On September 15, 2025, the Centers for Medicare and Medicaid Services (CMS) released a Notice of Funding Opportunity (NOFO) for the $50 billion Rural Health Transformation Program (referred to here as the “rural health fund”). The Notice describes what states need to do to apply for funds, the deadline for state applications, and the criteria that CMS will use to determine how funds will be allocated. The rural health fund was established by the tax and spending reconciliation law of 2025. It was created to help offset the impact on rural areas of the law—which includes an estimated $911 billion in federal Medicaid spending reductions over the next ten years, including an estimated $137 billion in rural areas based on KFF estimates—particularly given ongoing concerns about the financial vulnerability of many rural hospitals and reports of hospital closures. Distribution of the funds will begin before many of the Medicaid cuts under the reconciliation law take effect.

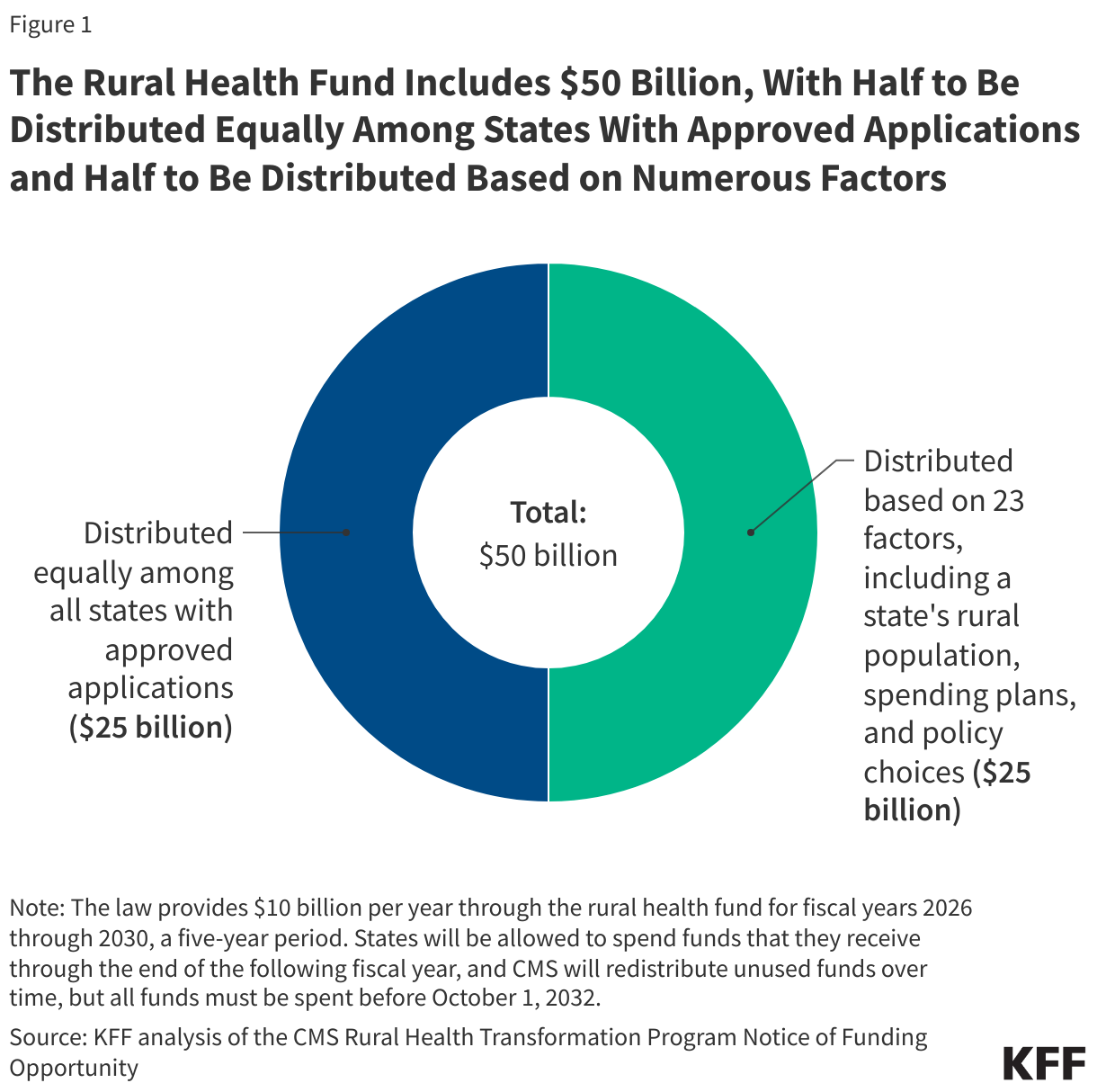

To receive any funds, states must submit complete applications that align with program requirements by November 5, 2025. CMS will decide which applications to approve by December 31, 2025. Half of the fund, $25 billion, will be allocated equally among states with approved applications, without regard to the state’s rural population or the needs of rural hospitals and other providers in the state. The other half, $25 billion, will be distributed among approved states based on a variety of factors specified in law and in the NOFO, such as the number of rural residents and health facilities, the relative amount of uncompensated care in the state, the quality of workforce and other state initiatives supported by the rural health fund, and the extent to which states adopt Make America Healthy Again (MAHA) policies. CMS will recalculate the allocation of this second tranche annually over the five-year period of funding primarily based on the progress of state initiatives and policy changes.By law, DC and the U.S. territories are ineligible for the rural health fund.

Although the Notice provides additional information, there are several outstanding questions, such as whether all states will receive funds, what share of the $50 billion will go to the about 1,800 hospitals in rural areas versus other providers and various state initiatives, and the extent to which the direct and indirect benefits for rural hospitals will offset their losses under the reconciliation law. The NOFO details the factors affecting how funds will be allocated across approved states, but CMS will continue to influence the distribution through ongoing evaluation of state initiatives and policy changes and decisions over whether to reduce, withhold, or recover funds from states for noncompliance and other reasons. Further, while federal law requires CMS to disclose state award amounts, neither the reconciliation law nor the NOFO explicitly directs CMS or states to publish timely information about administration and oversight, such as state applications or progress reports, which could make it difficult to track the distribution of dollars from the fund.

This brief describes five key takeaways from the rural health fund NOFO, including information about how CMS intends to review state applications and distribute funds and ongoing questions about the impact on rural hospitals, the distribution of funds across rural hospitals and states, and issues related to oversight and transparency.

CMS will distribute $25 billion equally across states with approved applications and the remaining $25 billion based on numerous factors, some more data driven than others

Of the $50 billion in the fund, half ($25 billion) will be distributed equally among states with approved applications (called “baseline funding”) and half ($25 billion) will be distributed among approved states based on a number of factors (called “workload funding”). A merit review panel of experts will review all applications that pass initial checks to determine whether an application is eligible for funding and to score the factors that determine how the second half will be allocated across eligible states. It is unclear from the NOFO who will sit on the merit review panel or what role agency appointees will play in reviewing state applications. The Trump administration issued an executive order in August 2025 requiring, among other things, that all discretionary grants be reviewed annually by senior appointees, which would presumably apply to the rural health fund, though the NOFO is silent as to what role such appointees will have.

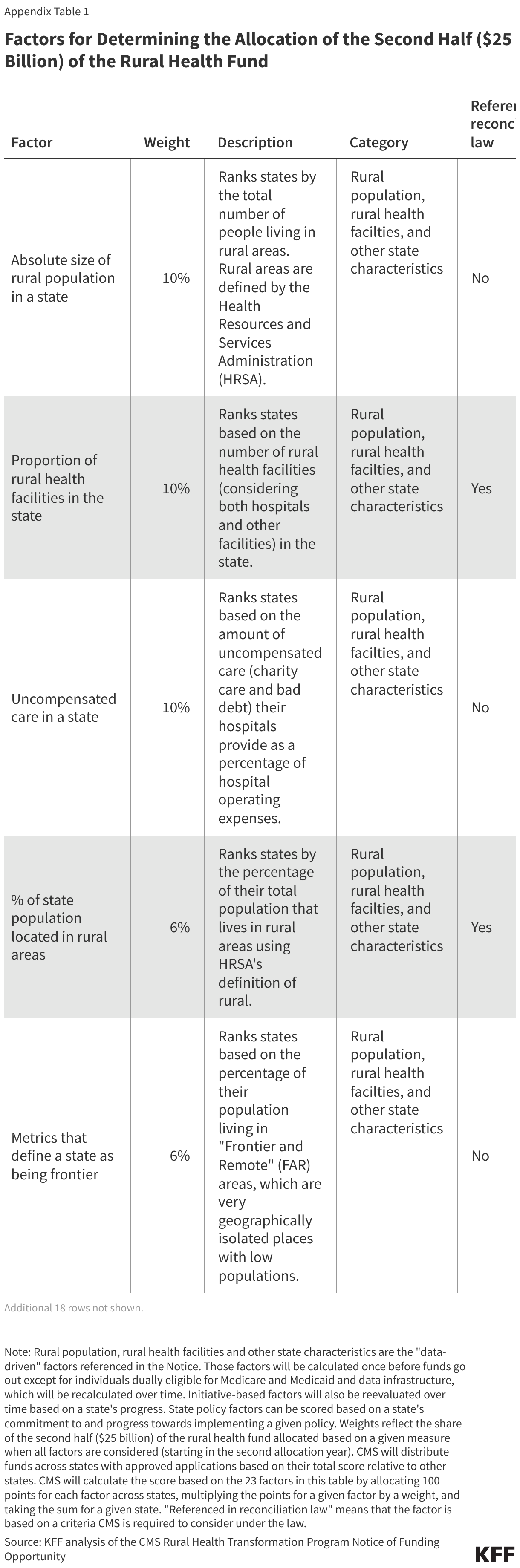

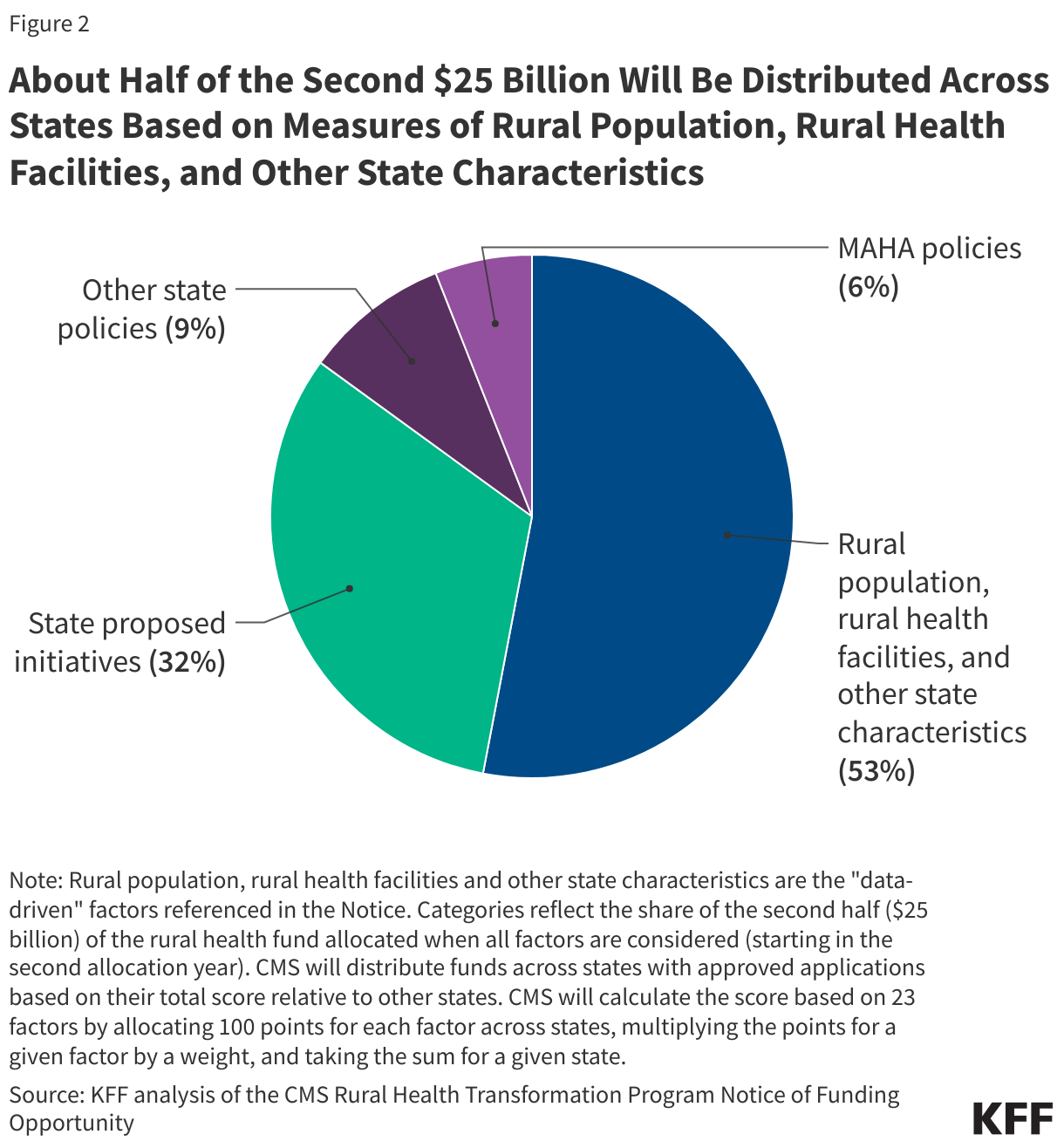

CMS will distribute the workload funding (the second $25 billion) across states based on 23 factors, weighted to varying degrees, as detailed in the NOFO (see Appendix Table 1 for more details). Of these 23 factors, three are based on measures specified in the reconciliation law, while the remaining 20 were added by CMS. The 23 factors include data-driven measures of the rural population, rural health facilities, and other state characteristics, such as the relative amount of hospital uncompensated care; state proposed initiatives; and state policies:

- Rural population, rural health facilities and other state characteristics. About half (53%) of the workload funding will be distributed across states based on published, historical data about the number of rural residents and health facilities in a state and other state characteristics (see Figure 1). Multiple indicators have a rural focus, such as the size of the state’s rural population (used to distribute 10% of workload funding) and the number of rural health facilities (a blend of hospitals and other facilities) in the state (used to distribute 10%). Other measures are not explicitly focused on rural areas, such as hospitals’ uncompensated care as a percent of operating expenses (used to distribute 10%) and the share of hospitals in the state that receive Medicaid DSH payments (used to distribute 3%). Most of these data factors will be calculated once and used during all subsequent allocation decisions and will not reflect changes over time (such as in uncompensated care).

- State proposed initiatives. About a third (32%) of the workload funding will be distributed based on CMS’s review of the initiatives the state is proposing to fund. This is a qualitative review based on the state’s plan and, in later years, the state’s progress in implementing the plan. Not all of the initiatives allowed under the rural health fund will be considered for the allocation, but the NOFO lays out those that will be taken into account, such as initiatives related to population health clinical infrastructure (used to distribute 3.75% of the workload funding), health and lifestyle (used to distribute about 2.8%), rural provider strategic partnerships (used to distribute 3.75%), and talent recruitment (used to distribute 3.75%).

- State policies. Less than one fifth (15%) of the workload funding will be distributed based on whether a state has adopted, made progress towards adopting, or committed to adopting certain policies. Some of these policies aim to promote competition among health care providers, such as by not having certificate of need (CON) laws (used to distribute 1.75% of the workload funding), making it easier for providers to practice in multiple states (used to distribute 1.75%), and providing an expansive scope of practice for nurse practitioners and other non-physicians (used to distribute 1.75%). Among other factors, three measure states’ progress in implementing certain MAHA policies (used to distribute about 6.4%) (see next section). All of the scored policies reflect state-wide changes that are not specific to rural areas.

Almost all factors will be used in allocating funding in each program year, but CMS will reevaluate state initiatives under the rural health fund and state policies over time before calculating the distribution of funds each year.

CMS may also choose to withhold, reduce, or recover baseline and workload funding from a given state if, for example, it determines that there is a violation of the state’s agreement. Funding after the first budget year may be contingent on a state’s progress and whether CMS decides that continued funding “is in the government’s best interest.” The law indicates that there will be no administrative or judicial review of these and other funding decisions made by CMS.

States will receive more funds if they adopt Make America Health Again (MAHA) policies.

States that have adopted certain MAHA policies will receive a larger share of the $25 billion workload funding (see above). States can also receive a partial increase if they have taken steps to implement these policies or have committed to doing so. These policies are not limited to rural areas and include requiring schools to reestablish the Presidential Fitness Test; prohibiting SNAP spending on non-nutritious items, like soda or candy; and requiring that nutrition be included in continuing medical education for physicians.

CMS also indicated the importance of the MAHA agenda for the rural health fund by including “make rural America healthy again” as one of its five strategic goals, which correspond to permitted uses of the funds. CMS describes this goal as supporting “rural health innovations and new access points to promote preventative health and address root causes of diseases.” CMS will also consider the quality of certain state MAHA initiatives under the rural health fund when deciding how to distribute funds across states, such as through a factor focusing on “health and lifestyle.”

While the $50 billion fund could help rural communities in a number of ways, the extent to which it will benefit rural hospitals and offset their losses under the reconciliation law is unclear

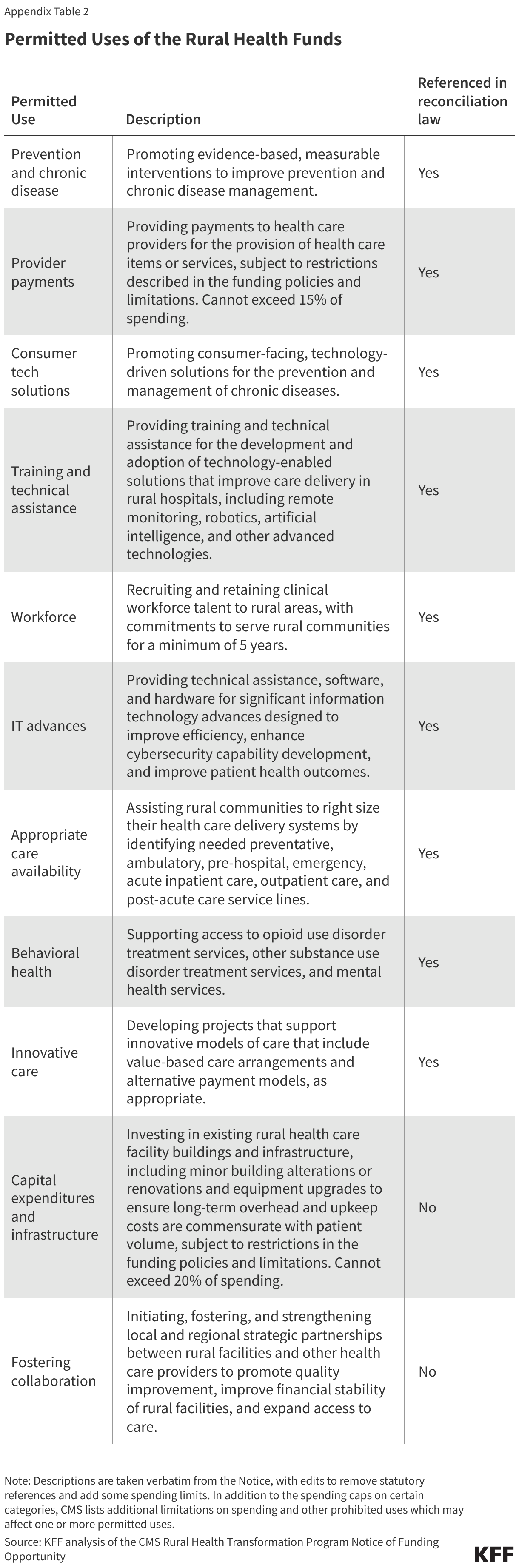

The rural health fund will “support…rural communities to improve healthcare access, quality, and outcomes through system transformation” according to the Notice, rather than providing general financial support exclusively to hospitals and other providers to use as they see fit. Further, CMS states that the “intent of this funding is not to be used for perpetual operating expenses, but rather for investments that can be made within the duration of the program that will have sustainable impact beyond the end of the program.”

States will be allowed to use the funds for a number of purposes (see Appendix Table 2), most of which are intended to improve the rural health care delivery system and how care is delivered. For example, states could use the funds to promote prevention and chronic disease management interventions, support collaboration among rural health care facilities (such as by sharing administrative services) and between rural providers and regional health systems, recruit clinical workers to rural areas, promote technological advancements (such as by expanding telehealth or promoting AI diagnostic tools), invest in existing hospital buildings and infrastructure, help hospitals determine which services should and should not be maintained, and support the adoption of value-based care and alternative payment models. It is also possible that some of the funds could flow to nonrural areas within a state.

In addition to specifying permitted uses of the funding, CMS has also detailed ways in which the funds cannot be used, many of which are particularly salient for hospitals and other providers. For example, rural health funds cannot be used for:

- Payments to providers for care that exceed 15% of total funds. Payments to providers also cannot be used to supplement existing fees, such as for Medicaid, or pay for care that is reimbursable by insurance, but they could be used to pay for, say, uncompensated care.

- Construction, building expansion, or purchasing buildings, but can be used for certain investments in existing rural health care facility buildings and infrastructure, not to exceed 20% of total funds.

- Replacements for previous HITECH-certified electronic medical record (EMR) systems that exceed 5% of total funds.

- Funds for gender-affirming care (a limitation that is not restricted to care for minors, as are many other federal measures) and reimbursement for most abortion services. There are also limitations related to “citizenship documentation requirements for payments made with respect to an individual.” Many hospitals do not currently collect patient immigration status but may need to do so to be reimbursed for patient care with rural health funds.

While the fund was established in part to address concerns about rural hospitals and closures, the extent to which it will benefit these facilities and offset losses under the reconciliation law is unclear. Although approval of state applications is ultimately up to CMS, states can choose how much of the funds will go to hospitals versus other rural providers and various other entities, such as contractors providing technical assistance for projects, universities participating in workforce initiatives, regional health systems in urban areas collaborating with rural providers, and vendors developing new health technologies.

Funds that flow to rural hospitals will need to be used for at least one of the approved purposes, rather than providing general financial support. Further, CMS has capped the amounts of funds that can be sent to hospitals and other providers for certain approved purposes, such as paying for patient care or investing in existing buildings and infrastructure (see above). The structure of the rural health fund contrasts with the federal government’s response to COVID-19, when it provided large amounts of support to providers to alleviate the financial impact of the pandemic.

Some initiatives intended to transform the rural health care delivery system could benefit hospitals to varying degrees. For example, among other initiatives with more direct implications for hospitals, funds could be used to strengthen collaboration among rural facilities and other rural providers, which could help rural hospitals operate more efficiently. Other initiatives, such as programs to promote health literacy and healthy behaviors, would have less direct implications for hospitals. The benefit to rural hospitals—and to other providers, patients, and rural communities—will also depend on how effective these initiatives are, which is difficult to predict.

Rural areas and hospitals will likely see many of the benefits from the rural health fund before the cuts under the reconciliation law take full effect. The law provides $10 billion through the rural health fund per year from fiscal years 2026 through 2030—and all funds must be spent before October 1, 2032—while nearly two thirds (64%) of the ten-year reductions in federal Medicaid spending would occur after fiscal year 2030 based on KFF’s analysis of CBO estimates. Additionally, the rural health fund will be temporary, while many of the cuts in health spending are not time limited, meaning that the longer-term impact on rural areas and hospitals could be less favorable. CMS requires states to include a sustainability plan in their applications and intends for these initiatives to promote lasting change, but the extent to which that will occur after the funds dry up is unclear.

It remains unclear which states and rural hospitals will benefit the most

While the NOFO includes many new details about how the funds will be distributed across states, questions remain about which states will receive funding, the final distribution across approved states, and how well this distribution will align with various definitions of need. The first $25 billion will be distributed equally among approved states, meaning that smaller states will benefit more relative to their size. For the second $25 billion in funding, most, if not all, of the allocation factors will benefit some states more than others. For example:

- 10% of the distribution is based on uncompensated care as a percent of hospital operating expenses, which tends to be higher in states that that have not expanded Medicaid under the Affordable Care Act.

- 5% of the distribution is based on the geographic size of a state, which will benefit the five largest states (Alaska, Texas, California, Montana, and New Mexico) by definition (the remaining 45 states will receive zero points for this factor).

- 3.75% of the distribution is based on a state’s progress in obtaining a waiver to prohibit the purchase of non-nutritious foods using Supplemental Nutrition Assistance Program (SNAP) benefits. Nearly all of the 12 states with approved waivers to date are states that President Trump carried in the 2024 election.

At the same time, CMS’s approach for evaluating rurality and other data-driven metrics moderates differences across states by focusing on rankings rather than raw differences. For instance, Alaska is more than twice the size of Texas, but Alaska’s score for the geographic factor will not be much higher than Texas’s score because Alaska and Texas are ranked next to each other.

It is also unclear how the benefits will be distributed across rural hospitals. This will depend in part on how CMS distributes funds across states (see above); how states in turn distribute these funds across hospitals, other providers, and various initiatives; and which hospitals states target. For example, states could distribute funds to rural hospitals broadly or target specific groups of rural hospitals, such as those in financial distress, in high-need areas, or that state policymakers prioritize for other reasons. Relatedly, there are also questions of how narrowly or broadly states will define “rural”, which CMS leaves to their discretion and could potentially encompass few or many hospitals, including hospitals that might not be viewed as rural by some (such as urban hospitals that receive a rural designation for certain payments). States could also use the funds for a variety of initiatives that could benefit some hospitals more than others, such as by attracting clinicians to certain, specific rural areas of the state.

It is unclear how transparent CMS and states will be about the distribution and oversight of the fund, such as by disclosing the flow of dollars to specific hospitals and other entities.

The reconciliation law and NOFO are silent on how transparent CMS and states will need to be about the distribution and oversight of funds. For example, it is unclear whether states will disclose to the public which specific hospitals and other entities are receiving how much money and for what purpose, both ahead of time and as funds go out the door. That information would be useful for understanding the effectiveness of the fund, such as whether funds are going to hospitals in need that serve as a critical access point for patients versus wealthy facilities. Some of this information may be available in state applications and progress reports, though it is unclear whether the agency will post these materials online or require states to do so. Those materials will include numerous other details that could be useful for monitoring the rural health fund, such as a description of rural health needs in a given state, an overall rural health transformation plan, details about each state initiative, key stakeholders, outcomes that will be evaluated, and state progress.

It is also unclear how much transparency there will be regarding other aspects of the program, such as the members of the merit review committee responsible for evaluating applications; modifications to state plans over time; CMS’s rationale for reducing or recovering rural health funds or reallocating funds over time; and state remediation plans for noncompliance. CMS retains broad discretion over whether to continue to fund states by considering criteria such as whether “continued funding is in the government’s best interest” and whether states are “improperly managing or using award funds, including fraud, waste, abuse, and criminal activity.”

Some of this information may be disclosed through existing regulation (e.g., CMS will be required to publicly disclose the amount it awards to each state) and Freedom of Information Act (FOIA) requests submitted by journalists and other groups.

This work was supported in part by Arnold Ventures. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.