How Could the Build Back Better Act Affect Uninsured Children?

Issue Brief

While current federal debate over policies to extend health insurance coverage to the remaining uninsured are largely focused on the 2.2 million people in the coverage gap and extension of increased premium help under the Affordable Care Act (ACA), which primarily benefit adults, many children (4.3 million1 ) in the US were uninsured in 2020. Further, the number of uninsured children has been increasing in recent years: after steadily declining in the years prior, the uninsured rate for children increased significantly from 2016 to 2020, growing by 0.7 percentage points or over 450,000 children.2 Most of the changes during this period occurred from 2016 to 2018, with the overall children’s uninsured rate remaining stable from 2018 to 2020. The vast majority of uninsured children are already eligible for Medicaid or CHIP, so policy action to extend children’s coverage largely focuses on enrollment and retention. Outreach to inform children and families about Medicaid/CHIP coverage may facilitate child enrollment, and continuous eligibility requirements for Medicaid/CHIP could prevent loss of coverage. Research also shows that expanding coverage for adults in households with children also can increase children’s coverage, so recent federal efforts to extend coverage for adults in the coverage gap could have spillover effects for children’s coverage.

This brief examines characteristics of uninsured children in 2020 and discusses how current policy proposals, including outreach efforts, continuous eligibility requirements, and closing the coverage gap, could affect children’s health coverage. Recent efforts to expand coverage for adults could benefit children’s coverage, especially for children in non-expansion states if the coverage gap is filled as proposed by the Build Back Better Act (BBBA).

What do we know about uninsured children?

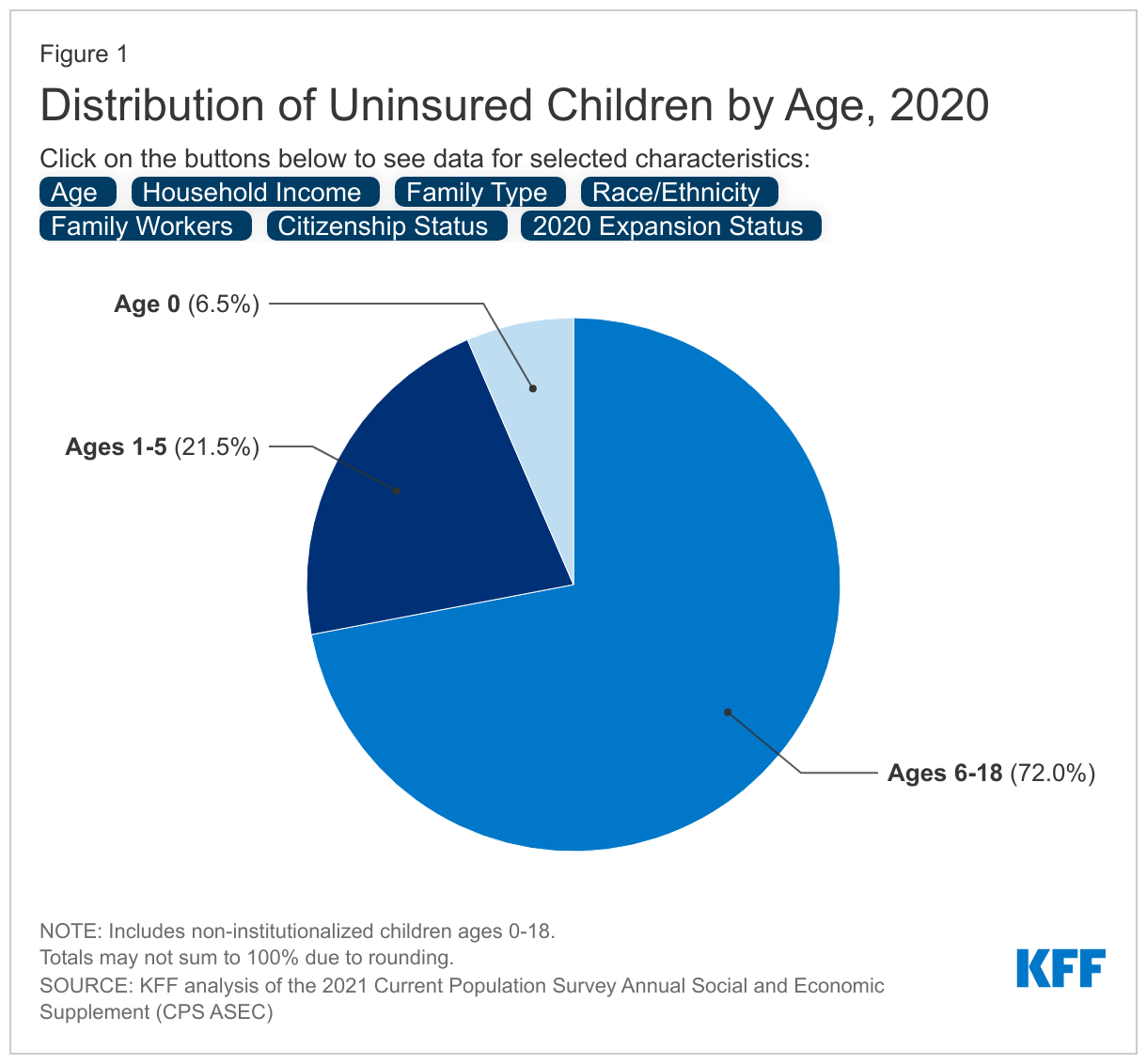

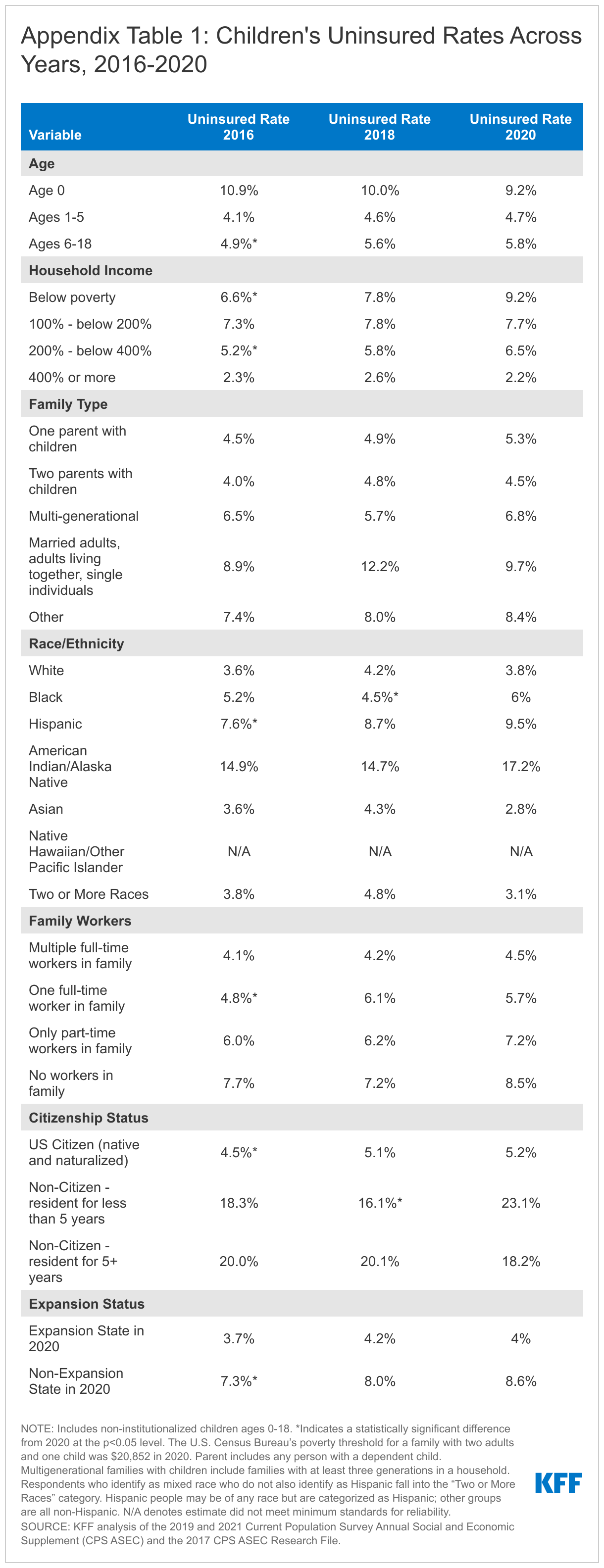

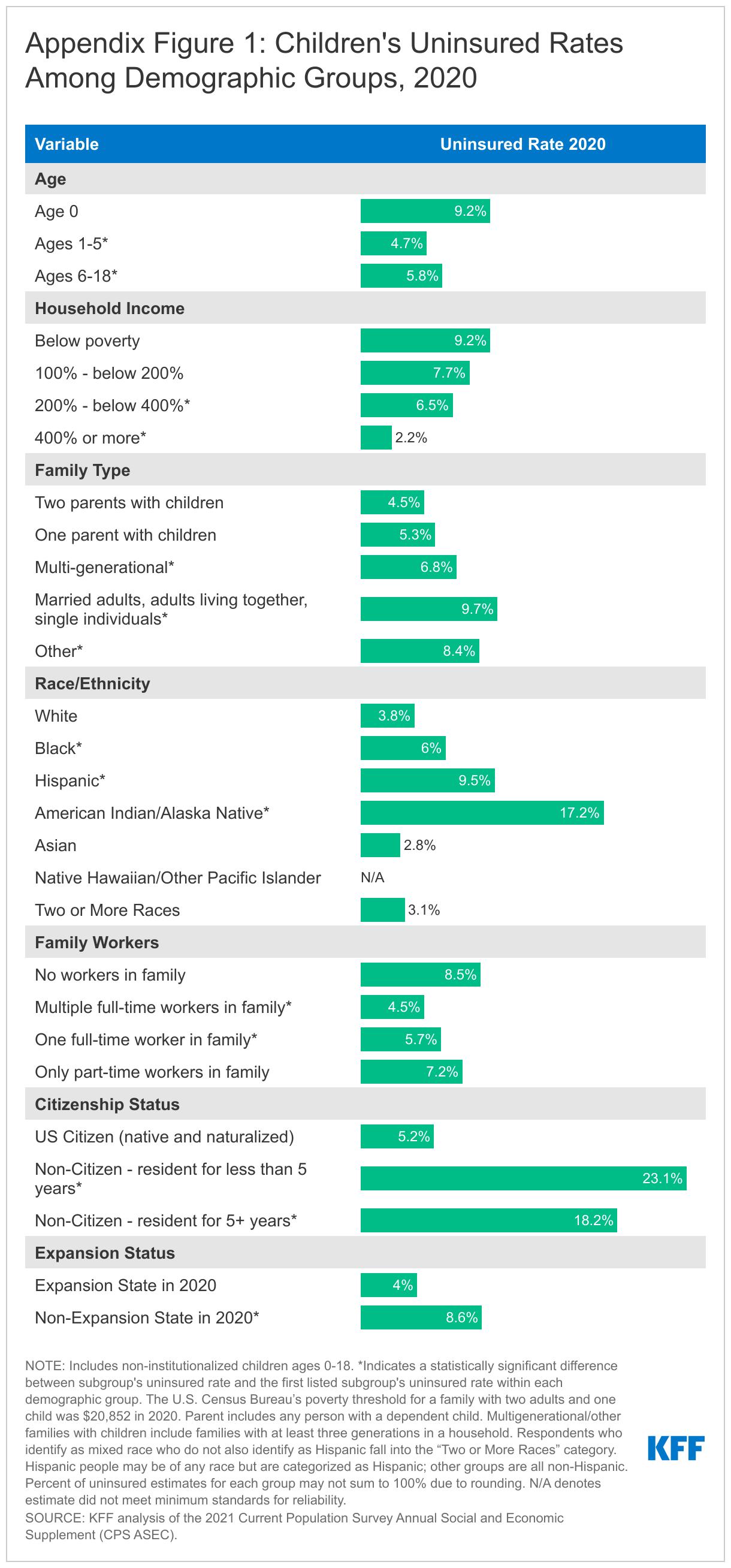

Most uninsured children in the US are school-aged, live in one or two parent families, and are US citizens (Figure 1). School-aged children (ages 6-18) make up almost three-quarters of uninsured children in the US; however, the children’s uninsured rate, or percentage of children with no health coverage, among infants was higher than the uninsured rate for children ages 1-5 and school aged children (Figure 1 and Appendix Figure 1). A majority of uninsured children live in one or two parent families (60.6%), and children in two parent families are less likely to be uninsured than those in multi-generational families, married adults, adults living together, single individual families, and other family types. Though US citizens make up the vast majority (89.7%) of uninsured children, they are less at risk of being uninsured than children who are not US citizens. While the children’s uninsured rate overall and for most demographic groups held steady in recent years, children who are not citizens and have been US residents for less than 5 years did experience significant increases in their uninsured rates from 2018 to 2020 (Appendix Table 1).

Children of color are disproportionately uninsured. Hispanic children make up the largest share (43.0%) of uninsured children (Figure 1). Children of color, together, make up nearly two-thirds of all uninsured children, but only make up 50.5% of all children in the US. Further, Black, Hispanic, and American Indian/Alaska Native children are more likely to be uninsured compared to white children (Appendix Figure 1). Black children experienced significant increases in their uninsured rates from 2018 to 2020 despite stability in the overall children’s uninsured rate (Appendix Table 1).

Children in poverty are more likely to be uninsured and make up a disproportionate share of uninsured children. Children living below 100% of the Federal Poverty Level (FPL; the federal poverty level was $20,852 for a family of two adults and a child in 2020) make up over a quarter of uninsured children, but account for only 16.5% of children in the US (Figure 1). The majority (53.5%) of uninsured children live below 200% FPL, and the vast majority (86.2%) live below 400% FPL. Children living below poverty are more likely to be uninsured compared to children living between 200 – 400% FPL and over 400% FPL (Appendix Figure 1). Further, children with no workers in their family are at more risk of being uninsured than those children with multiple workers or one full-time worker in their family. However, the vast majority (77.9%) of uninsured children have at least one full-time worker in their family, highlighting that many children live in families with lower income workers who likely do not obtain health coverage through their employer.

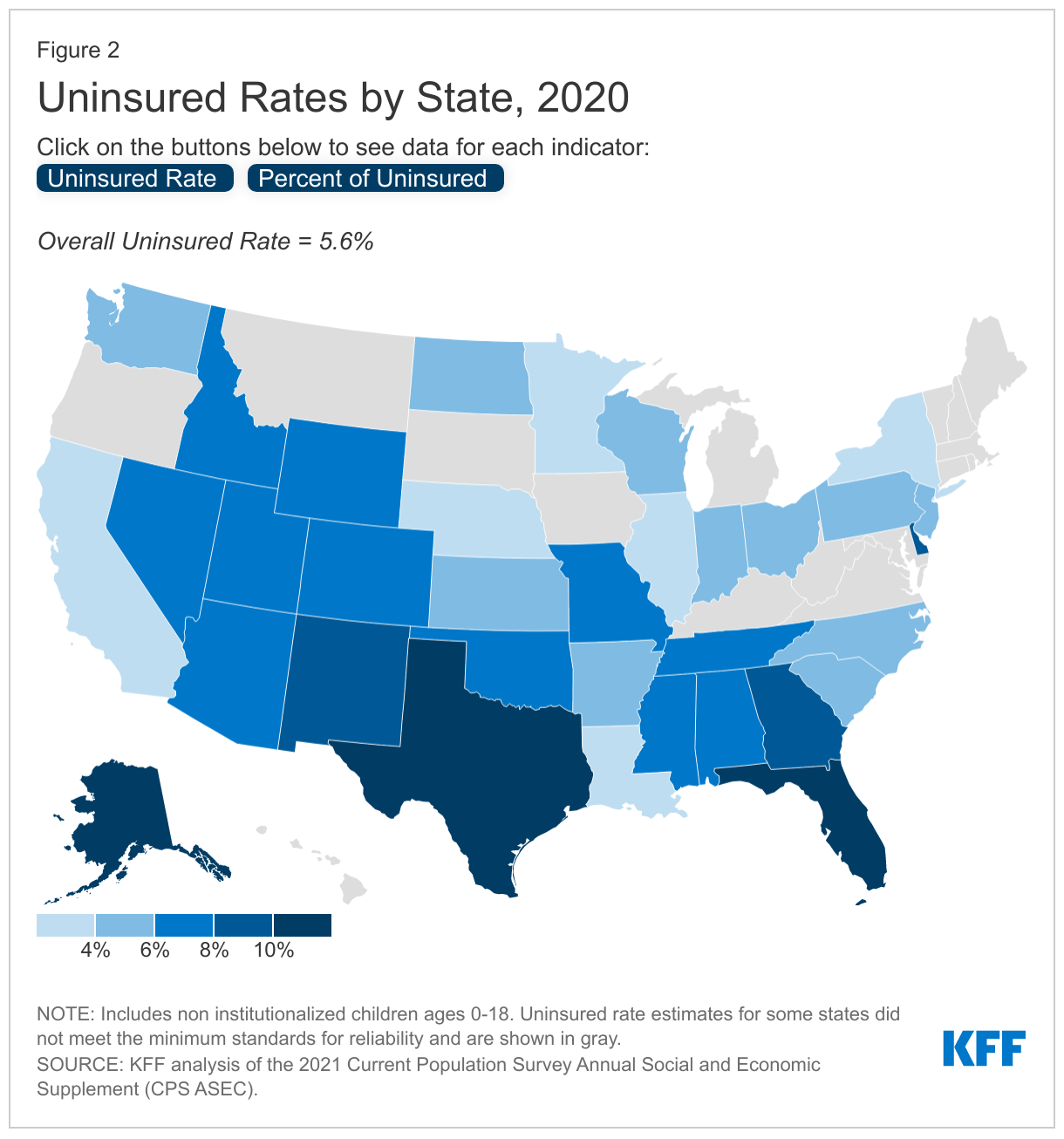

The uninsured rates for children in 2020 varied across states, ranging from 2.3% of children in New York to 12.0% in Alaska (though estimates for some states were not reportable) (Figure 2). Texas and Florida have the largest number of uninsured children, together accounting for almost one third (20.6% in Texas and 10.7% in Florida) of all uninsured children in the US (Figure 2).

How could current policy proposals reach uninsured children?

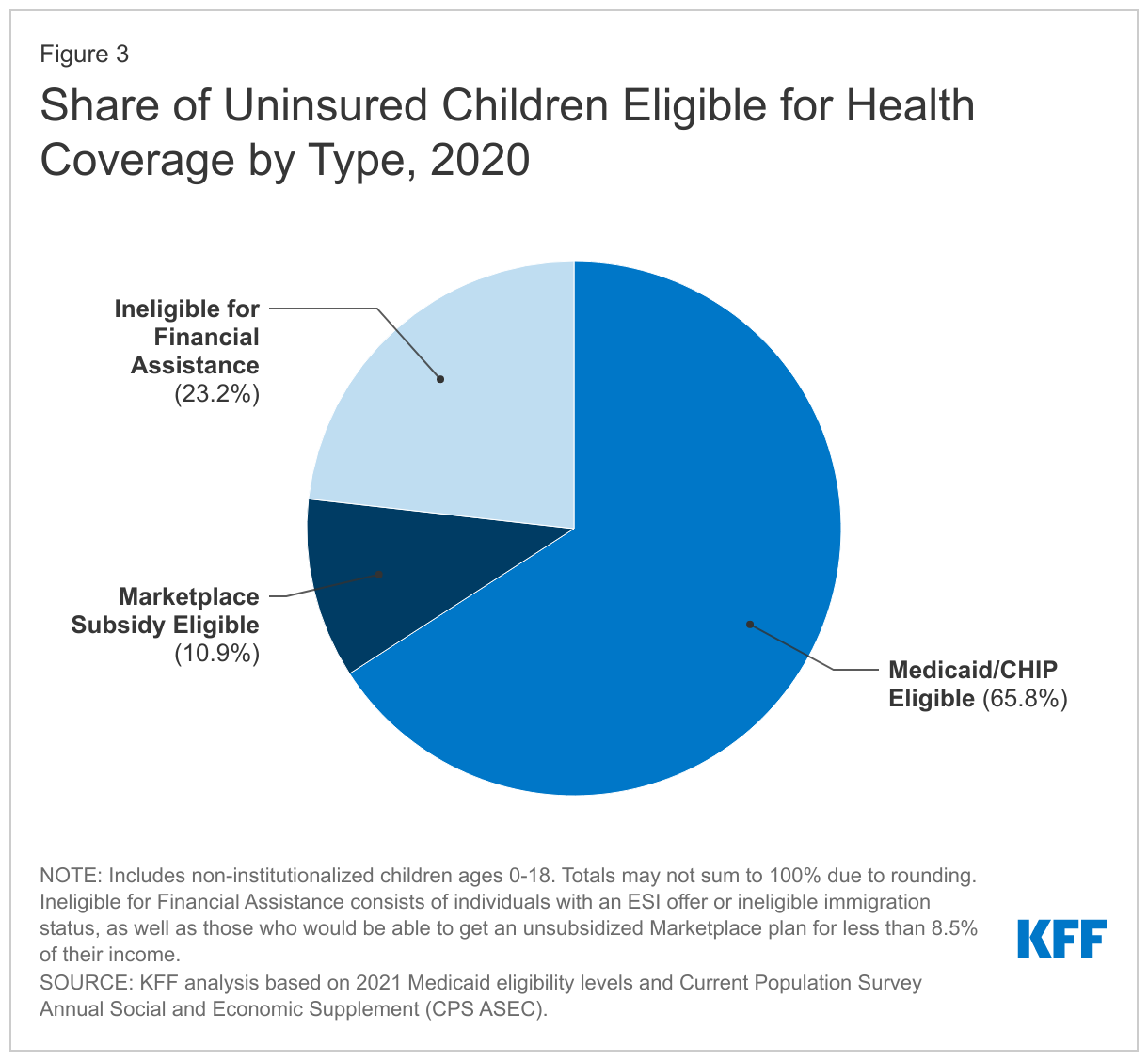

Outreach may improve children’s coverage rates since the vast majority of uninsured children are eligible for Medicaid or subsidized Marketplace coverage. In general, nearly all low-income children in the US are eligible for Medicaid/CHIP, with 49 states covering children at or above 200% FPL and more than a third of states covering children at or above 300% FPL. Two-thirds of all uninsured children are eligible for Medicaid/CHIP, and another 10.9% are eligible for subsidized Marketplace coverage (including those eligible under subsidies available under the American Rescue Plan Act) (Figure 3). Most remaining uninsured children are not eligible for financial assistance for coverage because their family has access to employer-based coverage. Children eligible for coverage may still be uninsured for several reasons including administrative barriers, language barriers and lack of internet access, lack of program knowledge and inadequate outreach, among others. Outreach can connect children to Medicaid/CHIP coverage, with outreach efforts following the implementation of the ACA contributing to children’s coverage gains leading up to 2016 even though the ACA did not materially increase children's eligibility for coverage. The current BBBA budget reconciliation package proposes funding for outreach and enrollment efforts through 2025 to inform individuals of their coverage options. The Biden Administration also recently extended the open enrollment period by 30 days, provided additional funding for Federally-facilitated Marketplace (FFM) Navigators, and re-launched the “Champions for Coverage” initiative in efforts to expand access to health coverage.

Closing the coverage gap could also affect the number of uninsured children. Children living in one of the 12 states that have not expanded Medicaid to adults under the ACA (non-expansion states) were over two times as likely to be uninsured as children in expansion states in 2020 (Appendix Figure 1). The uninsured rate increased significantly by 1.3 percentage points from 2016 to 2020 for children living in non-expansion states, while the uninsured rate held steady for children in expansion states (Appendix Table 1). Uninsured children are disproportionately concentrated in non-expansion states: only 35.2% of US children live a non-expansion state, but a majority of uninsured children (53.8%) live in non-expansion states (Figure 1).

Studies show a link between expanding parent Medicaid eligibility and growth in children’s health coverage.3 ,4 ,5 ,6 While research shows that children are more likely to gain and maintain coverage when parents gain access to the same coverage program, parents also say that affordability is the most important factor they care about in their children’s coverage, and they would be willing to enroll them in separate coverage for a lower cost. Following the implementation of the ACA, expansion states saw growth in children’s health coverage rates even though eligibility for children did not expand. One study estimates 710,000 low-income children gained coverage post ACA implementation and an additional 200,000 children would have gained coverage if all states had expanded Medicaid. Uninsured children are disproportionately concentrated in non-expansion states; thus, expanding access to health coverage to adults in the coverage gap could increase coverage for children.

The current version of the BBBA seeks to temporarily close the coverage gap by allowing people living in states that have not expanded Medicaid to purchase subsidized coverage on the ACA Marketplace through 2025. The proposal also extends provisions in the American Rescue Plan Act (ARPA) passed earlier this year that provide additional financial assistance for low-income people purchasing Marketplace plans through 2025. Parents in the coverage gap seeking Marketplace coverage through the “no wrong door” application process could enroll their eligible children in Medicaid/CHIP coverage. Additionally, there are provisions in the BBBA to increase in the federal Medicaid match rate for the expansion population (from 90% to 93%) through 2025 on top of already passed fiscal incentives in the ARPA. This could discourage states that have already expanded Medicaid from dropping, and could encourage new states to implement Medicaid expansion, particularly after the temporary effort to close the coverage gap expires.

Continuous eligibility for children in Medicaid/CHIP reduces gaps in health coverage. States currently have the option to provide 12 months of continuous coverage, and as of January 2020, 31 states provide 12-month continuous eligibility to children in Medicaid/CHIP. The BBBA includes a requirement for all states to provide 12-months of continuous coverage for children with Medicaid/CHIP, which would allow children to remain enrolled for a full year unless the child withdraws, moves, or turns 19. This provision could reduce children’s health coverage disruptions, which children of color are more likely to experience, and may reduce the number of uninsured children.

Looking Ahead

As congress continues to debate the BBBA, it is uncertain when an agreement will be reached and what provisions impacting children’s health coverage will remain in the final bill. If passed with current provisions, the bill has the potential to improve children’s health coverage.

As COVID-19 vaccines are rolled out for young children, linking children to coverage may be a step in helping children access vaccines. While the vaccine is available at no cost irrespective of insurance status, research shows uninsured children have lower vaccination coverage generally, potentially stemming from difficulties with access to care, information, or transportation. More broadly, children who lack insurance coverage have worse access to health care and face long-term consequences for their health and development. Given the range of challenges children have faced during the pandemic, actions to extend health insurance coverage to those lacking it may address some of the negative consequences.

Methods

This analysis uses data from the 2019 and 2021 Current Population Survey Annual Social and Economic Supplement (CPS ASEC) and the 2017 CPS ASEC Research File. Due to known data quality issues with the 2019 CPS ASEC data, which was collected at the onset of the pandemic in March 2020 and experienced low response rates, we do not to report the 2019 data. We provide trend data for 2016, 2018, and 2020 using the CPS ASEC. Estimates that do not meet the minimum standards for reliability are not shown.

There have been discussions around the inconsistencies between Medicaid administrative data and the CPS insurance coverage estimates for those with Medicaid/CHIP. Medicaid enrollment increases observed in administrative data in recent years are not mirrored in the CPS estimates. Some of the discrepancies may be related to the way in which the survey counts uninsured people or to ongoing challenges with response rates. The CPS counts people as uninsured only if they lack coverage for the full year and thus does not capture those who may have lost insurance during the year.

Appendix

Endnotes

- KFF analysis of the 2021 Current Population Survey Annual Social and Economic Supplement (CPS ASEC). ↩︎

- KFF analysis of the 2021 Current Population Survey Annual Social and Economic Supplement (CPS ASEC). ↩︎

- Julie Hudson and Asako Moriya, “Medicaid Expansion For Adults Had Measurable ‘Welcome Mat’ Effects On Their Children”, Health Affairs 36,9 (September 2017): 1643-1651. https://www.healthaffairs.org/doi/full/10.1377/hlthaff.2017.0347. ↩︎

- Adam Sacarny, Katherine Baicker, and Amy Finkelstein, “Out of the Woodwork: Enrollment Spillovers in the Oregon Health Insurance Experiment”, National Bureau of Economic Research, No. w26871 (March 2020), https://www.nber.org/system/files/working_papers/w26871/w26871.pdf. ↩︎

- Lisa Dubay and Genevieve Kenney, “Expanding Public Health Insurance to Parents: Effects on Children's Coverage under Medicaid”, Health Services Research: 38,5 (2003): 1283–1301. https://doi.org/10.1111/1475-6773.00177. ↩︎

- Jennifer Devoe, Miguel Marino, Heather Angier, et al., “Effect of Expanding Medicaid for Parents on Children’s Health Insurance Coverage: Lessons From the Oregon Experiment”, JAMA Pediatrics, 169,1 (2015). https://doi:10.1001/jamapediatrics.2014.3145. ↩︎