Access to Adult Dental Care Gets Renewed Focus in ACA Marketplace Proposal

Updated February 20, 2025, to correct the average deductible amount for standalone dental plans offered on the Marketplace in 2023.The 2023 KFF Consumer Survey of Consumer Experiences with Health Insurance finds cost barriers to adult dental care across coverage types. Conducted in February and March of 2023, the survey includes a nationally representative sample of 3,605 U.S. adults who have health insurance. This Policy Watch discusses a new proposal in the Health and Human Services (HHS) Benefit and Payment Parameters for 2025 that aims to expand access to adult dental care in Affordable Care Act (ACA) Marketplace plans.

Background

While dental coverage for children under the age of 18 is an essential health benefit (EHB) under the ACA statute, adult dental care is currently prohibited by agency regulation from being considered an EHB in individual and small group plans. As a result, it is excluded from the ACA’s major cost-sharing protections that apply to EHBs such as the ban on annual and lifetime dollar limits and maximum annual limits on out-of-pocket cost sharing for consumers and is not covered by premium subsidies. There are still coverage options for adults seeking dental care through the Marketplace, offered through stand-alone dental plans (SADPs) or embedded plans (medical plans that include dental coverage). Dental care is usually subject to a deductible, though the National Association of Dental Plans reports that many dental plans waive the deductible for preventive dental care such as cleanings or cover preventive care 100%. Dental coverage that is included in an embedded plan is generally subject to the medical deductible for the plan, which, on average, was $3,057 in 2024. This translates to greater consumer cost sharing before coverage of dental services begins. In contrast, the average deductible for standalone dental plans offered on the Marketplace in 2023 was $52 according to KFF analysis of the Health Insurance Exchange Plan Attributes Public Use Files, which includes all qualified and non-qualified stand-alone dental plans sold on- and off- the exchange.

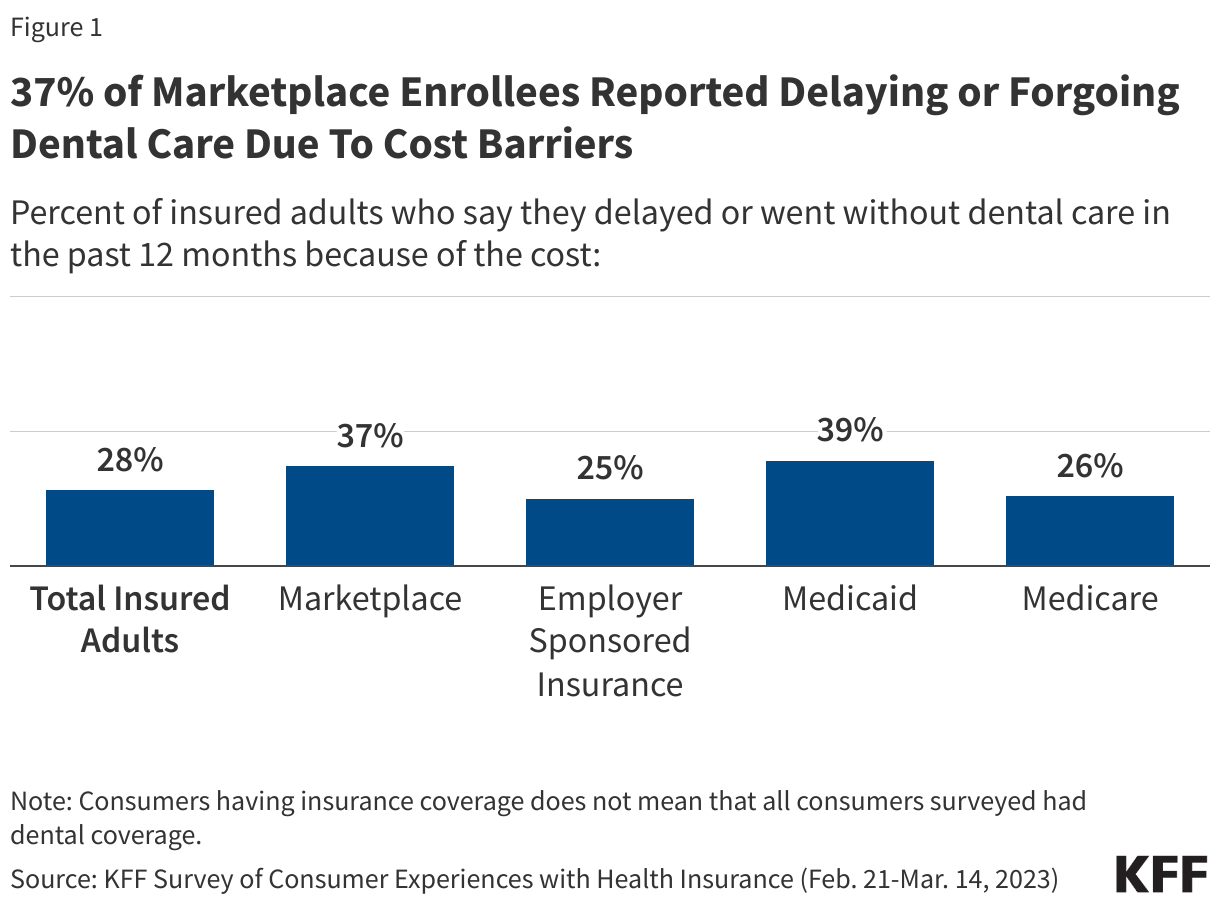

The KFF Consumer Survey of Consumer Experiences with Health Insurance finds that consumers who reported having insurance coverage at the time of the survey tend to avoid seeking dental care if the out-of-pocket costs are high. Across coverage types, at least one in four adults with health insurance report cost barriers to accessing dental care in the past year, including about four in ten of those with Medicaid (39%) and Marketplace coverage (37%) and a quarter of those with ESI (25%) and Medicare (26%) (Figure 1).

Delaying needed dental care could lead to more serious health problems down the road. Poor dental health is associated with chronic diseases such as diabetes, heart disease, and oral cancer, and could also lead to additional burdens on the healthcare system as patients seek care elsewhere.

The HHS Benefit and Payment Parameters Notice for 2025 proposes to remove the prohibition on the classification of routine adult dental health coverage as an EHB. Under this proposed rule, states would have the option of classifying adult dental care as an EHB. If a state chose to classify adult dental health as an EHB, the state (or the federal government as a fallback) would be required to enforce the same ACA protections for adult dental coverage that apply to other EHBs. They would also have the option of applying additional protections for adult dental coverage offered as an EHB that goes beyond the federal requirements for EHBs.

What Are the Key Issues to Watch?

Embedded deductibles might not provide consumers with financial protection for dental care. One issue raised in comment letters for the 2025 Payment Notice is that consumers who receive dental care through embedded dental coverage may have to meet the medical deductible before coverage of dental services can begin. If a state chooses to offer adult dental care as an EHB, medical plans would be required to cover it, and the medical deductible could apply. Deductibles under medical plans can be thousands of dollars, which may deter consumers from seeking dental care, especially people with lower incomes.

Classifying adult dental care as an EHB could come at an increased cost to the federal government and health issuers. CMS stated in the proposed rule that it does not anticipate any immediate costs as a result of giving states the option to include adult dental care as an EHB. However, it is possible that application of advanced premium tax credits towards dental care could raise costs for the federal government. Additionally, cost sharing provisions that apply to EHBs, such as the ban on annual and lifetime coverage limits and the maximum annual out of pocket limit, could increase costs for health plan issuers since they could no longer apply these restrictions on dental care.

The new provision could affect employer-sponsored plans. Small employer plans, like those in the individual market, are required to cover EHBs. While large employer plans do not have to meet EHB rules, federal regulations require that these plans choose a state benchmark in order to comply with the ACA’s prohibition on annual and lifetime dollar limits. CMS pointed out in the proposed Payment Notice that if a self-insured or fully-insured large employer plan selects a state benchmark plan that includes adult dental care as an EHB, they would be required to abide by the cost-sharing requirements that apply to other EHBs. Employer plans that offered dental plans separately as “excepted benefits” (which are not subject to ACA requirements for comprehensive medical insurance), however, would presumably not be required to abide by these requirements.

Consumers could be subject to cost-sharing for preventive dental services. The ACA requires most private health plans to cover, without cost sharing, preventive health services rated as an A or B in the United States Preventive Service Task Force recommendations; however, no adult dental services have received this A or B rating. Consumers could be subject to cost sharing for routine preventive dental services or be required to meet the deductible before coverage of preventive services began, although as stated above, many private health plans already cover preventive health services such as cleanings before the deductible.

Looking Forward

The ACA’s EHB requirements seek to ensure consumers in the individual and small group markets have comprehensive coverage that meets vital health needs. The law requires the Secretary of HHS to define EHB that covers at least 10 general categories of benefits and has a scope equal to those “under a typical employer plan.” According to the 2023 KFF Employer Health Benefits Survey, 90% of small firms and 94% of large firms offer dental insurance programs to their employees. If the proposed 2025 Payment Rule is finalized as proposed, this will allow states to choose to include adult dental care as a required benefit in state-regulated health plans. This could enhance efforts to increase access to dental care, especially for lower income adults who are particularly susceptible to having unmet dental health needs. In addition, KFF research shows that dental costs are a contributor to medical debt. CMS and states may evaluate the most appropriate ways to structure an adult dental benefit that provides financial protections to avoid debt for common basic care, balanced by potential increases in federal costs.

This work was supported in part by a grant from the Robert Wood Johnson Foundation. The views and analysis contained here do not necessarily reflect the views of the Foundation. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.