The Uninsured at the Starting Line in Missouri: Missouri findings from the 2013 Kaiser Survey of Low-Income Americans and the ACA

This report provides new data to help policymakers further understand early challenges in implementing the Affordable Care Act (ACA) in Missouri and highlight the health insurance and health care needs of those who may remain uninsured. The report is part of an ongoing series of comprehensive surveys nationally and in select states that will provide data on these groups’ experience with health coverage, current patterns of care, and family finances. The Missouri report, based on the baseline 2013 Kaiser Survey of Low-Income Americans and the ACA, provides a snapshot of health insurance coverage, health care use and barriers to care, and financial security among insured and uninsured adults in Missouri across the income spectrum at the starting line of ACA implementation.

Executive Summary

The 2010 Affordable Care Act (ACA) has the potential to reach many of the 47 million Americans who lack insurance coverage, including over 800,000 in Missouri, as well as millions of insured people who face financial strain or coverage limits related to health insurance. In January 2014, the major coverage provisions of the ACA went into full effect. These provisions include the creation of new Health Insurance Marketplaces where low and moderate income families can receive premium tax credits to purchase coverage and, in states that opted to expand their Medicaid programs, the expansion of Medicaid eligibility to adults with incomes at or below 138% of the federal poverty level (FPL). The marketplace in Missouri is federally facilitated, as the state opted not to run its own. In addition, as of March 2014, Missouri had not expanded its Medicaid program, leaving many uninsured adults below poverty in Missouri who would have been newly-eligible for Medicaid without a coverage option.

Though ACA implementation is underway in Missouri and across the country and people are already enrolling in coverage, policymakers continue to need information on the uninsured population. Reports of difficulties in enrolling in coverage, continued confusion and lack of information about the law point to challenges in the early stages of implementation, and information about the population targeted for coverage expansion can inform efforts to address these difficulties. In addition, because Missouri could still opt to expand its Medicaid program, it is important to have detailed data on the population that could benefit from such a coverage expansion. Specifically, information on poor and moderate–income adults’ experiences with health coverage, current patterns of care, and family situations can provide insight into some of the challenges that are arising in the first months of coverage and highlight the potential impact of gaining coverage on poor and moderate- income adults.

This report, based on findings from the 2013 Kaiser Survey of Low-Income Americans and the ACA, provides a snapshot of health insurance coverage, health care use and barriers to care, and financial security among insured and uninsured Missouri adults across the income spectrum at the starting line of ACA implementation. The survey, conducted between July and September 2013, is a nationally representative survey that also includes a state-representative sample of over 1,800 nonelderly (age 19-64) adults in Missouri. It was designed to focus on the low- and moderate-income populations in the state and includes over-samples of people in the income range for financial assistance under the ACA (< 138% FPL for Medicaid and 139-400% FPL for Marketplaces), as well as a comparison group with incomes over 400% FPL. Since many uninsured adults with incomes below 100% FPL are left in a coverage gap in Missouri, our analysis focused on poor adults (<100% FPL) and moderate-income adults (100%-400% FPL) who will be eligible for premium subsidies. The survey includes adults with employer coverage, nongroup, Medicaid, and other sources of coverage, as well as those with no health insurance. The Missouri component of the survey and report on its findings complements a report on similar findings for the nation.1

This survey and report provides new data to help policymakers further understand early challenges in implementing health reform and highlight the health insurance and health care needs of those who may remain uninsured. This survey also provides a baseline for future assessment of the impact of the ACA in Missouri on health coverage, access, and financial security of poor and moderate-income individuals. Detailed information on the survey design, sample, and analysis can be found in the Methods section at the end of the full report.

Background: The Challenge of Expanding Health Coverage in Missouri

Prior to implementation of the ACA, 834,000 Missourians—16% of the state’s nonelderly population—were without health insurance coverage. Because publicly-financed coverage has already been expanded to most low-income children and Medicare covers nearly all of the elderly, the vast majority of uninsured people in Missouri and across the country are nonelderly adults.2 The main barrier that people have faced in obtaining health insurance coverage is cost: health coverage is expensive, and few people can afford to buy it on their own. While most Americans traditionally obtain health insurance coverage as a fringe benefit through an employer, not all workers are offered employer coverage. Medicaid covers many low-income children, but eligibility for parents was limited before the ACA and nonexistent for childless adults, leaving many adults without affordable coverage. As of January 2014, Medicaid eligibility for adults in Missouri is limited to parents with incomes below 23% of poverty, or about $5,500 a year for a family of four.3 Adults without dependent children are ineligible regardless of their income.4

Barriers to coverage are reflected in the characteristics of the uninsured population in Missouri. Uninsured Missouri adults are more likely to be poor than Missourians with private health insurance (including employer coverage and nongroup coverage), while adults with Medicaid coverage are particularly poor (reflecting eligibility limits). Though the majority of uninsured adults are in a family with either a full- or part-time worker, uninsured Missouri adults are less likely than privately insured adults to be in families with either a full- or part-time worker. The unique demographics of the state population also play a role in shaping the profile of uninsured Missourians. Missouri’s population resides in both rural and urban settings. The rural population is very low-income, leaving a large percentage of that population uninsured. The population in Missouri’s two major cities is very diverse with a majority of the population in St. Louis identifying as a race other than White.5 These geography and demographic differences have implications for outreach efforts as well as access to care as many uninsured adults in Missouri will likely remain uninsured in 2014 without a Medicaid expansion.

I. Patterns of Coverage and the Need for Assistance

Examining patterns of coverage and the reasons the uninsured lack coverage can inform both outreach avenues and potential barriers to outreach and enrollment. Key survey findings on access to coverage include:

For many currently uninsured adults in Missouri, lack of coverage is a long-term issue. While some people experience short spells of uninsurance due to job changes, income fluctuations, or renewal issues, for many uninsured Missouri adults, lack of coverage is a chronic issue. The survey shows that 43% of uninsured adults report being uninsured for 5 years or more, including 14% of the uninsured who report that they have never had coverage in their lifetime.

Many uninsured adults in Missouri report trying to obtain insurance coverage in the past, but most did not have access to affordable coverage. Prior to the ACA, Missouri’s uninsured reported difficulty gaining insurance coverage due to the high cost of coverage and limits on Medicaid eligibility for adults. More than eight in ten (83%) uninsured adults report no access to employer insurance, and the majority of people who had access to coverage through an employer report that the coverage offered to them is not affordable. One-third of uninsured Missouri adults (34%) reported trying to sign up for Medicaid in the past five years, and the majority of them were unsuccessful because they were told they were ineligible. And one in four uninsured Missouri adults (25%) reported trying to obtain nongroup coverage in the past five years, with most not purchasing a plan because the policy they were offered was too expensive.

Health insurance coverage is not always stable. For most insured adults in Missouri, coverage is continuous throughout the year and over time, but a sizable number have a gap or change in coverage. When accounting for both insured Missourians with a gap in their coverage and uninsured Missourians who recently lost coverage, the survey indicates that 11% of adults in Missouri, or almost 400,000 people, lose or gain coverage over the course of a year. In addition to those who lose or gain coverage over the course of a year, 320,000 continuously insured adults report having a change in their health insurance plan. The most common reasons for a change in coverage appear to be related to employment. Last, a small number of insured Missouri adults report challenges in either renewing or keeping their coverage, another indication of instability in coverage throughout the year.

Informing Missouri’s ACA Implementation: Many of the barriers to coverage that Missouri’s uninsured reported facing in the past are addressed by the ACA’s provisions to expand Medicaid and provide premium tax credits for Marketplace coverage. However, since Missouri has not expanded Medicaid coverage at this time, many uninsured adults will be left in a coverage gap and will remain uninsured. In addition to limited coverage options, some uninsured adults may continue to face financial and other barriers to coverage. Missourians targeted by the ACA have varying levels of experience with the insurance system. A large share of uninsured adults in Missouri has been outside the insurance system for quite some time, and the long-term uninsured may require targeted outreach and education efforts to link them to the health care system and help them navigate their new health insurance. In addition, people who have attempted to obtain coverage in the past may be unaware that rules and costs have changed under the ACA; outreach and education will be needed to inform people that financial assistance is available to offset the cost of private coverage.

While there has been much focus on enrolling currently uninsured people into coverage, survey findings demonstrate that people will continue to move around within the insurance system throughout the year as their income or job situations change. Thus, implementation is not a “one shot” effort that will be done once open enrollment ends in March 2014, but rather will require a continuous effort to enroll and keep people in coverage. Also, if Missouri decides to later expand Medicaid, a second round of outreach and enrollment strategies will be needed to inform uninsured adults of this policy change.

II. What to Look for in Enrolling in New Coverage

While many currently uninsured adults in Missouri have limited experience in signing up for and using health coverage, the past successes and challenges of insured poor and moderate-income adults can inform the experiences of those seeking coverage under the ACA. Key survey findings related to plan enrollment and plan choice are:

While many adults in Missouri report facing no difficulty in applying for Medicaid coverage prior to the ACA, some encountered difficulties in the process of applying for public coverage in the past. Missouri adults who currently have Medicaid or who have attempted to enroll in the past five years reported little difficulty in taking steps to enroll in Medicaid, with almost half (49%) saying the entire process was very or somewhat easy. However, the rest found at least one aspect of the process – finding out how to apply, filling out the application, assembling the required paperwork, or submitting the application – to be somewhat or very difficult. The most commonly-reported difficulty assembling the required paperwork, which 37% of Missourians who applied or enrolled said was somewhat or very difficult.

When adults with Medicaid or private insurance have a choice of plan, they do not always prioritize costs over other plan features in making that choice, and many find some aspect of the plan choice process to be a challenge. Adults chose health plans for various reasons, with 38% of those who had and made a choice of plan reporting that they chose their plan because it covered a wide range of benefits or a specific benefit that they need, 27% because their costs would be low, and 19% because the plan had a broad selection of providers or included their doctor. In choosing a plan, even if they have limited options, Missourians may face challenges in comparing costs, services, and provider networks, as these factors have typically varied greatly across plans in the past. In general, insured adults in Missouri report that they did not have difficulty in comparing their plan choices, but about a third found some aspect of plan choice—comparing services, comparing costs, and comparing providers— to be difficult.

Overall, adults in Missouri with employer coverage, nongroup, or Medicaid report satisfaction with their current coverage but also report gaps in covered services and problems when using their coverage. Most (84%) insured adults in Missouri rate their pre-ACA coverage as excellent or good, but they also report gaps in services that are covered by their current insurance. One in six (17%) insured adults in Missouri report needing a service that is not covered by their current plan, typically ancillary services, such as dental, vision care, and chiropractor services. Many insured adults in Missouri reported experiencing a problem with their current insurance plan covering a specific benefit, either because they were denied coverage for a service they thought was covered (23%) or their out-of-pocket costs for a service were higher than they expected (38%).

Informing ACA Implementation. The ACA includes provisions to simplify the Medicaid application and enrollment process for coverage. The ACA also requires plans in the Marketplace to provide detailed, standardized plan information for people to compare coverage options. Uninsured Missouri adults applying for coverage after these new processes are implemented should encounter fewer challenges in navigating enrollment and plan choice than applicants have in the past. However, in evaluating the success of plan enrollment, it is important to bear in mind that, even prior to the ACA, insured adults faced some challenges in comparing and selecting insurance coverage. While provisions in the ACA could address these challenges, some are inherent to the complexity of insurance coverage. It is also important to remember that people place utility on a range of factors related to insurance, including scope of services and provider networks. Assessments of whether people are choosing the optimal plan for themselves and their family will need to consider the multiple priorities that people balance in plan selection. Last, while the ACA aims to ensure coverage of at least a basic set of essential health benefits (EHB), many of the ancillary services that people report needing coverage for—such as dental services—are not included in the EHB. Newly-insured Missourians may be surprised to learn that some ancillary services are not included in their plan, and education efforts will be needed to help Missourians understand their coverage.

III. Gaining Coverage, Getting Care

As uninsured adults in Missouri gain coverage, there are likely to be changes in how often they seek care, what type of care they seek, and where they seek care. By comparing their current interactions with the health care system to their insured counterparts, the survey can provide insight into likely changes. It can also highlight potential ongoing unmet need among those who remain uninsured. Key findings in this area include:

A large segment of the uninsured in Missouri has little or no connection to the health care system. Many uninsured adults report few connections to the health care system. Only 55% of uninsured adults report that they have a usual source of care, or a place to go when they are sick or need advice about their health, and only 36% of uninsured adults say they have a regular doctor, about half of the rate of insured adults in Missouri. This lack of a connection to the health care system leads many uninsured adults to go without care. Six in ten uninsured adults in Missouri (60%) reported at least one health care visits in the past year, compared to 93% of Medicaid beneficiaries and 87% of adults with employer coverage.

Many uninsured Missourians have health needs, many of which are unmet or only met with difficulty. Uninsured adults are less likely than their insured counterparts to report receiving care for an ongoing health condition. When uninsured individuals do receive care, they sometimes receive free or reduced-cost care, though the majority who use services do not. More than half (56%) of the uninsured and more than half (54%) of Medicaid beneficiaries in Missouri report needing but postponing care, compared to 27% of adults with employer coverage. The most common reason for postponing care among the uninsured is cost, as the uninsured have no coverage to help them with the cost of care.

Many uninsured Missourians report limited options for receiving health care when they need it. Uninsured adults in Missouri are less likely than their insured counterparts to receive care in a private physician’s office when they do get care. Uninsured adults are about half as likely to report choosing their usual source of care because a preferred physician (26%) as compared to 49% of adults with Medicaid and 56% of adults with employer coverage.

Informing ACA Implementation: The survey findings reinforce conclusions based on prior research: having health insurance affects the way that people interact with the health care system, and people without insurance have poorer access to services than those with coverage. Thus, gaining coverage could connect many currently uninsured Missouri adults to the health care system. Given the health profile of Missouri’s currently uninsured population, there is likely to be some pent-up demand for health care services among the newly-covered. However, outreach may be needed to link the newly-insured to a regular provider and help them establish a pattern of regular preventive care. In particular, some individuals who have relied on emergency rooms or urgent care centers as their usual source of care may require help in establishing new patterns of care and navigating the primary care system. While Missouri’s uninsured may have more options for where to receive their care once they obtain coverage under the ACA, many uninsured adults will remain uninsured so safety net providers such as clinics and hospitals that already see a large share of uninsured adults may continue to play an important role in serving this population. Last, while coverage gains may reduce cost barriers to care, it will be important to monitor whether other barriers to care among the poor and moderate-income population—such as transportation or wait times for appointments—continue to pose a challenge for access.

IV. Health Coverage and Financial Security

In addition to facilitating access to health care, health insurance serves primarily to protect people from high, unexpected medical costs. However, for poor families in Missouri, health costs can still be a burden, even if they have insurance. Understanding these issues can help policymakers monitor ongoing financial barriers to health services.

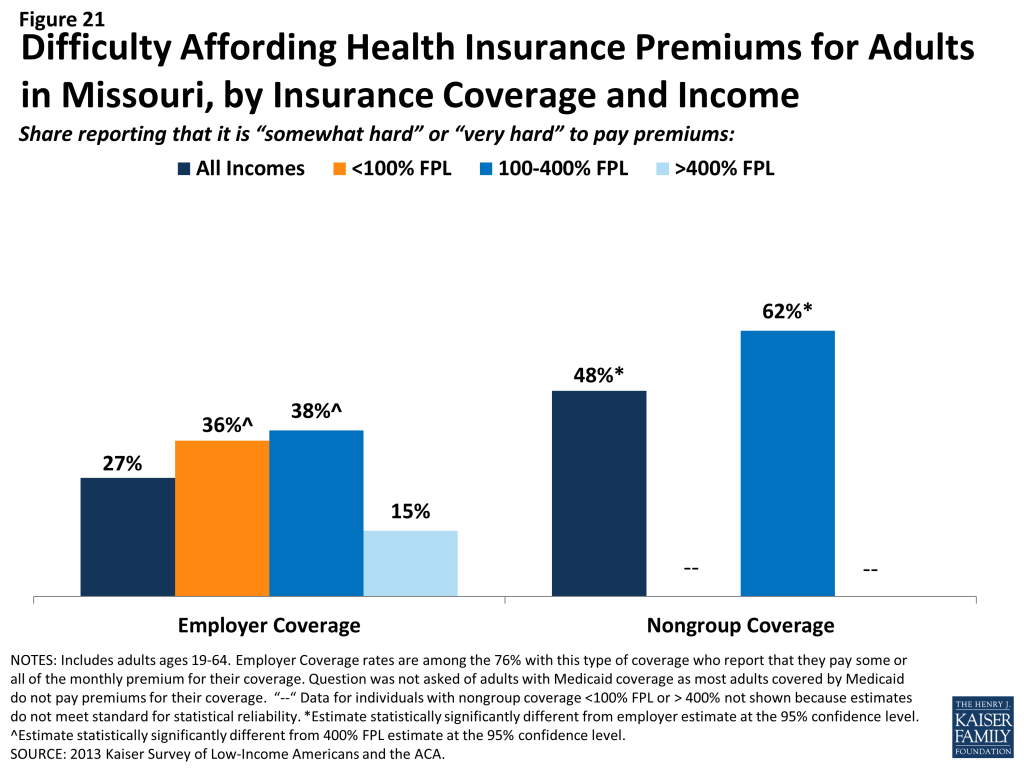

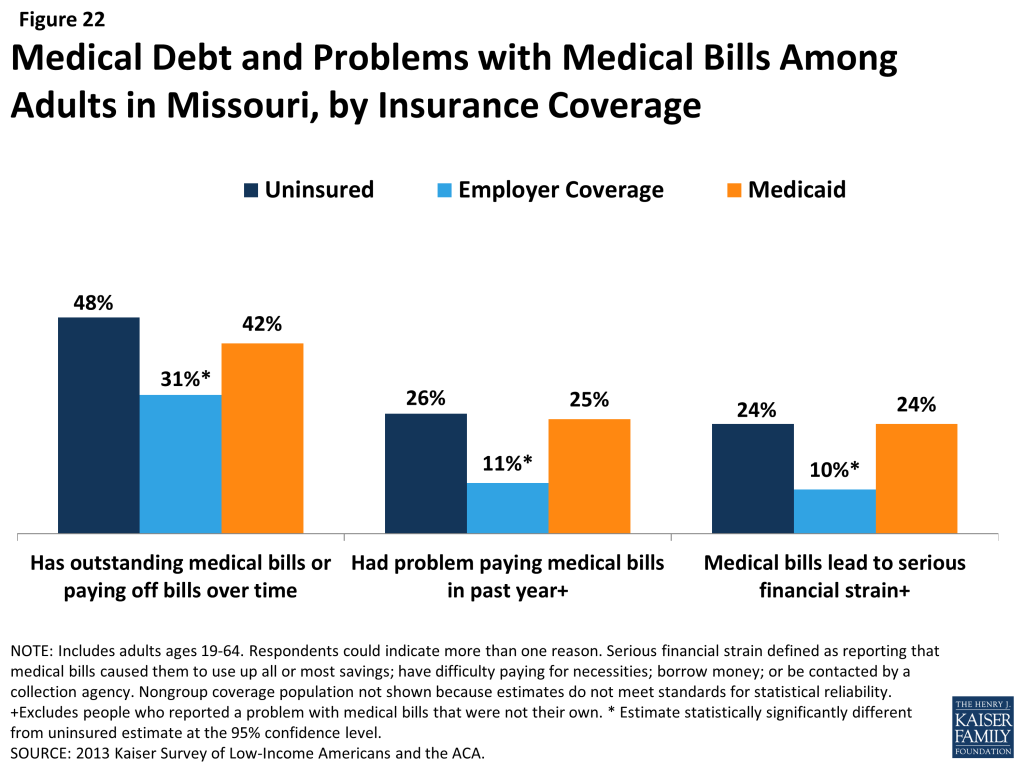

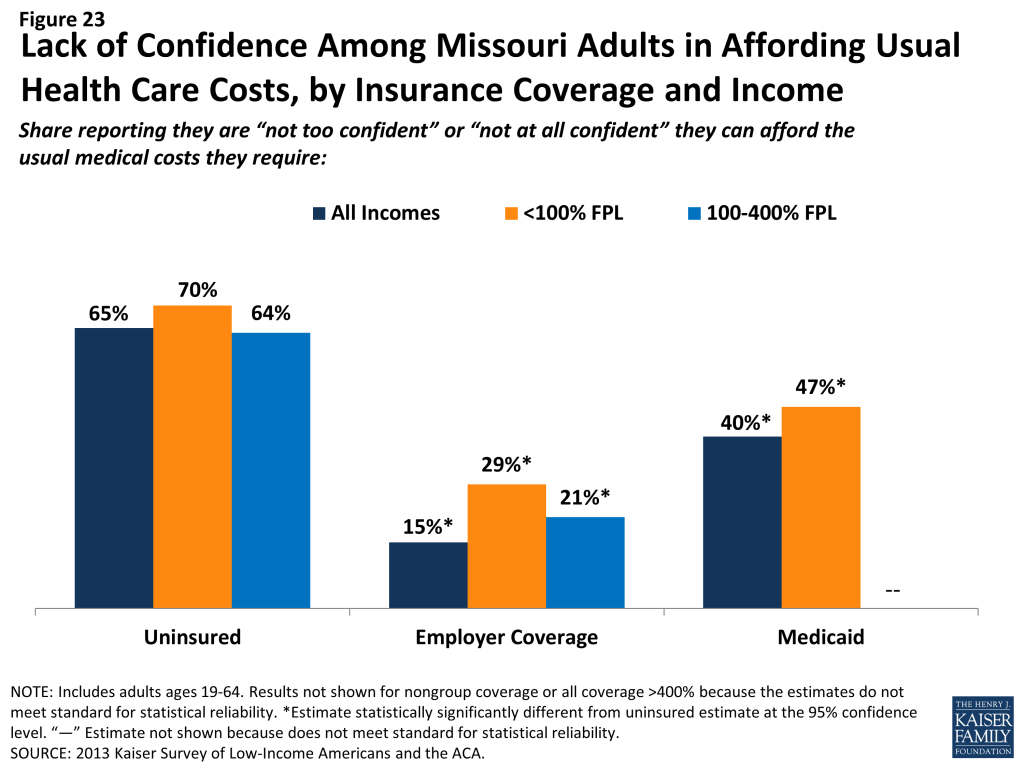

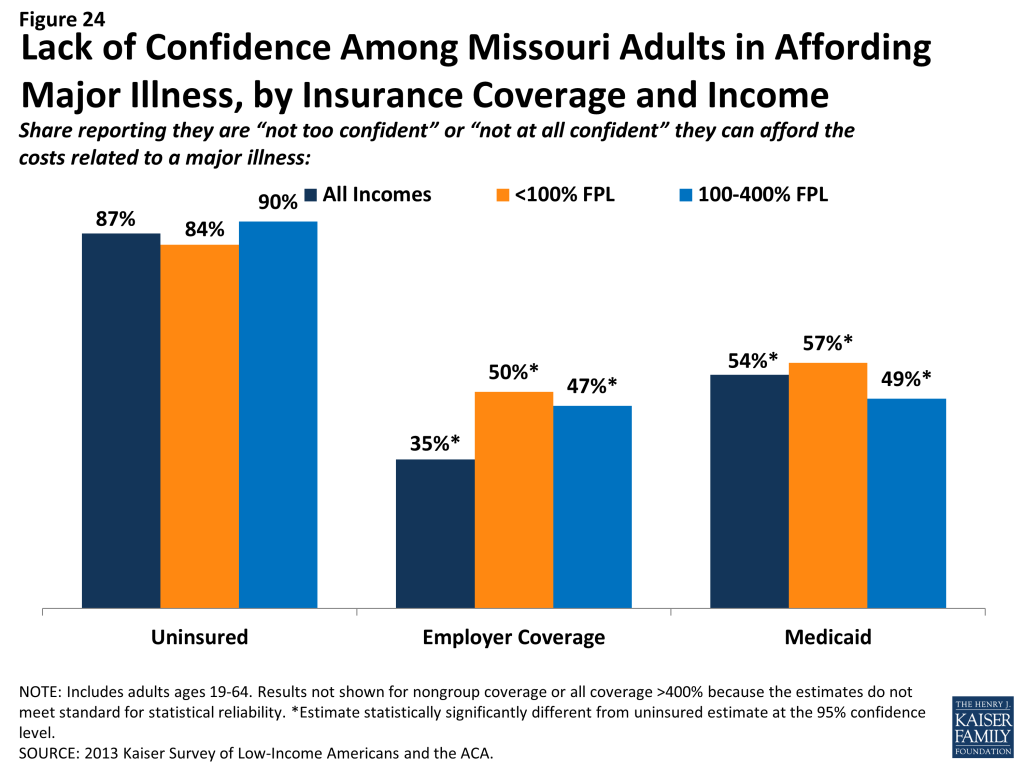

Health care costs pose a challenge for poor and moderate-income families in Missouri, even if they have insurance coverage. Even among those with insurance, health care costs can be a burden, particularly for poor and moderate-income adults. Over three in ten (36%) poor and moderate-income adults in Missouri who are covered by employer coverage report that their share of the premium is somewhat hard or very hard for them to afford, and 62% of moderate-income adults in Missouri with nongroup coverage report difficulty paying their premiums. Health care costs translate to medical debt for many poor adults, and these medical bills can cause serious financial strain. Notable shares of poor insured adults also report that they lack confidence in their ability to afford health care, given their current finances and health insurance situation.

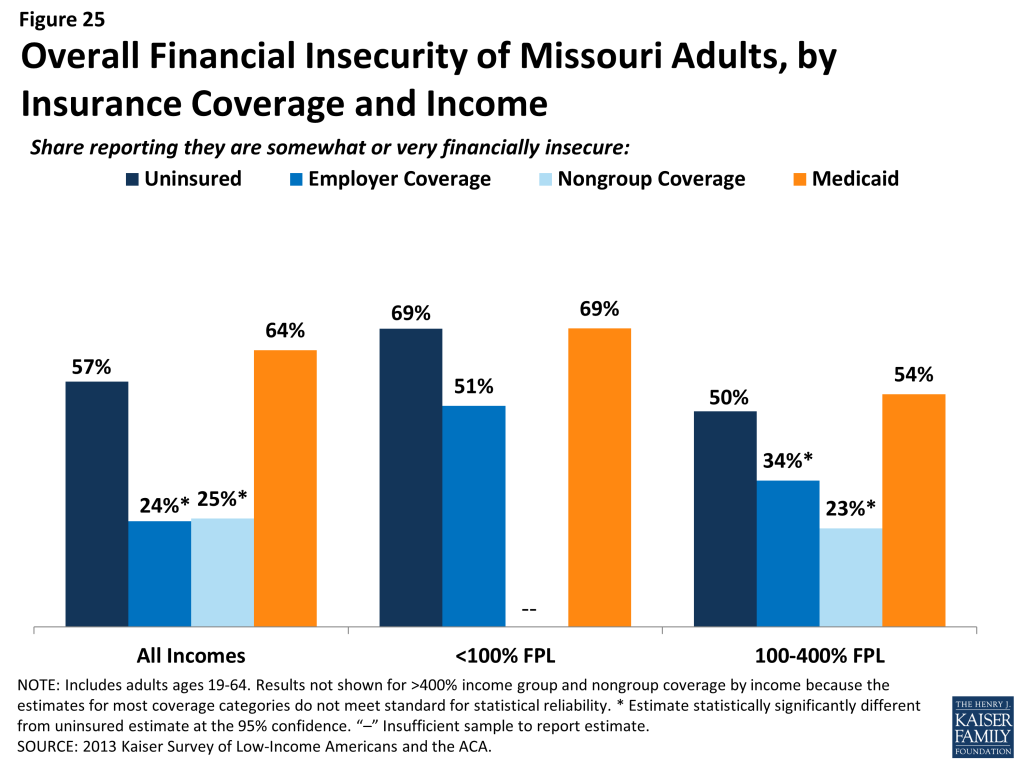

Poor families face fragile financial circumstances. Poor and moderate-income adults in Missouri across coverage groups report not being financially secure. However, adults who are poor and uninsured or covered by Medicaid are particularly vulnerable to financial insecurity even outside of health care. General financial insecurity translates to concrete financial difficulties in making ends meet. Uninsured adults and those enrolled in Medicaid are more likely than privately-insured adults to have difficulty paying for other necessities, such as food, housing, or utilities, with 49% of the uninsured and 61% of those on Medicaid reporting such difficulty compared to 20% of those with employer coverage and 25% of those with nongroup coverage. While poor adults across the coverage spectrum report high rates of difficulty paying for necessities, those with employer coverage report the lowest rates in this income group. These individuals may have stronger or more stable ties to employment than their counterparts with other or no insurance coverage. Higher rates of financial insecurity among Medicaid enrollees may reflect Medicaid eligibility rules, which targeted very vulnerable adults.

Informing ACA Implementation: Both insured and uninsured poor adults in Missouri struggle with medical bills and debt, and assistance with premium costs and, for some, cost-sharing, and limits on out-of-pocket costs under the ACA have the potential to ameliorate the financial issues associated with the cost of health care. Many uninsured poor adults will continue to face medical bills and debt as they are likely to remain uninsured without a Medicaid expansion. However, given survey findings that many poor insured Missourians continue to face financial challenges related to health care, it will be important to track whether there are ongoing financial barriers as people enroll in coverage and seek care. While insurance coverage can provide financial protection in the event of illness or injury, it is not curative of all of the financial burdens faced by poor families. Given their overall situation, health insurance alone may not lift poor Missourians out of poverty, and many poor Missouri adults may continue to face financial challenges even after gaining coverage.

Report: Introduction

In January 2014, the major coverage provisions of the 2010 Affordable Care Act (ACA) went into full effect in Missouri and across the country. These provisions include the creation of a new Health Insurance Marketplace where moderate income families can receive premium tax credits to purchase coverage and, in states that opted to expand their Medicaid program, the expansion of Medicaid eligibility to low-income adults. In Missouri, the federal government is operating the Marketplace, as the state opted not to run its own. In addition, as of March 2014, Missouri had not expanded its Medicaid program, known as MO HealthNet, leaving many poor uninsured adults in Missouri who would have been newly-eligible for Medicaid without a coverage option (referred to as the coverage gap). However, there is no deadline for states to opt to expand Medicaid, and Missouri may choose to do so at a later date, expanding the potential of the ACA to reach many of the 800,000 uninsured Missourians.

Though ACA implementation is underway and people are already enrolling in coverage, policymakers continue to need information on the uninsured population. Reports of difficulties in enrolling in coverage, continued confusion and lack of information about the law point to challenges in the early stages of implementation, and information about the population targeted for coverage expansion can inform efforts to address these difficulties. In addition, because Missouri could still opt to expand its Medicaid program, it is important to have detailed data on the population that could benefit from such a coverage expansion. Specifically, information on poor and moderate–income adults’ experiences with health coverage, current patterns of care, and family situations can provide insight into some of the challenges that are arising in the first months of coverage and highlight the potential impact of gaining coverage on poor and moderate- income adults.

Based on findings from the 2013 Kaiser Survey of Low-Income Americans and the ACA, this report provides a snapshot of health insurance coverage, health care use and barriers to care, and financial security among insured and uninsured adults in Missouri at the starting line of ACA implementation and discusses how these findings can inform early implementation. The survey, conducted between July and September 2013, is a nationally representative survey that also includes a state-representative sample of over 1,800 nonelderly (ages 19-64) adults in Missouri. It was designed to focus on people targeted for financial assistance under the ACA and includes nonelderly adults with low incomes (< 138% FPL, or about $27,000 for a family of three in 2014) or moderate incomes (139-400% FPL, between approximately $27,000 and $79,000 for a family of three), as well as a comparison group with incomes over 400% FPL. Since Missouri has not expanded Medicaid coverage to adults with incomes <138% of FPL, we chose to present the findings among adults with incomes <100% FPL (most of whom will fall into the “gap population” that is ineligible for subsidies or coverage), or about $20,000 for a family of three in 2014, 100%-400% FPL (Marketplace subsidy eligible), and >400% FPL to better reflect coverage eligibility of uninsured Missouri adults.

The survey includes adults with employer coverage, nongroup, Medicaid, and other sources of coverage, as well as those with no health insurance. The Missouri component of the survey and report on its findings complements a report on similar findings for the nation.6 This survey and report provides new data to help policymakers further understand early challenges in implementing health reform and assist outreach and enrollment workers, health plans, and providers and health systems. The survey also provides a baseline for future assessment of the impact of the ACA on health coverage, access, and the financial security of poor and moderate-income individuals in Missouri. A detailed explanation of the methods underlying the survey and analysis is available in the Methods section of the report.

Report: Background: The Challenge Of Expanding Health Coverage In Missouri

Lack of insurance coverage has been a longstanding policy challenge both nationwide and in Missouri. Not having health insurance has well-documented adverse effects on people’s use of health care, health status, and mortality, as the uninsured are more likely to delay or forgo needed care leading to more severe health problems.7 Lack of insurance coverage also has implications for people’s personal finances, providers’ revenue streams, and system-wide financing.8 ,9 ,10 Because public coverage has been extended to many children and Medicare covers nearly all of the elderly, the vast majority of uninsured people are non-elderly adults.

Missouri is home to over 800,000 uninsured nonelderly individuals, or 16% of the nonelderly population in the state.11 While the uninsured rate is lower than the national rate of 18%, the state’s uninsured population faces unique challenges. Primary care access is an issue for many state residents – over one in three people in Missouri live in a primary care Health professional shortage area (HPSA), limiting access to health care services.12 Missouri also has a substantial rural population, about 37% of the state.13 The rural population faces higher poverty rates than the urban population, and many rural families have limited access to employer coverage.14 The rural population also faces unique health care access issues: almost all rural counties are HPSAs, and lack of access to hospital and specialty services forces many rural residents to travel long distances to obtain care.15 Despite a significant rural population, a large percentage of the uninsured population in Missouri resides in two of the largest metro areas – St. Louis and Kansas City.16 Additionally, in St. Louis, over half of the city’s residents and over 40% of residents in Kansas City identify as a race other than White.17 Missouri is also surrounded by four states that have expanded Medicaid, creating a geographic inequality of health coverage.18

Medicaid provides health care coverage to may poor and low-income individuals. However, historically eligibility for Medicaid was restricted to specific categories of poor and low-income individuals, such as children, their parents, pregnant women, the elderly, or individuals with disabilities. In many states, including Missouri, adults without dependent children were ineligible regardless of their income. All states previously expanded eligibility for children to higher levels than adults through Medicaid and the Children’s Health Insurance Program (CHIP), and in Missouri, children with family incomes up to 305% of poverty (about $71,800 for a family of four) are eligible for Medicaid or CHIP. As was the case before the ACA, undocumented immigrants remain ineligible to enroll in Medicaid and recent lawfully residing immigrants are subject to certain Medicaid eligibility restrictions.19 As of January 2014, Medicaid eligibility for adults in Missouri was limited to parents with incomes below 23% of poverty, or about $5,500 a year for a family of four.20 Adults without dependent children remain ineligible regardless of their income.21

The uninsured rely on safety net providers to receive needed health care services. The health care safety net in Missouri’s second largest city, St. Louis, has suffered major provider losses in the past. The city and the state have countered these losses and preserved funding through an 1115 Medicaid waiver.22 The waiver program previously provided funding to safety net providers such as health centers and clinics.23 Today, the waiver program, now known as Gateway to Better Health, provides primary and specialty care services to uninsured adults who reside within the City and County limits.24 Eligibility for the waiver includes nonelderly uninsured adults ages 19-64 who are not eligible for Medicaid or Medicare, who are a patient at a participating health center, have incomes below 100% of poverty. The latest model of the waiver, extended to 2015, is designed to provide coverage to uninsured adults until they are able to enroll in coverage expansions under the ACA. 25 From 2012-2013, Gateway provided coverage to more than 28,000 uninsured adults in the St. Louis area who received 47,000 primary and dental visits as well as more than 28,000 specialty and diagnostic care visits.26 The program also provided care that prevented at least 50,000 emergency room visits in 2012.

Health Reform in Missouri

To address the challenge of the uninsured, the Affordable Care Act (ACA) includes an expansion of Medicaid and the creation of new Health Insurance Marketplaces. With the Supreme Court ruling in June 2012, the Medicaid expansion became optional for states, and as of March 2014, Missouri had opted not to expand its Medicaid program. This decision has created a “coverage gap” among poor adults. Under the ACA, people with incomes between 100% and 400% of poverty may be eligible for premium tax credits when they purchase coverage in a Marketplace. Because the ACA envisioned low-income people receiving coverage through Medicaid, people below poverty are not eligible for Marketplace subsidies. Thus, some adults in Missouri will fall into a “coverage gap” of earning too much to qualify for Medicaid but not enough to qualify for premium tax credits. People in the coverage gap are ineligible for financial assistance under the ACA, while people with higher incomes will be eligible for tax credits to purchase coverage.

In Missouri, about 23% of the uninsured fall into a coverage gap of earning too much money to qualify for Medicaid, but not enough to qualify for premium tax credits in the marketplace.27 These individuals have incomes below 100% of poverty. A small number of uninsured adult parents (4% of the uninsured in the state)28 are eligible for Medicaid in Missouri under existing eligibility pathways in place before the ACA. Not all eligible individuals are enrolled in Medicaid due to lack of knowledge about their eligibility and additional enrollment barriers. While the uninsured poor can purchase unsubsidized coverage in the Marketplace, they are unlikely to find coverage that is affordable.

In Missouri, the federal government is operating the Marketplace. Missouri voters passed a ballot measure blocking an Executive Order to establish a state-based Marketplace, so Missouri defaulted to a federally facilitated Marketplace.29 Voters also passed a ballot measure in 2012 prohibiting state officials from providing assistance toward establishing or operating a state-based Marketplace, and Missouri has also returned almost all of its Marketplace grant funding.30

While the state is not operating its own Marketplace or expanding Medicaid, there is some state activity around the ACA. Changes to the Medicaid enrollment process occurred in 2014, regardless of expansion decisions. Missouri must make Medicaid determinations based on new modified adjusted gross income (MAGI) eligibility levels. As of December 2013, Missouri’s MAGI conversation was in progress.31 The ACA also established a streamlined enrollment process for all states that allows people to use one single application for Marketplace or Medicaid coverage. Individuals are able to apply for coverage through HealthCare.gov, the state Medicaid/CHIP website, in person, on the phone, or through the mail. In addition, Medicaid eligibility determinations will now use verification based on existing data sources such as Social Security Administration data, rather than requiring families to provide paper documentation.32

Governor Jay Nixon (D), who supported state expansion of Medicaid, continues to support the expansion.33 While the legislature opposes the Medicaid expansion, efforts are currently underway in the legislature to find alternative ways to cover the uninsured and expand Medicaid, such as placing work requirements on Medicaid recipients or requiring monthly premiums.34 However, a recent report from the Missouri Department of Economic Development (state agency) indicated that expanding Medicaid would create 24,000 jobs in the state and bring in $9.9 billion in new wages and $402 million in state revenue over eight years.35

The impact of the expansion will also be greatest among those with the highest need. Additional research has also indicated that if Missouri expanded Medicaid, the most dramatic impact would be in rural areas – 31% of the uninsured population would gain coverage compared to 26% in St. Louis and 27% in Kansas City (Missouri’s two largest cities).36 Many advocates in the state, including the Missouri Hospital Association, continue to push lawmakers to adopt the Medicaid expansion.

Based on past evaluations of coverage expansions, targeted outreach and enrollment strategies are essential for reaching eligible populations. In Missouri, prior to open enrollment, the state legislature passed legislation creating extensive requirements for outreach and enrollment workers, also known as navigators, who receive federal funding to enroll people in coverage.37 These requirements, also passed in several other states, were considered prohibitive and were subsequently challenged in court. The regulation was recently struck down by a federal judge in January 2014.38 Regardless of the ruling, in February 2014, the Missouri State Senate passed legislation that requires navigators to pass exams, secure bonds, and pass background checks.39 Despite a lack of funding, advocates and organizations in the state are actively trying to enroll those who are eligible for coverage. Cover Missouri, a coalition led by the Missouri Foundation for Health, organized enrollment events throughout the state to reach and enroll Missourians in Medicaid or a Marketplace plan.40

The federally-facilitated Marketplace (FFM) for Missouri began accepting applications for coverage on October 1, 2013 through HealthCare.gov. Numerous issues with the website were initially experienced by individuals attempting to gain coverage, but many of those issues have since been resolved.41 The FFM also makes assessments of Medicaid eligibility based on pre-ACA levels, but the state makes the final determination after receiving the information.

As of February 1, 2014, over 50,000 Missourians have selected a health plan in the Marketplace, and about 27,000 were determined eligible for Medicaid and CHIP through the Marketplace.42 Additionally, over 6,000 people were determined eligible for Medicaid or CHIP at application through the state Medicaid agency.43 However, recent reports indicate a backlog of Medicaid determinations by the state from HealthCare.gov. The state Medicaid agency reported a sharp decline in Medicaid enrollment in 2014 due to the improving economy in Missouri, yet recent reports indicate that enrollment has dropped due to a back log in renewals and new applications.44 The state recently transitioned to accepting online applications, and the state reports the delays in eligibility determinations are due to the new systems.45 Enrollment for Medicaid coverage is continuous throughout the year and does not end with open enrollment (March 31, 2014).

A Profile of The Uninsured in Missouri

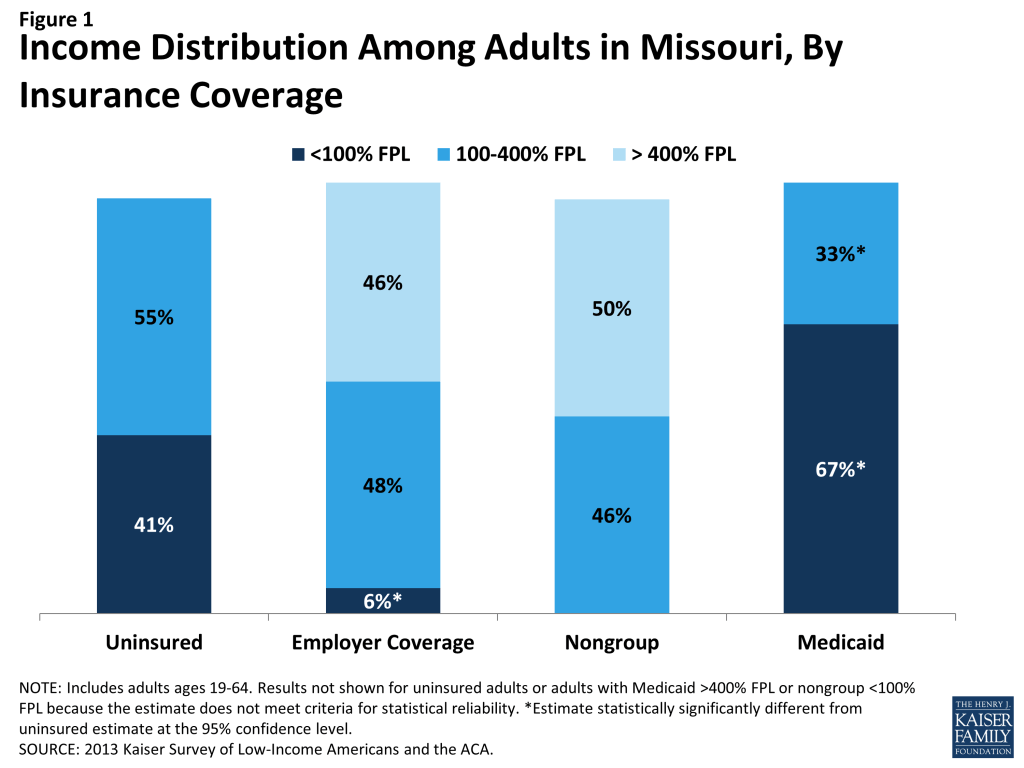

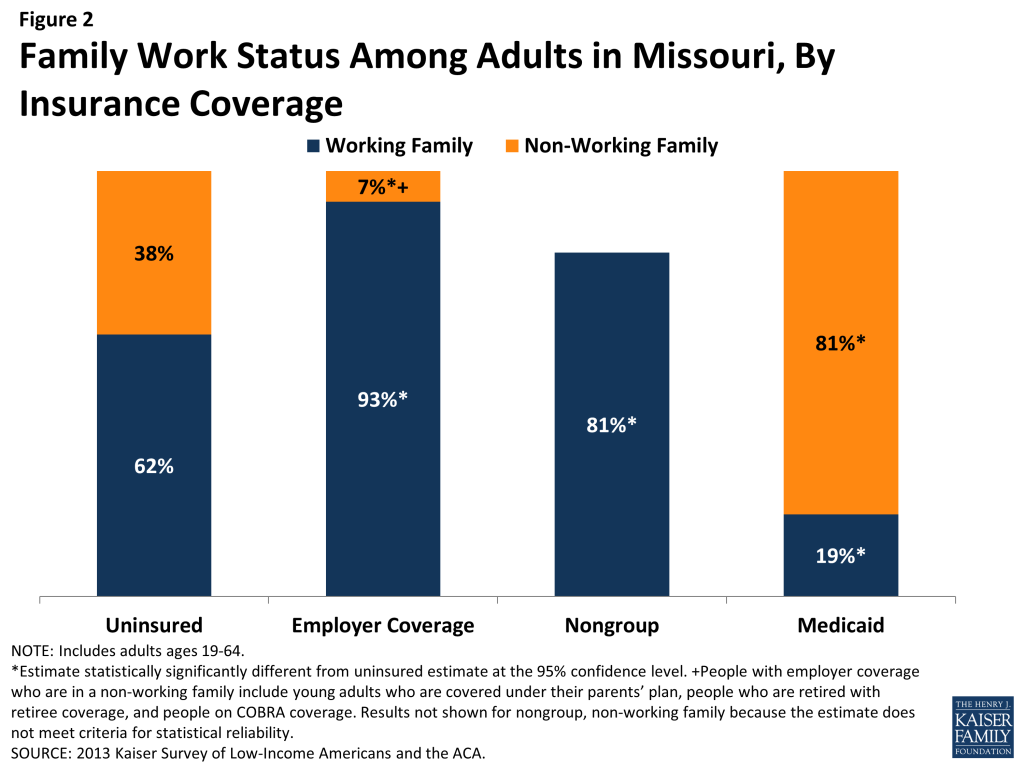

Barriers to coverage in the past and state demographics are reflected in the characteristics of the uninsured population in Missouri. For example, 41% of uninsured adults are poor (that is, living below the poverty line) and generally not eligible for coverage expansions, in contrast to 6% of adults with employer coverage (Figure 1 and Appendix Table A1). Adults with Medicaid are the most likely of any coverage group to be poor, reflecting the fact that adult income eligibility is limited. Further, the majority of uninsured Missourians live in families where they or their spouse are working (62%) (Figure 2). However, not surprisingly, uninsured adults in Missouri are less likely than adults with employer coverage or nongroup to be in a working family.

Uninsured adults in Missouri also differ from insured adults with regards to demographic characteristics, often reflecting an association with income or work status. Uninsured adults are likely to be younger than insured adults, as younger adults have lower incomes and looser ties to employment than older adults. Seven in ten (70%) uninsured adults are ages 19-44 compared to 52% of adults with employer coverage and 56% with Medicaid (Appendix Table A1). There also are significant racial and ethnic differences in health coverage among nonelderly adults, primarily reflecting differences in income by race/ethnicity. For example, uninsured adults are more likely to be Black, Non-Hispanic (14%) than adults with employer coverage (6%) but less likely than adults with Medicaid (23%).

As efforts continue to reach, educate, and enroll individuals into health coverage under the ACA, it is important to remember who the ACA aims to help and how their characteristics and previous interactions with the health system may inform efforts to connect with them. The demographics of the uninsured also highlight the population who is likely to remain uninsured without a Medicaid expansion and will likely continue to need services provided by the safety net.

Report: I. Patterns Of Coverage And The Need For Assistance

Coverage Dynamics among the Insured and Uninsured

Health insurance coverage is dynamic, and every year thousands of Missourians gain, lose, or change their health coverage. However, for most uninsured adults in Missouri, lack of coverage is a long-term issue that spans many years. Many uninsured adults in Missouri reported trying to obtain coverage in the past but were unsuccessful due to barriers such as ineligibility for public coverage or high costs of private coverage. Under the ACA, some uninsured are projected to gain coverage as those barriers are removed, but some may continue to experience gaps or changes in coverage.

For most currently uninsured adults in Missouri, lack of coverage is a long-term issue.

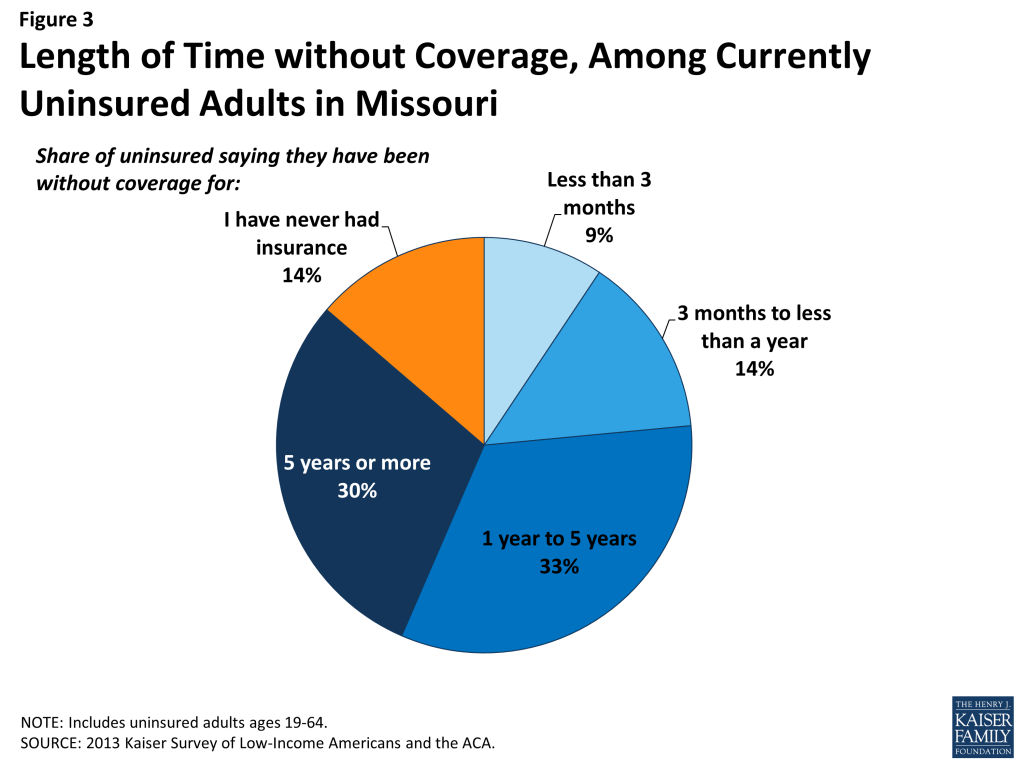

While some people lack health insurance coverage during short periods of unemployment or job transitions, for many uninsured adults in Missouri, lack of coverage is a chronic problem. The survey shows that a large share of uninsured adults in Missouri have been without insurance for a very long period of time: 43% reported being uninsured for 5 years or more, including 14% of the uninsured who reported that they have never had coverage in their lifetime (Figure 3). Of note, almost one in five (18%) poor uninsured adults (<100% FPL) reported never having coverage in their lifetime, and these adults will likely remain uninsured without a Medicaid expansion (see Appendix Table A2). The length of time adults have been uninsured does not differ significantly by income in Missouri.

It is important for policymakers in Missouri implementing coverage expansions on the Marketplace and considering a Medicaid expansion to be aware that people targeted by the ACA have varying levels of experience with the insurance system. While some previously had coverage, a substantial share of uninsured adults in Missouri has been outside the insurance system for quite some time. The long-term uninsured may require targeted outreach and education efforts to link them to the health care system and help them navigate their new health insurance.

Many uninsured adults in Missouri report trying to obtain insurance coverage in the past, but most did not have access to affordable coverage.

The uninsured report a desire to obtain coverage, but prior to implementation of the ACA in Missouri, options for coverage—particularly for the poor or moderate-income—were limited. The vast majority of uninsured adults in Missouri do not have access to employer coverage. More than eight in ten (83%) uninsured adults in Missouri report no access to employer coverage, either because no one in their family is working for an employer, their or their spouse’s employer does not offer coverage, or they are ineligible for that coverage (Table 1). For example, 47% of uninsured adults in Missouri are in a family without an employer, meaning both they and their spouse (if married) are either not working or are working but are self-employed. Over a quarter (26%) of uninsured adults are in a family that has an employer who does not offer coverage to any workers, and one in ten (10%) are in a family that works for an employer who offers coverage but they are ineligible for that coverage. Most are ineligible because they work part-time or are in a waiting period. About one in six (17%) uninsured adults in Missouri does have access to coverage through an employer, but the majority report that the coverage offered to them is not affordable. Notably, lack of access to employer coverage is particularly high among poor uninsured adults (91%), a group that generally will not be eligible for financial assistance in gaining coverage under the ACA.

| Table 1: Access to Employer Health Coverage Among Uninsured Adults in Missouri | ||||

| All | By Income | |||

| <100% FPL | 100-400% FPL | |||

| % | % | % | ||

| No Access to ESI | 83% | 91% | 76% | |

| No one in family has an employer* | 47% | 58% | 37%* | |

| Firm doesn’t offer coverage | 26% | 25% | 27% | |

| Not eligible for coverage | 10% | — | 12% | |

| Access to ESI | 17% | 9% | 24%^ | |

| Cannot afford premium | 13% | — | 17% | |

| Don’t think need coverage | — | — | — | |

| Some other reason | — | — | — | |

| Notes: Don’t Know and Refused responses not shown, they account for less than 4% of the uninsured population.*Individuals who are self-employed without other employment are treated as not having an employer.”–“: Estimates with relative standard errors greater than 30% are not provided.^ Estimate statistically significantly different from <100% FPL at the 95% confidence level.SOURCE: 2013 Kaiser Survey of Low-Income Americans and the ACA. | ||||

Similarly, poor and moderate-income adults reported limited access to coverage through Medicaid. While the state had expanded eligibility to children through Medicaid and the Children’s Health Insurance Program, Medicaid eligibility for adults remains very limited (see Background for more detail). In addition, some individuals who were eligible for Medicaid remained uninsured because they were not aware that they were eligible for coverage or they faced application or enrollment barriers.

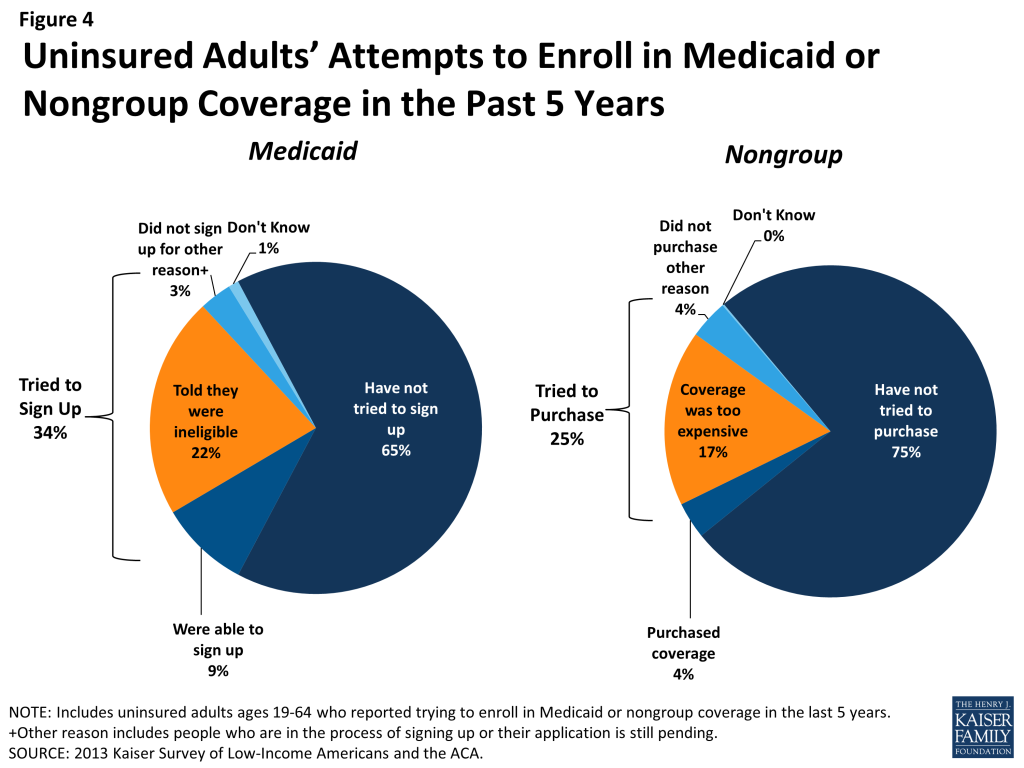

The gaps in Medicaid eligibility for adults and difficulties with the enrollment process posed barriers for many low-income adults seeking coverage. One-third of uninsured adults in Missouri (34%) reported trying to sign up for Medicaid in the past five years (Figure 4 and Appendix Table A2). The majority of adults in Missouri who tried to sign up for Medicaid were unsuccessful, and among those, most (22% of the uninsured) were unable to sign up because they were told they were ineligible (Figure 4). Notably, results are similar when looking at just poor uninsured Missourian adults. Most of the adults who were told they were ineligible will likely remain ineligible for public coverage, barring a change in their income, as Missouri has not yet expanded Medicaid under the ACA.

Prior to the ACA, there were also barriers to obtaining coverage on the nongroup, or individual, market. This type of coverage was not guaranteed in Missouri, and insurance companies could charge higher premiums for sicker or older individuals, making coverage unaffordable for many uninsured adults.46 Uninsured Missourians also report trying to obtain nongroup coverage. One in four uninsured adults in Missouri (25%) reported trying to obtain nongroup coverage in the past five years. Most of these Missourians (17% of the uninsured) did not purchase a plan because the policy they were offered was too expensive (Figure 4). Overall, almost half of uninsured adults reported trying to sign up for either Medicaid or nongroup coverage in the past five years (data not shown).

Some of the barriers to coverage that the uninsured have reported facing in the past are addressed by the ACA. Large employers (>50 workers) face penalties if they do not offer affordable coverage to their workers,47 and thousands of uninsured families are now able to purchase coverage in the Marketplace and receive premium tax credits to reduce the cost. Insurers are no longer able to deny coverage based on health status and are limited in what they charge people based on age, location, and tobacco use status. However, some uninsured adults may continue to face barriers to coverage. Missouri chose not expand Medicaid in January 2014, leaving many of these barriers in place for poor uninsured adults. Further, as was the case before the ACA, undocumented immigrants remain ineligible to enroll in Medicaid or Marketplace coverage, and recent lawfully residing immigrants are subject to certain Medicaid eligibility restrictions. Less than 2 percent of the uninsured in Missouri are undocumented immigrants (data not shown).

For those who are eligible for assistance in the Marketplace, education efforts regarding new coverage options are important, as three in four uninsured adults (76%) in the income range for premium tax credits reported knowing only a little or nothing at all about the Marketplace.48 People who have attempted to obtain coverage in the past may be unaware that rules and costs have changed under the ACA. Outreach and education will be needed to inform people that eligibility rules have changed and that financial assistance is available to offset the cost of coverage.

Health coverage is not always stable.

For most insured adults in Missouri, coverage is continuous throughout the year and over time. However, when accounting for both insured people with a gap in their coverage and uninsured people who recently lost coverage, the survey indicates that sizeable shares of adults in Missouri lose or gain coverage over the course of a year.

Among Missouri adults who were insured at the time of the survey, 8% reported being uninsured at some point in the past year (see Table 2), and those who had a gap in coverage were uninsured for over half the year (6.9 months) on average (data not shown). Further, some currently uninsured adults had coverage at some point within the past year. Among uninsured adults in Missouri, nearly one in four (23%) reported having lost coverage within the last year. Among both those with a gap in coverage or who recently lost coverage, the majority reported that they most recently had employer coverage (data not shown).

In addition to those who lose or gain coverage over the course of a year, many adults in Missouri who have coverage throughout the entire year have a change in their health insurance plan. Among adults with insurance coverage, 11% had coverage for the entire year but reported that they had a change in their coverage (Table 2). Coverage changes may be due to a number of different factors including changes in employment, changes in eligibility for public programs, or simply a change in plan or insurance carrier. The most common reasons for a change in coverage appear to be related to changes in employment or changes in plans during open enrollment, as most Missourians with a coverage change reported changing from an employer plan to another employer plan.

| Table 2: Coverage Dynamics Among Insured and Uninsured Adults In Missouri, by Income and Current Coverage | |||||||||

| All | By Income | By Current Coverage | |||||||

| <100% FPL | 100-400% FPL | >400% FPL | Employer | Nongroup | Medicaid | ||||

| % | % | % | % | % | % | % | |||

| Insured Adults | 100% | 100% | 100% | 100% | 100% | 100% | 100% | ||

| Gap in Coverage in Past Year | 8% | 21% | 8%^ | — | 5% | — | 23%* | ||

| Changed Coverage During Year | 11% | 8% | 13% | 10% | 13% | — | 6%* | ||

| Same Coverage for Full Year | 81% | 71% | 79% | 85%^ | 82% | 75% | 72%* | ||

| Uninsured Adults | 100% | 100% | 100% | 100% | 100% | 100% | 100% | ||

| Uninsured Full Year | 76% | 79% | 73% | — | NA | NA | NA | ||

| Lost Coverage Within Past Year | 23% | 20% | 27% | — | NA | NA | NA | ||

| NOTES: Don’t Know and Refused responses not shown. Excludes people covered by other sources, such as Medicare, VA/CHAMPUS, or other state programs.* Estimate statistically significantly different from employer estimate at the 95% confidence level.^ Estimate statistically significantly different from <100% estimate at the 95% confidence level.”–“: Estimates with relative standard errors greater than 30% are not provided.^ Estimate is statistically significantly different from <138% FPL estimate at the 95% confidence level.SOURCE: 2013 Kaiser Survey of Low-Income Americans and the ACA. | |||||||||

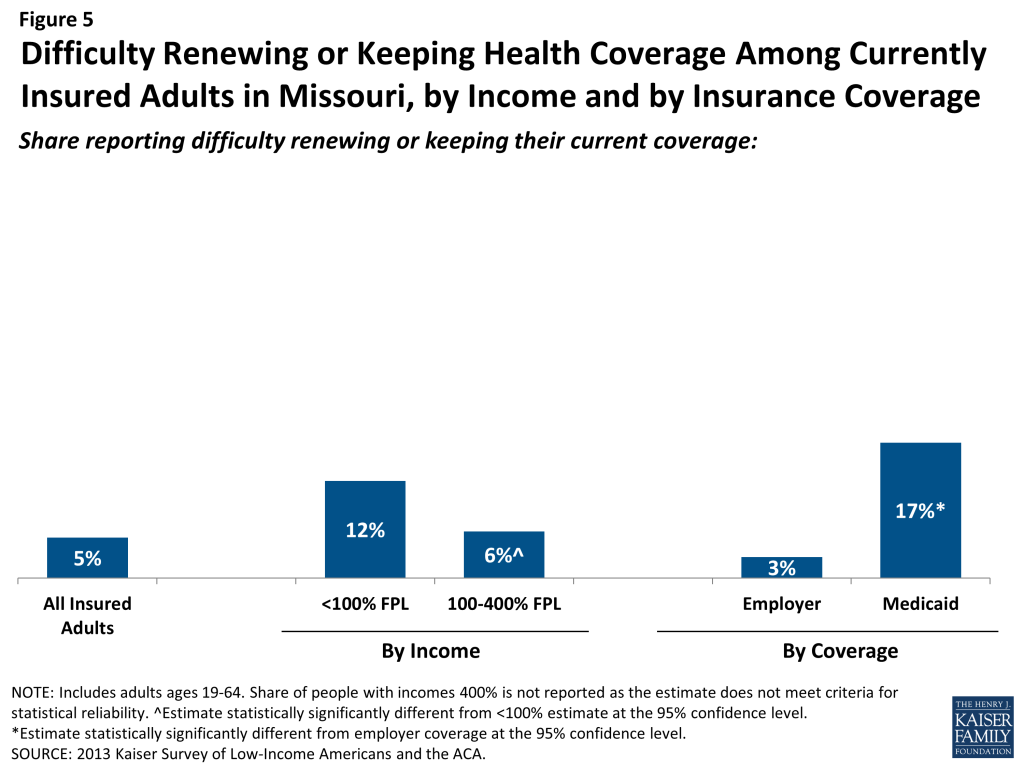

Last, a small number of insured adults in Missouri reported challenges in either renewing or keeping their coverage, another indication of instability in coverage throughout the year. Reflecting eligibility rules, adults with Medicaid are the most likely to report a challenge (17%) compared to adults with other insurance types (Figure 5). Medicaid eligibility is closely tied to income, and adults’ income may fluctuate throughout the year; adults must report changes in income that may affect their eligibility throughout the year, and poor and moderate-income people are very likely to have part-time or seasonal work that leads to income fluctuations over the course of a year. In addition, adults must renew their Medicaid coverage either in person, by phone, or online annually.

The survey findings on changes in insurance coverage during the year have implications for implementation of health reform in Missouri. While there has been much focus on enrolling currently uninsured people into Marketplace coverage, survey findings demonstrate that people will continue to move around within the insurance system throughout the year. Many people lose or gain employer coverage over the course of a year due to changing economic conditions and the delicate relationship between employment and health insurance. Further, there is some churning in insurance coverage resulting from Medicaid income eligibility limits: as adults’ income fluctuates, they may gain or lose Medicaid eligibility. Adults may also experience gaps in Medicaid coverage due to renewal requirements.

Gaps in coverage can cause people to postpone or forgo health care or accumulate medical bills,49 and changes in insurance plans may disrupt continuity of treatment. The ACA envisioned having insurance options available across the income spectrum to help people have coverage continuously throughout the year. However, poor adults in the state are likely to continue to experience gaps in coverage as they fall in and out of the coverage gap. Renewal simplifications for Medicaid coverage enacted as part of the ACA may address issues in coverage disruptions: whereas previously all adults in Missouri had to submit a paper form and documentation of income for Medicaid renewal, provisions under the ACA provide new options for them to renew on-line or by phone and use pre-populated forms when possible to reduce the need for paper documentation.50 However, even after implementation, adults are likely to experience coverage changes due to job changes or income fluctuation.

Report: Ii. What To Look For In Enrolling In New Coverage

How Poor and Moderate-Income Adults in Missouri Sign Up For and View Their Coverage

While many currently uninsured adults in Missouri have limited experience in signing up for and using health coverage, past successes and challenges of insured poor and moderate-income adults can inform the experiences of those seeking coverage under the ACA. A majority of insured Missourians do not experience problems choosing, enrolling in, and using their coverage, and this pattern holds true for both those in Medicaid and private insurance. Still, based on the experience of their insured counterparts, the uninsured population in Missouri that is being targeted by the ACA coverage expansions is likely to encounter some barriers in the process of choosing and enrolling in coverage. While the ACA aims to make the process smoother, it is likely that some challenges inherent in the complexity of health coverage will require concerted efforts to address.

While many adults in Missouri reported facing no difficulty in applying for Medicaid coverage prior to the ACA, some encountered difficulties in the process of applying for public coverage in the past.

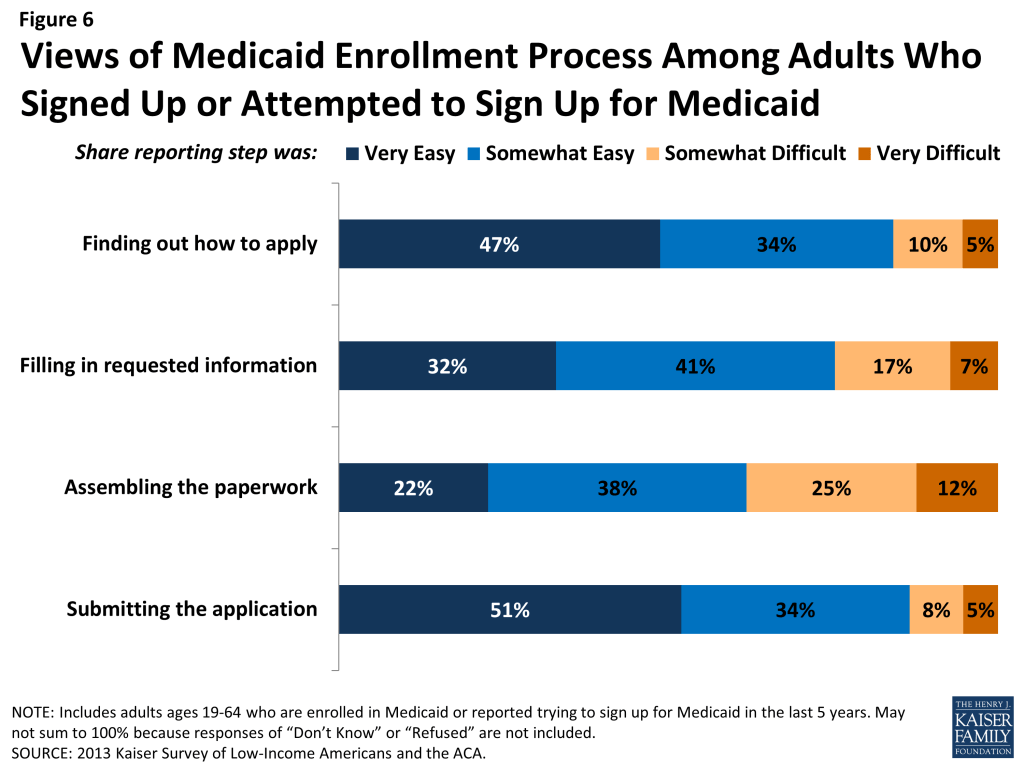

In comparison to the process for gaining coverage through an employer—which is typically facilitated by the firm or a representative and may require limited action on the part of the insured—applying for publicly-financed coverage typically requires proactive steps to gain coverage. Adults in Missouri who currently have Medicaid or who have attempted to enroll in the past five years reported little difficulty in enrolling in Medicaid. Almost half of adults (49%) who applied to Medicaid said the entire process was very or somewhat easy. However, the rest found at least one aspect of the process – finding out how to apply, filling out the application, assembling the required paperwork, or submitting the application – to be somewhat or very difficult. The most commonly reported difficulty was assembling the required paperwork, which over a third (37%) of Missourians who enrolled or applied said was somewhat or very difficult (Figure 6 and Appendix Table A3).

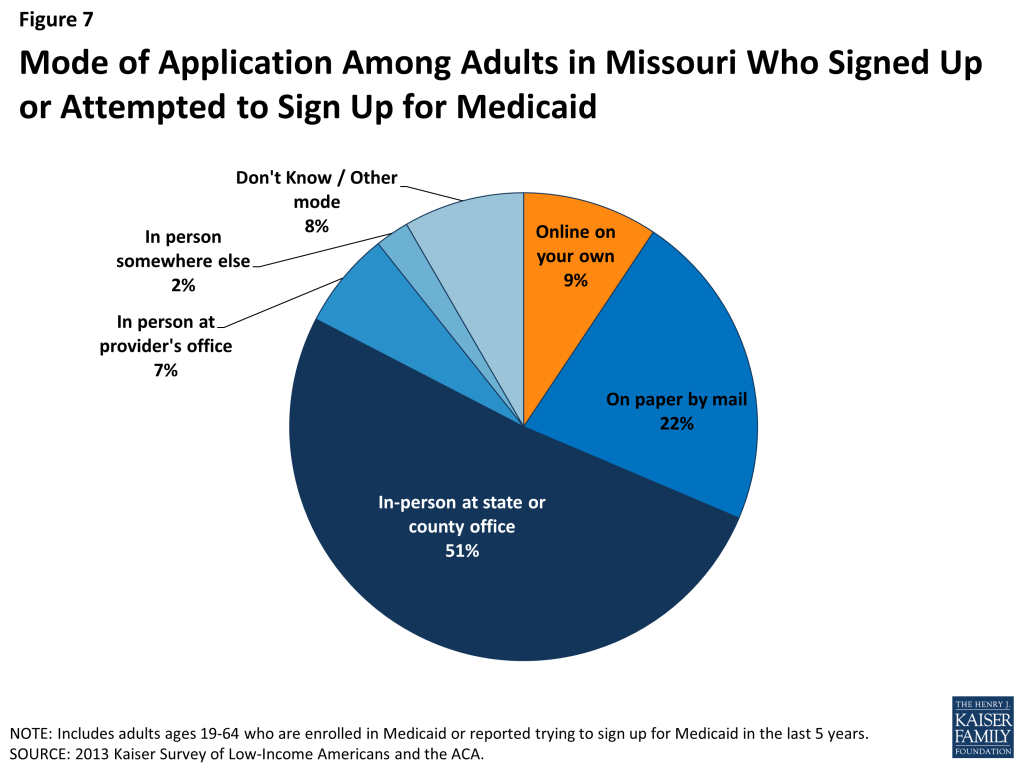

In recent years, Missouri, along with many other states, has made strides towards providing individuals multiple avenues to enroll in coverage, including through online applications to facilitate access to coverage and ease administrative burdens.51 However, more than half of Missourian adults (51%) who applied to Medicaid in the past five years reported that they did so through traditional routes—that is, in person at a state or county government office—and only 9% reported using an online application (Figure 7).

The ACA includes provisions to further simplify the application, enrollment, and renewal process for coverage in all states, regardless of whether they expand their Medicaid programs under the ACA. These requirements include the adoption of a single streamlined application that is available online, by phone, and on paper and that screens for all health coverage options; electronic transfers of accounts between agencies to facilitate transitions across health coverage programs; and reliance on trusted sources of electronic data, rather than requesting paper documentation, to verify eligibility criteria.52 As of late 2013, Missouri and other states were still in the process of implementing many of these changes and coordinating enrollment processes with the Marketplace.53 Once simplified enrollment processes are fully implemented, it is possible that people applying for MO Health Net will experience a smoother application and enrollment process than applicants have in the past.

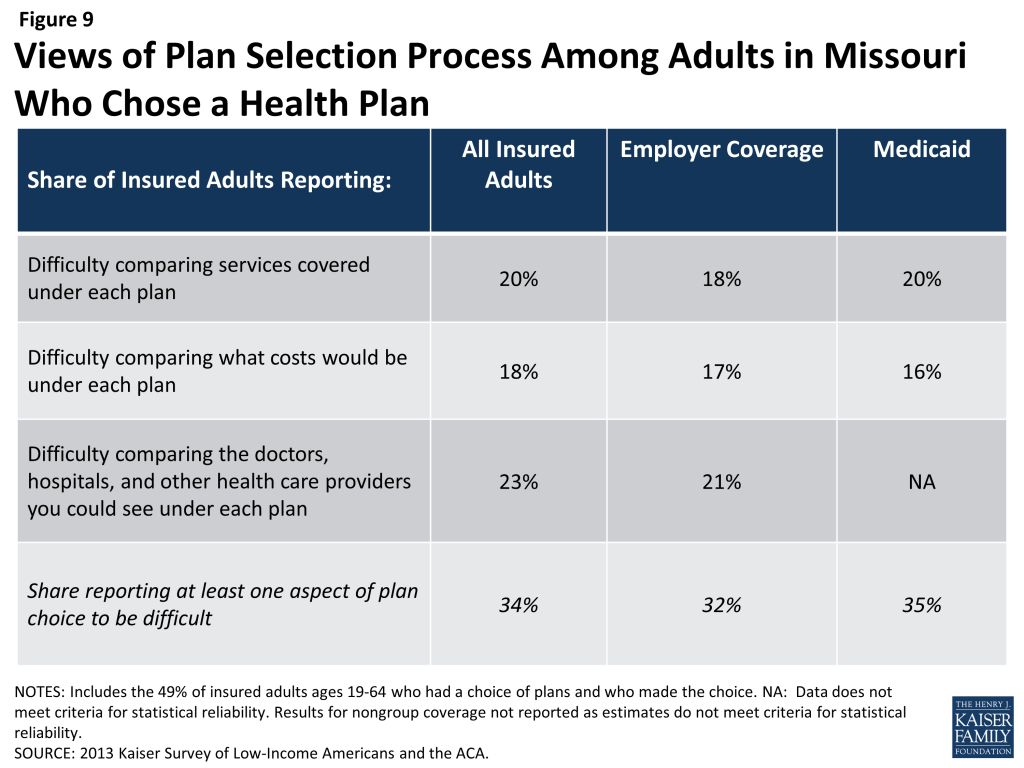

When adults with Medicaid or private insurance plan have a choice of plan, they do not always prioritize costs over other plan features in making that choice, and many find some aspect of the plan choice process to be a challenge.

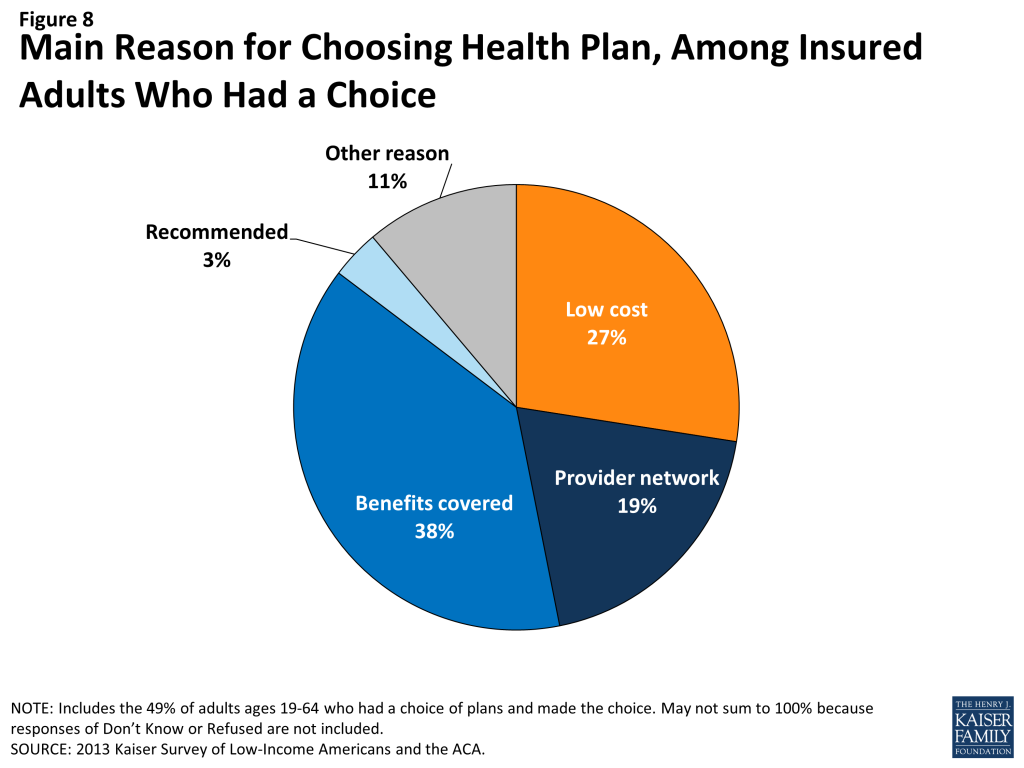

As Missourians gain coverage, many will have the option to select an insurance plan. People may chose a particular plan for a variety of reasons, including low cost, choice of providers, recommendations from friends and family, or coverage of a particular benefit. Among the 49% of insured adults in Missouri who had a choice of plans,54 a plurality (38%) reported that they chose their plan because it covered a wide range of benefits or a specific benefit that they need, roughly three in ten (27%) because their costs would be low, and 19% because of its provider network (Figure 8 and Appendix Table A4).

In choosing a plan, Missourians may face challenges in comparing costs, services, and provider networks across plans, as these factors typically varied greatly across plans in the past. In general, insured adults in Missouri reported that they did not have difficulty in comparing their plan choices, but 34% found some aspect of plan choice—comparing services, comparing costs, and comparing providers— to be difficult (Figure 9 and Appendix Table A4). Insured adults in Missouri were least likely to report difficulty comparing costs (versus providers or services) across plans (18%).

As enrollment numbers for particular plans are released and policymakers in Missouri begin to assess plan choice among new enrollees, these findings can inform evaluations of plan choice under the ACA. While the ACA requires health plans in the Marketplaces to provide a standard set of benefits and provide detailed information about what services are covered, which could make it easier for individuals to select a plan, it is important to bear in mind that, even before the ACA, insured adults faced some challenges in comparing and selecting insurance coverage. While provisions in the ACA could address these challenges, some are inherent to the complexity of insurance coverage.

Further, contrary to expectations that people may opt for the lowest cost plan,55 survey findings indicate that Missourians place value on a range of factors related to insurance, including scope of services and provider networks. Thus, assessments of whether people are choosing the optimal plan for themselves and their families will need to consider the multiple priorities that people balance in plan selection.

Overall, insured adults in Missouri reported satisfaction with their current coverage but also reported gaps in covered services and problems when using their coverage.

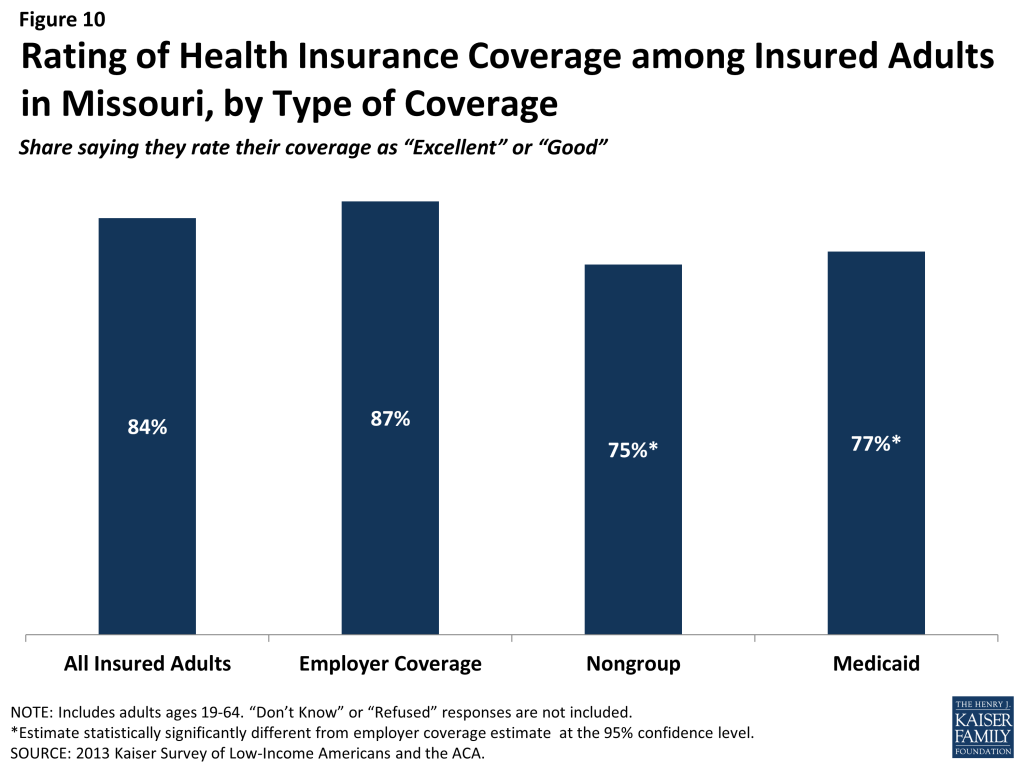

Most insured adults in Missouri reported high levels of satisfaction with their current coverage, but they also reported gaps in services that are covered by their current insurance. Eighty-four percent of insured adults in Missouri rate their coverage as excellent or good (Figure 10). Adults with employer coverage gave plans high ratings, with 87% grading their plans as excellent or good. Adults with Medicaid or nongroup coverage were less likely to give their plans high ratings, but over three-quarters in each coverage group (77% and 75%, respectively) rated their plans as excellent or good.

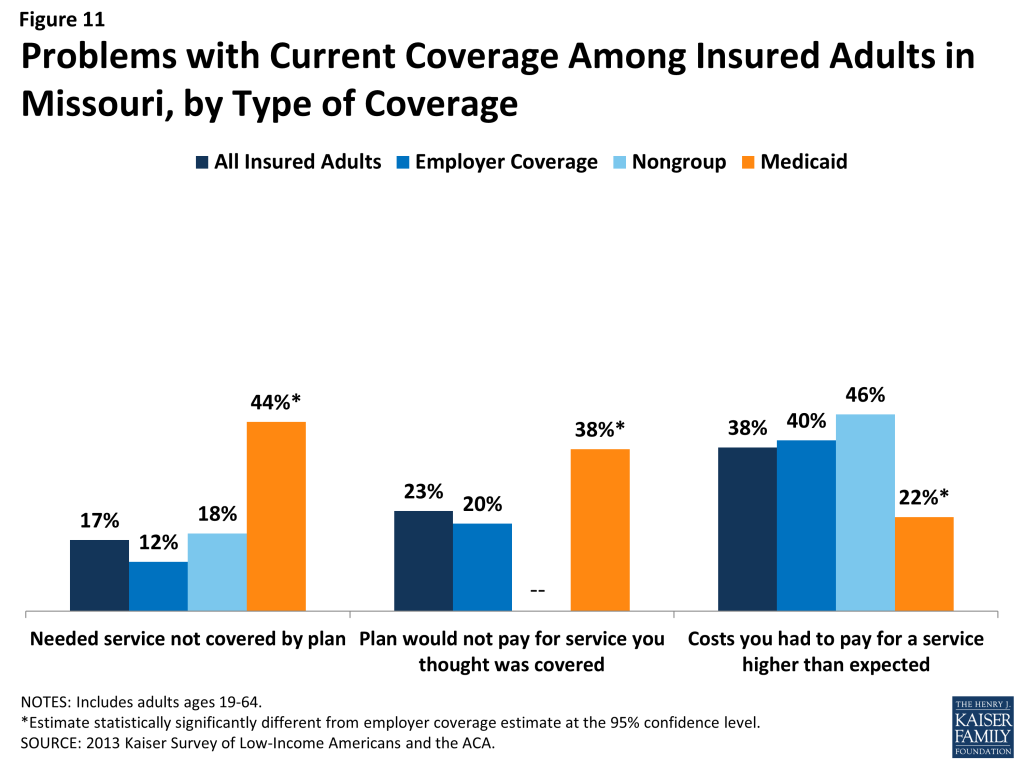

Despite the high ratings, notable shares of insured adults in Missouri reported a problem with their plan. Specifically, one in six (17%) insured adults reported needing a service that is not covered by their current plan (Figure 11 and Appendix Table A5). People with Medicaid coverage (44%) are more likely to report that their plan does not cover certain services compared to those with employer coverage (12%). The most frequently reported services people say they need but lack coverage for are ancillary services, such as dental, vision care, and chiropractor services. In private health coverage, these ancillary services are often covered under stand-alone private insurance policies that must be purchased separately from health coverage, and in Medicaid, most are not federally-required benefits, but rather are covered at state option. Lack of coverage for adult dental services in Medicaid—the most frequently reported service needed but excluded from coverage—has been a longstanding issue facing beneficiaries and providers, despite a particularly high need among the low-income population.56

Insured adults in Missouri also reported experiencing other problems with their insurance plans. Many insured adults reported facing a problem with their current insurance plan covering a specific benefit, either because they were denied coverage for a service they thought was covered (23%) or their out-of-pocket costs for a service were higher than they expected (38%). Some of these services may be over-the-counter products, which are excluded from the majority of insurance plans but which people may believe their plans should cover. Reports of these difficulties varied by insurance coverage. Missouri adults with Medicaid coverage (38%) were more likely than those with employer coverage (20%) to report they were surprised that their plan would not cover a service they believed was covered. Adults with Medicaid coverage have particularly high health needs, which could explain why they reported relatively high rates of problems. Adults with Medicaid (22%) were less likely to report facing higher costs than expected than privately insured adults (40% among those employer coverage and 46% among those with nongroup). This pattern most likely reflects the nominal out of pocket costs Medicaid beneficiaries are required to pay compared to the high cost-sharing of many private plans.

Among the goals of the ACA was ensuring that the coverage people gained provided at least a basic level of coverage and that the Marketplaces helped people navigate their insurance coverage. Thus, new coverage must include a set of essential health benefits (EHB), and participating plans in the Missouri Marketplace must report information on claims payment policies, cost-sharing requirements, out-of-network policies, and enrollee rights in plain language. These provisions may address some of the problems that insured adults in Missouri have experienced with their coverage in the past. However, many of the services that people report needing coverage for—such as dental services—are not included in the EHB. Many newly-insured Missourians may be surprised to learn that some ancillary services are not included in their plan, and education efforts will be needed to make sure people understand their coverage. In addition, some uninsured people who gain coverage may need help with plan selection, having not navigated the process before. Despite these possible challenges, most insured people—even those who reported difficulties—are overall satisfied with their coverage.

Report: Iii. Gaining Coverage, Getting Care

How New Insurance Coverage Could Change How Missourians Use Health Care

Uninsured adults in Missouri generally do not seek or receive health care services at the same rate as insured adults, even when they have a need for care. Many uninsured adults have substantial health care needs that are not monitored by a physician. Cost is the main reason uninsured Missourians do not receive care when needed, and many lack a regular provider to facilitate follow-up or ongoing care. When uninsured adults do receive care, they often have limited options. As coverage expands under the ACA, uninsured adults are likely to get care more frequently and establish relationships with providers, yet many uninsured adults will remain without a coverage option and continue to have unmet needs for care.

A large segment of the uninsured in Missouri has little or no connection to the health care system.

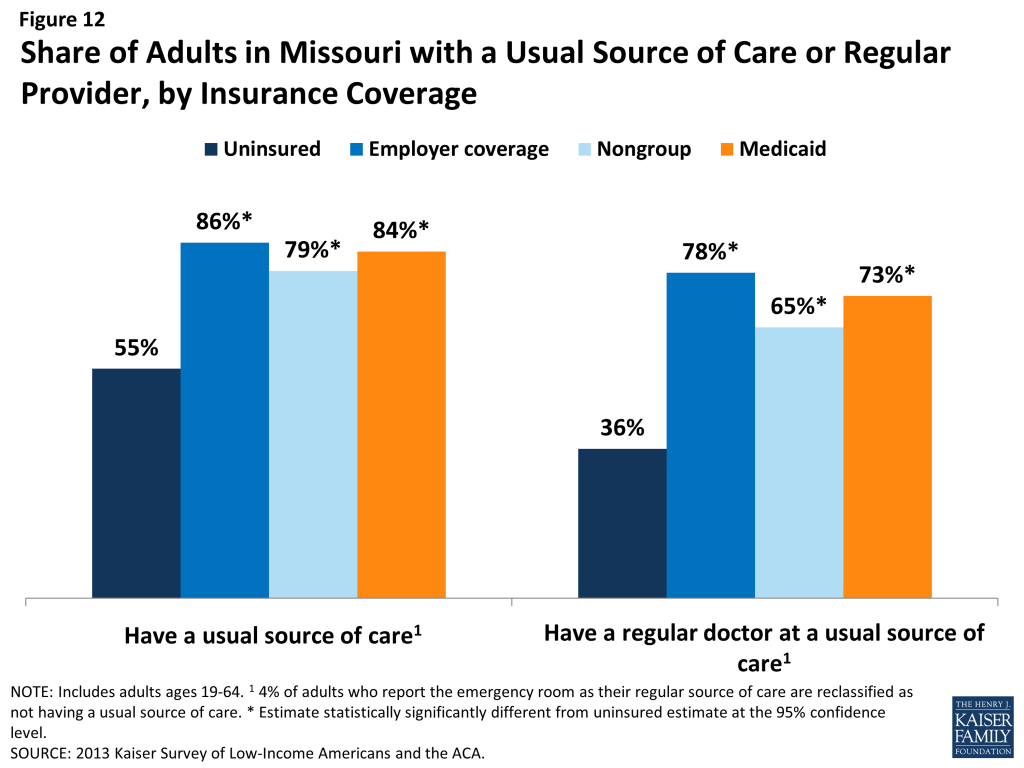

While some uninsured adults in Missouri did report receiving health care services, most reported few connections to the health care system. Slightly more than half of uninsured adults in Missouri (55%) report that they have a usual source of care, or a place to go when sick or need advice about their health (not counting the emergency room). Having a usual source of care is an indicator of being linked in to the health care system and having regular access to services. In comparison, nearly all insured adults in Missouri —86% of those with employer coverage, 79% of those with nongroup coverage, and 84% of those with Medicaid coverage— have a usual source of care (Figure 12). In addition, uninsured adults in Missouri are less likely to have a regular doctor at their usual source of care, with 36% of uninsured adults reported having a regular doctor, about half the rate of insured adults. Notably, poor uninsured adults in Missouri, those that will likely remain uninsured under the ACA, are the least likely to have a usual source of care or a regular physician (Table 3).

| Table 3: Share of Adults in Missouri with Usual Source of Care or Regular Provider, by Income and Coverage | |||||

| Uninsured | Insured | ||||

| Employer | Nongroup | Medicaid | |||

| Has a usual source of care^ | |||||

| All | 55% | 86%* | 79%* | 84%* | |

| By Income | |||||

| <100% FPL | 49% | 62% | — | 84%* | |

| 100-400% FPL | 59% | 87%* | 76%* | 82%* | |

| >400% FPL | — | 88% | — | — | |

| Has a regular provider at usual source of care1 | |||||

| All | 36% | 78%* | 65%* | 73%* | |

| By Income | |||||

| <100% FPL | 24% | 54%* | — | 72%* | |

| 100-400% FPL | 42% | 77%* | 60% | 74%* | |

| >400% FPL | — | 83% | — | — | |

| NOTES: Don’t Know and Refused responses not shown.”–“: Estimates with relative standard errors greater than 30% are not provided.^4% of adults who report the emergency room as their regular source of care are reclassified as not having a usual source of care. Excludes people covered by other sources, such as Medicare, VA/CHAMPUS, or other state programs.*Estimate is statistically significantly different from uninsured estimate at the 95% confidence level.SOURCE: 2013 Kaiser Survey of Low-Income Americans and the ACA. | |||||

This lack of a connection to the health care system leads many uninsured adults in Missouri to go without care. Six in ten uninsured adults in Missouri (60%) reported a health care visit—including hospital visits, doctor’s office or clinic visits, mental health services, or trips to the emergency room— in the past year, compared to 93% of Medicaid beneficiaries, 87% of adults with employer coverage, and 78% of adults with nongroup (Figure 13). This pattern holds across all income groups. Of particular concern is the lack of preventive visits among uninsured adults in Missouri. Three in ten (28%) of uninsured adults reported a preventive visit with a physician in the last year, compared to 75% of adults with employer coverage and 73% of adults with Medicaid (data not shown).

The survey findings reinforce conclusions based on prior research: having health insurance affects the way that people interact with the health care system, and people without insurance have poorer access to services than those with coverage.57 ,58 ,59 Thus, gaining coverage is likely to connect many currently uninsured adults in Missouri to the health care system. However, outreach may be needed to link the newly-insured to a regular provider and help them establish a pattern of regular preventive care. In addition, resources may be needed to reach out to the remaining uninsured in Missouri—including those who are in the coverage gap —to link them to the health care system and help them obtain preventive and acute health care services despite not having health insurance coverage.

Many uninsured Missourians have health needs, many of which are unmet or are being met with difficulty.

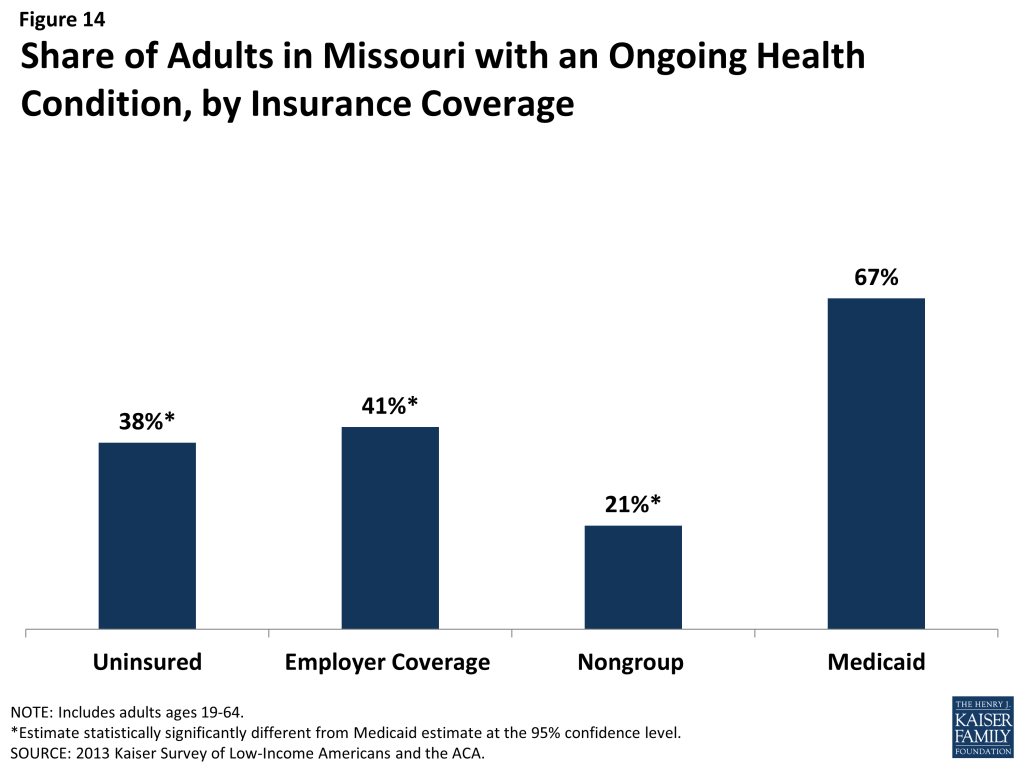

Missourians who lack health insurance still have health care needs. Nearly four in ten (38%) uninsured adults reported an ongoing health condition, compared to 21% with nongroup, and 67% with Medicaid (Figure 14). The lower percentage of adults with nongroup coverage reporting an ongoing health condition, compared to those with Medicaid or employer coverage, may reflect the ability of insurance companies to deny coverage to people with pre-existing health conditions prior to the ACA.60 In contrast, Medicaid beneficiaries are most likely to report having an ongoing health condition of all coverage groups, which reflects Medicaid’s role in caring for people with substantial health needs, such as individuals with disabilities or people who become impoverished due to high health care expenses. These findings hold across income groups (Table 4).

| Table 4: Health Status of Missouri Adults, by Income and Coverage | ||||||

| Uninsured | Insured | |||||

| Employer Coverage | Nongroup | Medicaid | ||||

| Fair or Poor Overall Health | All | 31% | 10%* | — | 52%* | |

| By Income | ||||||

| <100% FPL | 37% | — | — | 57%* | ||

| 100-400% FPL | 27% | 14%* | — | — | ||

| Fair or Poor Mental Health | All | 19% | 7%* | — | 40%* | |

| By Income | ||||||

| <100% FPL | 23% | — | — | 41%* | ||

| 100-400% FPL | 16% | 9% | — | 37%* | ||

| Have ongoing health condition that needs to be monitored regularly or needs regular care | All | 38% | 41% | 21%* | 67%* | |

| By Income | ||||||

| <100% FPL | 31% | 27% | — | 70%* | ||

| 100-400% FPL | 41% | 38% | 16%* | 63%* | ||

| Take prescription medication on regular basis^ | All | 30% | 49%* | 37% | 74%* | |

| By Income | ||||||

| <100% FPL | 21% | 29% | — | 73%* | ||

| 100-400% FPL | 34% | 47%* | 34% | 77%* | ||

| NOTES: Don’t Know and Refused responses not shown. Excludes people covered by other sources, such as Medicare, VA/CHAMPUS, or other state programs.”–“: Estimates with relative standard errors greater than 30% are not provided.^Excludes birth control.*Estimate statistically significantly different from uninsured estimate at the 95% confidence level.SOURCE: 2013 Kaiser Survey of Low-Income Americans and the ACA. | ||||||

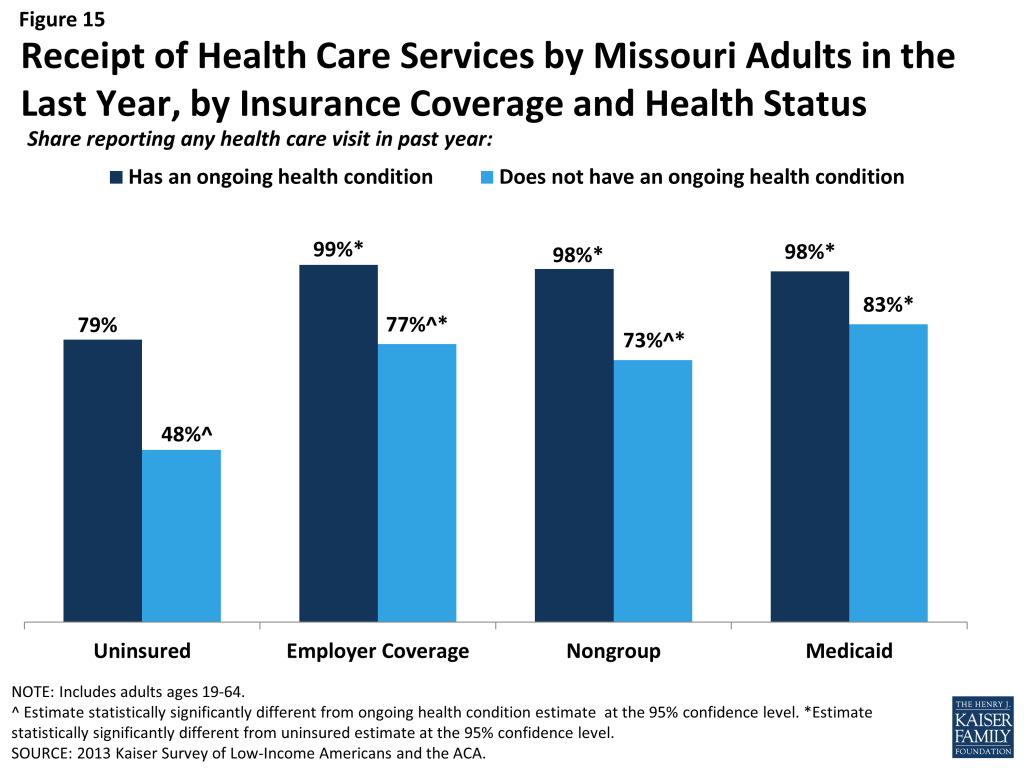

While uninsured Missourians with an ongoing health condition are more likely than those without to report receiving services (Figure 15), they are still less likely than their insured counterparts to receive care. While less than half (48%) of uninsured adults without an ongoing health condition say they received health care services in the last year, more than three-quarters (79%) of uninsured adults with a health condition received health care services. However, this rate is still lower than adults who have a health condition and have employer coverage, nongroup coverage, or Medicaid, nearly all of whom (99%, 98%, and 98%, respectively) reported receiving medical services over the course of the year.

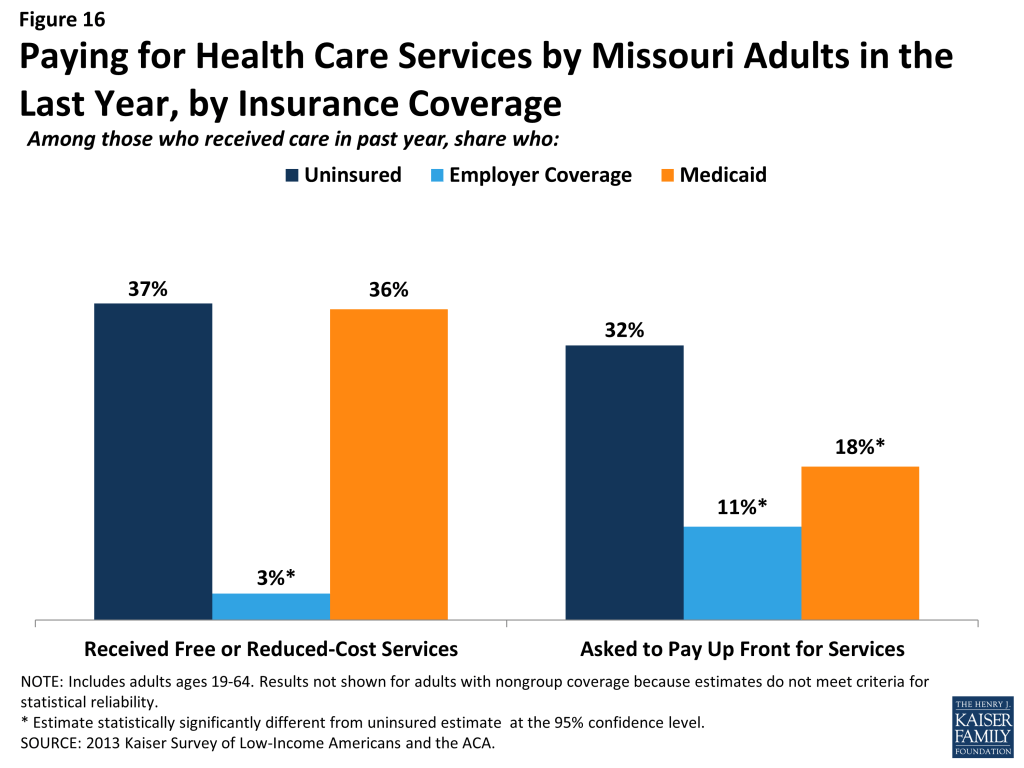

When uninsured Missourians do receive care, they sometimes receive free or reduced-cost care, though the majority does not. Among adults in Missouri who reported that they received a health care service in the past year, 37% of uninsured adults in Missouri reported receiving free or reduced cost care, versus just 3% of those with employer coverage (Figure 16). Notably, 36% of adults with Medicaid who received services reported that they received free or reduced cost care. They may have done so during a period of uninsurance in the previous year or may associate the fact that they pay little or no costs when they see a provider as receiving “free or reduced cost” care. Uninsured adults in Missouri who received care were much more likely than their insured counterparts to be asked to pay up front for care: almost one-third (32%) reported being asked to pay for the full cost of medical care (not counting copayments) before they could see the doctor or provider, compared to just 11% of those with employer coverage and 18% of adults with Medicaid. Again, adults with employer coverage or Medicaid may have experienced these issues during a period in the past year when they lacked coverage or when using a service not covered by their insurance.

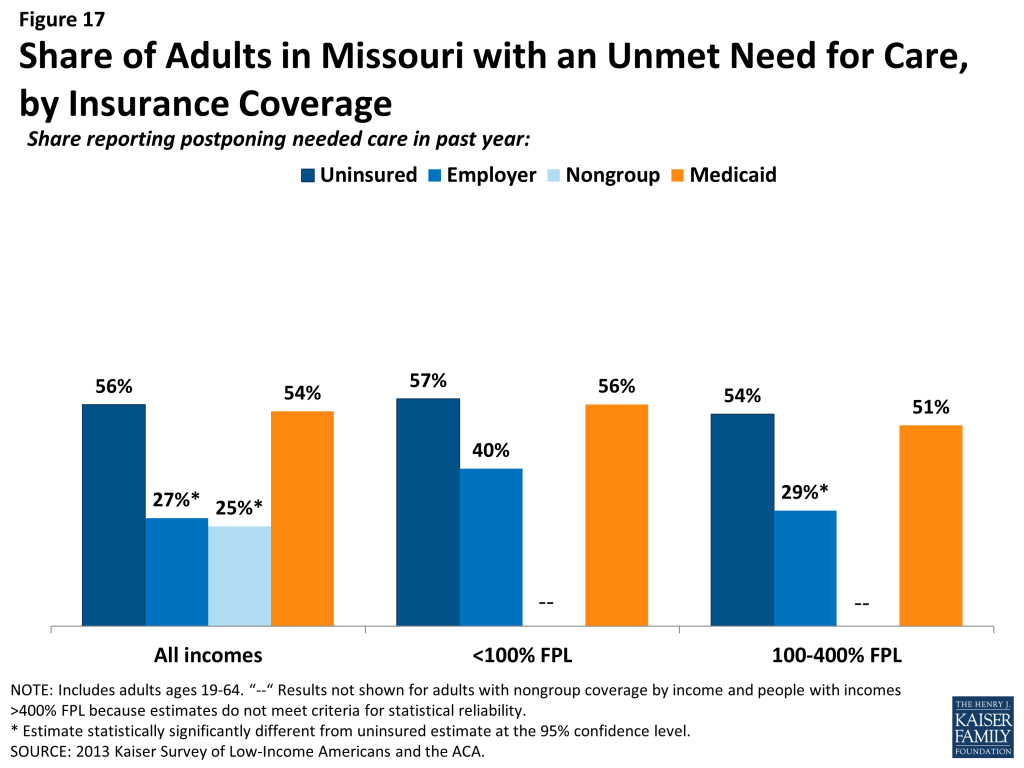

Although some uninsured and insured adults in Missouri reported receiving free or reduced cost health care services, a larger share reported an unmet need for care. More than half (56%) of the uninsured and Medicaid (54%) beneficiaries in Missouri reported needing but postponing care, compared to 27% of adults with employer coverage and 25% with nongroup, and this pattern holds across income groups (Figure 17).

The most common reason for postponing care among uninsured Missourians is cost (89%). Adults with employer coverage (57%) or Medicaid (59%) are less likely to report cost as a reason for postponing care because presumably their insurance pays most or all of that cost (Figure 18). However, adults with employer coverage or Medicaid may report postponing care due to cost if their health insurance does not cover a specific treatment that they need. Appointment availability was also reported as a significant reason for postponing care. Almost half of adults with Medicaid (49%) reported postponing care because they could not get an appointment soon enough compared to 28% of adults with employer coverage, and 16% of uninsured adults. Adults with employer coverage were twice as likely as uninsured adults to report the office not being open when they could get there as a reason for postponing. Many physicians do not have hours outside of the normal workday, so some working adults may need to take time off to get care.

Adults with Medicaid were more likely than uninsured adults to report that they postponed care because they had difficulty traveling to the doctor’s office or clinic or that they could not get an appointment soon enough. These issues may reflect problems with provider participation in Medicaid, limits on Medicaid coverage of transportation services, or transportation barriers unique to the low-income population (such as not having a car). Poor and moderate-income adults may also experience access challenges due to difficulty getting time off from work or obtaining childcare for the time when they are at the provider.

Given the health profile of currently uninsured adults in Missouri, there is likely to be some pent-up demand for health care services among the newly-covered. Health systems may see increases in adults seeking care and will need to prepare for the newly insured. As people gain coverage under the ACA, the cost barriers to health care services will be reduced, but other barriers such as transportation or wait times for appointments may remain. Low rates and low provider participation, may pose a challenge for newly-insured individuals’ ability to find a provider to treat them.61 ,62 In addition, it is important to bear in mind continuing access barriers among the population that remains uninsured under the ACA. As resources and attention shift to the newly-insured population, individuals left out of coverage expansions (such as poor adults) will continue to have health needs. The ACA included funds to expand service capacity in medically underserved areas, including expansion of community health centers, nurse-managed health centers, and school-based clinics. To meet the health care needs of both insured and uninsured individuals, it is important that these systems develop flexible treatment times and new models of care to accommodate people’s availability and expand capacity in areas where poor and moderate-income individuals reside or seek care.

Many uninsured Missourians reported limited options for receiving health care when they need it.

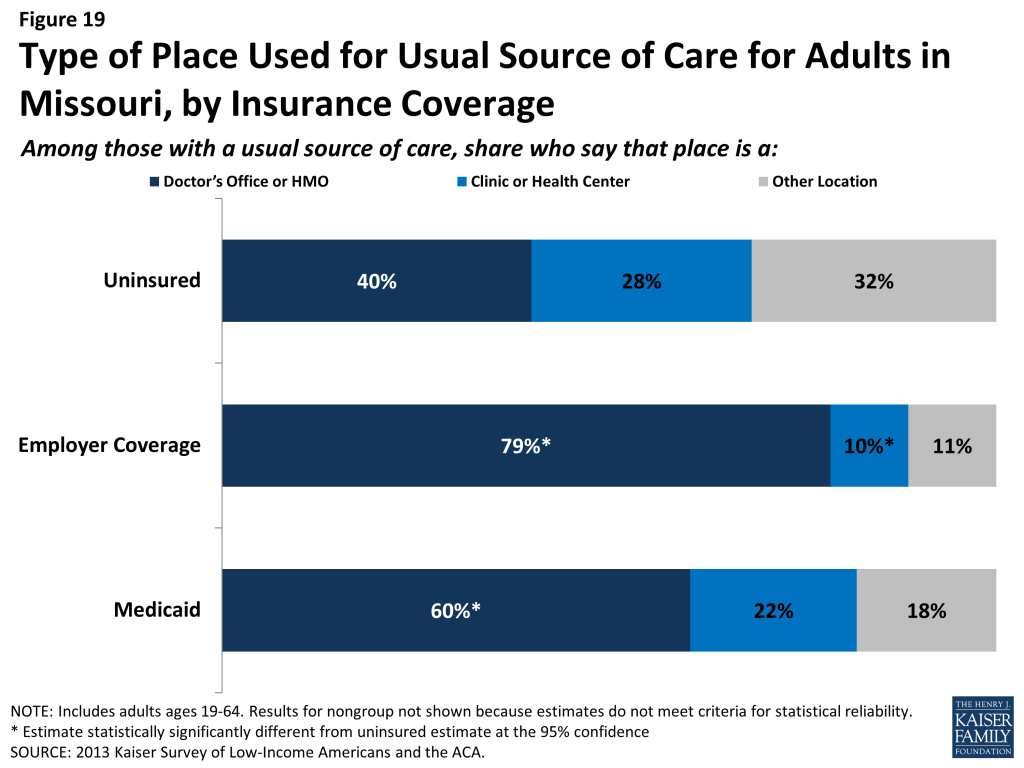

Uninsured adults in Missouri are less likely than their insured counterparts to receive care in a private physician’s office, but a physician’s office is the primary location for receiving care. Four in ten (40%) uninsured Missouri adults who have a regular source of care reported that it is a physician’s office or HMO, compared to over three-quarters (79%) of adults with employer coverage and 60% of adults with Medicaid (Figure 19). Almost one in three (28%) of uninsured adults in Missouri who have a regular source of care reported clinics or health centers as their usual source of care, almost three times as high as adults with employer coverage (10%). Notably, 12% of uninsured adults in Missouri reported the emergency room as their usual source of care – substantially higher than adults with private insurance, but lower than the rate for uninsured adults nationwide (data not shown).63