Medicare Advantage Has Become More Popular Among the Shrinking Share of Employers That Offer Retiree Health Benefits

Employer and union-sponsored retiree health plans play an important role in providing supplemental benefits to about a quarter (24%) of all people with Medicare or 14.5 million Medicare beneficiaries. However, the share of employers offering retiree health benefits has been shrinking. Among large employers that offer health benefits to active workers, the share offering retiree health benefits has dropped from 66% in 1988 to 24% in 2024, according to the latest KFF Employer Health Benefits Survey. And among large firms offering health benefits to active workers and retirees, 64 percent offer retiree health benefits to Medicare-age retirees in 2024. Among the declining share of large firms that offer retiree health benefits to Medicare-age retirees, Medicare Advantage has become more popular.

This analysis examines the extent to which large private and non-federal public employers that offer retiree health benefits are turning to Medicare Advantage, using data from the 2024 KFF Employer Health Benefits Survey (see methods).

Highlights:

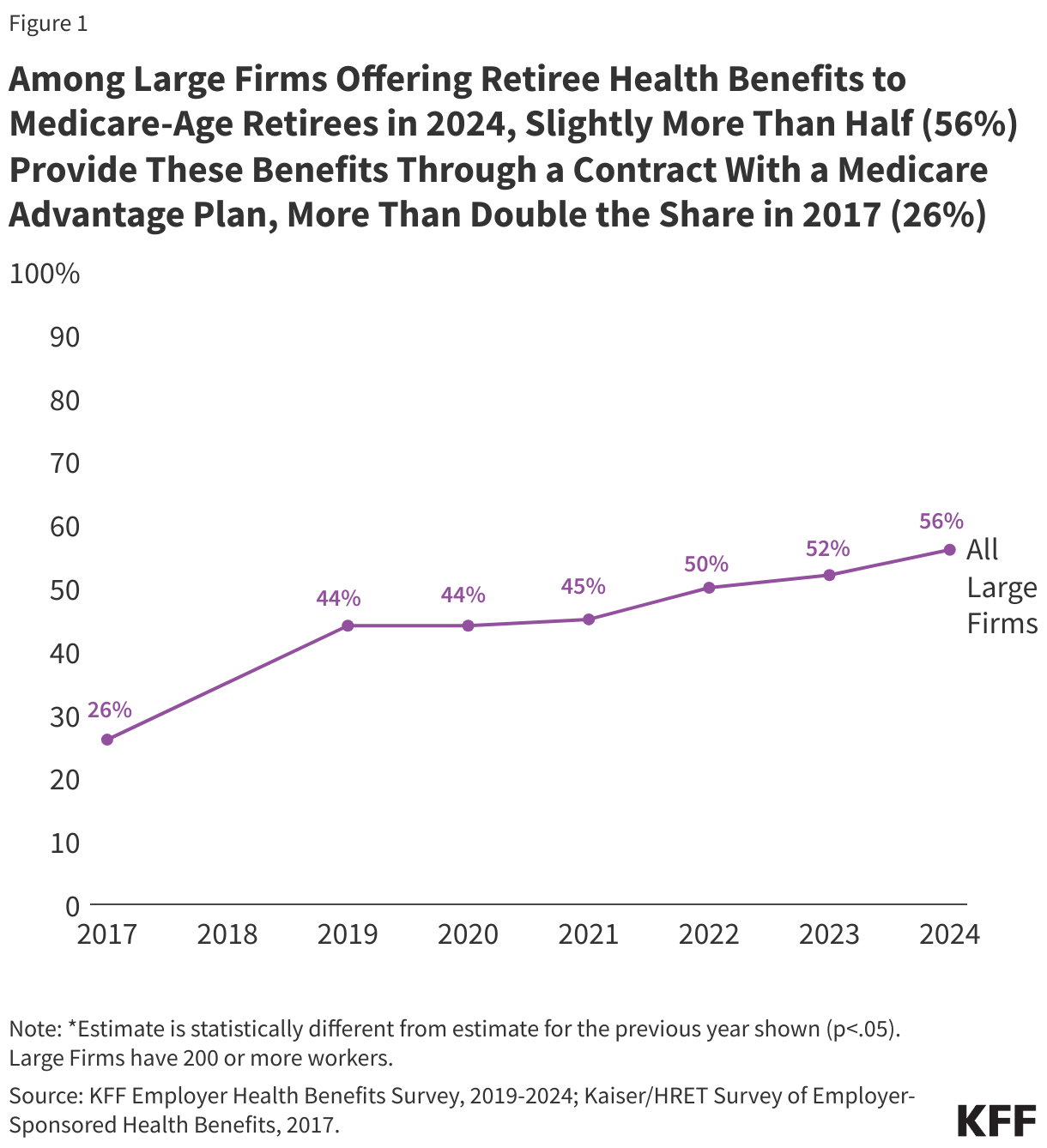

- Slightly more than half (56%) of large employers offering retiree health benefits to Medicare-age retirees in 2024 offer coverage to at least some retirees through a Medicare Advantage plan, more than double the share in 2017 (26%).

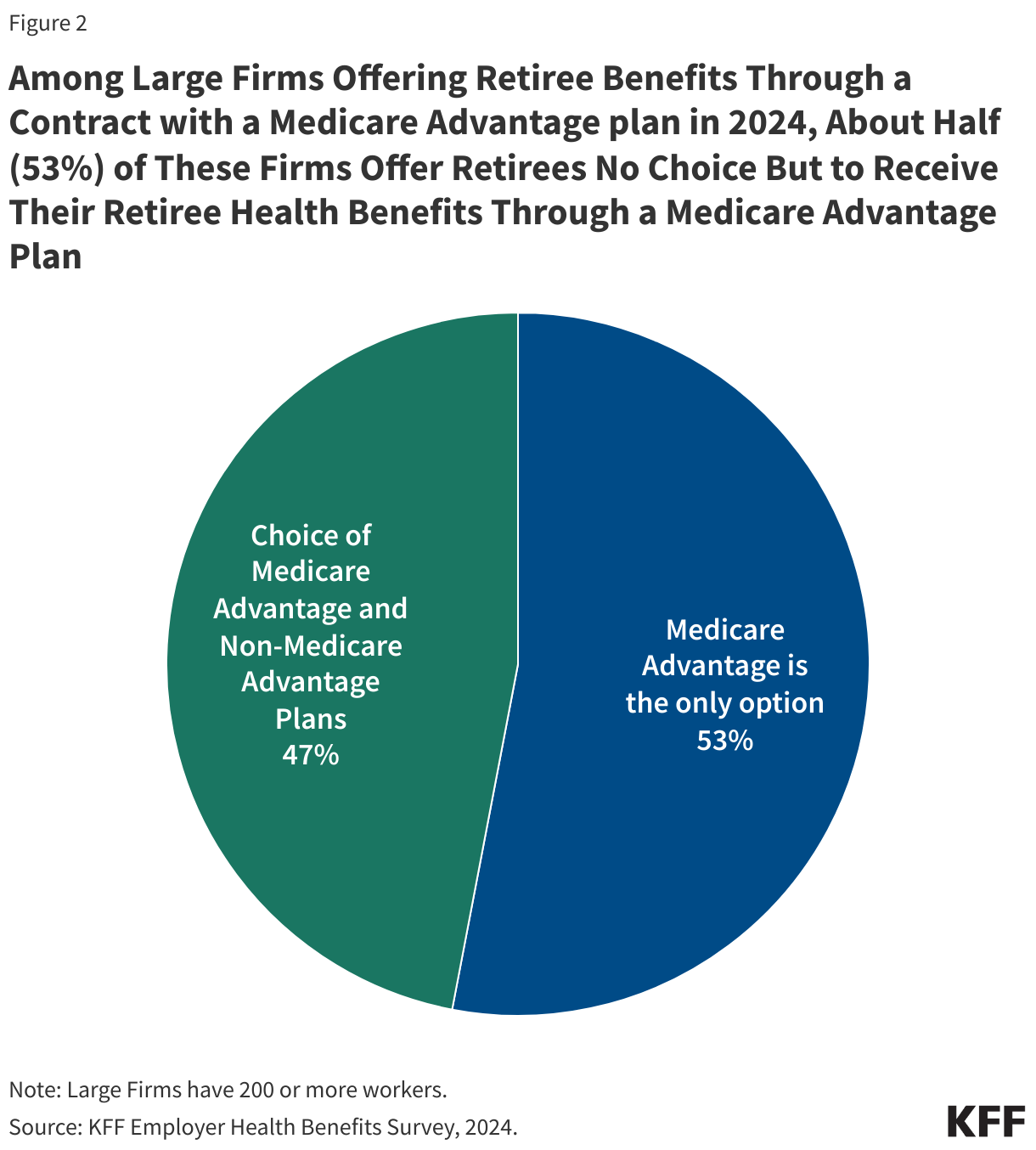

- About half of large employers (53%) that offer Medicare Advantage coverage to their retirees in 2024 do not give retirees a choice in coverage options.

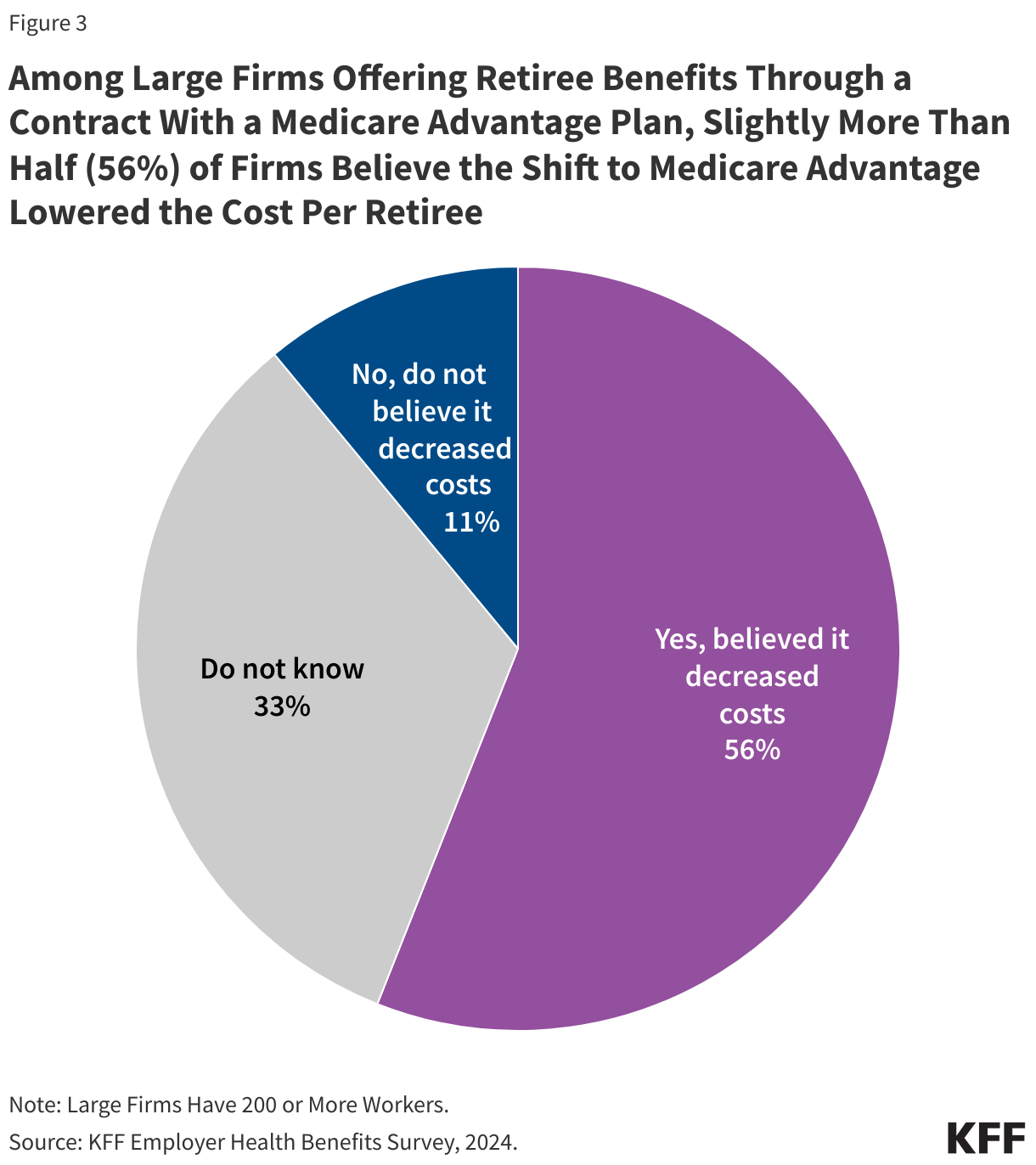

- Slightly more than half (56%) of large employers offering retiree benefits through a Medicare Advantage plan believe the shift to Medicare Advantage lowered the cost per retiree.

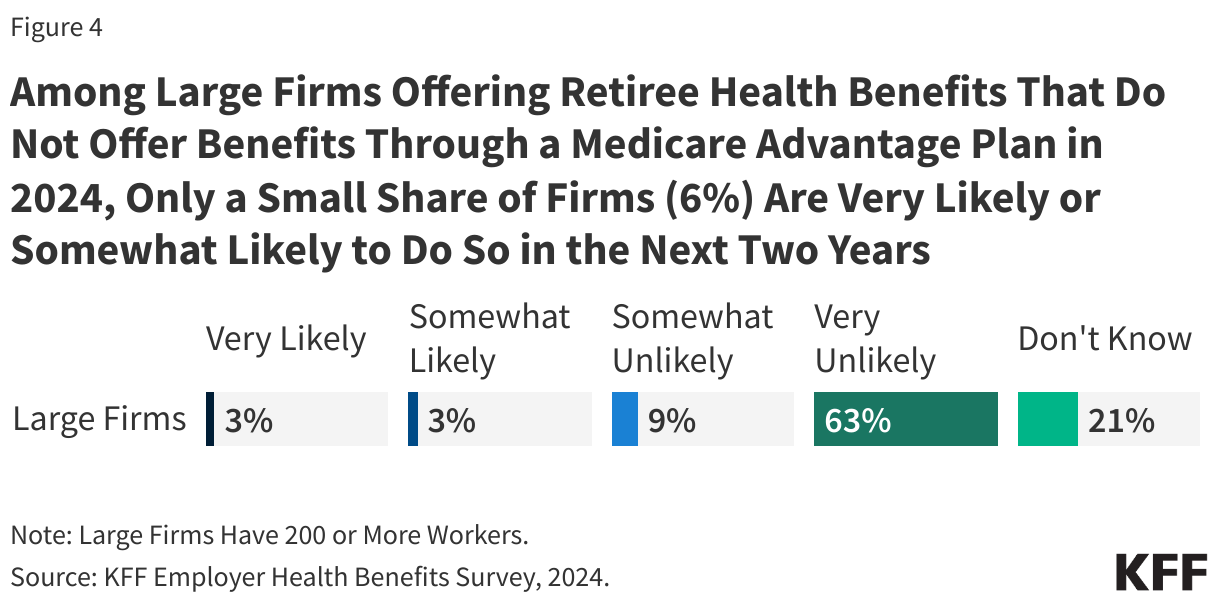

- Among large firms that offer retiree health benefits but do not offer benefits through a Medicare Advantage plan in 2024, 6% are very likely or somewhat likely to do so in the next two years.

Employer or union-sponsored retiree health benefits cover some or all of Medicare’s cost-sharing requirements and may provide supplemental benefits that are not covered by traditional Medicare. Until fairly recently, employer and union-sponsored retiree health benefits were typically designed to coordinate or wrap around traditional Medicare.

Concerns about retiree health benefit costs have led employers and unions to implement a variety of changes to limit their financial obligations, such as imposing caps on their retiree health liability, shifting toward defined contribution approaches, increasing retirees’ premium contribution, and more recently, by offering their Medicare-eligible retirees coverage through Medicare Advantage plans. Medicare Advantage plans, mainly HMOs and PPOs, provide all Medicare-covered benefits, typically include Part D drug coverage, and often include supplemental benefits such as lower cost sharing and vision, dental, and hearing benefits. Medicare Advantage enrollees continue to pay the Medicare Part B premium, but often pay no additional premium for covered benefits.

Unlike other Medicare Advantage plans, employer plans are not required to provide detailed information about their benefit design, including supplemental benefits. Therefore, it is not possible to assess how benefits and cost sharing compare for those enrolled in a group plan versus those enrolled in a plan that is generally available for individual purchase or a special needs plan. While group enrollment as a share of total Medicare Advantage enrollment has fluctuated between 17% to 20% since 2010, the actual number of group enrollees has increased from 1.8 million in 2010 to 5.7 million in 2024 as Medicare Advantage enrollment overall has grown.

Under this approach, employers and unions contract with a Medicare Advantage private insurer to provide all Medicare-covered benefits as well as any supplemental benefits for their Medicare-eligible retirees (and spouses). The employer (or union) and/or private insurer (acting on behalf of an employer) receives a payment from the federal government (Medicare) and agrees to cover all Medicare-covered benefits, along with a package of supplemental benefits for retirees in their group. Payments are based on the bids of other Medicare Advantage plans available to individual (non-group) enrollees, and set as a percentage of the area benchmark, adjusted for geography and risk. Employer plans are eligible to receive rebates and bonus payments from Medicare, both of which help cover the costs associated with supplemental benefits for their retirees and contribute to the growth in Medicare spending. Bonus payments for group Medicare Advantage plans accounted for $2.6 billion in spending in 2024.

Slightly more than half (56%) of all large firms (firms with 200 or more workers) that offer retiree health benefits to Medicare-age retirees do so through a Medicare Advantage plan in 2024, more than double the share in 2017 (26%) (Figure 1).

For retirees, the shift to Medicare Advantage can mean similar or better benefits and lower costs but can also mean more limited access to doctors and hospitals in the plan’s network and greater exposure to cost management tools, such as prior authorization, that may limit access to Medicare-covered services. These limitations are, in part, why public sector retirees in New York City sued to stop being moved to a Medicare Advantage plan in 2022 and may explain why a Manhattan Supreme Court Judge prohibited the implementation of this plan.

Among large firms (200 or more workers) offering retiree benefits through a contract with a Medicare Advantage plan, about half (53%) provide at least some retirees no choice but to receive their retiree health benefits through a Medicare Advantage plan in 2024 (Figure 2).

Retirees in firms that offer health benefits exclusively through Medicare Advantage plans have the option to enroll in traditional Medicare, but if they do, they may be required to give up retiree benefits in perpetuity. They may or may not be able to purchase a Medigap policy to supplement traditional Medicare, depending on their health condition, since most states do not have guaranteed issue protections for Medigap.

Among large firms (200 or more workers) offering retiree benefits through a contract with a Medicare Advantage plans, 56% believe that the shift to offering Medicare Advantage plans lowered their per retiree costs.

Further, 11% of large firms said the shift to Medicare Advantage plans did not lower their per retiree costs, while 33% did not know the answer.

More than half of all large employers offering Medicare Advantage to their retirees say the shift to Medicare Advantage plans lowered their per retiree costs, which may be a strategy to maintain benefits for their retirees, rather than terminate or scale back coverage. For example, in 2022, the state of Connecticut estimated the state would save $400 million over the following three years by switching retirees to a different Medicare Advantage administrator. Similarly, in 2023, New York City estimated that it would save $600 million annually by switching its city retirees to Medicare Advantage.

However, the rising number of Medicare-eligible retirees into Medicare Advantage plans has implications for Medicare spending because Medicare pays more for enrollees in Medicare Advantage plans (including for group plans) than it pays for similar people in traditional Medicare, which contributes to higher Medicare spending that ultimately affects the solvency of the Medicare Trust Fund and higher Medicare premiums paid by all beneficiaries, raising questions as to whether employers are limiting their liability for retiree health benefits at the expense of the Medicare program.

Among large firms (200 or more workers) offering retiree health benefits but do not offer benefits through a Medicare Advantage plan in 2024, 6% are very likely or somewhat likely to do so in the next two years.

In contrast, 73% of firms say they were somewhat unlikely or very unlikely to offer retiree benefits through a Medicare Advantage plan in the next two years, while 21% of firms said they do not know whether they are likely to do so.

This work was supported in part by Arnold Ventures. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

Methods

This analysis uses data from the KFF 2024 Employer Health Benefits Survey, published in October 2024 and fielded from January to July 2024. This survey asks retiree health benefits questions only of large firms offering health benefits to active worker (200 or more workers). The survey does not include information about union-administered benefits. For additional information, see Survey Designs and Methods.