Consumer Survey Highlights Problems with Denied Health Insurance Claims

Introduction

A KFF survey of adults with health insurance found that roughly 6 in 10 insured adults experience problems when they use their insurance. Problems studied include denied claims, network adequacy issues, preauthorization delays and denials, and others. The survey also explored how often consumers can successfully resolve health insurance problems when they arrive and the consequences of insurance problems. This Data Note takes a closer look at insured adults who said that in the past year, insurance did not pay for care that they received and thought was covered, which we will refer to as “denied claim.”

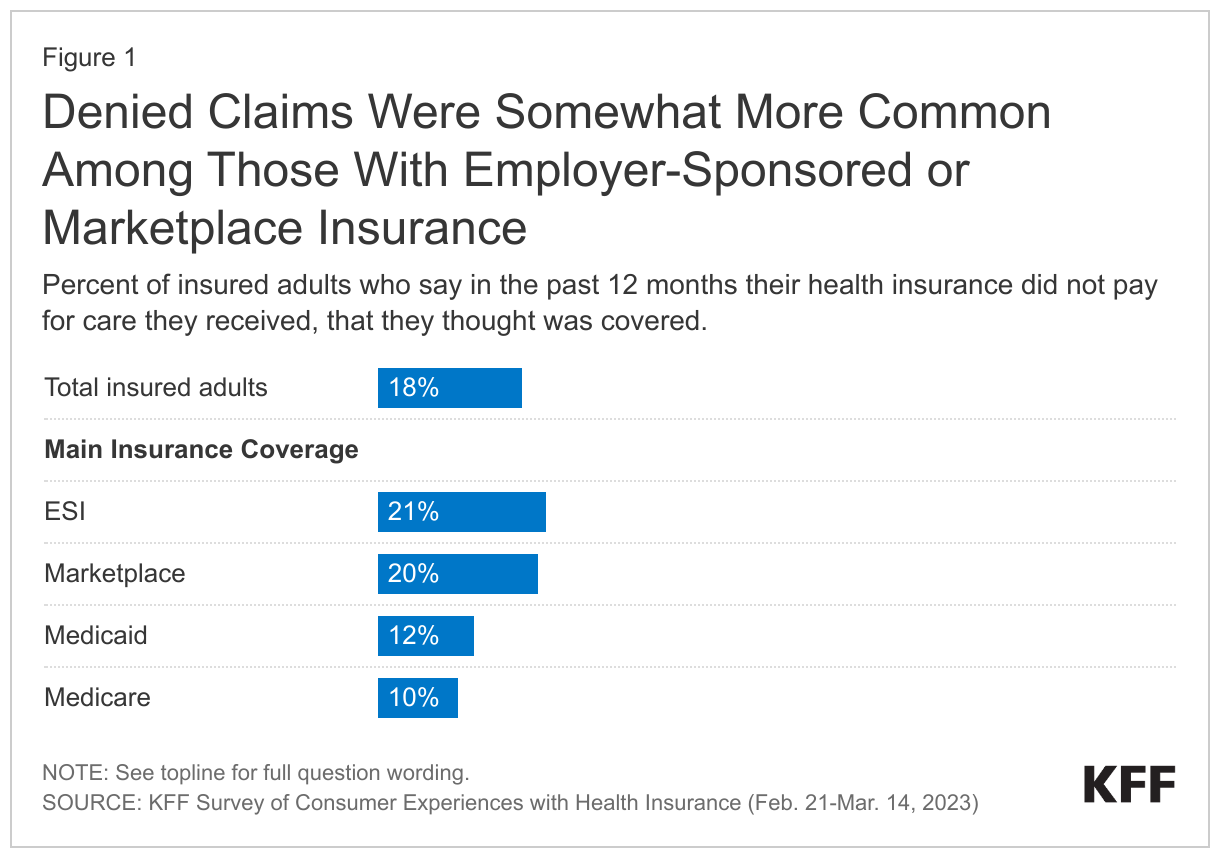

People with private insurance are more likely to have denied claims than people with public coverage

The KFF Survey of Consumer Experiences with Health Insurance found that 18% of insured adults say they experienced denied claims in the past year. This problem was somewhat more common among people with employer-sponsored insurance (21%) and marketplace insurance (20%), less so among people with Medicare (10%) or Medicaid (12%).

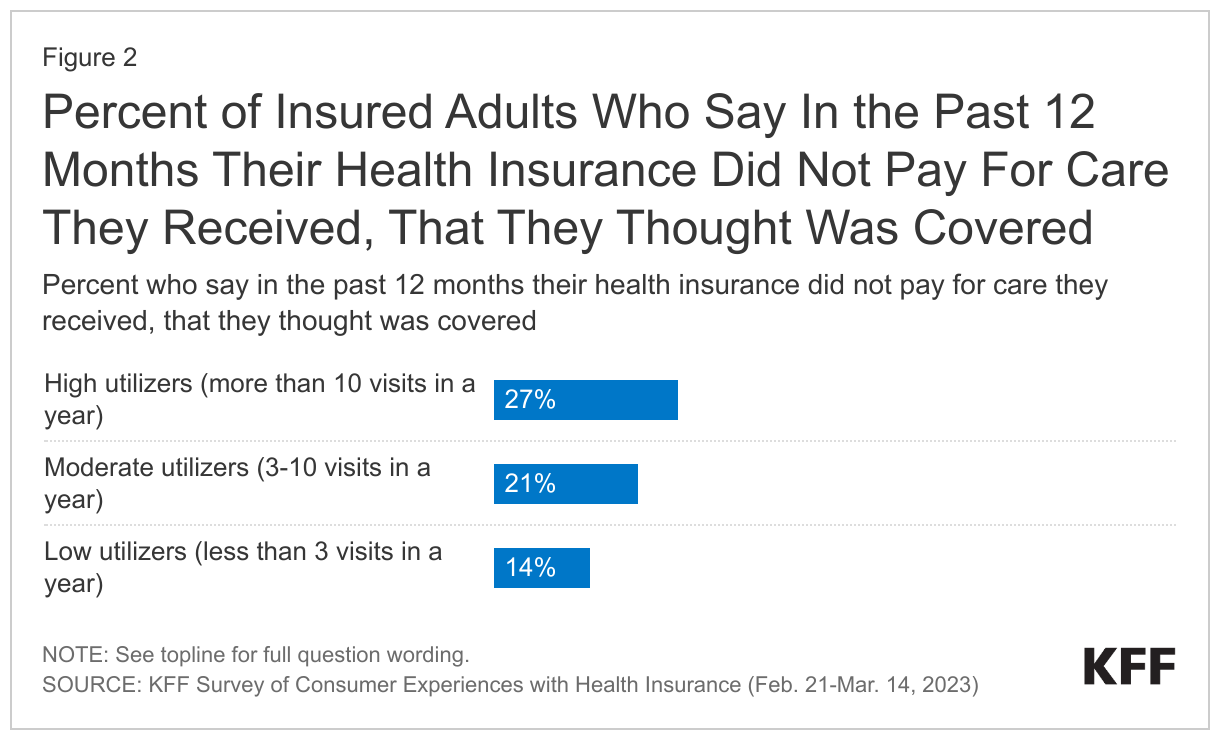

People who use more health services are also more likely to experience denied claims. Among high utilizers - patients who had more than 10 provider visits in the past year – 27% experienced a denied claim, while similar shares of moderate utilizers – who had 3-10 visits in a year – experienced a denied claim (21%). By contrast, smaller shares of patients who had fewer than 3 provider visits in a year experienced a denied claim (14%).

About one in five insured adults who used emergency room services (22%) or mental health services (22%) say they had a denied claim, though there is no way to tell from the survey if the denials were for claims related to these specific services. Finally, people who identify as LGBT are nearly twice as likely to experience denied claims compared to other consumers (30% vs. 17%).

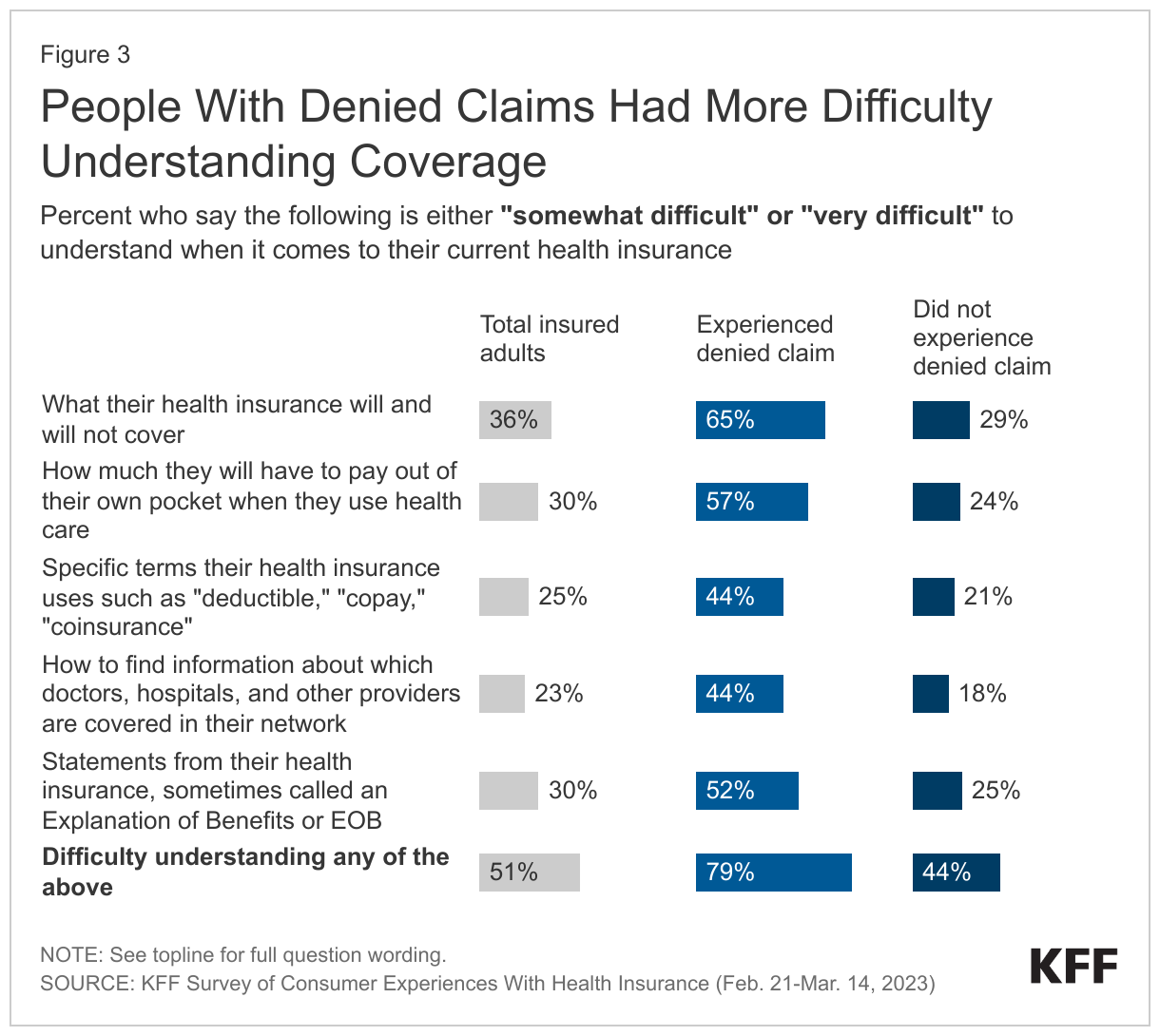

People with denied claims report more difficulty understanding coverage

Difficulty understanding aspects of their health coverage was reported more often among consumers who experienced denied claims compared to others. A majority of consumers who experienced denied claims report difficulty understanding what their health insurance covers (65%), what they’ll owe out of pocket (57%), and their EOBs (52%). It is not clear whether these challenges understanding coverage contribute to claims being denied, or whether denied claims compound the confusion consumers otherwise experience understanding their coverage.

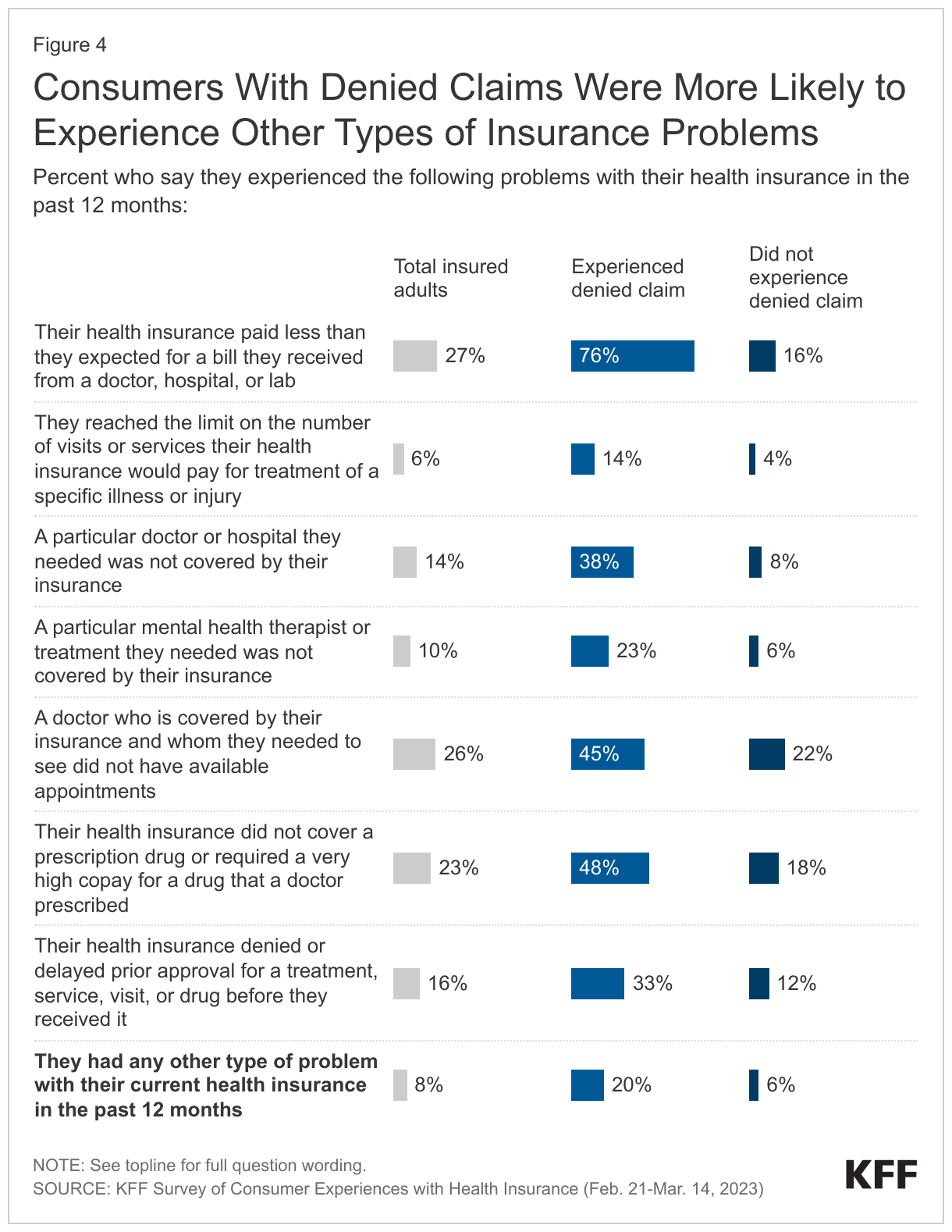

Consumers with denied claims were more likely to experience other types of insurance problems

Consumers who experienced denied claims were much more likely to have also encountered other problems using their coverage in the past year. On average, insured adults with denied claims experienced about 4 different types of insurance problem in a year. Compared to insured adults who did not experience denied claims, those who did were at least twice as likely to have experienced other insurance problems asked about in the survey (such as reaching the limit on covered services, not being able to find or access an in-network provider including a mental health provider, and prior authorization problems).

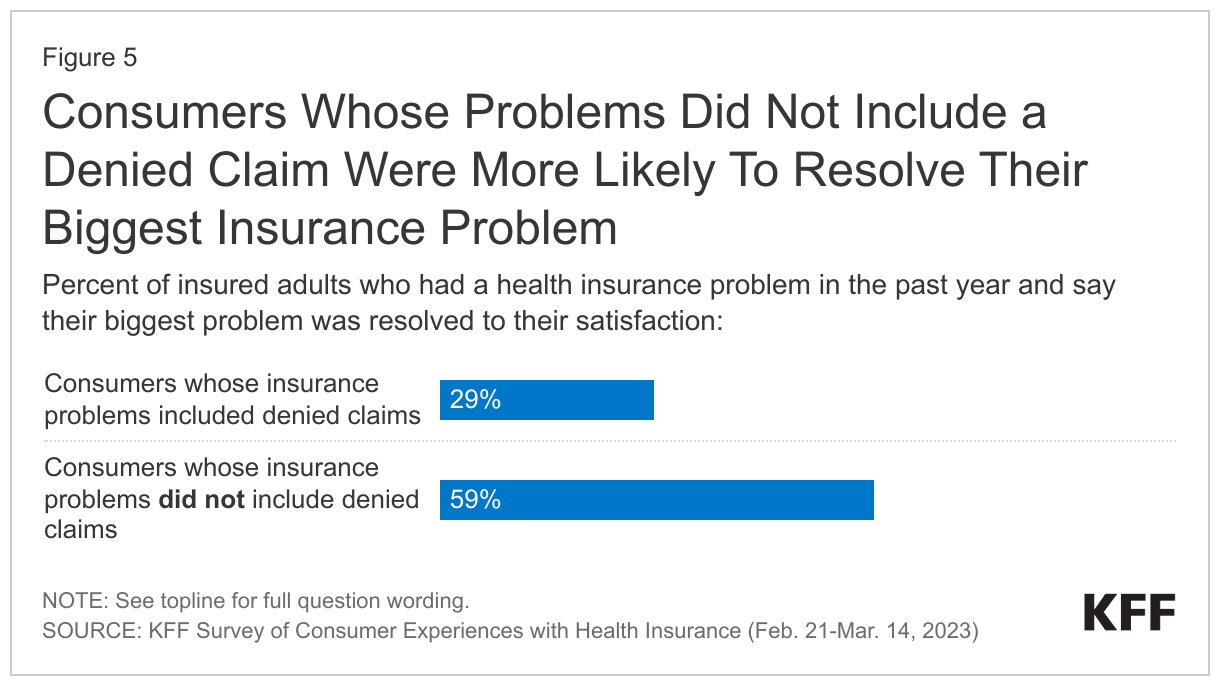

Consumers often cannot resolve problems satisfactorily

Among insured adults who report insurance problems in the past year, half (50%) say the biggest problem they had with their insurance was solved to their satisfaction. The survey did not ask consumers to specify which of their insurance problems was the “biggest.” However, consumers whose problems included a denied claim were half as likely to say their biggest problem was resolved satisfactorily compared to those whose problems did not include a denied claim (29% vs 59%), suggesting that denied claims may be especially challenging for consumers to solve on their own, though it may not be for lack of trying.

About eight in ten (84%) consumers with denied claims took some action to try to resolve the biggest problem they had with their insurance – such as calling the insurance company or asking their doctor or a friend or family member for help – and 15% filed a formal appeal.

Even so, like insured consumers overall, most of those who experienced denied claims do not know whether they have appeal rights (69%) or what government agency to call for help (86%).

The Affordable Care Act established Consumer Assistance Programs (CAPs) whose duties include helping consumers answer insurance questions, resolve insurance problems, and file appeals. By law, private insurance plan denial statements must include a notice with contact information for the CAP (if one is available) and indicating this program can help consumers file an appeal. Only 3% of adults who experienced insurance problems said they contacted a CAP for help, though 79% of all insured adults said they would be at least somewhat likely to seek help from a CAP for help with insurance problems.

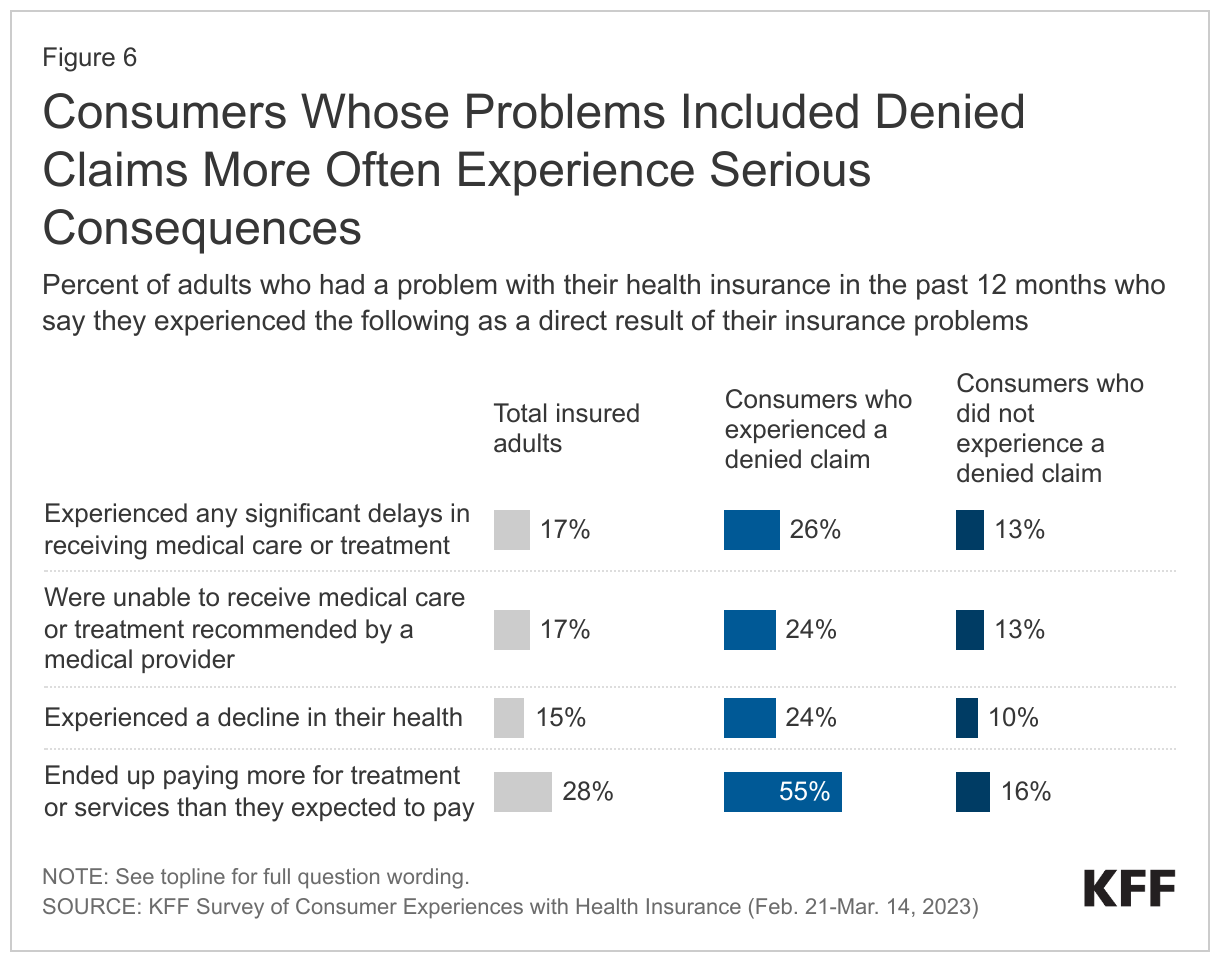

Serious health and financial consequences can result from insurance problems, including denied claims

The survey asked insured adults about the consequences of their insurance problems – whether needed care was delayed or not received, health status declined, and/or out-of-pocket costs increased. Because some people with denied claims also experienced multiple other types of insurance problems in the same year, there is no way to link consequences to a single type of problem. However, comparing consequences for adults whose problems did or did not include denied claims, those with denied claims were about twice as likely to have problems in the past year accessing care or to have health status decline, and more than three times as likely to have unexpectedly higher out-of-pocket costs.

Discussion

Nearly 1 in 5 insured adults (18%) said they experienced a denied claim in the past year. Among people who use the most health care, 27% experienced a denied claim. Claims denials appear to be connected to the complexity of insurance for consumers; while half of all insured adults find some aspect of insurance difficult to understand, among those who experience claims denials it is nearly 8 in 10. In addition, consumers whose problems include a denied claim are far less likely to have resolved their biggest insurance problem satisfactorily compared to those whose problems do not include denied claims. Serious health and financial consequences arise as a direct result of insurance problems, and consumers whose problems include denied claims are far more likely to have needed care delayed or denied, to experience a decline in health status, and to face higher out-of-pocket costs.

Most consumers with denied claims (69%) do not know that they have appeal rights, and the vast majority (85%) do not file formal appeals. Appeal rights vary depending on the type of coverage as do rules or filing appeals and the process can be complicated. Strategies to simplify the appeals process and make consumer notices about how to appeal more prominent and easy to understand might help. Even so, because people who need to appeal health insurance decisions will most often be those who use a lot of health services – and who may be too sick to advocate effectively for themselves – assistance navigating the insurance claims and appeals process is also important.

Congress authorized establishment of Consumer Assistance Programs (CAPs) to help people resolve their insurance problems and file appeals, though consumers with denied claims rarely call on CAPs for help. Connecticut recently implemented a requirement on health insurers to place a prominent, plain-language notice about CAP assistance on the front page of all health insurance denials, which has led to an increase in case referrals to that office. About eight in ten insured adults (79%) say they would likely call on such a program for help with insurance problems. CAPs do not exist in all states, however, and Congress has not appropriated funds for CAPs since 2010.

The KFF survey cannot tell how often claims denials are incorrect, or the extent to which consumer difficulties understanding the complexity of health coverage may contribute to denials. Increased oversight could help supply this information. A federal law requiring private plans to disclose data on denied claims remains largely unimplemented. Such data could be an important tool to monitor trends and differences in denial rates, and to hold insurers accountable to meet legal standards, such as requirements to provide mental health parity and coverage for surprise medical bills.

This work was supported in part by a grant from the Robert Wood Johnson Foundation. The views and analysis contained here do not necessarily reflect the views of the Foundation. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.