What Are the Implications of the Recent Elimination of the Medicaid Prescription Drug Rebate Cap?

As of January 1, 2024, the American Rescue Plan Act (ARPA) lifted the cap on the total amount of rebates that Medicaid could collect from manufacturers who raise drug prices substantially over time. Anticipating the implementation of this policy, drug manufacturers have made various changes allowing them to avoid increased rebates resulting from the lifting of the cap. Recent changes that have garnered attention include price cuts for insulin, used to treat diabetes, and the discontinuation of Flovent, a frequently used asthma inhaler. While the insulin price cuts have been portrayed by drug manufacturers as a step to improve affordability, they may in fact be revenue maximizing efforts in response to the changes in the Medicaid rebate formula. This policy watch explains what the rebate cap is, examines how many drugs might be impacted, and explores the implications of recent manufacturer responses on Medicaid programs and enrollees.

What is the rebate cap?

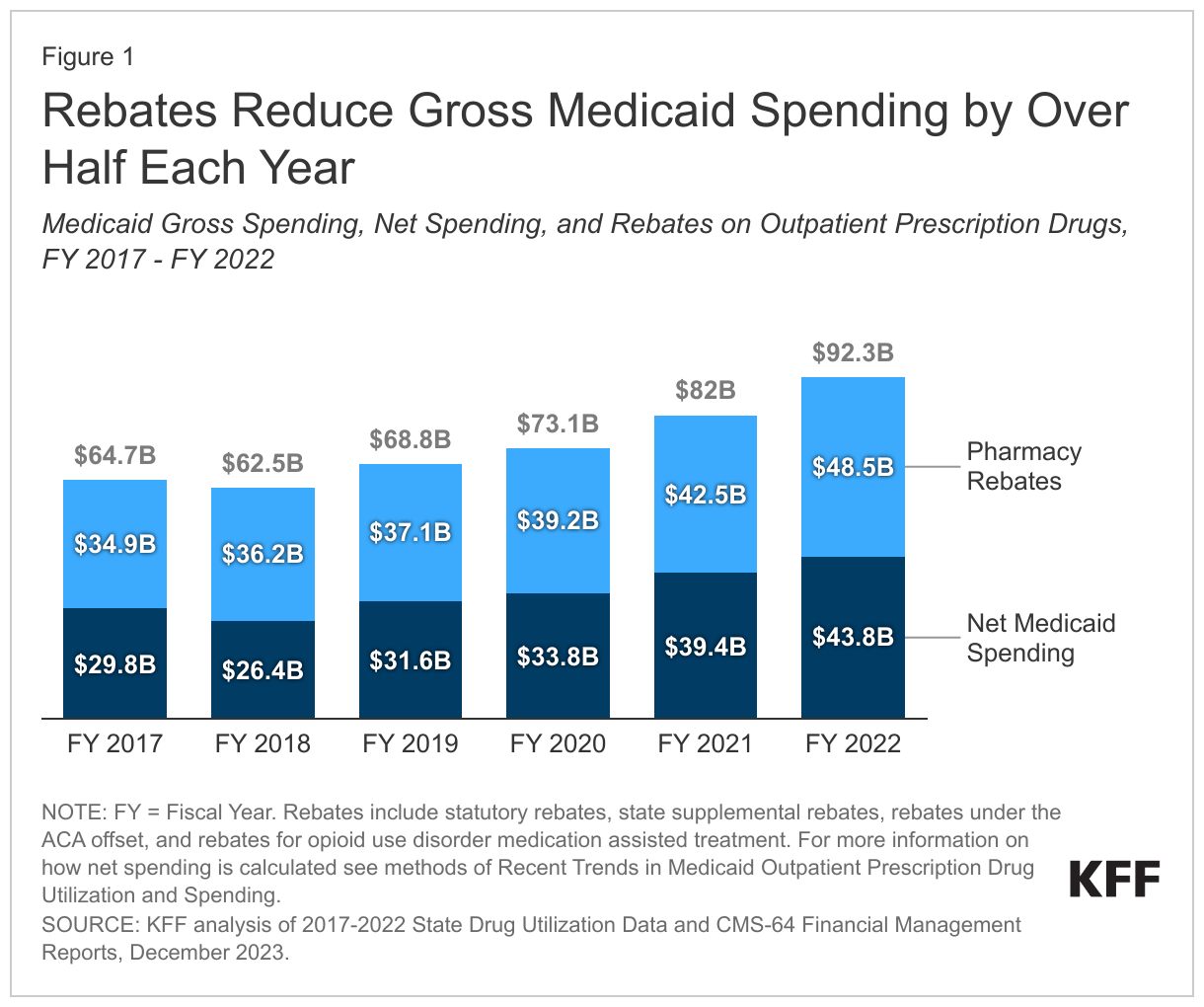

ARPA eliminated the limit on Medicaid drug rebates manufacturers pay starting January 1, 2024. Under the Medicaid Drug Rebate Program, drug manufacturers provide rebates to the federal government and states in exchange for Medicaid coverage of their drugs. The rebate amount includes two main components: a rebate based on a percentage of average manufacturer price (AMP) (or the difference between AMP and “best price,” whichever is greater) and an inflationary component to account for price increases. The AMP is the price charged by drug manufacturers to wholesalers. Because of the inflationary component, the calculated rebate on a drug whose price increases quickly over time could be greater than the AMP for that drug. However, the total rebate amount had been capped at 100% of AMP since 2010. As a result, manufacturers who hit the rebate cap did not face additional Medicaid rebates if they continued to increase prices. Recent KFF analysis found rebates reduced Medicaid spending on prescription drugs by over half each year from fiscal year 2017 through 2022 (Figure 1). However, ARPA, enacted in March 2021, eliminated the 100% AMP cap on Medicaid drug rebates as of January 1, 2024.

The lifting of the rebate cap is expected to have a substantial impact on brand drugs, especially those drugs that have already hit the rebate cap or have price increases much faster than inflation over time. A prior KFF analysis of gross prescription drug spending in Medicaid found that more than a third (34%) of drugs had price increases above inflation between 2015 and 2019, though not all these drugs hit the rebate cap. Drugs with fewer drugs in their therapeutic class were more likely to have increases above inflation. Other research has shown that around 15%-20% of all brand drugs have reached the cap. Further, recent MACPAC analysis found a small proportion of all drugs (4.7%) reached the rebate cap in FY 2020 but estimates total rebates would equal 130.8% of gross spending on those drugs without the rebate cap.

What are the implications of lifting the rebate cap?

In response to the elimination of the rebate cap, some drug companies are lowering drug prices or discontinuing drugs in favor of lower priced alternatives to avoid paying additional Medicaid rebates. After years of increasing list prices, insulin manufacturers have recently cut prices of some insulin products up to 80%. The lifting of the rebate cap was a major contributor to this response; research has shown insulin manufacturer Eli Lilly was expected to pay $430 million and Novo Nordisk $350 million in additional rebates to Medicaid in 2024. While these insulin price decreases are quite large, drug manufacturers may not actually see reduced revenues given the rebate payments they will avoid as result. Another drugmaker GSK is cutting prices of some products as well as discontinuing their brand drugs Flovent HFA and Flovent Diskus, frequently used asthma inhalers, and will instead sell a generic alternative, with a lower list price. It remains to be seen how many more drugs will see price cuts or be discontinued, and it can be difficult to predict which drugs or manufacturers will be most affected by the policy change as data on drug AMPs and rebates is currently proprietary. However, an analysis of 2017 data found 25 drugs, most of which were for diabetes treatment, accounted for 85% of rebates reduced by the cap. Manufacturers may also respond in other ways, such as by raising launch prices.

While under current law Medicaid must cover nearly all of a rebating manufacturer’s FDA approved drugs, if a particular drug is discontinued, Medicaid enrollees may experience some administrative challenges when trying to access alternatives. Because Medicaid must cover nearly all of a participating manufacturer’s FDA approved drugs, Medicaid would cover a rebating manufacturer’s new generic (as in the case of Flovent). However, states can use an array of payment strategies and utilization controls to manage pharmacy expenditures, including preferred drug lists and prior authorization (PA) policies linked to clinical criteria, which can impact access. There could be some administrative challenges Medicaid enrollees may need to navigate depending on the state or health plan. Individuals may need to switch prescriptions to a different product on the preferred drug list or get approval to use a non-preferred drug which could lead to delays in accessing prescriptions. Asthma prevalence is higher for people with Medicaid compared with private insurance, and children may be uniquely impacted as the Flovent inhaler made it possible for young children to use the medication. Manufacturer responses may also result in changes in out-of-pocket costs for commercial and uninsured patients; however, Medicaid enrollees usually pay little or no copays for prescription drugs, including for insulin.

Lifting the rebate cap was expected to reduce Medicaid spending, though the level of savings is dependent on how drug companies respond as well as impacted by later provisions in the Inflation Reduction Act (IRA). When enacted, eliminating the rebate cap was projected by the Congressional Budget Office to reduce federal spending by more than $17 billion over ten years. However, cost savings under changes to the rebate cap will be dependent on manufacturer responses to the change in policy. Further, the IRA, passed in 2022, requires drug companies to pay a rebate to the government if drug prices rise faster than inflation in Medicare starting in 2023 (this requirement already exists in Medicaid). The Medicare inflation-related rebates will mean slower growth in drug prices over time, leading to lower Medicaid inflation-related rebates and increased Medicaid drug spending. The lifting of the rebate cap magnifies the effects of the Medicare inflation-related rebates in the IRA on Medicaid.

States and managed care plans may adjust their preferred drug lists (PDLs) as the landscape shifts in response to the lifting of the rebate cap. Rebates are typically higher for brand name drugs, so states sometimes favor brand drugs with high rebates over generics. For example, while this may be shifting, insulin utilization in Medicaid has been largely concentrated among brand-name drugs likely due to high rebate amounts. As prices of brand drugs change and generic drugs come on the market, states may adjust their PDLs to maximize savings. For example, Massachusetts Medicaid has removed the PA requirement for three brand alternatives for Flovent and has added a PA requirement for the generic Flovent. The state will allow the use of the generic Flovent without PA until March to smooth the transition for members. New York Medicaid has made a similar change. States continually take action like this to contain Medicaid prescription drug costs, with over two-thirds of states in KFF’s annual survey of state Medicaid programs reporting new or expanded initiatives to contain prescription drug costs, including significant PDL or rebate changes.