Claims Denials and Appeals in ACA Marketplace Plans in 2021

Editorial Note: See KFF’s analysis of more recent data in Claims Denials and Appeals in ACA Marketplace Plans in 2024, published in March 2026.

In this brief, we analyze transparency data released by the Centers for Medicare and Medicaid Services (CMS) on claims denials and appeals for non-group qualified health plans (QHPs) offered on HealthCare.gov. Data were reported by insurers for the 2021 plan year and posted in a public use file in October 2022. We find that, across HealthCare.gov insurers with complete data, nearly 17% of in-network claims were denied in 2021. Insurer denial rates varied widely around this average, ranging from 2% to 49%.

CMS requires insurers to report the reasons for claims denials at the plan level. Of in-network claims, about 14% were denied because the claim was for an excluded service, 8% due to lack of preauthorization or referral, and only about 2% based on medical necessity. Most plan-reported denials (77%) were classified as ‘all other reasons.’

As in our previous analysis of claims denials, we find that consumers rarely appeal denied claims and when they do, insurers usually uphold their original decision. In 2021, HealthCare.gov consumers appealed less than two-tenths of 1% of denied in-network claims, and insurers upheld most (59%) denials on appeal.

The Affordable Care Act (ACA) requires transparency data reporting by all non-grandfathered employer-sponsored health plans and by non-group plans sold on and off the marketplace. Data are to inform regulators and consumers about how health plans work in practice. For example, transparency data could be helpful in oversight of compliance with the Mental Health Parity and Addiction Equity Act (MHPAEA), revealing how or whether claims denial rates differ for behavioral health vs other services. It could also make more transparent trends in the incidence and handling of claims for surprise medical bills, now protected under the No Surprises Act. Yet, the federal government’s broad authority to require transparency data reporting has not been fully implemented. Data to answer these questions are not collected; and data that are collected are not audited, for example, to ensure issuers report data consistently. Transparency data also are not used in oversight nor to develop other tools or indicators to help consumers see and compare differences across plans.

ACA Transparency Data

Under the ACA, required reporting fields for transparency-in-coverage data include:

- Claims payment policies and practices

- Periodic financial disclosures

- Data on enrollment

- Data on disenrollment

- Data on the number of claims that are denied

- Data on rating practices

- Information on cost-sharing and payments with respect to any out-of-network coverage

- Information on enrollee and participant rights under this title

- Other information as determined appropriate by the Secretary

The law requires data to be available to state insurance regulators and to the public.

Partial implementation of ACA transparency data reporting began with the 2015 plan year. To date, reporting is required only by issuers for their qualified health plans (QHP) offered on HealthCare.gov. Issuers report only on the number of in-network claims submitted and denied, the number of such denials that are appealed, and the outcome of appeals. Aggregate data are reported at the issuer level. In 2022, issuers reported aggregated data on all HealthCare.gov QHPs they offered in 2021. Since 2018, issuers are also required to report data at the health plan level, including certain reasons for claims denials. Issuers only report plan-level transparency data plans they seek to offer on HealthCare.gov in the coming year. As a result, for any given issuer, the total plan-level claims reported may not equal the issuer-level claims reported for the 2021 coverage year.1 CMS does not collect data on all fields enumerated in the ACA, including out-of-network claims submitted and out-of-network enrollee cost sharing and payments. Nor has it required any further detailed reporting (e.g., on claims or appeals by type of service or diagnosis.) Federal agencies have yet to require transparency in coverage data reporting by other non-group plans or employer-sponsored plans.2

Claims Denials and Appeals in 2021

This brief focuses on transparency data for the 2021 calendar year submitted by qualified health plans (QHPs) offered to individuals on HealthCare.gov as part of the 2023 plan certification process. Our analysis excludes stand-alone dental plans and issuers with incomplete data or less than 1,000 claims submitted. From the public use file, we developed a working file that is posted with this brief.

Claims submitted and denied

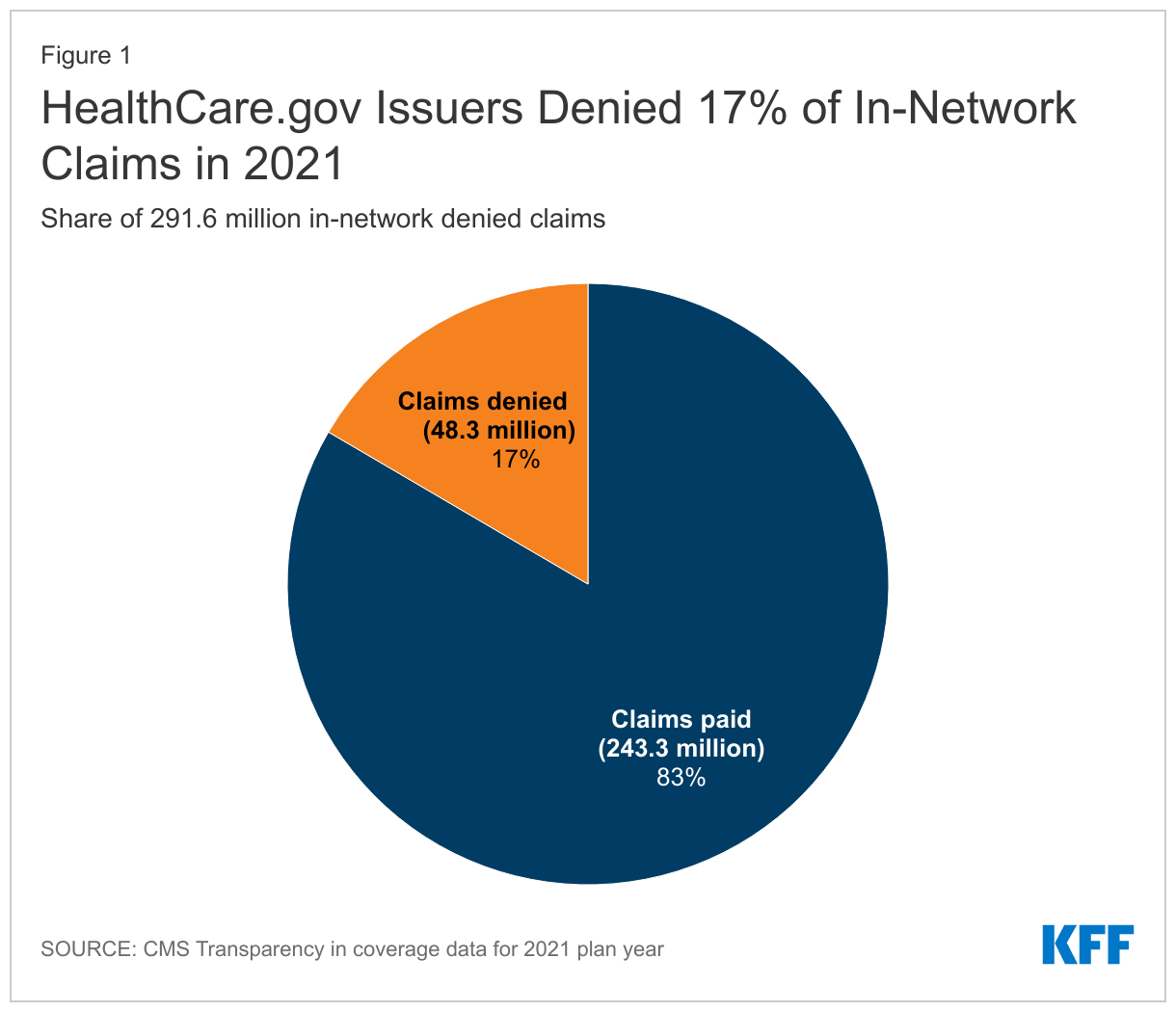

Of the 230 major medical issuers in HealthCare.gov states that reported for the 2021 plan year, 162 reported receiving at least 1,000 in-network claims and show data on claims received and denied. Together these issuers reported 291.6 million in-network claims received, of which 48.3 million were denied, for an average in-network claims denial rate of 16.6% (Figure 1)

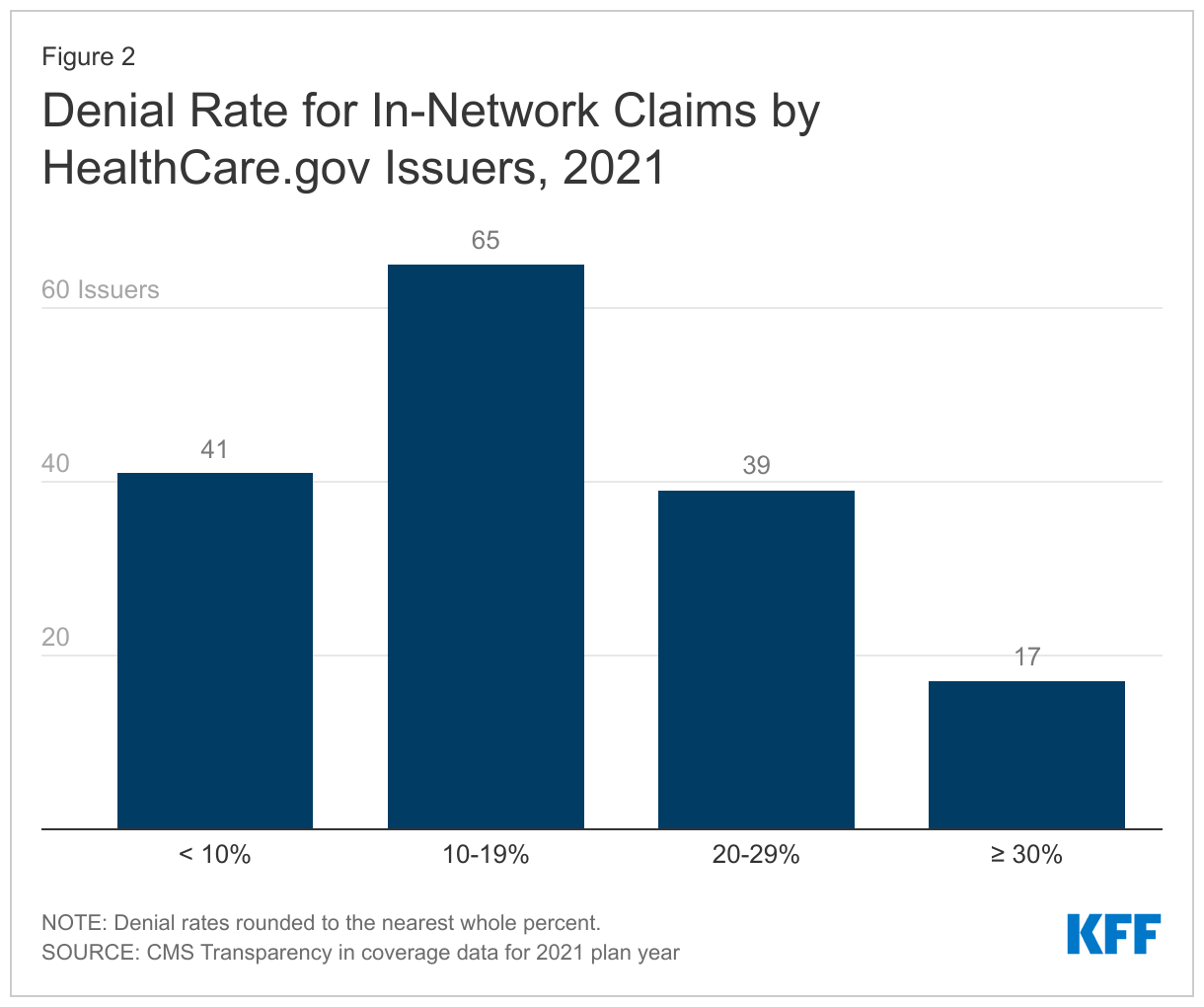

Issuer denial rates for in-network claims ranged from 2% to 49%. In 2021, 41 of the 162 reporting issuers had a denial rate of less than 10%, 65 issuers denied between 10% and 19% of in-network claims, 39 issuers denied 20-29%, and 17 issuers denied 30% or more of in-network claims. (Figure 2) Issuers that report denying one-third or more of all in-network claims in 2021 included Meridian Health Plan of Michigan, Absolute Total Care in South Carolina, Celtic Insurance in 7 states (FL, IL, IN, MO, NH, TN, TX), Ambetter Insurance in 3 states (GA, MS, NC), Optimum Choice in Virginia, Buckeye Community Health Plan in Ohio, Health Net of Arizona, and UnitedHealthcare of Arizona.

Table 1 shows denial rates for issuers who reported the highest volume of in-network claims in 2021, receiving over 5 million claims. Among these issuers, denial rates ranged from 5.7%. to 41.9%.

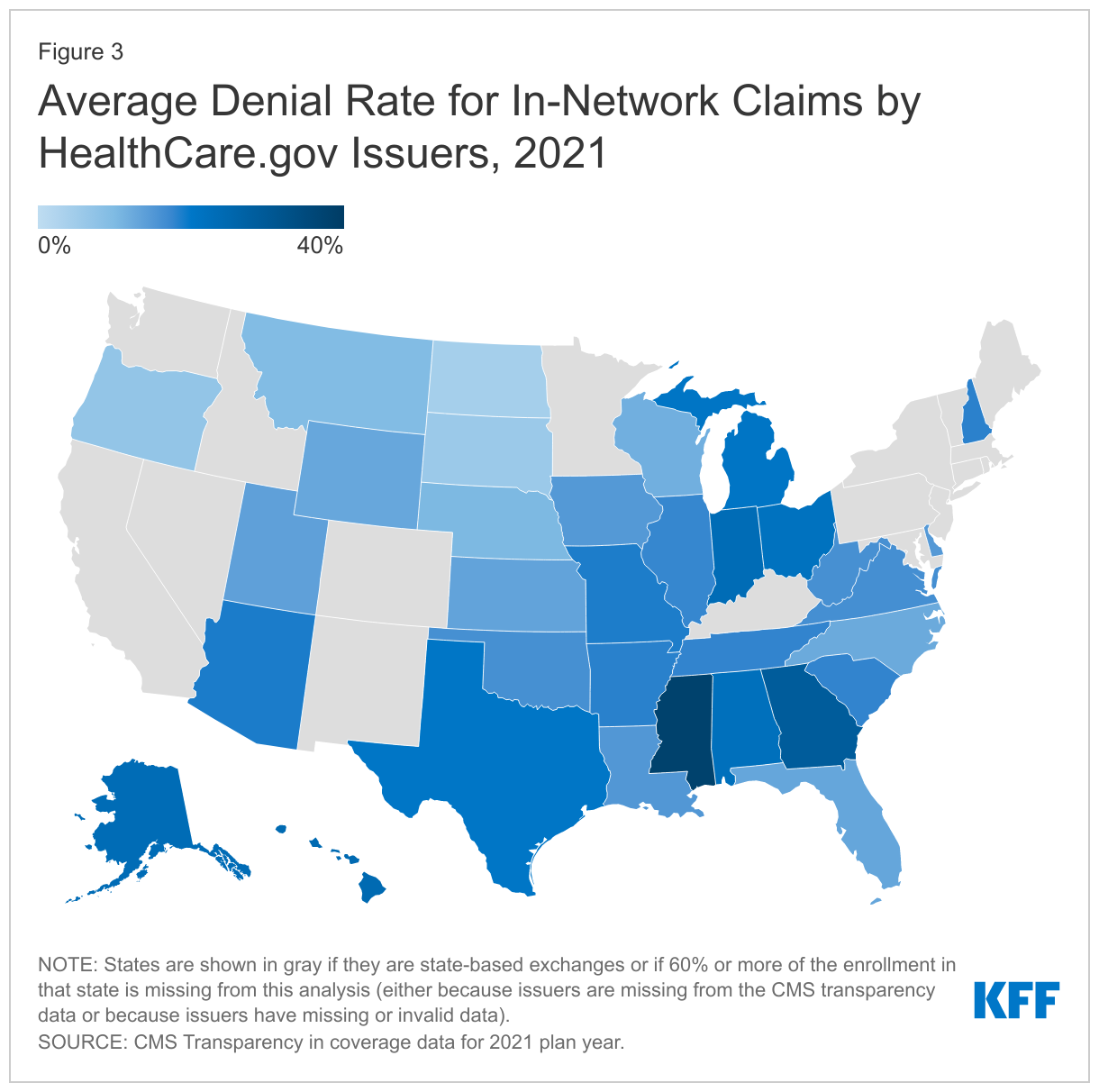

Denial rates also varied geographically. (Figure 3) State average denial rates can obscure variation within a state. For example, in Florida, where the average denial rate was 13% in 2021, the five issuers with largest market shares reported denial rates for in-network claims ranging from 15% to 42%.

Plan-level claims denial data

CMS also collects limited transparency data at the plan level. Of the 162 issuers reporting aggregate data, 158 report plan level data on in-network claims received and denied, as well as data on selected reasons for denials. Denial rates varied somewhat based on plan metal levels. On average, in 2021, HealthCare.gov issuers denied 15.9% of in-network claims in their bronze plans, 17.3% in silver plans, 17.1% in gold plans, 11.4% in platinum plans, and 19.7% in catastrophic plans.

Why do health plans deny claims?

HealthCare.gov plans also report on certain categories of reasons for in-network claims denials:

- Denials due to lack of prior authorization or referral

- Denials due to an out-of-network provider

- Denials due to an exclusion of a service

- Denials based on medical necessity (reported separately for behavioral health and other services)

- Denials for all other reasons

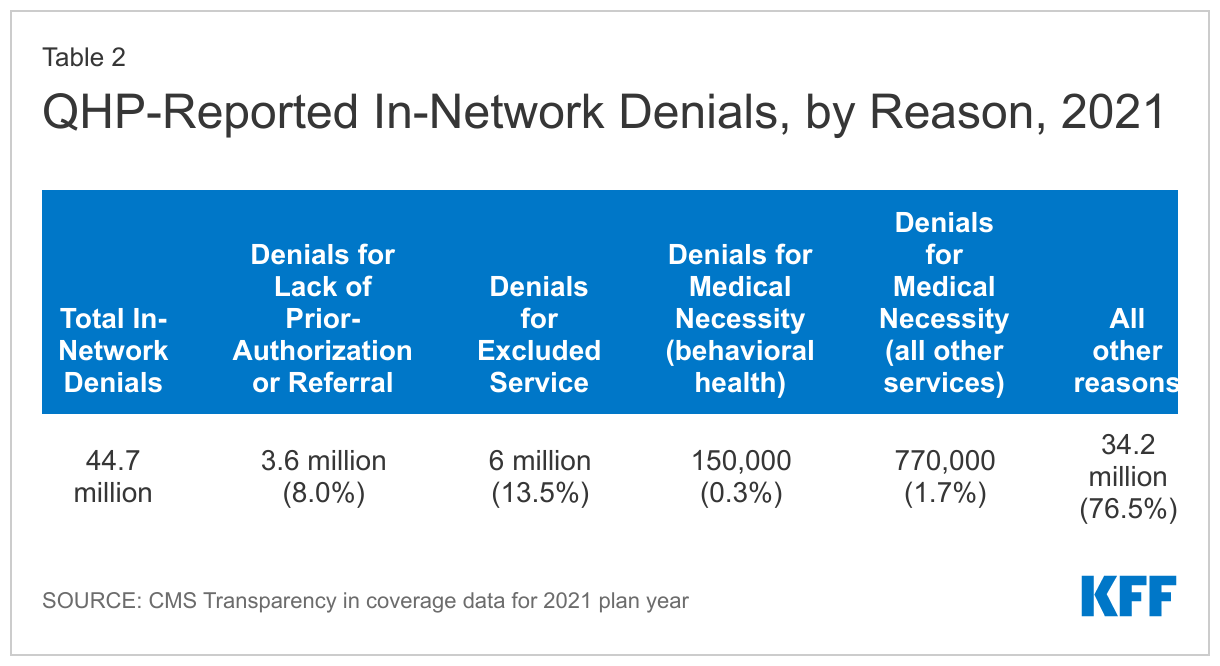

A claim might be denied for more than one reason. In addition, insurers are required to report reasons for denials of claims that ultimately are paid. In all, insurers reported 41.7 million denied in-network claims at the plan level for the 2021 coverage year. Insurers also reported 44.7 million reasons for denying in-network claims, including roughly 3 million denials of claims that were later paid.

The distribution of in-network denials by reason is shown in Table 2. (We set aside data for out-of-network claim denials because CMS does not require issuers to report on the number of out-of-network claims received.) About 8% of these 44.7 million denials were for services that lacked prior-authorization or referral, 13.5% were for excluded services, 1.7% for medical necessity reasons, and 76.5% for all other reasons.

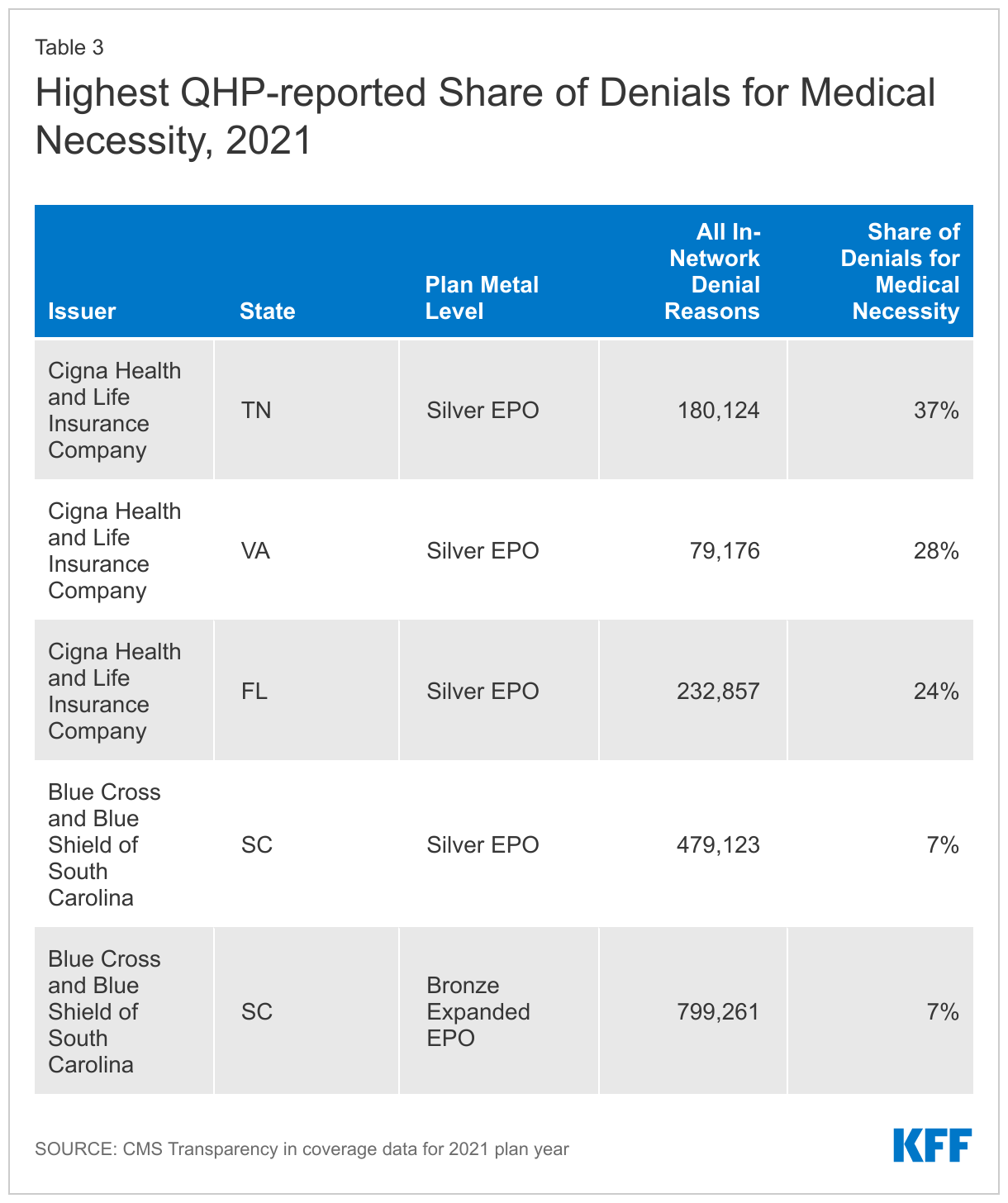

Again, totals obscure variation by plan. For example, while about 2% of all in-network claim denials by HealthCare.gov plans were based on medical necessity, several plans with large volume of denials (more than 75,000) reported much higher shares for medical necessity reasons, up to 37%. (Table 3)

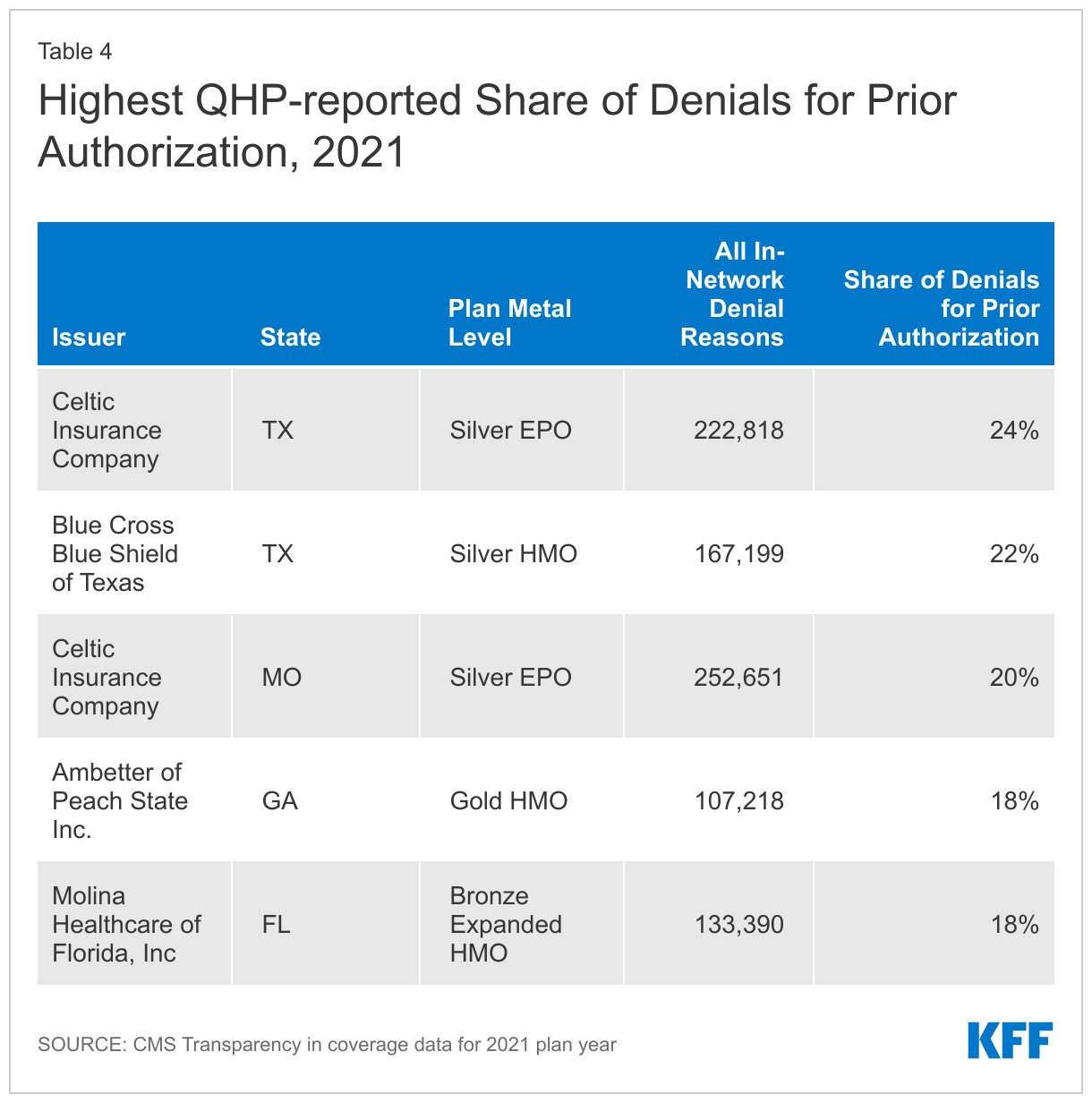

Similarly, while about 9% of all in-network denials by HealthCare.gov plans were based on lack of prior-authorization or referral, some plans reported a much larger share of their denials were for that reason – as high as 24%. (Table 4)

The transparency data indicate that plans seem to apply utilization review techniques very differently. However, without more detail on the types of claims subject to these denials, it is not possible to discern what the implications for patients might be.

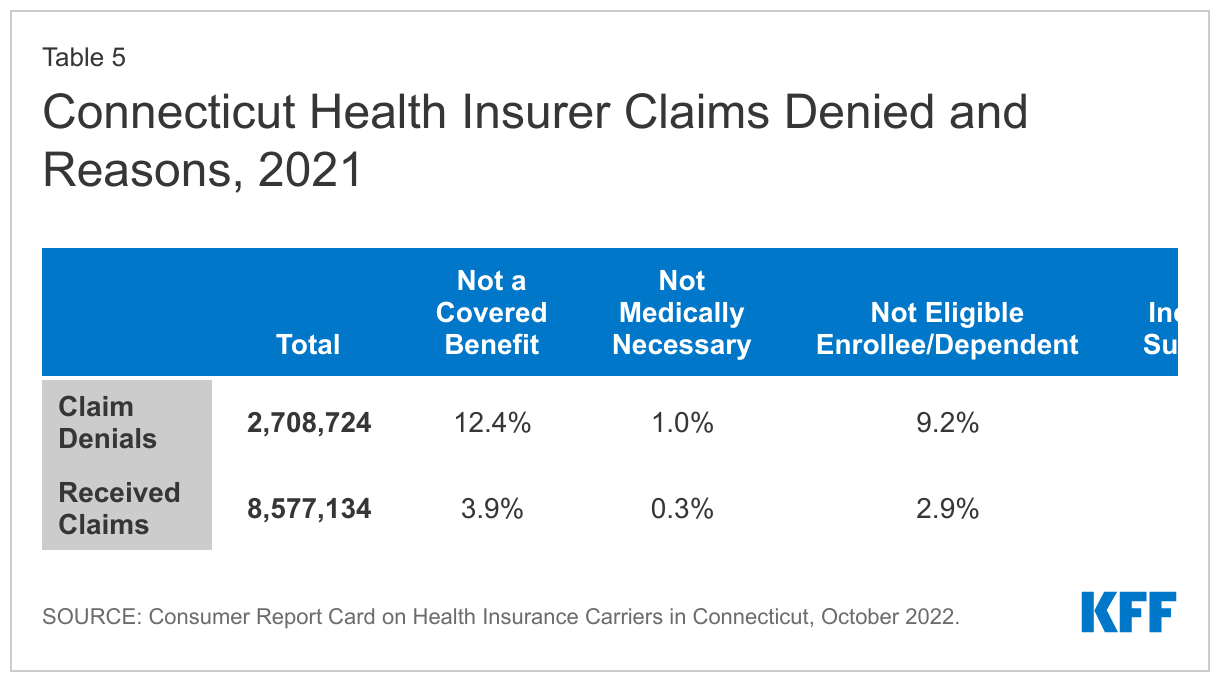

Of note, Connecticut regulators require health insurers in all market segments, including fully insured employer plans, to report annual data on claims payment practices, and other measures. Denial rates and reasons reported by Connecticut insurers are similar to those reported by HealthCare.gov QHPs. (Table 5)

Appeals

ACA transparency data show the number of denied in-network claims that consumers appealed to the plan (internal appeals) and the number of denials overturned at internal appeal. Consumers whose denial is upheld at internal appeal sometimes have the right to an independent external appeal. (Under federal regulations, eligibility for external appeal is generally restricted to medical necessity denials, though in some states all denials can be externally appealed.) HealthCare.gov issuers also report the number of external appeals made by consumers, and the number of externally appealed denials that were overturned. The CMS public use file suppresses values lower than 10.

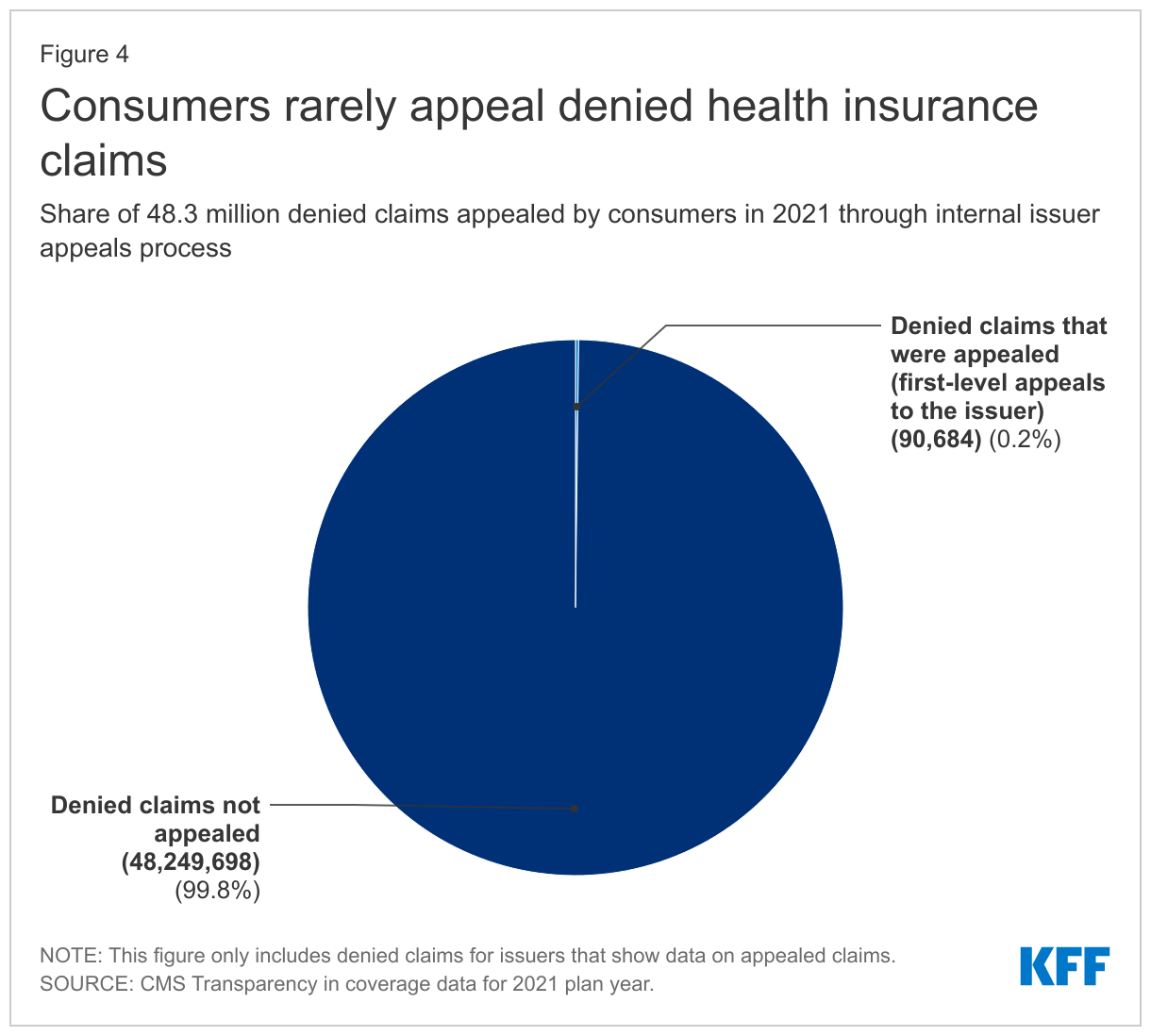

Consumers rarely appeal denied claims. Of the more than 48 million in-network denied claims in 2021, marketplace enrollees appealed 90,599 – an appeal rate of less than two-tenths of one percent. (Figure 4) Issuers upheld 59% of denials that were appealed.

Marketplace consumers also rarely file external appeals. From ACA transparency data (and imputing a value of “5” for each cell where values were suppressed) we estimate just over 2,500 external appeals were filed by marketplace enrollees in 2021.

Discussion

Limited ACA transparency data collected by the federal government continues to show wide disparities in the rate at which marketplace plans pay claims. While on average HealthCare.gov insurers denied nearly 17% of in-network claims in 2021, some insurers report denying nearly half of in-network claims submitted. The federal government has not expanded or revised transparency data reporting requirements in years and does not appear to conduct any oversight using data that are reported by marketplace plans. As a result, consumers are not provided any information about how reliably marketplace plan options pay claims and plans reporting high claims denial rates do not appear to face any consequences.

- If an issuer offered a plan in 2021 that it no longer intends to offer in 2023, it should report issuer-level data for that 2021 plan, but no plan-level 2021 data will be reported for that plan. Similarly, if an issuer seeks to offer a plan in 2023 that it did not offer in 2021, it will report transparency data of “NA” for that plan in 2022. Under these reporting rules, the total issuer-level claims data for 2021 may include plans that will not be offered in 2023; as a result the plan-level claims total may not equal the issuer-level claims total. For more detailed transparency data reporting instructions, see “Qualified Health Plan Issuer Application Instructions, Plan Year 2023” starting at page 2E-1. ↩︎

- In 2020, the Trump Administration issued a final regulation requiring all non-grandfathered plans – including those sponsored by employers or offered by issuers outside of HealthCare.gov – to report billed charges and negotiated allowed amounts for covered items and services, enforceable beginning July 1, 2022. The regulation invokes ACA transparency data reporting authority but does not require plans to report prices to CMS; instead, price data must be posted online by each plan sponsor and issuer, making it unlikely that the price data across plans and issuers will be compiled into a single public use file provided by the federal government. ↩︎