10 Key Facts About Women with Medicare

Medicare is the federal program that provides health coverage to over 66 million people ages 65 and older and younger people with long-term disabilities. More than half of all people with Medicare are women, including more than 31 million ages 65 and older and about 4 million under age 65 with long-term disabilities. Medicare plays a key role in supporting the health and well-being of women, covering a broad range of services essential to women’s health, including preventive, reproductive, primary, and specialty care, and prescription drugs.

This brief presents 10 key facts about women with Medicare, based on data from various sources (see methods for additional information). (A separate KFF brief, Coverage of Sexual and Reproductive Health Services in Medicare, describes Medicare coverage of services for women of reproductive age.) The language used here attempts to be as inclusive as possible, but the analysis draws on survey data that uses specific gender labels for female and male for the data year used for this analysis, not inclusive of gender non-binary, transgender and other gender expansive identities. In addition, due to sample size and data collection limitations, analysis is unavailable by race and ethnicity for Asian adults, American Indian and Alaska Native adults, and Native Hawaiian and Pacific Islander adults.

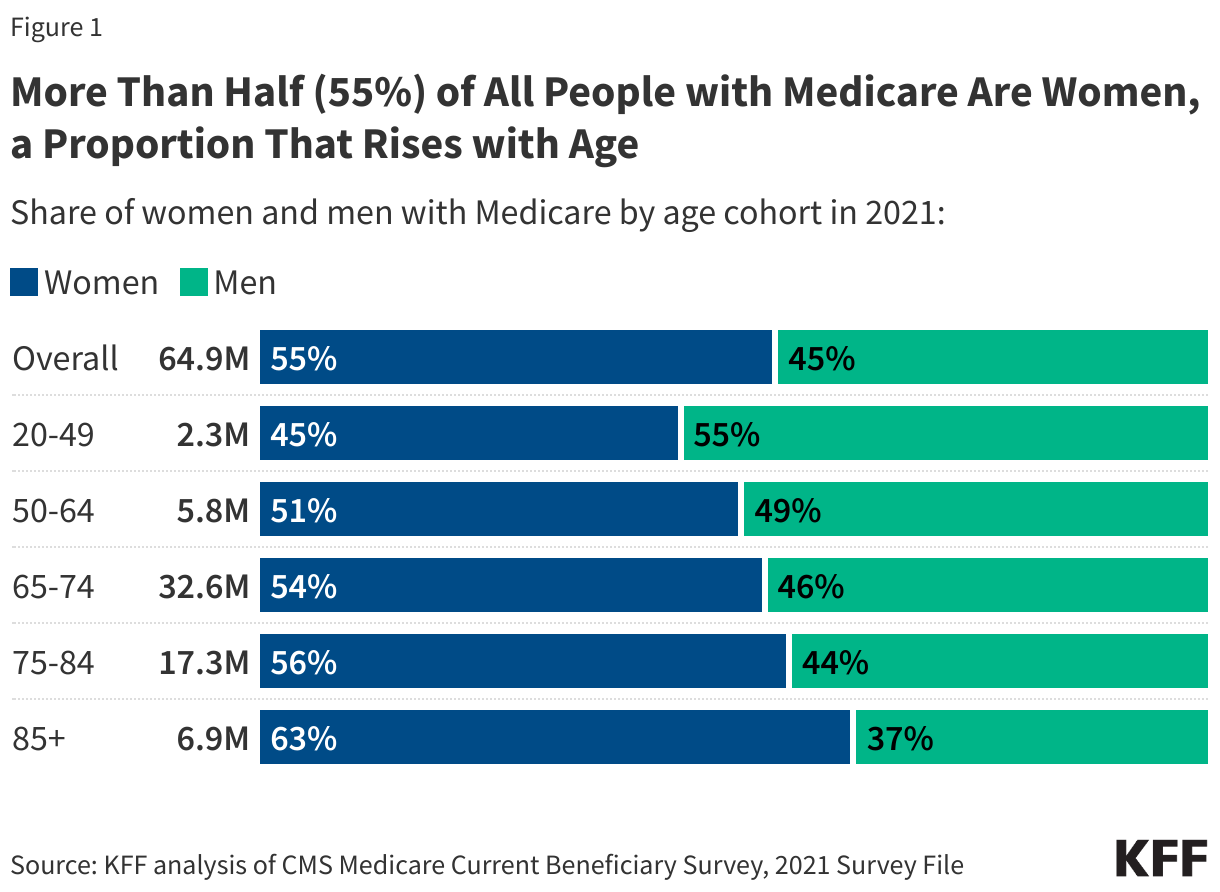

1. More Than Half of All People with Medicare Are Women, a Proportion That Rises with Age

In 2021, more than half (55%) of all Medicare beneficiaries were women and 45% were men (Figure 1). Of the more than 35 million women with Medicare, about 4 million are under age 65 with long-term disabilities (11%) and 4.3 million are ages 85 and older (12%). Since women live longer than men, on average (having 19.7 years of life expectancy at age 65 vs. 17 for men in 2021), women represent a larger share of older age cohorts. For example, nearly two-thirds (63%) of Medicare beneficiaries ages 85 and older are women.

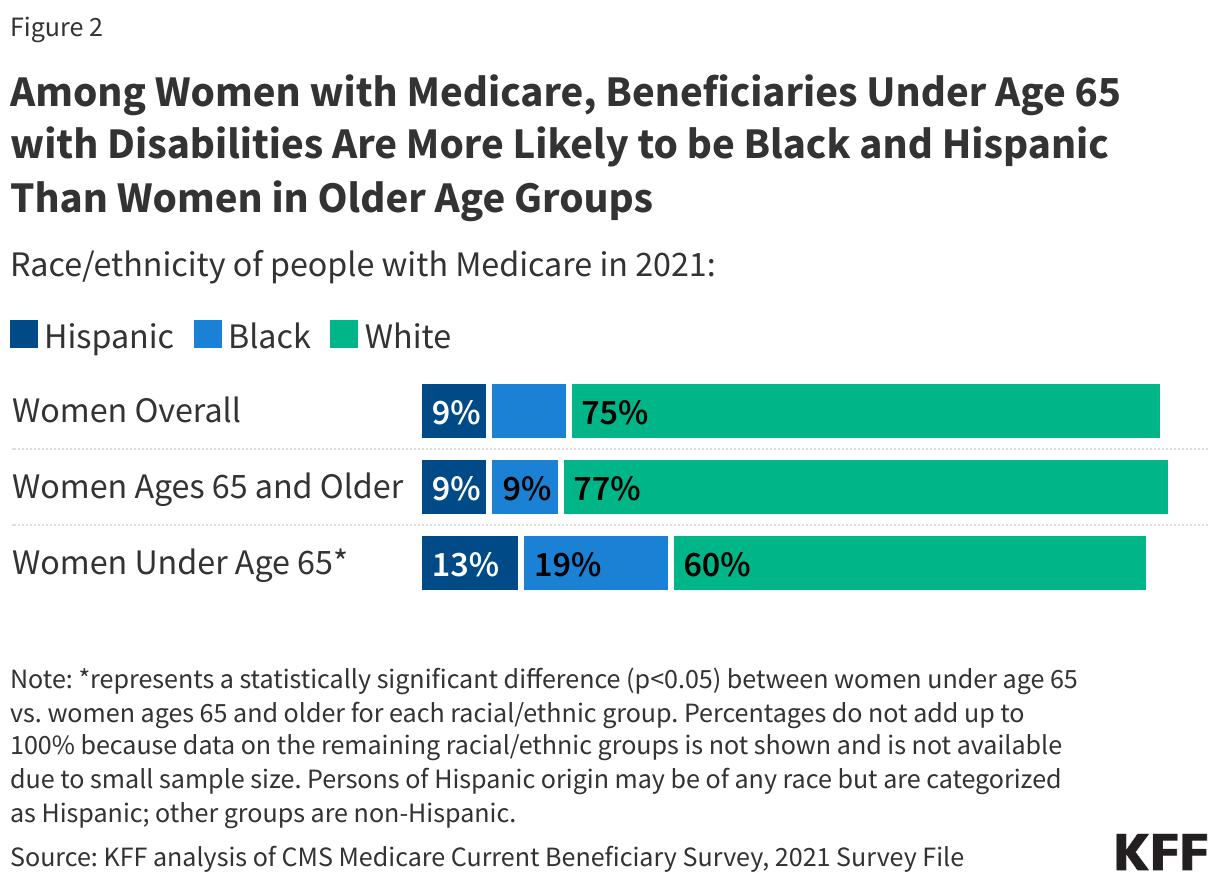

2. Among Women with Medicare, Beneficiaries Under Age 65 with Disabilities Are More Likely to be Black and Hispanic Than Women in Older Age Groups

Reflecting the demographics of older residents of the U.S., White people are the largest racial/ethnic group among people with Medicare, both men and women, while Black and Hispanic people together represent approximately 2 in 10 beneficiaries. Among women with Medicare, Black and Hispanic women represent larger shares of those under age 65 – who qualify for Medicare due to having a long-term disability – than of women ages 65 and older (Figure 2). People on Medicare who are under age 65 with disabilities report worse access to care, more cost concerns, and lower satisfaction.

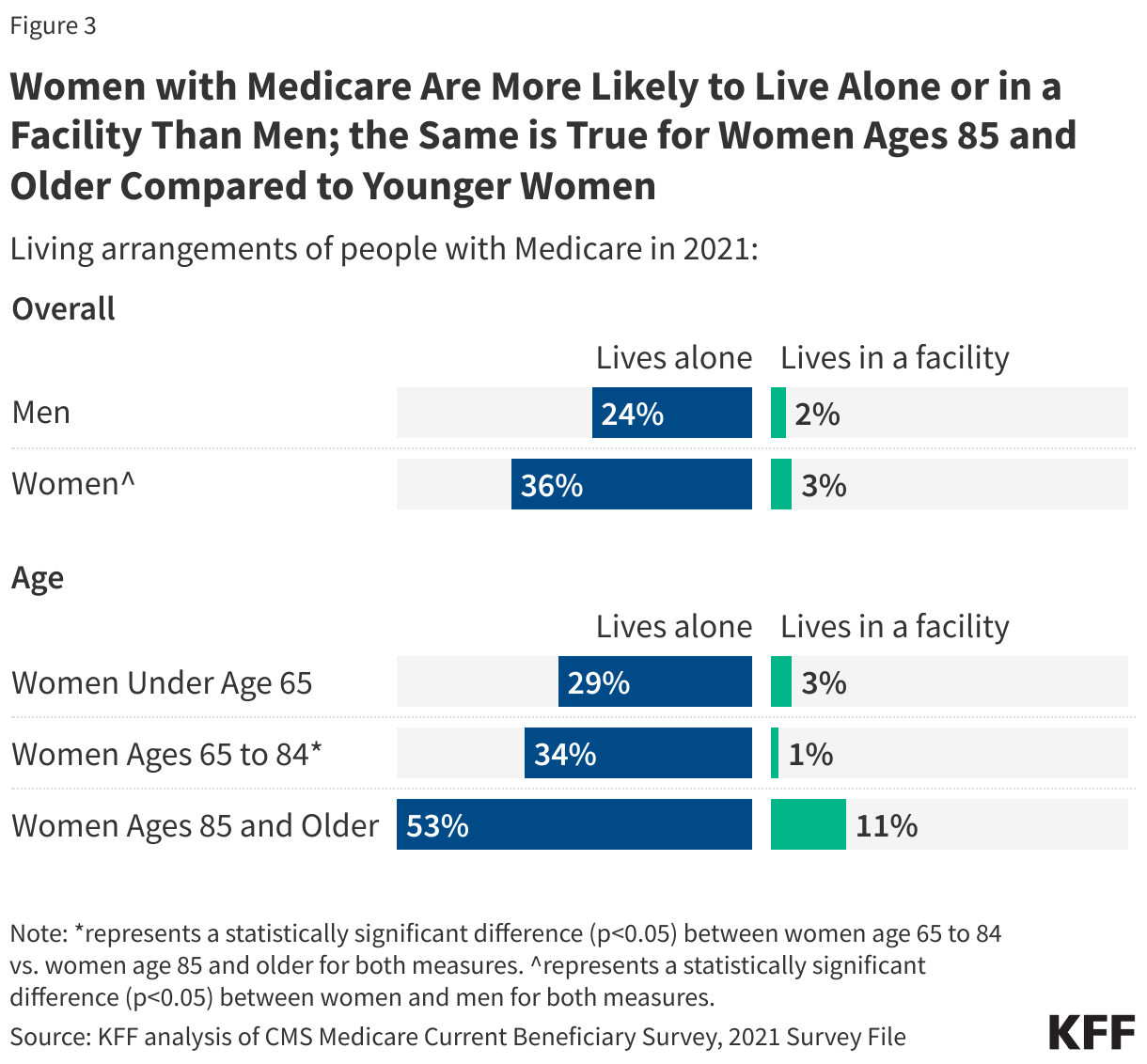

3. Women with Medicare Are More Likely to Live Alone or in a Facility Than Men; the Same is True for Women Ages 85 and Older Compared to Younger Women

Among Medicare beneficiaries, women are more likely than men to live alone, which may pose challenges as they grow older and are at greater likelihood of needing long-term care services and supports (LTSS). More than one-third of all women with Medicare (36%) live alone, rising to more than half (53%) of all women ages 85 and older (Figure 3). Women ages 85 and older are also considerably more likely than women ages 65 to 84 to live in facility (11% vs. 1%), including nursing homes, assisted living facilities, and other long-term care facilities. Medicare offers only time-limited coverage for skilled nursing facility services (up to 100 days) and does not typically cover long-term care services and supports needed by people who are unable to care for themselves in the community. (Medicaid is the primary payer of LTSS in the U.S., covering 20% of women with Medicare in 2021, as described below.)

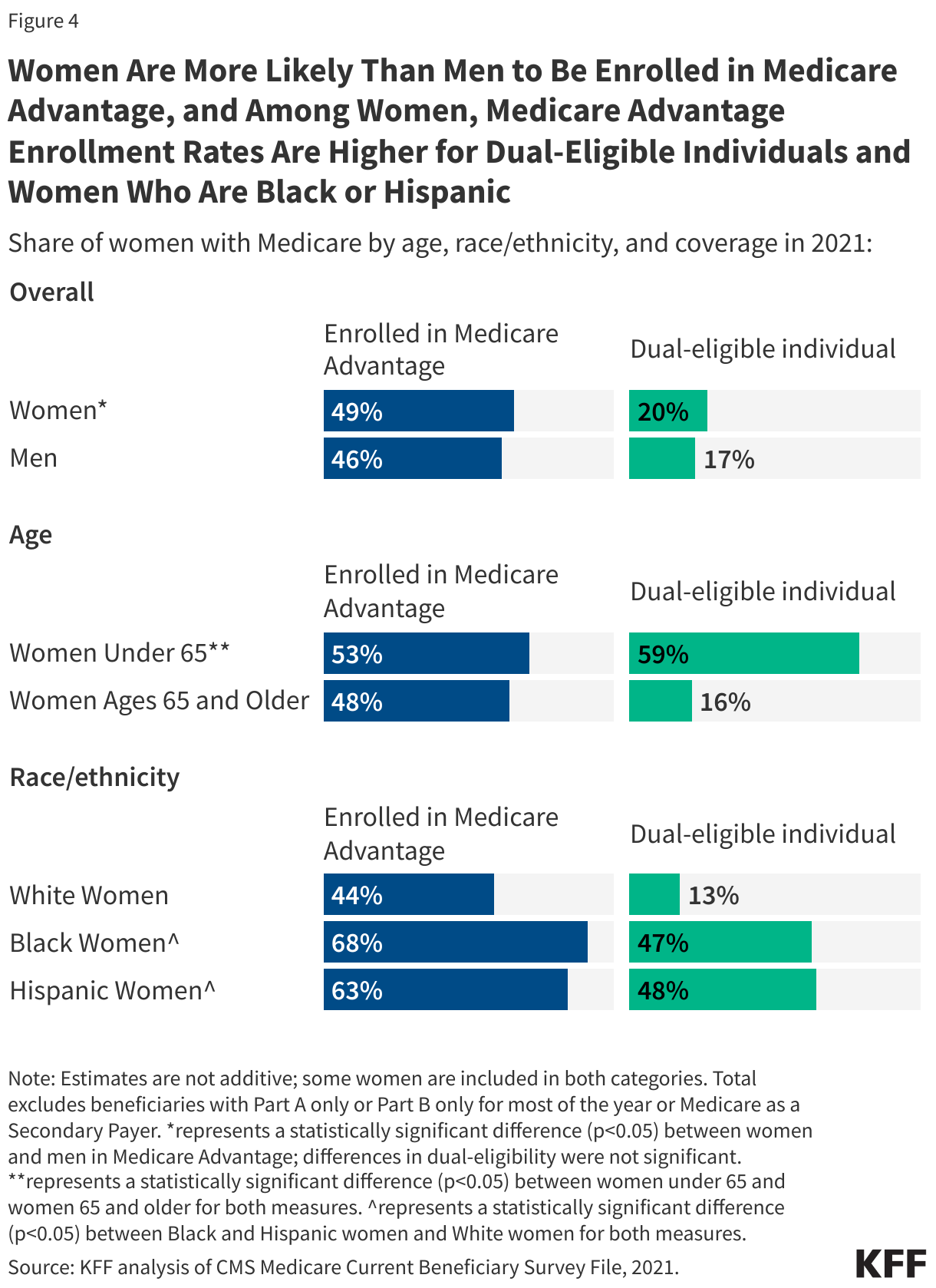

4. Women Are More Likely Than Men to Be Enrolled in Medicare Advantage, and Among Women, Medicare Advantage Enrollment Rates Are Higher for Dual-Eligible Individuals and Women Who Are Black or Hispanic

Medicare beneficiaries can choose to get their Medicare benefits through the traditional Medicare program or a private Medicare Advantage plan. Many Medicare beneficiaries also have some type of additional coverage, which can help with Medicare cost-sharing requirements and, in some instances, provides benefits not otherwise covered by Medicare. This includes Medicaid, the federal-state health insurance program for people with low-incomes and modest assets.

In 2021, 49% of women covered by Medicare were enrolled in Medicare Advantage plans, a significantly higher share than men (46%) (Figure 4). (The share of all eligible Medicare beneficiaries enrolled in Medicare Advantage has increased since then and now exceeds 50% of all eligible beneficiaries.) Larger shares of Black and Hispanic women with Medicare were enrolled in Medicare Advantage in 2021 than White women (68%, 63%, and 44%, respectively).

In 2021, 20% of women with Medicare were also enrolled in Medicaid. Women under 65 were enrolled in Medicaid at over three times the rate of women ages 65 and older (59% vs. 16%); Black (47%) and Hispanic (48%) women with Medicare were also significantly more likely to have Medicaid than White women (13%). Having supplemental Medicaid coverage gives women financial assistance in paying their Medicare deductibles and cost sharing, whether they receive their Medicare coverage through traditional Medicare or a Medicare Advantage plan. In addition, they qualify for coverage of long-term services and supports under Medicaid than can provide support for care in a facility or community-based at home supportive care to assist with a range of health and functional needs.

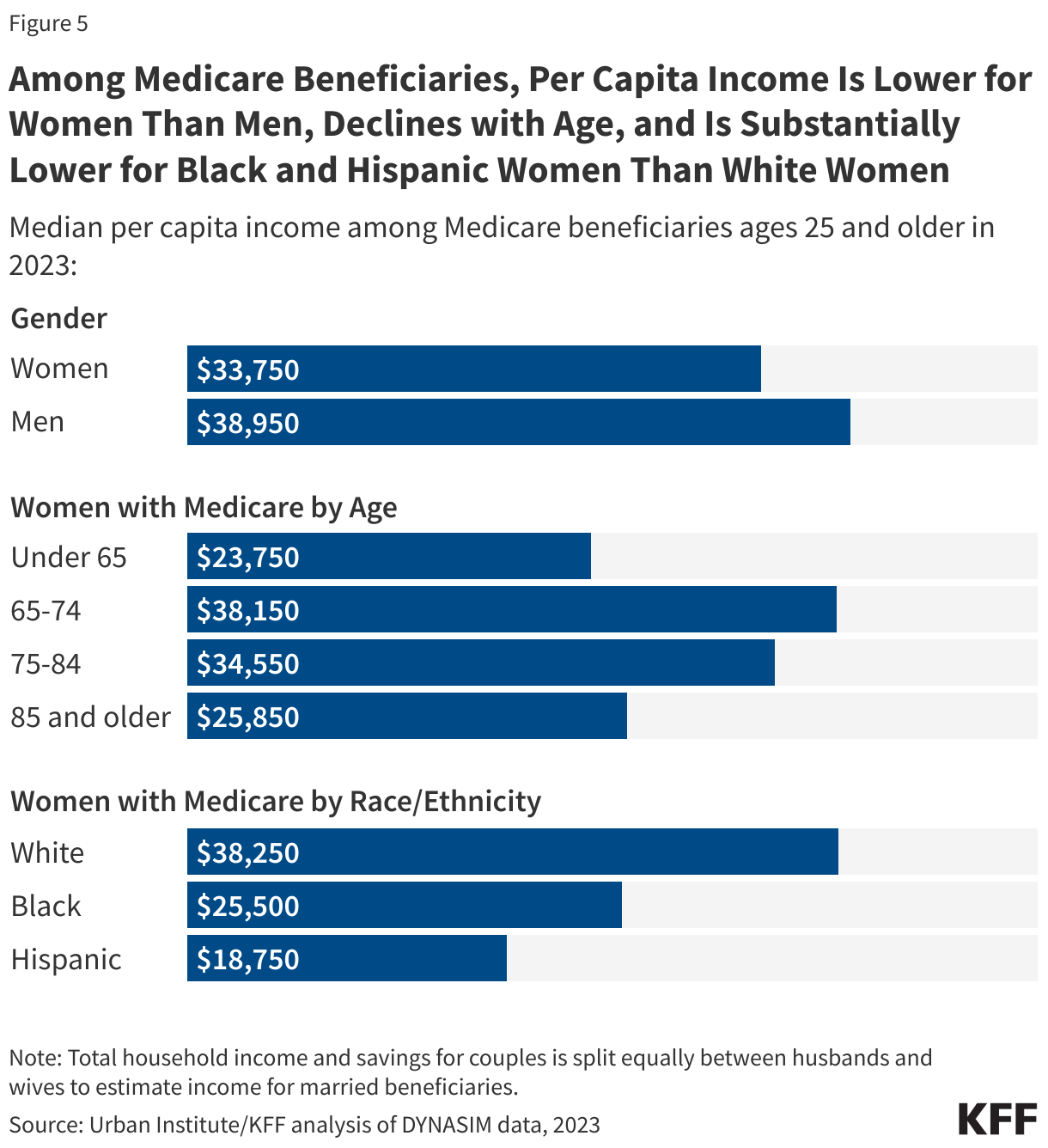

5. Per Capita Income Is Lower for Women with Medicare Than Men, Declines with Age, and Is Substantially Lower for Black and Hispanic Women Than White Women

Overall, women with Medicare have lower per capita incomes than men. This is largely due to the fact that average Social Security income and pension benefits are lower for women than men, primarily because women generally have lower-paying jobs than men during their working years and because many worked part-time or left the workforce for periods of time to raise families or care for aging family members. For example, the average annual Social Security benefit was substantially lower for women than men ages 65 and older in 2021 – $14,204 and $18,101, respectively.

KFF analysis shows that in 2023, half of all women with Medicare had per capita income of $33,750 or less, which is about $5,000 lower than median per capita income for men with Medicare ($38,950) (Figure 5). Among those ages 65 and older, median income declines with age, from $38,150 for women ages 65 to 74 to $25,850 for women 85 and older. Median income is also substantially lower for Black and Hispanic women compared to White women; half of all Black women with Medicare had per capita incomes of $25,500 or less, and half of all Hispanic women with Medicare had per capita incomes of $18,750 or less in 2023, compared to median per capita income of $38,250 for White women.

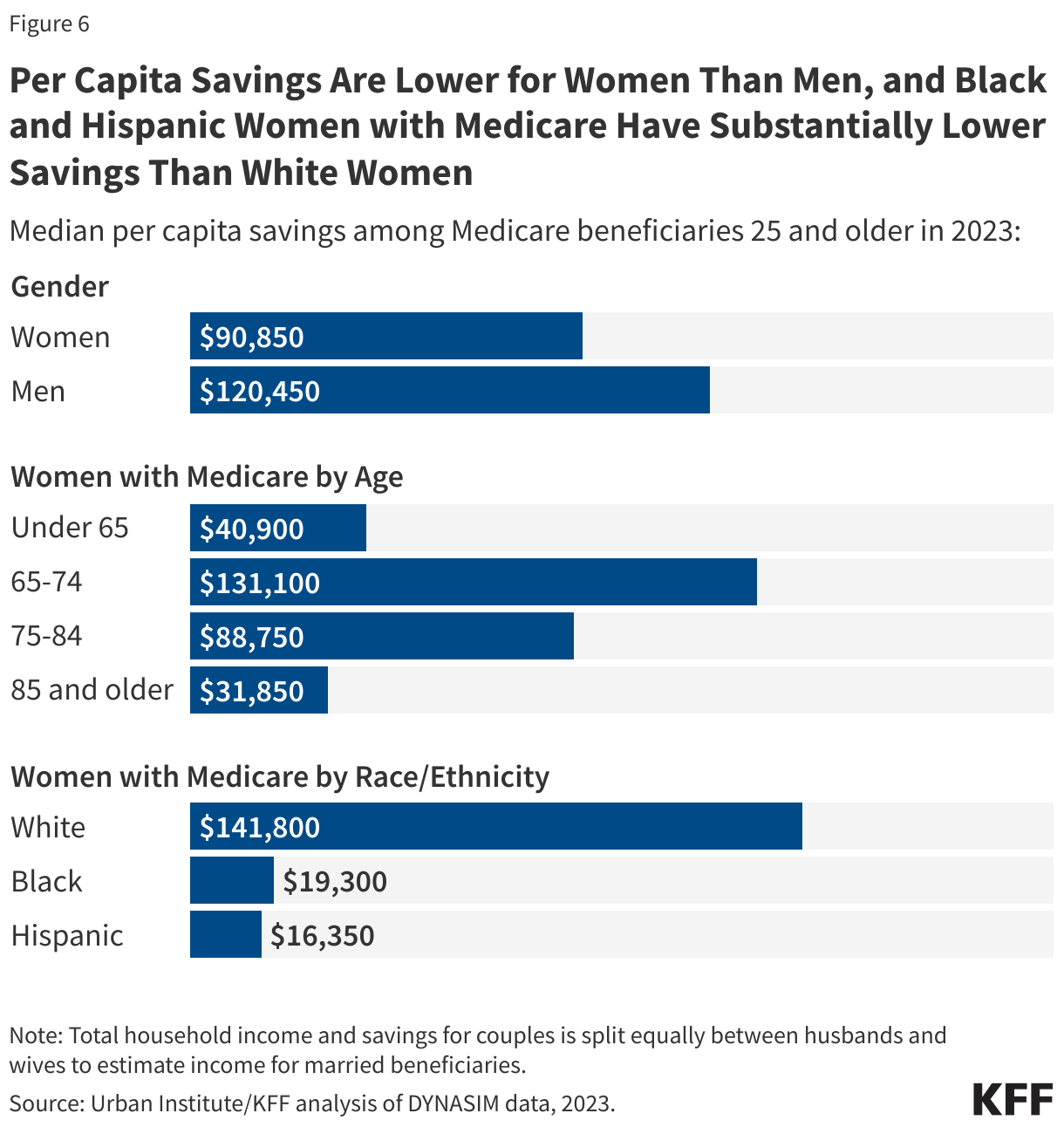

6. Per Capita Savings Are Lower for Women Than Men, and Black and Hispanic Women with Medicare Have Substantially Lower Savings Than White Women

As with income, savings are also much lower for women with Medicare compared to men, with half of all women having per capita savings of $90,850 or less compared to $120,450 for men (Figure 6). Among women with Medicare, both the youngest and the oldest age cohorts have substantially lower per capita savings than women ages 65 to 74 ($131,100, compared to $40,900 for those under age 65 and $31,850 for those ages 85 and older).

Median per capita savings are much lower for Black and Hispanic women than White women with Medicare. Half of all Black women have $19,300 or less in savings, which is 7 times lower than that of White women in 2023. Half of all Hispanic women have savings of $16,350 or less, which is nearly 9 times lower than that of White women. Differences in income and savings among Black and Hispanic women compared to White men and White women reflect the cumulative impact of differences in education, job opportunities, access to retirement benefits and inherited wealth. Women overall are also slightly more likely to have no savings or to be in debt compared to men (11% vs. 9%).

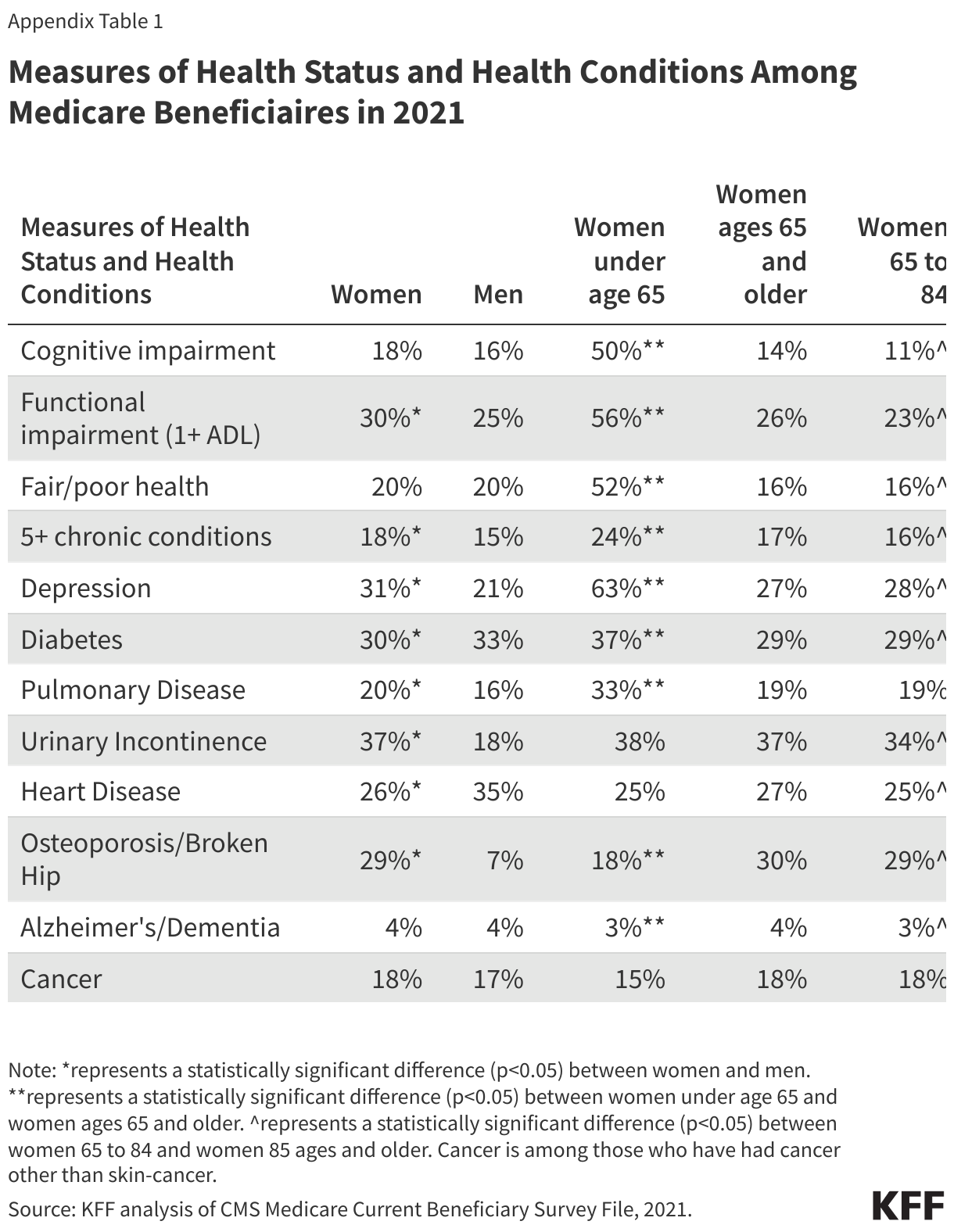

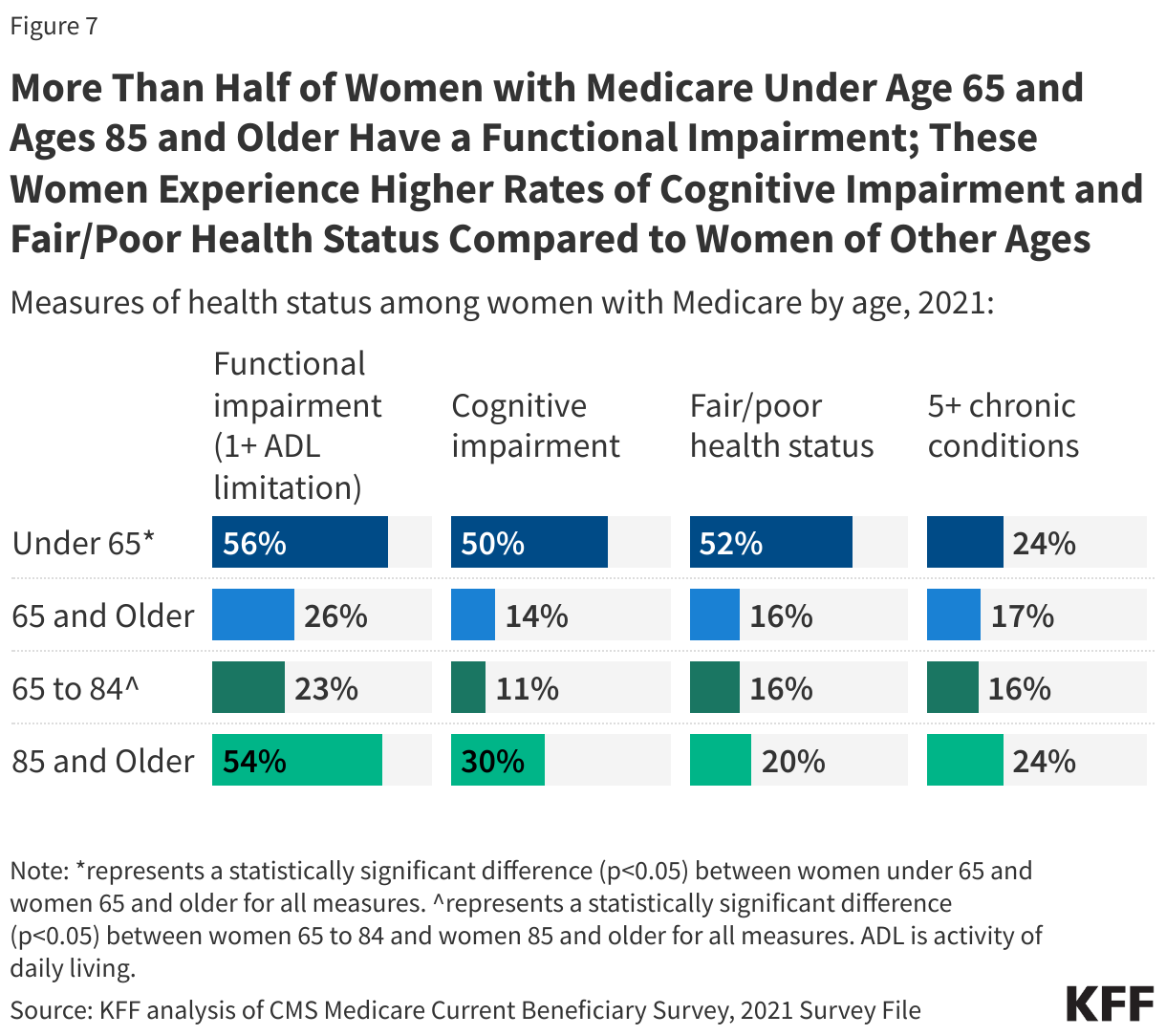

7. More Than Half of Women with Medicare Under Age 65 and Ages 85 and Older Have a Functional Impairment; These Women Experience Higher Rates of Cognitive Impairment and Fair/Poor Health Status Compared to Women of Other Ages

Reflecting the fact that for people under age 65, eligibility for Medicare is based on having a long-term disability, women with Medicare under age 65 experience considerably higher rates of functional and cognitive impairment and poorer health status than their older counterparts on Medicare. Half of those under age 65 have a cognitive impairment, over three times the rate of women ages 65 and older (14%) (Figure 7). Women under age 65 are also more likely to have a functional impairment (56%) than women ages 65 and older (26%). Women under age 65 report fair or poor health (52%) at over three times the rate of women ages 65 and older (16%) and are more likely to have 5 or more chronic conditions (24%) compared to older women (17%).

Measures of overall health, cognitive, and functional status also reflect the poorer health status of women in the oldest age cohort relative to other older women. More than half of women ages 85 and older have a functional impairment (54%), nearly double the rate among women ages 65 to 84 (23%). Nearly one-third of women ages 85 and older have a cognitive impairment (30%) compared to 11% of women ages 65 to 84. Women ages 85 and older are also significantly more likely than women ages 65 to 84 to be in fair or poor health (20% vs. 16%) and have 5 or more chronic conditions (24% vs. 16%).

A significantly higher share of women than men have a functional impairment including limitations in activities of daily living (30% of women vs. 25% of men) and have five or more chronic health conditions (18% vs. 15%) (Appendix Table 1). Similar shares of women and men have a cognitive impairment (18% vs. 16%), and report being in fair or poor health (20% for both groups).

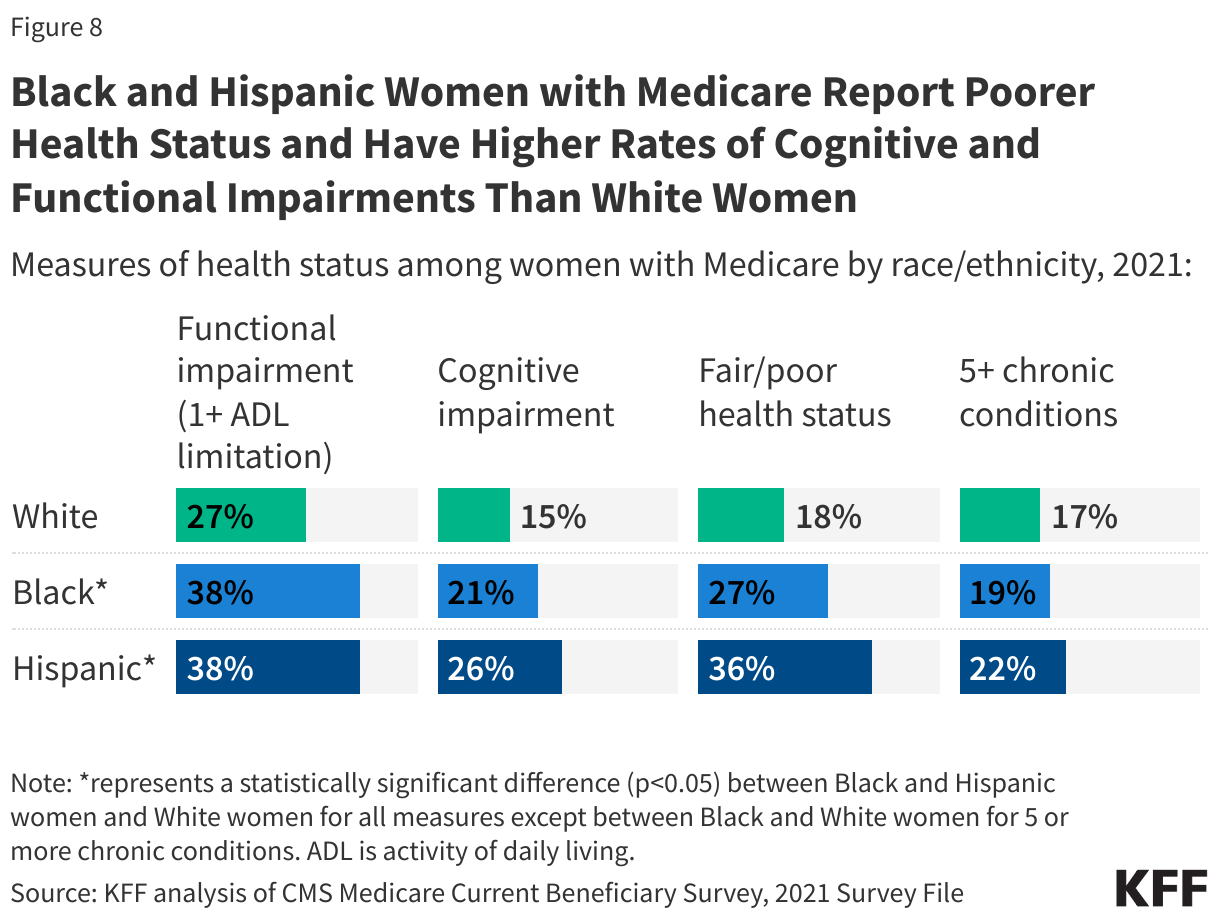

8. Black and Hispanic Women with Medicare Report Poorer Health Status and Have Higher Rates of Cognitive and Functional Impairments Than White Women

Black and Hispanic women with Medicare are significantly more likely than White women with Medicare to fare worse along certain measures of health status. For example, nearly four in ten (38%) Black and Hispanic women have a functional impairment compared to less than three in ten (27%) White women; 26% of Hispanic women and 21% of Black women have a cognitive compared to 16% of White women (Figure 8). Additionally, 36% of Hispanic women and 27% of Black women report being in fair or poor health compared to 18% of White women.

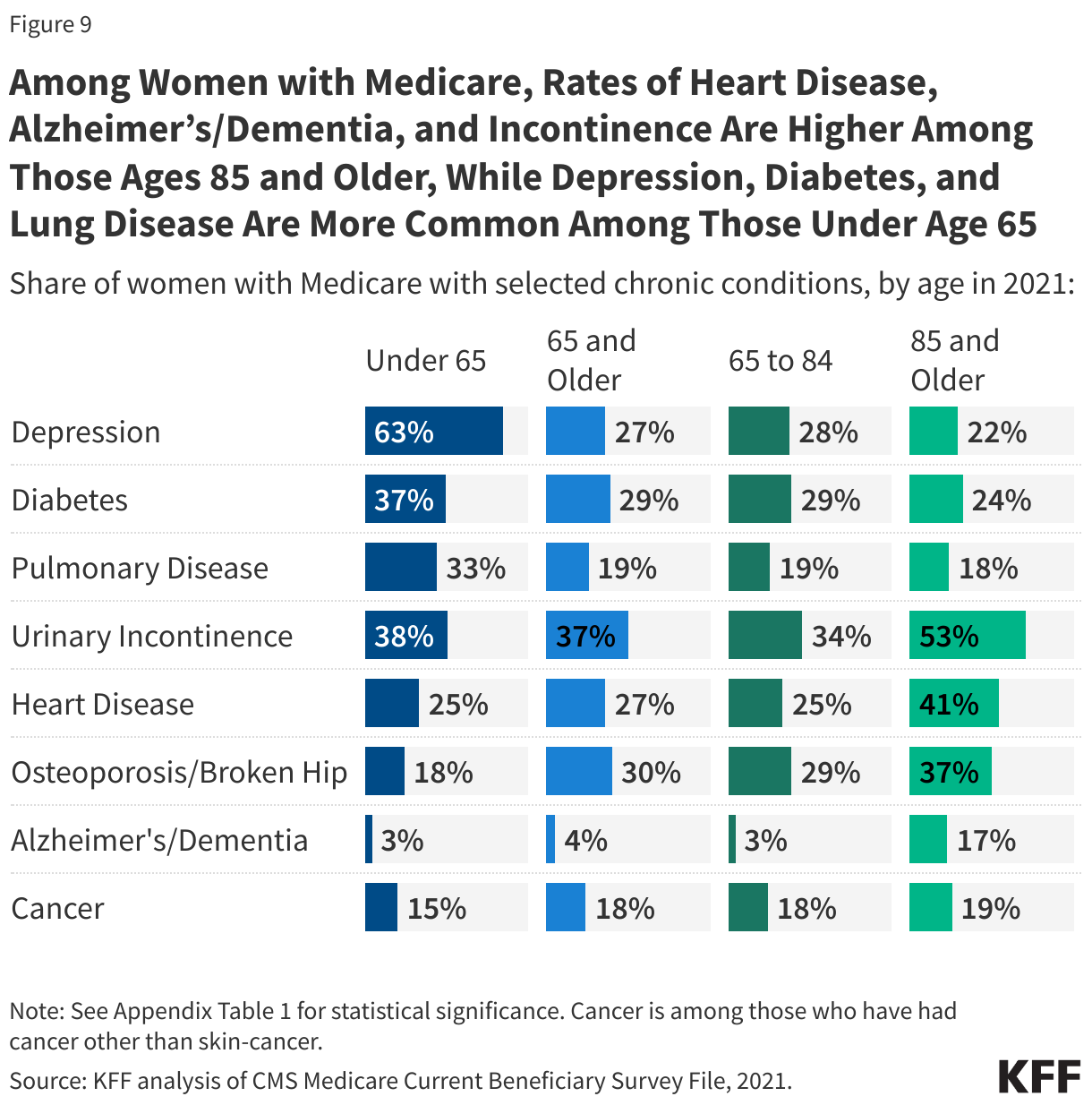

9. Among Women with Medicare, Heart Disease, Alzheimer’s/Dementia, and Incontinence Are More Common Among Those Ages 85 and Older; Depression, Lung Disease, and Diabetes Are More Common Among Those Under Age 65

Health conditions of women enrolled in Medicare differ by age cohort (Figure 9, Appendix Table 1). Women ages 85 and older are significantly more likely than women ages 65 to 84 to have heart disease (41% vs. 25%), Alzheimer’s/dementia (17% vs. 3%), and urinary incontinence (53% vs. 34%). Women under 65 are significantly more likely than women 65 and older to have depression (63% vs. 27%), diabetes (37% vs. 29%) and pulmonary disease (33% vs. 19%).

Women with Medicare overall experience higher rates of certain health conditions compared to men; for example, urinary incontinence (37% vs. 18%), depression (31% vs. 21%), osteoporosis (29% vs. 7%), and pulmonary disease (20% vs. 16%) (Appendix Table 1). Conversely, a larger share of men than women with Medicare had heart disease (35% vs. 26%) and diabetes (33% vs. 30%).

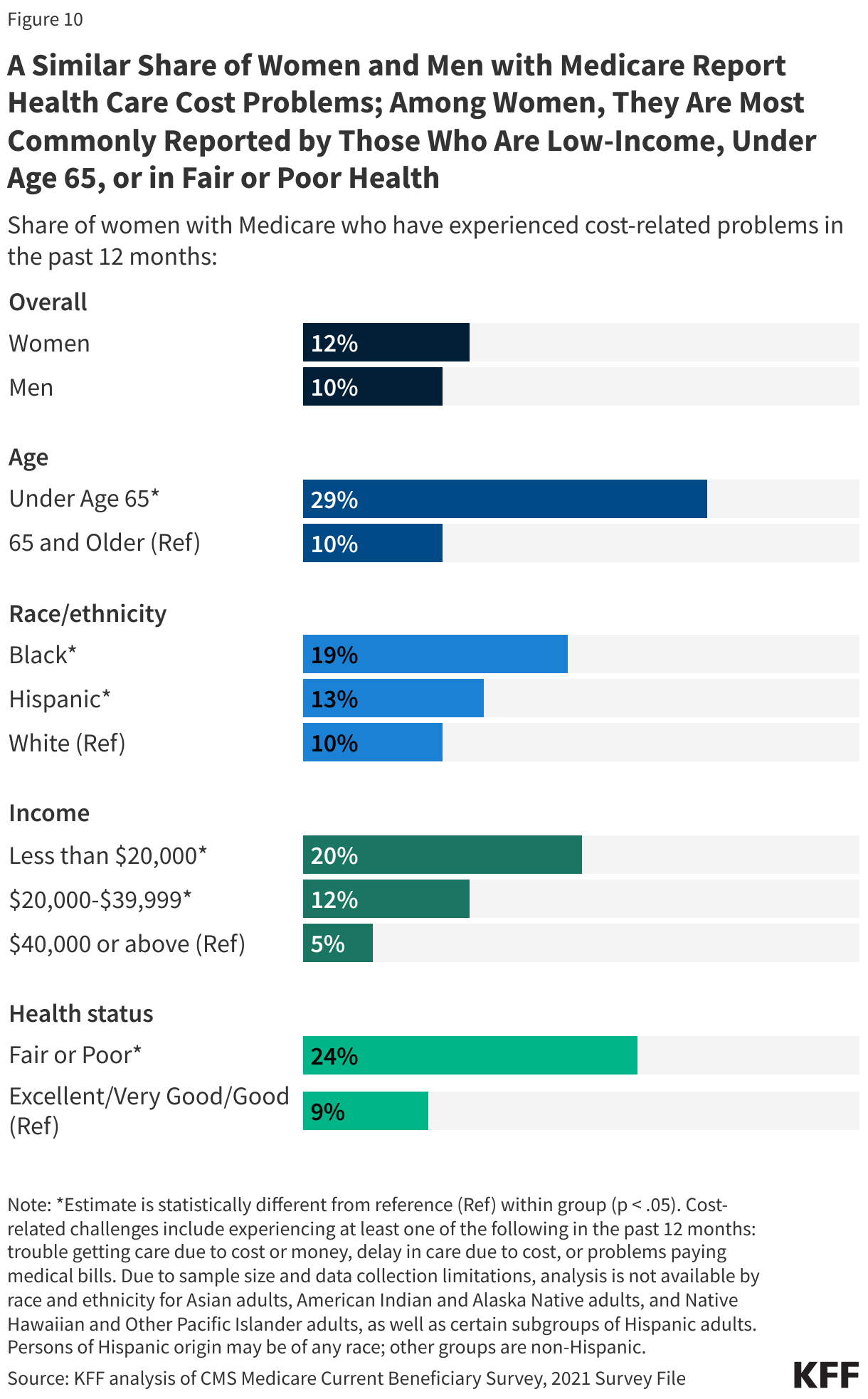

10. A Similar Share of Women and Men with Medicare Report Health Care Cost Problems; Among Women, They Are Most Commonly Reported by Those Who Are Low-Income, Under Age 65, or in Fair or Poor Health

Gaps in benefits, cost-sharing requirements, and premiums for Medicare and supplemental coverage can lead to cost-related challenges for some people with Medicare, including trouble getting care due to cost or money, delay in care due to cost, or problems paying medical bills. In 2021, a similar share of women and men with Medicare (12% vs 10%, respectively) reported that they faced at least one or more of these cost-related problems (Figure 10; data for men not shown). A higher share of women under age 65 (29%), Black (19%) and Hispanic (13%) women, women in fair or poor health (24%), and women with incomes below $20,000 (20%) reported experiencing more cost-related challenges than their counterparts.

Methods

This analysis is based on data from the Centers for Medicare & Medicaid Services 2021 Medicare Current Beneficiary Survey (MCBS) (the most recent year available), a nationally representative survey of Medicare beneficiaries. Sources of coverage are determined based on the source of coverage held for the most months of Medicare enrollment in 2021. For more information, see methods in the following brief: A Snapshot of Sources of Coverage Among Medicare Beneficiaries.

The analysis on cost-related problems excludes beneficiaries in institutional settings since the analysis was based on questions asked of community residents only. “Cost-related problems” was defined based on positive responses to any of the following four questions:

- Since (12 months prior), have you had any trouble getting health care that you wanted or needed because the cost was too high?

- Since (12 months prior), have you had any trouble getting health care that you wanted or needed because you did not have enough money?

- Since (12 months prior), have you delayed seeking medical care because you were worried about the cost?

- Since (12 months prior) have you had problems paying or were unable to pay any medical bills?

Income and asset levels in 2023 are based on the Urban Institute’s Dynamic Simulation of Income Model (DYNASIM4). DYNASIM4 is a dynamic microsimulation model that projects the population and analyzes the long-term distributional consequences of retirement and aging issues. See Income and Assets for Medicare Beneficiaries in 2023 for more information on methods.