Medicaid Public Health Emergency Unwinding Policies Affecting Seniors & People with Disabilities: Findings from a 50-State Survey

Key Takeaways

Medicaid remains an important source of coverage for seniors and people with disabilities, often providing access to long-term services and supports (LTSS) not covered by Medicare or private coverage. Provisions in the Families First Coronavirus Response Act (FFCRA) require states to provide continuous coverage for Medicaid enrollees until the end of the month in which the COVID-19 public health emergency (PHE) ends in order to receive enhanced federal funding. The PHE is currently in place through October 2022, and is expected to be extended until at least January 2023. Centers for Medicare and Medicaid Services guidance recognizes that returning to normal operations when the PHE does end will require planning to avoid inappropriate coverage loss as states review eligibility for a large volume of enrollees.

This issue brief describes anticipated enrollment changes in pathways based on old age or disability (“non-MAGI”) after the PHE ends, state enrollment and renewal policies for non-MAGI groups as of July 1, 2022, and state plans for resuming normal operations when the PHE ends. These pathways are known as “non-MAGI” pathways because they do not use the Modified Adjusted Gross Income (MAGI) financial methodology that applies to eligibility for pregnant people, parents, and children with low incomes. The data were collected from March through May 2022 in KFF’s survey of Medicaid state eligibility officials. Overall, 50 states and the District of Columbia responded to the survey, though response rates for specific questions varied. Key findings include the following:

- Most states reported that non-MAGI enrollment increased during the COVID-19 PHE, and most states anticipate coverage losses at the end of the PHE. Of the 37 states responding, states most frequently cited change in income, followed by returned mail or inability to contact the enrollee as the primary reasons for anticipated coverage losses. A median of 10 percent of non-MAGI enrollees are expected to lose coverage at the end of the PHE (14 states responding).

- Staffing shortages and enrollee confusion were the most frequently identified issues expected to affect non-MAGI enrollees as states return to normal operations when the PHE ends.

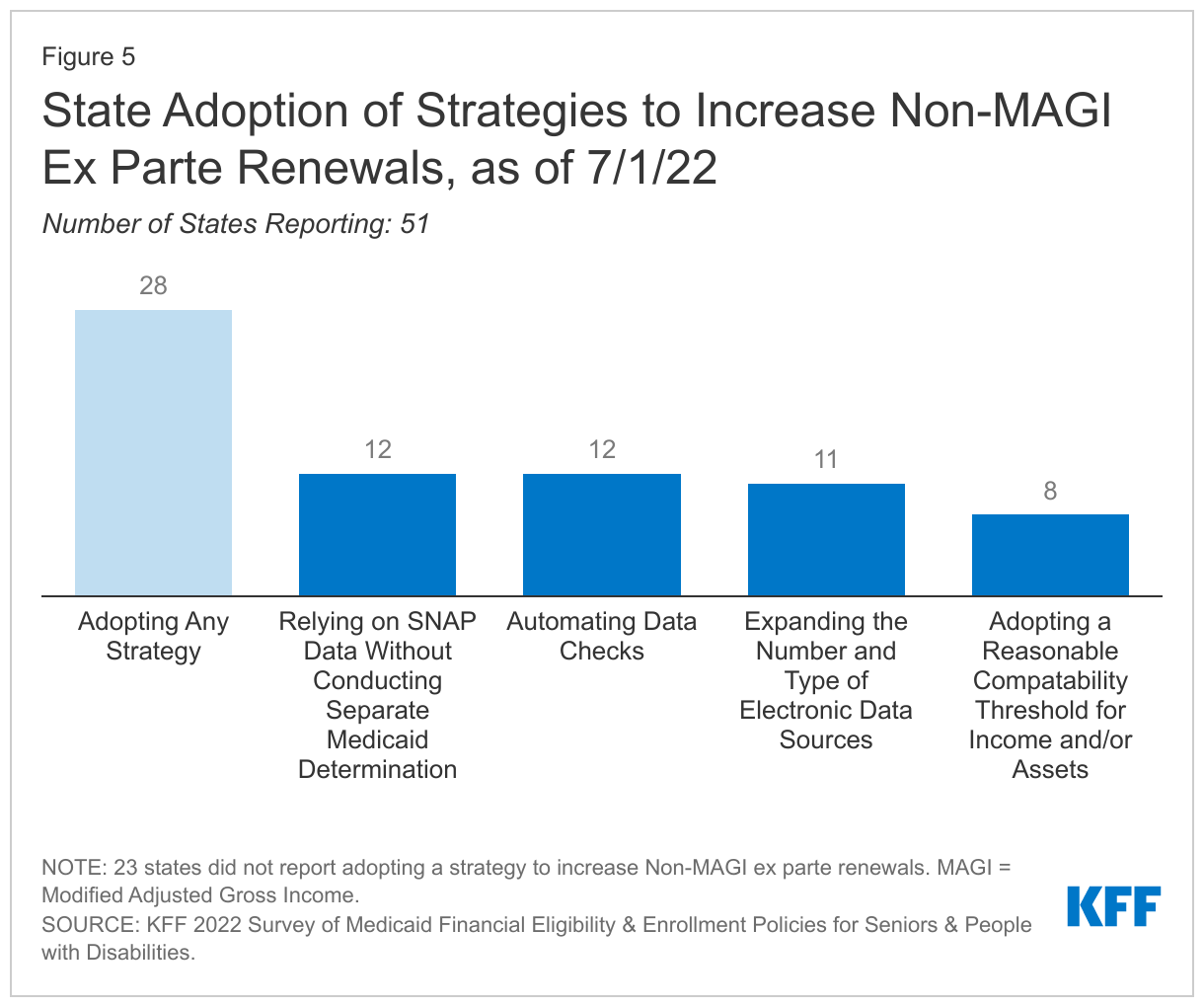

- More than half of states currently renew eligibility for some non-MAGI enrollees on an ex parte basis (without requiring information from the enrollee). However, 28 states have adopted at least one strategy to increase the share of ex parte renewals including relying on SNAP data without conducting a separate Medicaid determination (12 states), automating data checks (12 states), and expanding the number and type of electronic data sources used (11 states).

- Most states are planning to partner with other entities, such as health plans, providers, or community-based organizations, to provide information and/or assistance to seniors and people with disabilities who need to renew Medicaid eligibility or transition to other coverage (such as Medicare or Marketplace coverage) after the PHE ends.

Looking ahead to the PHE end, ensuring that eligible people remain enrolled or successfully transition to other coverage can help minimize gaps in coverage. This is especially important for seniors and people with disabilities, many of whom have chronic health needs and rely on long-term services and supports to meet daily needs. Historically, people who are enrolled in Medicaid in pathways based on old age or disability experience lower rates of churn, compared to children and non-elderly adults enrolled based solely on low income because they are less likely to experience changes in income or other factors affecting their on-going Medicaid eligibility. However, at the end of the PHE when millions of enrollees will need to complete a renewal, staffing shortages and enrollee confusion about how to navigate the process could increase risks of coverage loss. State policies to streamline eligibility and enrollment, such as increasing the share of non-MAGI renewals completed ex parte can minimize staff burden and promote continuity of coverage.

Issue Brief

The COVID-19 pandemic has disproportionately affected seniors and people with disabilities, especially those who rely on long-term services and supports (LTSS) to meet daily self-care and independent living needs. As it was before the pandemic, Medicaid remains an important source of coverage for these populations. While some people with disabilities qualify for Medicaid solely based on their low income, other people with disabilities and seniors qualify in pathways where eligibility is based on disability or old age, in addition to income, and often, assets. These pathways are known as “non-MAGI” pathways because they do not use the Modified Adjusted Gross Income (MAGI) financial methodology that applies to eligibility pathways for pregnant people, parents, and children with low incomes based on the rules in the Affordable Care Act (ACA). In addition to using rules about countable income that differ from MAGI pathways, most non-MAGI pathways also have asset limits, which do not apply to MAGI pathways.

States must maintain Medicaid coverage for people enrolled on or after March 18, 2020, as a condition of receiving enhanced federal matching funds during the COVID-19 public health emergency (PHE) under the Families First Coronavirus Response Act. This “continuous enrollment” requirement extends through the end of the month in which the PHE ends. During this time, states generally cannot disenroll people whose eligibility otherwise may need to be redetermined based on a change in circumstances or as part of a regular coverage renewal. The PHE is currently in place through October 2022, and is expected to be extended until at least January 2023. Recognizing the substantial work involved in returning to normal operations, the Centers for Medicare and Medicaid Services (CMS) has released a series of guidance for states as they plan to resume regular processing of applications, post-eligibility verifications, redeterminations, and renewals after the PHE ends. CMS emphasizes the importance of maintaining continuity of coverage and avoiding inappropriate coverage loss as states review eligibility for a large volume of enrollees after the PHE ends.

This issue brief provides a snapshot of non-MAGI enrollment during the PHE and anticipated changes after the PHE ends as well as key state enrollment and renewal policies in place as of July 2022, and state plans for resuming normal operations when the continuous enrollment requirement is lifted. The data were collected from March through May 2022 in KFF’s survey of Medicaid state eligibility officials. Overall, 50 states and the District of Columbia responded to the survey, though response rates for specific questions varied. The Appendix Tables contain detailed state-level information. A related brief presents state-level survey data on Medicaid financial eligibility criteria and adoption of major non-MAGI eligibility pathways.

Non-MAGI Medicaid Enrollment During and After the PHE

Most states reported that non-MAGI enrollment increased during the COVID-19 PHE (44 of 48 responding). The median increase in non-MAGI enrollment was 6% from February 28, 2020 (the month before the continuous enrollment requirement took effect) through December 31 2021, in the 40 states able to estimate the amount of the increase. The amount of increased enrollment in these states varied, ranging from 1% to 22% percent. Four states reported a small decrease in non-MAGI enrollment during this period, largely attributable to enrollee deaths during the pandemic. Across all eligibility pathways, Medicaid and CHIP enrollment increased by nearly 25% between February 2020 and May 2022. Enrollment increases may reflect changes in the economy, policy changes such as recent state adoption of the ACA’s Medicaid expansion, and the continuous enrollment requirement in place during the COVD-19 PHE. As of 2019, non-MAGI enrollment accounted for a minority (21%) of total Medicaid enrollment, but covered services for these enrollees comprised the majority (55%) of Medicaid spending, on account of their often intensive and chronic health and long-term care needs.

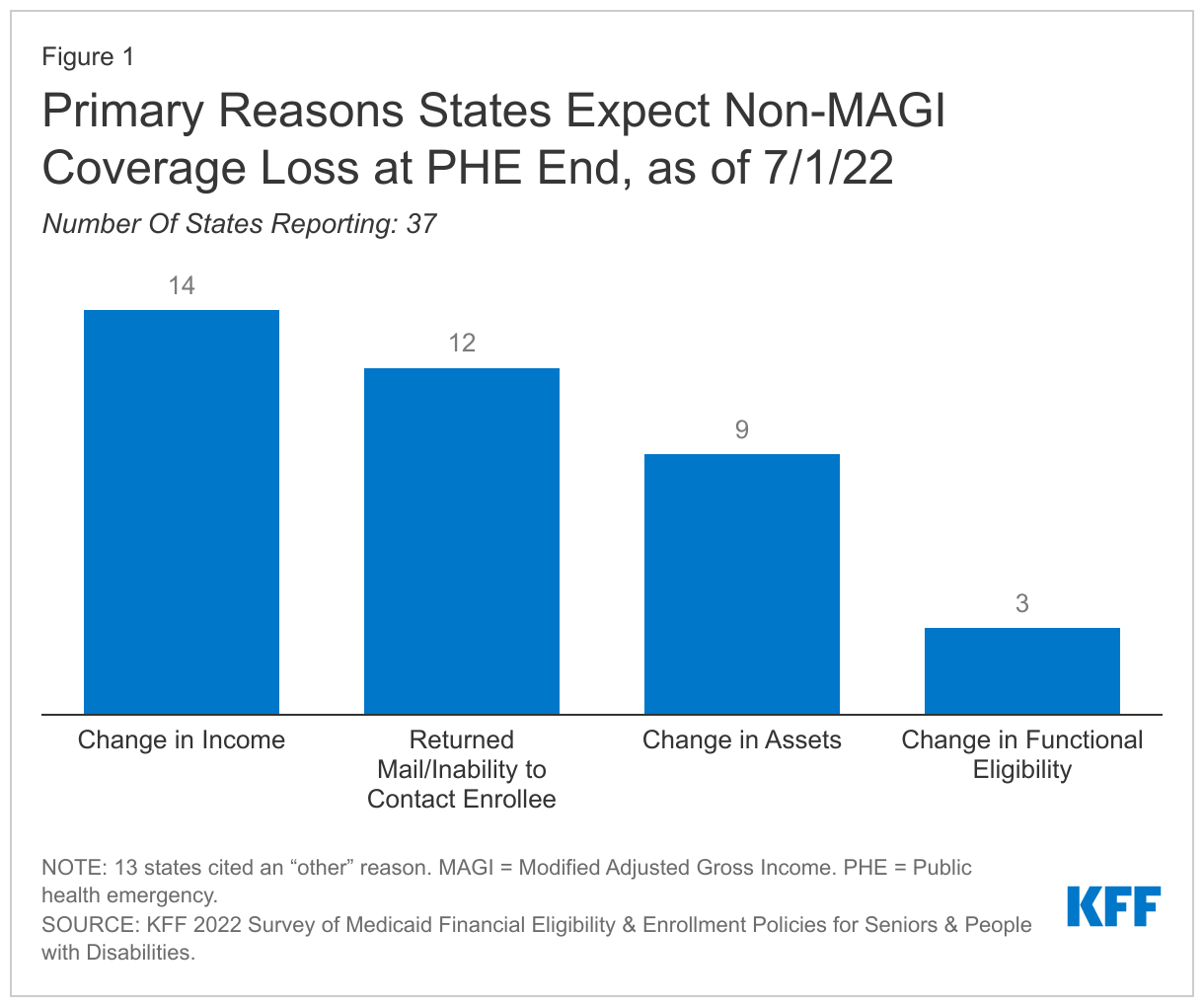

A median of 10% of non-MAGI enrollees are expected to lose coverage at the end of the PHE, across the 14 states able to report these data. Coverage loss estimates in these states ranged from 3% to 23%. At the time of our survey, most states (37) were unable to estimate the share of non-MAGI enrollees likely to be determined ineligible at the end of the PHE. However, most states (37) were able to identify a primary reason for which they expected non-MAGI enrollees would lose coverage at the end of the PHE: states most frequently cited change in income, followed by returned mail, or the inability to contact the enrollee (Figure 1). Six of the states that volunteered an “other” reason for anticipated coverage loss cited administrative reasons, such as enrollees failing to provide verifications or complete the renewal process. In addition to preventing coverage loss during the PHE, the continuous enrollment requirement has halted churning, temporary coverage loss experienced when enrollees dis-enroll and then re-enroll during a short period of time. Often, these enrollees inappropriately lose coverage, despite remaining eligible, due to administrative barriers such as failing to complete renewals.

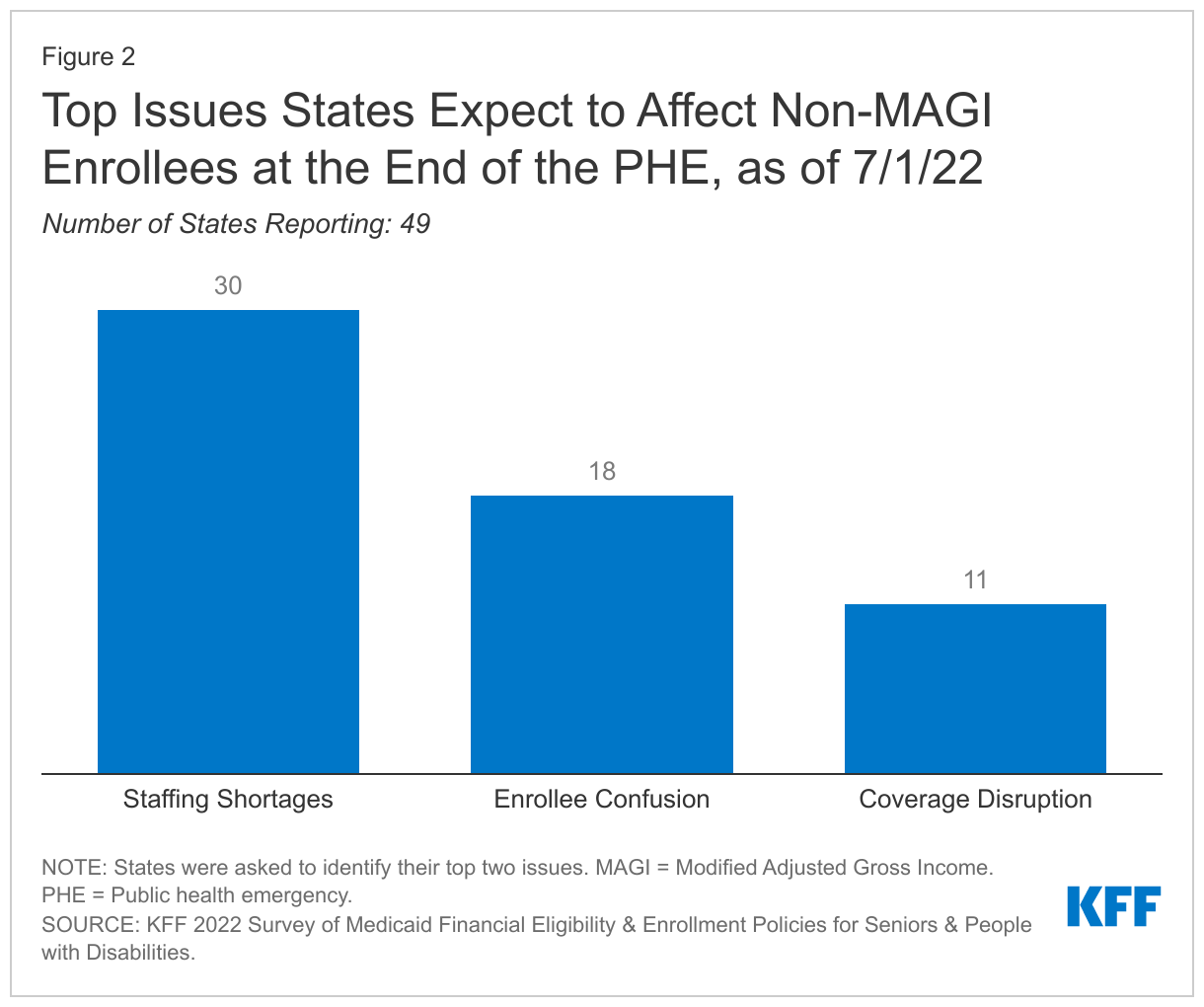

Staffing shortages and enrollee confusion were the most frequently identified issues expected to affect non-MAGI enrollees as states return to normal operations when the PHE ends among the 49 states responding to this question (Figure 2). (States were asked to identify their top two issues.) Other issues volunteered by multiple states include not being able to reach or re-establish contact with enrollees, updating enrollee contact information, and anticipated low enrollee response rates to renewal requests.

Application Processing Time and Verification Policies

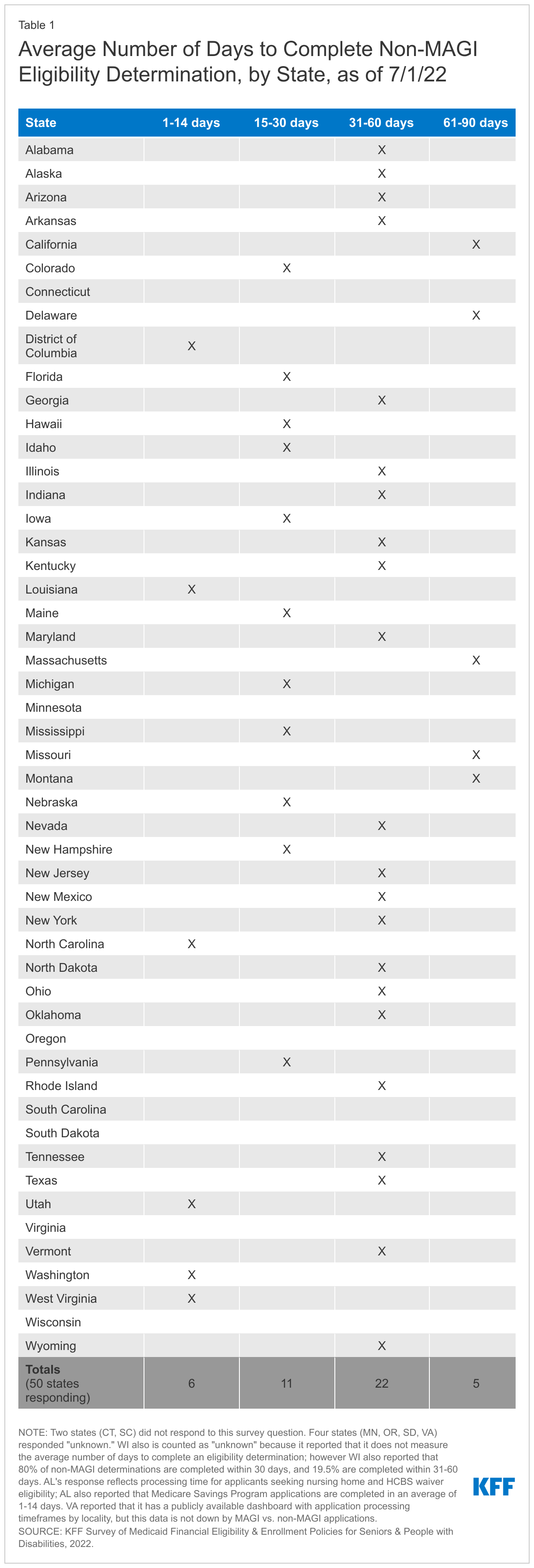

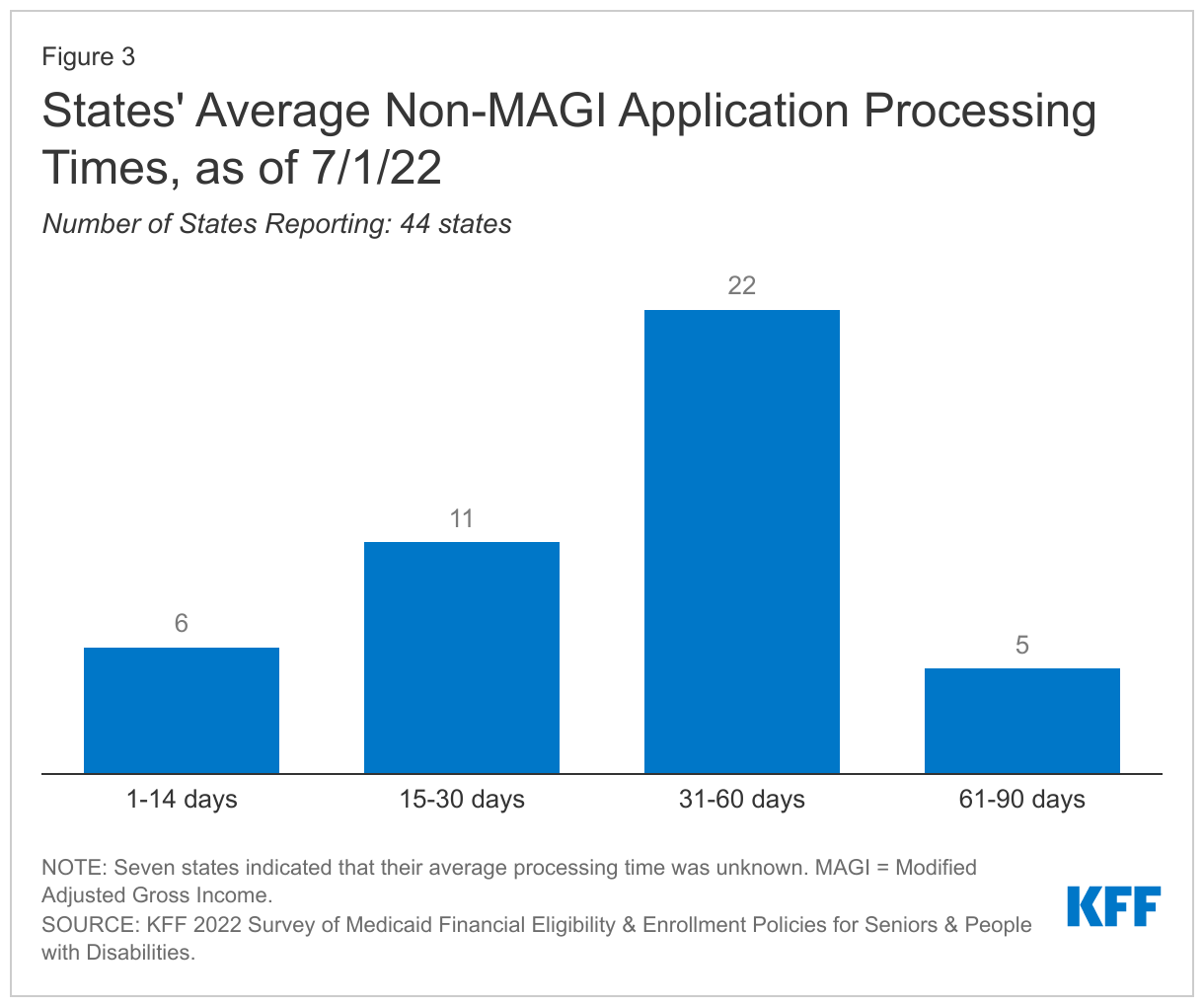

Most states take between one to two months on average to complete a non-MAGI eligibility determination (Figure 3 and Appendix Table 1). Half of the 44 states able to provide these data reported that non-MAGI eligibility determinations take an average of 31 to 60 days to complete (Figure 3). Federal rules allow states up to 90 days to complete disability-related Medicaid eligibility determinations. Unlike MAGI eligibility determinations, which many states now make in “real time,” all aspects of non-MAGI eligibility determinations cannot be easily automated or verified through electronic data sources. Nearly 232,000 non-MAGI applications were pending an eligibility determination as of January 1, 2022, across the 32 states able to report these data. CMS expects states to prioritize processing new applications while the PHE is still in effect, to complete eligibility determinations on all pending disability-related applications received during the PHE within three months after the PHE ends, and to resume timely eligibility determinations for all applications with four months after the PHE ends.

Most states require paper documentation from non-MAGI applicants or enrollees to verify income and/or assets only if electronic data sources are unavailable. Specifically, 43 states adopt this verification policy for income, and 36 do so for assets. Two states (ND, RI) always require paper documentation to verify income, and five states (CT, GA, MN, RI, WY) always require paper documentation to verify assets. Increased reliance on electronic data sources, where available, and decreased reliance on paper documentation can shorten application processing times and alleviate administrative burdens on applicants and state staff. A couple of states noted that assets were being disregarded under Medicaid emergency authorities to streamline eligibility determinations during the PHE.

Few states accept self-attestation from non-MAGI applicants to verify income and/or assets. Specifically, three states accept self-attestation without additional verification for income and assets (DC, KY, TX), and two states do so only for assets (AK, UT). Another five states accept self-attestation with post-eligibility verification for income and assets (CA, HI, IN, MD, NH), two states do so only for income (DE, ME) and two states do so only for assets (TX, WA). A couple of states noted that self-attestation is used only for Medicare Savings Program pathways. States can choose whether to accept self-attestation to verify income and/or assets under regular program rules. Some states newly adopted or expanded the use of self-attestation to streamline eligibility and enrollment during the PHE using Medicaid emergency authorities. States have the option to continue many policies adopted under emergency authorities when they return to normal operations, and two states (OH, OR) plan to continue to accept self-attestation to verify income after the PHE ends. New Hampshire also noted that it expanded self-attestation prior to the PHE and plans to continue this policy after the PHE ends. Box 1 describes New Jersey’s experience with accepting self-attestation when evaluating asset transfers for applicants seeking long-term services and supports (LTSS).

Box 1: Self-Attestation of No Asset Transfers in New Jersey

Under a Section 1115 demonstration waiver, New Jersey eliminates state review and instead allows applicants with income below the federal poverty level applying for Medicaid LTSS to self-attest that they had no asset transfers during the five-year look-back period. The look-back period delays the date of Medicaid eligibility for applicants who transferred assets for less than fair market value, which instead could have been used to pay for LTSS needs. New Jersey conducted electronic asset verification of randomly selected applications in 2015 and 2016, and found a 0% error rate on these sampled self-attestations, concluding that “the often burdensome five year lookback process can be safely eliminated for many low-income applicants.”

Nearly all states (50 of 51 responding) are using electronic asset verification systems (AVS). Among these states, most (43) are using AVS for all non-MAGI pathways with an asset test, while the remainder use AVS only for some non-MAGI pathways with an asset test. The benefits of electronic AVS most frequently cited by states include reduced burden on applicants/enrollees (37 states), faster eligibility determinations (22 states), and reduced burden on state staff (17 states). The challenges of electronic AVS most frequently cited by states include results not being available in real time (38 states), lack of financial institution participation (30 states), uncertainty about whether system reports complete information on all countable assets (16 states), and system is expensive to use (7 states). Four states volunteered that AVS identified unreported assets.

Nearly 40 percent of states (20 of 51 responding) use electronic data matching to check financial eligibility for non-MAGI enrollees between renewal periods. States may choose to use electronic data matching between renewal periods to identify changes in enrollees’ circumstances that may affect eligibility. Among these states, 4 use data matching on a monthly basis, and 3 do so on a quarterly basis. The remaining 13 states use another time period, such as annually, or indicate that the time period varies by data source. Box 2 below describes the state option to adopt continuous eligibility for non-MAGI groups, a policy that allows enrollees to retain coverage regardless of changes in circumstances for a certain period.

Box 2: State Option to Provide Continuous Eligibility for Non-MAGI Enrollees

Continuous eligibility is a state option that allows enrollees to retain coverage regardless of changes in circumstances for the duration of a period elected by the state. This policy can reduce administrative burden on state agency staff and promote continuity of coverage and care for enrollees. Recent CMS guidance explains that states can use state plan authority to adopt income and asset disregards under Section 1902 (r)(2) to provide continuous eligibility for most people enrolled based on old age, disability, or LTSS need.

Renewal Policies and PHE Unwinding Outreach

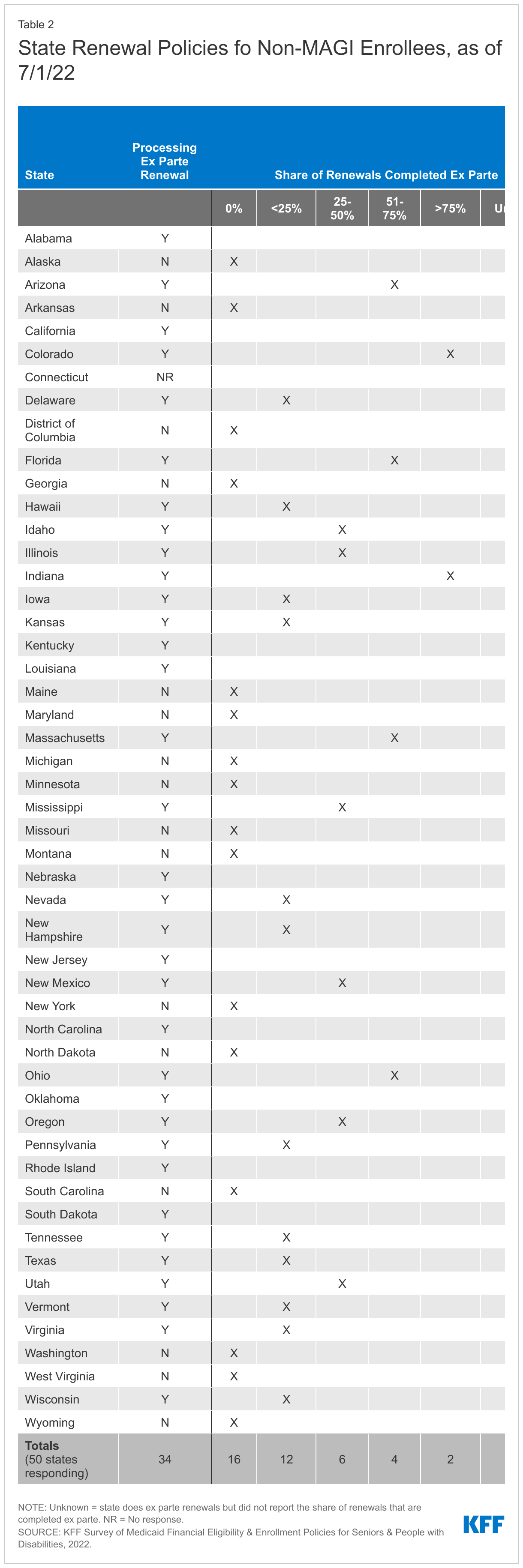

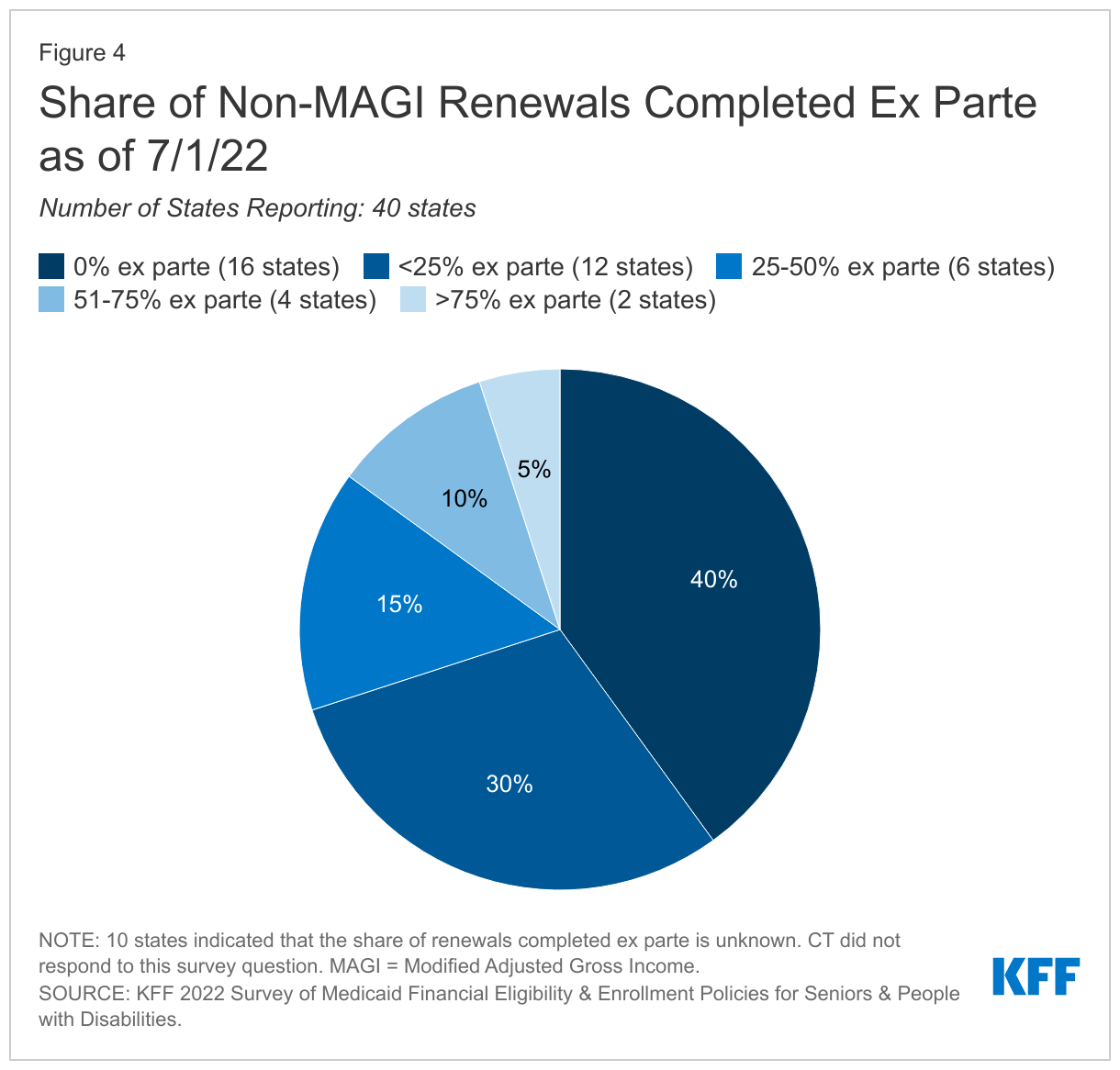

Nearly all states (50 of 51 responding) renew non-MAGI eligibility annually, and most states (34) of 50 responding) are processing at least some ex parte eligibility renewals for non-MAGI enrollees as of January 1, 2022 (Appendix Table 2). West Virginia is the only state that renews non-MAGI eligibility every six months instead of annually. While annual renewals are required for MAGI groups, states have the option to renew non-MAGI eligibility more frequently. Ex parte renewals are completed using electronic and other available data sources, without requiring the enrollee to complete a form or provide information. Of the 16 states that had not yet resumed processing ex parte renewals as of January 1, 2022, 9 planned to resume doing so when the continuous eligibility requirement is lifted. One state (MD) planned to resume in October 2022, and plans were still being formulated in the remaining states. CMS guidance recommends that states process ex parte renewals during the PHE to alleviate potential backlogs when the continuous coverage requirement is lifted. After the PHE ends, CMS guidance requires states to have initiated all renewals within 12 months and to have completed them within 14 months.

A majority of states (28 of 51 responding) have adopted at least one strategy to increase the share of non-MAGI renewals completed ex parte (Figure 5). Increasing the share of renewals completed ex parte can shorten processing times, reduce administrative burden on state staff, and help ensure that eligible people remain enrolled and do not lose coverage due to administrative reasons. The strategies most frequently adopted include relying on SNAP data without conducting a separate Medicaid determination, followed by automating data checks, expanding the number and type of electronic data sources, and adopting a reasonable compatibility threshold for income and/or assets (Figure 5). Each of the remaining strategies – increasing an existing reasonable compatibility threshold, creating a hierarchy to prioritize the most recent reliable data sources, and streamlining, increasing, or eliminating asset limits – was adopted by 3 states. Among the 28 states adopting at least one strategy, half have adopted more than one strategy, and some have adopted three or more strategies. CMS identified these strategies to mitigate the risk of eligible people inappropriately losing coverage due to procedural or administrative reasons.

Most states (36 of 51 responding) are sending pre-populated renewal forms to non-MAGI enrollees when they are unable to confirm eligibility on an ex parte basis, as of January 1, 2022 (Appendix Table 2). Most states have adopted the option to send pre-populated renewal forms to non-MAGI enrollees, though some states have paused doing so during the PHE while the continuous enrollment requirement is in effect. Sending pre-populated forms can simplify the renewal process and help eligible people retain coverage, which in turn can strengthen continuity of care. Most states (35 of 51 responding) also opt to offer a reconsideration period in which non-MAGI enrollees can regain coverage without completing a new application if they lost coverage for failure to respond to a renewal request.

Few states plan to prioritize populations that may include seniors or people with disabilities when the PHE ends and renewals resume. CMS guidance requires states to adopt a methodology to prioritize which renewals and other pending actions to complete and recommends that states consider certain factors when doing so. Six states plan to prioritize people who gained Medicare eligibility during the PHE, while three states plan to prioritize people dually eligible for Medicare and Medicaid.

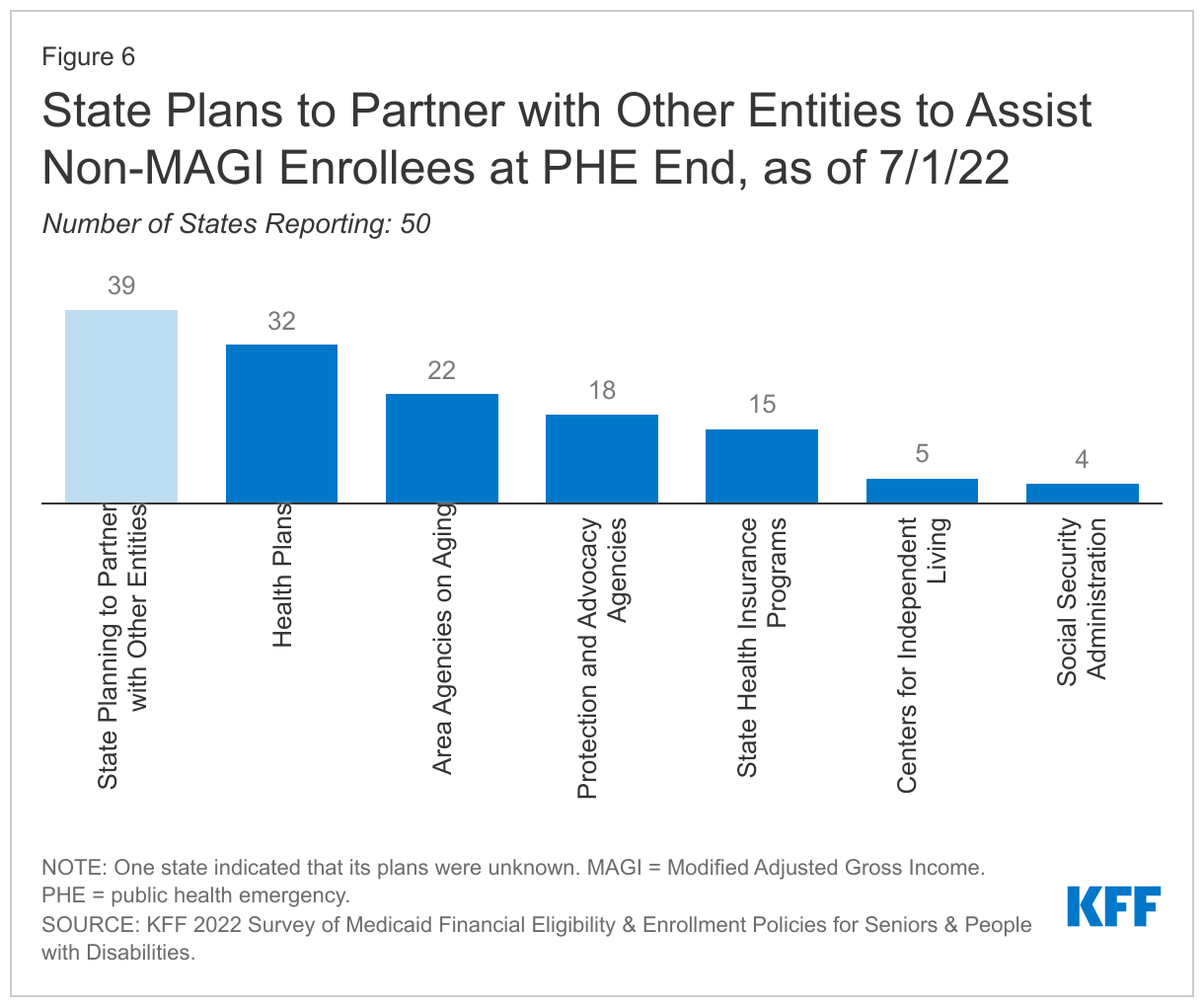

Most states (40 of 50 responding) are planning communication or outreach strategies targeted to seniors or people with disabilities about the end of the continuous enrollment requirement. Nearly all of these states (39 of 50 responding) are planning to partner with other entities to provide information and/or assistance to seniors and people with disabilities who need to renew Medicaid eligibility or transition to other coverage (such as Medicare or Marketplace coverage) after the PHE ends. States most frequently reported plans to partner with health plans, followed by Area Agencies on Aging, protection and advocacy agencies for people with disabilities, and State Health Insurance Programs (Figure 6). Some states also volunteered that they are planning to partner with providers such as nursing homes.

One-third of states (16 of 48 responding) are planning to attempt to contact non-MAGI enrollees twice before terminating coverage after the continuous enrollment requirement ends if the enrollee must take action to maintain coverage. Ten states reported that they would contact enrollees in these circumstances once, while eight states reported that they would make three contacts. The remaining states reported “other” plans or indicated that their plans were not yet known.

Other Eligibility and Enrollment Policies

Fifteen states (of 51 responding) use hospital presumptive eligibility for one or more non-MAGI groups. This state plan option allows states to authorize hospitals to enroll people who appear likely to be eligible for coverage, while the state processes the full Medicaid application and makes a final eligibility determination. Presumptive eligibility can facilitate access to coverage when individuals in need of critical services also may need extra time to collect the information needed to complete a full eligibility determination, which is required to retain ongoing services. Two states (AZ, NC) elect this option but have no participating hospitals. Ohio noted that it adopted this option during the PHE but discontinued it due to “non-use.” Box 3 describes state experience with presumptive eligibility using entities other than hospitals.

Box 3: State Experience with Presumptive Eligibility for Seniors and People with Disabilities

A few states allow entities other than hospitals to determine presumptive eligibility for certain populations and/or benefits. Presumptive eligibility can provide faster access to services, such as home and community-based services (HCBS), when individuals in need of critical services also need extra time to complete a full eligibility determination. Individuals determined presumptively eligible receive a full eligibility determination to retain services after the presumptive eligibility period ends.

Indiana adopted a pilot program during the COVID-19 PHE that allows certain HCBS providers to determine seniors presumptively eligible. The program expedites Medicaid eligibility determinations by allowing providers to authorize Medicaid eligibility and HCBS on the date of application for individuals who are “most likely eligible,” followed by post-eligibility verification by the state agency for services to continue. The program’s goal is to begin HCBS within 10 days of authorization and help alleviate the need to move into a nursing facility. Indiana adopted this policy in October 2020 using Appendix K emergency authority and plans to continue it after the PHE ends.

Three months retroactive coverage is available for non-MAGI enrollees in 48 states (of 51 responding). Florida, Iowa, and Tennessee have Section 1115 waivers that allow them to eliminate retroactive eligibility, while Arizona’s waiver allows it to offer retroactive eligibility only for children with disabilities. The estimated share of non-MAGI enrollees who have a retroactive claim paid varies widely in the 10 states able to report these data, ranging from less than 1% to 66%. Retroactive coverage safeguards low-income enrollees from unpaid medical bills and helps encourage providers to participate in Medicaid by ensuring payment. Some people may not be eligible for Medicaid until after they experience a traumatic event, such as a stroke, that requires ongoing long-term care. Retroactive coverage protects patients and providers by ensuring that medical bills are paid even if a Medicaid application is not filed until the calendar month following a traumatic event.

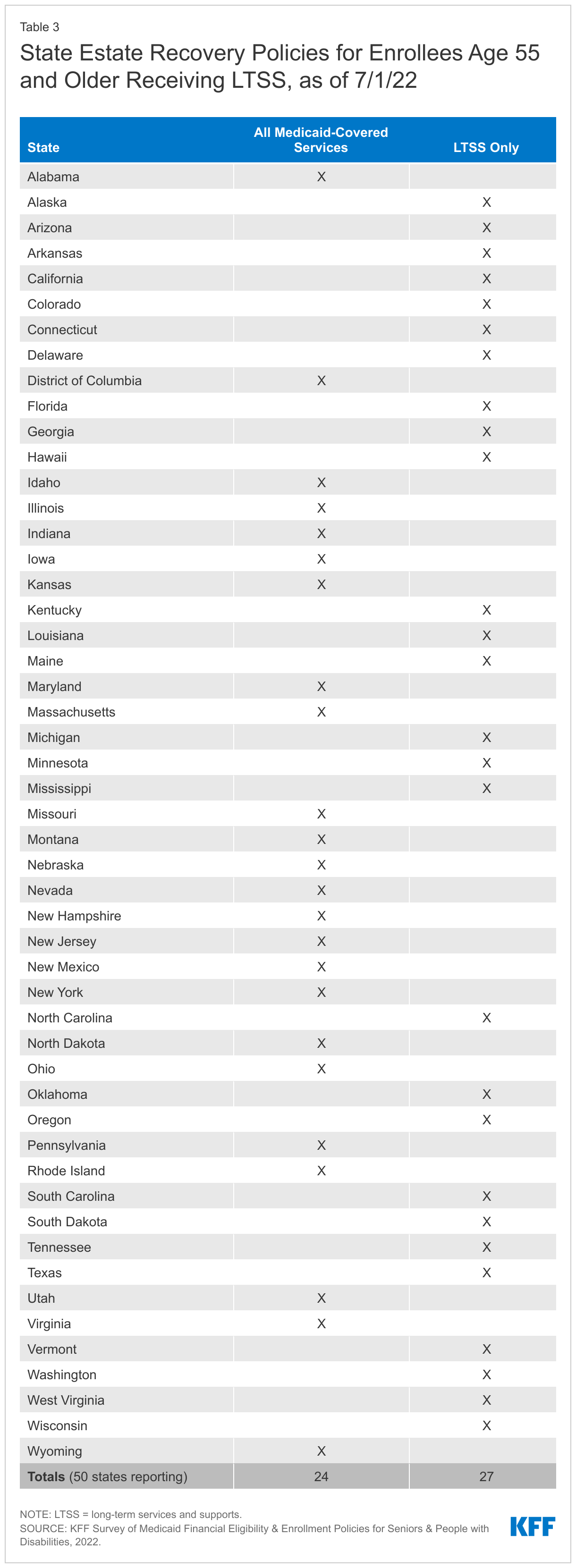

Over half of states (27 of 51 responding) opt to pursue estate recovery only for LTSS provided to enrollees ages 55 and older (Appendix Table 3). The remaining responding states pursue estate recovery for all Medicaid-covered services provided to these enrollees. Federal law requires states to attempt to recover the cost of certain Medicaid-covered services provided to enrollees ages 55 and older from their estates after their deaths. States must pursue estate recovery for LTSS and may choose to do so for other covered services. The Medicaid Payment and Access Commission (MACPAC) has recommended that Congress make all estate recovery optional for states, noting that the policy “contributes to generational poverty and wealth inequity, placing particular burdens on people of color.” MACPAC also found that “[e]state recovery recoups relatively little—only about 0.55 percent of total fee-for-service LTSS spending.”

Looking Ahead

Looking ahead to the PHE end, ensuring that people remain enrolled or successfully transition to the coverage for which they are eligible will help provide continuity of care. This is especially important for seniors and people with disabilities, many of whom have chronic health needs and rely on LTSS to meet daily needs. Historically, people who are enrolled in Medicaid in pathways based on old age or disability experience lower rates of churn, compared to children and non-elderly adults enrolled based solely on low income. This indicates that people in non-MAGI pathways are less likely to experience changes in income or other factors affecting their on-going Medicaid eligibility. Yet, the risk of eligible people losing coverage could be intensified due to staffing shortages and enrollee confusion about how to navigate the renewal process. State policies to streamline eligibility and enrollment, such as increasing the share of non-MAGI renewals completed ex parte can minimize staff burden and promote continuity of coverage. For people whose eligibility has changed during the PHE, efforts to facilitate smooth transitions to Medicare or the Marketplace can help to minimize gaps in coverage.

Appendix