Health Care Debt In The U.S.: The Broad Consequences Of Medical And Dental Bills

Overview

The KFF Health Care Debt Survey is part of a broader investigative project on health care debt conducted by our colleagues at KHN in partnership with NPR. The survey was designed and analyzed by public opinion researchers at KFF in collaboration with KHN journalists and editors. This Report contains findings from the survey as well as the topline and methodology. The KFF Health Care Debt Survey provides a broad measure of health care debt, including medical and dental bills people are unable to pay as well as different forms of debt accruing from health care bills such as payment plans, credit cards, bank loans, and borrowing from family and friends. It also explores the effects of health care debt on individuals and the financial and personal sacrifices they make due to their debt.

Diagnosis: Debt is a multimedia investigative journalism series by KHN and NPR that explores the scale, impact, and causes of health care debt in America. It represents a fusion of the investigative power of KHN and NPR, the public opinion survey expertise of the KFF polling team, and original data analysis.

Explore the project’s journalism:

Diagnosis Debt:100 Million People in America Are Saddled With Health Care Debt, published June 16, 2022.

Upended: How Medical Debt Changed Their Lives, published June 16, 2022.

NPR Morning Edition: Sick and struggling to pay, 100 million people in the U.S. live with medical debt, aired June 16, 2022.

Medical Bills Can Shatter Lives. North Carolina May Act to ‘De-Weaponize’ That Debt, published June 21, 2022.

In America, Cancer Patients Endure Debt on Top of Disease, published July 9, 2022.

Nursing Homes Are Suing the Friends and Family of Residents to Collect Debts, published July 28, 2022.

Few Places Have More Medical Debt Than Dallas-Fort Worth, but Hospitals There Are Thriving, published Sept. 28, 2022.

Main Findings

Introduction

This is a companion report by the KFF polling group for an investigative project on health care debt conducted by our colleagues at KHN in partnership with NPR. The KFF Health Care Debt Survey was designed and analyzed by public opinion researchers at KFF in collaboration with KHN journalists and editors. The survey provides a broad measure of health care debt in the U.S. and explores the effects of health care debt on individuals and the financial and personal sacrifices they make due to their debt.

Rising health care costs have been a dominant concern in the U.S. for both individuals and for the nation as a whole for many years. For individuals, these rising – and sometimes unexpected – health care costs can often lead to debt. Discussions about the problem of health care-related debt in the United States have typically focused more narrowly on medical bills that people are unable to pay or those that have been sent to collections. However, the problem of health care debt is ultimately much larger when looking at different types of debt that are caused at least partially by medical or dental bills. Indeed, often individuals use other forms of borrowing or debt, such as payment plans, credit cards, bank loans, and borrowing from family and friends to pay their medical and dental bills. These forms of debt are sometimes not included in estimates of medical debt from other surveys and administrative data.

To fill this gap, KFF conducted an in-depth, nationally representative survey with 2,375 adults, including interviews with 1,292 adults with current health care debt. The survey defined health care debt as any money respondents currently owe or debt they have due to medical or dental bills for their own or someone else’s medical or dental care, including any bills that are past due or that they are unable to pay, any bills they are paying off over time directly to a provider, any debt they owe to a bank, collection agency, or other lender that includes debt or loans used to pay medical or dental bills, any bills they have put on a credit card and are paying off over time and any debt owed to a family member or friend for money they borrowed to pay medical or dental bills.

Executive Summary

Debt due to medical and dental bills is a widespread issue in the United States, affecting both uninsured and insured adults. Health care related debt encompasses more than just unpaid or past due bills from providers. Substantial shares of adults carry debt from medical and dental bills that they have paid off by taking on other forms of debt, including credit cards, personal bank loans, or loans from family and friends. The KFF Health Care Debt Survey finds that four in ten adults have some form of health care debt. Yet the likelihood of having health care debt is not evenly distributed. Uninsured adults, women, Black and Hispanic adults, parents, and those with lower incomes are especially likely to say they have health care-related debt.

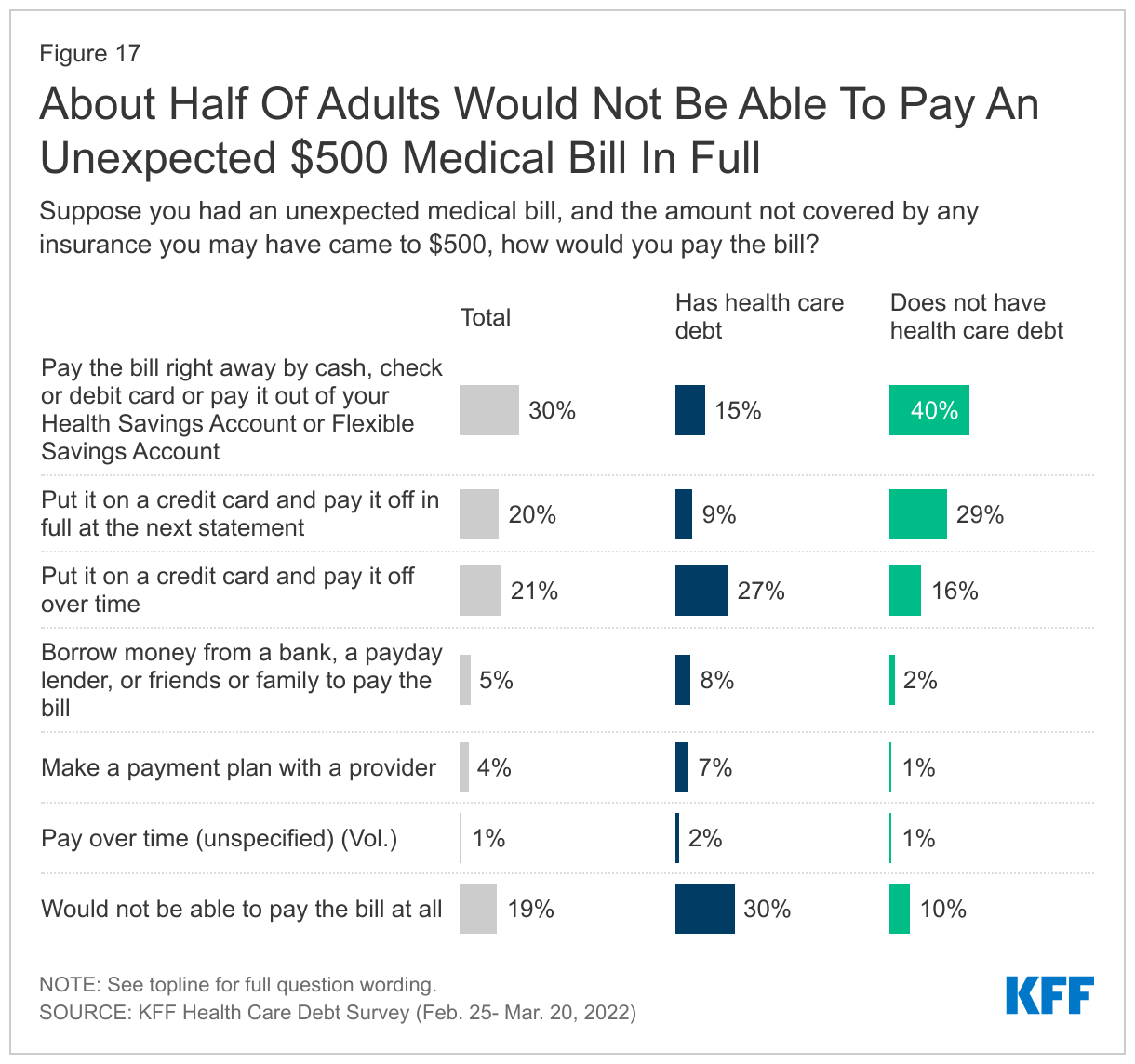

Unexpected bills can be a major contributor to health care debt. Most adults with health care debt say the bills that led to their debt were from a one-time or short-term medical expense, which are often unexpected. Indeed, about half of adults – including three in ten of those who do not currently have health care debt – are vulnerable to falling into debt, saying they would be unable to pay a $500 unexpected medical bill without borrowing money. While about a third of adults with health care debt owe less than $1,000, even small amounts of debt can have significant financial consequences for some. Though a third of those with current debt expect to pay it off within a year and about a quarter expect to pay it within one to two years, nearly one in five adults with health care debt think they will never be able to pay it off.

In their efforts to service or pay off their debt, adults with health care debt report making a number of sacrifices and enduring substantial financial consequences. Most report cutting back on household spending, and more than four in ten say they or a household member have used up all or most of their savings due to their health care debt. Many also report more serious consequences like skipping payment on other bills, delaying college or buying a home, or changing their housing situation as a result of their debt. In addition, about half of adults with health care debt say they have made what they feel to be a difficult sacrifice in order to pay down their debt. These sacrifices have left some individuals feeling as if they could not provide a good life for their families, or with a general sense that they will never be able to extricate themselves from debt. Other reported consequences of debt, such as being contacted by debt collectors and having their credit scores negatively affected, can lead to additional financial problems such as difficulty buying vehicles needed for work or buying or renting a home.

Health care debt can also affect the ability of individuals to access needed medical or dental care. One in seven adults with health care debt say they have been denied care by a provider due to unpaid bills. In addition, adults with health care debt are more than twice as likely as those without debt to say they or someone they live with have postponed or skipped getting needed health care because of the cost.

The unequal consequences of health care debt are evident in the survey results. Among those with debt due to medical or dental bills, those with lower incomes and people of color (particularly Black adults), are more likely than their counterparts to report experiences like being contacted by collection agencies due to health care debt, being denied subsequent care, and making difficult sacrifices like changing their housing situation to pay down their debt.

Who Has Health Care Debt Due To Medical And Dental Bills?

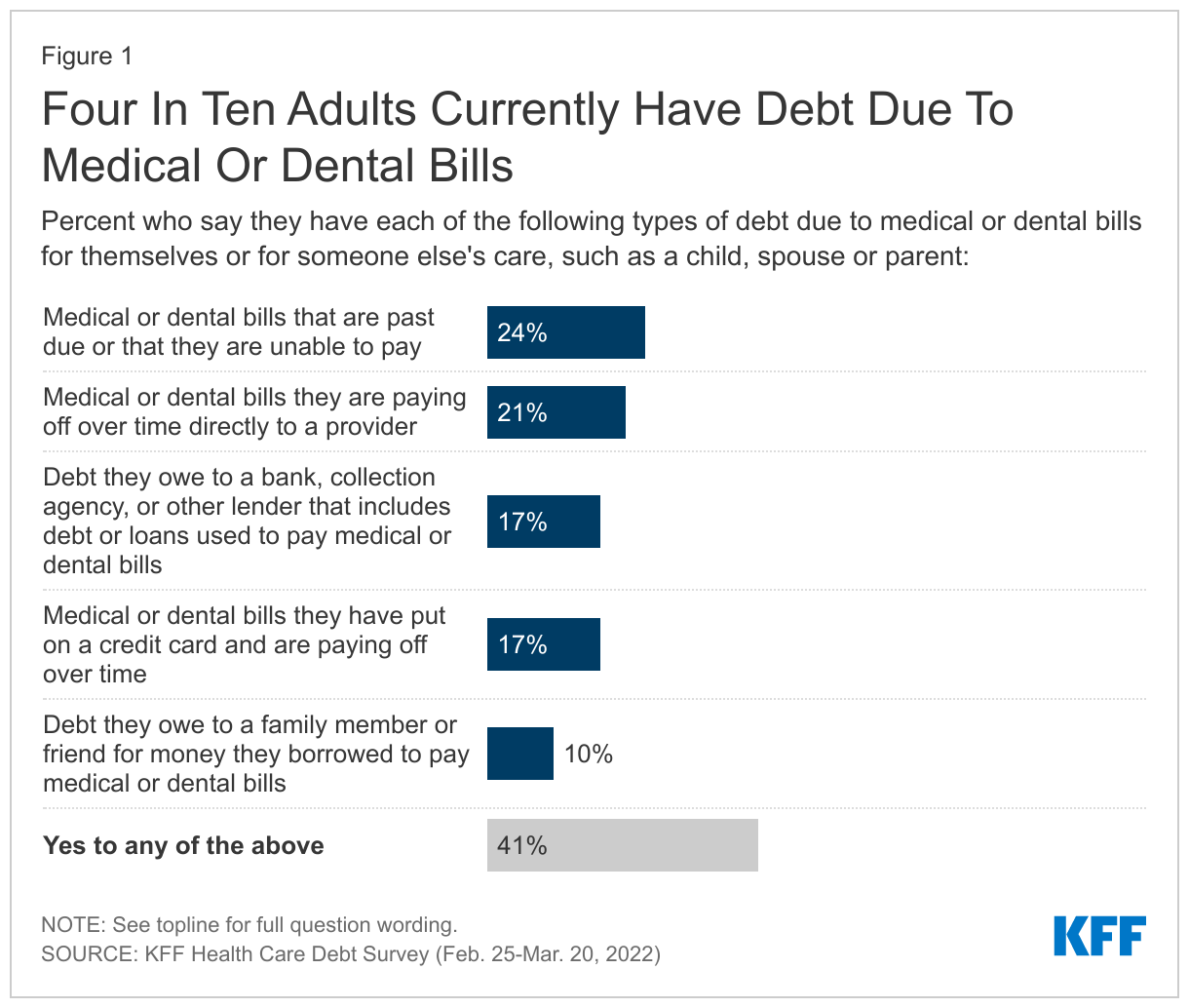

The KFF Health Care Debt Survey finds that 41% of adults currently have some debt caused by medical or dental bills. To develop this measure, we asked respondents to think about any money they currently owe or debt they have due to medical or dental bills for their own medical or dental care or someone else’s care, such as a child, spouse, or parent. We then asked whether they currently have five different types of debt due to medical or dental bills: any bills that are past due or that they are unable to pay; any bills they are paying off over time directly to a provider; any debt they owe to a bank, collection agency, or other lender that includes debt or loans used to pay medical or dental bills; any bills they have put on a credit card and are paying off over time; or any debt owed to a family member or friend for money they borrowed to pay medical or dental bills.

Estimating The Prevalence of Health Care Debt

The total share of U.S. adults with health care debt is difficult to estimate with precision and varies widely depending on the measures. The Consumer Financial Protection Bureau (CFPB) estimates that $88 billion in medical debt is reflected on Americans’ credit reports, though they acknowledge the total amount of medical debt is likely higher because not all medical debt is visible to consumer reporting companies and those data only reflect debt among people with credit reports (not all adults). A recent Census Bureau analysis of data from the 2020 Survey of Income and Program Participation (SIPP) on medical debt at the household level found 17% of households owed medical debt in 2019. A KFF analysis of the 2020 SIPP found that one in ten adults in the U.S. have significant medical debt (“significant” defined as medical debt of over $250) and that U.S. adults owe at least $195 billion in medical debt.

Nationally representative surveys generally capture a larger share of people and more types of medical debt than analyses of credit reports, yet challenges remain in capturing data of people who have debt due to medical and dental bills. Certain types of medical debt may not be disclosed or present on credit reports or can be disguised as another form of debt not typically captured in surveys. For example, people may pay for a medical expense on a credit card or fall behind on other payments in order to keep up with medical bills. The KFF Health Care Debt Survey asked about different forms of debt individuals may have used to pay their medical and dental bills in order to provide a broader estimate of adults who currently have health care debt. Other estimates of medical debt from recent years can be found in the Appendix of this report.

More specifically, about a quarter of adults (24%) say they currently have medical or dental bills that are past due or that they are unable to pay, about one in five (21%) say they have bills they are paying off over time directly to a provider, about one in six say they have debt they owe to a bank, collection agency, or other lender that for loans used to pay medical or dental bills (17%) or say they have medical or dental bills they have put on a credit card and are paying off over time (17%), and one in ten (10%) say they have debt they owe to a family member or friend for money borrowed to pay medical or dental bills.

Beyond the 41% of adults who currently have some form of health care debt, a further 16% of adults say they have had debt due to medical or dental bills in the past five years that has since been paid off.1 This means in total, most adults (57%) have experienced owing money due to medical or dental bills at some point in the past five years.

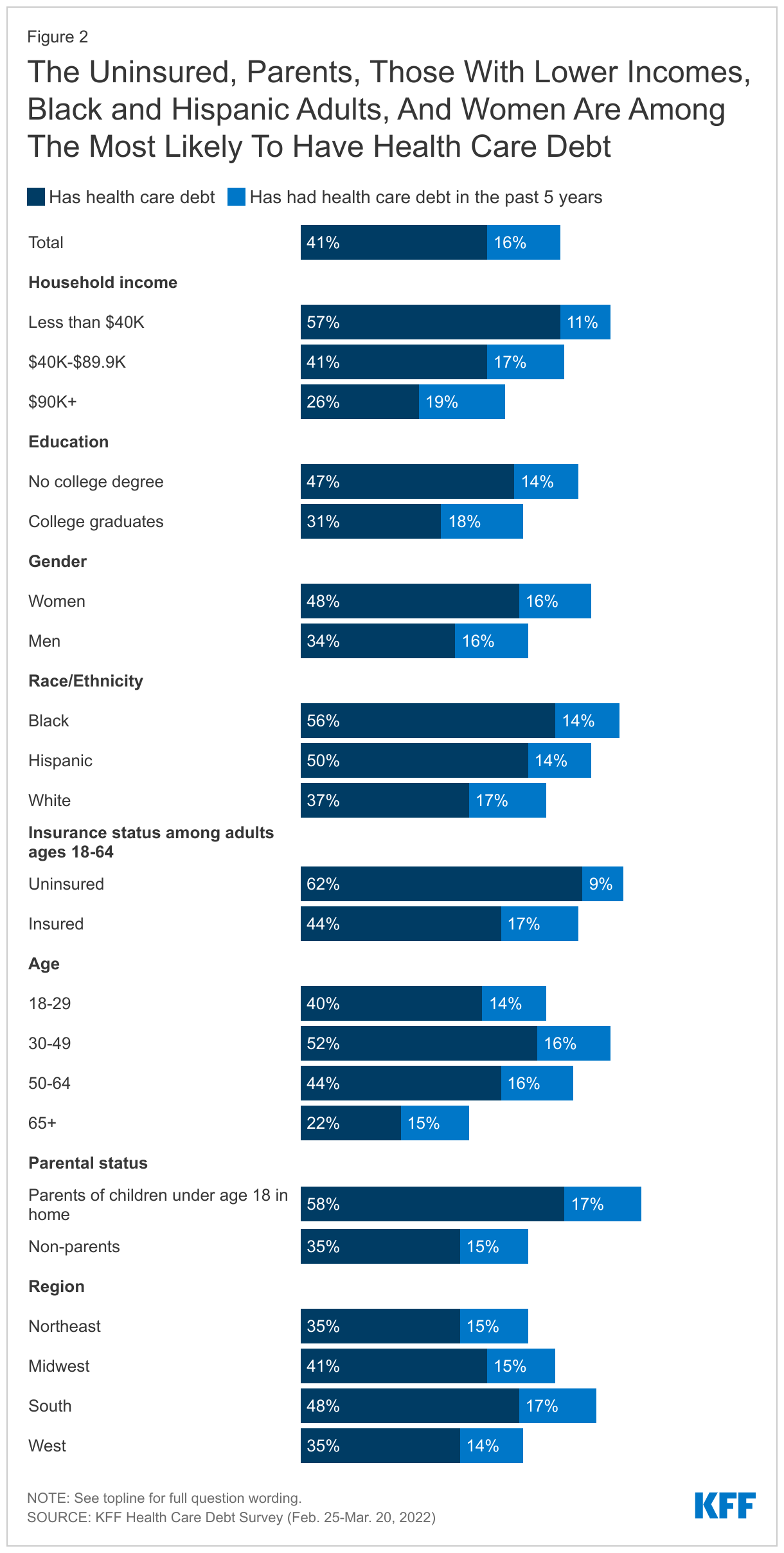

Adults with lower levels of education and income are more likely than those with higher education and higher income to say they have current health care debt due to medical or dental bills. Nearly half of without a college degree (47%) say they have health care debt compared to about three in ten college graduates (31%). While a majority (57%) of adults with household incomes under $40,000 say they currently have debt due to medical or dental bills, it is also notable that health care debt is not entirely uncommon among those with higher incomes (26% of those in households earning $90,000 or more). Among adults with health care debt, those with higher incomes are more likely to report debt due to medical bills in the form of credit card debt or bank loans, while those with lower incomes are more likely to report being indebted to friends or family.

There are also differences by gender, race, and ethnicity when it comes to current health care debt. Nearly half of women say they have debt due to medical or dental bills, compared to about a third of men (48% vs. 34%). Across race and ethnic groups, at least half of Black (56%) and Hispanic (50%) adults say they have debt due to medical or dental bills, compared to fewer White adults (37%). Unsurprisingly, among adults under 65, those who are currently uninsured are more likely to say they have health care debt than those who currently have health insurance (62% vs. 44%), though it’s notable that over four in ten adults with health insurance also report current debt.

By age, health care debt peaks among those between the ages of 30 and 49, with 52% in this age group saying they have current health care debt. This is likely related to the fact that about half of people in this age group are parents of children under 18, and parents are significantly more likely than non-parents to report having health care debt from their own or someone else’s medical or dental bills (58% vs. 35%). Over one in five adults ages 65 and over (22%) say they currently owe money due to medical or dental bills. Medicare provides near universal coverage to seniors, but it has gaps that can leave beneficiaries with substantial out-of-pocket costs.

Notably, across regions of the country, almost half of adults in the South say they have health care debt, compared to about a third of adults in the Northeast and in the Western U.S. who say the same. In addition, nearly half of adults (47%) in the twelve states that have not expanded their Medicaid program under the Affordable Care Act say they have current health care debt, compared to 39% in Medicaid expansion states.

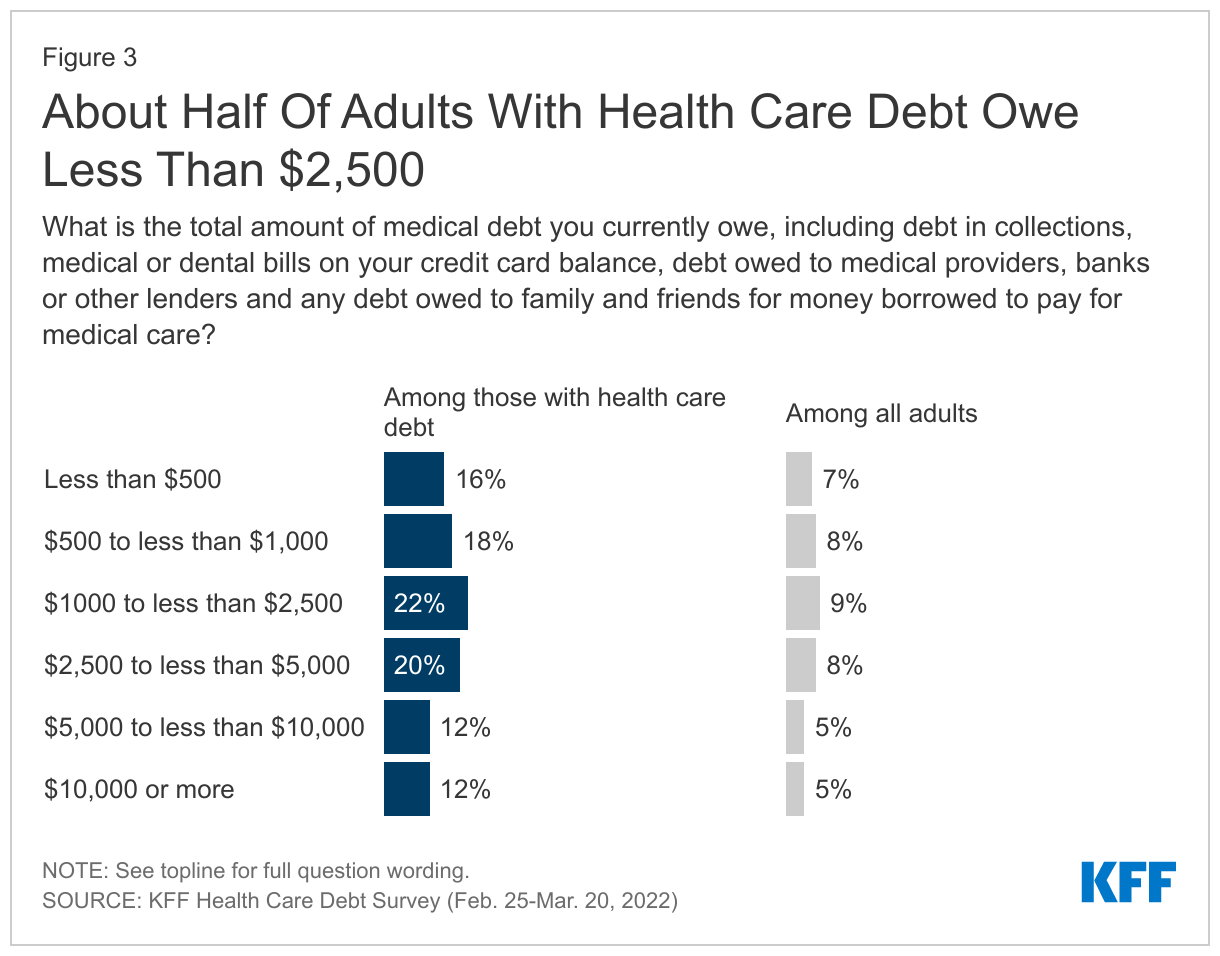

Health care debt does not have to be enormous for people to have problems paying it off, though some do report owing large amounts. About half of adults with current health care debt (56%) say they owe less than $2,500, including 16% who say they owe less than $500 and 18% who owe between $500 and $1,000. Nearly half (44%) report owing at least $2,500 due to medical or dental bills, including about one in eight (12%) who say they owe $10,000 or more.

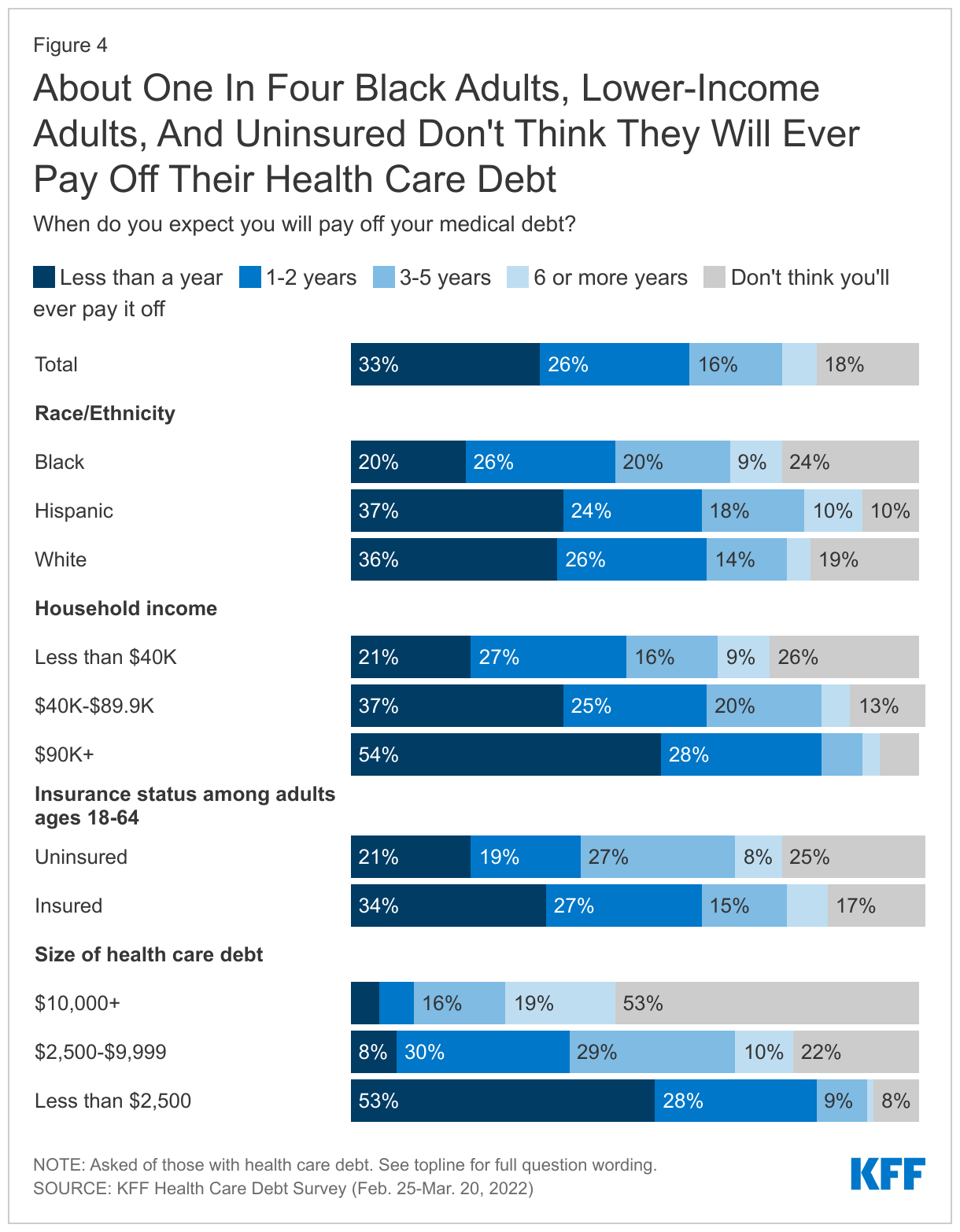

Most (59%) adults with current health care debt think they will be able to pay off their debt within two years, including a third who think they will pay it off within a year. However, nearly one in five (18%) say they don’t think they will ever pay it off. Notably, about one in four Black adults (24%), adults with household incomes under $40,000 (26%), and those who are uninsured (25%) say they don’t think they will ever pay off their health care debt.

Expectations of paying off health care debt also vary widely by the amount of debt. Among those who owe less than $1,000, nearly two-thirds (63%) say they expect to pay it off within one year. By contrast, about half (53%) of those who owe $10,000 or more say they’ll never be able to pay it off.

Causes Of Health Care Debt

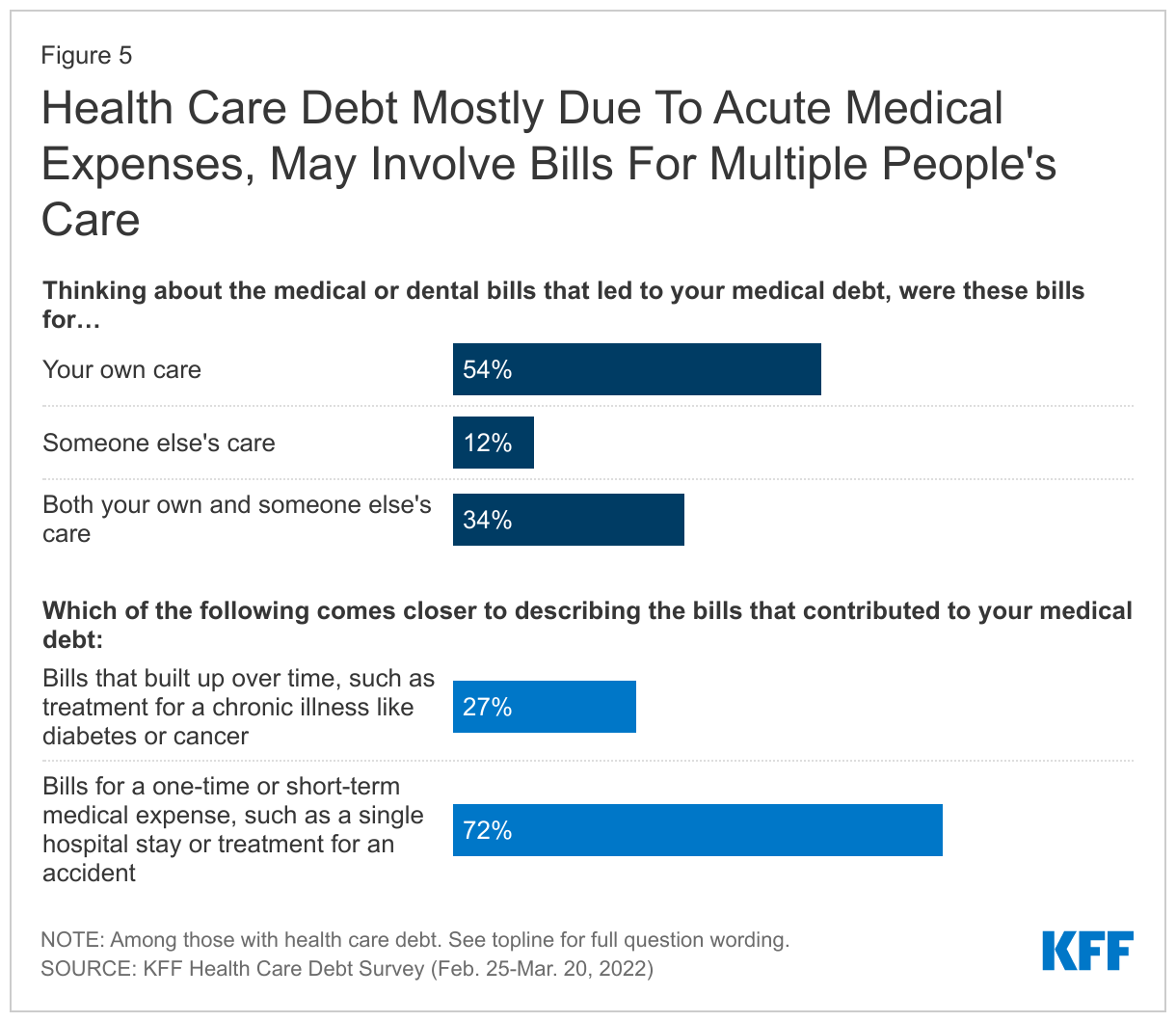

Debt due to health care bills can be driven by one individual’s medical care, but often multiple family members’ bills can contribute to overall debt. While about half (54%) of adults with health care debt say the bills that led to their debt were only for their own care, 12% say their health care debt stemmed from bills for someone else’s care and another third (34%) say that bills for both their own and someone else’s care contributed to the debt.

Highlighting how one acute medical or dental incident can lead to persistent debt, seven in ten adults with health care debt (72%) say the bills that led to their debt were for a one-time or short-term medical expense, such as a single hospital visit or treatment for an accident. Many in this group (24%, or 30% of all adults with health care debt) say the incident that led to their debt occurred three or more years ago. About a quarter of adults (27%) say their medical debt built up over time, such as treatment for a chronic illness.

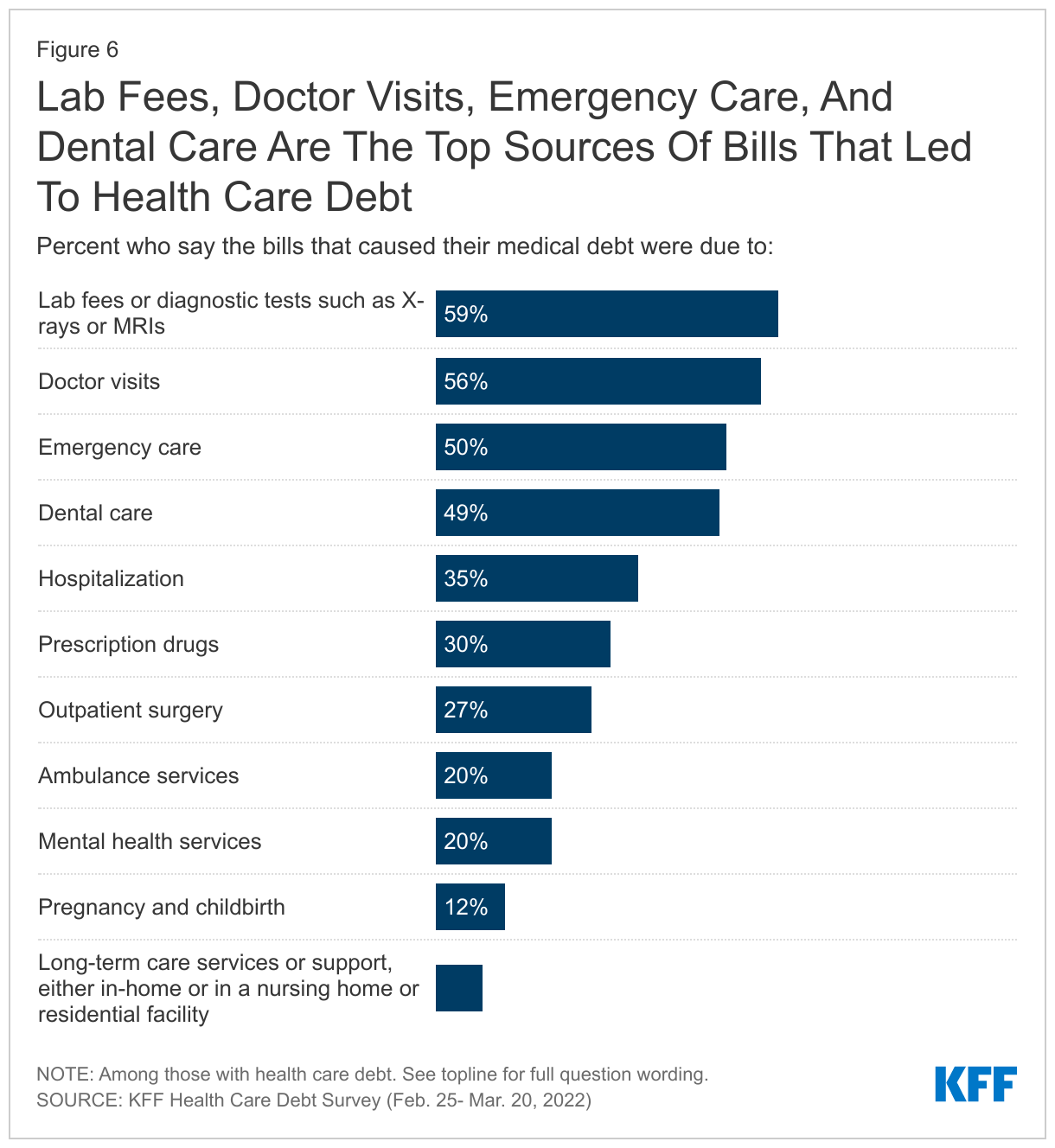

Common health care needs such as lab and diagnostic test and doctor’s visits are also common sources of health care debt. Among adults with health care debt, about six in ten (59%) say some of the bills that led to their debt were due to lab fees or diagnostic tests and over half (56%) say bills from doctor visits contributed to their debt. Half of adults with health care debt say bills from emergency care (50%) caused their debt, again highlighting how one-time acute medical events can cause people to fall into health care debt.

About half of adults with health care debt (49%) say dental bills caused some of their debt. Notably, dental insurance, which typically has annual limits on coverage, does not necessarily protect individuals from falling into debt due to dental bills. Among those who say dental bills contributed to their health care debt, 60% say they or the person whose bills led to their debt had dental coverage at the time.

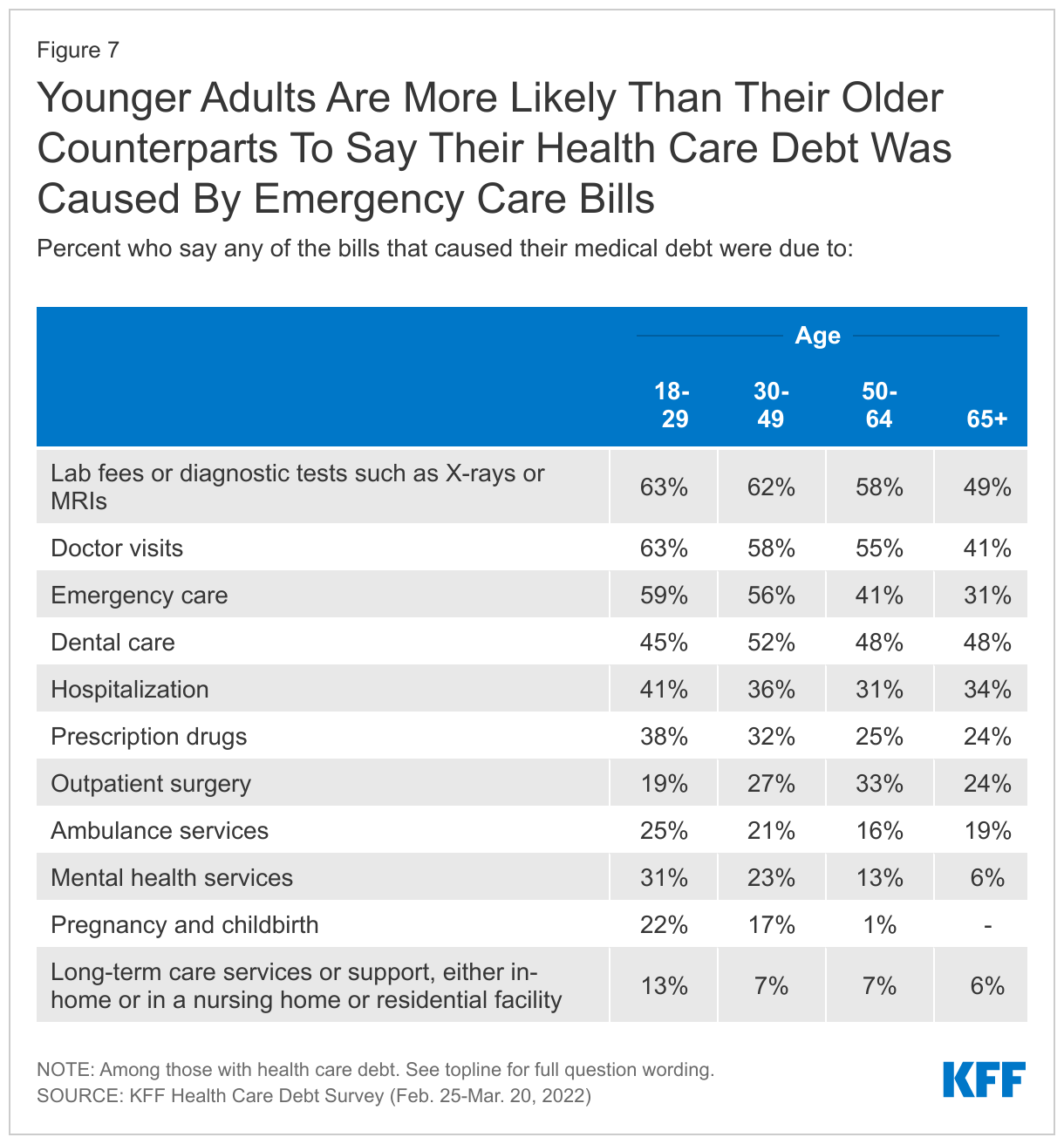

The types of bills that lead to health care debt vary by age. Notably, one of the most common types of bills leading to health care debt for older adults is dental care, likely because traditional Medicare does not provide dental coverage (though some beneficiaries in private Medicare Advantage plans do have dental coverage, with the scope varying widely). By contrast, older adults are less likely than their younger counterparts to say their health care debt resulted from lab fees, doctor visits, or emergency care.

Other types of bills are more common sources of health care debt among younger adults. A majority of adults with health care debt under age 50 say their debt was at least partially due to bills for emergency care, compared to about four in ten (41%) of those ages 50-64 and about three in ten (31%) of those ages 65 and over. Adults under age 30 are also more likely than their older counterparts to report their health care debt is due at least partially to bills for mental health services (31%).

For young families, pregnancy and childbirth can lead to health care debt. Among adults under age 30 who have health care debt, 22% say that bills from pregnancy and childbirth contributed to their debt, rising to 29% of women in this age range.

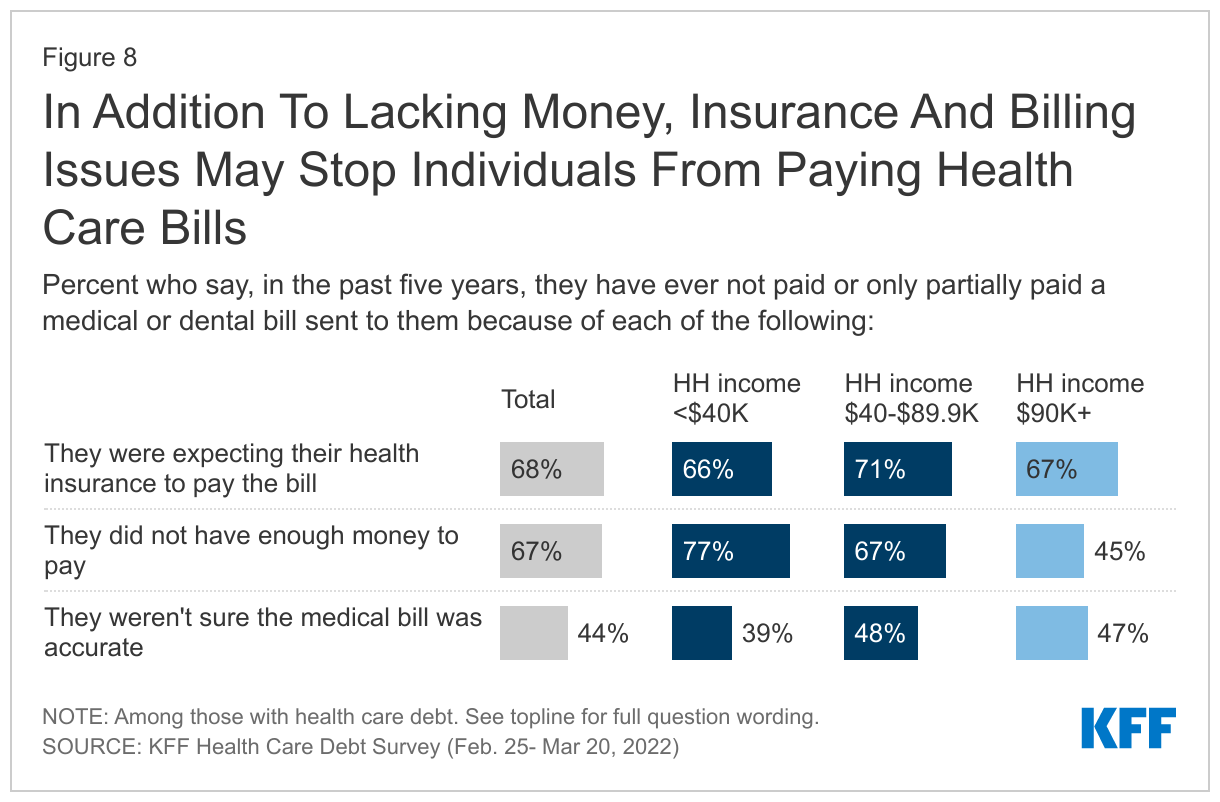

Lacking money to pay a bill is often a reason people fall into debt, but complications in billing and insurance practices may also be contributing factors for some. Two-thirds (67%) of those with health care debt say that in the past five years, they have not paid or only partially paid a medical bill because they didn’t have enough money to pay it. But a roughly equal share (68%) say they have not paid a bill in full because they were expecting their health insurance to pay the bill. About four in ten (44%) adults with health care debt say that they did not pay a bill in full in the past five years because they weren’t sure the bill was accurate.

Unsurprisingly, lack of money to pay a bill is particularly an issue for those with lower household incomes. More than three in four adults with health care debt whose income is under $40,000 (77%) say they have failed to pay a medical bill for because they did not have enough money, compared to fewer than half of those with incomes of $90,000 or more. Yet issues with insurance occur across income levels as majorities with health care debt across income groups say they have not paid a medical or dental bill that was sent to them because they expected their health insurance to pay.

The Consequences Of Health Care Debt

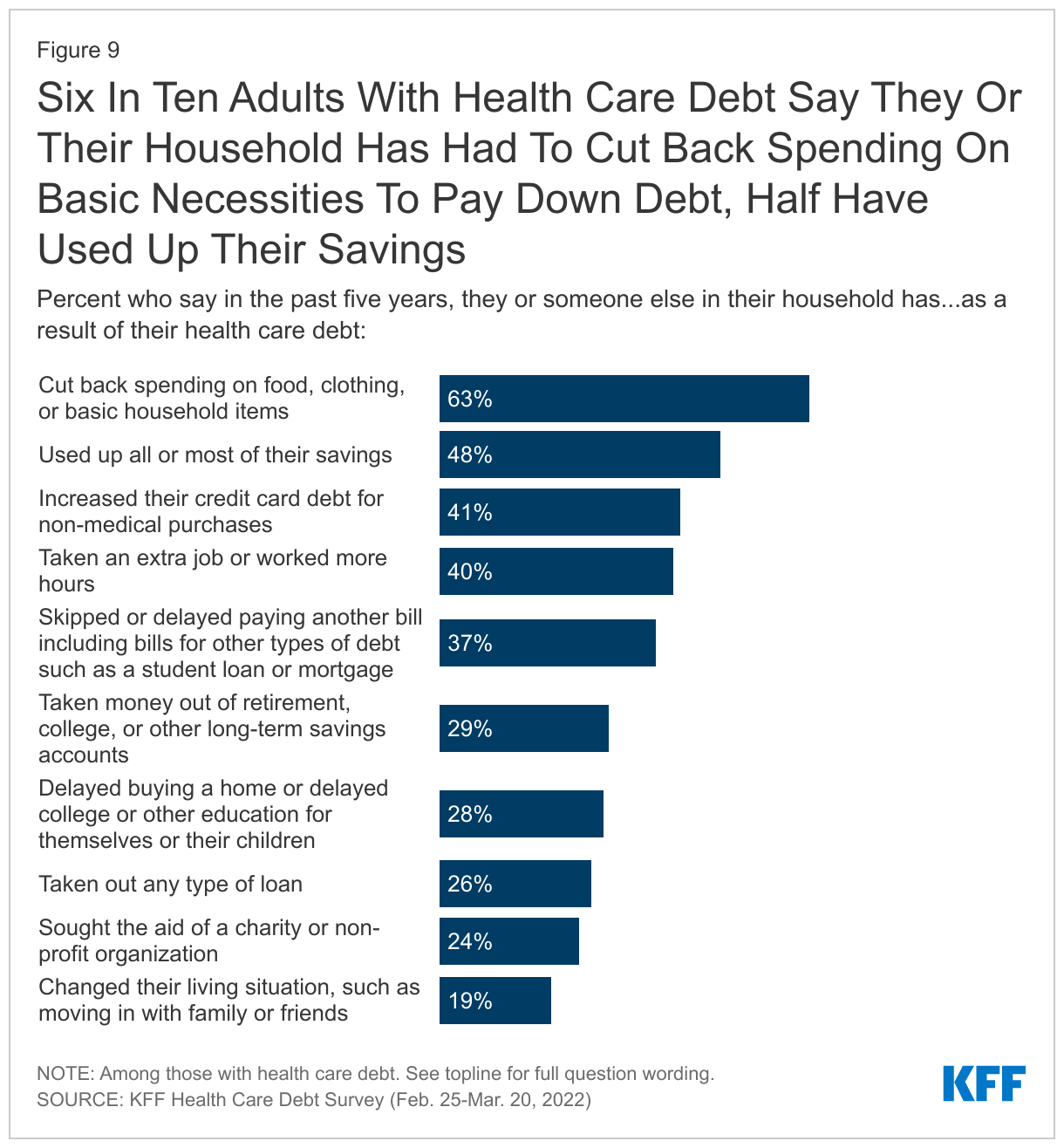

Debt due to medical and dental bills can have broad consequences for individuals and families. When asked about some specific problems they or someone in their household may have experienced in the past five years as a result of their health care debt, six in ten adults with health care debt say they cut back spending on food, clothing, and basic household items (63%). Nearly half say they used all or most of their savings (48%) and about four in ten say they increased their credit card debt for other purchases (41%), took on an extra job or worked more hours (40%), and skipped or delayed paying other bills or debt (37%) due to their health care debt. Fewer, but substantial shares, say they have taken money out of long-term savings accounts (29%), delayed buying a home or delayed education for themselves or their child (28%), taken out other loans (26%), sought aid from a charity (24%) or changed their living situation, such as living with family or friends because of their health care debt (19%).

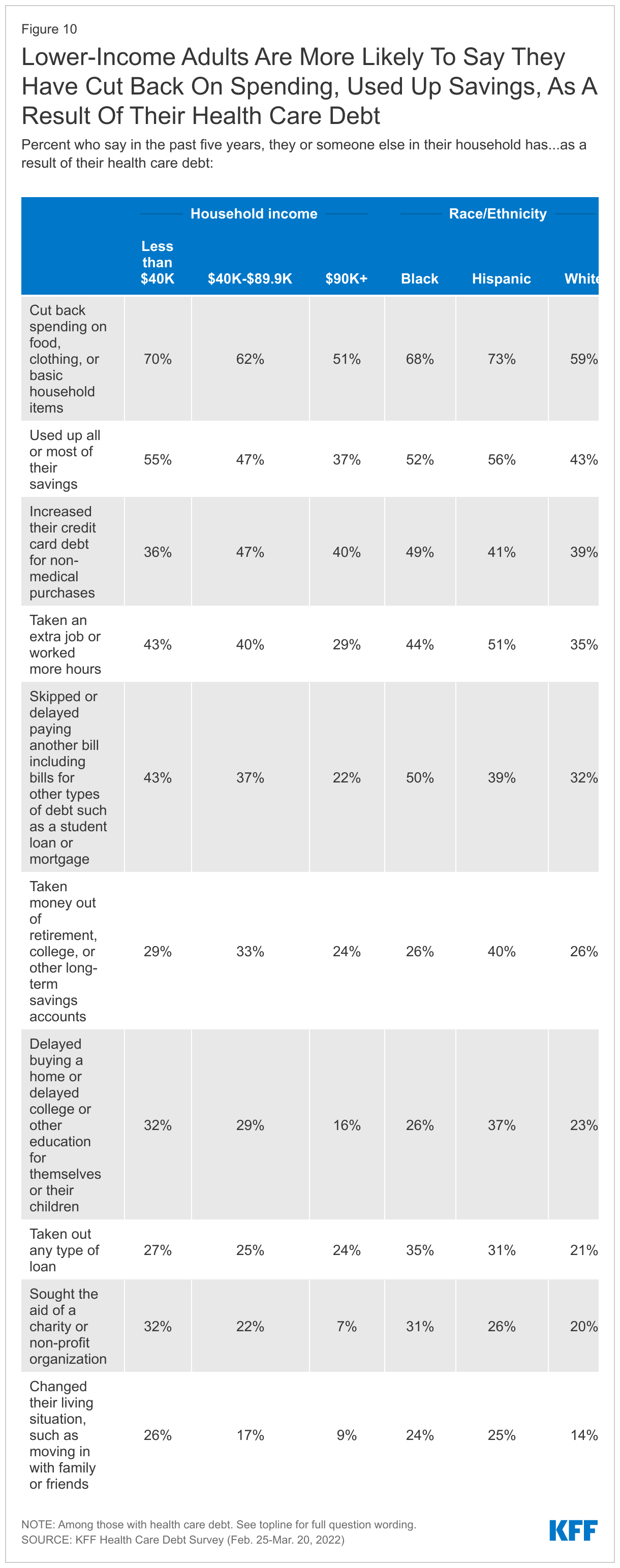

Among adults with health care debt, majorities across race and ethnic groups and at least half across income groups say they have cut back on household spending due to their medical debt. However, lower-income adults are more likely than those with higher incomes to say they have experienced certain negative consequences due to their debt. For example, over half (55%) of those with health care debt whose household income is less than $40,000 say they used up all or most of their savings due to their debt, which may put them in a further precarious financial position if they encounter future medical or other expenses. Compared to those with higher incomes, larger shares of lower-income adults with debt say they have skipped or delayed paying other bills (43%) or sought aid from charity or non-profit organization (32%). Notably, about a quarter of lower-income adults (26%), Black adults (24%), Hispanic (25%) adults with health care debt say they had to change their housing situation, such as moving in with family or friends, as a result of their debt.

Sacrifices Made Due To Health Care Debt

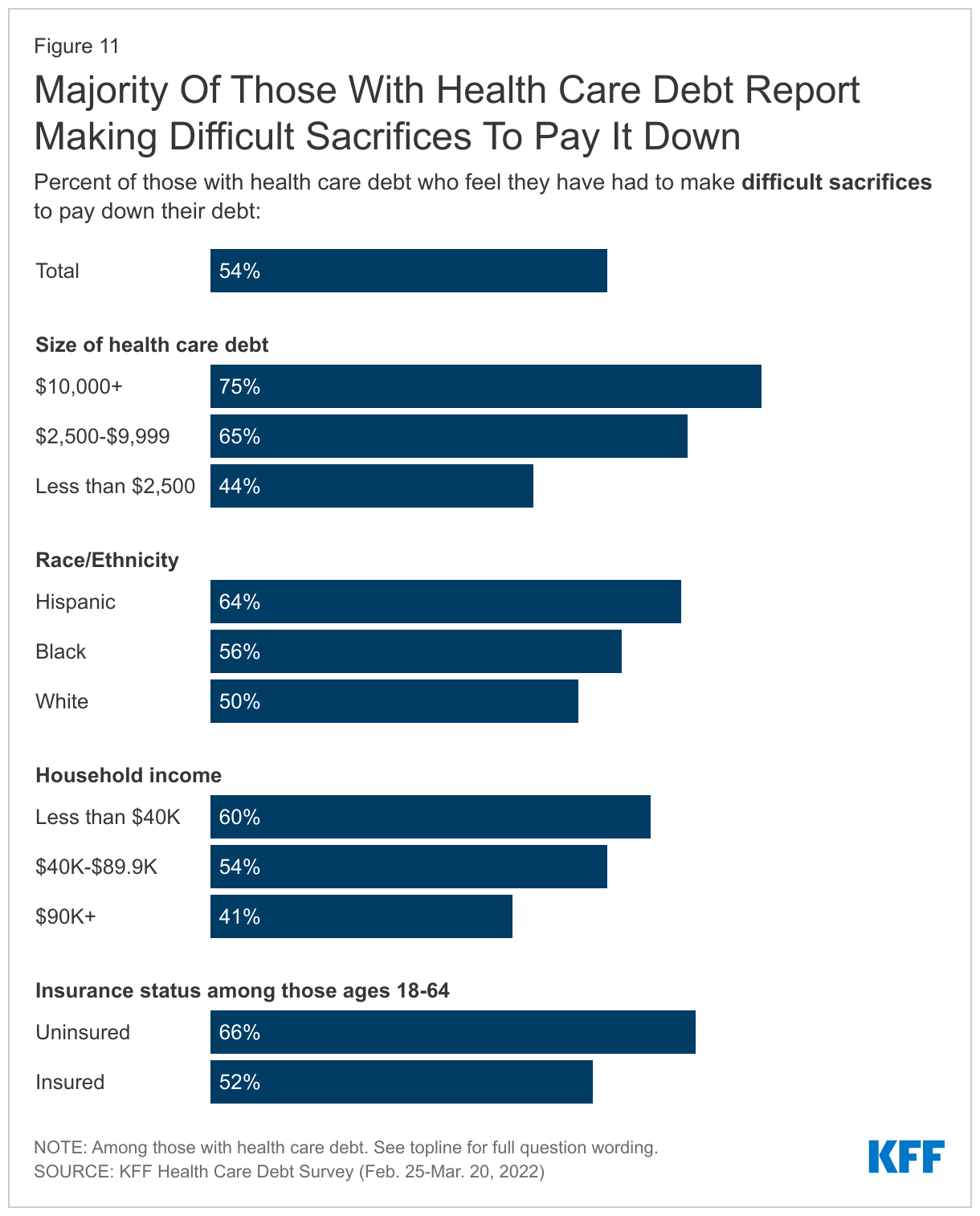

In addition to the specific consequences discussed above, over half (54%) of adults with debt due to health care bills say they have had to make what they feel is a difficult sacrifice to pay down their debt, Including at least six in ten of those in households with incomes under $40,000 (60%), Hispanic adults (64%) and those with current debt who were uninsured at the time the debt was incurred (66%).

Not surprisingly, those with greater amounts of debt are more likely to report having to make sacrifices, with three in four of those with debts of $10,000 or more reporting making a difficult sacrifice. A significant share of adults with smaller debts, however, also say they’ve had to make sacrifices (44% of those with debts under $2,500).

The sacrifices adults with health care debt say they have had to make due to their debt are wide-ranging. When adults with health care debt were asked to describe in their own words the most difficult sacrifices they have made, the most commonly cited sacrifices include cutting back spending on food or eating less (14%), followed by cutting back on discretionary spending on things such as vacations and entertainment (8%), changing their housing or living situation (7%), and increasing work hours (7%). Other sacrifices mentioned include skipping or missing payments on other bills (6%), cutting back spending in general (5%), skipping medical or dental care (5%), taking money out of savings (5%), and delaying or not buying a vehicle or selling their vehicle (5%). Many of the sacrifices cited by adults with health care debt have their own consequences that can further negatively affect their financial and emotional wellbeing. Below, in their own words, are some examples of the difficult sacrifices that adults with health care debt say they have made to pay down their debt.

In Their Own Words: What is the most difficult sacrifice you’ve made to pay down your medical debt?“

Had to move into rental place from home and not able to buy a house. Cut in some household or good food for kids.” -35 year old woman with $5,000-$10,000 in medical debt, Texas

“Quality of life. We've never been able to 'get ahead' because we have a 35 year old disabled daughter. We've had medical debt for 35 years varying from 30k down to $500.” -60 year old woman with $2,500-$5,000 in medical debt, Tennessee

“Not paying bills on time, creating larger bills due to late fees. Depleted savings.” -38 year old man with $2,500-$5,000 in medical debt, North Carolina

“Cutting out any expenses/services I can. No job, fixed income and chemo. Even with insurance, no one can afford cancer.” -67 year old woman with more than $25,000 in medical debt, Nebraska

“Limiting birthday/Christmas gifts for children and grandchildren.” -83 year old woman with $1,000-$2,500 in medical debt, New Jersey

“Getting a second job. I'm exhausted and I don't see a way out.” -44 year old woman with $1,000-$2,500 in medical debt, Ohio

“I can't do anything; I literally stay at home. Never taken my kids on vacation. I'm a single mother and all my money supports the household. So, there are not a lot of extras in my house.” -55 year old woman, with $2,500-$5,000 in medical debt, Missouri

“Strain on relationship with [my] father due to asking for help to pay medical expenses; negative impact on mental health issues (e.g., significant increase in anxiety symptoms).” -35 year old woman with $10,000-$25,000 in medical debt, New York

“This was medical debt for my (now deceased) husband -- my credit cards are maxed-out, savings is gone, I will need to relocate to afford rent and pay down bills.” -67 year old woman with $10,000-$25,000 in medical debt, Illinois

Financial And Housing Consequences

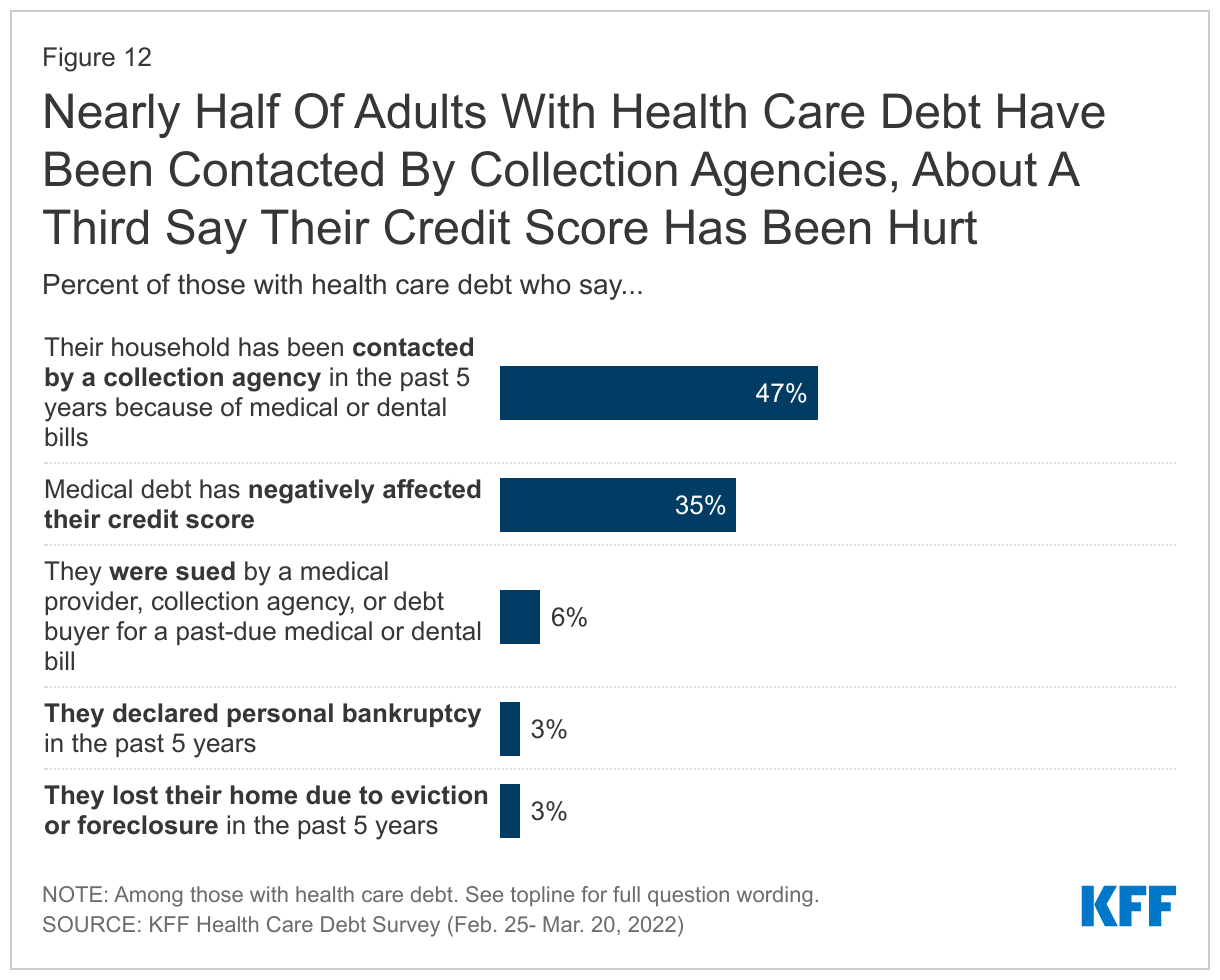

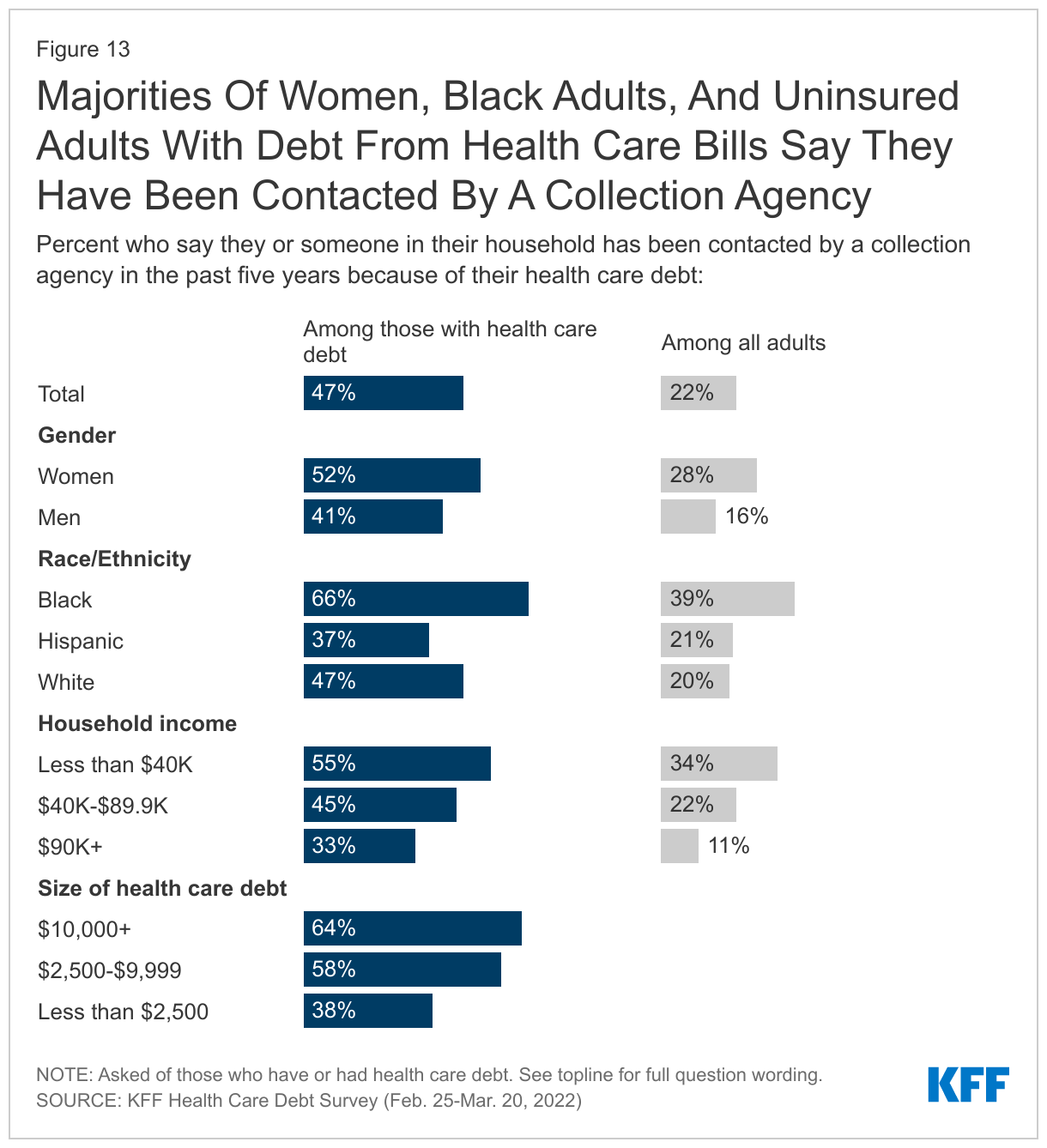

Health care debt can have significant financial consequences, including having bills going to collections, lowering credit scores, and for some can contribute to bankruptcy, home foreclosures or evictions. Nearly half of adults with health care debt say they or a member of their household has been contacted by a collection agency in the past five years because of medical or dental bills. In addition, a third of those with health care debt (35%) say it has negatively affected their credit score. Fewer say they have experienced more serious financial consequences in the past five years such as being sued by a provider (6%), declaring personal bankruptcy (3%), or losing their home due to foreclosure or eviction (3%).

Collections Agencies

Collection agencies are third-party, private companies contracted by lenders and creditors to recover funds that are past due. The Fair Debt Collection Practices Act (FDCPA) federally regulates debt collector’s malpractices to protect consumers from abusive, unfair, or deceptive practices. However, often those with debt can feel harassed and intimidated by collectors.

While half (47%) of adults with debt due to medical or dental bills say that they or someone in their household has been contacted by a collection agency because of these bills in the past five years, these shares are higher among Black adults (66%), those with lower incomes (55% of those with incomes under $40,000), and women (52%).

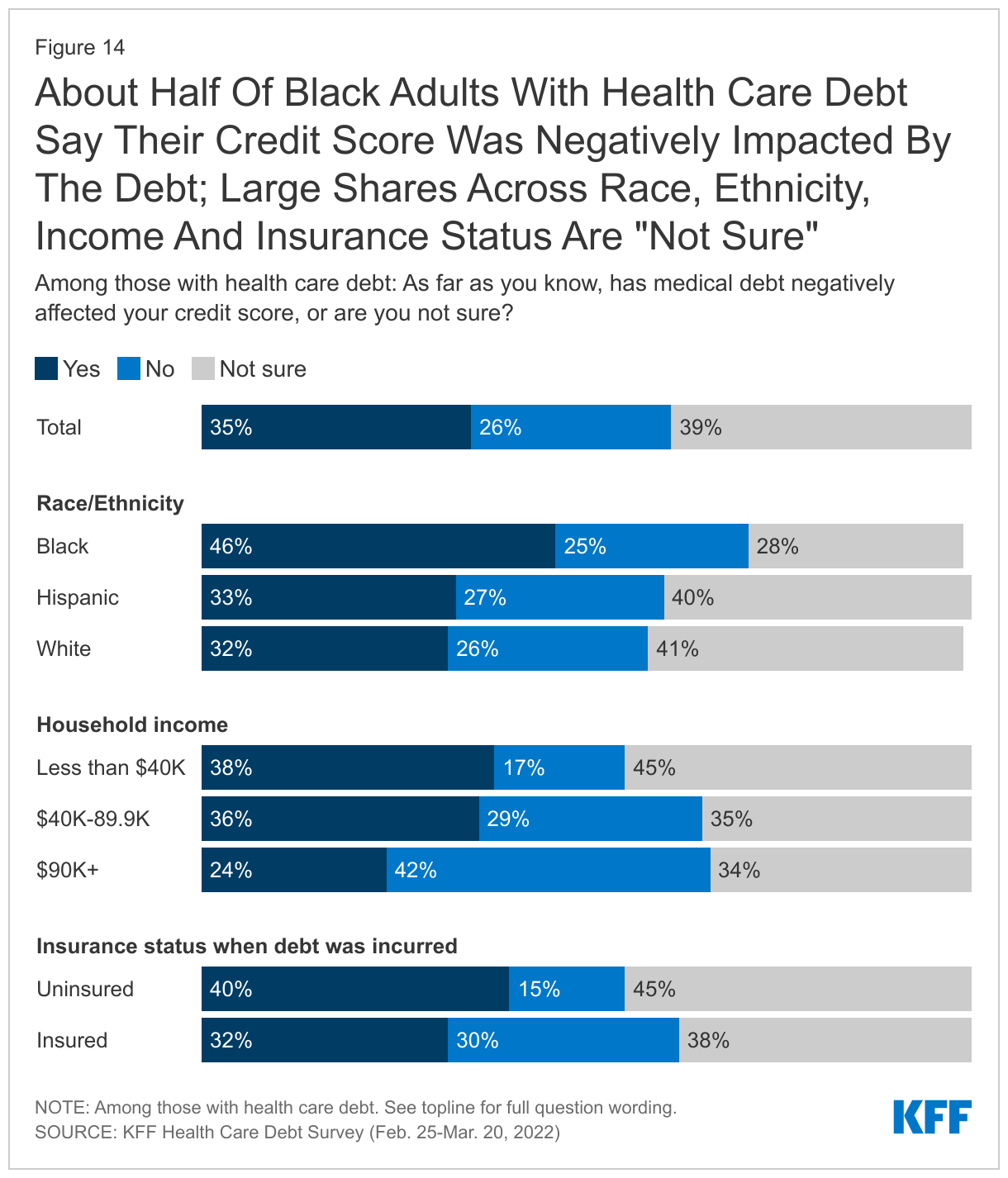

Credit Scores

Credit scores in the U.S. are important in determining financing for large purchases such as vehicles, for buying or renting a home, and for rates on future debts such as credit cards. Having a low credit score can be difficult to recover from and cause adults to go into further debt. Credit scores are determined by a number of factors, such as length of credit, unpaid balances, and missed or late payments. For many adults, it can be difficult to understand what factors are influencing the score. Recently, the three major credit bureaus in the U.S. announced that they would “no longer include medical collection debt under at least $500 on credit reports”, a move they estimate will remove nearly 70% of medical collection debt from credit reports.

The KFF Health Care Debt survey finds that more than a third (35%) of adults with health care debt say this debt has negatively impacted their credit score, yet a similar share (39%) say they are unsure if their debt has impacted their credit score. Credit score decreases are more commonly reported by Black adults with debt, as nearly half (46%) say their credit score has been negatively impacted by the health care debt they carry, compared to a third of White (32%) and Hispanic (33%) adults who say the same. Nearly four in ten (38%) adults with health care debt in households with lower incomes say their credit score has been negatively impacted by their debt, compared to one in four (24%) of those with debt in higher earning households.

The negative effect of health care debt on credit scores is noted by some adults with debt when asked to describe the sacrifices they’ve made. Some describe how poor credit scores have led to more severe financial consequences such as losing access to vehicles needed for work and to stable housing options.

In Their Own Words: The Effect Of Negative Credit Scores Due To Health Care Debt

“Said goodbye to any positive credit scores, meaning that since all my medical bills went to collections, I’ve lost over 250 points on my credit score and can no longer be even considered for any [loans].” -38 year old man with $1,000-$2,500 in medical debt, Iowa

“My credit score is so low I can't get financing for a vehicle causing me to lose my job due to lack of transportation.” -31 year old woman with $5,000-$10,000 in medical debt, Arkansas

“I became homeless because my debt has hurt my credit score.” -33 year old woman with 1,000-$2,500 in health care debt, California

Consequences For Getting And Receiving Health Care

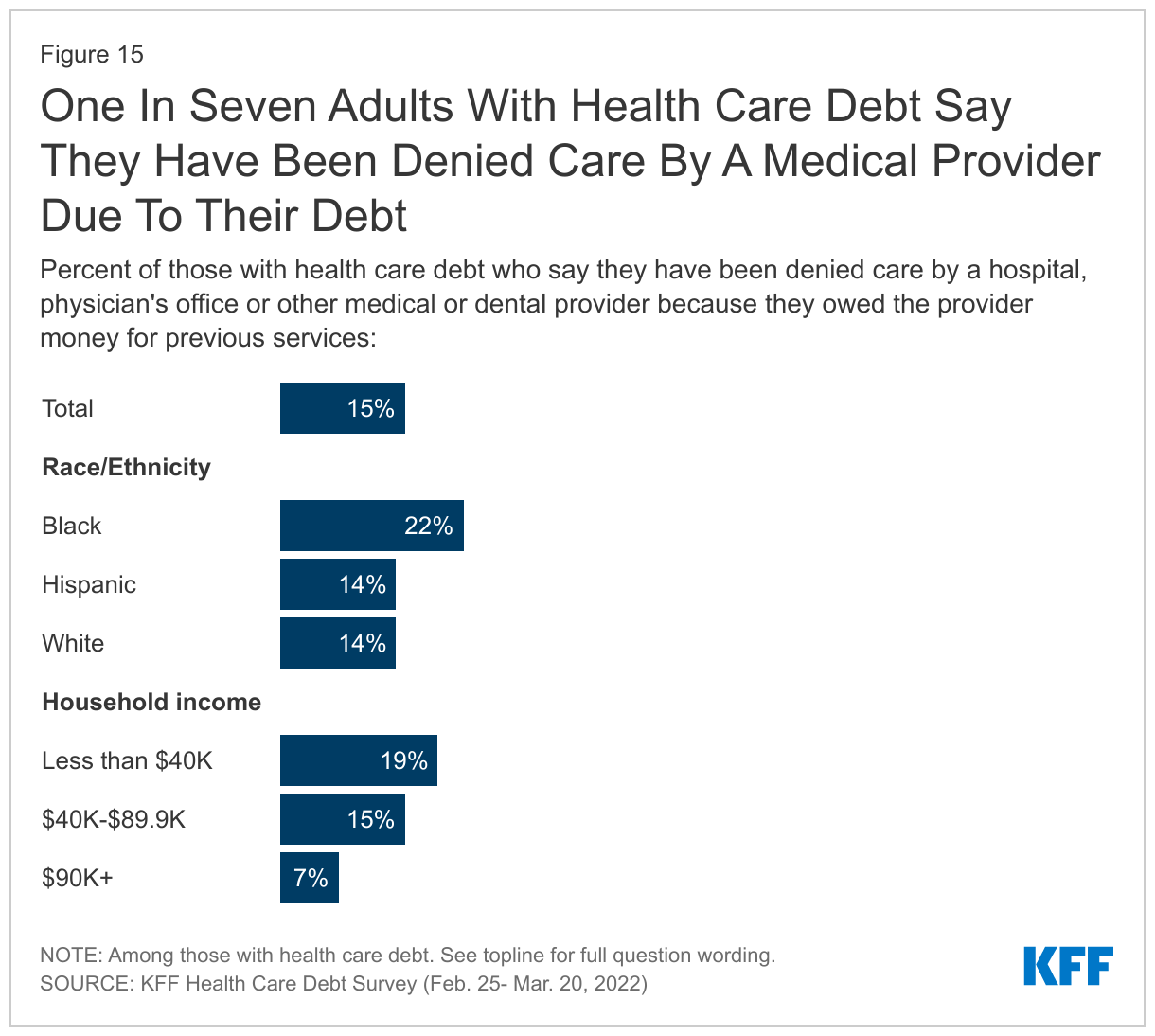

The consequences of health care debt are not limited to finances. For many, taking on health care debt can affect their ability to get future health care services or continue ongoing treatment. Fifteen percent of adults who currently have health care debt say they have been denied care by a hospital or other medical or dental provider because of their debt. Larger shares of Black adults with health care debt (22%) report this happening to them than their White (14%) or Hispanic (14%) counterparts. One in five (19%) adults with debt in households making less than $40,000 report being turned away from a medical provider, compared to 13% of those with higher household incomes.

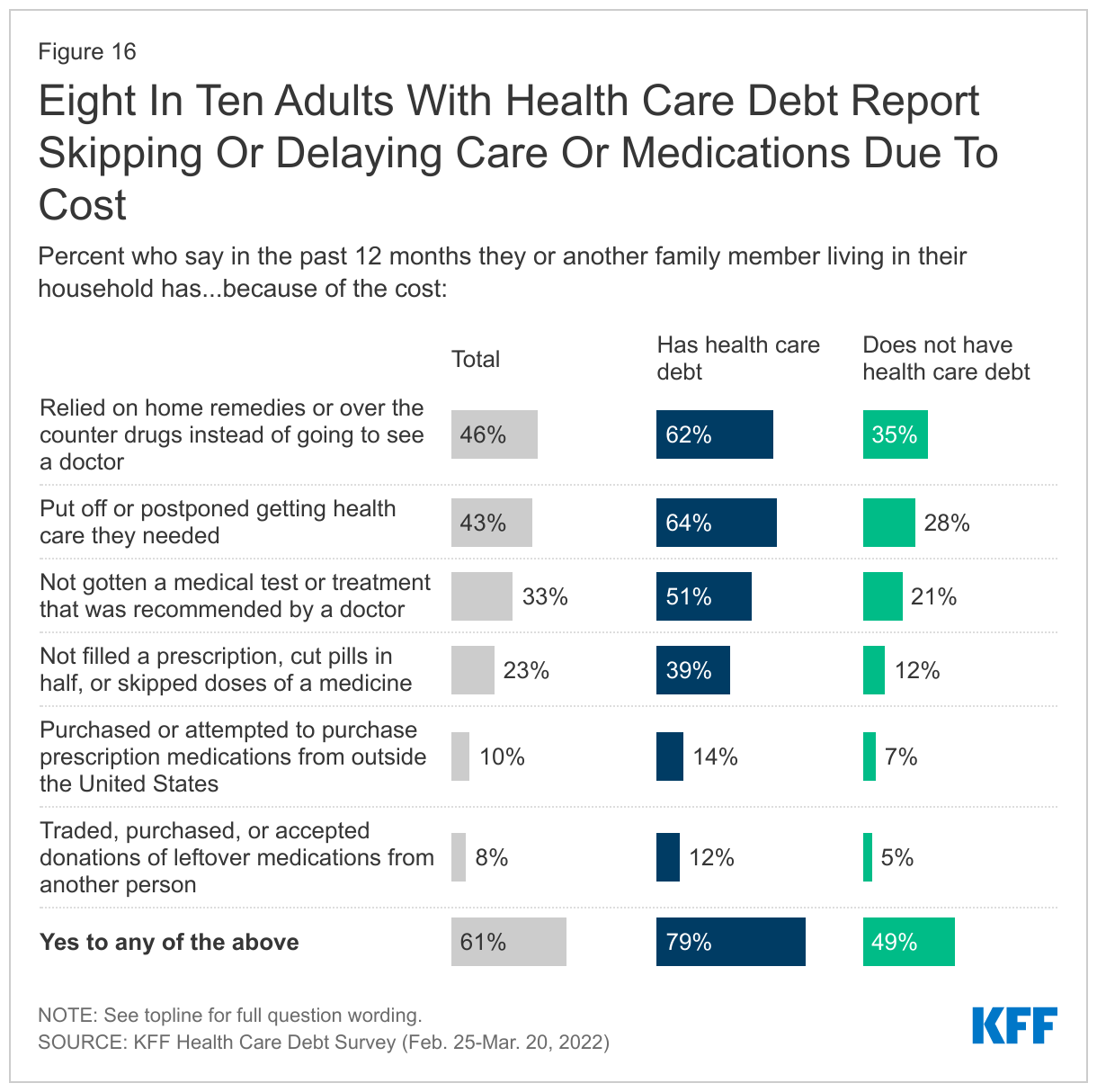

KFF polling has found that health care costs are a top concern for U.S. adults, and many—even those without debt—make decisions about whether to seek care based on how much it costs and whether they can afford it. This survey finds that those with health care debt are more likely to report delaying or skipping medical care due to costs, though significant shares of those without medical debt also say they or someone in their household has done these things as well. Adults with health care debt are more than twice as likely as those without debt to say they or someone in their family has put off health care they needed due to costs in the past 12 months (64% vs. 28%). Similarly, six in ten (62%) adults with health care debt, compared to about one-third (35%) of those without, say they have relied on home remedies or over-the-counter drugs in the last year instead of going to see a doctor due to costs. Adults with health care debt are also at least twice as likely as those without to say that in the past 12 months, because of the cost, they have skipped a medical test or treatment recommended by a doctor (51% vs. 21%), not filled a prescription, cut pills in half, or skipped doses of a medicine (39% vs. 12%), purchased or tried to purchase medications from outside the U.S. (14% vs. 7%), or obtained leftover medications that were prescribed to another person (12% vs. 5%).

Overall, about eight in ten (79%) of those with health care debt report taking at least one of these actions in the past 12 months because of the cost, compared to about half (49%) of those without health care debt.

When asked to describe the sacrifices they’ve made to pay down debt, many mention their reluctance to seek future medical or dental care for fear of incurring even greater bills.

In Their Own Words: How Health Care Debt Affects Access To Medical And Dental Care“

We left the hospital a day after my wife gave birth via caesarean because we couldn't afford to stay.” -37 year old man with $5,000-$10,000 in medical debt, Texas

“Have neglected personal preventive [health care] since I feel like I have no right to step into a hospital since I am unable to pay.” -36 year old woman with $1,000-$2,500 in medical debt, Washington

“The most difficult sacrifice due to medical debt is avoiding dental [care] to avoid incurring any more debt. I have 6 broken teeth that could have been saved at some point if I had dental coverage.” -50 year old woman with less than $500 in health care debt, Minnesota

“I have skipped picking up prescriptions or seeking treatment, so my bill doesn't continue to get higher. The prescriptions are really the problem.” -60 year old woman, $500-$1,000 in health care debt, New Mexico

“I'm currently sacrificing my teeth. Insurance won't cover root canals. Only teeth pulling. And it's still like $500!” -29 year old man, $2,500-$5,000 in health care debt, New York

“There is a permanent anxiety with calling a doctor's office and scheduling a visit because I never know beforehand how much it will cost. Then, out of the blue, I'll get slammed with a bill I can't pay.” -25 year old woman with $500-$1,000 in health care debt, Ohio

A Precarious Position: Vulnerability To Health Care Debt

In addition to the four in ten adults who say they currently owe money due to medical or dental bills, many more may be one large bill away from landing themselves in this position. A KFF analysis has found that even among those with health insurance, many do not have the savings to pay typical health plan deductibles.

Among those with current health care debt, it is not surprising that the large majority say that if they got an unexpected medical bill for $500, they would either have to incur further debt to pay it (45%) or would not be able to pay the bill at all (30%). However, even among those who do not currently have health care debt, about three in ten say they would have to borrow money in order to pay such a bill (20%) or would not be able to pay it at all (10%).

Public’s Views Of Policy Interventions To Address Or Assist Those With Health Care Debt

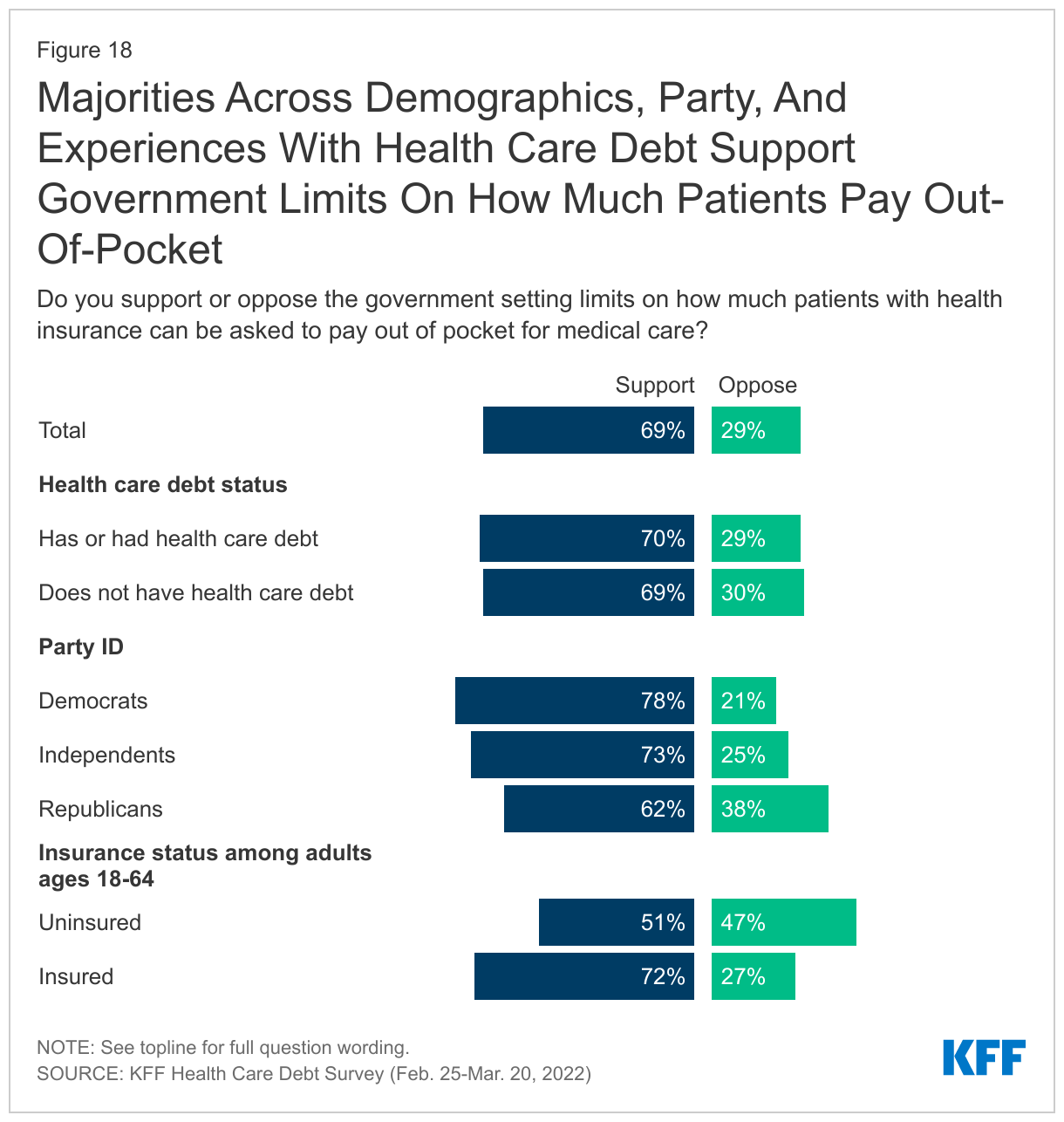

Given the relatively widespread nature of health care debt and the sizeable share of adults who would have to turn to debt to pay for a $500 unexpected medical bill, policies aimed at limiting costs for patients could potentially help individuals avoid health care debt. Majorities of both those who have and haven’t experienced health care debt say they support the government setting limits on how much patients with health insurance can be asked to pay out of pocket for medical care. While government regulation of health care is generally less popular among Republicans, majorities across partisans support such a proposal (though the share supporting among Democrats is 16 percentage points higher than among Republicans). Notably those who are insured and under age 65 (72%) are more likely to support this policy proposal than those who are uninsured (51%), likely because it would directly impact them.

It is worth noting that while overall support for this policy is high, the question on this survey did not ask individuals to consider any potential trade-offs related to the policy, such as higher health plan premiums or increased financial pressure of health care providers.

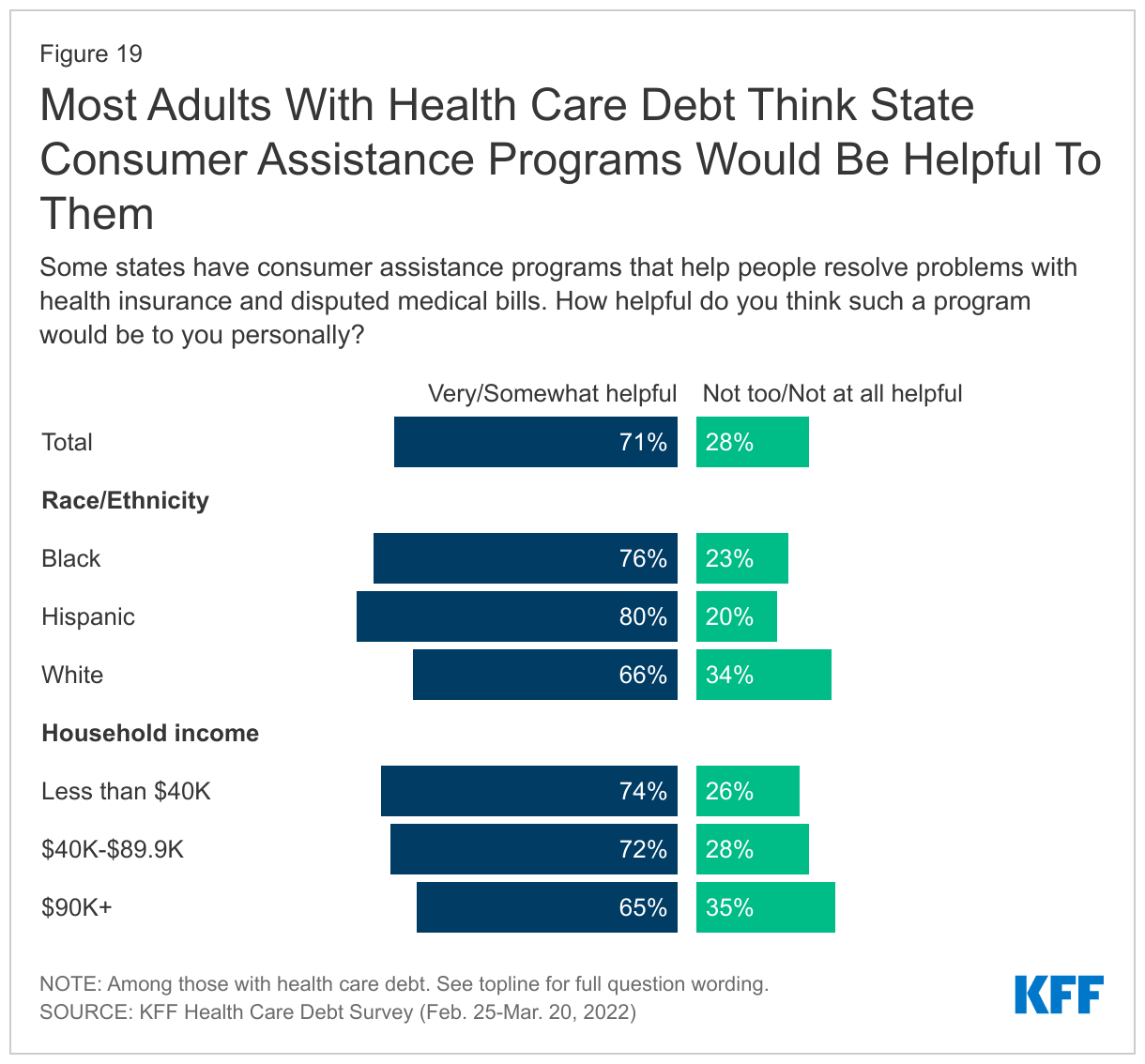

Consumer assistance programs have been established in many states to help individuals resolve issues with insurance providers and disputed medical bills, though no federal funding has been appropriated for these programs since 2010. With two-thirds of adults with health care debt reporting they have not paid a bill because they were expecting their insurance to pay it, it follows that many would welcome assistance in navigating disputes with insurance providers. Indeed, seven in ten adults with health care debt say they think a state consumer assistance program would be helpful to them personally. Black (76%) and Hispanic (80%) adults with debt are particularly likely to think these programs would be helpful to them compared to slightly fewer White adults (66%) who say the same. Moreover, majorities of adults with health care debt across income groups think consumer assistance programs would be helpful to them personally.

Appendix

Appendix

Below are studies and analyses with measures and estimates of medical debt from recent years, including some which utilize a more narrow definition of medical debt.

| Study | Question Wording / Analysis source | Finding | Dates |

| KFF Health Care Debt Survey | Please think about any money you currently owe or debt you have due to medical or dental bills. This may include bills for your own medical or dental care or someone else’s care, such as a child, spouse, or parent. Do you currently have: a. Any medical or dental bills that are past due or that you are unable to pay b. Any medical or dental bills you are paying off over time directly to a provider c. Any debt you owe to a bank, collection agency, or other lender that includes debt or loans used to pay medical or dental bills d. Any medical or dental bills you have put on a credit card, and you are paying off over time e. Any debt you owe to a family member or friend for money you borrowed to pay medical or dental bills | 41% of adults have health care debt due to medical or dental bills | February 25 – March 20, 2022 |

| Peterson-KFF: The burden of medical debt in the United States | Analysis of the 2020 Survey of Income and Program Participation (SIPP) Did ... have any medical bills he/she was unable to pay in full? Include bills for doctors, dentists, hospitals, therapists, medication, equipment, nursing home or home care. Include any bills of the respondent's children that have not already been reported. | 23 million people (nearly 1 in 10 adults) owe significant medical debt ($250 of more). The SIPP survey suggests people in the United States owe at least $195 billion in medical debt. | January– December, 2019 |

| Consumer Financial Protection Bureau | Analysis of consumer credit records | $88 billion in medical debt on consumer credit records | June 2021 |

| Commonwealth Fund Health Care Coverage and COVID-19 Survey | Adults who reported that over the prior 12 months they or a family member had problems paying medical bills, had been contacted by a collection agency about unpaid bills, had to change their way of life to pay their bills, or were paying off medical bills and debt over time. | 38% of adults reported problems paying bills, contact by collection, changing way of life or paying medical bills and debt over time | March 9 – June 8, 2021 |

| U.S. Census Bureau, Survey of Income and Program Participation, 2020 | Did ... have any medical bills he/she was unable to pay in full? Include bills for doctors, dentists, hospitals, therapists, medication, equipment, nursing home or home care. Include any bills of the respondent's children that have not already been reported. | 17% reported medical bills they were unable to pay in full | January-December, 2019 |

| 2019 Pew Research Center’s American Trends Panel – Wave 54 | Do you have any of the following types of loans or debt? Debt from medical bills | 29% yes, have debt from medical bills | Sep 16-29, 2019 |

| 2018 National Financial Capability Study | Do you currently have any unpaid bills from a health care or medical service provider (e.g., a hospital, a doctor’s office, or a testing lab) that are past due? | 23% reported past-due medical debt | June-October, 2018 |

Methodology

This KFF Health Care Debt Survey was designed and analyzed by public opinion researchers at the Kaiser Family Foundation (KFF) in collaboration with KHN journalists and editors. The survey was conducted February 25 through March 20, 2022 online and via telephone, in English and Spanish, among a nationally representative sample of 2,375 U.S. adults. The sample includes 1,674 adults with current or past health care debt and 698 adults who have not had health care debt in the past five years. The majority of respondents (n=2,146) were reached online through the SSRS Opinion Panel. The SSRS Opinion Panel is a nationally representative probability-based web panel recruited randomly in one of two ways: (a) Through invitations mailed to respondents randomly sampled from an Address-Based Sample (ABS). ABS respondents are randomly sampled through the U.S. Postal Service’s Computerized Delivery Sequence (CDS). (b) from a dual-frame random digit dial (RDD) sample, through the SSRS Omnibus survey platform. To ensure representation of respondents less likely to be reached online, 177 interviews were conducted from a random digit dial telephone sample of prepaid cell phone numbers. Both the RDD sample for the SSRS Omnibus and the prepaid cell phone numbers were obtained through Marketing System Groups (MSG).

The survey was designed to reach adults who currently have health care debt or have had health care debt in the last five years. In order to do this, the probability panel sample included an oversample of panel members with annual household incomes less than $30,000, individuals with current or past health care debt (n=641) were included in the sample. In addition, 52 adults with past or current health care debt were reached by calling back respondents that had previously completed an interview on the SSRS Omnibus poll (and other RDD polls) and reported an annual household income of less than $25,000.

The combined online and telephone samples, excluding oversamples, were weighted to match the sample’s demographics to the U.S. population using data from the Census Bureau’s 2021 Current Population Survey (CPS). On the basis of this weighted sample, parameters for the debt and no-debt populations were extracted. Weighting parameters for each group included sex, age, education, race/ethnicity, region, education, and income, as well as patterns of civic engagement from the September 2017 Volunteering and Civic Life Supplement data from the CPS. The sample was also weighted to match population density parameters from the Census Planning Database 2020. The weights take into account differences in the probability of selection for each sample type. This includes adjustment for the sample design and geographic stratification of the cell phone sample, within household probability of selection, and the design of the panel-recruitment procedure.

The margin of sampling error including the design effect for the full sample is plus or minus 3 percentage points. Numbers of respondents and margins of sampling error for key subgroups are shown in the table below. For results based on other subgroups, the margin of sampling error may be higher. Sample sizes and margins of sampling error for other subgroups are available by request. Sampling error is only one of many potential sources of error and there may be other unmeasured error in this or any other public opinion poll. Kaiser Family Foundation public opinion and survey research is a charter member of the Transparency Initiative of the American Association for Public Opinion Research.

| Group | N (unweighted) | M.O.S.E. |

| Total | 2,375 | ± 3 percentage points |

| Health Care Debt Status | ||

| NET: Current or past health care debt | 1,674 | ± 3 percentage points |

| Current health care debt | 1,292 | ± 3 percentage points |

| Past health care debt | 382 | ± 6 percentage points |

| No health care debt | 698 | ± 5 percentage points |

Endnotes

- Since adults with health care debt may carry that debt burden over a number of years, the survey asked adults to recall any health care debt they may have had in the past five years. Recall of health care debt was limited to a five-year time horizon as it may be difficult for people to accurately remember specifics about the type and origin of any debts incurred prior. ↩︎