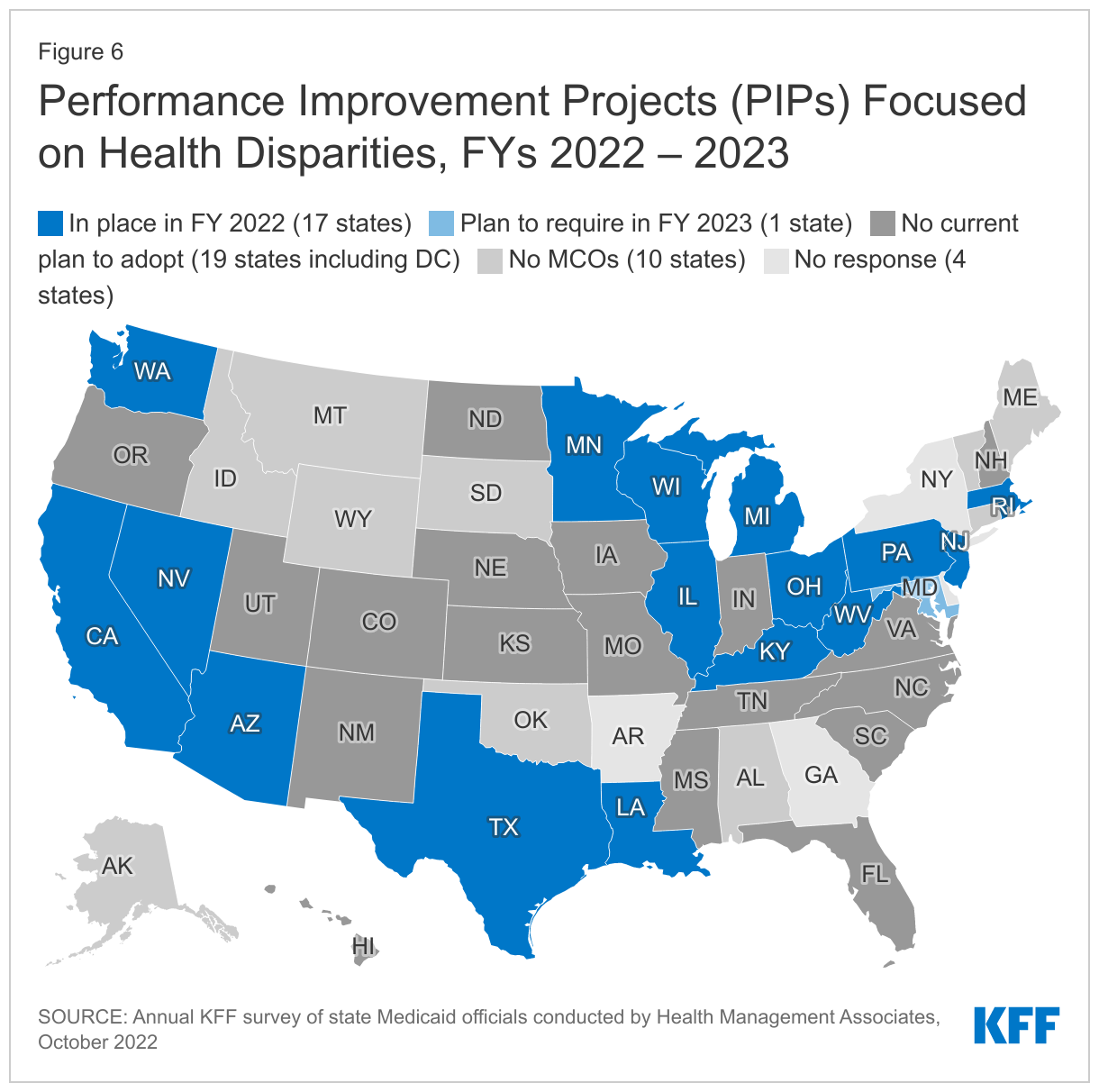

For contracts starting on or after July 1, 2017, federal regulations mandate that states require each MCO or limited benefit prepaid health plan (PHP) to establish and implement an ongoing comprehensive quality assessment and performance improvement (QAPI) program for Medicaid services that includes Performance Improvement Projects (PIPs). PIPs may be designated by CMS, by states, or developed by health plans, but must be designed to achieve significant, sustainable improvement in health outcomes and enrollee satisfaction. On this year’s survey, we asked states if they required MCOs to participate in PIPs focused on health disparities in FY 2022 or planned to in FY 2023.

About half of responding states that contract with MCOs (17 of 37) reported requiring MCOs to participate in PIPs focused on health disparities in FY 2022 (Figure 6). States reported a range of state-mandated PIP focus areas which include an emphasis on reducing disparities / improving health equity including related to:

- Maternal and child health (Illinois, Michigan, Minnesota, Nevada, and Texas)

- Social determinants of health assessment, referral, and follow up (Kentucky)

- Diabetes education and management (Ohio)

- Substance use disorder (SUD) (Pennsylvania)

- Access to culturally and linguistically appropriate services (Wisconsin)

- Lead screening in children (Rhode Island)

Three states (Arizona, Louisiana, and Massachusetts) reported all PIPs must include a health equity component or equity and disparities analysis; two states (California and New Jersey) reported requirements for MCOs to engage in at least one PIP focused on health disparities, and one state (Washington) requires MCOs to collaborate with other MCOs and the state on a statewide PIP addressing health equity. One state (West Virginia) did not specifically describe its health equity-related PIP requirement. One state (Maryland) reported plans to require MCO participation in PIPs focused on prenatal and postpartum care health disparities in FY 2023. While not within the survey period, Mississippi reported that its new MCO contracts, which will become operational in FY 2024, will require MCOs to collaborate with each other and with the state on joint PIPs addressing health disparities identified by the state.

Benefits

Context

State Medicaid programs are statutorily required to cover a core set of “mandatory” benefits, but may choose whether to cover a broad range of optional benefits. States may apply reasonable service limits based on medical necessity or to control utilization, but once covered, services must be “sufficient in amount, duration and scope to reasonably achieve their purpose.”49 State benefit actions are often influenced by prevailing economic conditions: states are more likely to adopt restrictions during downturns and expand or restore benefits as conditions improve. However, during the COVID-19 pandemic, despite an early and deep economic downturn, additional federal funds and the goal to maintain access to needed services resulted in states using Medicaid emergency authorities to temporarily expand or enhance benefits. Similarly, in 2020 and 2021, permanent (i.e., non-emergency) benefit expansions continued to far outweigh benefit restrictions, consistent with prior years.

Recent trends in state changes to Medicaid benefits (both prior to and during the COVID-19 pandemic) include behavioral health service expansions as well as efforts to advance maternal and infant health. New federal legislation and requirements can also affect state Medicaid benefits; for example:

- The American Rescue Plan Act of 2021 included expanded federal funding for home and community-based services (HCBS).50

- The Bipartisan Safer Communities Act of 2022 aimed to improve and expand provision of the Medicaid EPSDT benefit and school-based Medicaid services by providing updated guidance for states. The Act also allocated grant funding for states to expand school-based Medicaid services.51

- The Inflation Reduction Act of 2022 requires Medicaid coverage of all adult vaccines recommended by the Advisory Committee on Immunization Practices (ACIP) without cost-sharing, beginning in 2023.52

- In July 2022, the federally mandated crisis number, 988, became available to all landline and cell phone users, per the National Suicide Hotline Designation Act of 2020.53 988 provides a single three-digit number to access a network of over 200 local and state funded crisis centers. State Medicaid programs may participate in financing of services provided through 988.

- The Consolidated Appropriations Act of 2021 requires states to cover routine patient costs associated with participation in qualifying clinical trials, beginning January 1, 2022.54

This section provides information about:

- Non-emergency benefit changes

- Clinical trial participation coverage

- In lieu of services

Findings

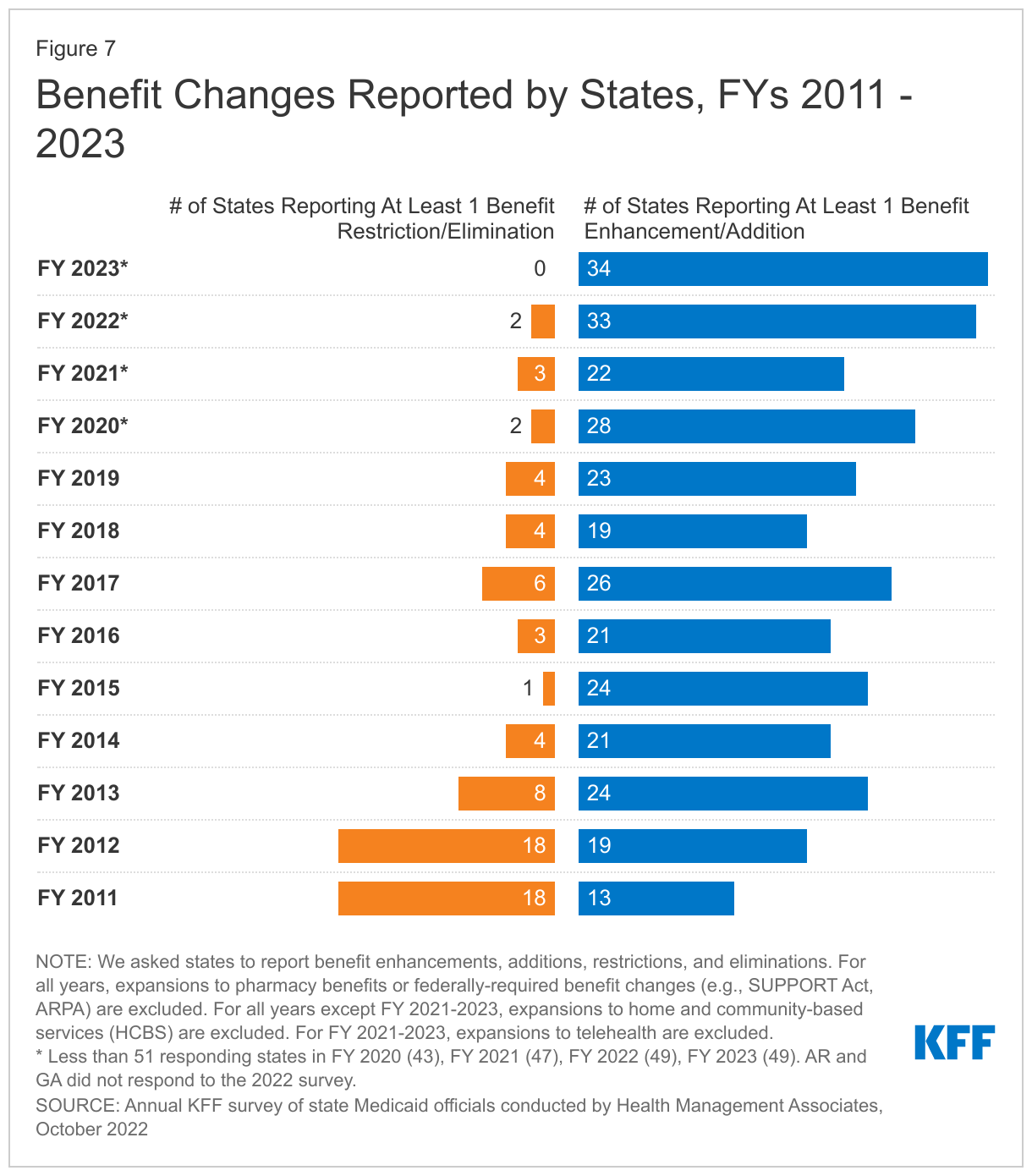

Non-Emergency Benefit Changes

We asked states about non-emergency benefit changes implemented during FY 2022 or planned for FY 2023, excluding telehealth, pharmacy, and temporary changes adopted via emergency authorities in response to the COVID-19 pandemic but including emergency changes that have or will become permanent (i.e., transitioned to traditional, non-emergency authorities). Benefit changes may be planned at the direction of state legislatures and may require CMS approval.

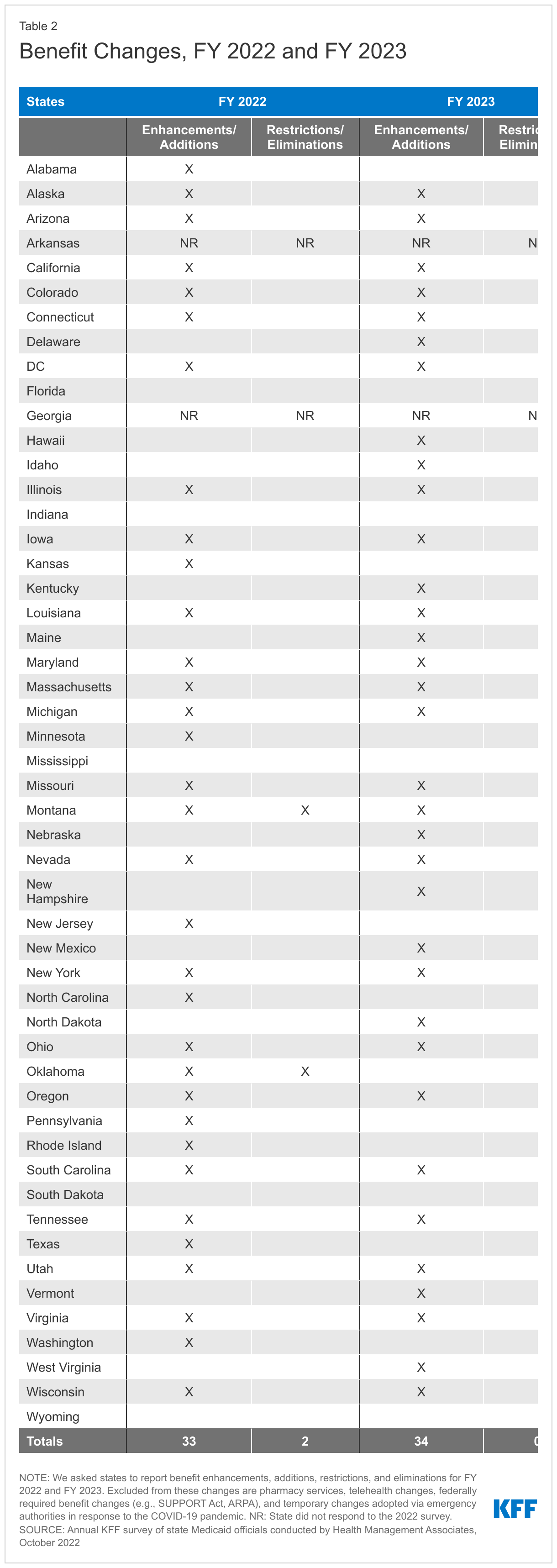

The number of states reporting new benefits and benefit enhancements greatly outpaces the number of states reporting benefit cuts and limitations (Figure 7 and Table 2). Thirty-three states reported new or enhanced benefits in FY 2022 and 34 states are adding or enhancing benefits in FY 2023.55 Two states reported benefit cuts or limitations in FY 2022 and no states reported cuts or limitations in FY 2023. We provide additional details about several benefit categories below (Exhibit 4). In addition to these benefit categories, several states reported updated and expanded benefits in HCBS waivers (which may be reflected in other categories below); such expansions may take advantage of enhanced ARPA HCBS funding.

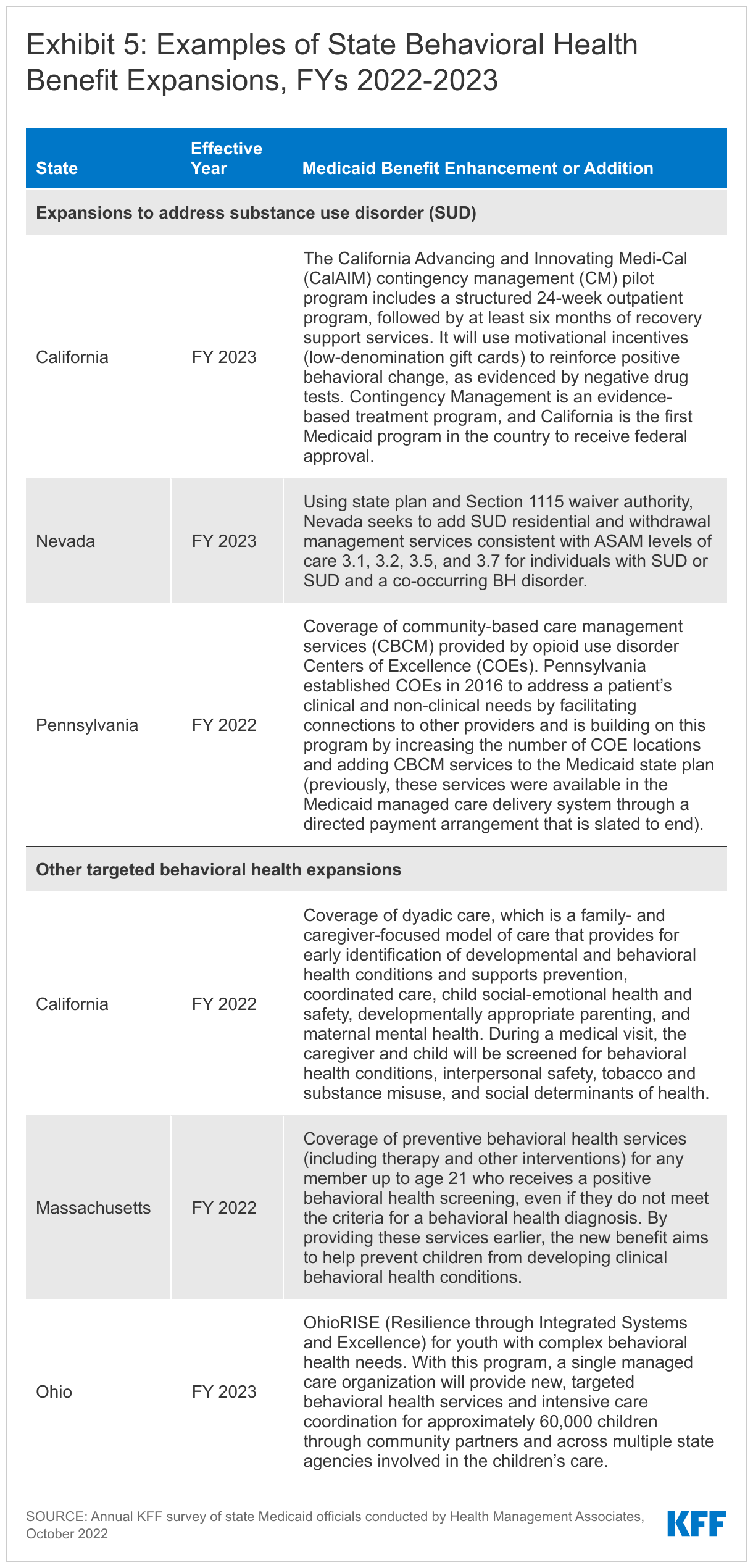

Behavioral Health ServicesStates continue to focus on behavioral health through the introduction of new and expanded mental health and/or substance use disorder (SUD) services in FY 2022 and FY 2023. States reported service expansions across the behavioral health care continuum, including institutional, intensive, outpatient, home and community-based, and crisis services (see Exhibit 5 for state examples). Many of these benefit expansions are targeted to specific populations, including notable expansions and programming for youth. A number of states reported benefits aimed to improve the integration of physical and behavioral health care, including adoption of Certified Community Behavioral Health Clinics (CCBHCs)56 or the Collaborative Care model (CoCM).57 State approaches to addressing SUD outcomes include coverage of opioid treatment programs, peer supports, and enhanced care management. At least ten states are expanding coverage of crisis services, which aim to connect Medicaid enrollees experiencing behavioral health crises to appropriate community-based care.58 These include mobile crisis response services and crisis stabilization centers. In many states, crisis service expansions require coordination with state behavioral health agencies, including related to the implementation and funding of the new national 988 crisis number.

Pregnancy and Postpartum ServicesStates continue to expand and transform care for pregnant and postpartum individuals to improve maternal health and birth outcomes. In April 2022, a temporary option to extend Medicaid postpartum coverage from 60 days to 12 months took effect. This option, included in the American Rescue Plan Act, is part of broader federal and state efforts to improve maternal and infant health outcomes and address racial/ethnic health disparities. Alongside this eligibility change, some states are enhancing Medicaid services available during the postpartum period. Additionally, nine states are adding coverage of services provided by doulas (California, District of Columbia, Illinois, Maryland, Michigan, New Mexico, Nevada, Rhode Island, and Virginia). Doulas are trained professionals who provide holistic support to individuals before, during, and shortly after childbirth. Seven states are investing in the implementation or expansion of home visiting programs to teach positive parenting and other skills aimed at keeping children healthy and promoting self-sufficiency (Alabama, Delaware, Illinois, Maryland, Ohio, Oregon, and Vermont). Other examples of expanded pregnancy and postpartum services include:

- In FY 2023, Illinois plans to expand services available during the postpartum period to include those provided by certified lactation counselors and consultants, public health nurses, and medical caseworkers.

- In FY 2022, Washington implemented a Newborn Administrative Day Rate to cover hospital stays up to five days for a postpartum parent who has been medically discharged, but whose newborn remains inpatient due to monitoring for neonatal abstinence syndrome (NAS) or neonatal opioid withdrawal syndrome (NOWS). The rate will provide daily reimbursement to help offset hospital costs of providing these postpartum parents with room and board and limited additional services centered on the care and well-being of the newborn, including medications to treat SUD.59

- In FY 2023, West Virginia plans to implement its Drug Free Moms and Babies (DFMB) Program (previously a pilot project), an integrated comprehensive medical and behavioral health program for pregnant and postpartum individuals with SUD that provides a targeted case management benefit.60

- In FY 2023, Maine and Maryland are expanding their Maternal Opioid Misuse (MOM) Models, a Center for Medicare and Medicaid Innovation (CMMI) initiative for pregnant and postpartum women with opioid use disorder.

Preventive ServicesSixteen states reported expansions of preventive care in FY 2022 or FY 2023. Preventive care—including immunizations and regular screenings that permit early detection, treatment, and improved management of chronic conditions—improves the prospects for better health outcomes. States must cover certain preventive services for adults newly eligible under the ACA’s Medicaid expansion, but this coverage is not required for “traditional” Medicaid adults. (In contrast, states are required to provide comprehensive preventive care to children through the EPSDT benefit.) States reported enhancing a range of preventive benefits, especially for adult enrollees, in FY 2022 and FY 2023. For example, seven states are expanding services to prevent and/or manage diabetes, such as continuous glucose monitoring.61 Other reported preventive benefit enhancements relate to asthma services, vaccinations, and genetic testing and/or counseling.

Services Targeting Social Determinants of HealthMany states reported new and expanded benefits related to enrollees’ social needs. Social determinants of health (SDOH) are the conditions in which people are born, grow, live, work, and age that shape health; these include but are not limited to housing, food, education, employment, healthy behaviors, transportation, and personal safety. Generally, states have not been able to use federal Medicaid funds to pay the direct costs of non-medical services like housing and food.62 However, within Medicaid, states can use a range of state plan and waiver authorities to add certain non-clinical services to the Medicaid benefit package. Historically, non-medical services have been included as part of Medicaid HCBS programs for people who need help with self-care or household activities as a result of disability or chronic illness, and states have more limited flexibility to address SDOH outside of Medicaid HCBS authorities. CMS released guidance for states about opportunities to use Medicaid and CHIP to address SDOH in January 2021. In December 2021, CMS approved a California proposal to use “in lieu of” services (ILOS) to offer a menu of health-related services through managed care, and further guidance from CMS on the ILOS regulation is expected (also see ILOS section below).

In FY 2022 and/or 2023, twelve states reported new or expanded housing-related supports, as well as other services and programs tailored for individuals experiencing homelessness or at risk of being homeless.63 Some states reported enhancing benefits that target the social needs of enrollees receiving HCBS, such as home-delivered meals or supported employment. Examples of expanded services targeting SDOH include:

- California’s CalAIM initiative, which launched in January 2022, seeks to take the state’s whole person care approach statewide, with a central focus on improving health and reducing health disparities and inequities. Under CalAIM, Medi-Cal managed care plans will provide Enhanced Care Management (ECM) and Community Supports to targeted high-need beneficiaries.64 The new ECM benefit includes care coordination and comprehensive care management services to address clinical, behavioral, and social needs. Community Supports will address social drivers of health; examples include housing navigation services, recuperative care (medical respite), short-term post hospitalization housing services (up to six months), environmental accessibility adaptations, medically tailored meals, and sobering centers (also see ILOS section below).65

- Recently approved Section 1115 waivers in Arizona, Massachusetts, and Oregon allow the states to provide evidence-based health-related social needs (HRSN) services to certain high-need enrollees, when clinically appropriate, to address food insecurity and/or housing instability. HRSN services vary by state and include housing supports (such as eviction prevention, security deposits, housing transition navigation services, and medically necessary home modifications); short-term post-transition rent/temporary housing for up to six months (in Arizona and Oregon only); case management and linkages to other benefit programs; and nutrition supports (such as nutrition counseling and education, time-limited food assistance, and medically tailored meals) (in Massachusetts and Oregon only). Enrollees must meet health and risk criteria (which vary by state) to be eligible for HRSN services. For example, target populations include homelessness or risk of homelessness, justice-involvement, and behavioral health needs/diagnoses.66

- In FY 2022, Connecticut implemented its Connecticut Housing Engagement and Support Services (CHESS) initiative that provides eligible enrollees with supportive housing benefits under Medicaid, coordinated with Medicaid services and non-Medicaid housing subsidies.67 Beginning July 1, 2022, Connecticut is also covering Community Violence Prevention Services to promote improved outcomes, prevent injury, reduce recidivism, and decrease the likelihood that victims of violence will commit violence themselves.68

- If approved by CMS, in FY 2023 Wisconsin plans to establish a new Section 1915(i) HCBS eligibility group of adults with certain health conditions who are experiencing homelessness and will provide these enrollees with housing support services such as housing consultation, housing transition and sustaining supports, and relocation supports.69

- Two states (Oregon and Wisconsin) reported coverage for interpretation services for enrollees with limited English proficiency (LEP). All Medicaid providers are obligated to make language services available to those with LEP; states are permitted but not required to reimburse providers for the cost of these services. Both Oregon and Wisconsin are adding reimbursement for the cost of ensuring access to interpreters in conjunction with a Medicaid-covered service.

Dental ServicesStates aim to improve oral health by expanding covered dental benefits and extending coverage to new populations. Nine states are adding comprehensive adult dental coverage,70 while additional states report expanding specific dental services for adults. Several states expanded dental services for certain populations, including pregnant individuals or people with disabilities. For example, in FY 2023, Nevada proposes to offer a limited dental benefit to adults with diabetes to address their unmet oral health needs, improve health outcomes, and lower overall costs for a population at higher risk for periodontal disease.71 A few states are adding or expanding coverage of fluoride, including three states that are adding coverage of Silver Diamine Fluoride (SDF).72 SDF is a topical agent that can be used to halt the development of cavities in children and adults.73

Just two states reported benefit restrictions in FY 2022 and no states reported such restrictions planned for FY 2023. Benefit restrictions reflect the elimination of a covered benefit, benefit caps, or the application of utilization controls such as prior authorization for existing benefits. In FY 2022, Montana eliminated its Nurse Advice Line and Oklahoma eliminated its behavioral health ACA Health Home initiative. In both states, however, public documents suggest enrollees will continue to have access to similar services. For example, Montana acknowledged increased availability of telehealth in its state plan amendment to eliminate its Nurse Advice Line.74 In Oklahoma, the Health Home population will continue to receive integrated services provided by Community Mental Health Centers (CMHCs) and through Certified Community Behavioral Health (CCBH) service delivery, as well as other care coordination models, with most Health Home providers transitioning to the CCBH model.75

Clinical Trial Participation Coverage

Historically, state Medicaid programs were not required to cover costs associated with participation in clinical trials, even if such costs were for services that Medicaid would ordinarily cover. However, as documented in a State Medicaid Director letter, the Consolidated Appropriations Act of 2021 requires states to cover routine patient costs associated with participation in qualifying clinical trials beginning January 1, 2022. These costs include any item or service (such as physician, laboratory, or medical imaging services) provided to the individual under the qualifying clinical trial that would otherwise be covered under the Medicaid state plan or Section 1115 waiver.76

Most states reported coverage of routine patient costs associated with participation in qualifying clinical trials prior to the new federal requirement. Thirty-three states (of 47 responding) indicated that at least some of these costs were covered prior to the requirement’s effective date of January 1, 2022. About one-quarter of all responding states noted operational challenges and other concerns. These included having to expand the benefit to cover additional costs (e.g., transportation and/or out-of-state coverage), increased administrative burden (e.g., new provider attestation requirements and/or the 72-hour coverage determination timeframe), and regulatory efforts (e.g., legislation, rulemaking, and/or provider manual updates needed). A small number of states reported other challenges, including difficulty identifying eligible populations and provider education and outreach needed to ensure awareness.

In Lieu of Services

States use a combination of fee-for-service and managed care arrangements to deliver care to Medicaid beneficiaries, with many services increasingly being provided by managed care organizations (MCOs). Under federal Medicaid regulations, states may allow MCOs the option to offer services or settings that substitute for those that are covered under the state plan, so long as the substitute service is determined to be medically appropriate and cost-effective.77 If an MCO opts to offer in lieu of services (ILOS), the services must be identified in the MCO contract and enrollees may not be required to use them.78 In recent years, states have increasingly used MCO “in lieu of” authority to cover services provided to nonelderly adults in “institutions for mental disease” (IMDs) that otherwise would be ineligible for federal Medicaid funding. The 2018 SUPPORT Act codified the existing Medicaid managed care regulation allowing capitation payments to include IMD services up to 15 days per month using “in lieu of” authority.

Most states reported allowing MCOs to use “in lieu of” authority to cover certain services, especially behavioral health services and services to address SDOH. Thirty-four of 39 responding MCO states indicated permitting at least one ILOS as of July 1, 2021; nearly all of these states reported that the permitted ILOS included certain behavioral health services. By far, the most commonly cited ILOS was services provided to nonelderly adults in IMDs, which are otherwise ineligible for Medicaid funding except through in lieu of or waiver authority. Some states mentioned other approved behavioral health services (including mental health and SUD services), such as mobile crisis and crisis stabilization services, outpatient treatment in lieu of hospitalization, and group or peer supports. Nearly one-third of states permitting ILOS reported that allowable ILOS include services to address SDOH, such as food and housing needs. For example, California’s Community Supports ILOS package builds on the state’s experience with Whole Person Care Pilots and includes housing transition navigation services, environmental accessibility adaptations (home modifications), asthma remediation, medically tailored meals, and sobering centers.79 Following the CMS approval of California’s Community Supports, guidance from CMS on the ILOS regulation is expected. Approximately one-quarter of states that permit ILOS reported leveraging this authority to provide coverage of HCBS, such as adult day care, homemaker services, and covered HCBS services in excess of established limits. At least one state acknowledged MCOs have been slow to take advantage of their optional ILOS authority, particularly for SDOH-related services, and the state will be evaluating updated approaches to ensure coverage in the future.

Telehealth

Context

Telehealth can be an important component of facilitating access to care for Medicaid enrollees during and beyond the COVID-19 pandemic. States have broad authority to cover telehealth in Medicaid without federal approval, including flexibilities for allowable populations, services and payment rates, providers, technology, and managed care requirements. Prior to the pandemic, the use of telehealth in Medicaid was becoming more common. However, while all states had some form of Medicaid telehealth coverage, policies regarding allowable services, providers, and originating sites varied widely;80 further, Medicaid telehealth payment policies were unclear in many states.81 To increase health care access and limit risk of viral exposure during the pandemic, all 50 states and DC expanded coverage and/or access to telehealth services in Medicaid. For example, states expanded the range of services that can be delivered via telehealth; established payment parity with face-to-face visits; expanded permitted telehealth modalities; and broadened the provider types that may be reimbursed for telehealth services. As of July 2021, most states reported covering a range of services delivered via audio-visual and audio-only telehealth in their Medicaid fee-for-service (FFS) and managed care programs.

These telehealth expansions contributed to substantial growth in Medicaid and CHIP services delivered via telehealth during the public health emergency (PHE).82 However, telehealth access may not be equally available to all enrollees. For example, research indicates that video telehealth rates have been lowest among Black, Asian, and Hispanic individuals, potentially due to more limited internet or computer access—leading researchers to conclude that “policy efforts to ensure equitable access to telehealth, in particular video-enabled telehealth, are needed to ensure that disparities that emerged during the pandemic do not become permanent.” Similarly, while telehealth has the potential to facilitate access to care for Medicaid enrollees in rural areas with fewer provider and hospital resources,83 inadequate and/or unaffordable broadband access can be a barrier. Research suggests that telehealth utilization during the pandemic has been lower for rural Medicaid enrollees versus those living in urban areas.84

This section provides information about:

- Telehealth policy adopted in response to COVID-19 (audio-only coverage)

- Telehealth utilization trends during the pandemic

- Telehealth quality and other challenges

- Permanent telehealth policy changes and key issues to watch

Findings

Telehealth POLICY ADOPTED IN RESPONSE TO COVID-19

To increase health care access and limit risk of viral exposure during the pandemic, all 50 states and DC expanded coverage and/or access to telehealth services in Medicaid. Because states previously reported somewhat less coverage of audio-only telehealth and indicated that continued coverage of this modality was under consideration, on this year’s survey we asked states to report prior changes to and current coverage of audio-only telehealth.

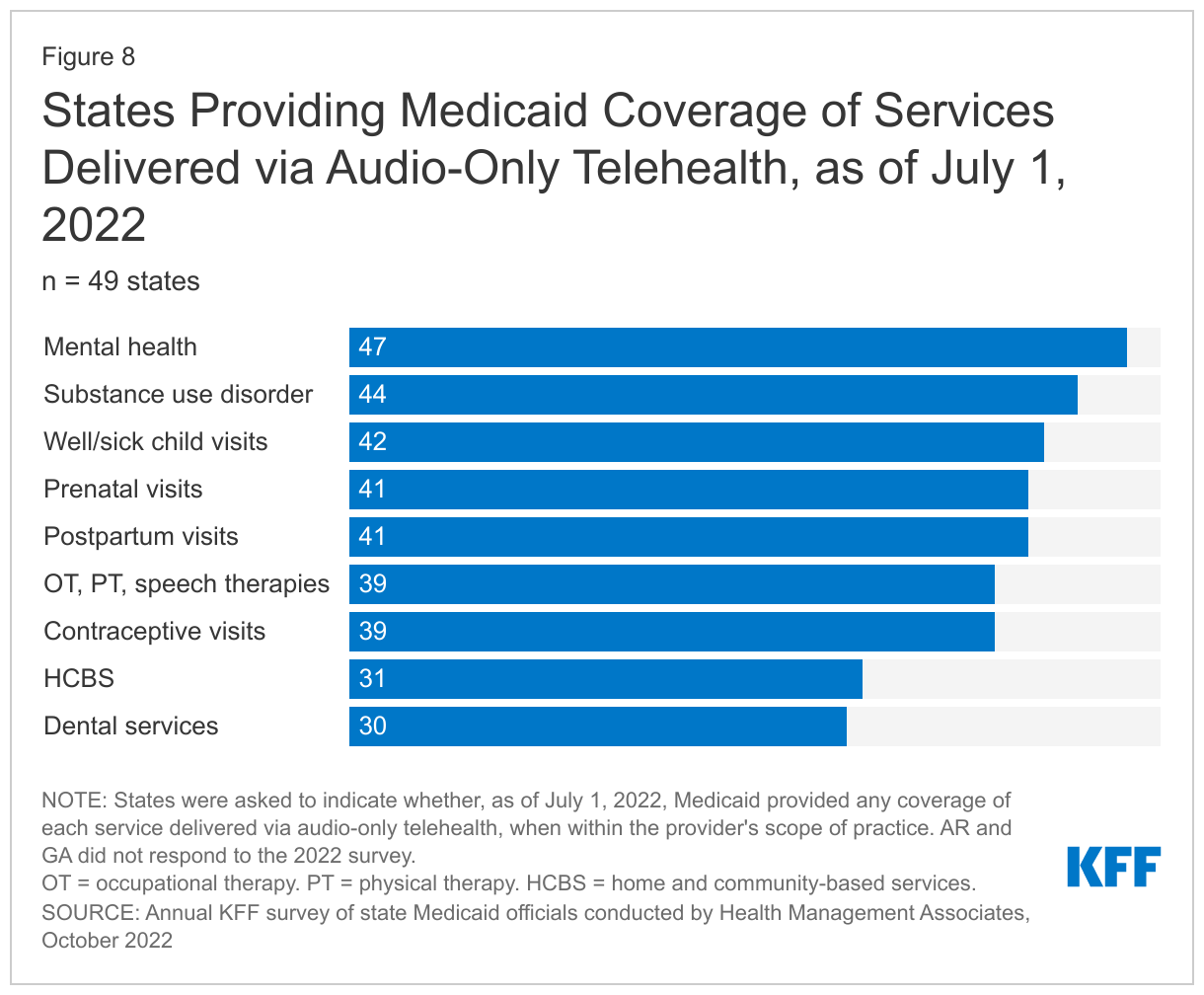

Nearly all responding states added or expanded audio-only telehealth coverage in Medicaid in response to the COVID-19 pandemic. Twenty-eight states reported that they newly added audio-only coverage (i.e., had no audio-only Medicaid coverage prior to the pandemic) while 19 states expanded existing coverage.85 We also asked states to indicate whether, as of July 1, 2022, Medicaid provided any coverage of specified services delivered via audio-only telehealth, when within the provider’s scope of practice. For each service type, a majority of states reported providing audio-only coverage (at least sometimes) (Figure 8). In particular, nearly all states reported audio-only coverage of mental health and substance use disorder (SUD) services. States least frequently reported audio-only coverage of home and community-based services (HCBS) and dental services. Two states (Mississippi and Wyoming) reported no coverage of audio-only telehealth for the services in question.

Telehealth Utilization Trends

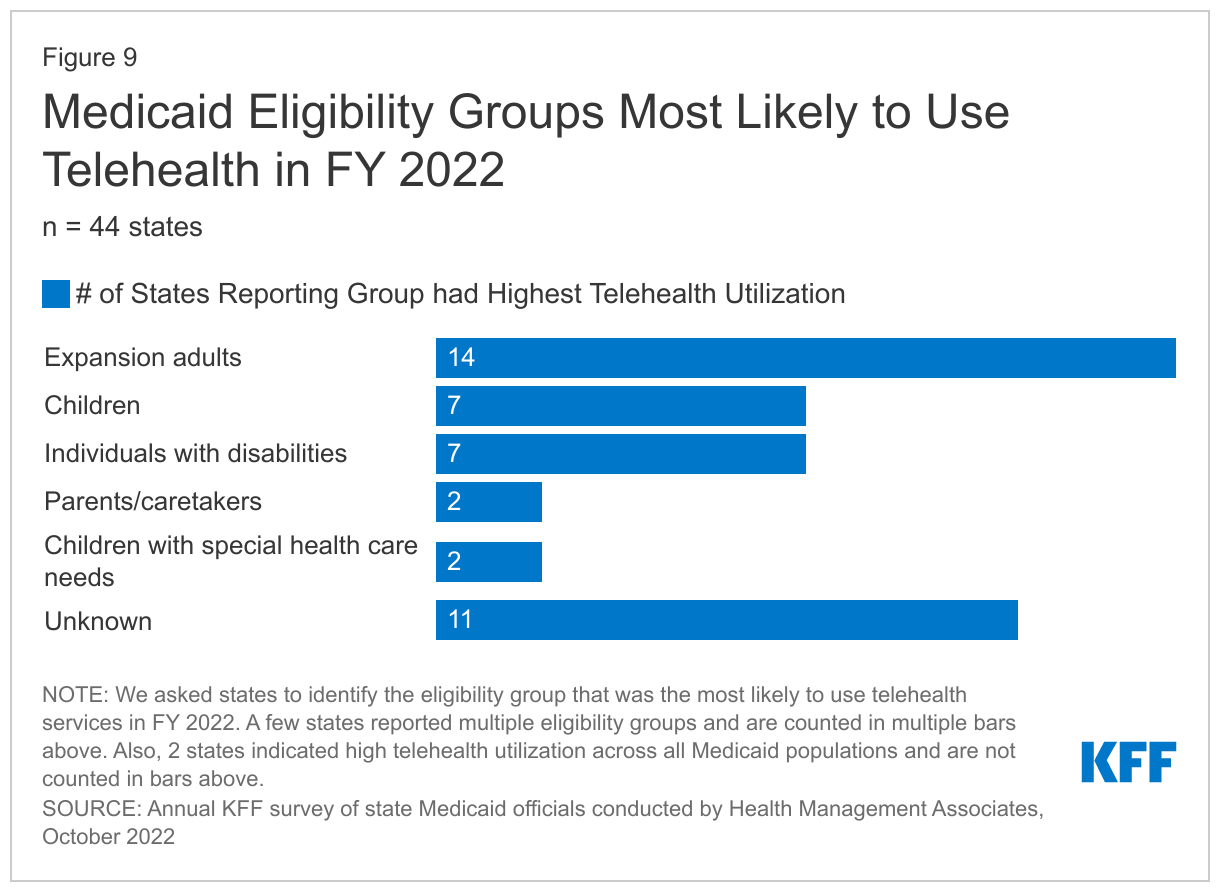

To better understand the impacts of telehealth policy changes during the pandemic, we asked states to report notable trends in Medicaid telehealth utilization in FY 2022 or anticipated for FY 2023. Notable trends reported included telehealth utilization over time, top services with high or increased telehealth utilization, and populations most likely to use telehealth.