As ACA Marketplace Enrollment Reaches Record High, Fewer Are Buying Individual Market Coverage Elsewhere

With Marketplace enrollment at a record high in early 2023, the upcoming open enrollment period could be among the busiest yet. In addition to Marketplace enrollees renewing coverage, uninsured people and those buying individual coverage off-Marketplace – as well as those losing Medicaid coverage as the pandemic-era continuous enrollment provision unwinds – may want to check if they are eligible for expanded subsidies under the Inflation Reduction Act.

This analysis looks at how many people are signed up for each type of individual market coverage—both on- and off-Marketplace and with or without subsidies—as of early 2023. The number of people enrolled in compliant and non-compliant plans was also evaluated up to 2022, the latest year this data is publicly available. A key takeaway from this analysis is that as Marketplace enrollment has reached record highs with enhanced premium assistance, fewer people are buying coverage off-Marketplace, but the overall individual market is nonetheless growing.

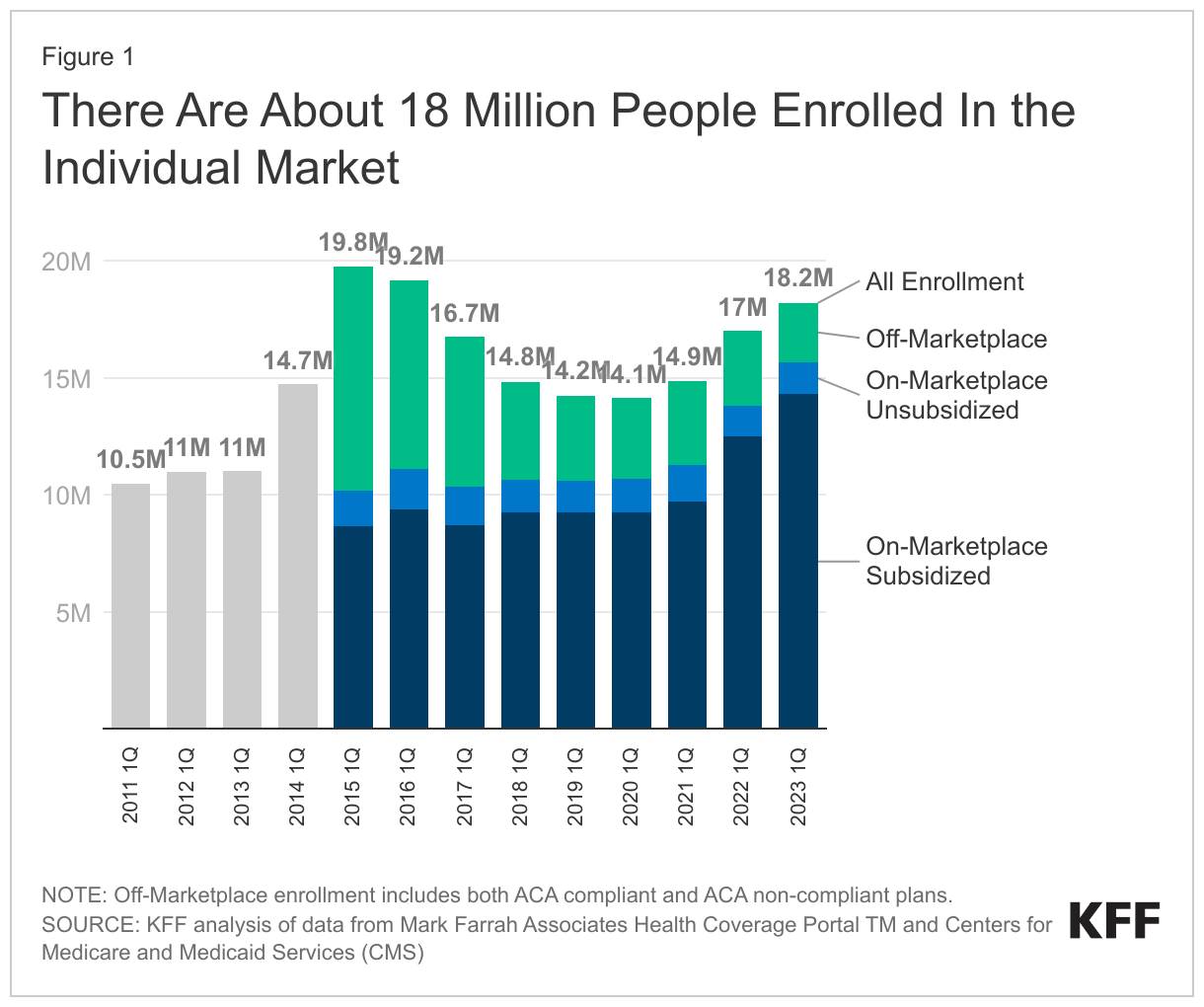

Individual market enrollment continues to grow, driven by enhanced subsidies. As of early 2023, an estimated 18.2 million people have individual market coverage, the highest since 2016 (Figure 1). The individual health insurance market grew rapidly in the early years of ACA implementation, reaching nearly 20 million people in early 2015, nearly double the approximately 11 million signed up before the ACA. However, these enrollment gains were partially offset by subsequent declines driven by steep premium increases, particularly among people not receiving subsidies. By early 2020, the individual market had declined to about 14 million enrollees.

During this period of decreasing individual market enrollment, subsidized enrollment increased from 2017-2019 which corresponds with the Trump Administration ending federal cost-sharing reduction (CSR) payments; this led to insurers “silver loading” premiums for CSRs and increased premium subsidies for some.

With passage of enhanced subsidies in the American Rescue Plan Act (ARPA), combined with boosted outreach and an extended enrollment period, 2021 marked the first year since 2015 when there was an increase in individual market enrollment. Individual market enrollment grew about 5% from 14.1 million in first quarter 2020 to 14.9 million in first quarter 2021.

The ARPA’s subsidies didn’t simply bring people from off-Marketplace plans to the Marketplace; the subsidies also helped bring overall individual market enrollment higher, up to 18.2 million in early 2023, an increase of about 29% from early 2020.

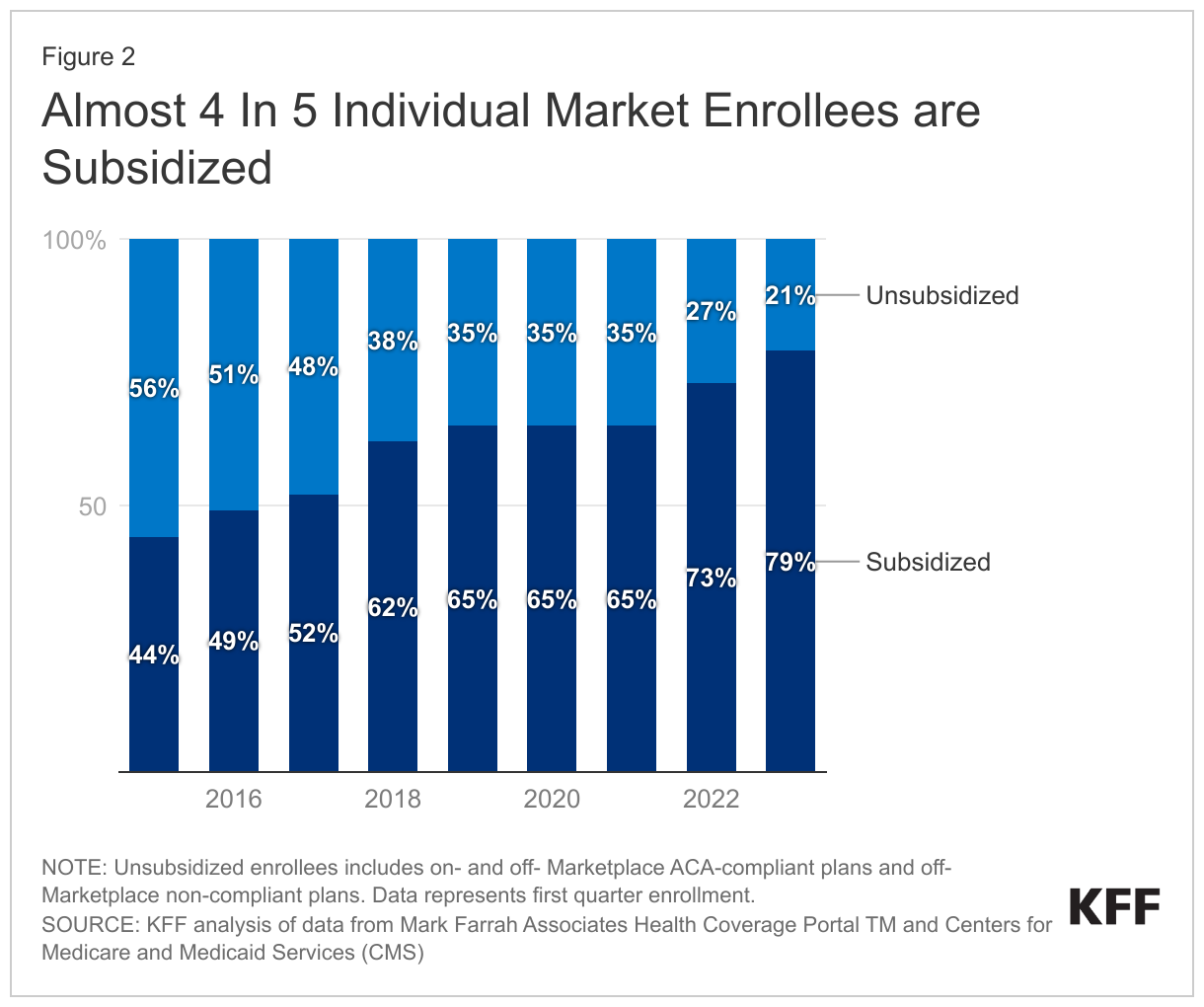

Now, with enhanced subsidies in place, the vast majority of people buying individual market coverage are subsidized. The Inflation Reduction Act continues the ARPA subsidies without interruption for another three years through 2025. That means premiums are capped for people with incomes over 400% of the poverty level ($120,000 for a family of 4 in 2024) who were ineligible for subsidies previously, and those who were already eligible for subsidies are paying even less than they were before. Overall, about 4 in 5 individual market enrollees are now subsidized (Figure 2) – the highest share since the ACA was implemented – and some of those who aren’t receiving a subsidy might find they are eligible if they moved onto the Marketplace.

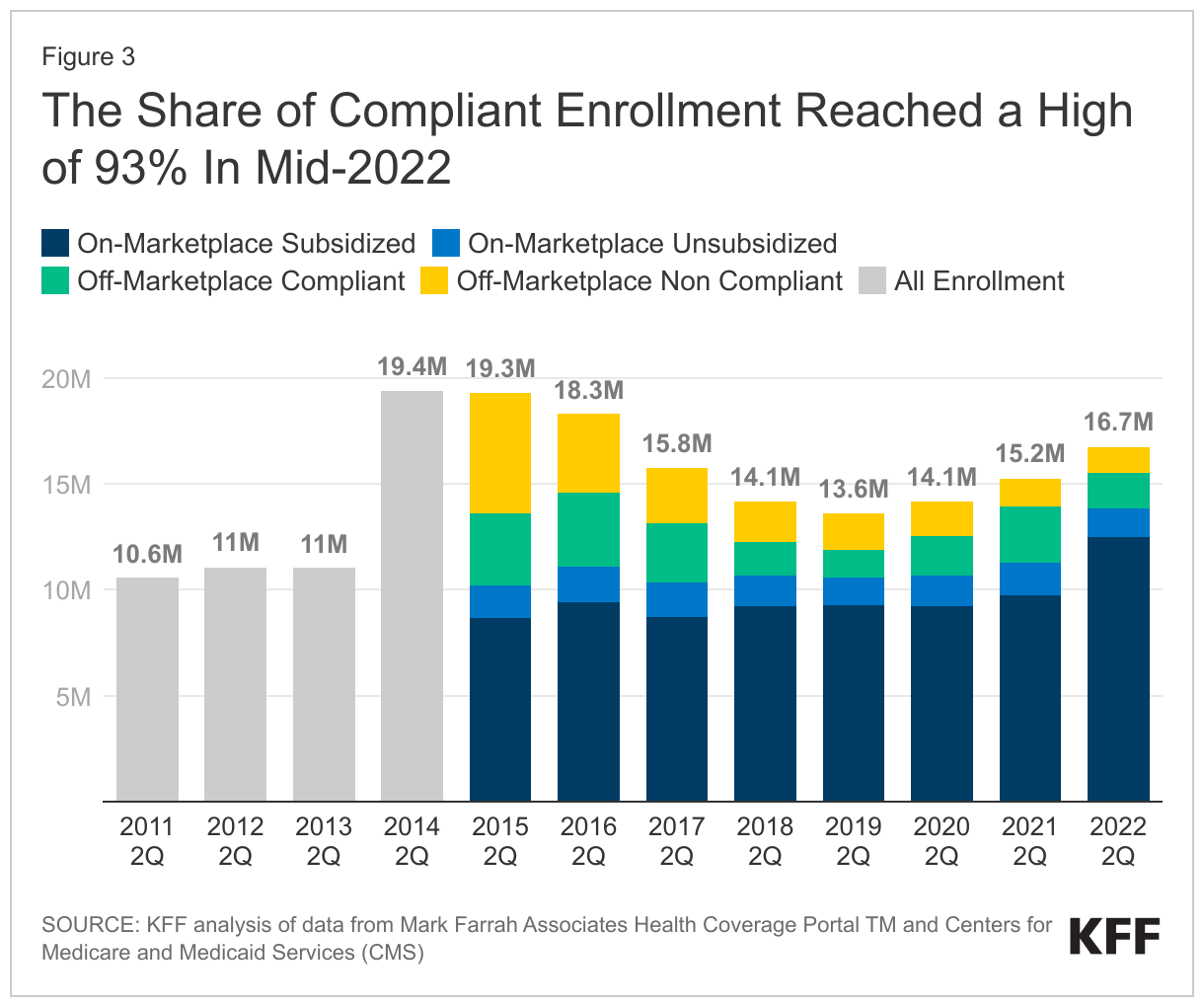

Heading into 2024 open enrollment, we estimate there are still about 2.5 million people buying unsubsidized coverage off-Marketplace, including some in non-ACA-compliant plans (like grandfathered and short-term plans). Early 2023 off-Marketplace enrollment decreased by 20% compared to early 2022. Despite Trump Administration efforts to promote non-compliant coverage, the number of people in non-compliant plans has fallen each year.

While enrollment in non-ACA-compliant plans is at a record low, a substantial number continue enrolling in non-compliant plans. Using federal risk adjustment data and data compiled by Mark Farrah Associates, we estimate 1.2 million people were in non-ACA-compliant plans in mid-2022, compared to 5.7 million in mid-2015 (Figure 3). Although we don’t yet have complete 2023 data, it’s likely ACA-compliant enrollment (both on- and off-Marketplace) is currently at a record high and that non-compliant enrollment is at a record low.

Non-compliant short-term plans often do not include certain benefits or coverage for pre-existing conditions, and can impose a dollar limit on insurance coverage. For example, of short-term plans reviewed, none covered maternity care, most didn’t cover prescription drugs, about half didn’t include mental health or substance use treatment, and most imposed a dollar limit on covered services or drugs. The Biden Administration’s proposed rule, which would reverse Trump Administration’s expansion of short-term plans, may further reduce enrollment in non-compliant plans if it is finalized.

The share of individual market enrollment in ACA compliant plans has increased to 93% in mid-2022 compared to 71% in mid-2015. These data are only available through mid-2022, and non-compliant enrollment may have fallen even further in 2023.

Some off-Marketplace enrollees will find they are still ineligible for subsidies, even with enhanced subsidies. Undocumented immigrants and people with affordable offers of employer coverage are ineligible for Marketplace subsidies. Additionally, although there is no longer an upper income limit for subsidies, people with higher incomes who would pay less than 8.5% of their income for an unsubsidized benchmark silver plan do not qualify for subsidies because their premium isn’t high enough to trigger financial help. Even so, some of the latter group may find it advantageous to purchase on the Marketplace because if they experience midyear changes in their income or other circumstances, they may begin receiving subsidies mid-year without changing plans or they could retroactively claim a subsidy when they file taxes.

Yet others who were previously ineligible for Marketplace subsidies may now be eligible. For example, the Biden Administration’s fix to the “family glitch” means dependents of workers, who have affordable self-only coverage but unaffordable family coverage through their employers, can get Marketplace subsidies starting in 2023.

Marketplace enrollment data are as of the first quarter of 2023. In the second quarter of 2023, states started to disenroll people from Medicaid, some of whom may be signing up for subsidized Marketplace coverage.

How might future premium increases affect people in the individual market? Looking back over the last ten years of the ACA, changes in individual market enrollment closely mirror changes in what people had to pay for coverage. In years when premiums were rising steeply from 2016-2018, unsubsidized individual market enrollment fell. When premiums held mostly steady from 2019 to 2020, so did individual market enrollment. Then, as new subsidies became available in 2021-2023, individual market enrollment picked up again, driven by an increase in the number of subsidized enrollees.

Heading into 2024, we may see unsubsidized premiums rise, pushed up by rising health care prices and utilization. However, unlike when premiums rose in past years, the Inflation Reduction Act’s enhanced subsidies could shield the vast majority of individual market enrollees from increases, even those with higher incomes. In fact, some people who aren’t subsidized in 2023 may find premium increases in 2024 make them newly eligible for subsidies (if their benchmark premium rises above 8.5% of their income). But, to take advantage of subsidies, they would need to shop on the Marketplace during open enrollment.

Methods

Federal enrollment and risk adjustment data were combined with administrative data insurers report to state regulators, as compiled by Mark Farrah Associates, to determine the number of enrollees in each type of individual market coverage. Early effectuated enrollment reports (available for years 2015-2023) were used to determine the number of on-Marketplace and subsidized enrollees. Risk adjustment data (available for years 2014-2022) were used to determine the total number of enrollees in ACA-compliant plans. The number of compliant enrollees in Massachusetts and Vermont in 2015-2021 and Massachusetts in 2022 was estimated using a ratio of total Exchange enrollment to total compliant enrollment in all the other states.

Mark Farrah Associates data were used to estimate the total number of enrollees in the individual market. Because some plans do not file quarterly data, we adjust these plans’ enrollment numbers based on enrollment changes seen in plans that do file quarterly. We also remove likely Children’s Health Insurance Program, or CHIP, enrollees from the individual market total.