Experience of the Five Largest Publicly Traded Companies Operating Medicaid Managed Care Plans During Unwinding

Note: For the latest data on the experiences of the five largest publicly traded companies, view our 2025 brief

At the start of the “unwinding” period, in April 2023, Medicaid enrollment peaked at 94.5 million, an increase of 23 million or 32% from before the pandemic. As of December 2023, Medicaid enrollment declined by more than 9% across states, a decline of over 9 million people. The Centers for Medicare and Medicaid Services (CMS) continues to highlight the role managed care organizations (MCOs) can play in helping people eligible for Medicaid use and keep their coverage, as nearly three-quarters of Medicaid beneficiaries are enrolled in a managed care plan. This brief takes a closer look at the five largest publicly traded companies (also referred to as “parent” firms) operating Medicaid MCOs, which account for half of Medicaid MCO enrollment nationally. This analysis presents the latest parent firm enrollment and financial data (through the end of CY 2023) as well as key takeaways from the firms’ unwinding experience. Information and data reported in this brief come from quarterly company earnings reports and calls, financial filings and other company materials as well as from national administrative data. Key takeaways include:

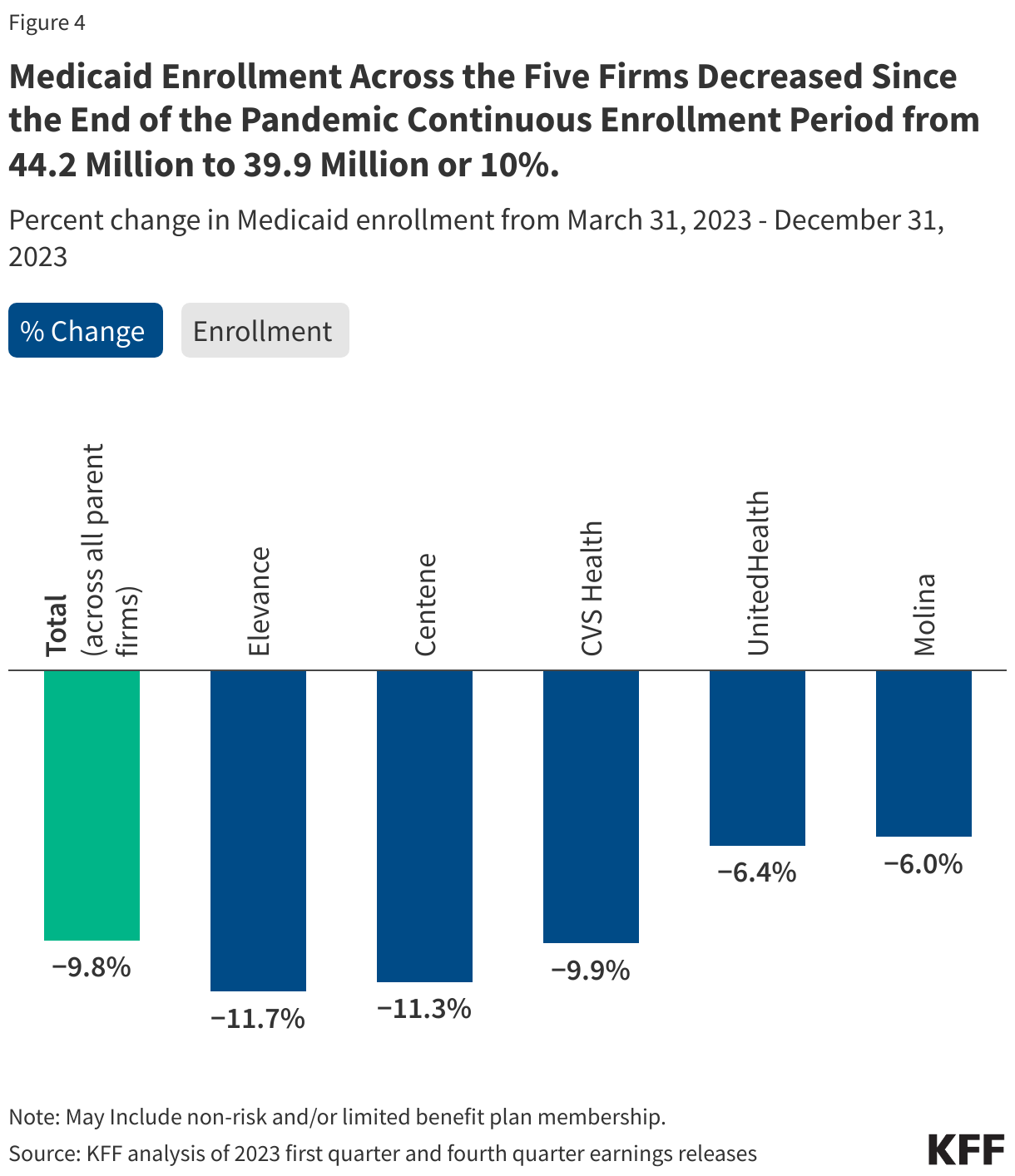

- Medicaid Enrollment. From March 2023 to December 2023, Medicaid enrollment declined by nearly 10% across the five firms, tracking the rate of decline seen nationally.

- Medicaid Revenue. Although firms saw a 10% decline in Medicaid enrollment as of the end of 2023, the firms that report Medicaid-specific revenue information reported year-over-year (2023 over 2022) growth in Medicaid revenue ranging from 3% to 18%.

- Unwinding Impacts. In earnings calls, firms have discussed the impacts of unwinding, including high procedural disenrollment rates of 70% or above and gaps in member coverage that can extend for several months. Several firms reported states have been making mid-cycle and retrospective rate adjustments to account for the impact of redeterminations on the average risk profile (or “acuity”) of members who remain enrolled.

Medicaid enrollment in the five largest publicly traded companies operating Medicaid MCOs

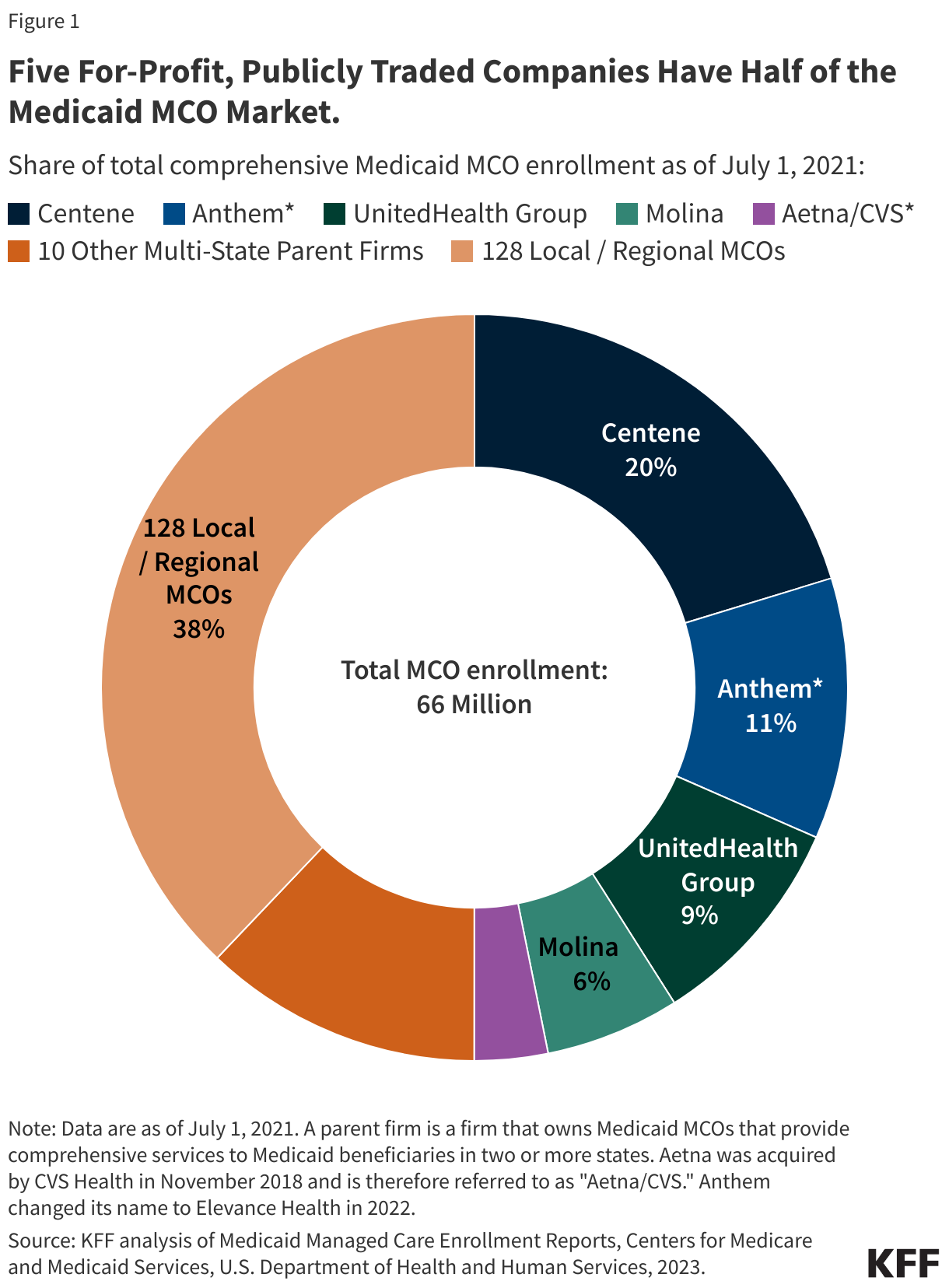

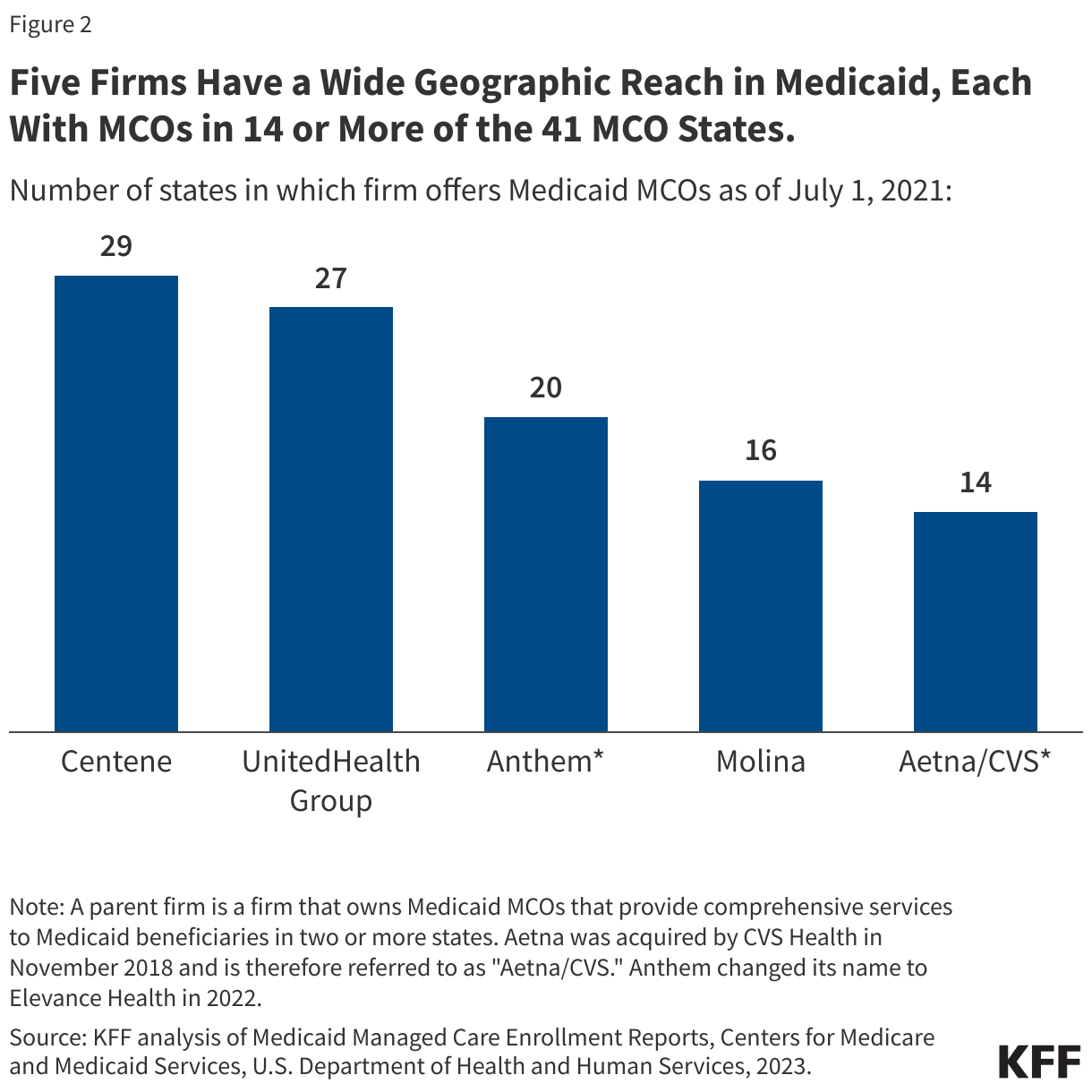

Five for-profit, publicly traded companies – Centene, Elevance (formerly Anthem), UnitedHealth Group, Molina and CVS Health – account for 50% of Medicaid MCO enrollment nationally (Figure 1). All five are ranked in the Fortune 500, and four are ranked in the top 100, with total revenues that ranged from $34 billion (Molina) to $372 billion (UnitedHealth Group) for 2023. Each company operates Medicaid MCOs in 14 or more states (Figure 2).

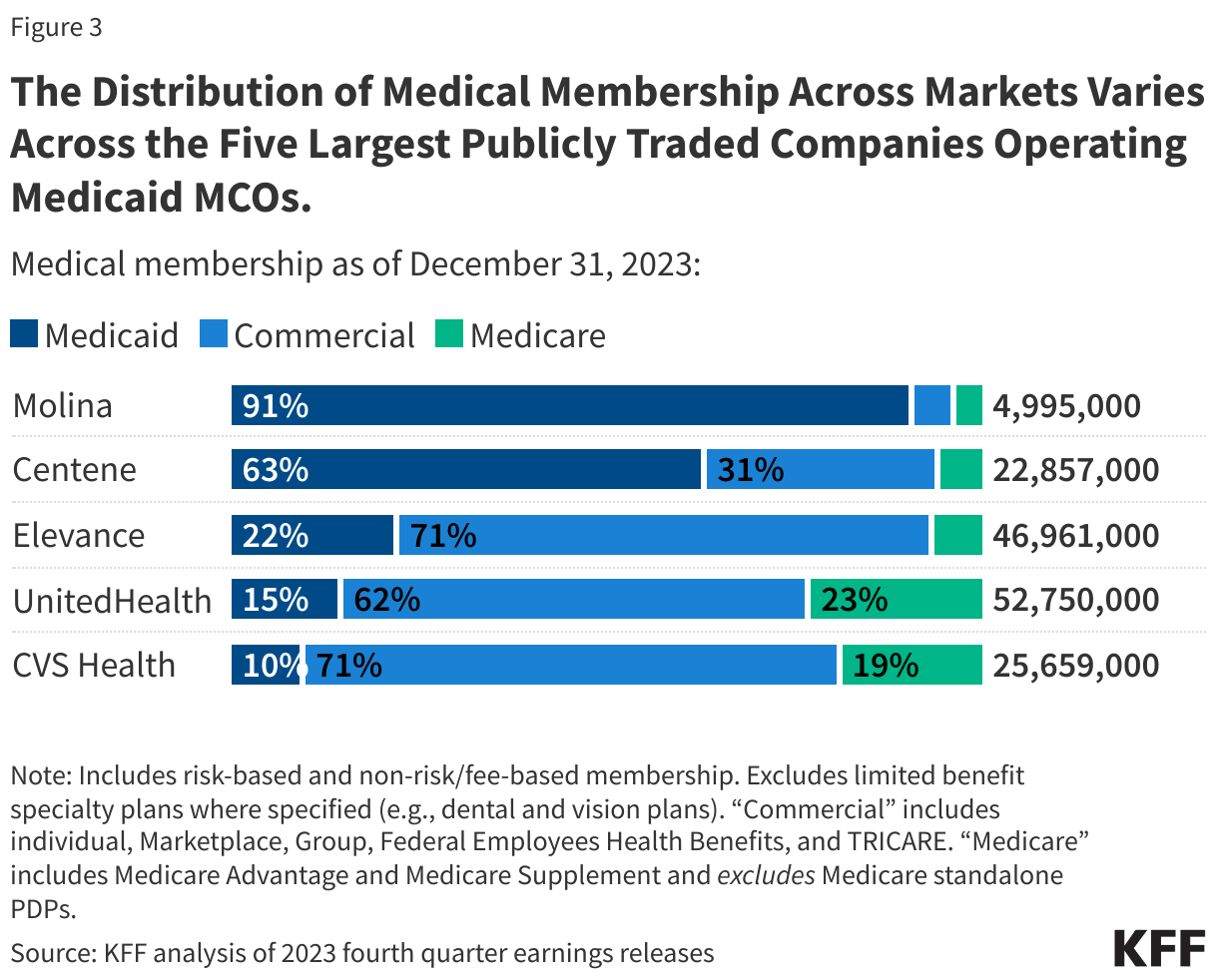

All five firms also operate in the commercial and Medicare markets (Figure 3); however, the distribution of membership across markets varies across firms. Two firms – Molina and Centene – have historically focused predominantly on the Medicaid market. Medicaid members accounted for over 90% of Molina’s overall medical membership and nearly 65% of Centene’s medical membership as of December 2023 (Figure 3). Since the start of unwinding, Medicaid membership as a share of total medical membership has declined for all five firms. The unwinding may be contributing to membership distribution shifts.

Combined Medicaid enrollment across the five firms decreased by 4.3 million or 9.8% from March 2023 to December 2023 (Figure 4). Similar to the enrollment decline experienced by the five parent firms, national data show total Medicaid/CHIP enrollment declined by more than 9% from March 2023 to December 2023. Changes in “net” enrollment reflect the people who are dropped from Medicaid as well as those who newly enroll, and those who re-enroll within a short timeframe following disenrollment, also known as “churn.” Changes in parent firm enrollment may reflect activity including firm acquisitions or sales and new or lost Medicaid contracts. Although Medicaid enrollment has declined across parent firms since the start of the unwinding, the three firms that report Medicaid-specific revenue information (UnitedHealth, Molina, and Centene) reported year-over-year (2023 over 2022) growth in Medicaid revenue (18%, 6%, and 3%, respectively). Molina reported the medical margin earned by the Medicaid segment was $3.0 billion in 2023 (medical margin = premium revenue – medical costs). Since enrollment declines escalated throughout 2023, it’s possible that the Medicaid revenue picture for these firms could get worse in the coming months. However, it’s also possible that insurers have been able to maintain Medicaid revenues in spite of enrollment declines in part through retrospective rate adjustments.

Impact of unwinding for the five largest publicly traded companies operating Medicaid MCOs

All five firms report monitoring the impact of unwinding, including disenrollment, “churn”, coverage transitions, gaps in coverage, and changes in member acuity. Key highlights from Q2 – Q4 2023 earnings calls include:

- Procedural Disenrollment. In earnings calls since the start of the unwinding, firms have reported procedural disenrollments make up a large percentage of their total disenrollments. Firms that provided estimates reported procedural disenrollment rates of 70% or above. Procedural disenrollments occur when an enrollee is unable to complete the renewal process. Elevance reported that disenrolled members are facing barriers to renewal, including awareness of the process and actions required to maintain coverage. In Q3 2023, Elevance reported that nearly 40% of their Medicaid members procedurally disenrolled were children/youth (under age 18). KFF tracking shows, overall, about 70% of disenrollments so far have been “procedural,” but the rate varies substantially across states. Many strategies are available to states to minimize procedural terminations, including temporary waivers that allow states to obtain updated enrollee contact information from MCOs, permit MCOs to assist enrollees in completing certain parts of renewal forms, and extend automatic reenrollment into an MCO plan from the standard 60 days up to 120 days.

- “Churn”. According to firm monitoring, some individuals who have been disenrolled are reenrolling in Medicaid coverage. Firms report continuing with outreach efforts to help people retain or regain their Medicaid coverage or find other affordable coverage. Of the firms that shared this information, Medicaid reenrollment rates ranged from 20-30%. Centene noted that CMS action requiring states to reinstate coverage due to systems issues has impacted reenrollment rates.

- Coverage Transitions. Firms are also monitoring transitions to coverage through the Affordable Care Act (ACA) Marketplace. All five firms offer a Marketplace plan in many states where they operate a Medicaid MCO, however, there may not be plan alignment if plans operate regionally. Centene reported 10-15% of members disenrolled from Medicaid transitioned to their Marketplace product. Other firms have not provided specific Marketplace transition rates/estimates but note one driver of Marketplace growth has been Medicaid redeterminations. Some individuals eligible for coverage in the Marketplace (which has higher income eligibility thresholds than Medicaid) qualify for plans with zero premiums; however, Medicaid may provide more comprehensive benefits and lower cost-sharing compared to Marketplace coverage. Recent data show that Marketplace signups have reached 21.3 million people, exceeding last year’s record high by another 5 million people. Medicaid unwinding is only one factor contributing to that growth – which is being driven in large part by enhanced premium subsidies – and a relatively small share of people disenrolled from Medicaid are transitioning to Marketplace or Basic Health Plan coverage.

- Gaps in Coverage. Some enrollees are experiencing gaps in coverage that, according to some firms, can extend for multiple months. This is consistent with a pre-pandemic analysis of national survey data that show two-thirds of enrollees experience a period of uninsurance in the 12 months following Medicaid disenrollment. In focus groups conducted by KFF in September 2023 with Medicaid enrollees who recently completed the renewal process, several participants who were disenrolled reported facing substantial out-of-pocket costs for medically necessary care during gaps in coverage. Focus group participants also reported needing one-on-one assistance from caseworkers and community-based organizations to help them regain Medicaid coverage.

- Member Acuity. In earnings calls, several firms reported states have been making mid-cycle and retrospective rate adjustments to account for the impact of redeterminations on average member acuity (i.e., health status, which can affect use of services and drugs). Although states may have built enrollment and acuity change assumptions into capitation rates (for 2023 and 2024), states and plans faced considerable uncertainty at the start of the unwinding–understanding that while membership losses would become immediately apparent, new utilization and acuity trends would take longer to discern. Prior to the start of unwinding, plans reported expecting the overall risk profile of members to increase, as they anticipated “stayers” would be sicker than “leavers.” At least one firm noted continued effects of risk corridors (where states and plans agree to share profit or losses) from earlier contract years, requiring plan payback.

Looking Ahead

As of December 2023 (timeframe for this analysis), states were nine months into the unwinding of the Medicaid continuous enrollment provision. It is highly uncertain what national Medicaid enrollment will be at the end of unwinding. Focus groups with enrollees revealed that while many have been able to successfully renew Medicaid coverage, many have been disenrolled due to confusion and barriers to completing the renewal process. While many individuals who are disenrolled may “churn” back to Medicaid or transition to other coverage, unwinding will likely contribute to increases in the number of people who are uninsured. People who are uninsured face more barriers to care, go without needed care, and may experience higher out of pocket costs and medical debt. Changes in the uninsured will depend on whether individuals who are no longer eligible and are disenrolled from Medicaid transition to other coverage, including employer plans and the Marketplace. Medicaid managed care plans have a financial interest in maintaining enrollment in Medicaid and facilitating transitions to the Marketplace (and other products). The five publicly traded firms that are the subject of this analysis account for about half of all Medicaid MCO enrollment nationally. Medicaid managed care plans can continue to assist state Medicaid agencies in communicating with enrollees, conducting outreach and renewal assistance, and in facilitating transitions to Marketplace coverage. Quarterly earnings reports and calls can provide further insight into the impact of the unwinding on Medicaid enrollees, including disenrollments, gaps in coverage and transitions to the Marketplace.