2022 Survey of ACA Marketplace Assister Programs and Brokers

Executive Summary

The Affordable Care Act (ACA) expanded affordable health coverage options in the U.S., helping to reduce the number of uninsured individuals. Even so, KFF has found that most people who remain uninsured are nonetheless eligible for coverage and financial assistance through the Marketplace or Medicaid. Many consumers – including most uninsured – have limited awareness of affordable coverage options available to them under the ACA. And the steps people must take to get and keep coverage can sometimes be complex. Accordingly, the ACA required federal and state Marketplaces to establish and invest in consumer assistance to conduct outreach and public education and to help connect people to affordable coverage.

KFF conducted a national, online survey of Marketplace Assister Programs and brokers in 2022. To build the sample for the survey, contact information for Assister Programs and brokers was collected from State Marketplaces (SBM), the Center on Medicare and Medicaid Services (CMS) which administers the Federal Marketplace (FFM), and the Health Resources and Services Administration (HRSA) which oversees enrollment assistance by Federally Qualified Health Clinics (FQHCs). A total of 3,496 Assister Programs were invited by email to participate in the survey, and 258 Programs responded and were included (for a response rate of 7.4%). We also contacted 68,705 brokers certified to sell Marketplace coverage and 1,424 responded and were included (for a response rate of 2.1%). Additional description of survey methods is included in the Topline accompanying this report.

Our survey asked Assister Program directors and brokers about the help they provided consumers before, during and after the 2022 Open Enrollment Period, reasons people sought help, factors affecting the enrollment process, and other issues. Key findings include:

Assister Programs and brokers report that the need for consumer assistance is high among people they serve. Overwhelmingly, Assister Programs (76%) and brokers (69%) said most or nearly all of the consumers they helped during this ninth ACA Open Enrollment lacked confidence to apply on their own; about two-thirds of Assister Programs (64%) and brokers (66%) said most to nearly all the people they helped had limited understanding of ACA requirements and benefits. Most Assister Programs and brokers (54% each) also said the majority of consumers they helped had difficulty understanding basic health insurance terms and concepts. Consumers also needed help answering questions about their household income and composition, and help comparing a large number of plan choices. Some consumers present with complex cases or need language assistance – challenges that Assister Programs say require more resources and technical help than is available from the Marketplace.

Most Assister Programs and brokers said the average time needed to help people newly applying through the Marketplace continued to be between 1 and 2 hours; for consumers returning to renew or change coverage, it was up to 1 hour. This is similar to findings in previous KFF surveys in 2016, 2015, and 2014.

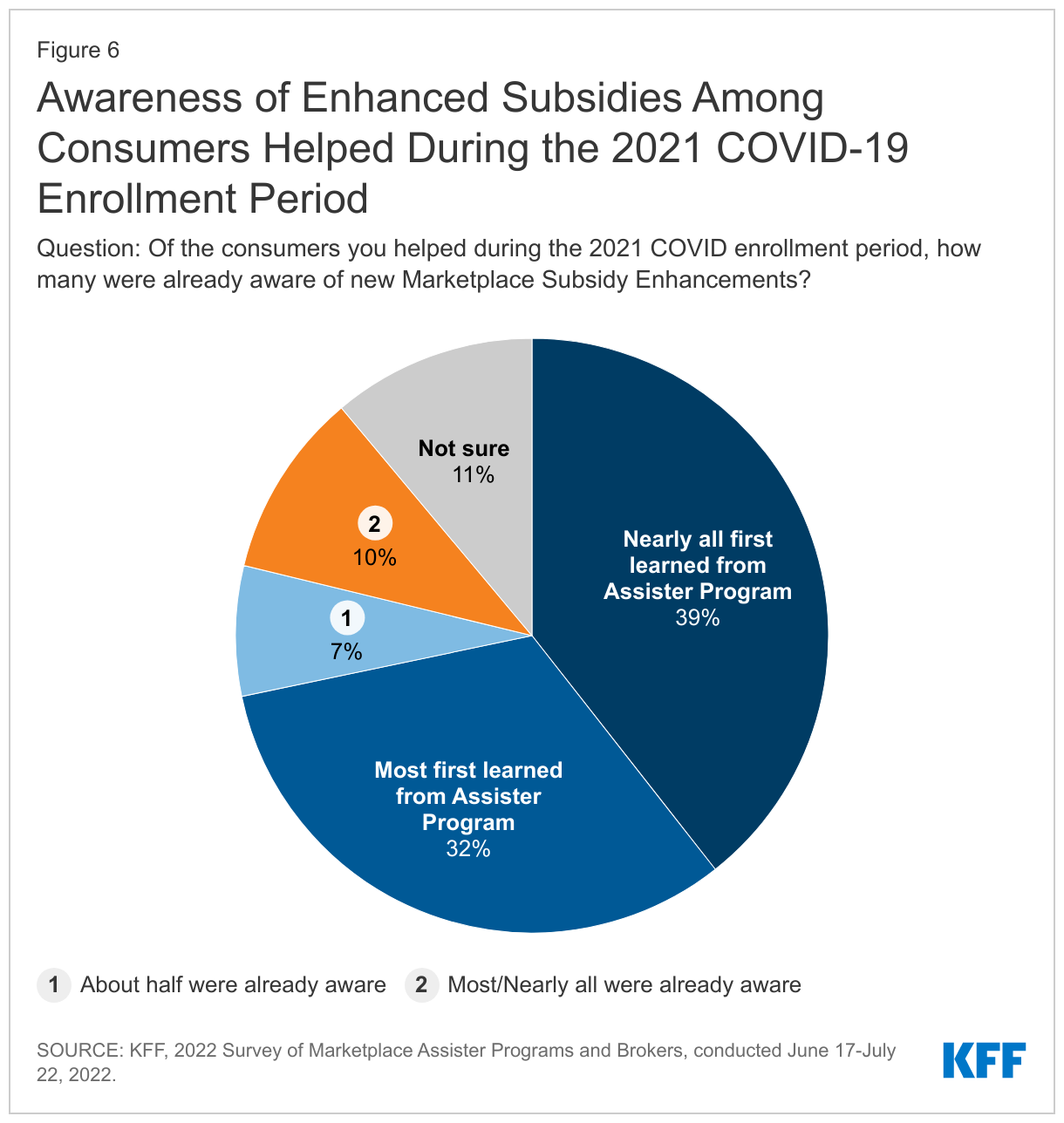

Consumer awareness about Marketplace subsidies and rules is still limited. Nearly all Assister Programs (89%) and brokers (80%) this year also helped consumers last year to sign up for coverage or update subsidies during the 2021 COVID-19 enrollment period. Newly enhanced Marketplace subsidies became effective during the 2021 COVID enrollment period, though our respondents observed that consumer awareness about the enhanced subsidies was low; 71% of Assister Programs and 75% of brokers said most to nearly all consumers they helped during the 2021 COVID enrollment period were unaware of the new, improved subsidies when they first came in for help.

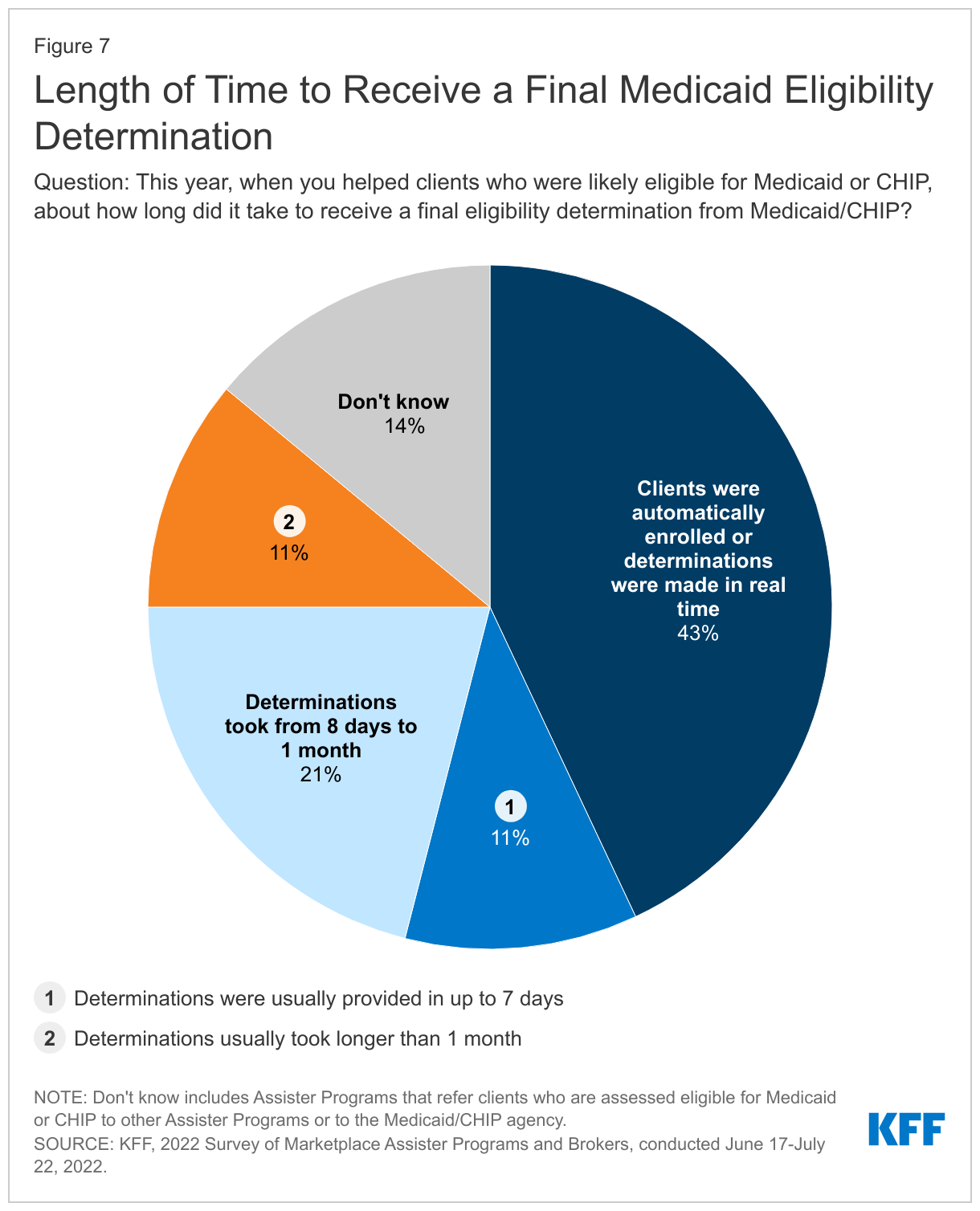

Assister Programs report that some consumers eligible for Medicaid experience delays in getting a final eligibility determination. In 17 states the Marketplace determines Medicaid eligibility, while in the rest, the Marketplace transfers files to Medicaid for a final eligibility determination, which can cause delays. As a result, Assister Programs report the time it takes for consumers to receive an eligibility determination varies widely. Forty-three percent of Programs said eligibility determinations were determined in real time or Medicaid enrollment was automatic, while an equal share of Programs said the process takes longer – 11% said Medicaid determinations were provided in up to 7 days, 21% said determinations took from 8 days to one month, and 11% said it took longer than a month.

Help from Brokers and Assister Programs is similar in many respects but not interchangeable. We also surveyed brokers certified by the Marketplace to sell qualified health plans. The type of help brokers reported providing and people they reported helping resembled that of Assister Programs, though there were important differences, likely reflecting differences in the clients served. In particular, brokers – who rely on commissions – were far less likely to help consumers sign up for Medicaid or CHIP (39% of brokers vs 88% of Assister Programs) and far less likely to conduct outreach activities (27% vs 62% of Assister Programs). Compared to Assisters, Brokers who responded to the survey reported that a smaller share of the consumers they helped were Hispanic, needed language assistance or help with immigration-related problems, or were uninsured.

Brokers rely on private web sites over Marketplace sites. Most brokers (72%) surveyed report using private websites instead of the Marketplace to enroll consumers in QHPs at least some of the time. In most states brokers can use so-called direct enrollment (DE) sites, for example hosted by insurance companies, where consumers can sign up for Marketplace QHPs, though consumers generally are re-directed to the Marketplace site if they also need subsidies. The federal government also promotes use of Enhanced Direct Enrollment (EDE) sites – only available in federal marketplace states – where consumers can apply for both QHPs and marketplace subsidies without ever visiting HealthCare.gov. A majority of brokers in federal marketplace states (55%) said they never initiate QHP applications on HealthCare.gov. When asked why they prefer these alternate enrollment channels, many brokers cited technological features which HealthCare.gov does not offer, such as dashboards that enable them to more easily track client accounts and communicate with clients. Sixty percent of brokers surveyed who use private sites said they would use the Marketplace website more often if offered similar functionality.

Brokers also continue to sell non-ACA-compliant policies. Most brokers (75%) said they also sold non-ACA-compliant policies – such as short-term plans — during Open Enrollment as an alternative or supplement to QHPs, though the volume of these sales was lower compared to QHP sales. For example, most brokers (54%) said they sold more than 50 QHPs during the 2022 Open Enrollment period, while most who also sold non-ACA-compliant policies (67%) said they sold 10 or fewer of these policies.

Most Assister Programs expect to play a role helping consumers through the public health emergency (PHE) unwinding. It is anticipated that the COVID-19 Public Health Emergency may end sometime in 2023, at which point, state Medicaid agencies will resume eligibility redeterminations and will disenroll people who are no longer eligible or who are unable to complete the renewal process even if they remain eligible. As a result, between 5 and 14 million people are estimated to lose Medicaid coverage. Many who lose Medicaid may be eligible to buy subsidized QHPs, if they can navigate that transition. About half of Assister Programs (53%) said they have good working relationships with their state Medicaid agency and nearly 6 in 10 said they have contacted Medicaid to find out how they can help educate consumers about the need to renew their coverage. Half of all Assister Programs reported they are planning outreach activities to educate the public about the PHE unwinding and most (58%) said they will try to re-contact consumers whom they helped apply for Medicaid coverage in the past two years to collect updated contact information.

Report

Section 1: Help From Assister Programs During Open Enrollment

Types of Assister Programs

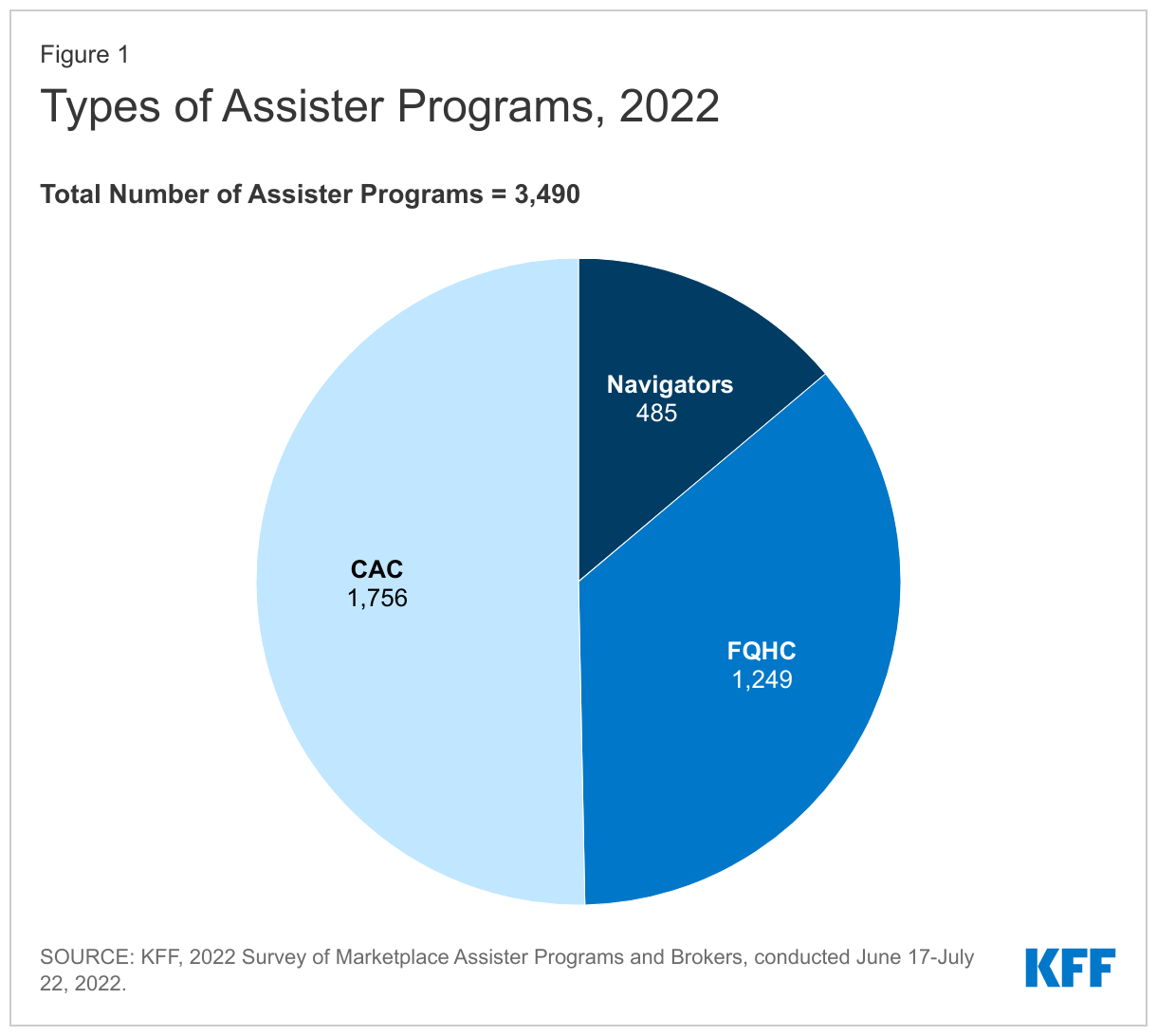

In all, based on administrative data, 3,490 Marketplace Assister Programs provided outreach and enrollment help to consumers during the ninth Affordable Care Act (ACA) Open Enrollment period, referred to in this report as the 2022 Open Enrollment. This is a smaller number of Programs (5,094) than operated in 2016. The Appendix to this report provides more detail on different types of Assister Programs. We surveyed Programs that fall into three main types:

- Navigator Programs, by law, must be established and funded in every federal and state Marketplace to provide free, objective outreach and enrollment assistance. Staff must have expertise in eligibility and enrollment rules, the range of qualified health plan (QHP) options, financial help – both QHP subsidies and Medicaid/CHIP – and the needs of underserved and vulnerable populations, including individuals with limited English proficiency.

- Certified Application Counselor (CAC) Programs must be certified by every Marketplace but not funded by the Marketplace. Most CAC Programs are sponsored by community non-profit organizations that voluntarily support outreach and enrollment assistance.

- Federally Qualified Health Center (FQHC) Programs are operated by the network of clinics that receive federal funding to provide health care to low-income and underserved populations. The federal government provides additional funding to FQHCs to also provide eligibility and enrollment assistance in their communities. Most FQHCs (1,249 in 2022) are certified by Marketplaces as CAC Programs, but 85 centers are also certified as Marketplace Navigator Programs. (Figure 1)

Assister Programs tend to serve local communities. About three-fourths (77%) of Assister Programs served consumers in a limited geographic within a state. However, about four-in-ten (41%) Navigator Programs had state-wide service areas.

Nearly all Assister Programs (93%) have been providing enrollment assistance for a number of years. Eighty-two percent of Assister Programs this year provided help to consumers during 5 or more Marketplace Enrollment Periods. Only 7% of Assister Programs said they provided enrollment assistance to consumers for the first time during the 2022 Open Enrollment period.

Consumer Assistance Needs

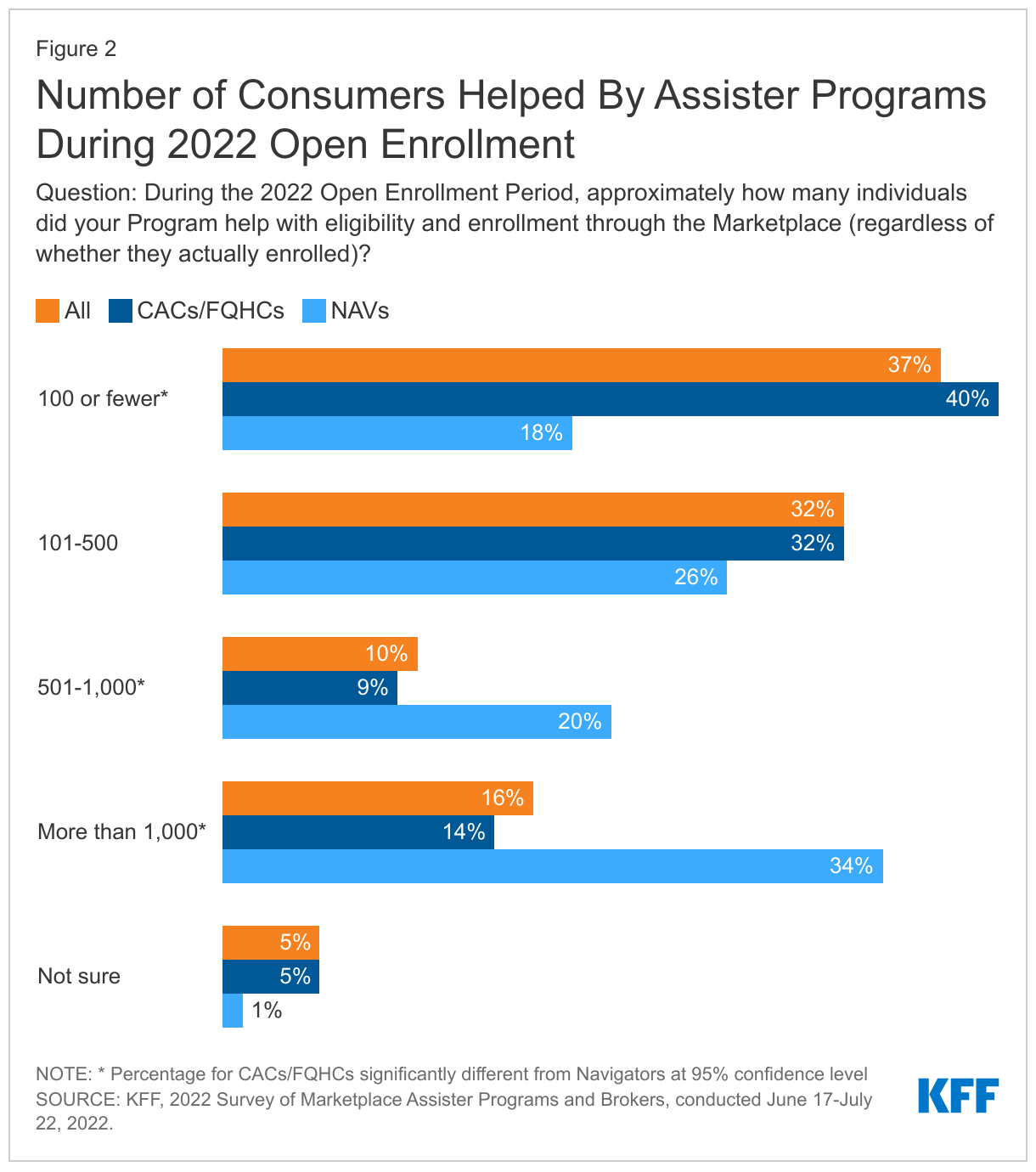

Navigator Programs tended to operate at a larger scale, helping more consumers compared to other types of Programs. During the 2022 Open Enrollment, most Navigator Programs (54%) helped at least 500 consumers and 34% of Navigator Programs helped more than 1,000 consumers. By contrast, among the other types of Assister Programs (CAC and FQHC), 40% said they helped no more than 100 consumers and 14% said they helped more than 1,000 people. (Figure 2)

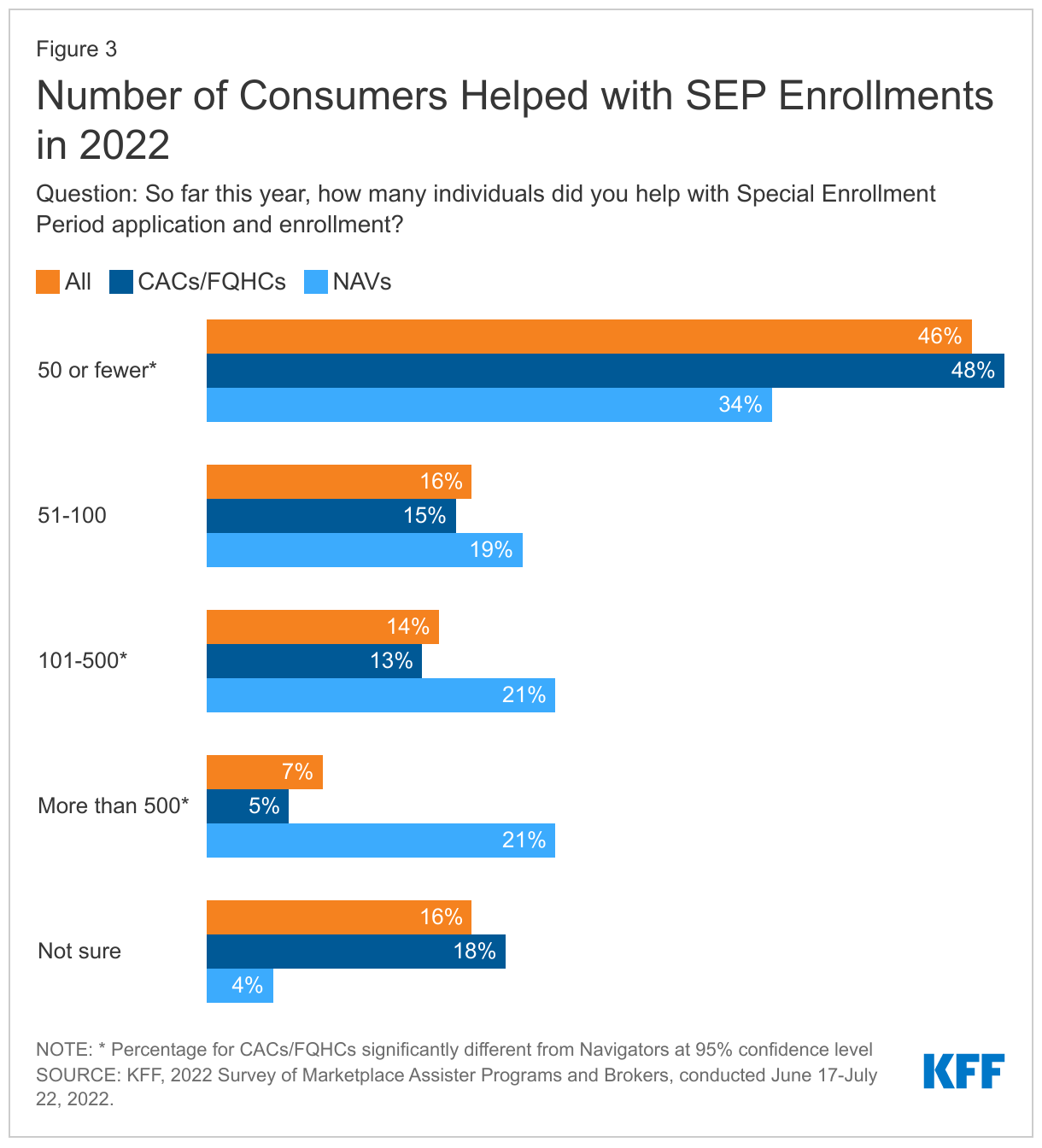

Assister Programs also reported helping consumers eligible for Marketplace special enrollment periods (SEP). Outside of Open Enrollment, consumers can sign up for Marketplace coverage if they have a qualifying event, such as loss of other coverage, that makes them eligible for a SEP. Again, Navigator Programs tended to help more consumers with SEPs than did other Assister Programs. (Figure 3)

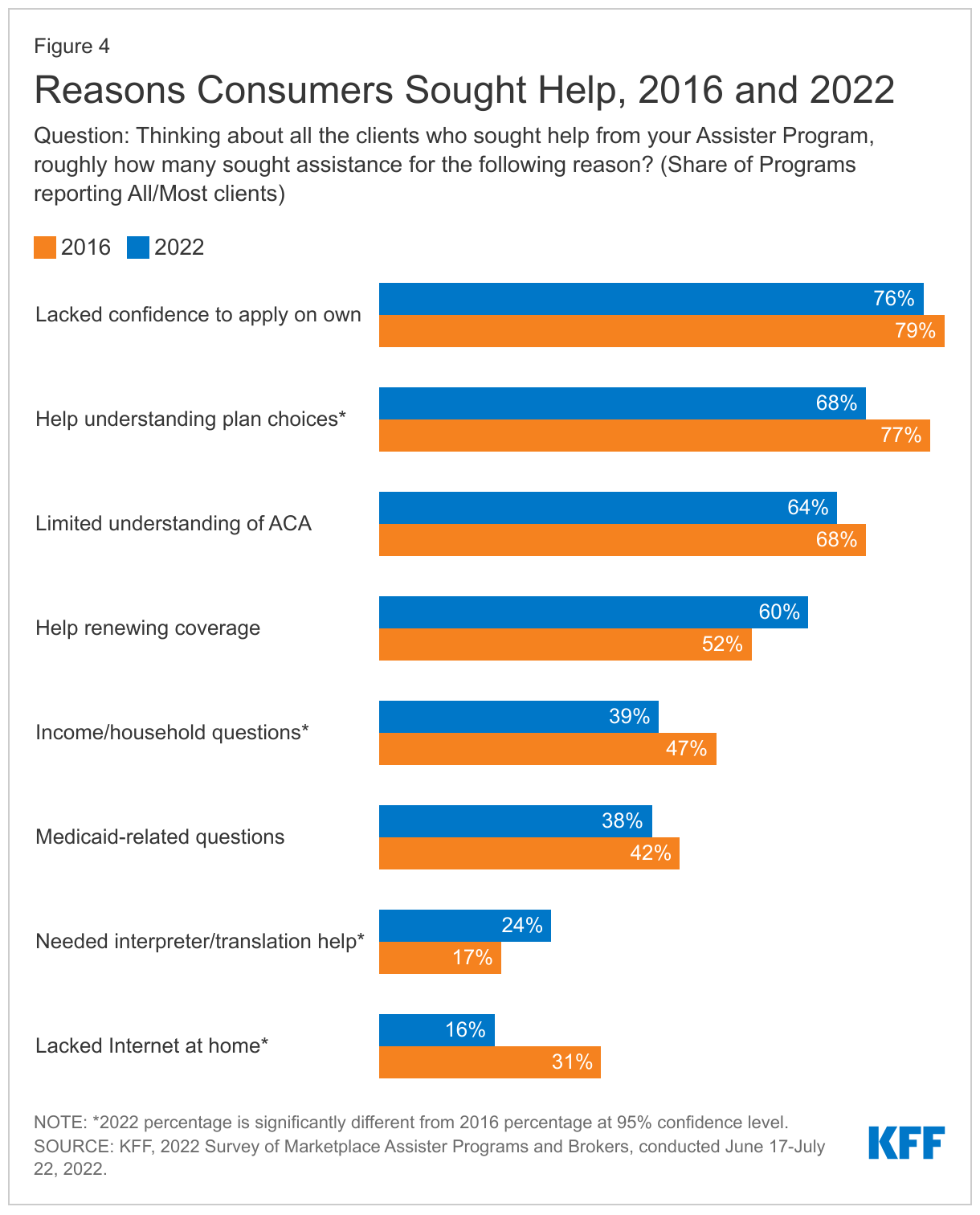

The reasons consumers seek help from Assister Programs has not changed much since 2016. About three-quarters of Assister Programs (76%) said most-to-nearly-all consumers sought help this year because they lacked confidence to apply for coverage and financial help on their own, and 64% said most or nearly all clients had limited understanding of the ACA. These findings are similar to what Programs reported in 2016. This year, fewer Assister Programs said most or all clients lacked Internet at home (16% vs 31% in 2016); but more Programs said most or nearly all clients needed language assistance (24% vs 17%) (Figure 4)

The need for help, as reported by Assister Programs, continues even though most consumers now come to the Marketplace to renew coverage. This year, 48% of Assister Programs reported that most or nearly all consumers they helped were returning to the Marketplace to renew or change coverage.

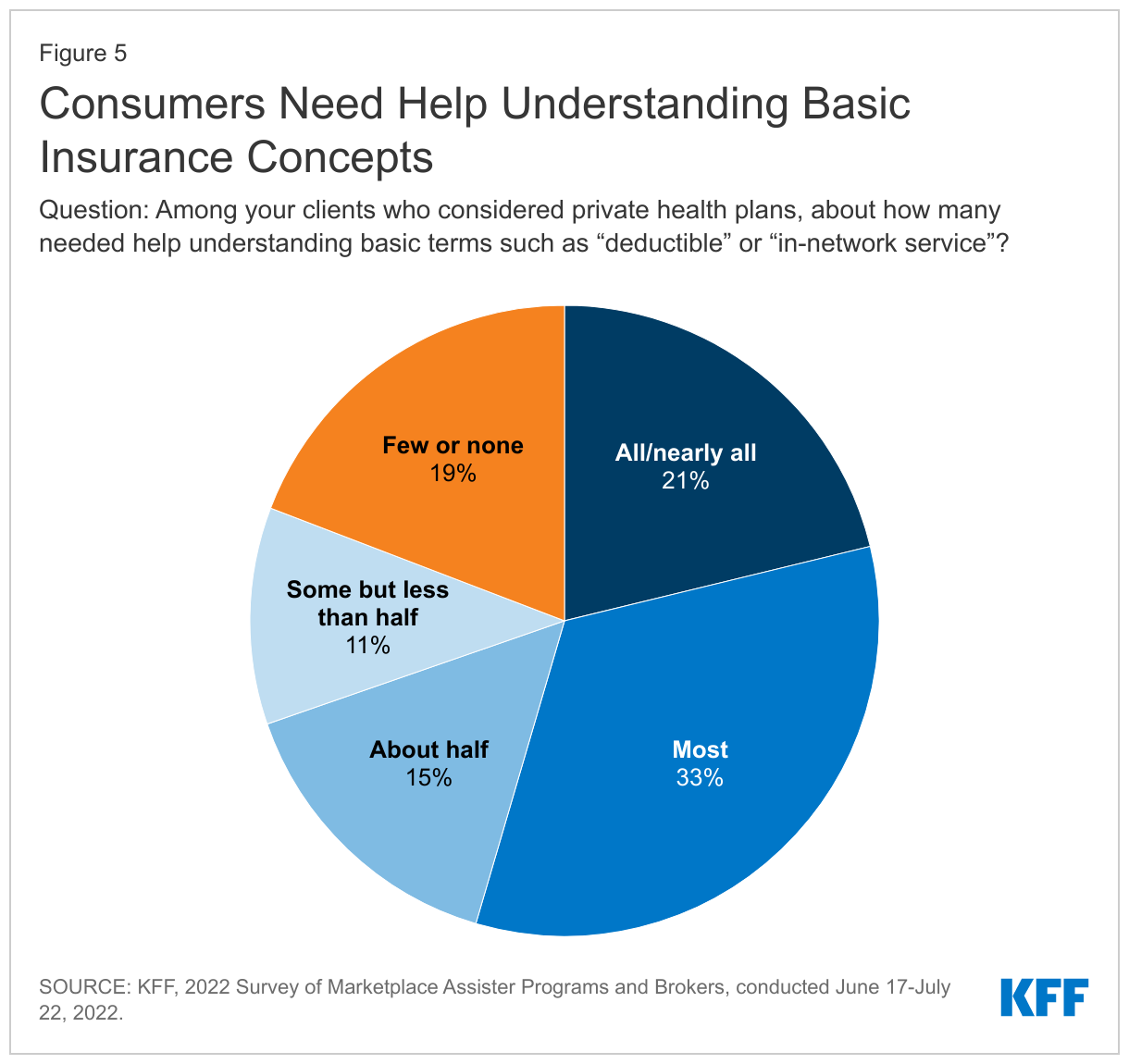

Insurance literacy limitations remain a challenge. Most Assister Programs (69%) said half or more of their clients needed help understanding basic insurance terms such as “deductible” and “in-network service,” (Figure 5)

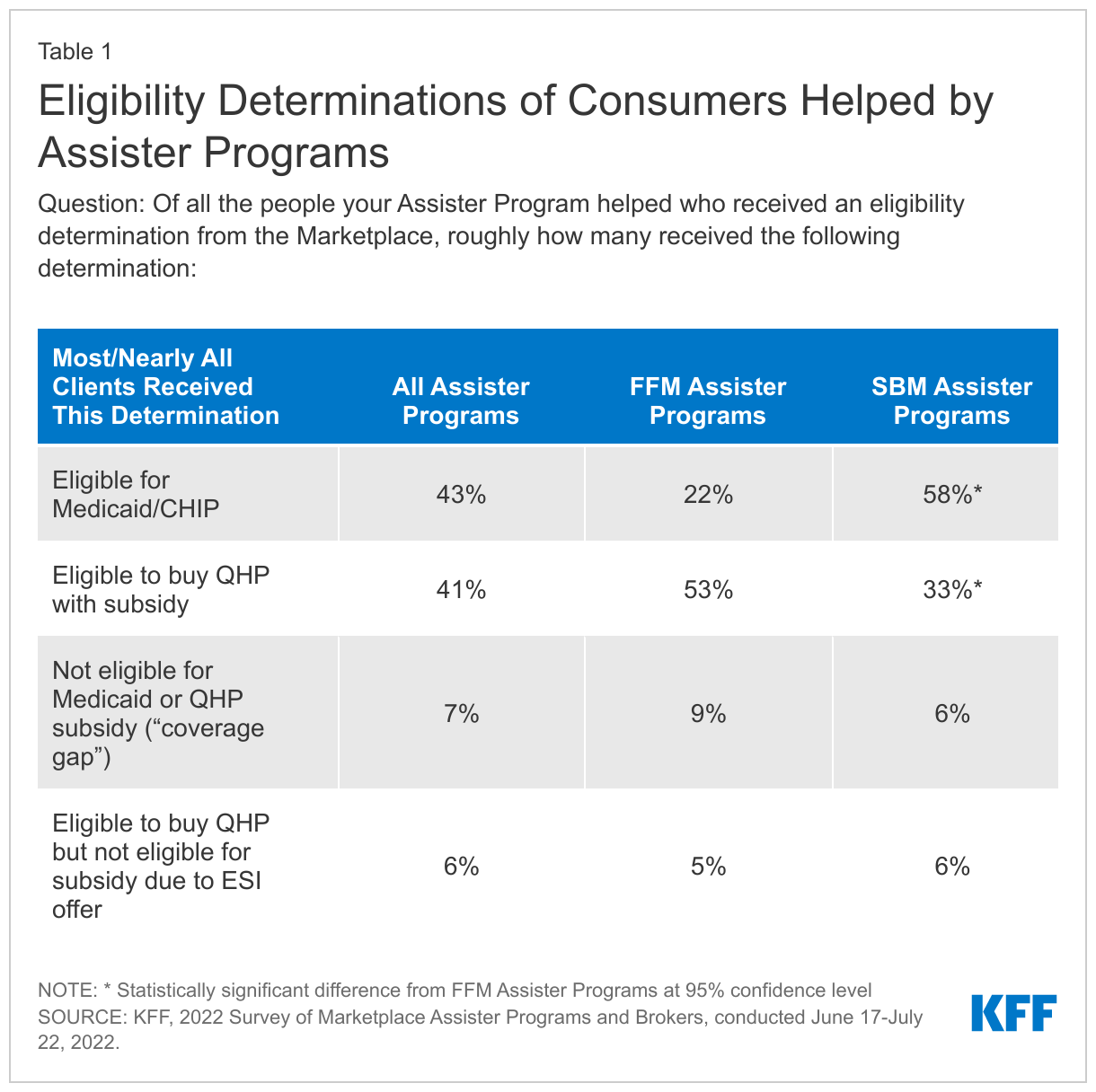

A substantial share of consumers helped by Assister Programs were eligible for Medicaid. Nationwide, 43% of Assister Programs reported that most or nearly all consumers they helped were determined eligible for Medicaid or CHIP. More Programs in State-based marketplaces (SBM) said this was the case compared to those in federal-marketplace (FFM) states (58% vs 22%). All 21 SBM states have implemented the ACA Medicaid eligibility expansion while 12 of the FFM states have not. (Table 1)

Assister Programs report serving consumers of diverse racial/ethnic backgrounds. A majority (56%) of Assister Programs estimate that half or more consumers they helped were non-white; with 32% of Programs reporting that at least three-quarters of their clients were non-white. One in five Programs (22%) reported half or more of the clients they served were Hispanic. Data about race and ethnicity, is key to understanding how the ACA is affecting access to coverage for people of color. All Marketplaces ask consumers to volunteer information about their race/ethnicity, but many do not answer. Most Assister Programs (63%) said they tell their clients why reporting this information can be useful.

Section 2: Help Applying for Financial Assistance

A primary role of Assister Programs is to educate the public about the availability of financial assistance – either through Marketplace subsidies or Medicaid – and to help people apply.

Marketplace subsidy enhancements

Through the American Rescue Plan Act (ARPA) Congress temporarily strengthened QHP subsidies, effective in 2021, and recently extended this subsidy enhancement through the end of 2025. QHP subsidy improvements were substantial, particularly for the lowest income individuals, making it possible for people with income up to 150% FPL ($19,320 for a single person in 2022, $32,940 for a family of 3) to apply for zero-premium plans with comprehensive cost sharing reductions (CSR). Previously, the poorest individuals were required to contribute at least 2.07% of income toward the premium for CSR plans. People with incomes above 400% of the poverty level ($51,520 for a single person, $87,840 for a family of 3 in 2022) also became eligible for premium assistance for the first time.

Nearly all Assister Programs (89%) provided help to consumers during the extended COVID Enrollment period in 2021. As the new ARPA subsidies taking effect in 2021, the federal government required all Marketplaces to reopen for a special COVID-19 enrollment period that lasted seven months in HealthCare.gov states, and even longer in some state-based marketplaces. This special enrollment period gave Marketplace enrollees a chance to claim the newly enhanced subsidies and gave uninsured individuals a second chance to sign up for affordable plans. More than 2.5 million consumers signed up for new coverage during the 2021 COVID-19 enrollment period, and more than 2.6 million already-enrolled consumers came back to claim the enhanced subsidies.

Overwhelmingly, Assister Programs said most consumers they helped during the COVID Enrollment period were unaware of the ARPA subsidy enhancements. 71% of Programs reported that most to nearly all clients first learned about the extra financial help from Assister Programs. (Figure 6)

Despite enhanced subsidies, assisters report that consumers still face tradeoffs between lower premiums and higher cost sharing. While new ARPA subsidies give consumers with the lowest income (up to 150% FPL) access to zero-premium silver plans with very low deductibles, those earning between 150&-250% FPL must pay at least a portion of the premium for CSR silver plans. For these consumers, cheaper (even zero-premium) bronze plans are also often available, but with very high deductibles, usually in excess of $7,000 per year. We asked Assister Programs to estimate the share of their clients overall who were eligible for CSR silver plans and who nonetheless elected cheaper bronze plans. Just 18% of Assister Programs estimated that none of their clients made this choice, while 27% of Programs estimated that 10% or more of their clients in this situation chose a cheaper bronze plan; 26% were not sure.

Marketplace coordination with Medicaid

In all FFM states and in some SBM states, Marketplace and Medicaid eligibility systems are not integrated, requiring consumer files to be transferred between the systems. The ACA creates a “no wrong door” approach to applying for coverage and requires a single streamlined application for financial assistance that can be used to determine eligibility for QHP subsidies and Medicaid or the Children’s Health Insurance Program (CHIP). That means that people must be able to apply for Medicaid or CHIP through the Marketplace. While SBM states can choose to integrate Medicaid and CHIP into their Marketplace eligibility system to facilitate enrollment into each program and transitions of coverage among Medicaid, CHIP, and the Marketplaces, not all states have done so. In ten SBM states, the Marketplace eligibility system also determines eligibility for the expansion Medicaid population, but in eight SBM states, files must be transferred to the Medicaid agency for an eligibility determination. Of the 33 states that use HealthCare.gov, seven states allow HealthCare.gov to determine Medicaid eligibility, though files are then transferred to state Medicaid agencies to complete enrollment. In the remaining states, HealthCare.gov makes an initial assessment of Medicaid eligibility, then transfers the consumer’s file to the state Medicaid agency for a final eligibility determination and to complete enrollment.

Assister Programs report that some consumers face delays in getting a final Medicaid eligibility determination. Programs reported that over four in ten (43%) clients who were determined eligible for Medicaid were either automatically enrolled into Medicaid or the eligibility determination was made in real time. However, an equal share of Programs reported that the final Medicaid determination took longer, including 11% that said determinations were provided in up to 7 days, 21% that said determinations took from 8 days to one month, and 11% that said it took longer than a month (Figure 7). Federal rules require states to complete Medicaid eligibility determinations in 45 days for MAGI populations. A report on Medicaid application processing times for January 2022 indicated that 48% of applications took from 1 day to more than 45 days. Some Assister Programs said they refer clients who are assessed as eligible for Medicaid or CHIP to other Assister Program (5%) or to the Medicaid/CHIP agency (4%) to complete the application and enrollment process.

Despite delays in Medicaid eligibility determinations, in most cases, Assister Programs learned whether the client ultimately enrolled in Medicaid. Three-quarters of Assister Programs reported they knew clients’ final Medicaid enrollment status all or most of the time, while 8% said they knew clients’ status about half of the time. The remaining 17% of Assister Programs said they knew the outcome in less than half of the cases, including 6% of Programs that reported knowing the Medicaid enrollment status rarely or never.

Section 3: Factors Affecting the Enrollment Process

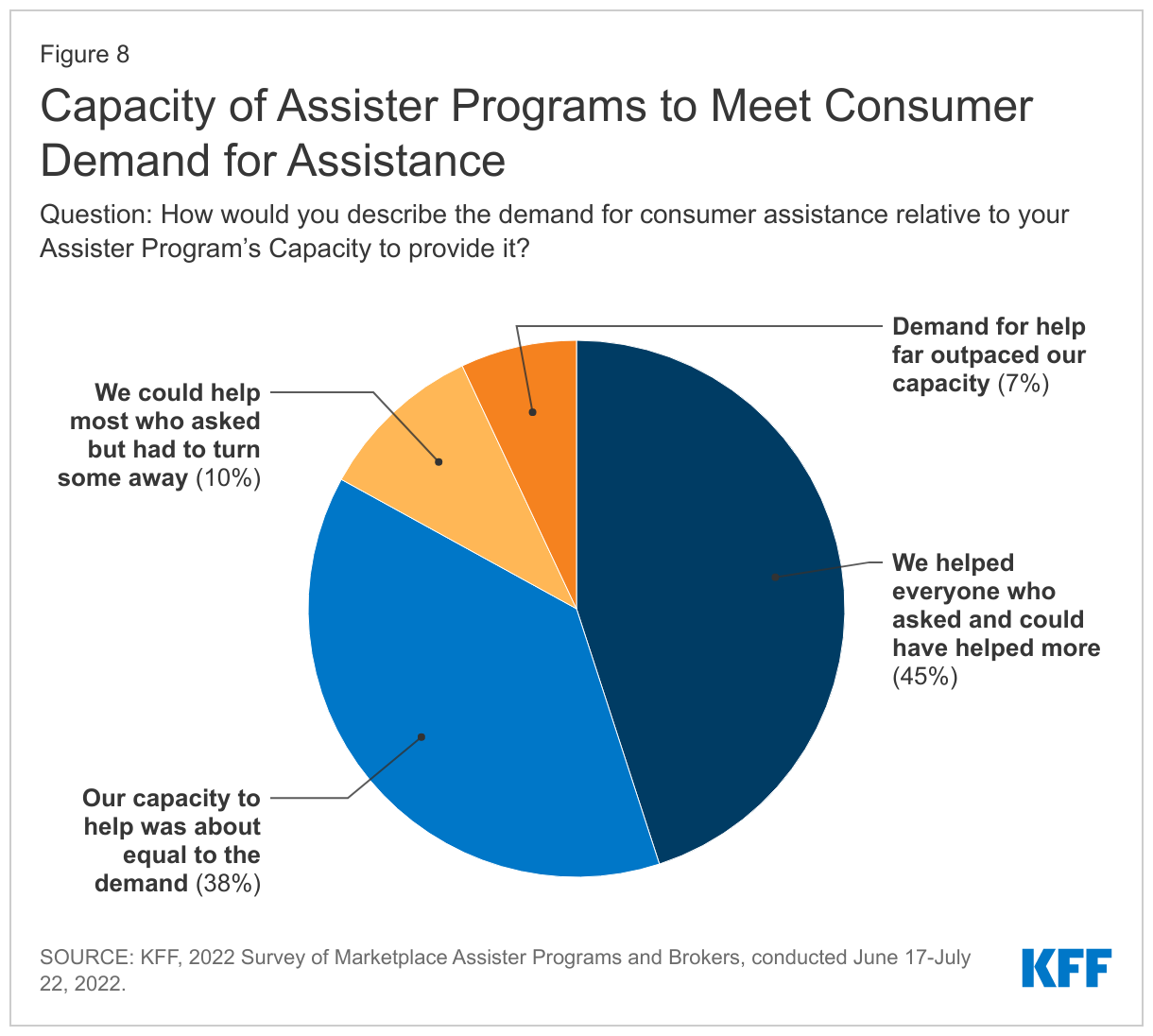

Most Assister Programs report sufficient capacity to meet demand, but some had to turn people away. The vast majority of Assister Programs said they had capacity to serve all consumers who sought help during the last Open Enrollment period; however, 17% said they had to turn at least some consumers away – similar to the share who said demand exceeded capacity for the 2016 Open Enrollment Period. (Figure 8)

Assister Programs’ reliance on remote assistance developed during the COVID-19 pandemic. Before the pandemic, as a matter of policy, Marketplaces generally encouraged face-to-face enrollment assistance whenever possible. For the 2022 Open Enrollment period, however, 40% of Assister Programs said they provided remote assistance to half or more of their clients. 20% of Programs said they helped most consumers face-to-face, and 39% of Programs said all or nearly all consumers they helped received face-to-face assistance.

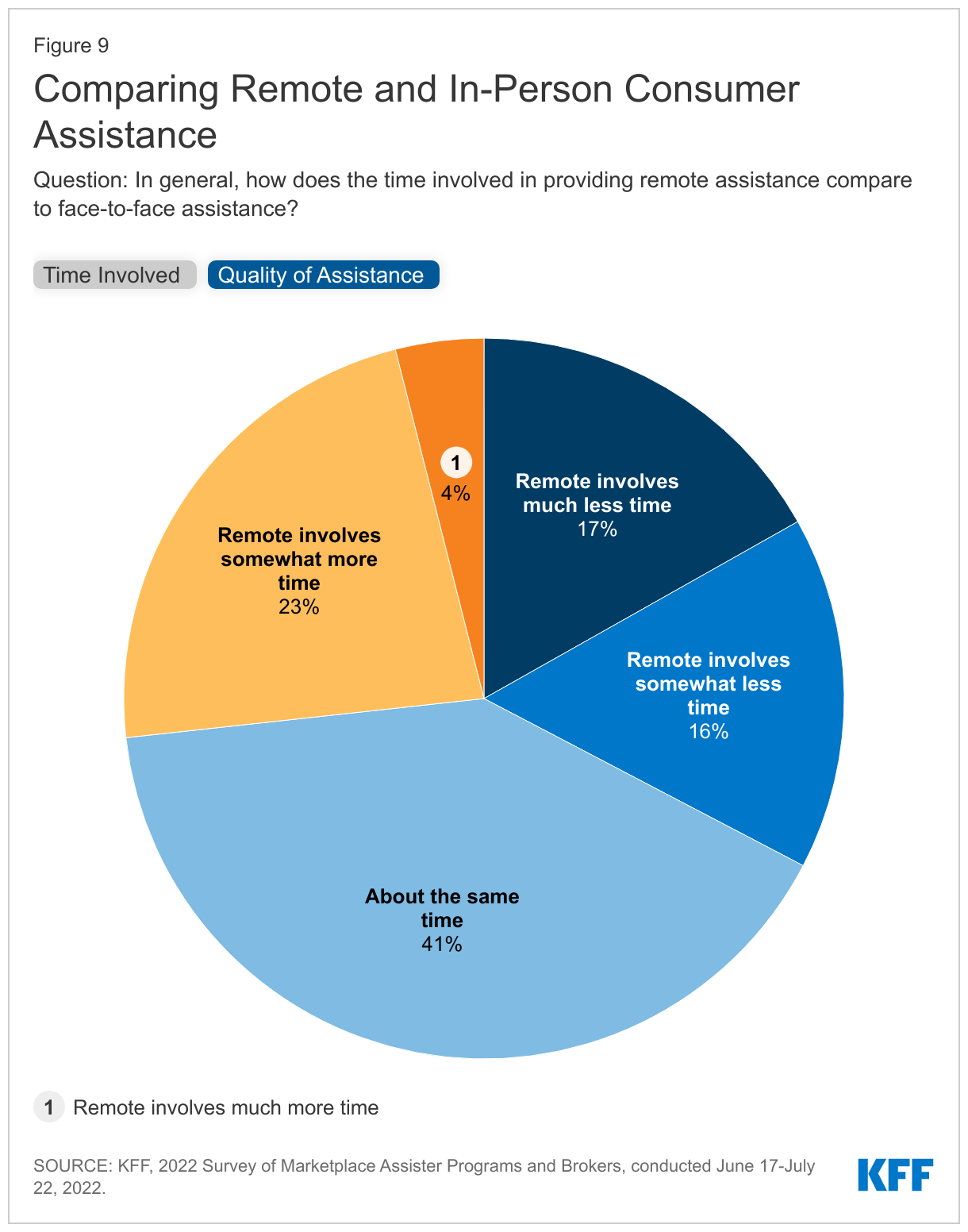

Assister Programs reported mixed experience with remote assistance. Among those who provided both in-person and remote assistance, one-third of Programs said remote assistance appointments generally took less time; 41% said remote appointments took about the same time and 27% said remote appointments generally took longer. Two-thirds of Programs who provide both types of assistance thought the quality of help they could provide was about the same compared to in-person appointments, while 26% said the quality of was not as high. (Figure 9)

Most assisters believe the number of plan choices is about right, but comparing Marketplace plan options posed challenges for some. In many states this year consumers faced a choice of more than 100 QHP options. While most Assister Programs (55%) said they thought the number of QHP choices offered their clients was about right, 34% of Programs said they often found it challenging to identify meaningful differences in QHP benefits and costs that their clients cared about.

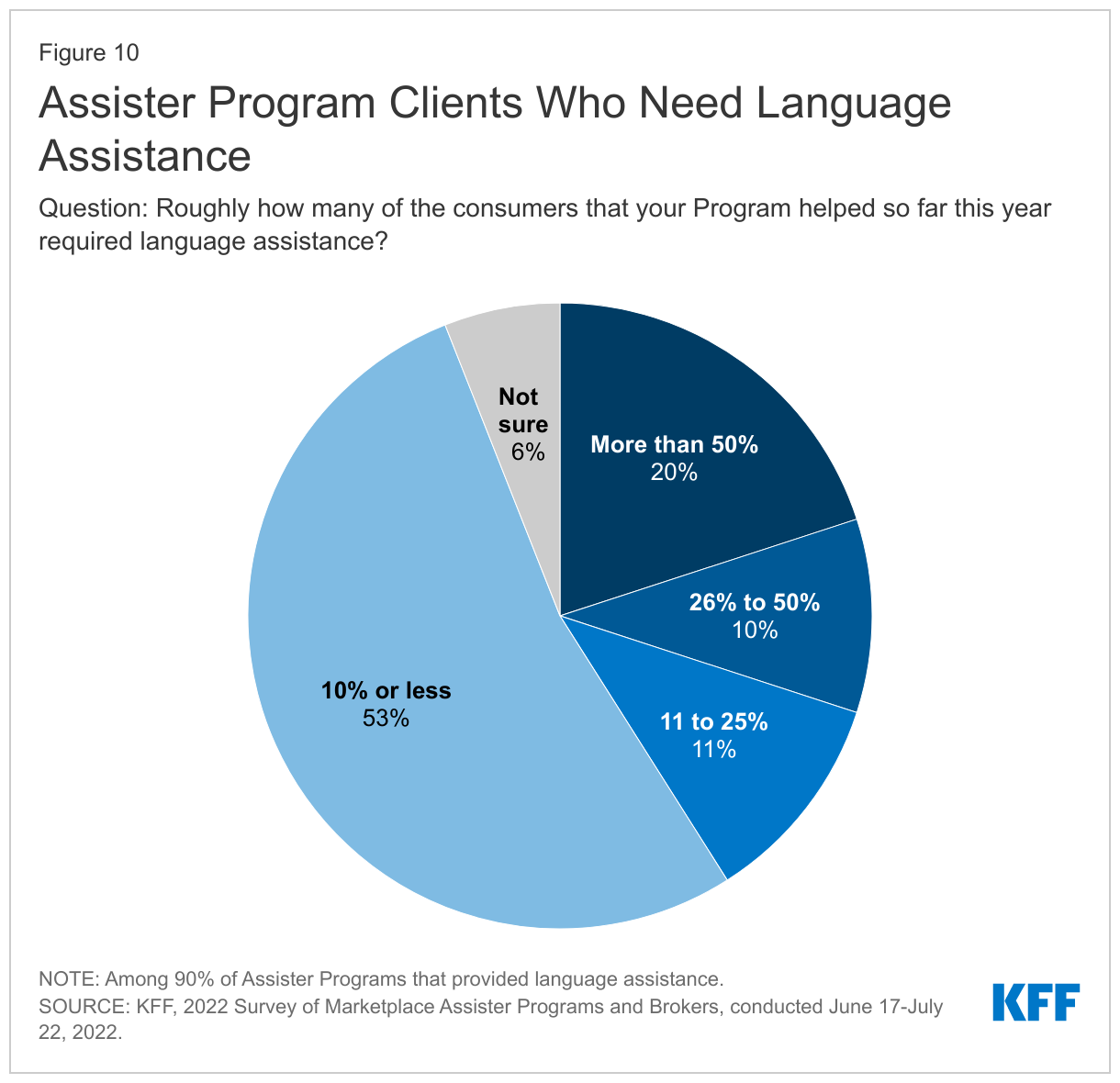

Most Assister Programs say they provided language assistance to their clients who needed it. Consumers with limited English proficiency require language assistance – help translating the Marketplace application and plan information into another language, or interpreter services to verbally communicate in another language, or both. Ninety percent of Assister Programs said they helped at least some consumers who needed language assistance. When we asked these Programs about the share of clients who required language assistance during the first half of 2022, 53% of Programs that provide language assistance estimated it was needed by up to 10% of their clients while 20% of Programs said more than half of their clients needed language assistance. (Figure 10)

Nearly three-quarters of Programs that help customers who need language assistance said they have bilingual or multilingual staff or volunteers. Most Programs that provided this help (61%) said they were able to meet clients’ language needs all or nearly all of the time, while 35% of Programs said they could do so most of the time. Even so, more than one-third of Programs that provided language assistance (39%) said it is at least somewhat difficult for their clients to access written information and materials translated into the language they need.

Some consumers need more complex help. Nearly all Assister programs (97%) reported helping at least some consumers with complex cases, i.e., those that either took longer-than-average to help or presented with problems that challenged Programs’ ability to help. Examples of complex cases could include families with mixed eligibility status for coverage and subsidies, consumers with volatile work status who have trouble estimating annual income, or consumers who need help providing extra documentation to verify their income, immigration, or eligibility status. Many (41%) Assister Programs said fewer than 10% of their clients presented with complex cases. But 10% said more than one-in-five clients presented with complex cases.

Assister Programs can access outside help with complex cases, though the effectiveness of help varies. For example, 85% of Assister Programs that helped people with complex cases said they sought help from the Marketplace call center’s first tier of customer service, including 51% who said the call center was helpful most or nearly all of the time and one quarter (24%) who said it was helpful rarely or less than half of the time.

HealthCare.gov offers help with complex cases that Assister Programs can access through a “complex case web form.” It is unclear how many Assister Programs may be aware of this help; 65% of FFM Assister Programs said they did not use this resource at all.

Nearly all Assister Programs (92%) said that if their Marketplace offered additional training in complex case topics in order to receive advanced certification, they would be interested to have one or more of their staff complete such advanced training.

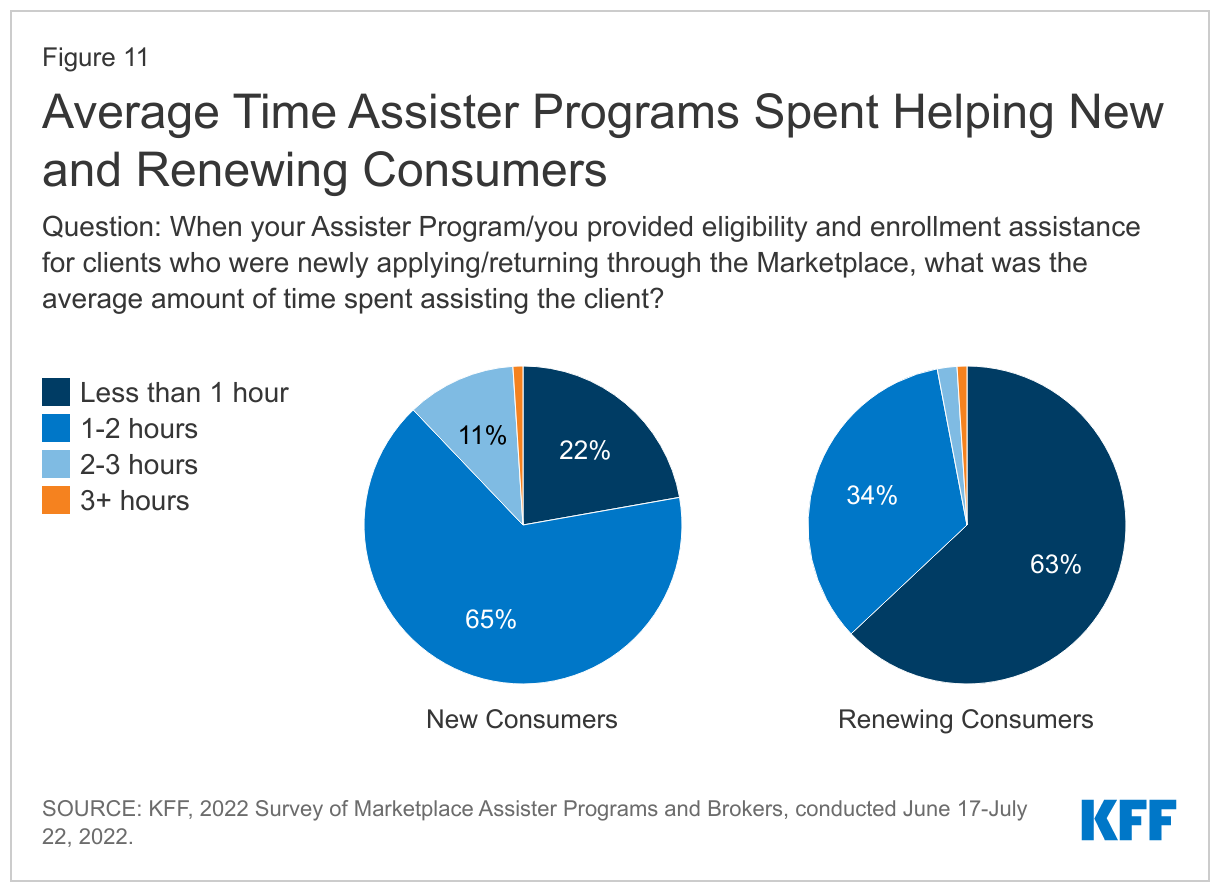

For these and other reasons, eligibility and enrollment assistance remains time intensive. As has been the case every year we conducted this survey, most Assister Programs (65%) reported that on average it took between 1 and 2 hours to help consumers who were applying to the Marketplace for the first time. For consumers returning to renew or change coverage, most Programs (63%) said n average appointments took less than 1 hour. (Figure 11)

Section 4: Consumer Assistance by Agents and Brokers

In addition to Marketplace Assister Programs, private health insurance agents and brokers (referred to as “brokers” in this report) also help consumers shop for health coverage. To be certified to sell Marketplace coverage, brokers must be licensed by a state to sell health insurance, register with the Marketplace, and complete the Marketplace required training. Brokers are not paid by the Marketplace, rather they earn commissions from insurers for each consumer they help enroll in a QHP. Distinct from Assister Programs, brokers are permitted to recommend specific plans to consumers. Marketplaces require brokers to provide consumers with correct information and prohibit marketing practices that are misleading, coercive or discriminatory. A 2020 report by the federal government estimated that nearly half of QHP enrollments through HealthCare.gov were broker-assisted, and the Federal marketplace continues to promote broker assistance on its Find Local Help page.

Most brokers who responded to the survey are licensed to sell health insurance in more than one state. Just over 1/3 of brokers certified to sell Marketplace coverage (37%) reported being licensed in a single state; 35% said they were licensed in 2-4 states, and 28% were licensed in five or more states. For survey questions about state-specific issues, we asked brokers to answer with respect to the state where they sell the most coverage.

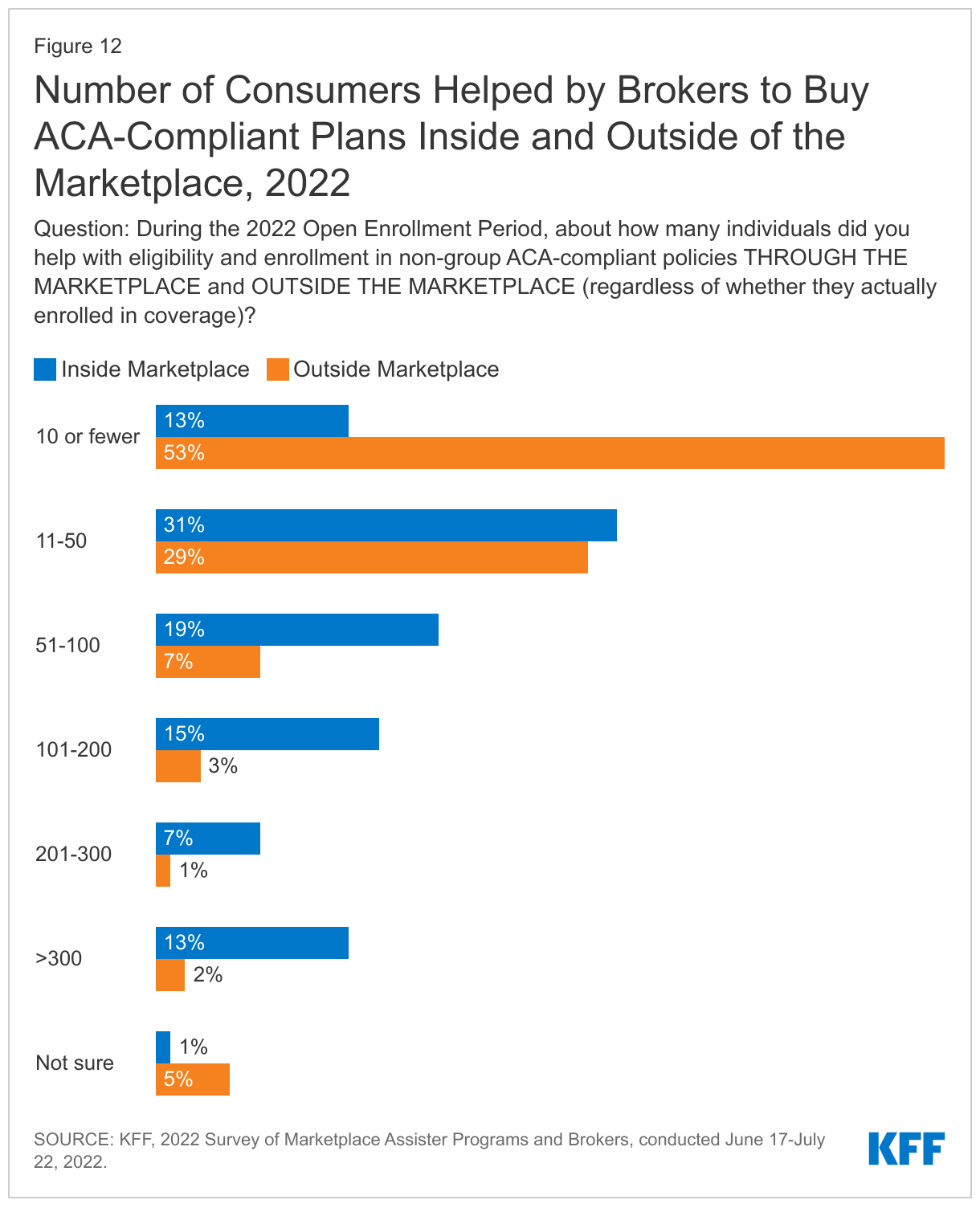

Most brokers (65%) helped up to 100 consumers with eligibility and enrollment through the Marketplace during the 2022 Open Enrollment period. However, one in five brokers helped more than 200 consumers. Brokers also continued to sell ACA-compliant policies offered outside of the Marketplace during 2022 Open Enrollment; such policies are not eligible for subsidies, and the volume sold was much lower. Most brokers (53%) said they sold no more than 10 ACA compliant-policies outside of the Marketplace during 2022 Open Enrollment. (Figure 12) This may be because the extension of premium subsidies to people with incomes above 400% of the poverty level created a strong incentive for these enrollees to switch to the marketplace.

Brokers also reported helping consumers with SEP applications this year and during the COVID-19 SEP. In the 6-month period after OE 2022 ended, 37% of brokers helped 10 or fewer consumers with SEPs, while 16% of brokers helped more than 50. In addition, 80% of brokers said they helped consumers helped apply for 2021 coverage during the special extended COVID Enrollment Period. Like Assister Programs, 75% of brokers reported that most or nearly all consumers they helped during this time were unaware of newly available ARPA subsidy enhancements and instead learned of them first from the broker.

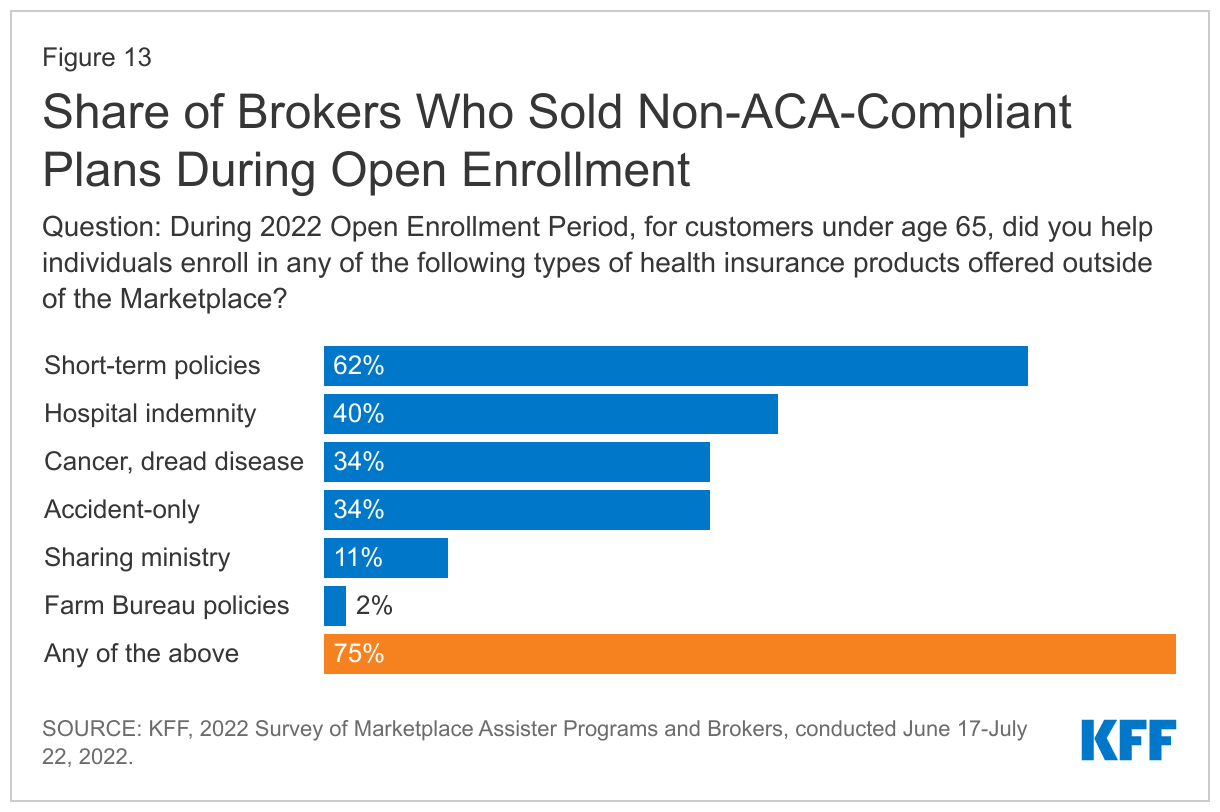

Broker assisted sale of non-ACA-compliant coverage

During the 2022 Open Enrollment period, most brokers (75%) reported they also helped consumers enroll in at least some types of non-ACA compliant plans sold outside of the Marketplace. Sixty-two percent of brokers who responded to the survey reported selling short-term policies (which exclude coverage of pre-existing conditions); 40% sold hospital indemnity policies (that pay a flat dollar per day in hospital benefits), 34% sold dread-disease policies (e.g. that only cover cancer), 34% sold accident-only coverage, 11% sold sharing ministry products and 2% sold Farm Bureau policies (neither of which are licensed as health insurance). (Figure 13)

However, brokers reported selling a much lower volume of non-ACA compliant policies than QHPs during Open Enrollment. Two-thirds of brokers who responded to the survey said that during the 2022 Open Enrollment, they sold 10 or fewer non-ACA compliant policies instead of or as a supplement to QHPs. Eight percent of brokers said they sold more than 50 such policies.

Comparing consumer assistance from brokers and Assister Programs

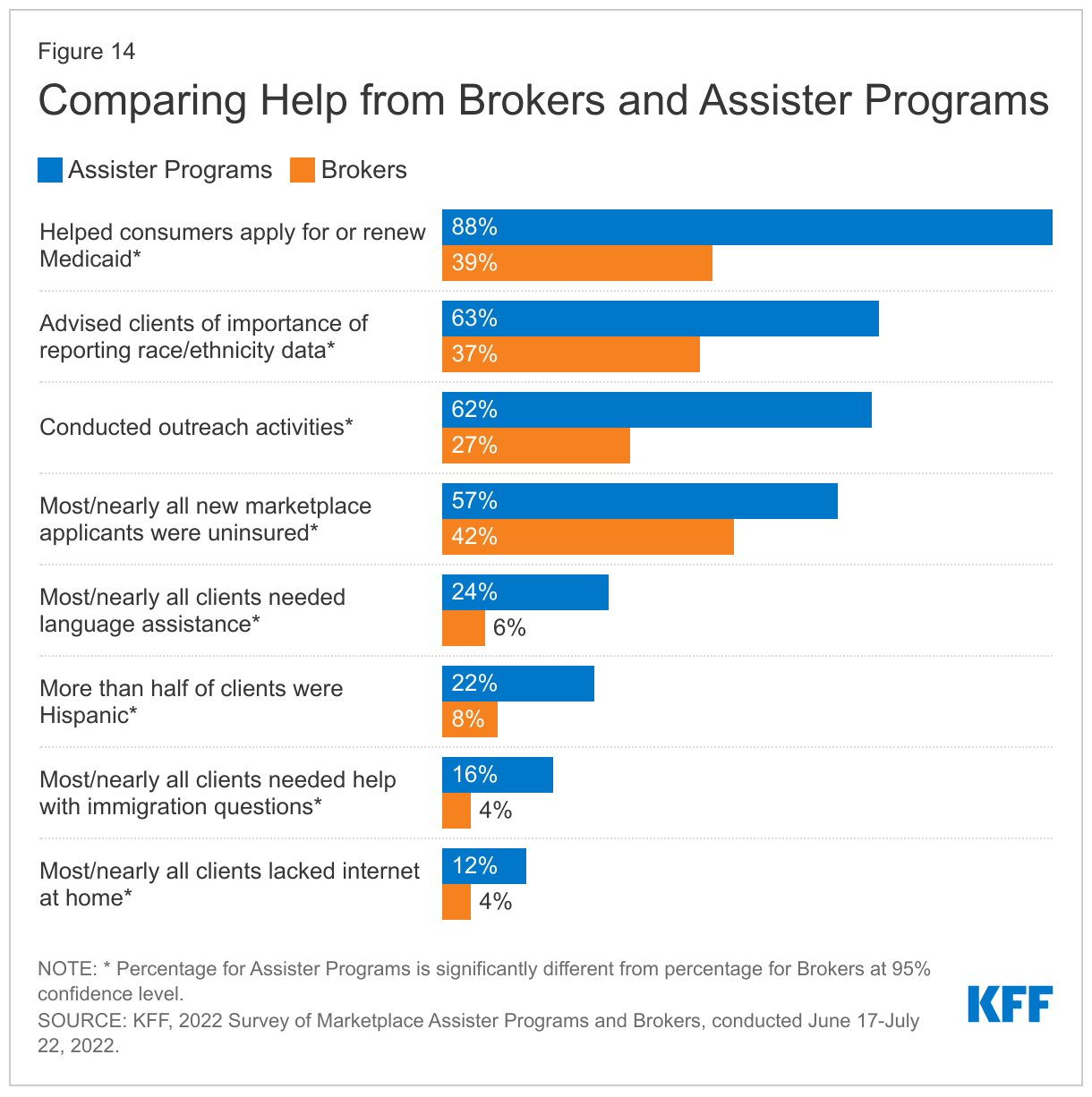

Help provided by brokers is similar in many respects to that provided by Assister Programs. As with Assister Programs, most brokers also report helping consumers apply for financial assistance, compare plan options, and understand how to use their insurance. The time involved in providing enrollment reported by brokers help mirrors that reported by Assister Programs. In other respects, though, the kinds of activities brokers report engaging in and the types of people they report helping are different compared to Assister Programs. (Figure 14)

- 39% of brokers said they help consumers apply for or renew coverage under Medicaid/CHIP, compared to 88% of Assister Programs. Among consumers they did help, most brokers (52%) said few or none of their clients were determined eligible for Medicaid or CHIP compared to 17% of Assister programs who answered the same. Brokers are not paid commissions by Medicaid.

- 27% of brokers said they conduct outreach activities to inform the public about the Marketplace, compared to 62% of Assister Programs.

- Brokers were less likely to report helping uninsured consumers; 42% of brokers who responded said most/nearly all new Marketplace applicants they helped were uninsured, compared to 57% of Assister Programs.

- Brokers were less likely to provide language assistance; 6% of brokers said most to nearly all people they helped during 2022 Open enrollment needed language assistance, vs. 24% of Assister Programs.

- Brokers were also less likely to report helping Hispanic consumers; 8% of brokers said at least half the people they helped during 2022 Open Enrollment were Hispanic, compared to 22% of Assister Programs. Brokers were also far less likely to say they advise their clients about the importance of reporting information about their race/ethnicity to the Marketplace; 37% of brokers said they do this, compared to 63% of Assister Programs who say they do.

- 4% of brokers said most or nearly all their clients needed help with immigration issues, and 4% said most/nearly all of their clients lacked Internet at home, compared to 12% and 16% of Assister Programs, respectively.

Broker use of alternatives to Marketplace web sites

For years, ACA-compliant policies have also been sold directly by insurers outside of the marketplace; but consumers who needed subsidies were re-directed from these “direct enrollment” (DE) sites back to the Marketplace to apply, then redirected back to the DE site to complete their enrollment. Starting in 2018, however, the federal government opened a new pathway for the sale of subsidized QHPs as an alternative to HealthCare.gov. These so-called enhanced direct enrollment (EDE) sites are privately operated, for example, by web-brokers. They coordinate with HealthCare.gov in the background, transmitting the consumer’s application and receiving the Marketplace’s eligibility determination for subsidies so that consumers can complete their application and select a plan entirely on the EDE site. EDEs offer an alternative to HealthCare.gov, but so far are not permitted in state-based marketplaces.

EDE sites generally are required display all QHP information shown on HealthCare.gov shows, though sites are permitted to not display information on QHPs they are not authorized to sell. In such cases, EDEs must display a notice that consumers can see additional plan information on HealthCare.gov. EDEs also can display QHP information in a different order, but cannot favorably display QHPs based on the web-broker’s commission.

CMS has promoted development of EDEs in recent years and reports that enrollment in QHPs through DE and EDE channels is increasing, accounting for 37% of QHP plan selections during the 2021 Open Enrollment period.

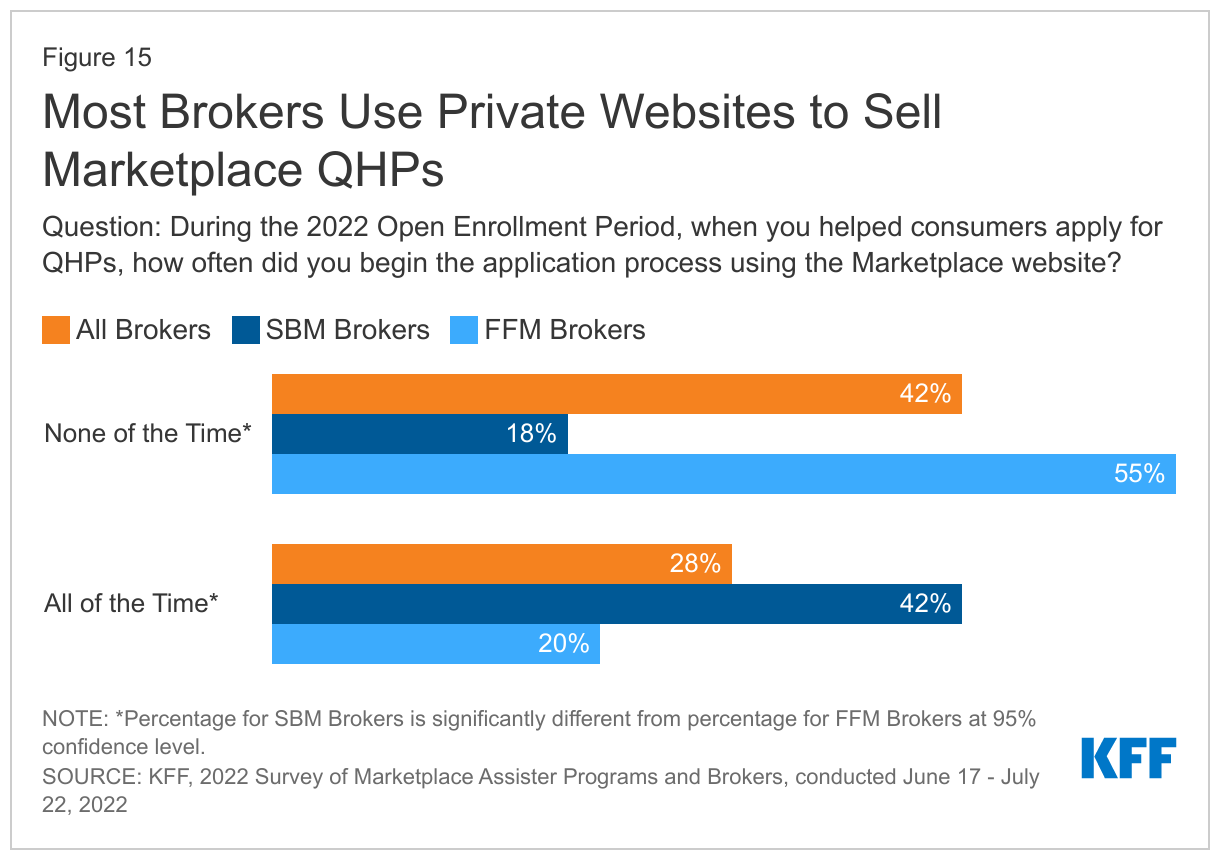

Only 28% of brokers initiate all QHP applications on the Marketplace web site. Most brokers (55%) selling QHPs in FFM states in 2022 said they never initiate applications on HealthCare.gov. In SBM states where DEs are an option but EDEs are not, 42% of brokers said they initiate all QHP applications on the Marketplace web site. (Figure 15)

When asked why they rely on private sites over the Marketplace, brokers named several key reasons. Sixty-two percent of brokers who did not always use the marketplace site said it generally takes less time to complete a QHP application on a private site. Sixty-one percent said private sites offer a dashboard or other tools they can use to track the status of their client applications and accounts. Many also cited tools on private sites that that let them track client notices from the Marketplace (48%), or communication tools to help them contact clients (43%). A smaller share said they use private sites because there they can also show consumers other lines of insurance, such as life insurance policies (15%), or non-ACA compliant policies (10%). Federal rules require that such products must be displayed at separate tabs.

Finally, we asked brokers who use alternative enrollment sites if they would use the Marketplace site more often if it offered a secure broker portal that gave them direct access to client accounts and tools to facilitate tracking and communication with clients; 60% said they would, 11% said they would not, and 30% were not sure.

Section 5: The Public Health Emergency Unwinding

Provisions in the Families First Coronavirus Response Act (FFCRA), enacted at the start of the pandemic, prohibit states from disenrolling people from Medicaid until the month after the COVID-19 public health emergency (PHE) ends. This Medicaid continuous enrollment requirement has prompted a substantial increase in Medicaid enrollment during the pandemic. However, once the PHE ends, which is expected sometime in 2023, states will resume Medicaid redeterminations and will disenroll people who are no longer eligible or who are unable to complete the renewal process even if they remain eligible. As a result, KFF estimates that between 5 and 14 million people could lose Medicaid coverage.

Consumers enrolled in Medicaid today may need more help to remain covered next year. As states resume eligibility redetermination millions of current enrollees may no longer be eligible for Medicaid because of changes in income or other circumstances or may be disenrolled, despite remaining eligible, if they are unable to complete the redetermination process. Medicaid enrollees may need help completing the renewal process and, to avoid becoming uninsured, those who are no longer eligible for Medicaid may need help transitioning to other coverage. Many consumers who are disenrolled due to higher incomes will likely be eligible for subsidized Marketplace coverage, and the extension of enhanced subsidies in the Inflation Reduction Act (IRA) will make the transition easier. However, the 2021 special COVID enrollment experience showed that many such consumers may not be aware of this affordable coverage alternative. Further complicating the situation, the termination of the PHE will occur after the end of the Marketplace Open Enrollment Period and while individuals will qualify for 60-day SEP when they lose Medicaid coverage, that may not be enough time to enroll in Marketplace coverage, especially if they are not aware of the option or how to apply.

About half of Assister Programs (53%) said they have a good working relationship with their state Medicaid agency and are regularly in touch about matters affecting consumer eligibility and enrollment. But 36% of Programs said they have only limited contact, and 12% said they do not interact with their state Medicaid agency much if at all. In part because of these working relationships with Medicaid agencies, two-thirds of Assister Programs reported being familiar with their state’s plan for resuming routine operations once the PHE ends.

Most Assister Programs reported proactively reaching out to their states to explore ways to help consumers. Nearly six in ten Assister Programs (58%) said they had contacted their state to explore ways to educate consumers about the need to renew their Medicaid coverage. Given their broader scope of responsibilities, Navigator Programs were more likely than other Programs to report contacting their state (73% vs. 55%). Conducting outreach to consumers to inform them of steps they will need to take to complete the renewal process, and to provide assistance when needed, could help reduce the likelihood that eligible individuals will lose coverage because they could not complete the process.

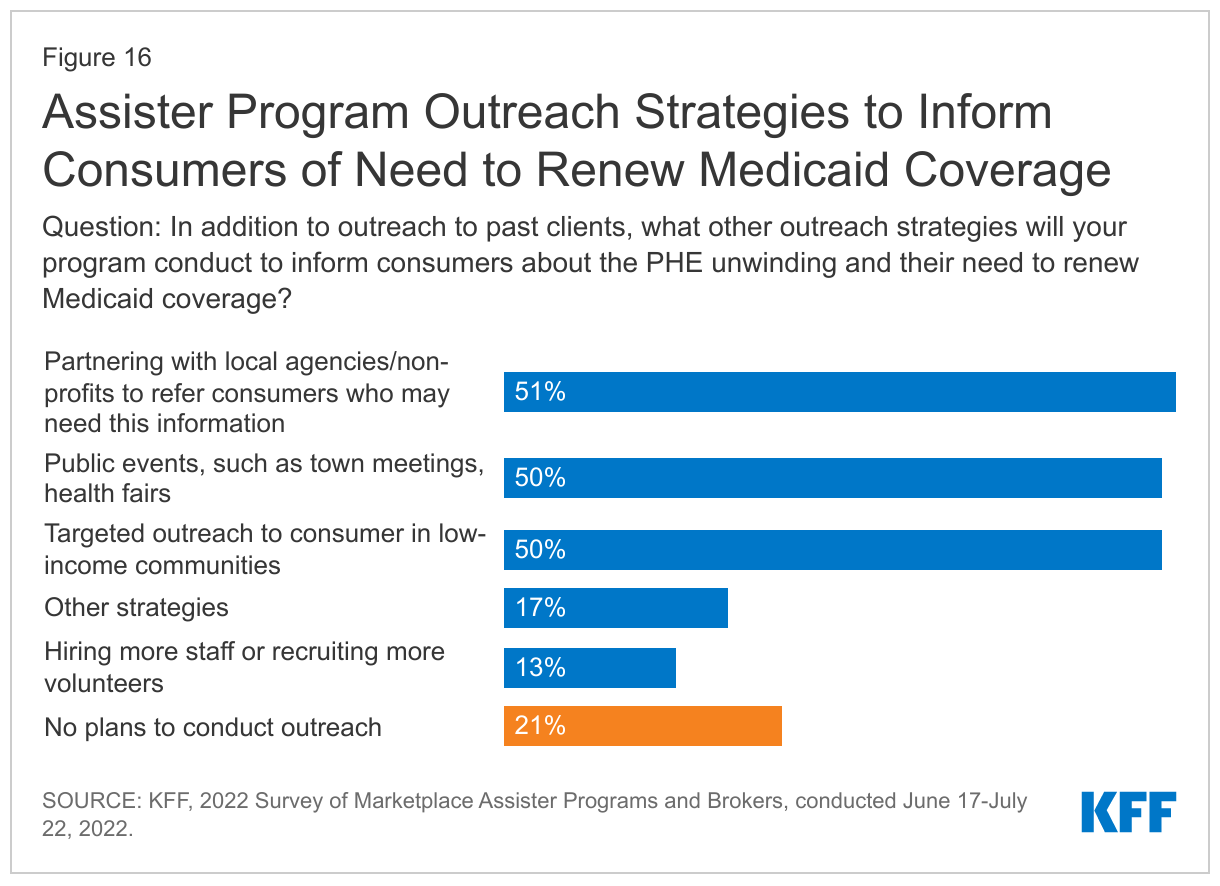

Most Assister Programs reported planning outreach activities to raise consumer awareness about the end of the PHE. About half of Assister Programs said they were planning public education events, targeted outreach to consumers in low-income communities, or to partner with local agencies or non-profits to refer consumers who need additional information (Figure 16). A smaller share (17%) of Assister Programs reported adopting other outreach strategies, including social media outreach campaigns, engaging local media to educate the public through stories on the PHE unwinding, and partnering with other community groups that serve low-income people. Fewer Programs (13%) said they planned to hire more staff or recruit more volunteers.

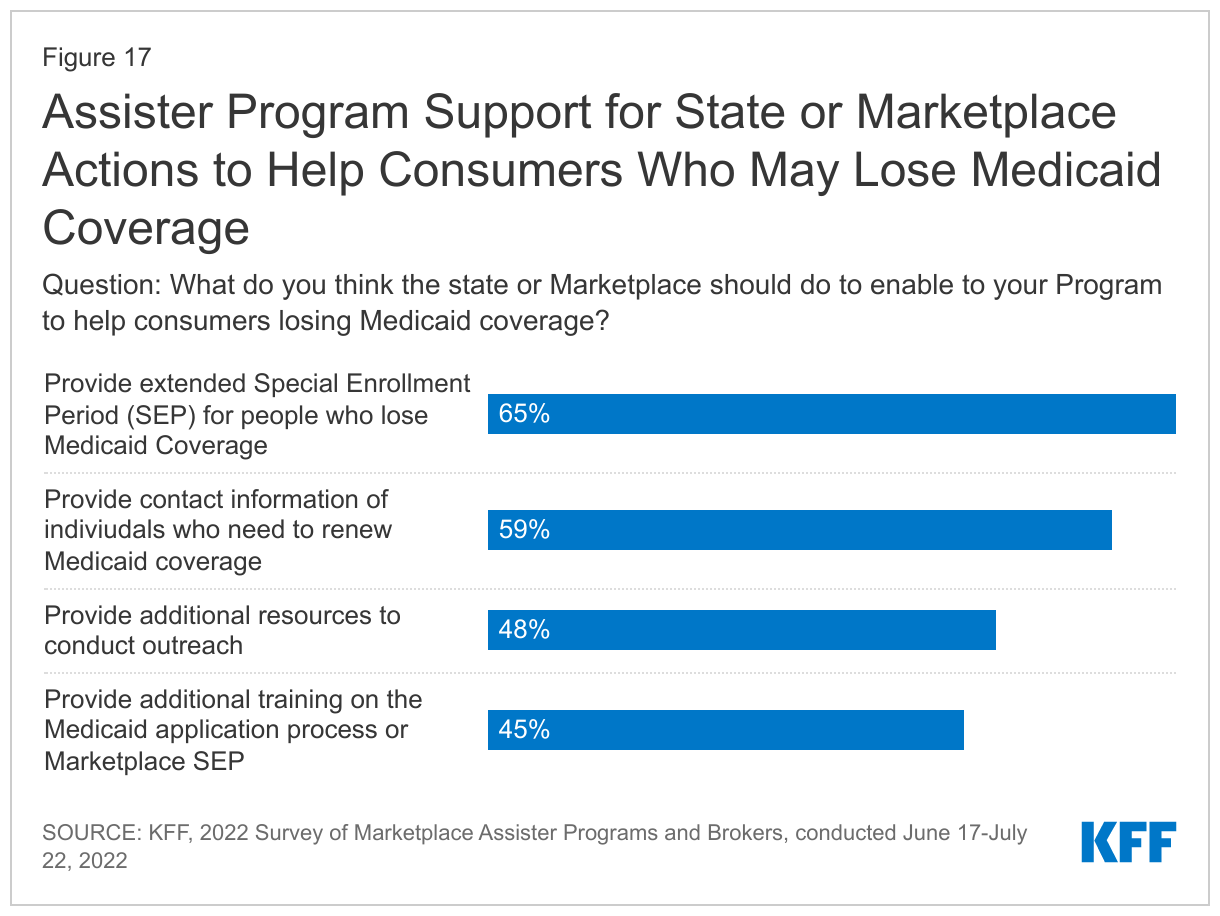

Assister Programs expressed support for additional actions states could take that would enable them to help consumers retain Medicaid or transition to other coverage. More than six in ten Assister Programs (65%) said they thought the state or Marketplace should provide an extended SEP for people losing Medicaid coverage to enroll in Marketplace coverage. while 59% supported the state sharing contact information on individuals who need to renew their Medicaid coverage. Nearly half of Assister Programs also supported having the state provide additional resources to conduct outreach and/or hire more staff and provide additional training on the Medicaid application process or Marketplace Special Enrollment Periods (Figure 17).

Both Assister Programs and brokers indicated they will try to re-contact Medicaid clients to update contact information, and most were confident they could reach their clients. About six in ten (58%) Assister Programs and about four in ten (38%) brokers surveyed said they would try to collect updated contact information from Medicaid clients they had helped in the past two years. Providing updated mailing addresses and other contact information to the Medicaid agency can help ensure enrollees receive renewal and other notices and any requests for information. If enrollees do not respond to these requests for information or documentation, even if they do not receive the request, their Medicaid coverage can be terminated. Among Assister Programs and brokers indicating they would re-contact Medicaid clients, eight in ten (83% of Assister Programs and 80% of brokers) said they were very or somewhat confident they would be able to reach those clients.

Few Assister Programs (29%) and brokers (9%) expect the Medicaid agency to provide them with information on consumers who may be eligible for Marketplace coverage, although nearly half were unsure of their state’s plans. Under certain circumstances], states can share information with trusted partners, including information on consumers who are disenrolled from Medicaid and likely eligible for subsidized coverage in the Marketplace. These consumers will need to complete a Marketplace application to obtain coverage. Assister Programs can educate consumers about the process and assist them with completing the application.

Although the number of people needing assistance with Medicaid renewals and other issues is expected to increase, most Assister Programs and brokers said they could serve all consumers who seek help. Nearly 60% of Assister Programs and brokers reported having enough resources to serve the all the clients who will need help renewing their coverage or applying for Marketplace coverage after being disenrolled from Medicaid. 17% of Assister Programs and 16% of brokers said they did not have adequate resources while about a quarter were unsure.

Appendix

Appendix: Characteristics of Assister Programs

Three types of Marketplace Assister Programs were surveyed for this report.

Navigator Programs – The ACA requires all Marketplaces to establish and fund Navigator Programs to provide outreach and enrollment assistance to all consumers. Navigators are required to have expertise in eligibility and enrollment rules, the range of qualified health plan (QHP) options, affordability programs – both QHP subsidies and Medicaid/CHIP – the needs of underserved and vulnerable populations, including individuals with limited English proficiency, and privacy and security standards. Navigators must offer objective advice to consumers. They must not be operated by insurance companies nor receive compensation from insurers; and they may not help with enrollment in any private health coverage offered outside of the Marketplace. At least one Navigator grantee in each state should be a community-based non-profit organization. Navigator Programs tend to be the consumer assistance workhorse – compared to other Assister Programs, they are more likely to operate statewide service areas, serve a higher number of clients, and operate with larger budgets; although some Navigator Programs are small, local, and have more limited resources. For the 2022 coverage year, state and federal Marketplaces provided a combined $162.2 million in funding for Navigator Programs. (Total does not reflect spending for New Mexico or Washington state.) Of this total, the federal Marketplace awarded $90.2 million and SBMs together awarded $72 million.

Certified Application Counselor Programs (CACs) – Marketplaces are also required to recognize, certify, and provide training for CAC Programs sponsored by non-profits and provider organizations. This Assister Program designation was created prior to the first Open Enrollment – when funding for Navigators, at least in the FFM, was still uncertain – to ensure that willing volunteer Programs would also be available to help. Under federal rules, CAC Programs are not required to engage in all activities required of Navigators, and do not undergo training as extensive as that required for Navigators. CAC Programs generally do not receive funding support from the Marketplace; they are primarily supported by their own sponsoring organizations and other outside sources such as foundations. For the 2022 coverage year, a total of 1,756 CAC Programs served Marketplace consumers.

Federally Qualified Health Centers (FQHCs) – The federal government supports a network of nonprofit health clinics in the US to provide health care to uninsured, low-income, and other underserved populations. Starting in 2014, the federal government required FQHCs to also provide outreach and enrollment assistance to consumers seeking coverage through the Marketplace and provided additional funding for this purpose. Of the 1,334 FQHCs surveyed, 85 are also certified as Navigators and shown as Navigator Programs in this report. The other 1,249 must complete CAC training to be Marketplace certified and are shown as FQHC Programs in this report. For the 2022 coverage year, the federal government provided FQHCs $150 million to support enrollment assistance.

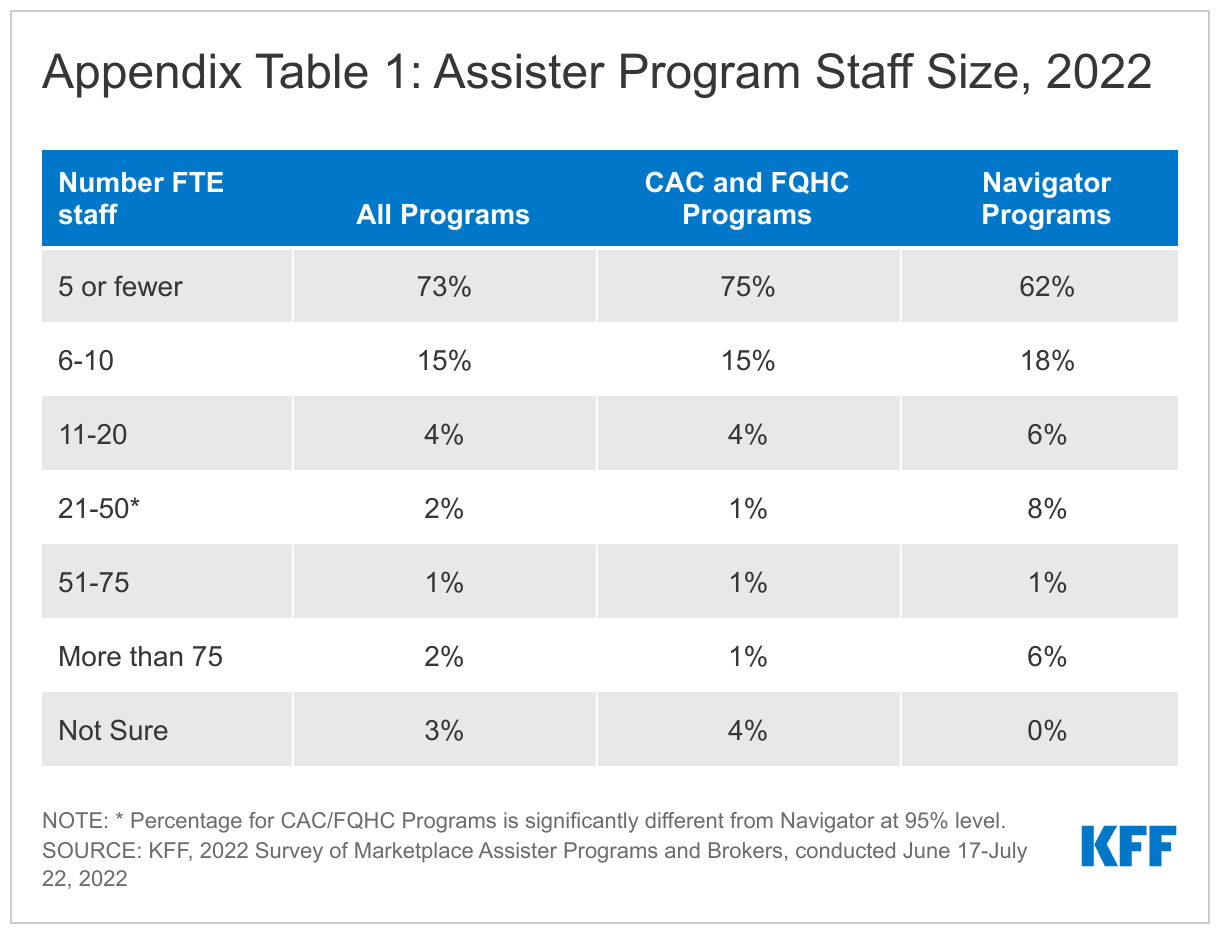

While the size of Assister Programs varies, most had a relatively small number of full-time equivalent staff during the 2022 Open Enrollment. Most Assister Programs (73%) indicated that they had five or fewer FTEs during the 2022 Open Enrollment, while 15% had between 6 and 10 FTEs. Navigator Programs had somewhat larger staff compared to the other Program types. (Appendix Table 1) Assister Programs report nearly all FTE staff were paid, not volunteer. Most Assister Programs (66%) indicated that the number of FTEs in 2022 was about same as in prior year; 13% say FTE staff grew from 2021 while 21% of Programs said staff size is smaller than in the year before.

Staff continuity in Assister Programs is high. 77% of Programs say most or almost all staff this year worked for them during the previous year’s Open Enrollment. Program staff typically work year-round, not just during Open Enrollment; 71% of Programs say staff size held steady since the 2022 Open Enrollment Period ended; while 21% of Programs say the number of FTEs has since declined.

Assister Programs were confident that the current level of funding will be available for 2023.Seventy-eight percent of all Assister Programs are very or somewhat confident current funding will continue for 2023. The highest rate of confidence is among Navigator Programs (93%), followed by FQHC (76%) and CAC Programs (68%). Following years of funding cuts, Federal marketplace Navigator funding was significantly increased for the 2022 Open Enrollment to $80 million, with a supplemental $10.2 million awarded shortly thereafter. For 2023, CMS has announced Federal Marketplace Navigator grants of $98.9 million (grants were announced after this survey closed.) Currently CMS cooperative agreements with Navigator Programs are for a 3-year period, through August 2024, though annual funding amounts are determined each year and not guaranteed.