Millions of Uninsured People Can Get Free ACA Plans

The opportunity to enroll in Affordable Care Act (ACA) plans is soon ending for most people needing Marketplace coverage in 2023. People in need of private ACA health plans must sign up for coverage during the open enrollment season, which closes on January 15 in most states. After that, only limited circumstances, such as loss of coverage or very low income, will qualify potential enrollees for a special enrollment period.

Despite most uninsured people being eligible for some form of assistance, either through Medicaid or ACA subsidies, 28 million people remained uninsured in 2021. Many uninsured people do not even shop for health coverage, often because of perceptions of high costs.In reality, though, millions of uninsured people are eligible for free plans. We previously estimated that almost half of uninsured people could get health coverage for free either through Medicaid or with ACA subsidies that were enhanced by the American Rescue Plan (and continued for another three years by the Inflation Reduction Act).

Using similar methods and updating the analysis with 2023 ACA premiums and subsidy amounts, we now find that about 5 million uninsured people are eligible for an ACA Marketplace plan that is essentially free. (This does not include uninsured people who previously fell in the family glitch and who may now be eligible for free plans, so the number of people eligible for a free plan may be slightly higher, though most people in the family glitch were already insured).

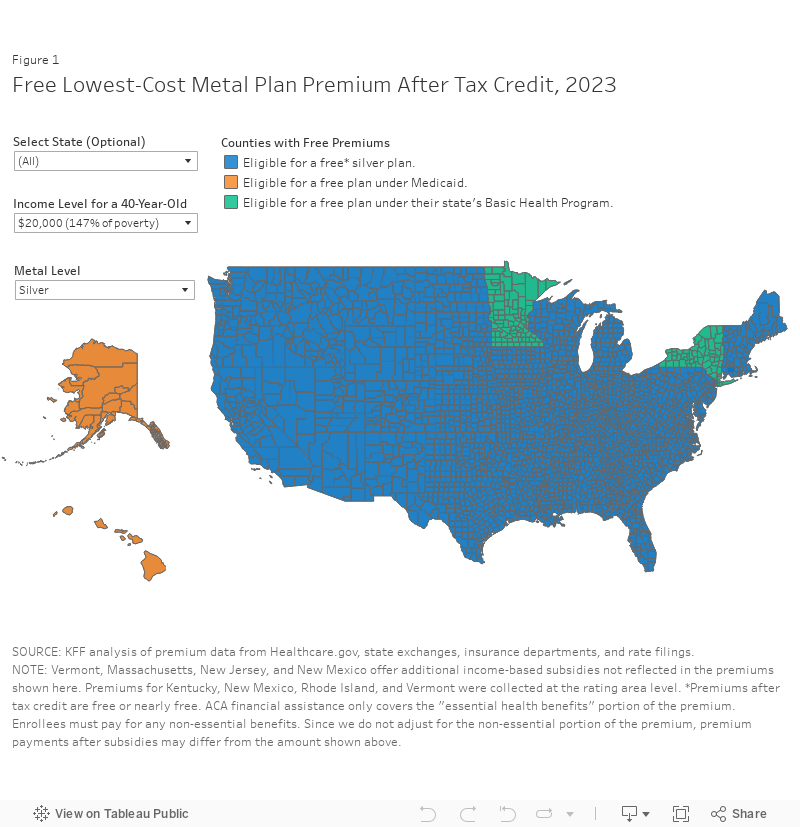

In many cases, $0 premium plans also come with cost sharing reductions, which significantly lower deductibles. Under the Inflation Reduction Act, free or nearly-free premium silver plans with very low deductibles are available to all Marketplace subsidy-eligible enrollees with incomes up to 150% of poverty ($20,385 for individuals or $41,625 for families of four enrolling in 2023). We say “free or nearly free” because in some cases an individual may have to pay for the “non-essential” part of their premium. In some cases, there could be a small extra charge – usually no more than a few dollars per month – for non-essential benefits covered by the plan.

Enrollees with incomes below 250% of poverty enrolling in silver plans qualify for reduced cost sharing. The most generous cost sharing reductions are available for people with income up to 150% FPL. For these enrollees, the level of cost sharing is similar to a platinum plan (referred to as silver CSR 94 plans). Somewhat less generous cost sharing reductions are available for people with income of 151% FPL up to 200% FPL (CSR 87 plans), which makes cost sharing in these plans similar to a gold plan. And for people with income above 200% up to 250% FPL, cost sharing reductions modestly reduce deductibles and copays (CSR 73 plans) from those found under a normal silver plan (non-CSR 70 plans).

In some parts of the country, people with incomes above 150% of poverty can also get free or nearly free silver plans, with somewhat less generous cost-sharing reductions. For example, as can be seen in the interactive map, a 40-year-old making $25,000 per year (184% of poverty) could get a free or nearly free silver plan with a smaller cost-sharing reduction in about 8% of counties, excluding counties where individuals are eligible for Medicaid or Basic Health Program (BHP) plans.

The vast majority of people with incomes below 200% of poverty are also eligible for free bronze plans, though they would generally be better off paying extra premium for a silver plan with cost-sharing subsidies because those deductibles are a fraction of a bronze deductible in that income range. Last year, the average deductible for people with incomes up to 150% of poverty in a silver plan was $146 and the average deductible for people with income between 150-200% of poverty in a silver plan was $756. Meanwhile, the typical deductible in a bronze plan was $7,051.

People with incomes above 250% of poverty do not qualify for cost-sharing reductions and may find a free bronze plan to be a better option than remaining uninsured. In 50% of counties, a 40-year-old with a $35,000 income (258% of poverty) can get a free or nearly free bronze plan. Although deductibles can be quite high in bronze plans, all ACA Marketplace plans offer free preventive services (such as screenings, annual physicals, and contraceptives) and many plans cover some other services before the deductible. All ACA Marketplace plans also have an annual limit on out-of-pocket liability, limiting exposure to unaffordable bills.

Compared to the U.S. population, uninsured people eligible for free Marketplace coverage are young adults, without college educations, Hispanic, non-native English speakers, or working in the fields of entertainment, recreation, and construction. They are also concentrated in a handful of large states (Texas, Florida, North Carolina, and Georgia).

Marketplace enrollment has reached record highs, in part because of enhanced subsidies in the American Rescue Plan Act and the Inflation Reduction Act, as well as increased marketing and outreach, and an extended enrollment period. It is also possible the pandemic has motivated more people to retain their health coverage. Nonetheless, millions of people remain uninsured, many of whom are likely unaware they could get covered for free or very low-cost and that they need to act by January 15.