Health Provisions in the 2025 Federal Budget Reconciliation Law

Editorial Note: Originally published Aug. 4, 2025, this summary has been updated to include the CBO’s coverage estimates for the relevant provisions.

Overview

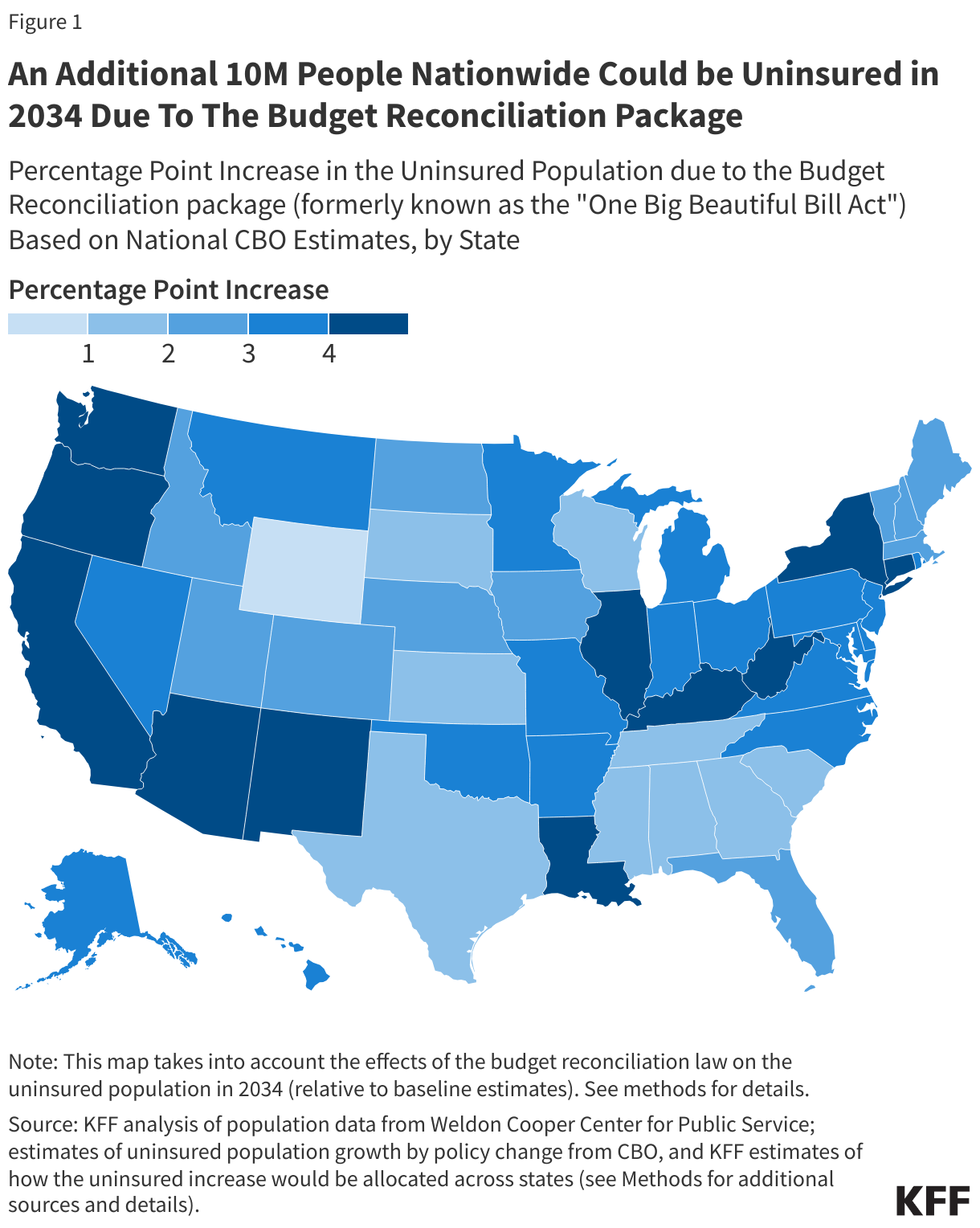

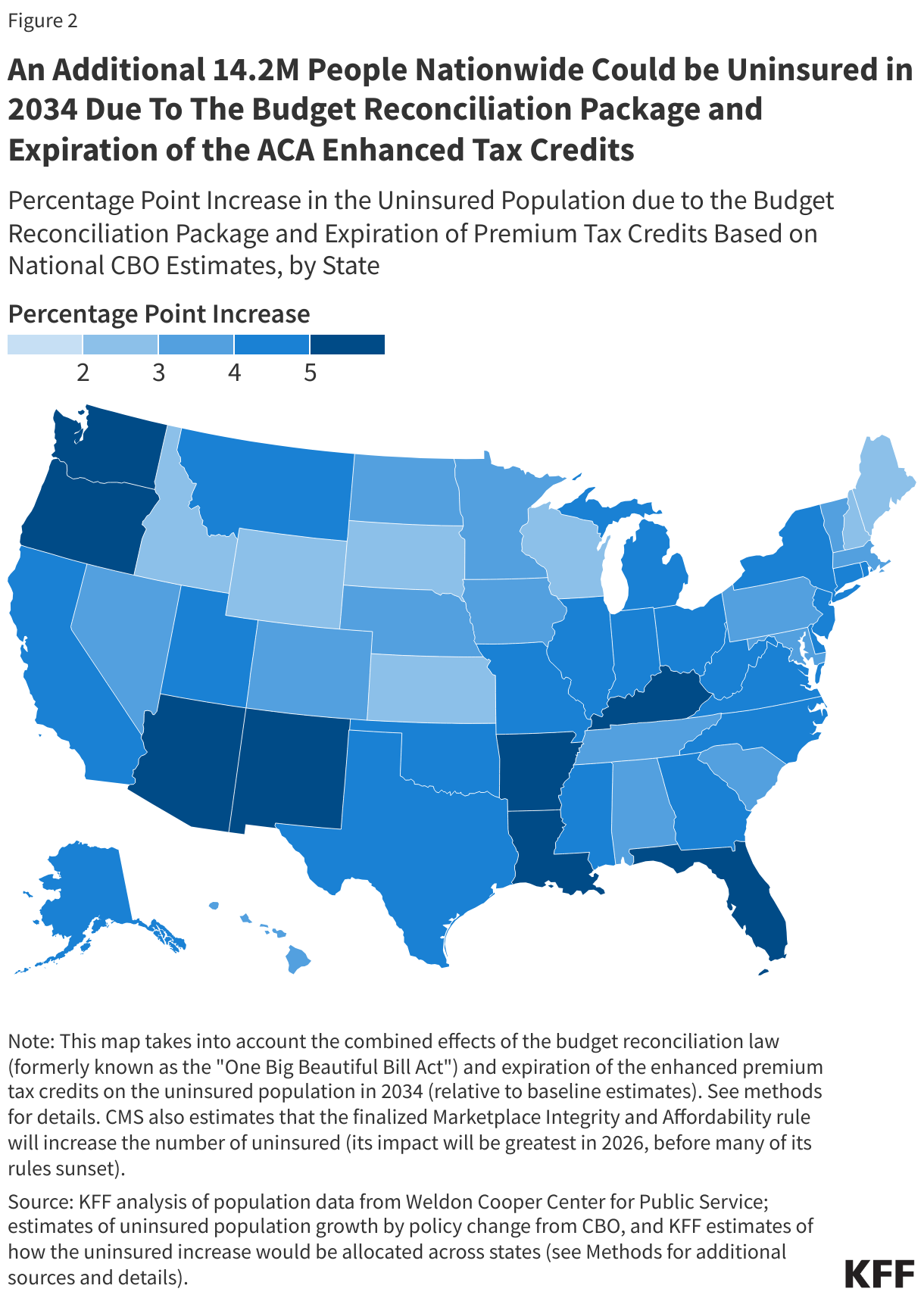

On July 3, the House passed the same version of the budget reconciliation bill that the Senate passed on July 1. On July 4, President Trump signed the bill, previously known as the “One Big Beautiful Bill Act,” into law. This summary describes the health care provisions in four categories: Medicaid, the Affordable Care Act, Medicare and Health Savings Accounts (HSAs). Included are the Congressional Budget Office (CBO) estimates for the impact of each provision (note coverage estimates for each provision will not sum to the law’s total coverage estimate). The CBO has stated the law will reduce federal spending on health care by over $1 trillion and lead to a 10 million increase in the country’s uninsured population.

An implementation timeline of the health provisions is available along with more background and a side-by-side comparison of the House and Senate passed bills.

Medicaid

Eligibility and Cost Sharing Policies

Section 71119: Work Requirements

Background

Prior to passage of the federal budget reconciliation law, Medicaid eligibility could not be conditioned on meeting a work or reporting requirement without obtaining a Medicaid Section 1115 waiver. During the first Trump administration, 13 states received approval to implement work requirements through Section 1115 waivers. Work requirement waiver approvals were either rescinded by the Biden administration or withdrawn by states, and Georgia is the only state with a Medicaid work requirement waiver currently in place. Since the beginning of Trump’s second term, some states have shown renewed interest in pursuing work requirement policies through 1115 waivers.

Description

- Requires states to condition Medicaid eligibility for individuals ages 19-64 applying for coverage or enrolled through the ACA expansion group (or a waiver) on working or participating in qualifying activities for at least 80 hours per month or attending school at least half-time.

- Mandates that states exempt certain adults, including parents with children ages 13 and under, those who are medically frail, and those who are participating in a substance use disorder treatment program, from the requirements.

- Requires states to verify that individuals applying for coverage meet the requirements for 1 and up to a maximum of 3 consecutive months preceding the month of application and that individuals who are enrolled meet the requirements for 1 or more months between the most recent eligibility redeterminations (at least twice per year).

- Requires states to use data matching “where possible” to verify whether an individual meets the requirement or qualifies for an exemption.

- Specifies that if a person is denied or disenrolled due to work requirements, they are also ineligible for subsidized Marketplace coverage.

- Prohibits these provisions from being waived, including under Section 1115 authority.

- Allows the Secretary to exempt states from compliance with the new requirements until no later than December 31, 2028, if the state is demonstrating a good faith effort to comply and submits progress in compliance or other barriers to compliance.

- Provides $200 million in funding to states for systems development for FY 2026 and an additional $200 million to HHS to support implementation (for FY 2026).

Effective Date: Not later than December 31, 2026, or earlier at state option.

Budgetary and Coverage Impact

CBO estimates this provision will reduce federal Medicaid spending by $326 billion over 10 years and will increase the number of people who are uninsured by 5.3 million in 2034.

KFF Resources

- A Closer Look at the Medicaid Work Requirement Provisions in the “Big Beautiful Bill”

- Implementing Work Requirements on a National Scale: What We Know from State Waiver Experience

- Implications of Medicaid Work and Reporting Requirements for Adults with Mental Health or Substance Use Disorders

- Medicaid Work Requirements: Implications for Low Income Women’s Coverage

- Understanding the Intersection of Medicaid and Work: An Update

- Different Data Source, But Same Results: Most Adults Subject to Medicaid Work Requirements Are Working or Face Barriers to Work

- 5 Key Facts About Medicaid Work Requirements

- An Overview of Medicaid Work Requirements: What Happened Under the Trump and Biden Administrations?

- Section 1115 Waiver Tracker Work Requirements

Section 71107: More Frequent Eligibility Determinations

Background

Under the Affordable Care Act (ACA), states are required to renew eligibility every 12 months for Medicaid enrollees whose eligibility is based on modified adjusted gross income (MAGI), including children, pregnant individuals, parents, and expansion adults. For enrollees whose eligibility is based on age 65+ or disability, states must renew eligibility at least every 12 months . States are required to review eligibility within the 12-month period if they receive information about a change in a beneficiary’s circumstances that may affect eligibility.

Description

- Requires states to conduct eligibility redeterminations every 6 months for Medicaid expansion adults.

- Provides $75 million in implementation funding for FY 2026.

Effective Date: For renewals scheduled on or after December 31, 2026.

Budgetary and Coverage Impact

CBO estimates this provision will reduce federal Medicaid spending by $63 billion over 10 years years and will increase the number of people who are uninsured by 700,000 in 2034.

KFF Resources

- Medicaid and CHIP Eligibility, Enrollment, and Renewal Policies as States Resume Routine Operations Following the Unwinding of the Pandemic-Era Continuous Enrollment Provision

- Recent Medicaid/CHIP Enrollment Declines and Barriers to Maintaining Coverage

Section 71103: Verifying Enrollee Address and Other Information

Background

The Eligibility and Enrollment final rule issued in April 2024 requires states to leverage reliable data sources to update enrollee address information, effective June 2025.

Description

- Requires states to update enrollee address information using reliable data sources, including the National Change of Address Database and managed care entities.

- Requires the Secretary to establish a system to share information with states for purposes of preventing individuals from being simultaneously enrolled in two states and requires states to submit monthly enrollee SSNs and other information to the system.

Effective Date: January 1, 2027 for states to obtain contact information; October 1, 2029 to establish system to prevent enrollment in two states simultaneously.

Budgetary and Coverage Impact

CBO estimates this provision will reduce federal Medicaid spending by $17 billion over 10 years. This provision is not expected to impact the number of people who are uninsured.

KFF Resources

Section 71104: Ensuring Deceased Individuals Do Not Remain Enrolled

Description

- Requires states to review the Master Death File at least quarterly to determine if any enrolled individuals are deceased.

Effective Date: January 1, 2027.

Budgetary and Coverage Impact

CBO estimates this provision will not affect federal Medicaid spending over 10 years. This provision is not expected to impact the number of people who are uninsured.

KFF Resources

Section 71102: Eligibility and Enrollment Final Rule

Background

In April 2024, CMS issued a final rule to streamline application and enrollment processes in Medicaid, align renewal policies for all Medicaid enrollees, facilitate transitions between Medicaid, CHIP, and subsidized Marketplace coverage, and eliminate certain barriers in CHIP. Implementation deadlines for states vary across provisions, but many provisions in the rule are already in effect, and for others, states are already in compliance.

Description

- Prohibits the Secretary from implementing, administering, or enforcing certain provisions that have not yet taken effect in an April 2024 CMS final rule until October 1, 2034.

Effective Date: Upon enactment.

Budgetary and Coverage Impact

CBO estimates this provision will reduce federal Medicaid spending by $56 billion over 10 years and will increase the number of people who are uninsured by 400,000 in 2034.

KFF Resources

- Medicaid Changes in House and Senate Reconciliation Bills Would Increase Costs for 1.3 Million Low-Income Medicare Beneficiaries

- 5 Things to Know: A Look at the Proposed Medicaid Eligibility & Enrollment Rule

- What Does the Medicaid Eligibility Rule Mean for Low-Income Medicare Beneficiaries and the Medicare Savings Programs (MSPs)?

- Potential Effects of the Proposed Medicaid Eligibility Rule for Newly Enrolled Medicare-Medicaid Enrollees

Section 71101: Medicare Savings Program Final Rule

Background

In September 2023, CMS issued a final rule to reduce barriers to enrollment in Medicare Savings Programs (MSPs), which provide Medicaid coverage of Medicare premiums and cost sharing for low-income Medicare beneficiaries. Implementation deadlines for states vary across provisions in the rule, but many provisions are already in effect, and for others, states are already in compliance.

Description

- Prohibits the Secretary from implementing, administering, or enforcing certain provisions in a September 2023 final rule that have not yet taken effect until October 1, 2034.

Effective Date: Upon enactment.

Budgetary and Coverage Impact

CBO estimates this provision will reduce federal Medicaid spending by $66 billion over 10 years. This provision is not expected to impact the number of people who are uninsured.

KFF Resources

- Medicaid Changes in House and Senate Reconciliation Bills Would Increase Costs for 1.3 Million Low-Income Medicare Beneficiaries

- 5 Things to Know: A Look at the Proposed Medicaid Eligibility & Enrollment Rule

- What Does the Medicaid Eligibility Rule Mean for Low-Income Medicare Beneficiaries and the Medicare Savings Programs (MSPs)?

- Potential Effects of the Proposed Medicaid Eligibility Rule for Newly Enrolled Medicare-Medicaid Enrollees

Section 71109: Restricting Immigrant Eligibility for Medicaid and CHIP

Background

In addition to meeting other eligibility requirements, lawfully present immigrants must have a “qualified” immigration status to be eligible for Medicaid or CHIP. Qualified immigrants include: lawful permanent residents (LPRs); refugees; individuals granted parole for at least one year; individuals granted asylum or related relief; certain abused spouses and children; certain victims of trafficking; Cuban and Haitian entrants; and citizens of the Freely Associated States (COFA migrants) residing in states and territories. Many lawfully present immigrants must wait five years after obtaining qualified status before they may enroll in Medicaid; states may waive the five-year wait for children and pregnant individuals (referred to as the ICHIA option). Some states have state-only funded coverage programs for undocumented immigrants.

Description

- Restricts the definition of qualified immigrants for purposes of Medicaid or CHIP eligibility to Lawful Permanent Residents (“green card” holders), certain Cuban and Haitian immigrants, citizens of the Freely Associated States (COFA migrants) lawfully residing in the US, and lawfully residing children and pregnant adults in states that cover them under the ICHIA option.

- Provides $15 million in implementation funding for FY 2026.

Effective Date: October 1, 2026.

Budgetary and Coverage Impact

CBO estimates this provision will reduce federal Medicaid spending by $6 billion over 10 years and will increase the number of people who are uninsured by 100,000 in 2034.

KFF Resources

Section 71112: Retroactive Coverage

Background

Under current law, states are required to provide Medicaid coverage for qualified medical expenses incurred up to 90 days prior to the date of application for coverage.

Description

- Limits retroactive coverage to one month prior to application for coverage for individuals enrolled through the Medicaid expansion and two months prior to application for coverage for traditional enrollees.

- Provides $15 million in implementation funding for FY 2026.

Effective Date: January 1, 2027.

Budgetary and Coverage Impact

CBO estimates this provision will reduce federal Medicaid spending by $4 billion over 10 years and will increase the number of people who are uninsured by 100,000 in 2034.

Section 71120: New Cost Sharing Requirements for Certain Expansion Individuals

Background

States have the option to charge premiums and cost-sharing for Medicaid enrollees within limits, and certain populations and services (emergency, family planning, pregnancy and preventive) are exempt from cost-sharing. Cost-sharing is generally limited to nominal amounts but may be higher for those with income above 100% of the federal poverty level (FPL). Out-of-pocket costs cannot exceed 5% of family income. States may allow providers to deny services to enrollees for nonpayment of copayments.

Description

- Requires states to impose cost sharing of up to $35 per service on expansion adults with incomes 100-138% FPL; maintains existing exemptions of certain services from cost sharing and exempts primary care, mental health, and substance use disorder services and services provided by federally qualified health centers, behavioral health clinics, and rural health clinics from cost sharing; limits cost sharing for prescription drugs to nominal amounts.

- Maintains the 5% of family income cap on out-of-pocket costs.

- Permits states to allow providers to deny services for failure to pay cost sharing but does not prevent providers from reducing or waiving cost sharing.

- Eliminates enrollment fees or premiums for expansion adults.

Effective Date: October 1, 2028.

Budgetary and Coverage Impact

CBO estimates this provision will reduce federal Medicaid spending by $7 billion over 10 years. This provision is not expected to impact coverage.

KFF Resources

- Cost Sharing Requirements Could Have Implications for Medicaid Expansion Enrollees With Higher Health Care Needs

- Understanding the Impact of Medicaid Premiums & Cost-Sharing: Updated Evidence from the Literature and Section 1115 Waivers

Financing

Section 71115: Provider Taxes

Background

States are permitted to finance the non-federal share of Medicaid spending through multiple sources, including state general funds, health care related taxes (or “provider taxes”), and local government funds. Federal rules specify provider taxes must be broad-based and uniform (i.e., states can’t limit provider taxes to only Medicaid providers) and may not hold providers “harmless” (i.e., guarantee providers receive their money back). The hold harmless requirement does not apply when tax revenues comprise 6% or less of providers’ net patient revenues from treating patients (referred to as the “safe harbor” limit).

Description

- Prohibits all states from establishing any new provider taxes or from increasing the rates of existing taxes.

- Reduces the safe harbor limit for states that have adopted the ACA expansion by 0.5% annually starting in fiscal year 2028 until the safe harbor limit reaches 3.5% in FY 2032.

- Applies the new safe harbor limit in expansion states to state and local government taxes on all providers except nursing facilities and intermediate care facilities.

- Provides $20 million in implementation funding for FY 2026.

Effective Date: Upon enactment for prohibition of new or increased taxes; October 1, 2027 for reduction in safe harbor limit.

Budgetary and Coverage Impact

CBO estimates this provision will reduce federal Medicaid spending by $191 billion over 10 years and will increase the number of people who are uninsured by 1.1 million in 2034.

KFF Resources

- Which States Might have to Reduce Provider Taxes Under the Senate Reconciliation Bill?

- 5 Key Facts About Medicaid and Provider Taxes

- Medicaid Budget Survey 2024-2025 – Provider Rates and Taxes

Section 71117: Requirements for Provider Tax Uniformity Waivers

Background

States are permitted to finance the non-federal share of Medicaid spending through multiple sources, including state general funds, health care related taxes (or “provider taxes”), and local government funds. Federal rules specify provider taxes must be broad-based and uniform (i.e., states can’t limit provider taxes to only Medicaid providers) and may not hold providers “harmless” (i.e., guarantee providers receive their money back).

Description

- Revises the conditions under which states may receive a waiver of the requirement that taxes be broad-based and uniform so that some currently permissible taxes, such as those on managed care plans, will no longer be permissible in future years.

- Provision overlaps with a proposed rule released May 12, 2025.

Effective Date: Upon enactment; HHS Secretary may provide a transition period of up to three years.

Budgetary and Coverage Impact

CBO estimates this provision will reduce federal Medicaid spending by $35 billion over 10 years and will increase the number of people who are uninsured by 100,000 in 2034.

KFF Resources

- Which States Might have to Reduce Provider Taxes Under the Senate Reconciliation Bill?

- 5 Key Facts About Medicaid and Provider Taxes

- Medicaid Budget Survey 2024-2025 – Provider Rates and Taxes

Section 71116: State Directed Payments

Background

States are generally not permitted to direct how managed care organizations (MCOs) pay their providers. However, subject to CMS approval, states may use “state directed payments” (SDPs) to require MCOs to pay providers certain rates, make uniform rate increases (that are like fee-for-service supplemental payments), or to use certain payment methods.

A 2024 rule on access to care in Medicaid managed care codified that the upper limit for SDPs is the average commercial rate for hospitals and nursing facilities, which is generally higher than the Medicare payment ceiling used for other Medicaid fee-for-service supplemental payments.

Description

- Directs HHS to revise Medicaid regulations for state directed payment to cap the total payment rate for inpatient hospital and nursing facility services at 100% of the total published Medicare payment rate for expansion states and at 110% of the total published Medicare payment rate for non-expansion states.

- Prevents payments approved after May 1, 2025 in excess of the new limits from taking effect unless they are for rural hospitals.

- Reduces existing payments that are above the allowable Medicare-related payment limit by 10 percentage points each year until they reach the new lower limit.

- Specifies that in the absence of published Medicare payment rates, the limit is set at the Medicaid fee-for-service payment rate.

Effective Date: Upon enactment for lower limit on new state directed payments; January 1, 2028 for reduction in existing state directed payments above new allowable Medicare-related limit.

Budgetary and Coverage Impact

CBO estimates this provision will reduce federal Medicaid spending by $149 billion over 10 years. This provision is not expected to impact coverage.

KFF Resources

- Reconciliation Language Could Lead To Cuts in Medicaid State-Directed Payments to Hospitals and Nursing Facilities

- 10 Things to Know About Medicaid Managed Care

- 5 Key Facts about Medicaid and Hospitals

- Medicaid Budget Survey FY 2024-2025, Provider Rates and Taxes

Section 71118: Section 1115 Demonstration Waiver Budget Neutrality

Background

Under long-standing policy and practice, Section 1115 demonstration waivers must be “budget neutral” to the federal government over the course of the waiver. Federal costs under an 1115 waiver may not exceed what they would have been for that state without the waiver. Typically, budget neutrality calculations are determined on a per enrollee basis—so, per enrollee spending over the course of the waiver (usually 5 years) cannot exceed the projected per enrollee spending calculated in the “without-waiver baseline.”

Budget neutrality calculations and the use of “savings” when expenditures decrease on account of the waiver are negotiated between states and CMS and the Office of Management and Budget.

Description

- Specifies the Chief Actuary for CMS must certify 1115 waivers are not expected to result in an increase in federal expenditures compared to federal expenditures without the waiver.

- Provides $5 million in implementation funding for each of FY 2026 and FY 2027.

Effective Date: January 1, 2027.

Budgetary and Coverage Impact

CBO estimates this provision will reduce federal Medicaid spending by $3 billion over 10 years. This provision is not expected to impact coverage.

KFF Resources

Section 71106: Payment Reduction for Certain Erroneous Medicaid Payments

Background

Federal law directs CMS to recoup federal funds for erroneous payments made for ineligible individuals and overpayments for eligible individuals if the state’s eligibility “error rate” exceeds 3%. CMS may waive the recoupment if the Medicaid agency has taken steps to demonstrate a “good faith” effort to get below the 3% allowable threshold.

Description

- Requires HHS to reduce federal financial participation to states for identified improper payment errors related to payments made for ineligible individuals and overpayments made for eligible individuals.

- Expands the definition of improper payments to include payments where insufficient information is available to confirm eligibility.

Effective Date: October 1, 2029.

Budgetary and Coverage Impact

CBO estimates this provision will reduce federal Medicaid spending by $8 billion over 10 years and will increase the number of people who are uninsured by 100,000 in 2034.

KFF Resources

Medicaid Expansion

Section 71114: Eliminating Temporary Financial Incentive for Medicaid Expansion

Background

The Affordable Care Act expands Medicaid eligibility to non-elderly adults with incomes up to 138% FPL based on modified adjusted gross income and provides 90% federal financing for the expansion population. The Supreme Court effectively made expansion an option for states. The American Rescue Plan Act (ARPA) added a temporary financial incentive for states that newly adopt expansion. Currently, 41 states, including DC, have implemented the Medicaid expansion.

Description

- Eliminates the temporary incentive for states that newly adopt the Medicaid expansion.

Effective Date: January 1, 2026.

Budgetary and Coverage Impact

CBO estimates this provision will reduce federal Medicaid spending by $14 billion over 10 years and will increase the number of people who are uninsured by 100,000 in 2034.

KFF Resources

- 5 Key Facts About Medicaid Expansion

- New Incentive for States to Adopt the ACA Medicaid Expansion: Implications for State Spending

- Eliminating the Medicaid Expansion Federal Match Rate: State-by-State Estimates

- Medicaid Expansion Tracker

Section 71110: Federal Medical Assistance Percentage (FMAP) for Emergency Medicaid

Background

Emergency Medicaid reimburses hospitals for the costs of emergency care provided to immigrants who would qualify for Medicaid except for their immigration status, which hospitals are required to provide under federal law. States receive federal matching payments based on the federal medical assistance percentage (FMAP), which is computed using a formula that takes into account states’ per capita income, for traditional populations; they receive a 90% federal match rate for individuals enrolled in the Medicaid expansion.

Description

- Limits federal matching payments for Emergency Medicaid for individuals who would otherwise be eligible for expansion coverage except for their immigration status to the state’s regular FMAP.

- Provides $1 million in implementation funding for FY 2026.

Effective Date: October 1, 2026.

Budgetary and Coverage Impact

CBO estimates this provision will reduce federal Medicaid spending by $28 billion over 10 years. This provision is not expected to impact coverage.

KFF Resources

Long-term Care

Section 71111: Nursing Home Staffing Final Rule

Background

A 2024 Biden-administration final rule requires long-term care facilities (LTC) to meet minimum staffing levels (including a 24/7 RN on-site and a minimum of 3.48 total nurse staffing hours per resident day), requires state Medicaid agencies to report the share of Medicaid payments for institutional LTC that are spent on worker compensation, and provides funding for people to enter careers in nursing homes.

Description

- Prohibits the Secretary of Health and Human Services from implementing, administering, or enforcing the minimum staffing levels required by the final rule until October 1, 2034.

Effective Date: Upon enactment.

Budgetary and Coverage Impact

CBO estimates this provision will reduce federal Medicaid spending by $23 billion over 10 years. This provision is not expected to impact coverage.

KFF Resources

- Texas Judge Overturns Controversial Nursing Facility Staffing Rule

- A Closer Look at the Final Nursing Facility Rule and Which Facilities Might Meet New Staffing Requirements

- 10 Things About Long-Term Services and Supports (LTSS)

Section 71108: Home Equity Limits

Background

Most Medicaid enrollees who qualify for Medicaid because they need long-term care (LTC) are subject to limits on their home equity. In 2025, federal rules specified that states’ limits on home equity must be between $730,000 and $1,097,000, and those amounts are updated each year for inflation.

Description

- Reduces the maximum home equity limits to $1,000,000 regardless of inflation.

- Allows states to apply different requirements for homes that are located on farms.

Effective Date: January 1, 2028.

Budgetary and Coverage Impact

CBO estimates this provision will reduce federal Medicaid spending by $195 million over 10 years. This provision is not expected to impact the number of people who are uninsured.

KFF Resources

Section 71121: New Home and Community Based Services (HCBS)

Background

States are required to cover nursing facility care under Medicaid, but nearly all home care (HCBS) is optional. Nearly all states provide home care through “1915(c) waivers,” which limit services to people who require an institutional level of care. Because those services are optional, states may limit the amount of care people receive and the number of people receiving services. Most states have waiting lists because the number of people seeking services exceeds the amount of care available.

Description

- Allows states to establish 1915(c) HCBS waivers for people who do not need an institutional level of care.

- Requires state waiver submissions to demonstrate that new waivers will not increase the average amount of time that people who need an institutional level of care will wait for services.

- Includes $50 million in FY 2026 and $100 million in FY 2027 for implementation.

Effective Date: July 1, 2028 for new waiver approvals.

Budgetary and Coverage Impact

CBO estimates this provision will increase federal Medicaid spending by $7 billion over 10 years. This provision is not expected to impact the number of people who are uninsured.

KFF Resources

- What is Medicaid Home Care (HCBS)?

- A Look at Waiting Lists for Medicaid Home- and Community-Based Services from 2016 to 2024

Access

Section 71401: Rural Health Transformation Program

Description

- Establishes a rural health transformation program that will provide $50 billion in grants to states between fiscal years 2026 and 2030, to be used for payments to rural health care providers and for other purposes.

- Distributes 50% of payments equally across states with approved applications; the remaining funds will be distributed by CMS based at least in part on states’ rural populations that live in metropolitan statistical areas, the percent of rural health facilities nationwide that are located in a state, and the situation of hospitals that serve a disproportionate number of low-income patients with special needs.

- Uses of funds include promoting care interventions, paying for health care services, expanding the rural health workforce, and providing technical or operational assistance aimed at system transformation.

- Provides CMS with $200 million in implementation funding for FY 2025.

Effective Date: Upon enactment but funding is first available in fiscal year 2026. CMS to determine state application deadline, which will be no later than December 31, 2025.

Budgetary and Coverage Impact

CBO estimates this provision will increase federal spending by $47 billion over 10 years. This provision is not expected to impact coverage.

KFF Resources

- A Closer Look at the $50 Billion Rural Health Fund in the New Reconciliation Law

- How Might Federal Medicaid Cuts in the Senate-Passed Reconciliation Bill Affect Rural Areas?

- 5 Key Facts About Medicaid Coverage for People Living in Rural Areas

- 10 Things to Know About Rural Hospitals

Section 71113: Prohibiting Federal Medicaid Payments to Certain Providers

Background

States must generally allow beneficiaries to obtain Medicaid services from any provider that is qualified and willing to furnish services. Managed care organizations (MCOs) may restrict enrollees to providers in the MCO’s network, except that such plans cannot restrict free choice of family planning providers.

Description

- Prohibits federal Medicaid funds to be paid to providers that meet the following criteria on October 1, 2025: are nonprofit organizations, essential community providers primarily engaged in family planning services or reproductive services, provide for abortions outside of the Hyde exceptions and received $800,000 or more in payments from Medicaid in 2023; this would affect Planned Parenthood and other Medicaid essential community providers.

- Provides $1 million in implementation funding for FY 2026.

Effective Date: Upon enactment for 1 year; implementation is currently blocked for some providers due to ongoing litigation.

Budgetary and Coverage Impact

CBO estimates this provision will increase federal spending by $53 million over 10 years. This provision is not expected to impact coverage.

KFF Resources

- Planned Parenthood Remains in Limbo as Court Reviews Their Request to Block Federal Medicaid Funding Ban

- What’s at Stake in the Supreme Court Case Medina v. Planned Parenthood South Atlantic?

- The Impact of Medicaid and Title X on Planned Parenthood

- Recent Policy Proposals Could Weaken the Reproductive Health Safety Net as More People Become Uninusred

Section 71105: Medicaid Provider Screening Requirements

Background

Provider screening and enrollment is required for all providers in Medicaid fee-for-service or managed care networks. Additionally, the ACA requires states to terminate provider participation in Medicaid if the provider was terminated under Medicare or another state program. CMS has multiple tools to assist states with provider screening and enrollment compliance, including leveraging Medicare data.

Description

- Requires states to conduct checks at provider enrollment or reenrollment and on a quarterly basis of the Social Security Administration’s Death Master File to determine whether providers enrolled in Medicaid are deceased.

Effective Date: January 1, 2028.

Budgetary and Coverage Impact

CBO estimates this provision will not affect federal Medicaid spending over 10 years. This provision is not expected to impact coverage.

KFF Resources

Affordable Care Act

Sec. 71303: Pre-Enrollment Verification of Eligibility for Premium Tax Credit

Background

Currently, new enrollees are granted conditional eligibility if there is a mismatch in the information they provided and that in federal databases. Enrollees can retain coverage and tax credits for up to 90 days while submitting verification documents. Returning enrollees who take no action during open enrollment are auto-renewed into the same or similar plan. Nearly half of Marketplace enrollees in 2025 auto-renewed.

Description

- Requires verification of household income, health coverage status or eligibility for coverage, place of residence, family size, status as an eligible alien, and any other information that the Secretary of Health and Human Services deems necessary are verified before coverage.

- Exchanges can use any third-party sources and any available data for verification.

- Consumers can still enroll in a plan but cannot receive premium tax credits or cost-sharing reductions (CSRs) until after they verify their eligibility.

- This provision effectively ends auto-renewals.

- Restricts premium tax credit eligibility for enrollees who fail to file and reconcile their premium tax credits for one year.

- Restricts premium tax credit eligibility for enrollees who fail to file and reconcile their premium tax credits for one year.

Effective date: Taxable years beginning after December 31, 2027.

Budgetary and Coverage Impact

Decreases budgetary spending by $36.9 billion and increases revenue by $4.4 billion through 2034 and will increase the number of people who are uninsured by 700,000 in 2034.

KFF Resources

- FAQs: Health Insurance Marketplace and the ACA

- State Health Facts: Affordable Care Act

- Signing Up for Marketplace Coverage Remains a Challenge for Many Consumers

Sec. 71305: Recapture of Excess Premium Tax Credits

Background

Currently, if an enrollee receives excess premium tax credits because their estimated income was lower than their actual income, they must repay the excess. However, for most enrollees, there is a repayment cap that varies based on household income. For enrollees with household incomes at least 400% of the federal poverty level (FPL), there is no limit. They must repay the entirety of their excess tax credit. Other repayment limits vary from $375 for a single person with an income that is 100% FPL up to 200% FPL to $3,250 for families with an income between 300%-400% FPL for tax year 2025.

Description

- Requires that all premium tax credit recipients repay the full amount of any excess, no matter their income.

Effective date: taxable years beginning after December 31, 2025.

Budgetary and Coverage Impact

Decreases budgetary spending by $17.3 billion and increases revenue by $2.3 billion through 2034 and will increase the number of people who are uninsured by 100,000 in 2034.

KFF Resources

Sec. 71301: ACA Marketplace Coverage Eligibility for Lawfully Present Immigrants

Background

Currently, U.S. citizens and lawfully present immigrants are eligible to enroll in ACA Marketplace coverage and receive premium subsidies and cost-sharing reductions.

Description

- Limit eligibility for subsidized ACA Marketplace coverage to lawfully present immigrants who are lawful permanent residents (LPRs or “green card” holders), Compact of Free Association (COFA) migrants residing in the U.S., or Cuban and Haitian entrants as defined in section 501(e) of the Refugee Education Assistance Act of 1980, eliminating eligibility for many lawfully present immigrants including refugees, asylees, and people with Temporary Protected Status.

Effective date: Taxable years beginning after December 31, 2026.

Budgetary and Coverage Impact

Decreases budgetary spending by $69.8 billion and increases revenue by $4.8 billion through 2034 and will increase the number of people who are uninsured by 900,000 in 2034.

KFF Resources

- FAQs: Health Insurance Marketplace and the ACA

- Potential Impacts of 2025 Budget Reconciliation on Health Coverage for Immigrant Families

Sec. 71302: Premium Tax Credit Eligibility for Lawfully Present Immigrants Ineligible for Medicaid

Background

Currently, lawfully present immigrants with incomes under 100% of the federal poverty level (FPL) who do not qualify for Medicaid coverage due to their immigration status also are eligible for ACA Marketplace coverage.

Description

- Prohibits lawfully present immigrants ineligible for Medicaid due to immigrant status from receiving tax credits if making below 100% of poverty.

Effective Date: taxable years beginning after December 31, 2025.

Budgetary and Coverage Impact

Decreases budgetary spending by $49.5 billion and increases revenue by $176 million through 2034 and will increase the number of people who are uninsured by 300,000 in 2034.

KFF Resources

- FAQs: Health Insurance Marketplace and the ACA

- Potential Impacts of 2025 Budget Reconciliation on Health Coverage for Immigrant Families

Sec. 71304: Special Enrollment Periods (SEPs) and Tax Credit Eligibility

Background

In addition to qualifying life events (QLEs) that enable eligibility for an SEP, people in states that use Federally-Facilitated Marketplaces (FFM) and make no more than 150% of the federal poverty level can apply for a year-round SEP to sign up for coverage. Some state-based exchanges also offer SEPs that are based on the relationship of people’s income to the poverty line. Any person who enrolls in a plan via an SEP is eligible for both premium tax credits and cost-sharing reductions (CSRs). In 2025, enrollees with an income of less than 150% of the federal poverty line made up the largest share of all Marketplace enrollees (47%).

Description

- Bars any consumer who enrolls in a plan via a non-qualifying life event (QLE) SEP from receiving either premium tax credits or CSRs.

Effective date: Plan years beginning after December 31, 2025.

Budgetary and Coverage Impact

Decreases budgetary spending by $39.5 billion and increases revenue by $1.3 billion through 2034 and will increase the number of people who are uninsured by 400,000 in 2034.

KFF Resources

- FAQs: Health Insurance Marketplace and the ACA

- State Health Facts: Affordable Care Act

- Explaining Health Care Reform: Questions About Health Insurance Subsidies

Expiration of Enhanced Premium Tax Credits

Background

The enhanced premium tax credits were first made available as part of the American Rescue Plan Act in 2021 and later extended through the end of 2025 as part of the Inflation Reduction Act. The ARPA and IRA’s enhanced health insurance tax credits both increase the amount of financial help available to those already eligible for assistance under the ACA and also newly expand subsidies to middle-income people (with incomes over four times the poverty level), many of whom were previously priced out of coverage. These enhanced tax credits, combined with increased funding for outreach and marketing have led to record-high enrollment in the ACA Marketplaces.

Description

- There was no extension of the enhanced tax credits in the law. The Republican-led Senate opted to use a “current law” baseline for Congressional Budget Office scoring of the budget impact. Therefore, the expiration of the enhanced tax credits was not scored as a new policy change and has no impact in the law’s official budget and coverage estimates.

- The number of uninsured people will rise by 4.2 million through 2034, and gross benchmark premiums will increase by 7.9% through 2034 without an extension. Permanent extension would increase the budget deficit by $335 billion through 2034.

Effective date: January 1, 2026 (unless extended by Congress).

KFF Resources

- How Much More Would People Pay in Premiums if the ACA’s Enhanced Subsidies Expired?

- Inflation Reduction Act Health Insurance Subsidies: What is Their Impact and What Would Happen if They Expire?

- Five Things to Know about the Renewal of Extra Affordable Care Act Subsidies in the Inflation Reduction Act

- Early indications of the impact of the enhanced premium tax credit expiration on 2026 Marketplace premiums

- KFF Health Tracking Poll: ACA Enhanced Subsidies

Medicare

Eligibility Policies

Section 71201: Limiting Medicare Coverage of Certain Individuals

Background

Prior to passage of the law, residents of the United States, including citizens, permanent residents, and other immigrants that are lawfully present in the country, were eligible for premium-free Medicare Part A if they or their spouses have worked in a job for at least 40 quarters where they paid Medicare payroll taxes and are at least 65 years old. People under age 65 with a qualifying disability, end-stage renal disease (ESRD), and amyotrophic lateral sclerosis (ALS) are also generally eligible. Legal immigrants age 65 or older who do not have this work history could purchase Medicare Part A after residing legally in the U.S. for five years continuously.

Description

- Restricts Medicare eligibility to U.S. citizens, green card holders, Cuban-Haitian entrants, and people residing under the Compacts of Free Association, eliminating Medicare eligibility for people not included in these groups, such as those with temporary protected status and refugees and asylees.

- Terminates Medicare coverage no later than 18 months from enactment for anyone who is currently covered but no longer eligible under these changes.

Effective Date: Upon enactment.

Budgetary and Coverage Impact

CBO estimates this provision will reduce Medicare spending by $5.1 billion over 10 years and will increase the number of people who are uninsured by 100,000 in 2034.

KFF Resources

- Key Facts on Health Coverage of Immigrants

- Medicare Open Enrollment FAQ: Can immigrants enroll in Medicare?

Section 71101: Moratorium on Implementation of Rule Relating to Eligibility and Enrollment in Medicare Savings Programs

Background

In September 2023, CMS issued a final rule to reduce barriers to enrollment in Medicare Savings Programs (MSPs), which provides Medicaid coverage of Medicare premiums and cost sharing for low-income Medicare beneficiaries. Implementation deadlines for states vary across provisions in the rule, but some provisions are already in effect, and for others, states are already in compliance.

Description

- Prohibits the Secretary from implementing, administering, or enforcing certain provisions in a September 2023 CMS final rule that have not yet taken effect until October 1, 2034.

Effective Date: Upon enactment.

Budgetary and Coverage Impact

CBO estimates the moratorium on this rule will reduce federal Medicaid spending by $66 billion over 10 years due to lower enrollment in the Medicare Savings Programs than if all the provisions of the rule were implemented and enforced. CBO has not provided an updated estimate of how many fewer dual-eligible individuals will be enrolled in Medicaid.

KFF Resources

- Medicaid Changes in House and Senate Reconciliation Bills Would Increase Costs for 1.3 Million Low-Income Medicare Beneficiaries

- 5 Things to Know: A Look at the Proposed Medicaid Eligibility & Enrollment Rule

- What Does the Medicaid Eligibility Rule Mean for Low-Income Medicare Beneficiaries and the Medicare Savings Programs (MSPs)?

- Potential Effects of the Proposed Medicaid Eligibility Rule for Newly Enrolled Medicare-Medicaid Enrollees

Physician Payment

Section 71202: Temporary Payment Increase Under the Medicare Physician Fee Schedule

Background

Medicare payment rates to physicians and other clinicians under the Physician Fee Schedule are determined in part by a scaling factor, known as the conversion factor, which is updated each year. Under current law, conversion factor updates are based on statutory factors and other budgetary requirements. Beginning in 2026, the Physician Fee Schedule conversion factor was scheduled to increase by 0.25% each year for most Medicare providers.

Description

- Provides a temporary one-year increase of 2.5% to the Physician Fee Schedule conversion factor for all services furnished between January 1, 2026 and January 1, 2027.

Effective Date: January 1, 2026.

Budgetary and Coverage Impact

The CBO estimates that this change will increase Medicare spending by $1.9 billion in 2026 and 2027. This provision is not expected to impact coverage.

KFF Resources

Prescription Drugs

Section 71203: Expanding and clarifying the exclusion for orphan drugs under the Drug Price Negotiation Program

Background

Under the Medicare Drug Price Negotiation Program, drugs qualify for price negotiation if they are single source brand-name drugs or biological products without therapeutically equivalent generic or biosimilar alternatives, and are at least 7 years (for small-molecule drugs) or 11 years (for biologics) past the FDA approval or licensure date, as of the date that the list of drugs selected for negotiation is published. Under the Inflation Reduction Act of 2022, the law that established the drug price negotiation program, drugs designated for only one rare disease or condition and approved for an indication (or indications) only for that disease or condition were exempt from negotiation. This is known as the orphan drug exclusion.

Description

- Modifies the orphan drug exclusion of the Medicare drug price negotiation program to exclude drugs from negotiation that are designated for one or more rare diseases or conditions and where the only approved indication or indications are for one or more rare diseases or conditions, rather than only one rare disease or condition.

- Excludes the period of time that drugs are on the market with only one or more orphan indications from the 7-year or 11-year waiting period that determines a drug’s eligibility for selection for price negotiation.

Effective Date: applies for drug price selection beginning in February 2026 for negotiated prices available on or after January 1, 2028.

Budgetary and Coverage Impact

The CBO estimates that this change will increase Medicare spending by $4.9 billion over 10 years. This provision is not expected to impact coverage.

KFF Resources

Long-term Care

Section 71111: Moratorium on Implementation of Nursing Home Staffing Final Rule

Background

A 2024 Biden administration final rule requires long-term care facilities (LTC) to meet minimum staffing levels (including a 24/7 RN on-site and a minimum of 3.48 total nurse staffing hours per resident day), requires state Medicaid agencies to report the share of Medicaid payments for institutional LTC that are spent on worker compensation, and provides funding for people to enter careers in nursing homes.

On April 7, 2025, the US District Court for Northern Texas ruled to overturn the minimum staffing requirements, and it is expected that the Administration will not appeal that decision.

Description

- Prohibits the Secretary of Health and Human Services from implementing, administering, or enforcing the minimum staffing levels required by the final rule until October 1, 2034.

Effective Date: Upon enactment.

Budgetary and Coverage Impact

The CBO estimates the moratorium of this rule will reduce federal spending by $23 billion over 10 years. This provision is not expected to impact coverage.

KFF Resources

Health Savings Accounts

Section 71306. Permanent Extension of Safe Harbor for Absence of Deductible for Telehealth Services

Background

Health savings accounts (HSAs) are tax-advantaged savings accounts that enrollees in certain high-deductible health plans (HDHPs) can use to pay for qualified medical expenses. Enrollees must pay all medical costs, except for certain preventive services and insulin products, out-of-pocket until they reach the deductible. Individuals cannot have other health coverage in order to be eligible for an HDHP with an HSA. In response to the COVID pandemic, federal law permitted HSA-eligible HDHPs to cover telehealth and other remote services before the deductible until the end of 2024.

Description

- Permanently allows HDHPs with an HSA to cover telehealth and other remote services before the enrollee meets the deductible.

- Individuals that have other coverage for telehealth and other remote care services will still be eligible for an HDHP with an HSA.

Effective date: Plan years beginning after December 31, 2024.

Budgetary and Coverage Impact

The CBO and JCT estimate a decrease in revenue of $4.3 billion through 2034. This provision is not expected to impact the number of people who are uninsured.

KFF Resources

- Expansions to Health Savings Accounts in House Budget Reconciliation: Unpacking the Provisions and Costs to Taxpayers

- Health Savings Accounts and High Deductible Health Plans: Are They An Option for Low-Income Families?

- 2024 KFF Employer Health Benefits Survey

Section 71307. Allowance of Bronze and Catastrophic Plans in Connection with Health Savings Accounts

Background

ACA-compliant health insurance plans are categorized into “metal levels” based on the amount of cost sharing they require. Some bronze plans meet the deductible requirements to be paired with an HSA (the out-of-pocket maximum or other design features might not meet IRS rules though). Catastrophic plans, which have the highest cost sharing and are only available to people under age 30 or those who cannot find other affordable ACA-compliant coverage, are ineligible to be paired with an HSA.

Description

- Treats bronze and catastrophic plans sold on the ACA Marketplace as HDHPs that can be paired with an HSA.

Effective date: January 1, 2026.

Budgetary and Coverage Impact

The CBO and JCT estimate a decrease in revenue of over $3.5 billion through 2034. This provision is not expected to impact the number of people who are uninsured.

KFF Resources

Section 71308. Treatment of Direct Primary Care Arrangements

Background

Direct primary care (DPC) arrangements typically offer unlimited primary care services to patients in exchange for a periodic fee paid to the DPC practice. Current law may treat DPC arrangements as a health plan under certain circumstances, making an individual covered by a DPC arrangement ineligible to use an HSA.

Description

- Certain DPC arrangements will not be considered health plans, allowing individuals covered by these arrangements to be eligible for an HSA. This will apply if the only compensation for the DPC is a fixed periodic fee that does not exceed $150 monthly, or $300 monthly where more than one individual is covered.

- For the purposes of this provision, DPC arrangements not considered health plans are limited to those only offering primary care services, and do not include:

- services that require general anesthesia;

- prescription drugs, except for vaccines, and;

- laboratory services not typically administered in an ambulatory primary care setting.

- Treats fees paid for any DPC arrangement as a medical expense (not the payment of insurance) that can be paid for with HSA funds.

Effective date: January 1, 2026.

Budgetary and Coverage Impact

The CBO and JCT estimate a decrease in revenue of over $2.8 billion through 2034. This provision is not expected to impact the number of people who are uninsured.

KFF Resources