Q&A: Implications of the Ruling on the ACA’s Preventive Services Requirement

Note: This post was updated on April 4, 2023, to include additional details and a table showing potentially affected preventive services.

On June 21, 2024, the 5th Circuit Court of Appeals affirmed the district court’s ruling that the ACA’s requirement to cover without cost-sharing services recommended by United States Preventive Services Task Force (USPSTF) is unconstitutional. However, the 5th Circuit ruled that a nationwide remedy was not proper and that only the plaintiffs are permitted to exclude USPSTF recommended services from their plans. The Appeals Court sent back to the district court the plaintiffs’ claim that the Secretary of Health and Human Services’ ratification of HRSA and ACIP recommendations violates the Administrative Procedure Act for further briefing and a judgment.

On March 30, 2023, a judge in the U.S. District Court in the Northern District of Texas issued a final judgment in a court case challenging the provision of the Affordable Care Act (ACA) that requires most private health plans to cover a range of preventive services without any cost-sharing for their enrollees. Having concluded in September that aspects of the requirement were unconstitutional and violated religious rights, the judge’s remedy in the Braidwood Management v. Becerra imposes new limits on the government’s ability to enforce those requirements nationwide. This Q&A summarizes some of the key issues related to the ruling.

What does the ruling mean for the public?With about 100 million privately insured people using preventive services required by the ACA to be covered without out-of-pocket costs, the preventive services coverage requirement is the provision of the ACA that affects the broadest number of people, and it has been enormously popular with the public. Because of the ACA requirement, the vast majority of private health plans have to cover a range of preventive services and cannot impose deductibles or copays for them. If the ruling stands, over time, millions of people could end up paying more for preventive care and some may lose access to certain services. However, as sweeping as the ruling is, it does not completely and immediately wipe out preventive services coverage under the ACA.

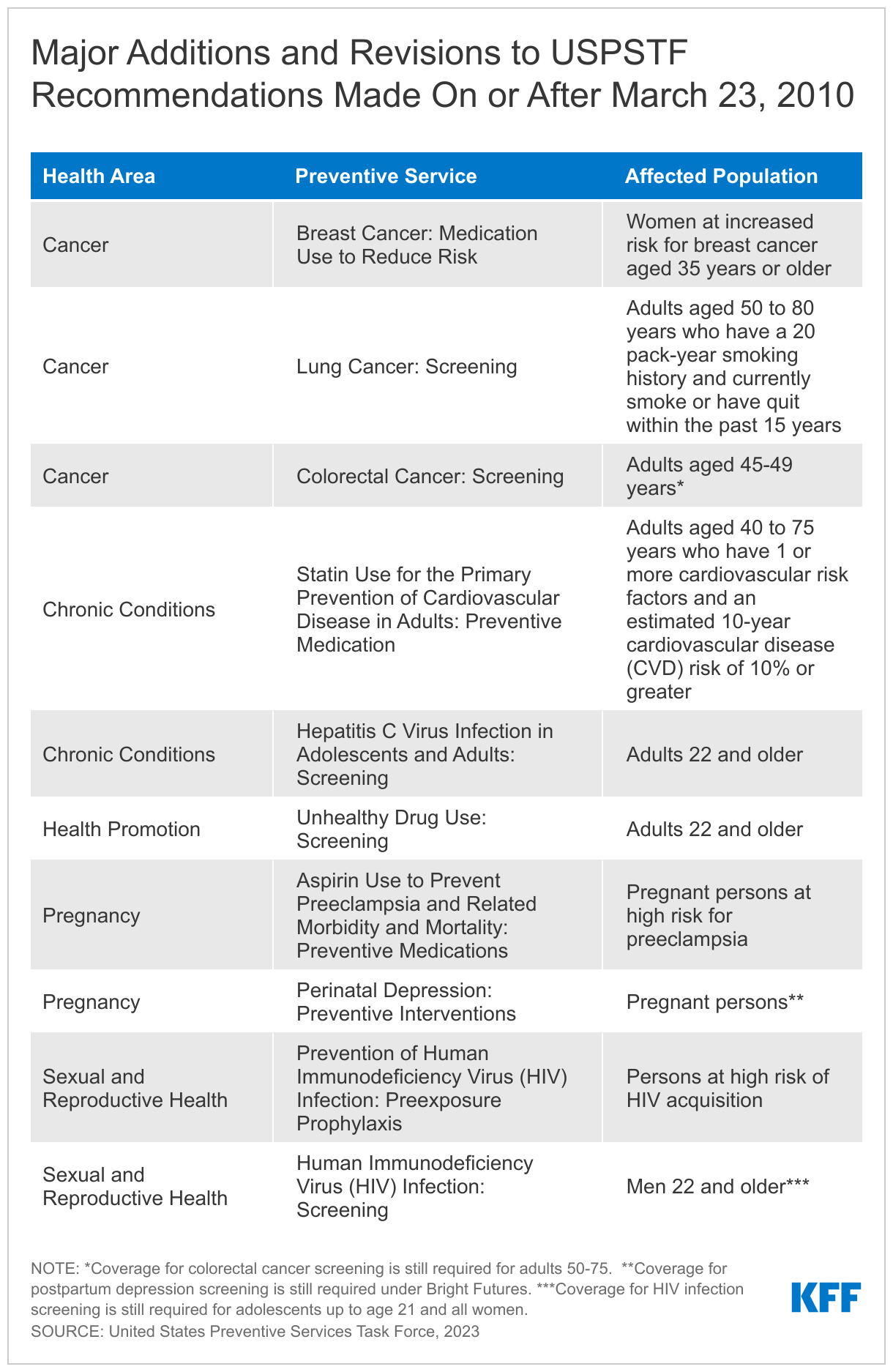

That’s because the ruling applies specifically to services recommended by the US Preventive Services Taskforce (USPSTF) that were made after 2010 when the ACA was enacted. The ruling would not overturn coverage requirements for vaccines recommended by the Advisory Committee on Immunization Practices (ACIP), women’s preventive health services (such as contraception, well women care and prenatal care, breastfeeding support services, and intimate partner violence screening) recommended by the Health Resources and Services Administration (HRSA), or services for children and young adults recommended by Bright Futures, though the plaintiffs had asked that those be struck down as well and that decision could be appealed. The ruling also only applies to updates to or new USPSTF recommendations issued since March 2010, when the ACA was enacted. It would effectively lock in place coverage requirements based on evidence from 13 years ago.

The ruling separately finds that the mandate to cover pre-exposure prophylaxis (PrEP), a medication taken to prevent HIV, violates the plaintiffs’ religious rights under the Religious Freedom Restoration Act (RFRA). While the RFRA remedy is limited specifically to the plaintiffs, because PrEP was recommended by the USPSTF after 2010, the medication and certain ancillary lab services can now be subject to out-of-pocket costs across all health plans and plans could elect to drop coverage altogether.

Coverage will not necessarily change immediately. Although the ruling is effective immediately, in many cases, health plan contracts are in place for the calendar year, and employers do not typically make changes to coverage or cost midyear. (It may be easier for plans to change formularies to allow for cost-sharing with respect to impacted drugs.)

Will cancer screenings be covered by insurance plans without out-of-pocket costs?

Screenings like mammography and cervical cancer screening would still be covered without out-of-pocket costs because they were recommended by the USPSTF prior to March 2010. Although colorectal cancer screening was included as a recommended service in 2010, it was limited to adults ages 50 to 75. In 2021, the USPSTF expanded their colorectal cancer screening recommendation to also include adults ages 45 to 49. Therefore, because of this ruling, people in their late 40s may begin to face cost barriers to colorectal screening. Similarly, lung cancer screening with low dose CT scans for adults aged 50 to 80 years with a 20 pack-year smoking history and currently smoke or have quit within the past 15 years was recommended in 2021 and could therefore be subject to out-of-pocket costs.

What are some examples of services that may now be subject to out-of-pocket costs?

Any service that was first recommended by USPSTF after March 2010 (and is not also recommended by another group like HRSA or ACIP) would no longer be required to be covered without out-of-pocket costs. For example, services and medications like statins to prevent heart disease, lung cancer screening, PrEP to prevent HIV, and medications to lower the risk of breast cancer (e.g., tamoxifen) for high-risk women may now be subject to copays, deductibles, or coinsurance.

Additionally, because some USPSTF recommendations that were in place before March 2010 have since been changed, there could be some groups of people who lose access to certain types of no-cost preventive care. The USPSTF typically updates its recommendations every five years so that some of the recommendations could have changed slightly from the recommendation that was in place in 2010. This is the case with colorectal cancer screening discussed above and with HIV screening which was initially only recommended for high risk individuals and is now recommended for the general population.

Why were these preventive services originally included in the ACA?

One of the reasons this provision was included in the ACA was because research showed that cost-sharing, even in small amounts, reduces the likelihood that people use preventive services. Millions of people each year report delaying or forgoing needed health care due to costs.

The USPSTF is a group of independent experts that use a rigorous evidence-based process to review research, weighing both the benefits and risks of services. The group recommends services where there is sufficient evidence that the benefits of screening or other preventive care outweigh the risks associated with those interventions.

In the ACA, the preventive care coverage mandate was tied to recommendations by the USPSTF and other groups as a way of having a standard definition of what preventive care means, including changes over time as new evidence becomes available.

What is PrEP and how will the ruling affect access to it?PrEP is a medication that is 99% effective at preventing HIV through sex and at least 74% effective at prevention through injection drug use. Because of its effectiveness, PrEP has been a cornerstone of the federal plan to address HIV in the U.S.

While some health plans could opt to drop PrEP coverage altogether, we are more likely to see plans requiring copays, coinsurance, or deductibles. For generic PrEP, out-of-pocket costs might be nominal (the cash price for the drug is about $30 per month); for a brand name drug, particularly the new long acting injectable formation, cost-sharing could be substantial. For example, some enrollees could face a 20% or 50% cost in coinsurance for a $2,000 per month drug. Enrollees may also face cost-sharing for some of the ancillary care that is necessary for PrEP users, such as certain labs and provider visits. Before the ruling, these had been covered without cost-sharing following a 2021 clarification from the federal government that the PrEP recommendation encompassed those ancillary services.

Can states preserve coverage for these benefits?

There's a long history of states regulating private insurance and mandating coverage of certain services, including some of these preventive services before the Affordable Care Act took effect. But there are real limits to what states can do—for example, they cannot regulate self-insured employer plans, which cover most people with private insurance, including 64% of people with employer-based coverage. So while states can, and are moving to, fill in some of the gaps that this ruling leaves, big gaps would likely remain.

Are these rulings final or will there be more legal action ahead?The Biden administration is appealing this ruling and will seek a stay of this remedy from the Fifth Circuit Court of Appeals. The Fifth Circuit may or may not issue that stay or do so in an expedient way, and the rulings could be appealed to the Supreme Court, specifically to what is known as the “shadow docket,” which means that the Supreme Court would review the issue of the stay, not the merits of the case as a whole. However, the merits of the case itself could eventually be reviewed by the Supreme Court.

What broader implications does this ruling have for the ACA?This is not the potentially fatal blow to the ACA like previous court cases, but it would limit a very popular benefit that millions of people use. For people who use preventive services, a key to access is what people have to pay out of their own pockets. Regardless of your plan, these ACA-required preventive services were covered without cost-sharing, meaning that the individual didn’t pay for the services. But if these rulings hold, individuals may have to pay something for the affected services as insurers review what is covered and by how much. This is the first time a court has ruled that the ACA preventive services coverage requirement other than the contraceptive coverage requirement violates employers' religious rights. This has the potential to open the door to employers objecting to other services, such as vaccines.

Additional Resources:

Preventive Services Use Among People with Private Insurance Coverage

Explore an analysis of preventive services that finds roughly 100 million people received ACA-required preventive services with no patient cost-sharing in a typical year.

Learn about the implications of the most recent legal challenge contesting the ACA requirement that most private insurance plans cover specific preventive care items and services at no cost to patients.

Answer key questions about pre-exposure prophylaxis (PrEP) and its coverage, which prompted the court challenge.

Review findings on women’s receipt of cancer screenings and other preventive services as well as knowledge of insurance coverage requirements for these services.

Preventive Services Covered by Private Health Plans under the Affordable Care Act

Read a summary of the federal requirements for coverage for preventive services in private plans, major updates to the requirement, and recent policy activities.

Explore the adult preventive services most private plans must cover, including a summary of the recommendation, the target population, and related federal coverage clarifications.