What Does the Medicaid Eligibility Rule Mean for Low-Income Medicare Beneficiaries and the Medicare Savings Programs (MSPs)?

On September 21, 2023, the Centers for Medicare and Medicaid Services (CMS) finalized a rule that is intended to help low-income Medicare beneficiaries gain access to Medicaid coverage of Medicare premiums and often, cost sharing, through the Medicare Savings Programs. The new Medicaid rule will streamline the Medicaid application process for the Medicare Savings Programs, in part, by further automating the application process for people with Medicare’s Part D Low-Income Subsidy and automatically enrolling some Medicare beneficiaries, including those who receive Supplemental Security Income. After the effects of the rule are fully in place, in 2029, CMS expects the rule to increase enrollment in the Medicare Savings Programs by nearly 1 million. New enrollments include people who enroll in the Medicare Savings Programs because of the rule and additional months of coverage among people who would have enrolled anyway but now face fewer administrative barriers to doing so and gain more months of coverage. The final rule is one component of a larger proposed rule that would make broader changes to Medicaid eligibility.

What do the Medicare Savings Programs cover for low-income Medicare beneficiaries?

Through Medicaid, the Medicare Savings Programs cover premiums and, in most cases, cost sharing for Medicare beneficiaries who meet financial eligibility requirements. The programs provide coverage of Medicare premiums and cost sharing to Medicare beneficiaries with incomes below the federal poverty level ($1,235 for an individual in 2023) and financial resources below 300% of the limit for Supplemental Security Income ($9,090 for an individual in 2023, unlike Supplemental Security Income, asset limits for the Medicare Savings Programs are adjusted for inflation and increase each year). Medicare beneficiaries with incomes between 100% and 135% of the federal poverty level ($1,660 for an individual) who meet the same requirements for financial resources are eligible for coverage of Medicare premiums but only receive coverage of Medicare cost sharing if the state chooses to provide it. The federal eligibility thresholds for the Medicare Savings Programs are minimum levels and states may elect to offer coverage to people with incomes or assets that exceed federal minimums, which had been done by 17 states in 2022. When states expand coverage or eligibility, the federal government continues to pay the federal share of the costs.

Among the 12.5 million people with Medicare and Medicaid, nearly all participate in the Medicare Savings Programs, and nearly three quarters also receive full Medicaid benefits. Most people who have both Medicare and Medicaid are also enrolled in the Medicare Savings Programs. There are some people who have full Medicaid and Medicare but do not qualify for the Medicare Savings Programs. In such cases, states may choose whether to cover Medicare premiums and cost sharing or not. In 2020, 73% of people with both Medicare and Medicaid were also eligible for the full range of Medicaid benefits that are not otherwise covered by Medicare, such as long-term services and supports and non-emergency medical transportation.

Eligibility for the Medicare Savings Programs can be quite complicated—which often leads to varying participation rates across the states and coverage loss among Medicare beneficiaries within their first year of Medicare-Medicaid enrollment. Nationally, 16% of all Medicare beneficiaries were enrolled in the MSPs, but KFF found that the in 2019, the rate ranges from 7% in North Dakota to 33% in the District of Columbia. Variation across the states can be attributed to differences in eligibility criteria, poverty rates, and application processes that could make it more difficult for beneficiaries in some states to apply. Recent KFF analysis also shows that among Medicare enrollees who have full Medicaid benefits, 28% lost Medicaid coverage at some point during their first year of enrollment. Among Medicare enrollees who enrolled in the Medicare Savings Program but not full Medicaid, 17% lost that coverage within the first year.

How would the new Medicaid eligibility rule affect dual-eligible individuals’ enrollment and spending?

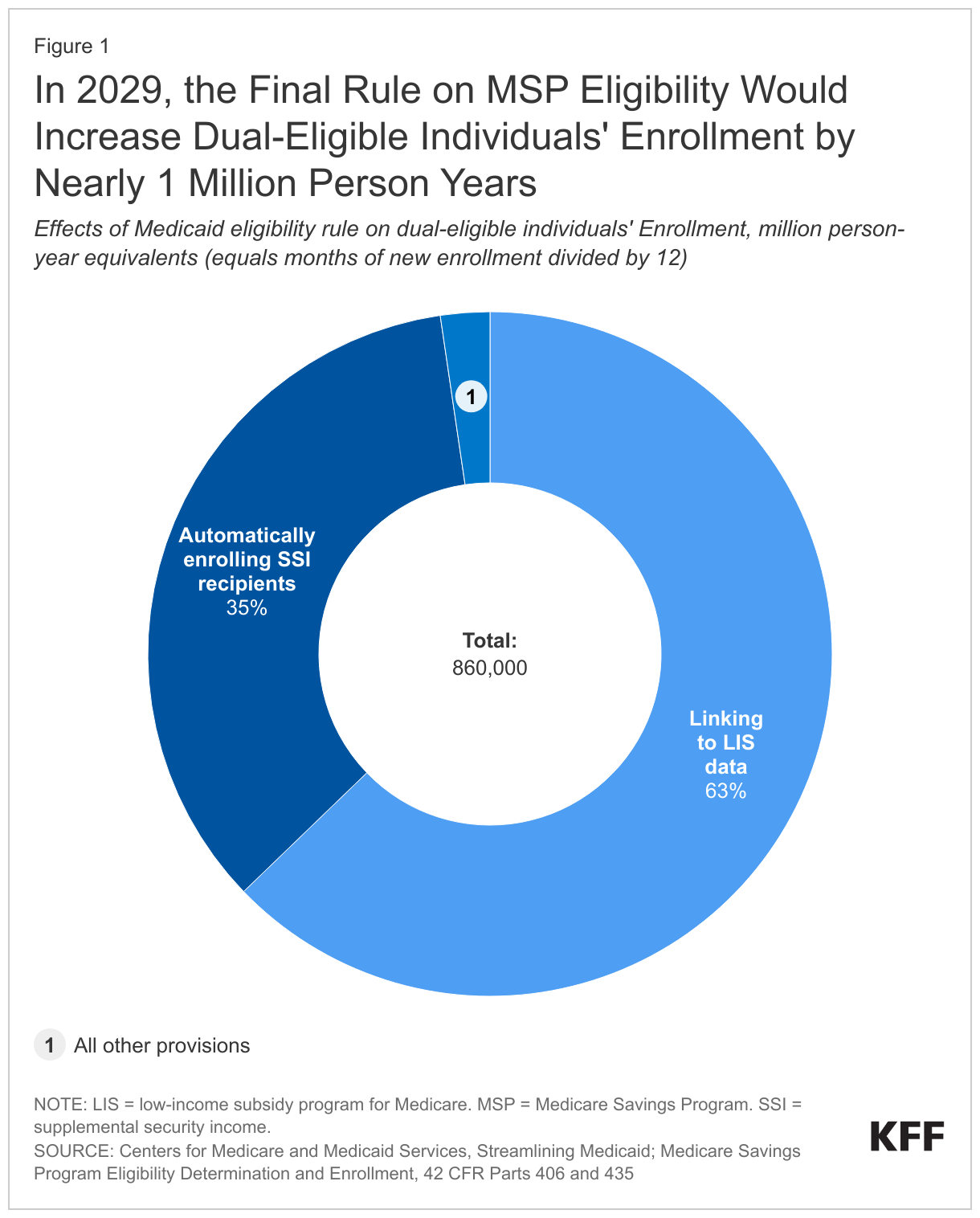

CMS expects the new Medicaid eligibility rule to increase enrollment of dual-eligible individuals by nearly 1 million person-years in 2029 (Figure 1). Person-years of enrollment equal the number of months of additional enrollment in the Medicare Savings Programs divided by 12. They include people who newly enroll in the program but also additional months of enrollment among people who would already enroll but now have additional months of coverage. CMS estimates that the new rule will increase Medicaid spending by $4.2 billion and Medicare spending by $1.9 billion. New Medicaid spending includes spending on Medicare premiums and cost sharing and in some cases, spending for full Medicaid benefits for newly enrolled individuals. New Medicare spending reflects CMS’ assumption that coverage of Medicare cost sharing will result in use of more Medicare-covered services.

The final rule improves alignment between the Medicare Savings Programs and applications for Medicare’s Part D Low-Income Subsidy program (LIS), resulting in an additional 0.5 million person-years of enrollment. Medicare beneficiaries with low income and limited assets receive help paying for prescription drugs through LIS. To increase participation in LIS, people who enroll in the Medicare Savings Programs are automatically enrolled in LIS, but people in LIS are not automatically enrolled in the Medicare Savings Programs. Instead, the Medicare Improvements for Patients and Providers Act of 2008 requires the Social Security Administration to send LIS applications to states and requires states to treat those data as an application for the Medicare Savings Programs.

Despite the requirement for states to use LIS data to initiate an application to the Medicare Savings Programs, the application process is often not streamlined because the two programs have different methods for measuring income and financial resources. For example, the Medicare Savings Programs include the following forms of income and assets that are excluded from the LIS definition: interest and dividends, non-liquid resources, certain burial funds, whole life insurance, and in-kind support and maintenance. The final rule notes that most Medicare beneficiaries in LIS have limited income and assets from those sources but documenting their value can be quite cumbersome for applicants. To address such barriers to enrollment in the Medicare Savings Programs, the rule makes the following changes to the application process:

- The rule encourages states to adopt the LIS definitions for defining financial eligibility, in which case the LIS application would include all required information for an application to the Medicare Savings Program.

- Starting April 1, 2026, states that elect to keep their methods for defining financial eligibility, rather than use the LIS criteria, would be required to accept applicants’ self-reported values for all financial resources that are not included with the LIS application. All applicants whose self-reported values are within state eligibility criteria would be enrolled in the Medicare Savings Programs.

- If states have data that are not compatible with applicants’ self-reported amounts, they may ask for additional information prior to enrolling applicants.

- States may also request further documentation after enrollment as part of the post-enrollment eligibility verification process.

- States that require applicants to submit documentation of financial resources beyond what is required for an LIS application will be required to take a more active role in helping applicants find the appropriate materials, including directly contacting financial or fiduciary institutions in some circumstances.

The rule also requires states to automatically enroll Medicare beneficiaries with Supplemental Security Income into the Medicare Savings Programs, resulting in 0.3 million new person years of enrollment in 2029. The financial eligibility criteria for Supplemental Security Income are lower than that of the Medicare Savings Program for people with income below 100% of the federal poverty level. Thirty-three states and the District of Columbia already automatically enroll Medicare beneficiaries with Supplemental Security Income into Medicaid. Starting October 1, 2024, all states would be required to enroll Medicare beneficiaries with Supplemental Security Income in the Medicare Savings Program. Other provisions in the rule that would have smaller effects on enrollment include modifying the definition of family size for determining eligibility and making the effective date of coverage earlier for certain Medicare beneficiaries who must pay a premium for Medicare’s hospital insurance. (Most Medicare beneficiaries do not pay a premium for hospital insurance, also known as “Part A,” but do pay a premium for medical insurance or “Part B.”)

The final rule also requires states to provide LIS applicants with information about the availability of full Medicaid benefits. In the proposed rule, there was a requirement for states to use the LIS data to initiate an application for full Medicaid benefits, but that provision is not included in the final rule. In providing required information in the final rule, CMS explained that it dropped the provision because Medicaid applications generally require more information and disclosures than are included in the LIS application. Such disclosures include notification from states to applicants that Medicaid may recover the costs of providing certain Medicaid services from the estates of deceased Medicaid enrollees, a practice known as “estate recovery.” Estate recovery is prohibited in the Medicare Savings Programs and therefore, not disclosed on the application. The final rule requires states to provide LIS applicants with information about the availability of Medicaid benefits and an opportunity to provide further information needed to complete an application. That requirement may increase enrollment in Medicaid beyond the effects resulting from a streamlined MSP application.

What are key issues to watch?

It is unknown how states will respond to the new rule, but it may increase the number of states that increase or eliminate limits on financial assets when determining eligibility for the Medicare Savings Programs. Most children and adults under age 65 who are eligible for Medicaid qualify on the basis of income but are not subject to limits on assets. Prior to the Affordable Care Act, in most states, adults needed to be over age 65, a parent, or have a significant disability to qualify for Medicaid, but the Affordable Care Act expanded Medicaid coverage to nearly all adults with incomes up to 138% of the federal poverty level. As of October 2023, 40 states and the District of Columbia had adopted that expansion. When Medicaid enrollees eligible through the expansion (or less often, eligible because they are parents) turn 65 and become eligible for Medicare, they reach a coverage cliff and must start paying Medicare premiums and cost sharing. The Medicare Savings Programs can blunt the effects of losing Medicaid for people who quality—especially those who have coverage of both premiums and cost sharing—but some people with incomes within the Medicare Savings Program eligibility range have assets that render them ineligible.

As of November 2022, 11 states had completely eliminated counting assets when determining eligibility for the Medicare Savings Programs, and starting January 1, 2024, California will not count assets when determining eligibility for all Medicaid applicants. California is also increasing income eligibility for all groups to 138% of the federal poverty level to align with eligibility for younger adults. That change is expected to increase enrollment of people who are ages 65 or older or have a disability.

By encouraging states to adopt income and asset requirements that are at least as permissive as the LIS requirements, the final rule on the Medicaid Savings Programs may incentivize states to reconsider existing income and asset limits. Some states may align with the LIS definitions, but others may further increase limits on income or eliminate asset limits to maintain coverage for people who are aging into Medicare.

The final rule includes several pieces from a much larger proposed rule on Medicaid eligibility, that could have additional coverage implications for people who are eligible for Medicaid because they are age 65 or older or have a disability. It is unknown when the remainder of the rule will be finalized or what the provisions of the final rule will be, but they are expected to simplify the application and eligibility renewal processes. States are currently renewing eligibility for all Medicaid enrollees after a 3-year period of continuous enrollment and during this unwinding, millions of people are being disenrolled, many on account of the renewal procedures. Although simplified application and renewal procedures are not in place for the unwinding, in the future, the rule on the Medicare Savings Programs and other forthcoming rules may increase enrollment and make it easier to obtain and retain coverage for people with Medicaid.

This work was supported in part by Arnold Ventures. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.