Policy Options to Sustain Medicare for the Future

Section 4: Medicare Program Structure

Benefit Redesign

Options Reviewed

This section discusses two policy options for redesigning Medicare’s benefit package:

» Restructure Medicare’s traditional benefit design with a unified deductible, modified cost sharing, and a limit on out-of-pocket spending, possibly in conjunction with policies to discourage or restrict supplemental coverage

» Provide a new government-administered plan with a comprehensive benefit package, as an alternative to traditional Medicare and Medicare Advantage

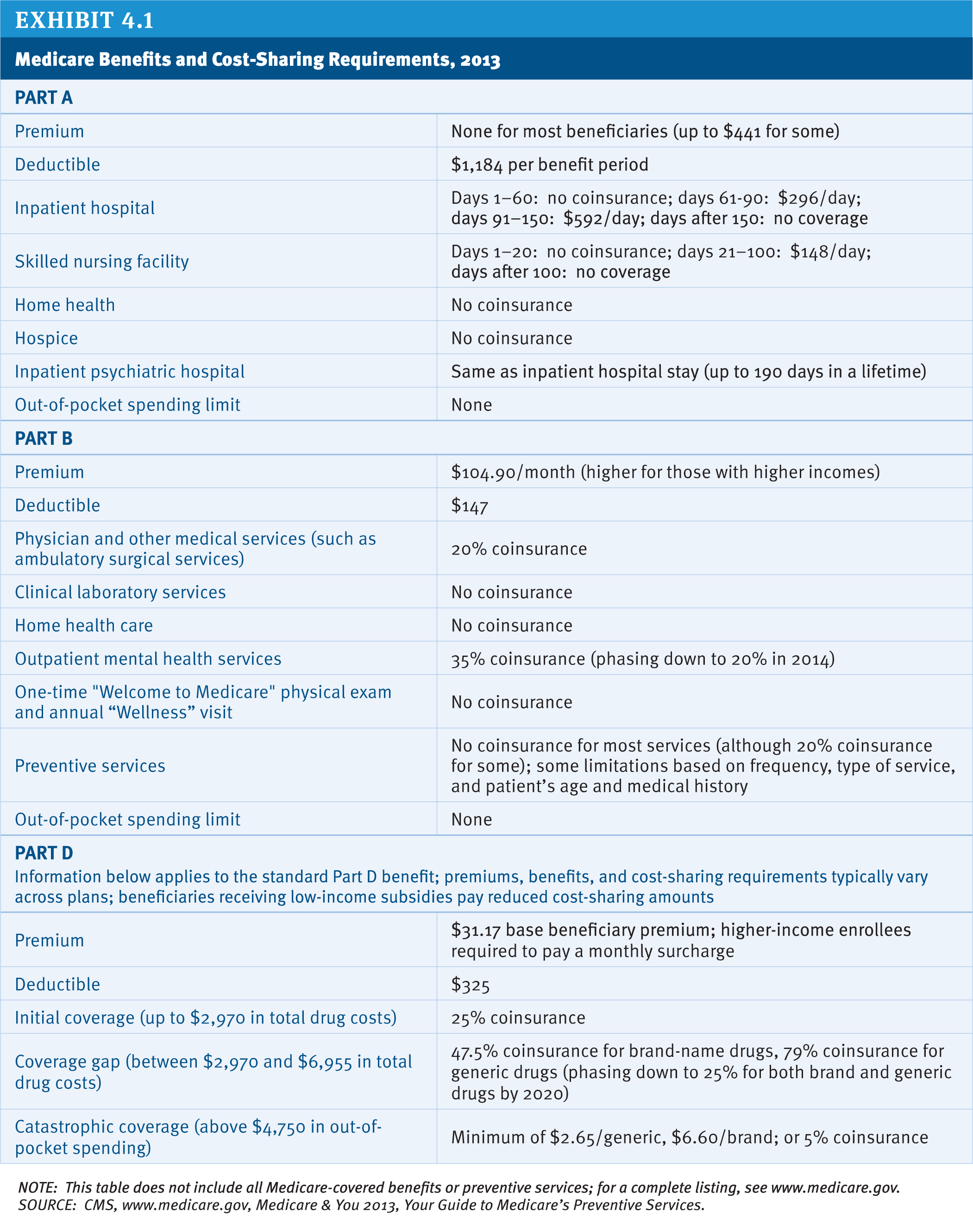

Medicare’s benefits were designed by Congress through a series of statutes beginning with the original 1965 law. Under current law, traditional Medicare covers services under three separate parts: Part A (hospital and other inpatient services), Part B (physician, preventive, and other outpatient services), and Part D (prescription drug coverage provided by private plans).1 Traditional Medicare has separate cost-sharing requirements that vary by the type of service, and there is no limit on annual or lifetime out-of-pocket spending (Exhibit 4.1).2 The traditional Medicare program provides less generous coverage on average than typical large employer health plans—including the most common plan offered under the Federal Employees Health Benefits Program (FEHBP)—largely due to Medicare’s relatively high Part A deductible, the lack of a spending limit for Part A and Part B services, and less generous drug coverage (Kaiser Family Foundation 2012a).

Most people with Medicare also have some type of supplemental insurance to help cover Medicare’s cost-sharing requirements. In 2009, nearly a quarter of beneficiaries (24%) purchased a Medigap policy to supplement traditional Medicare and more than one-third (35%) had an employer-sponsored supplemental plan (these numbers include the 5 percent of beneficiaries who have both).3 Currently, insurers can offer 10 types of Medigap policies, the most common of which (Plans C and F) cover most of Medicare’s cost-sharing obligations. The typical employer-sponsored supplemental plan requires enrollees to pay some degree of deductible and cost sharing. Additionally, some low-income beneficiaries are enrolled in Medicaid and receive help paying Medicare’s premiums and/or cost-sharing requirements.

Medicare’s traditional benefit design could be restructured in ways that could achieve savings, modernize and simplify the benefit design, and provide a new limit on beneficiaries’ out-of-pocket spending. Proposals to restructure Medicare’s benefit design would simplify the program’s cost-sharing requirements, provide greater protection against very high out-of-pocket spending, and reduce the need for supplemental insurance. For example, one proposal would combine the Part A and Part B deductibles, establish a uniform coinsurance rate for most Medicare-covered services, and create an out-of-pocket spending limit. Some, but not all, of the proposals to restructure Medicare’s benefit design also seek to reduce Federal spending. Achieving savings without increasing cost sharing for the average beneficiary may be difficult without incorporating other reforms.

Policy Options

OPTION 4.1

Restructure Medicare’s benefit design with a unified deductible, modified cost sharing, and a limit on out-of-pocket spending, possibly in conjunction with policies to discourage or restrict supplemental coverage

There are many ways in which Medicare’s cost sharing could be modified; this section discusses three approaches:

» Option 4.1a: Establish a combined deductible, uniform coinsurance rate, and a limit on out-of-pocket spending.

» Option 4.1b: Establish a combined deductible, uniform coinsurance rate, and a limit on out-of-pocket spending, along with Medigap reforms.

» Option 4.1c: Establish a combined deductible, varying copayments, and a limit on out-of-pocket spending in a way that will not change aggregate beneficiary liabilities, along with a surcharge on supplemental plans.

These options would produce Federal savings directly by shifting costs to beneficiaries and third-party payers and indirectly by creating financial incentives to reduce utilization of services. Although not discussed here, benefit-restructuring proposals could be modified (e.g., with lower combined deductibles or reduced coinsurance requirements for certain services) to minimize costs for beneficiaries. Doing so would likely mean lower Federal savings. Similarly, some or all of the savings could be used to provide additional premium and cost-sharing assistance to low-income or otherwise vulnerable beneficiaries. The new benefit design could also include an income-related out-of-pocket spending limit, with greater protections for lower-income beneficiaries, although implementing this option (e.g., identifying beneficiaries’ incomes) could be administratively complex.

A restructured benefit design also could be implemented in conjunction with other reforms that are intended to modernize the benefits provided by the program (see Section Five, Coverage Policy). For instance, such a policy might include preferred provider networks with tiered cost sharing to encourage beneficiaries to seek higher-value providers, requirements that beneficiaries pay more for certain services with less-costly but functionally-equivalent alternatives, or other reforms. To the extent that these reforms produce efficiencies, savings could be increased or beneficiary cost-sharing obligations could be reduced.

OPTION 4.1A

Establish a combined deductible, uniform coinsurance rate, and a limit on out-of-pocket spending

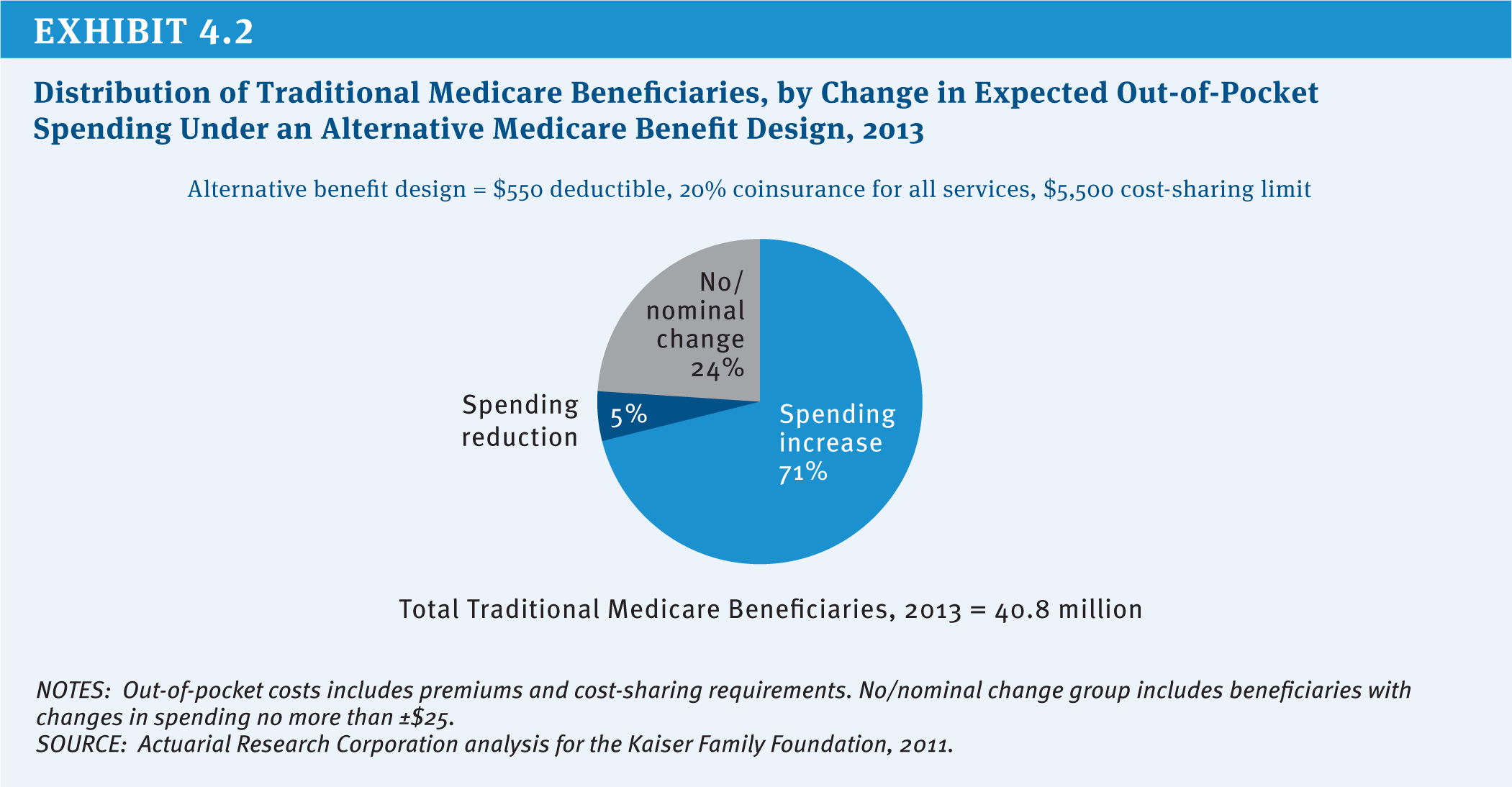

In a 2011 report, the Congressional Budget Office (CBO) evaluated a restructured benefit design that would include the following:

A $550 combined deductible for Part A and Part B services. This is higher than the current Part B deductible ($147 in 2013) but lower than the current Part A deductible ($1,184 per benefit period in 2013).

A uniform 20 percent coinsurance rate. Beneficiaries are required to pay a 20 percent coinsurance for most Part B services. This option would replace copayments for inpatient and skilled nursing facility (SNF) stays, and introduce new cost sharing for clinical lab services, home health services, the first 60 days of a hospital stay, and the first 20 days of a SNF stay.4

A new annual out-of-pocket spending limit of $5,500, after which Medicare would cover all of a beneficiary’s annual medical expenses.

The National Commission on Fiscal Responsibility and Reform (the Simpson-Bowles commission) recommended a similar approach. None of the proposals put forward to date have included Part D in the restructured benefit design.

Budget effects

CBO estimated that if this option were implemented in 2013, savings would be $32 billion over 10 years (2012–2021) (CBO 2011).

Discussion

This option would achieve Federal savings and increase aggregate spending for beneficiaries and third-party payers. Some beneficiaries would have lower costs (e.g., beneficiaries with very high costs who would benefit from the limit on out-of-pocket spending), but most people with Medicare would pay more (Exhibit 4.2). Out-of-pocket costs would increase for those beneficiaries who use fewer services, primarily because of the higher deductible for those who only use Part B services.

The impact of these benefit design changes also would be affected by beneficiaries’ supplemental coverage (Medigap, retiree coverage, Medicaid, or none). Beneficiaries with supplemental coverage could be insulated from higher cost-sharing requirements if their plans covered all or some of the new costs, but would likely face higher premiums if Medigap insurers and employers raised premiums in response to higher costs covered by their plans. Beneficiaries without supplemental coverage—roughly 4.1 million beneficiaries in 2013—would be exposed to large changes in out-of-pocket spending, with about two-fifths (42 percent) spending at least $250 more in 2013 (Kaiser Family Foundation 2011c).

This option likely would reduce the demand for care by making some beneficiaries responsible for a greater share of their health expenses. However, studies have shown that people forgo both unnecessary and necessary care in response to higher cost sharing. Beneficiaries who forgo needed care may require new services—such as hospitalizations—over the long term (Swartz 2010).

OPTION 4.1B

Establish a combined deductible, uniform coinsurance rate, and a limit on out-of-pocket spending, along with Medigap reforms

Some have proposed combining a restructured benefit design with policies to restrict or place a surcharge on supplemental coverage in order to achieve greater Medicare savings. CBO has evaluated a policy that combines (1) a new benefit design with a $550 combined deductible, a uniform 20 percent coinsurance, and a $5,500 spending limit (as in Option 4.1a above) with (2) Medigap coverage restrictions that eliminate Medigap coverage of the first $550 and limit coverage to 50 percent of the next $4,950 (see Section One, Beneficiary Cost Sharing). The Simpson-Bowles commission included a similar combination of changes in its recommendations (National Commission on Fiscal Responsibility and Reform 2010).5

Budget effects

CBO estimated that combining the restructured benefit design with restrictions on first-dollar Medigap coverage as described would save $93 billion over 10 years (2012–2021), if implemented in 2013 (CBO 2011). Greater savings are expected under this option relative to Option 4.1a as a result of expected reductions in utilization when beneficiaries with Medigap are faced with higher out-of-pocket cost sharing.

Discussion

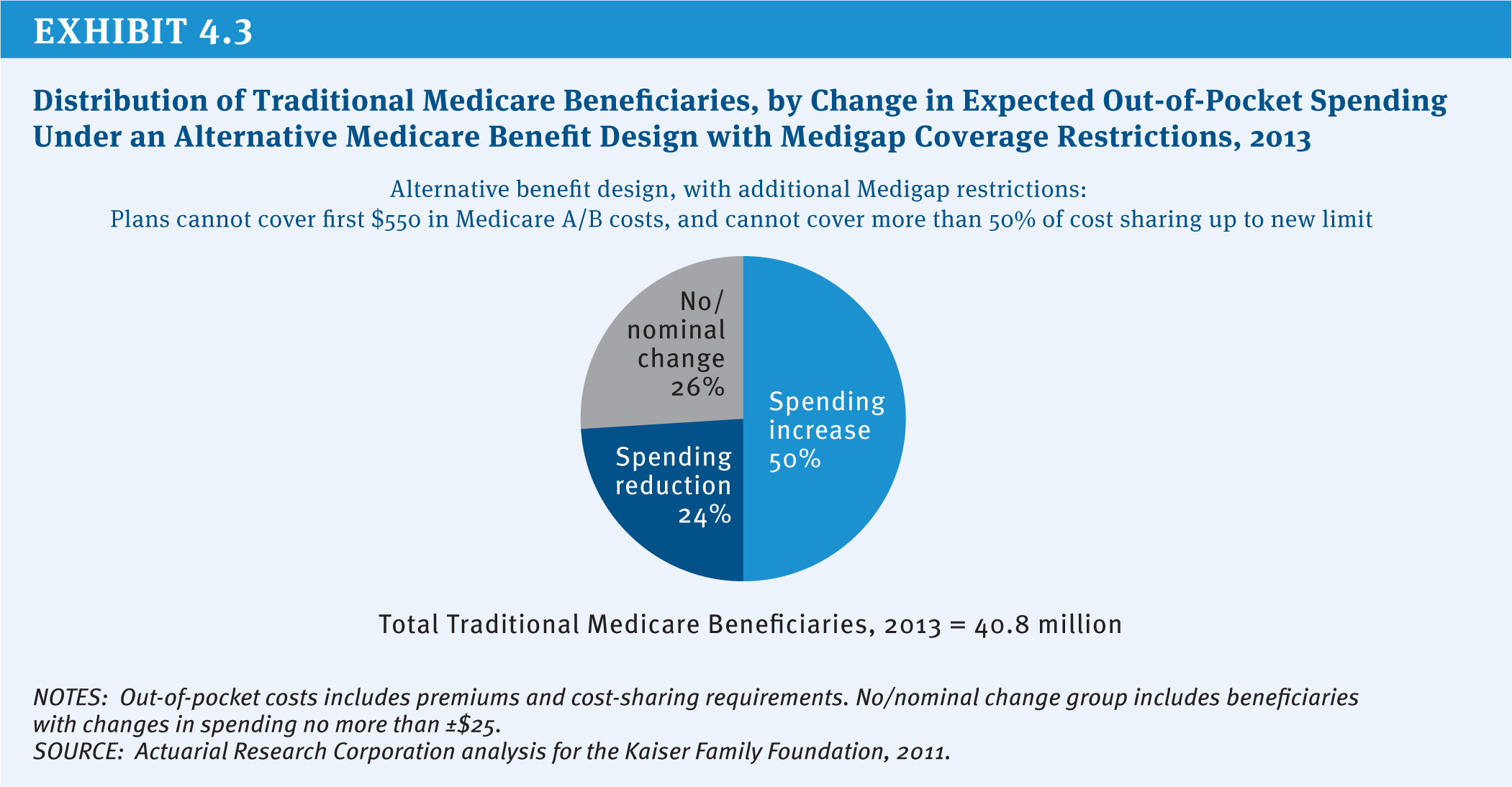

As discussed under Option 4.1a, a restructured benefit design by itself would likely reduce out-of-pocket spending for a group of beneficiaries who otherwise would incur relatively high out-of-pocket costs in the absence of a limit on out-of-pocket spending, while increasing spending for a larger number of beneficiaries who use relatively few services. Adding restrictions on Medigap policies likely would decrease Medigap premiums (because plans would cover fewer expenses) and Part B premiums (due to the expectation that beneficiaries would use less care when facing cost-sharing requirements directly). As a result, about half of all beneficiaries would be expected to pay more under this combined option, compared with 71 percent paying more under Option 4.1a (Kaiser Family Foundation 2011c) (Exhibit 4.3).

However, restricting Medigap coverage also would require enrollees to pay a greater share of their medical expenses on their own. For some enrollees with high levels of utilization, including a relatively large share of those with one or more hospitalizations, the higher cost-sharing obligations would more than offset any reductions in premiums. The prohibition of first-dollar Medigap coverage also would expose enrollees to more uncertainty about their future medical expenses, which could be a drawback for all policyholders, even those who would save money in the short-term.

There is some debate about supplemental plans’ impact on beneficiaries’ use of care and, in turn, on Medicare expenses (MedPAC 2012). If having Medigap coverage has a smaller impact on utilization than some assume, savings to Medicare from Medigap restrictions could be smaller than projected.

OPTION 4.1C

Establish a combined deductible, varying copayments, and a limit on out-of-pocket spending in a way that will not change aggregate beneficiary liabilities, along with a surcharge on supplemental plans

The Medicare Payment Advisory Commission (MedPAC) has recommended that Congress develop a new Medicare benefit design with an annual limit on out-of-pocket spending that differs in several ways from the options described above (MedPAC 2012). MedPAC suggested that the new benefit design should not affect aggregate beneficiary cost-sharing liability, whereas Options 4.1a and 4.1b do not have this restriction. MedPAC also recommended establishing copayments that vary by the type of service or provider, rather than a uniform coinsurance rate, noting that copayments are easier for beneficiaries to understand. Instead of restricting Medigap coverage, MedPAC recommended placing a surcharge on all supplemental plans, including employer-sponsored retiree plans. Finally, MedPAC was open to either a combined or separate Part A and Part B deductible.

As an example, MedPAC evaluated a benefit design that would include: a $5,000 out-of-pocket spending limit, a $500 combined Part A and Part B deductible, and copayments for inpatient hospital stays ($750 per admission), skilled nursing facility stays ($80 per day), home health care ($150 per episode), primary care ($20 per visit), specialty care ($40 per visit), and other cost-sharing requirements varying by service type. The illustrative design also included a 20 percent surcharge on supplemental plan premiums, which would apply to both Medigap and retiree health plan premiums.

Budget effects

MedPAC estimated that this illustrative benefit design would have reduced 2009 Medicare spending by 0.5 percent (approximately $2.5 billion, based on 2009 total outlays) if supplemental plan enrollees maintained their coverage despite the 20 percent surcharge (MedPAC 2012).6 MedPAC estimated greater Medicare savings if some or all supplemental plan enrollees dropped their coverage in response to the surcharge.

Discussion

According to MedPAC, more beneficiaries would see their out-of-pocket spending increase by at least $250 than would see their spending decrease by that amount under the new benefit design (separate from the supplemental surcharge), although most beneficiaries would see changes in spending of less than $250. Beneficiaries who use few Part B services, who are not hospitalized during the year, and who have supplemental coverage would be more likely than others to see annual out-of-pocket spending increases of $250 or more. People with Medicare who have higher than average health care expenses and do not have supplemental coverage would be more likely than others to see annual out-of-pocket savings of at least $250.

The impact of adding a supplemental plan premium surcharge would depend on the number of people who drop their supplemental coverage in response to the new surcharge. If all beneficiaries with employer/Medigap coverage elected to pay the surcharge and maintain their coverage, Medicare would achieve savings from the surcharge while enrollees incurred higher costs. If everyone dropped their coverage, enrollees would be required to pay more cost sharing out of their own pockets but would also no longer need to pay plan premiums. Taken together, this would tend to reduce spending for supplemental plan enrollees who have low levels of utilization in a given year (because reductions in premiums would more than offset any increase in cost sharing), but could increase spending for supplemental plan enrollees who use many services (because new out-of-pocket costs could outweigh the premium reductions). Under both scenarios, net Part B expenses would likely decline (either due to income from the surcharge or expected reductions in care if beneficiaries drop supplemental coverage and pay cost sharing on their own), and Part B premiums would decrease for all beneficiaries as a result.

There is some debate as to whether the supplemental plan surcharge should apply to employer-sponsored plans. Some support doing so in order for the surcharge to apply to all supplemental policies rather than Medigap policies only. Also, employer coverage tends to be more common among beneficiaries with comparatively higher incomes who more likely could afford the surcharge. Others argue that retiree plans should be excluded, given that employees may have sacrificed additional earnings during their working years in exchange for retiree benefits, and because the typical retiree plan does not have first-dollar coverage. Some might prefer to restrict the surcharge on Medigap policies to Plans C and F, but exempt other policy types that do not offer first-dollar coverage (see Section One, Beneficiary Cost Sharing).

OPTION 4.2

Provide a new government-administered plan with a comprehensive benefit package, as an alternative to traditional Medicare and Medicare Advantage

In 2005, several experts proposed a new, alternative Medicare option that would include a more comprehensive benefit package as a way of improving the benefit design for beneficiaries and potentially achieving program savings (Davis et al. 2005). It would merge Part A and Part B coverage into a single benefit package along with Part D drug coverage. This approach would provide coverage on top of the standard package, which could mitigate the need for supplemental insurance. For instance, the comprehensive package might have lower deductibles and cost sharing and could include an annual limit on beneficiary out-of-pocket liabilities for covered inpatient and outpatient services. Enrollees would cover the cost of any new benefits through an additional monthly premium, although lower-income enrollees could receive government assistance for coverage under this option.

A more recent version of this approach also would incorporate incentives for beneficiaries to seek care from “high-value” providers and care systems, in addition to the reforms discussed above (Commonwealth Fund 2013). For example, the more recent plan would lower cost-sharing requirements for enrollees who register with a primary care practice or medical home, and (eventually) for enrollees who obtain care from accountable care networks (such as accountable care organizations, or ACOs). Alternatively, the plan could encourage beneficiaries to seek higher-value providers by establishing a preferred provider network with tiered cost-sharing requirements. The plan also could incorporate coverage and payment innovations intended to improve the value of care, such as by adopting “least costly alternative” approaches or relying on new value-based payment systems, among other changes (see Section Four, Delivery System Reform and Section Five, Coverage Policy). As proposed by The Commonwealth Fund, new Medicare beneficiaries automatically would be enrolled in the new plan, unless they opt for traditional Medicare or Medicare Advantage. As in the earlier version of this option, beneficiaries who enroll in this new plan would pay a premium set at a level that would offset any changes in Federal spending associated with the new plan. Finally, the more recent version of this option also includes Medigap restrictions, by which Medigap policies are prohibited from covering the first $250 of beneficiary cost-sharing requirements and are required to maintain copayments for physician ($20) and emergency room ($50) visits.7

Budget effects

No cost estimate is available for this option. This option is designed to be budget neutral for the Federal government by requiring enrollees to cover any new costs through the premium.

Discussion

This option would offer comprehensive coverage through a single Medicare plan, which could be simpler for beneficiaries than receiving care through some combination of traditional Medicare (Part A and Part B), Part D, and a supplemental plan. Combining multiple programs into one could also make it easier for Medicare to implement care coordination innovations and would reduce the cost of coordinating between coverage types. Such an approach might be a less expensive choice for beneficiaries than Medigap for obtaining supplemental coverage, since the government-administered plan would be expected to have lower administrative expenses and could include reforms intended to encourage higher-value care. Beneficiaries also could see savings on prescription drugs if Medicare were able to leverage lower prescription drug prices than are currently obtained by private Part D plans.

By allowing beneficiaries to purchase a comprehensive and expanded benefit package, this approach could enable traditional Medicare to better compete with private Medicare Advantage plans, given that Medicare Advantage plans today typically provide benefits covered under Parts A, B, and D in a single plan, have a limit on out-of-pocket spending, and often provide extra benefits and care management. This approach also would allow Medicare to introduce coverage, payment, and cost-sharing reforms in a more limited way before applying them to all of traditional Medicare (if at all).

The appeal of this type of government-administered plan to beneficiaries would depend in part on the cost of the expanded coverage compared with the cost and generosity of existing coverage options. This new plan could reduce demand for supplemental coverage; however, it also could attract a disproportionate share of sicker and more expensive enrollees. If so, premiums would be expected to rise and enrollment to decline, which could diminish the prospect of Medicare savings and threaten the plan’s stability over the longer term. This plan also could have difficulty building enrollment if beneficiaries with other forms of supplemental coverage were unwilling to reconsider their plan choices. Automatic enrollment of new beneficiaries (with the ability to opt-out) could, to some extent, address these concerns about enrollment and selection, as could new restrictions on Medigap coverage. Other policy changes also might be needed to ensure the viability of the new program.8

One concern about a new government-administered plan is that adding another coverage option to the existing set of Medicare options could be a source of confusion for beneficiaries.9 Another concern is that, while this option could allow traditional Medicare to better compete with Medicare Advantage plans by offering lower cost-sharing requirements or by including care management, it could also be the case that Medicare would have an “unfair” competitive advantage. For example, a government-administered plan could set lower provider payment rates than many private insurers, could have lower administrative expenses, and could have a marketing advantage. While some might view these factors as explicit benefits of the new plan option, others might view them as tilting the marketplace towards the government-administered plan and away from Medicare Advantage plans. Finally, determining the premium could be an administrative challenge, given that Medigap and Medicare Advantage plan premiums vary geographically and Medigap premiums are often age-rated, while premiums for the traditional Medicare program (both standard and income-related Part B premiums) are uniform nationwide.

References

Click to expand/collapse

Katherine Baicker and Dana Goldman. 2011. “Patient Cost-Sharing and Health Care Spending Growth,” Journal of Economic Perspectives, Spring 2011.

The Commonwealth Fund Commission on a High Performance Health System (Commonwealth Fund). 2013. Confronting Costs: Stabilizing Spending While Moving Toward a High Performance Health Care System, January 2013.

Congressional Budget Office (CBO). 2010. Medicare Baseline, August 25, 2010.

Congressional Budget Office (CBO). 2011. Reducing the Deficit: Spending and Revenue Options, March 2011.

Karen Davis, Marilyn Moon, Barbara Cooper, and Cathy Schoen. 2005. “Medicare Extra: A Comprehensive Benefit Option for Medicare Beneficiaries,” Health Affairs, October 2005.

Kaiser Family Foundation. 2011a. Medigap Reform: Setting the Context, September 2011.

Kaiser Family Foundation. 2011b. Medigap Reforms: Potential Effects of Benefit Restrictions on Medicare Spending and Beneficiary Costs, July 2011.

Kaiser Family Foundation. 2011c. Restructuring Medicare’s Benefit Design: Implications for Beneficiaries and Spending, November 2011.

Kaiser Family Foundation. 2012a. How Does the Benefit Value of Medicare Compare to the Benefit Value of Typical Large Employer Plans: A 2012 Update, April 2012.

Kaiser Family Foundation. 2012b. Medicare Advantage 2013 Spotlight: Plan Availability and Premiums, November 2012.

Kaiser Family Foundation. 2012c. Medicare Part D: A First Look at Part D Plan Offerings in 2013, November 2012.

Medicare Payment Advisory Commission (MedPAC). 2012. Report to the Congress: Medicare and the Health Care Delivery System, June 2012.

National Commission on Fiscal Responsibility and Reform. 2010. The Moment of Truth: Report of the National Commission on Fiscal Responsibility and Reform, December 2010.

Katherine Swartz. 2010. Cost-Sharing: Effects on Spending and Outcomes, Robert Wood Johnson Foundation, December 2010.

Premium Support

Options Reviewed

This section reviews key policy decisions related to premium support proposals and discusses three options for setting Federal contributions:

» Set Federal contributions per beneficiary at the lesser of the second lowest private plan bid in a given area or average spending per capita under traditional Medicare in the area

» Set Federal contributions per beneficiary at the average plan bid in a given area (including traditional Medicare as a plan), weighted by enrollment

» Set Federal base year payments equal to average traditional Medicare per capita costs and limit the growth per person to an economic index, such as the consumer price index (CPI)

One approach to Medicare reform that has garnered a fair amount of attention would transform Medicare from a program that offers a defined set of benefits to one that offers a defined Federal government contribution toward the purchase of health insurance. First proposed for Medicare in the early 1980s, this approach has been proposed in a variety of forms with various labels, including “defined contribution,” “premium support,” “defined support” and “vouchers.” Typically, proposals of this nature provide a fixed Federal payment per enrollee and give beneficiaries the opportunity to choose among plans based on their own preferences for premiums, benefits, and other plan attributes. Proponents say this approach would promote greater competition among insurance plans and produce stronger incentives to reduce Medicare spending. Critics argue it would shift costs to Medicare beneficiaries and erode their entitlement to a defined set of guaranteed benefits.

Background

Under the current Medicare program, beneficiaries legally are entitled to a defined set of benefits and can choose to receive those benefits under traditional Medicare or through a private Medicare Advantage plan. In 2012, 27 percent of Medicare beneficiaries enrolled in a Medicare Advantage plan, with the remaining 73 percent of beneficiaries enrolled in the traditional Medicare program. Traditional Medicare pays providers directly using a variety of payment methods. In contrast, Medicare Advantage plans receive a capitated, per beneficiary amount for providing Part A and Part B benefits, based on benchmark amounts varying by county. The plans in turn pay providers and are not obligated to use traditional Medicare payment methods or levels. If Medicare benchmarks exceed the bids submitted by plans to provide Medicare benefits, plans receive a portion of the difference, which they are required to use to provide additional benefits to enrollees. (For a more complete discussion, see Section Two, Medicare Advantage.)

In recent years, the idea of transforming Medicare into some form of premium support system has received greater attention as part of broader efforts to slow the growth in Medicare spending and reduce the Federal deficit. For example, in 1999, some members of the National Bipartisan Commission on the Future of Medicare advanced a premium support proposal. Ultimately, the Commission was unable to agree on a plan but some members—Senators John Breaux (D-LA) and Bill Frist (R-TN) and Rep. Bill Thomas (R-CA)—introduced a premium support bill in Congress.

More recently, premium support proposals have been put forward by Rep. Paul Ryan (R-WI), Chairman of the House Budget Committee. The Bipartisan Policy Center Debt Reduction Task Force—co-chaired by former Senator Pete Domenici (R-NM) and former U.S. budget director Alice Rivlin—proposed a different model. The National Commission on Fiscal Responsibility and Reform (Simpson-Bowles commission) recommended a target for total Federal health spending, and mentioned premium support as an option to consider if costs grew faster than the target.

Under premium support, rather than being entitled to a defined set of benefits, all beneficiaries would be entitled to a defined contribution that would be used to cover the cost of either a private plan or traditional Medicare. Proponents say that under this system, market competition would constrain Medicare spending by giving plans incentives to restrain costs and giving beneficiaries incentives to choose lower cost plans. Critics say a premium support system would erode current law protections, shifting cost and risk from the Federal government to elderly and disabled beneficiaries. They also question whether a premium support system would achieve savings unless it is paired with strict limits on Federal spending. There also is debate over the extent to which the government can or should regulate private plans in a premium support system, whether competition would result in lower cost plans, and the role of traditional Medicare under a premium support system.

A shift from the current program to a system of premium support would entail a number of policy choices, each of which could have significant implications for the coverage provided to beneficiaries, and for program spending.

Key Policy Issues for Premium Support Proposals

Among the policy issues are:

» Benefits. Premium support proposals vary in the extent to which they specify the required benefits. Some would give broad discretion to plans within fiscal constraints, subject to approval by government. Others would require plans to provide benefits that are at least actuarially equivalent—but not necessarily identical—to benefits currently covered under Parts A and B of Medicare. A third approach would build on the Medicare Advantage model, requiring plans to cover Part A and Part B benefits, with cost-sharing that is actuarially equivalent (with some constraints for specific services). If plans are permitted to provide benefits that are actuarially equivalent to the defined Medicare benefit package, without constraints, there is some concern that plans might impose higher cost sharing or not cover services used mainly by sicker, higher-risk individuals, which could discourage enrollment and raise costs for beneficiaries who use these services.

» Role of traditional Medicare. Some premium support proposals would phase out the traditional Medicare program while others would maintain the traditional program in some manner as one of the plans beneficiaries could consider. The traditional Medicare program could be included in premium support in different ways. For instance, it could be retained it in its current form with a uniform national premium, or it could be administered as a set of local plans throughout the country that would bid to compete with private plans in each area. A traditional Medicare plan could also have independent management to give it greater flexibility to compete with private plans in local markets (Antos et al 2012). In all cases, a key distinction from current policy is that if traditional Medicare is retained as a bidding plan and if the traditional Medicare bid is higher than the bids of private plans, beneficiaries would pay a higher premium to remain in traditional Medicare. Restructuring traditional Medicare into a set of local plans on par with private plans could make it more difficult for traditional Medicare to leverage lower prices and could raise concerns about the explicit lack of uniformity and consistency in the program.

» Caps on the growth in Medicare spending per beneficiary. Some premium support proposals include a strict limit on the growth in payments per beneficiary to ensure constraints on Medicare spending. The extent to which a cap achieves savings will depend on whether it is applied to the growth in aggregate Medicare spending or Medicare spending per beneficiary, the index used to constrain spending growth (e.g., the Consumer Price Index (CPI), gross domestic product (GDP) plus 1%), and the relationship between the target growth rate and the expected growth in Medicare spending. Another question is how a cap on Medicare spending growth would be enforced and the extent to which beneficiary premiums and/or additional assistance for low-income beneficiaries would be affected if the cap were breached. Some have proposed a “softer” cap on spending that would trigger action by Congress or other officials, although it is not clear how such a cap would be enforced or if it would produce scoreable savings. (For a more complete discussion of options to cap Medicare spending, see Section Five, Spending Caps.)

» Subsidies for low-income beneficiaries. Premium support proposals often include additional subsidies for low-income beneficiaries. Key questions include who would be eligible for such assistance; the nature of the assistance they would receive (premiums and/or cost sharing subsidies); the interaction with the Medicaid program for people who are dually eligible for Medicare and Medicaid; and the choice of health plans for low-income beneficiaries. One approach would establish medical savings accounts for low-income beneficiaries, with the government contributing a set amount into a beneficiary’s account that could be used to cover out-of-pocket health expenses, including plan cost-sharing requirements. Another would be to have Medicare or Medicaid cover all premiums or cost sharing for certain services. Strategies for providing additional support to low-income beneficiaries have important implications for Federal spending (Medicare and Medicaid), State expenditures (Medicaid), and low-income beneficiaries’ out-of-pocket spending, plan choices, and access to providers.

» Risk adjustment. Most premium support proposals would “risk adjust” payments to account for beneficiaries’ predicted spending based on their relative health risk, including age, race, diagnoses based on the prior year of medical claims, as well as disabilities, institutional status, and Medicaid status. With perfect risk adjustment, plans would not be penalized for enrolling sicker than average beneficiaries, or financially rewarded for enrolling healthier than average enrollees. While risk adjustment methods are improving, they are not perfect; recent studies demonstrate that Medicare Advantage plans continue to receive favorable selection despite the long-term use of a risk adjuster (Brown et al. 2011; MedPAC 2012). In the absence of a sufficiently robust risk adjustment system, plans, including traditional Medicare, that attract sicker, high-cost beneficiaries could experience an increase in premiums due to adverse selection, and could ultimately become unsustainable.

» Marketplace regulation. The extent to which the marketplace is regulated would have important implications for beneficiaries (for a discussion of options to establish an oversight structure, see Section Five, Governance and Management). Premium support proposals vary in the extent and means by which the marketplace would be regulated. Most premium support proposals would require plans to accept any beneficiary who applied without regard to age or health status, prevent plans from charging higher premiums to sicker beneficiaries, and limit the extent to which premiums could vary by age (if at all). Some envision a more structured oversight authority—like the Centers for Medicare & Medicaid Services (CMS) or the Office of Personnel Management (OPM)—to set requirements for benefits, marketing practices and other consumer protections, while others prefer allowing plans greater flexibility in benefit design, marketing, and other activities.

» Special Medicare payment supports. Medicare’s support for indirect medical education (IME) and graduate medical education (GME), as well as disproportionate share hospitals (DSH) and special adjusters for providers in rural communities is another important consideration for premium support proposals. Under current law, Medicare plays a key role in funding IME, GME and DSH as well as rural provider support and it is not clear how such costs would be financed if Medicare is converted to a premium support system. If these costs are included in the calculation of traditional Medicare spending (as a plan bid), then traditional Medicare would be incurring costs that are not covered by private plans, putting traditional Medicare at a financial disadvantage. If the costs of IME, GME, DSH, and rural supplements are excluded from the costs of traditional Medicare, then it raises the questions of how these costs would be covered and by whom.

Policymakers have also debated the timing of implementation of a premium support proposal. Some have suggested establishing a premium support system that would take effect a decade from now in order to protect people who are currently in the program or will be eligible within that 10-year window. However, if not implemented prior to 2023, this approach would do little to address deficit concerns within the traditional 10-year budget window. An alternative approach is to proceed in the short term with a demonstration project that would have private Medicare Advantage plans competitively bid against each other (traditional Medicare would not submit a bid) to test and improve the model before applying it to the entire Medicare population.

Policy Options

Setting Federal Contributions to Plans Under Premium Support

The methodology for determining the amount paid by the Federal government per Medicare beneficiary is a critical variable for understanding the expected effects on outlays, beneficiaries’ out-of-pocket spending, traditional Medicare, and private health plans. Following are three methodologies that have been discussed in recent policy proposals.

OPTION 4.3

Set Federal contributions per beneficiary at the lesser of the second lowest private plan bid in a given area or average spending per capita under traditional Medicare in the area

Under this approach, plans would bid to compete in local areas, such as counties, as is the case today with Medicare Advantage. Each year, the Federal government would pay plans an amount (known as “the benchmark”) that would be no higher than the second lowest private plan bid in a given area, or average traditional Medicare costs in that area. Beneficiaries who chose a plan with a bid above the Federal contribution would pay a higher premium, and those who chose a plan with a bid below the benchmark would pay less.

Budget effects

No cost estimate is available for this option. Medicare savings would vary based on some of the decisions cited above. A model advanced by Rep. Ryan, for example, would place a limit on Medicare spending equal to the rise of the gross domestic product plus 0.5 percent (GDP+0.5%) beginning after 2023. The Congressional Budget Office (CBO) estimated Rep. Ryan’s proposal would reduce projected growth in Medicare spending from 7 percent of GDP to 4.75 percent of GDP in 2050 and reduce Medicare spending for the average 66-year-old in 2030 from $9,600 a year to $7,400 (in 2011 dollars) (CBO 2012).10

Discussion

The effects of this approach would vary widely across the country, depending on the relationship between traditional Medicare costs and plan bids. In areas where traditional Medicare costs are high relative to plan bids, beneficiaries would pay more for traditional Medicare than they would pay under the current system. In areas where traditional Medicare costs currently are lower than private plan bids, beneficiaries in traditional Medicare would likely not pay higher premiums, but those in private plans would be expected to pay more unless they switched to traditional Medicare. According to a 2012 analysis by the Kaiser Family Foundation, about half of all beneficiaries enrolled in the traditional Medicare program would pay higher Medicare premiums under a fully implemented system, unless they switched to a low-cost plan in their area (Kaiser Family Foundation 2012). If this approach to premium support were to be enacted in conjunction with a cap on Medicare per capita spending, Federal savings could increase as would premiums and/or other out-of-pocket costs.

OPTION 4.4

Set Federal contributions per beneficiary at the average plan bid in a given area (including traditional Medicare as a plan), weighted by enrollment

Under the Federal Employees Health Benefits Program (FEHBP), the Federal government contributes the lesser of 72 percent of the weighted average plan premium, or 75 percent of a plan’s premium. If employees choose a plan that bids below the weighted average bid, they pay a lower premium; if they choose a plan with higher costs, they pay more. Medicare could take a similar approach and have each plan, including traditional Medicare, submit a bid and the Federal contribution would be equal to the average bid in each area, weighted by plan enrollment, with enrollees paying the difference between the plan bid and the contribution.

Budget effects

In 2008, CBO estimated that a premium support system with the Federal contribution set at 100 percent of the average plan bid would reduce Medicare spending by an estimated $161 billion over 2010–2019 (had it been implemented in 2012) (CBO 2008).11 Some have proposed setting the payment at 88 percent (rather than 100 percent) of the average bid in a given area, weighted by enrollment (Heritage 2011). Such an approach would further reduce spending.

Discussion

If Medicare payments per beneficiary are set to equal the weighted average bid, then Federal contributions would be more sensitive to the underlying cost of care and to beneficiary plan preferences than they would if the contribution was based on the lesser of the second lowest cost plan or traditional Medicare (as outlined in Option 4.3). For example, if the majority of beneficiaries in an area chose to enroll in a higher-cost plan, Medicare spending per beneficiary would be higher than they would be if payments were tied to the lowest cost plan in the area.

OPTION 4.5

Set Federal base year payments equal to average traditional Medicare per capita costs and limit the growth per person to an economic index

Under this approach, Medicare would calculate a payment per beneficiary in a base year and index these payments over time by a measure of inflation (e.g., the Consumer Price Index for Urban areas (CPI-U) or GDP), without regard to the growth in health care spending per beneficiary or geographic variations in the growth of health care spending. The payment would be applied toward the cost of a private plan, and beneficiaries would be responsible for any costs above the government contribution.12

Budget effects

No cost estimate is available for this option. The savings from this approach would depend on the index used to increase the Medicare contribution over time. Although CBO did not provide a cost estimate of Rep. Ryan’s Fiscal Year (FY) 2012 proposal, it is estimated that, within nine years of implementation, the Federal contribution for a typical 65-year-old would be about 22 percent lower than under CBO’s “alternative fiscal scenario” (CBO 2011).13 This would occur because the Federal contribution would rise slower than the costs of private plans, which would shift costs onto beneficiaries.

Discussion

This option would provide the greatest predictability for the Federal budget because payments would not be affected by variations in health care spending, plan bidding strategies, or beneficiaries’ plan choices. However, this option would shift financial risk onto beneficiaries, and could result in significant additional costs for people with Medicare. CBO estimated that if Rep. Ryan’s FY 2012 proposal were implemented in 2022, out-of-pocket spending would increase by $6,240 for a typical 65-year-old in that year (largely because the expected costs of providing benefits would be greater under private plans than under traditional Medicare) (CBO 2011).

References

Click to expand/collapse

American Enterprise Institute (AEI). 2012. Competitive Bidding Can Help Solve Medicare’s Fiscal Crisis, February 2012.

Joseph Antos, Mark V. Pauly, and Gail R. Wilensky. 2012. “Bending the Cost Curve through Market-Based Incentives.” New England Journal of Medicine, August 2, 2012.

Jason Brown, Mark Dugan, Ilyana Kuziemko, and William Woolston. 2011. “How Does Risk Selection Respond to Risk Adjustment? Evidence from the Medicare Advantage Program,” National Bureau of Economic Research, April 2011.

Congressional Budget Office (CBO). 2008. Budget Options, Volume 1: Health Care, December 2008.

Congressional Budget Office (CBO). 2011. Long-Term Analysis of a Budget Proposal by Chairman Ryan, April 5, 2011.

Congressional Budget Office (CBO). 2012. The Long-Term Budgetary Impact of Paths for Federal Revenues and Spending Specified by Chairman Ryan, March 2012.

The Heritage Foundation. 2011. The Second Stage of Medicare Reform: Moving to a Premium Support Program, November 2011.

Kaiser Family Foundation. 2011. Proposed Changes to Medicare in the “Path to Prosperity,” April 2011.

Kaiser Family Foundation. 2012. Transforming Medicare into a Premium Support System: Implications for Beneficiary Premiums, October 2012.

Medicare Payment Advisory Commission (MedPAC). 2012. Report to the Congress: Medicare and the Health Care Delivery System, June 2012.

Exhibit 4.1: Medicare Benefits and Cost-Sharing Requirements, 2013

Exhibit 4.2: Distribution of Traditional Medicare Beneficiaries, by Change in Expected Out-of-Pocket Spending Under an Alternative Medicare Benefit Design, 2013