Medicare Advantage Enrollment, Plan Availability and Premiums in Rural Areas

Medicare Advantage enrollment has grown rapidly in recent years, and in 2023, more than half (51%) of all eligible Medicare beneficiaries are in a Medicare Advantage plan. Most Medicare Advantage enrollees, and most Medicare beneficiaries, live in metropolitan areas. To understand the role of Medicare Advantage in rural areas, this analysis examines trends in enrollment, plan availability and premiums in less populated counties.

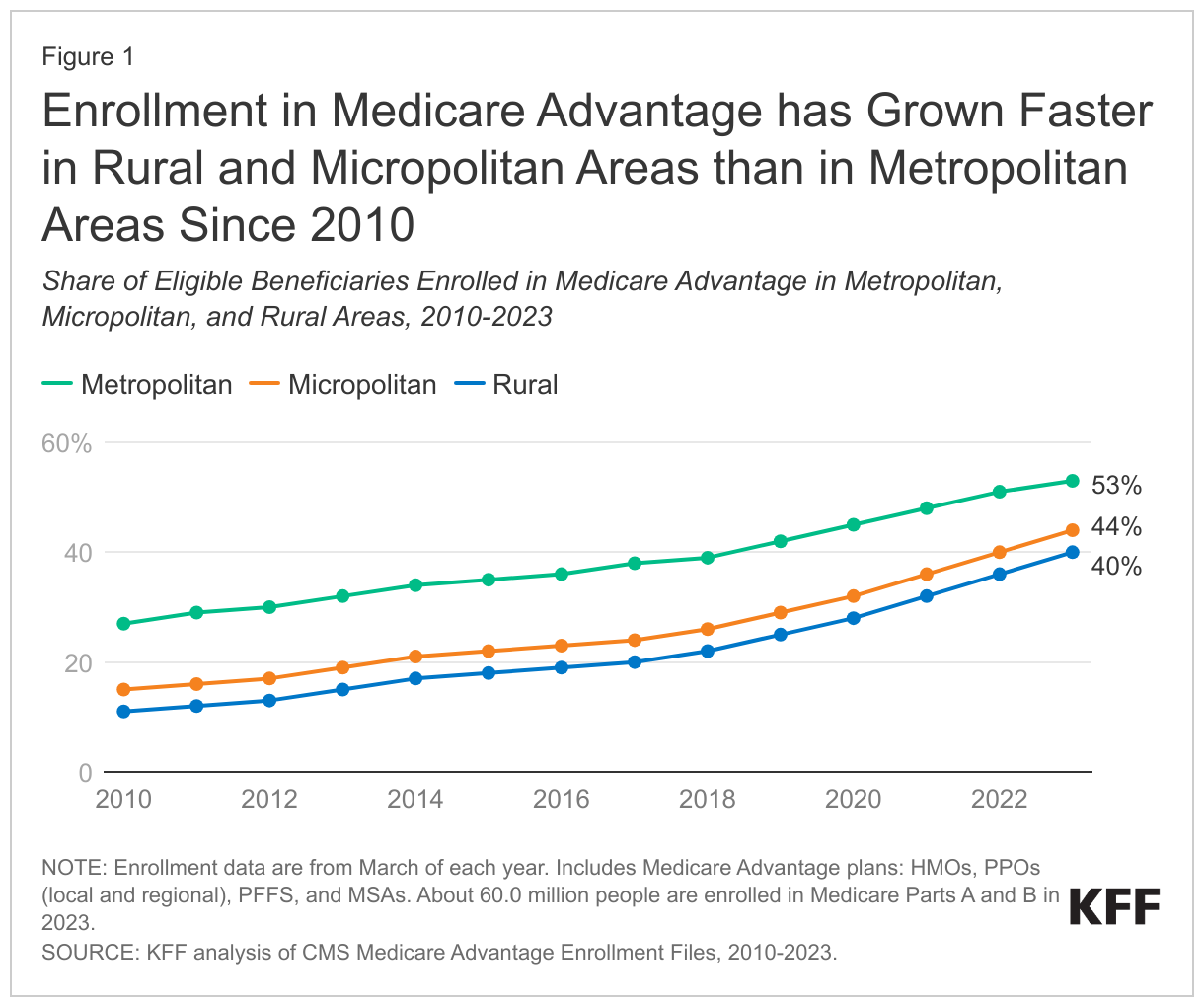

Medicare Advantage enrollment is lower, but has grown more rapidly in recent years in rural areas than in metropolitan areas. In 2023, 40% of all eligible Medicare beneficiaries in rural counties are enrolled in a Medicare Advantage plan, nearly four times the share in 2010 (11%). Rural Medicare Advantage enrollees can choose from among 27 plans, on average, which is triple the number of plans available just five years ago. In rural counties, like all areas, most Medicare Advantage enrollees are in a plan that charges no additional premium, other than the Part B premium.

Medicare Advantage in Rural Areas

Medicare Advantage enrollment has quadrupled in rural areas since 2010 and reached 40% in 2023.

In 2023, a smaller share (40%) of Medicare beneficiaries in rural areas – counties with less than 10,000 people – are enrolled in a Medicare Advantage plan than Medicare beneficiaries in micropolitan (10,000 to 50,000 people) or metropolitan (at least 50,000 people) areas (44% and 53%, respectively). Though Medicare Advantage enrollment is lowest in rural areas, it has grown more rapidly in these counties, nearly quadrupling from 11% of eligible Medicare beneficiaries in 2010 to 40% in 2023. Over the same period, the share of Medicare beneficiaries enrolled in a Medicare Advantage plan in micropolitan areas nearly tripled (from 15% to 44%), and nearly doubled in metropolitan areas (from 27% to 53%).

In 2023, more than 1.8 million Medicare beneficiaries in rural areas are enrolled in a Medicare Advantage plan, more than four times the number enrolled in 2010 (400,000). In metropolitan areas, enrollment increased from 9.7 million in 2010 to 26.3 million in 2023 and in micropolitan areas, enrollment rose from nearly 700,000 in 2010 to 2.6 million in 2023 (Appendix Table 1). The growth in enrollment translates into an average annual increase of 12% in rural areas and 11% in micropolitan areas, compared with 8% in metropolitan areas between 2010 and 2023.

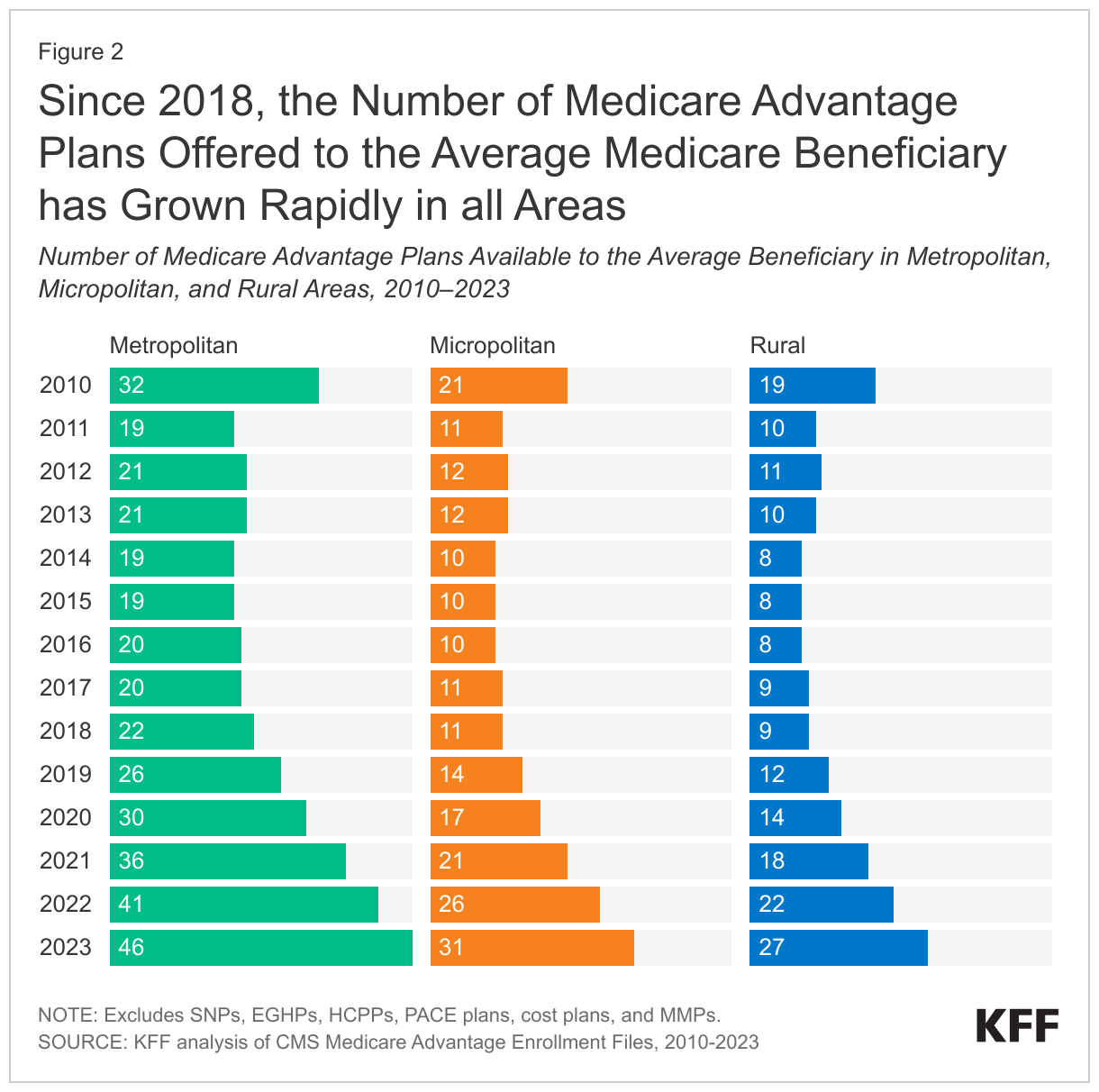

The average Medicare beneficiary living in a rural county can choose among 27 Medicare Advantage plans, triple the number of plans offered five years ago.

Across all areas, the number of Medicare Advantage plans available to the average Medicare beneficiary have risen steadily since 2018, after holding relatively constant in earlier years. In 2023, the average Medicare beneficiary in a rural area has 27 Medicare Advantage plans to choose from, which is three times more than the number of plans available in 2018 (9 plans). This is similar to the growth in micropolitan areas, where the average Medicare beneficiary has access to 31 plans in 2023, compared to 11 plans in 2018. In contrast, the average Medicare beneficiary in a metropolitan area can choose from substantially more plans - 46 in 2023, just over double the number in 2018 (22 plans) (Figure 2).

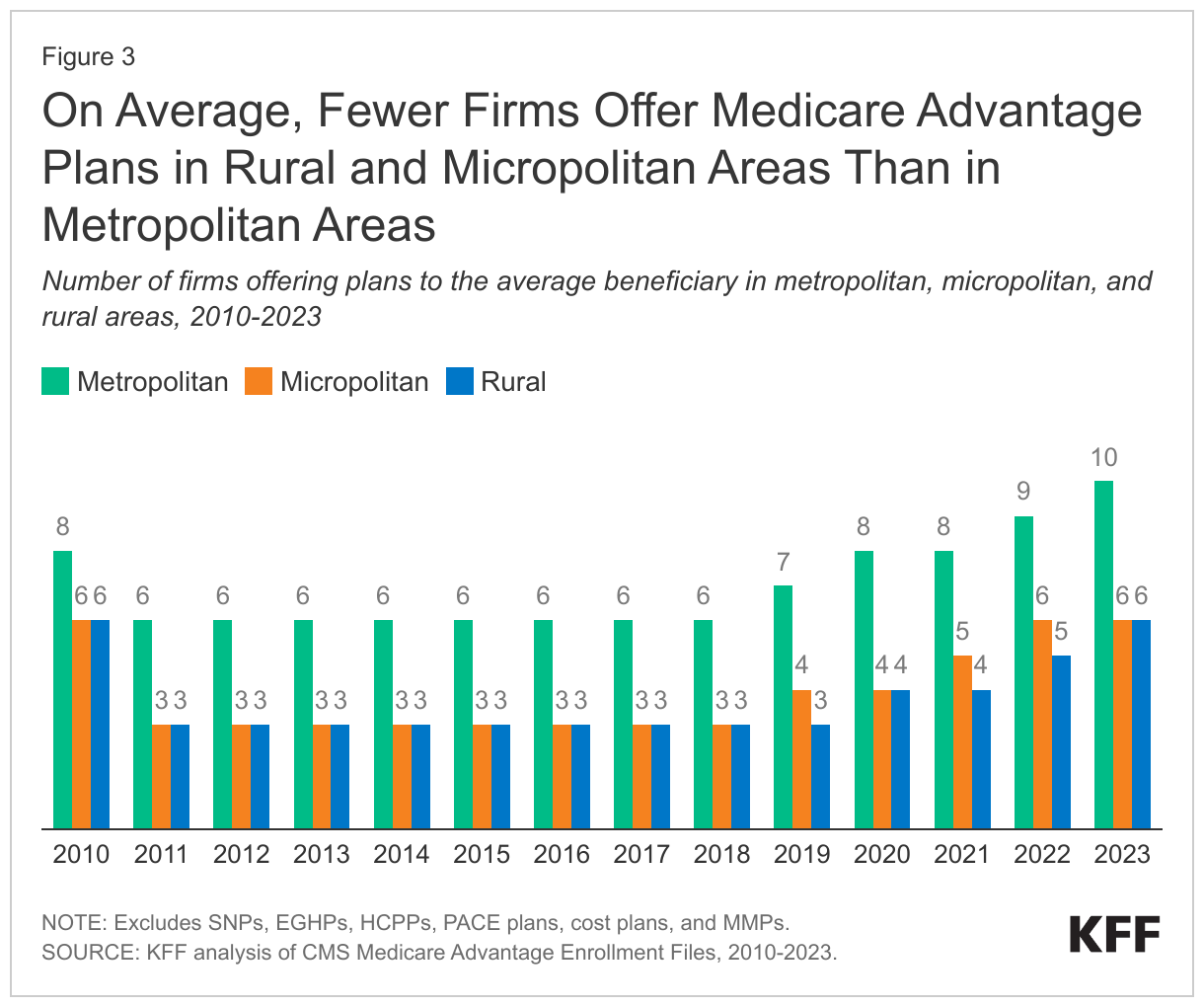

In 2023, the average Medicare beneficiary living in a rural area can choose among Medicare Advantage plans offered by six firms, twice the number of firms offering plans in these counties in 2018.

Since 2018, the average number of firms offering Medicare Advantage plans has increased in all areas. The average Medicare beneficiary in a rural area can choose from plans offered by six firms in 2023, which is double the number of firms offering plans in these areas in 2018 (3 firms). The trend in the number of firms offering plans in micropolitan areas is similar, rising from three in 2018 to six in 2023. The number of firms offering plans has been consistently higher in metropolitan areas than in other geographic areas, rising from six firms in 2018 to ten firms in 2023 (Figure 3).

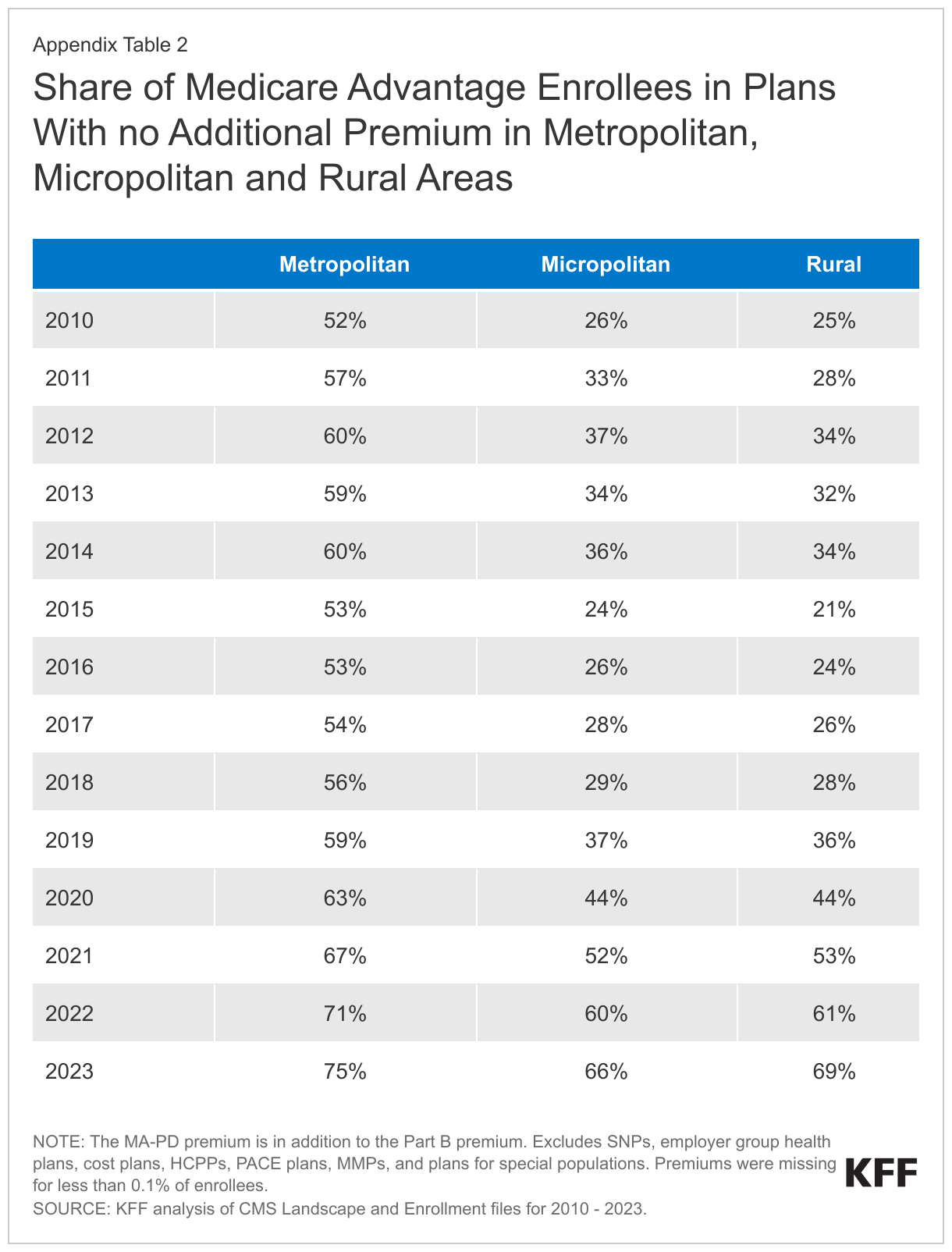

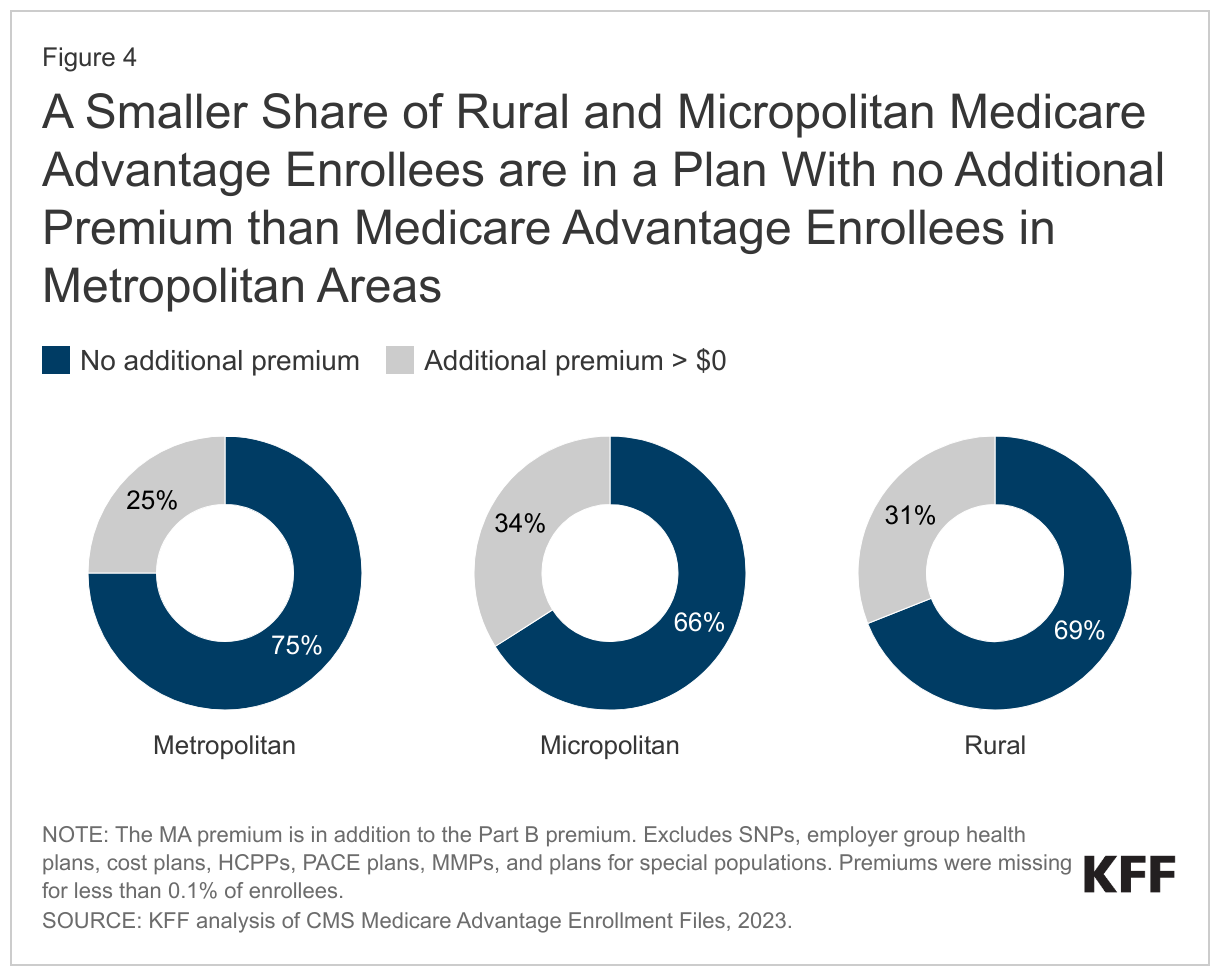

More than two-thirds (69%) of Medicare Advantage enrollees in rural areas are in a plan that requires no premium other than the Part B premium.

A somewhat smaller share of enrollees in rural (69%) and micropolitan (66%) counties pay no additional premium compared with enrollees in metropolitan areas (75%) (Figure 4). Medicare Advantage plans may impose a premium for the cost of Medicare-covered services above payments made by the federal government to the plans, as well as the cost of prescription drug coverage. Most Medicare Advantage plans offer extra benefits for no additional premium.

Since 2015, the share of Medicare Advantage enrollees in plans with no additional premium has increased steadily in all areas. Growth has been fastest in rural areas where the share of enrollees in plans with no additional premium increased from 21% in 2015 to 69% in 2023. Growth has been similarly rapid in micropolitan areas, rising from 24% in 2015 to 66% in 2023. In metropolitan areas, the share of enrollees in plans with no additional premium has been consistently higher than in rural or micropolitan areas, but has increased more slowly, rising from 53% in 2015 to 75% in 2023 (Appendix Table 2).

Discussion

Medicare Advantage enrollment and plan availability in rural areas have increased rapidly in recent years, as they have in more populated counties. Private plans often provide supplemental benefits to enrollees for no additional premium (other than the Part B premium), including some coverage of dental, vision, and hearing services, as well as reduced cost sharing compared to traditional Medicare without a supplemental plan. At the same time, Medicare Advantage plans may use provider networks, limiting coverage of services delivered by out-of-network providers. Provider networks may impose barriers to people living in rural areas who already face challenges obtaining health care services because of fewer providers and longer travel distances. Despite recent growth, Medicare Advantage enrollment in rural areas remains lower than enrollment in more populated areas. This could be the result of fewer investments in marketing and outreach in these areas by Medicare Advantage insurers, because financial returns are lower given the smaller population of potential enrollees. As Medicare Advantage enrollment continues to grow, understanding how plans differ across metropolitan, micropolitan and rural areas will be increasingly relevant to assessing how well private plans meet the needs of their enrollees.

Jeannie Fuglesten Biniek and Tricia Neuman are with KFF. Gabrielle Clerveau was with KFF at the time this brief was written. Anthony Damico is an independent consultant.

Appendix