Operating Margins Among the Largest For-Profit Health Systems Have Exceeded 2019 Levels for the Majority of the COVID-19 Pandemic

Recent reports have raised concerns about the financial stability of hospitals amidst disruptions caused by the COVID-19 pandemic and the looming prospect of an economic recession. Large amounts of government relief helped prop up hospital margins in 2020 and 2021. However, industry reports suggest that the outlook for hospitals and health systems has deteriorated in 2022 due to the ongoing effects of the pandemic (such as labor shortages), decreases in government relief, and broader economic trends that have led to rising prices and investment losses. According to at least one account, 2022 may be the worst financial year for hospitals in decades. These challenges could force hospitals to take steps to increase efficiency but may also result in price increases or cost-cutting measures that impair patient access or care quality. Against this backdrop, industry stakeholders have asked Congress to provide additional fiscal relief to hospitals and to stop scheduled Medicare payment reductions.

To provide context for these policy discussions, we evaluated the financial performance of the three largest for-profit health systems in the country—HCA Healthcare (“HCA”), Tenet Healthcare Corporation (“Tenet”), and Community Health Systems (CHS)—which collectively accounted for about 8 percent of community hospital beds in the US in 2020.1 These three systems are publicly traded, meaning that we were able to acquire timely financial data about these systems through their reports to the Securities and Exchange Commission (SEC), as well as data on their stock prices (see Methods for additional details).

Results

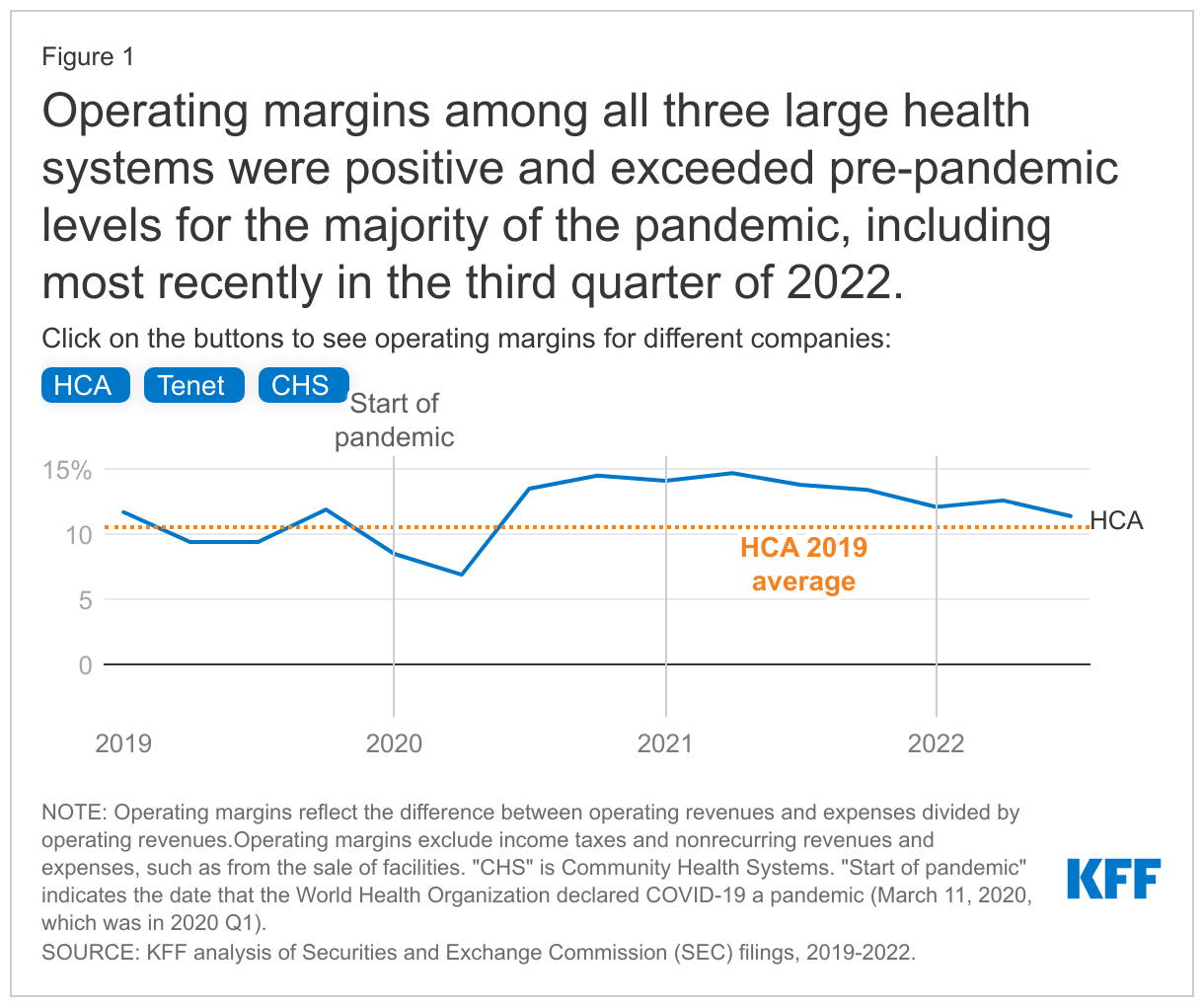

Operating margins among all three large health systems were positive and exceeded pre-pandemic levels for the majority of the pandemic, including most recently in the third quarter of 2022. Operating margins reflect the profit margins earned on patient care and other operations of a given health system—such as from gift shops, parking, and cafeterias—and incorporate government COVID-19 relief funds.2 Our definition of operating margins excludes income taxes and nonrecurring revenues and expenses, such as from the sale of facilities. HCA and Tenet had positive operating margins throughout the pandemic, and CHS had positive operating margins in all but two quarters of the pandemic (with one of those quarters being at the very beginning of the pandemic). HCA has had operating margins of at least 10 percent during the majority of the pandemic (9 out of 11 quarters). In other words, HCA’s revenue from patient care and other operations exceeded operating expenses by at least 10 percent for most of the pandemic. Tenet has had operating margins of at least 5 percent for the majority of the pandemic (9 out of 11 quarters), while CHS’s operating margins have been lower (less than 5% for 9 out of 11 quarters). CHS had lower margins than the other systems before the pandemic as well.

For all three systems, operating margins have exceeded pre-pandemic (2019) levels for most of the pandemic (9 out of 11 quarters), including the last quarter of our analysis (the third quarter of 2022), despite recent decreases in operating margins. HCA and Tenet dipped below their 2019 operating margins during two quarters of 2020, and CHS fell below their 2019 operating margins during the first quarter of 2020 and the second quarter of 2022 before increasing again. As of the third quarter of 2022, operating margins were 11.4 percent for HCA, 8.4 percent for Tenet, and 1.2 percent for CHS.

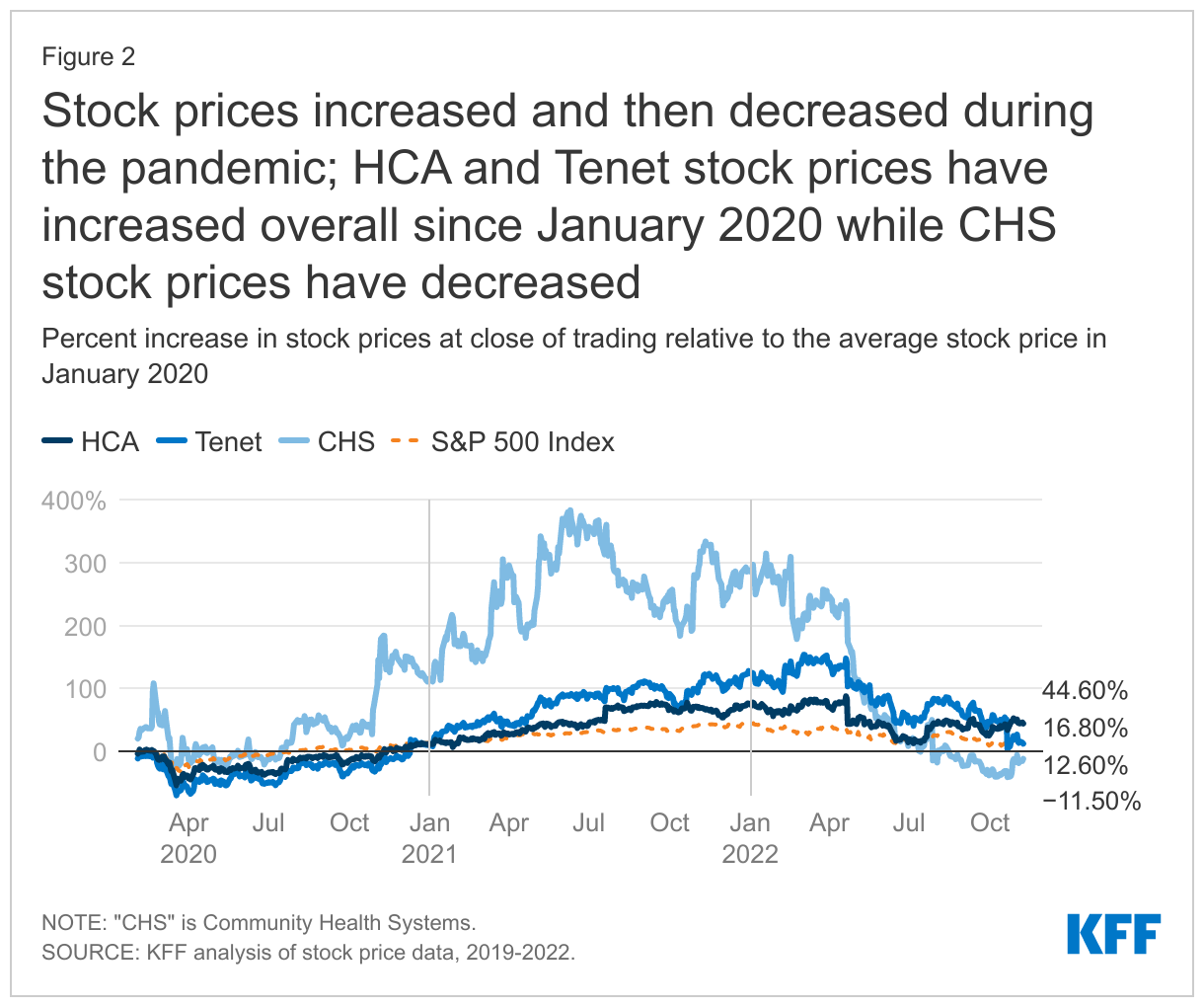

Stock prices increased and then decreased during the pandemic; HCA and Tenet stock prices have increased overall since January 2020 while CHS stock prices have decreased. Stock prices generally reflect investors’ evaluation of the future earnings potential of a given company. Stock prices increased dramatically during the first 1.5 to 2 years of the pandemic. At their heights, HCA stock prices had increased by 87.9 percent, Tenet stock prices had increased by 153.8 percent, and CHS stock prices had increased by 383.1 percent relative to January 2020.

Stock prices have also decreased substantially in 2022—in line with broader economic trends—and especially so among Tenet and CHS. As of November 8, 2022, HCA and Tenet stock prices have increased overall relative to January 2020 (by 44.6% and 12.6%, respectively).3 CHS stock prices have decreased by 11.5% since January 2020, though CHS has also experienced longstanding financial challenges that predate the pandemic. For purposes of comparison, HCA stock prices increased by a much greater amount than the S&P 500 during this period (44.6% versus 16.8%), while the S&P 500 slightly outperformed Tenet stock (16.8% versus 12.6%) and significantly outperformed CHS stock (16.8% versus -11.5%).

As of December 2, 2022, the majority of market analysts followed by MarketWatch were bullish on HCA and Tenet stock (with 18 buy, 3 overweight, and 5 hold recommendations for HCA stock and 14 buy, 2 overweight, and 4 hold recommendations for Tenet stock) and neutral about CHS stock (with 8 hold and 4 buy recommendations); none of the analysts rated these stocks as “sell” or “underweight.”

Discussion

Industry reports have suggested that hospitals had high margins in 2020 and 2021 but have faced significant financial challenges in 2022. Our analysis adds nuance to this discussion. So far this year, operating margins among the three largest for-profit health systems in the country have met or exceeded pre-pandemic levels. HCA and Tenet in particular have had high operating margins. CHS had negative operating margins in the second quarter of 2022, and its stock prices decreased overall from January 2020 to November 2022, but its financial challenges precede the pandemic. While some hospitals are struggling in the current environment—with high inflation and the ongoing burdens posed by COVID-19, flu, and respiratory syncytial virus (RSV)—our results indicate that the largest for-profit systems have had operating margins that exceed pre-pandemic levels.

Methods

We obtained financial data from each health system’s filings with the Securities and Exchange Commission (SEC). We relied on unaudited quarterly 10-Q filings for the first three quarters of a given calendar year. For the fourth quarter of a given calendar year, we subtracted the sum of the first three quarters from the annual value reported in audited 10-K filings. Health systems tend to provide conservative estimates of their financial performance in unaudited quarterly filings, meaning that our data on operating margins may be biased downwards for the first three quarters of a given year and upwards for the fourth quarter (which we obtain by subtracting unaudited quarterly values from audited annual values). Operating margins reflect the difference between operating revenues and expenses (also known as “net operating income”) divided by operating revenues. Our definition of operating margins excludes income taxes and nonrecurring revenues and expenses, such as from the sale of facilities. Our definition includes, among other things, equity in the earnings of affiliated businesses, such as ambulatory surgical centers, in which the system has a large but noncontrolling stake. It also incorporates government COVID-19 relief funds. The receipt and repayment of loans—such as through the Medicare Accelerated and Advance Payment Programs—do not factor into the determination of operating margins.

Each health system in our study used a unique approach for reporting revenues and expenses, which therefore required adding and subtracting different lines when calculating operating margins. Additional details are available upon request.

This work was supported in part by Arnold Ventures. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

Nancy Kane, an independent consultant, reviewed the methodology for this analysis.

- KFF analysis of the 2020 American Hospital Association (AHA) Annual Survey flat files. ↩︎

- In October 2020, HCA returned money that it had received through the Provider Relief Fund program. These dollars are excluded from our HCA calculations for all quarters. ↩︎

- A Wall Street Journal article presented a similar figure with much higher returns for HCA and Tenet than depicted here. The main reason for this difference is that the Wall Street Journal calculated returns relative to March 11, 2020; HCA and Tenet stock had fallen substantially in the two weeks leading up to March 11, 2020, likely reflecting the anticipated effects of the pandemic. ↩︎