2019 Employer Health Benefits Survey

Section 1: Cost of Health Insurance

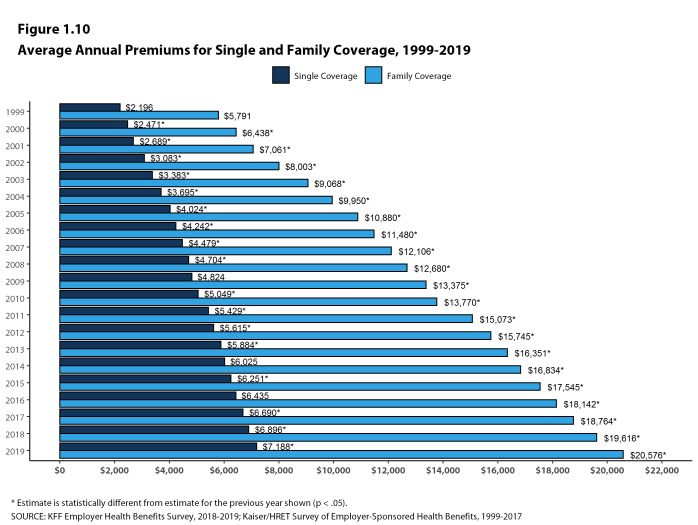

In 2019, the average annual premiums are $7,188 for single coverage and $20,576 for family coverage. The average premium for single coverage increased by 4% since 2018 and the average premium for family coverage increased by 5%. The average family premium has increased 54% since 2009 and 22% since 2014.

This graphing tool allows users to look at changes in premiums and worker contributions for covered workers at different types of firms over time: https://www.kff.org/interactive/premiums-and-worker-contributions/

PREMIUMS FOR SINGLE AND FAMILY COVERAGE

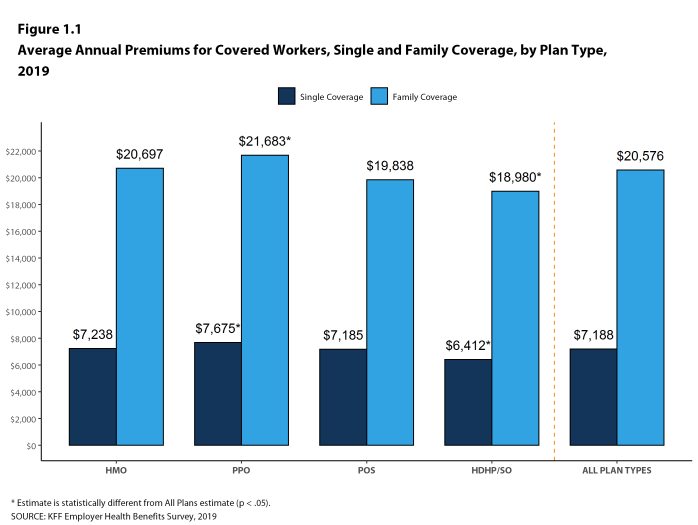

- The average premium for single coverage in 2019 is $7,188 per year. The average premium for family coverage is $20,576 per year [Figure 1.1].

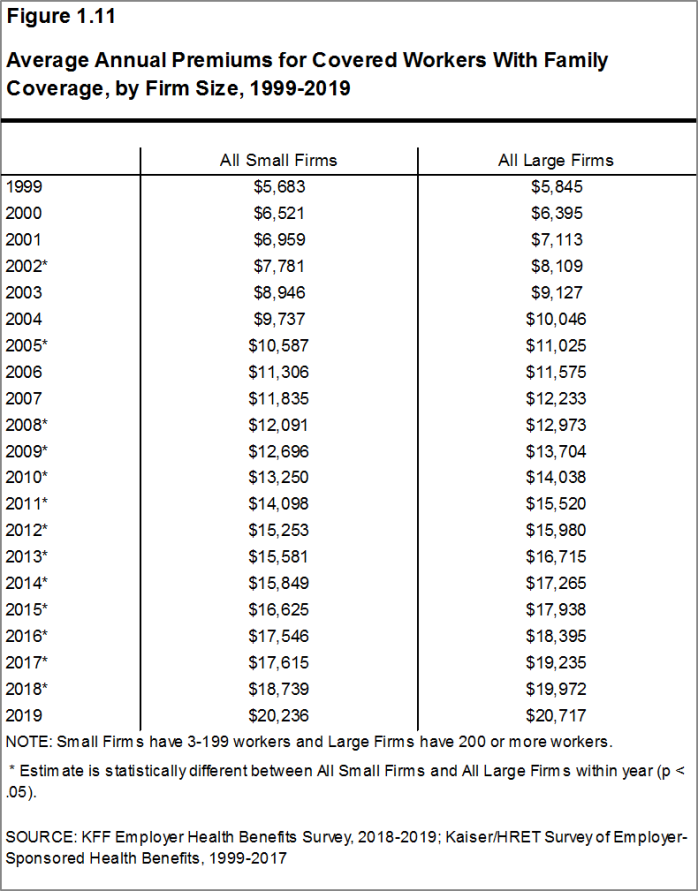

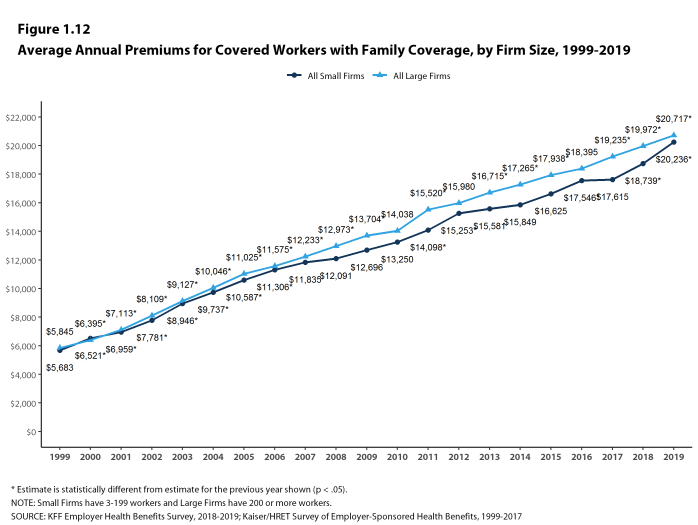

- The average annual premium for family coverage for covered workers in small firms ($20,236) is similar to the average premium for covered workers in large firms ($20,717). [Figure 1.2].

- The average annual premiums for covered workers in HDHP/SOs are lower for single coverage ($6,412) and family coverage ($18,980) than overall average premiums. The average premiums for covered workers enrolled in PPOs are higher for single ($7,675) and family coverage ($21,683) than the overall plan average [Figure 1.1].

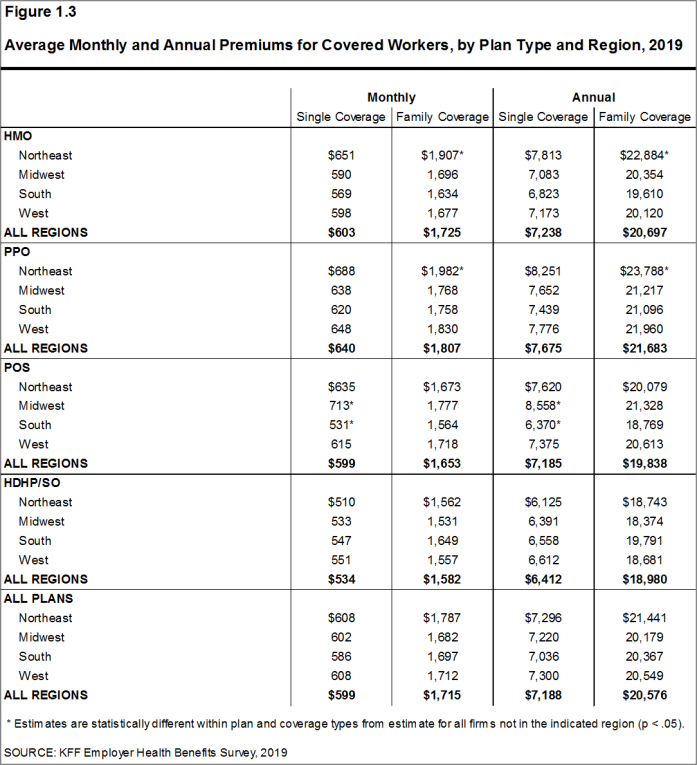

- The average premiums for covered workers with single coverage and for family coverage are similar across regions for all plan types [Figure 1.3].

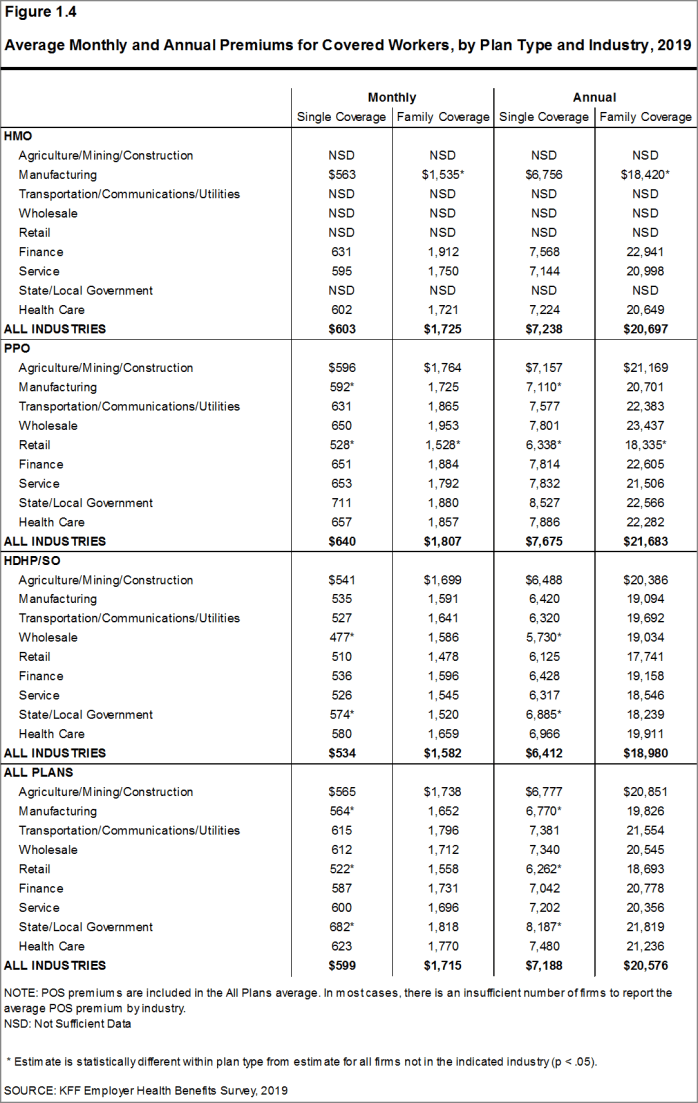

- The average premium for single coverage varies across industries. Compared to the average single premiums for covered workers in other industries, the average premiums for covered workers in the Manufacturing and Retail categories are relatively low and the average premium for State and Local Government workers are relatively high [Figure 1.4].

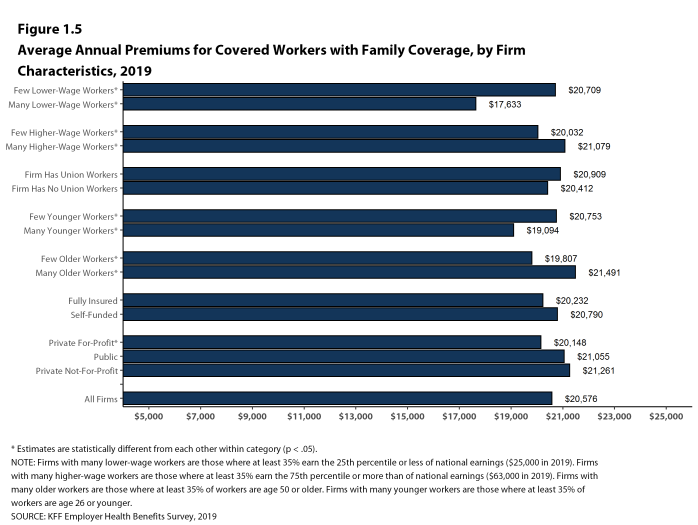

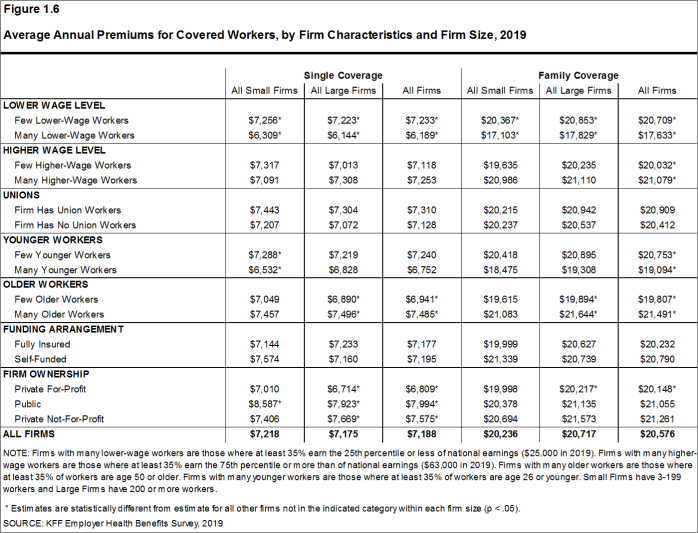

- The average premiums for covered workers in firms with a relatively large share of lower-wage workers (where at least 35% of the workers earn $25,000 annually or less) are lower than the average premiums for covered workers in firms with a smaller share of lower-wage workers ($6,189 vs. $7,233 for single coverage and $17,633 vs. $20,709 for family coverage) [Figure 1.6].

- The average premiums for covered workers in firms with a relatively large share of older workers (where at least 35% of the workers are age 50 or older) are higher than the average premiums for covered workers in firms with a smaller share of older workers ($7,485 vs. $6,941 for single coverage and $21,491 vs. $19,807 for family coverage) [Figure 1.6].

- The average premiums for family coverage for covered workers in firms with a relatively large share of younger workers (where at least 35% of the workers are age 26 or younger) are lower than the average premiums for covered workers in firms with a smaller share of younger workers ($19,094 vs. $20,753) [Figure 1.6].

- Premiums also vary by type of firm ownership. Covered workers at private for-profit firms have lower average annual premiums than covered workers at public firms or private not-for-profit firms for both single and family coverage [Figure 1.6].

Figure 1.1: Average Annual Premiums for Covered Workers, Single and Family Coverage, by Plan Type, 2019

Figure 1.2: Average Monthly and Annual Premiums for Covered Workers, by Plan Type and Firm Size, 2019

Figure 1.3: Average Monthly and Annual Premiums for Covered Workers, by Plan Type and Region, 2019

Figure 1.4: Average Monthly and Annual Premiums for Covered Workers, by Plan Type and Industry, 2019

Figure 1.5: Average Annual Premiums for Covered Workers With Family Coverage, by Firm Characteristics, 2019

Figure 1.6: Average Annual Premiums for Covered Workers, by Firm Characteristics and Firm Size, 2019

PREMIUM DISTRIBUTION

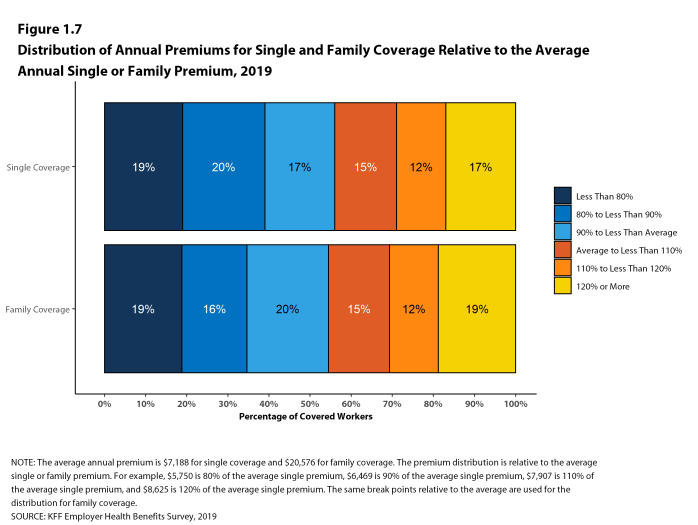

- There is considerable variation in premiums for both single and family coverage.

- Seventeen percent of covered workers are employed in a firm with a single premium at least 20% higher than the average single premium, while 19% of covered workers are in firms with a single premium less than 80% of the average single premium [Figure 1.7].

- For family coverage, 19% of covered workers are employed in a firm with a family premium at least 20% higher than the average family premium, while 19% of covered workers are in firms with a family premium less than 80% of the average family premium [Figure 1.7].

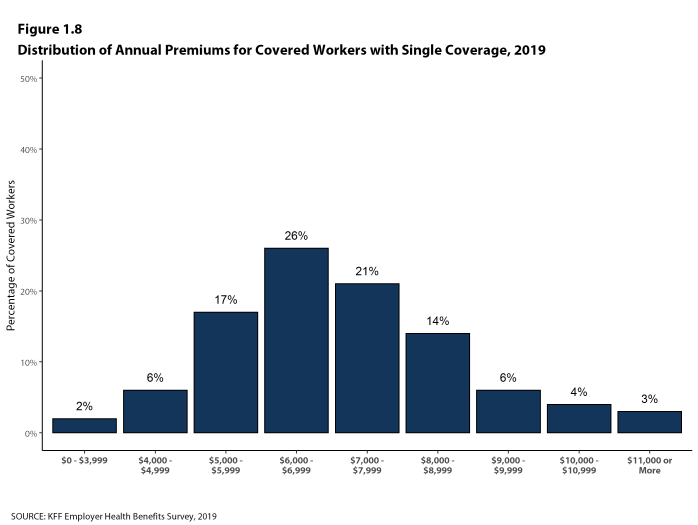

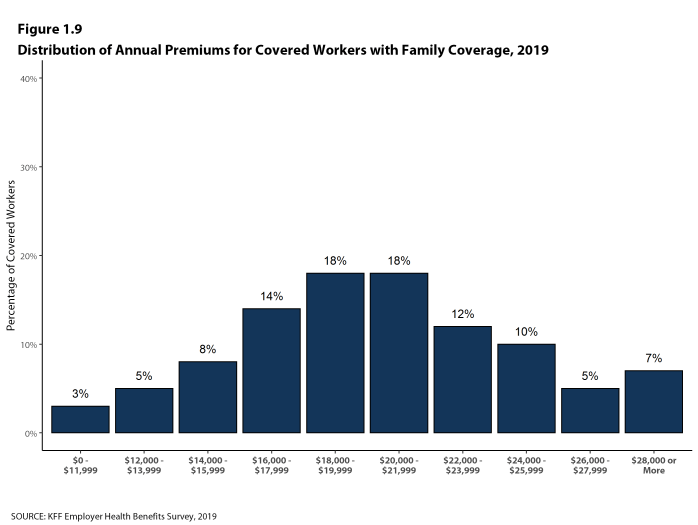

- Seven percent of covered workers are in a firm with an average annual premium of at least $10,000 for single coverage [Figure 1.8]. Seven percent of covered workers are in a firm with an average annual premium of at least $28,000 for family coverage [Figure 1.9].

Figure 1.7: Distribution of Annual Premiums for Single and Family Coverage Relative to the Average Annual Single or Family Premium, 2019

Figure 1.8: Distribution of Annual Premiums for Covered Workers With Single Coverage, 2019

Figure 1.9: Distribution of Annual Premiums for Covered Workers With Family Coverage, 2019

PREMIUM CHANGES OVER TIME

- The average premium for single coverage is 4% higher than the single premium last year, and the average premium for family coverage is 5% higher than the average family premium last year [Figure 1.10].

- The average premium for single coverage has grown 19% since 2014, similar to the growth in the average premium for family coverage (22%) over the same period [Figure 1.10].

- The average family premiums for both small and large firms have increased at similar rates since 2014 (28% for small firms and 20% for large firms). For small firms, the average family premium rose from $15,849 in 2014 to $20,236 in 2019. For large firms, the average family premium rose from $17,265 in 2014 to $20,717 in 2019 [Figures 1.11 and 1.12].

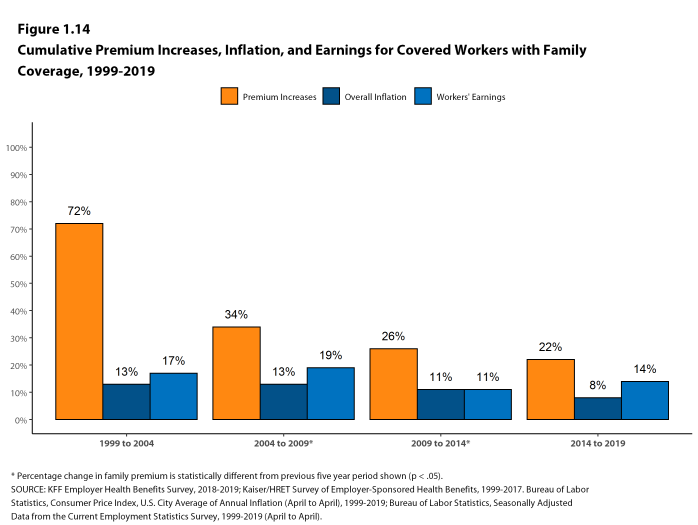

- The $20,576 average family premium in 2019 is 22% higher than the average family premium in 2014 and 54% higher than the average family premium in 2009. The 22% family premium growth in the past five years is similar to the 26% growth between 2009 and 2014 but slower than the 34% premium growth between 2004 and 2009 [Figure 1.14].

- The average family premiums for both small and large firms have increased at similar rates since 2009 (59% for small firms and 51% for large firms). For small firms, the average family premium rose from $12,696 in 2009 to $20,236 in 2019. For large firms, the average family premium rose from $13,704 in 2009 to $20,717 in 2019 [Figures 1.11 and 1.12].

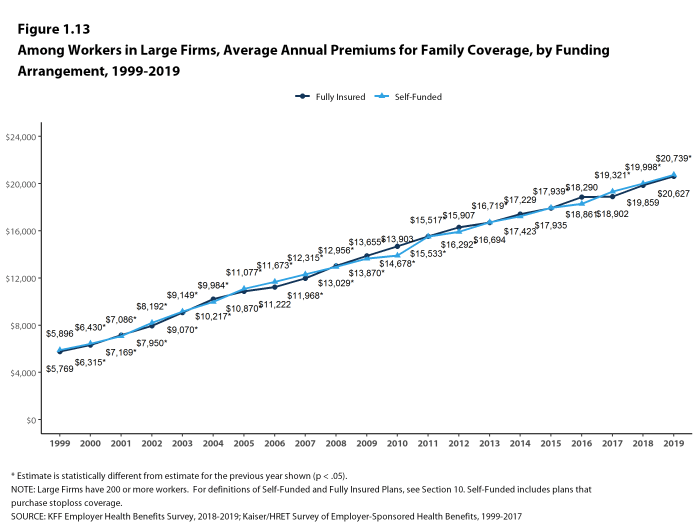

- For covered workers in large firms, over the past five years, the average family premium in firms that are fully insured has grown at a similar rate to the average family premium for covered workers in fully or partially self-funded firms (18% for fully insured plans and 20% for self-funded firms) [Figure 1.13].

- Premium growth continues to outpace both inflation and increases in workers’ earnings [Figure 1.14].

Figure 1.10: Average Annual Premiums for Single and Family Coverage, 1999-2019

Figure 1.11: Average Annual Premiums for Covered Workers With Family Coverage, by Firm Size, 1999-2019

Figure 1.12: Average Annual Premiums for Covered Workers With Family Coverage, by Firm Size, 1999-2019

Figure 1.13: Among Workers in Large Firms, Average Annual Premiums for Family Coverage, by Funding Arrangement, 1999-2019

Figure 1.14: Cumulative Premium Increases, Inflation, and Earnings for Covered Workers With Family Coverage, 1999-2019