KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

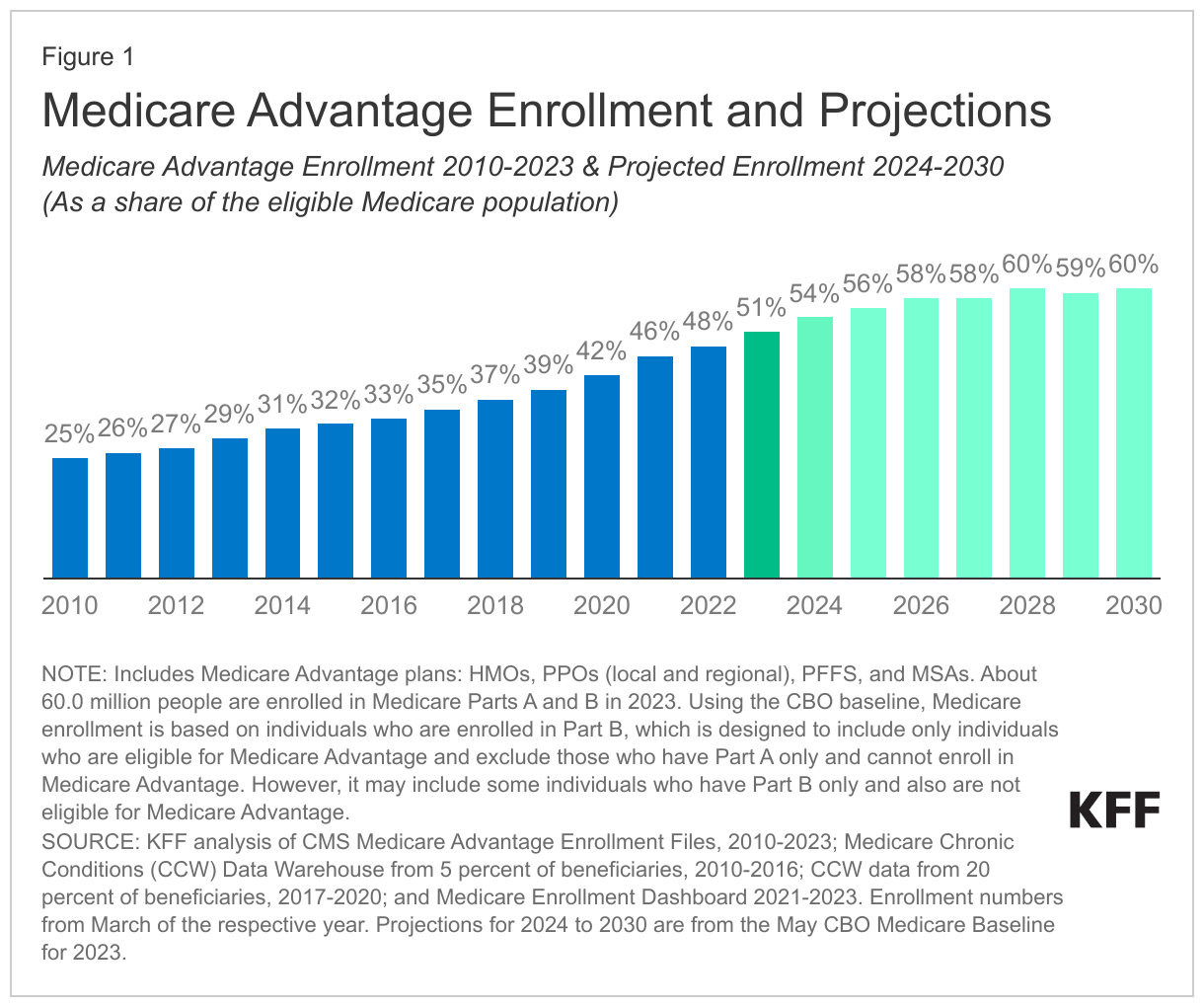

For the first time in Medicare’s history, more than half of all eligible people with Medicare, or 30.8 million people in 2023, are enrolled in private Medicare Advantage plans. Medicare Advantage plans are offered by private health insurance companies that receive payments from the federal government to provide Medicare-covered services. People with Medicare have a choice between traditional Medicare (sometimes called fee-for-service Medicare or Original Medicare) and Medicare Advantage plans. The growth in Medicare Advantage enrollment is driven by a number of factors, including the Medicare payment system, which has served to attract and retain insurers and beneficiaries, rather than reduce Medicare spending.

Medicare Advantage enrollment has more than doubled since 2010 and is projected to grow from 54% of the eligible population in 2024 to 60% by the end of this decade (Figure 1).

While some of the larger Medicare Advantage insurers are reporting lower profits due to a slowdown in enrollment growth and higher than expected utilization and costs among enrollees this year, there are many reasons to expect continued Medicare Advantage enrollment growth in the years ahead, given the financial incentives embedded in Medicare’s payment system.

The Medicare Payment Advisory Commission (MedPAC) recently reported that Medicare will pay Medicare Advantage plans an estimated 123% of the cost of similar beneficiaries in traditional Medicare, on average, in 2024, factoring in rebates, coding intensity (i.e., how plans record the health conditions of enrollees for payment purposes), and favorable selection. This year, MedPAC made a change in its estimation methodology to take into account the effects of favorable selection, building on the work of other researchers. Favorable selection occurs when plans are enrolling healthier and lower cost enrollees than predicted by the current payment system.

MedPAC now estimates that these higher payments to Medicare Advantage plans translate into $88 billion in additional Medicare spending in 2024 and $13 billion in higher Medicare Part B premiums paid by Medicare beneficiaries in 2024. While some may take issue with the methodology used to generate these estimates, the projected impact on Medicare spending is likely to raise concerns among some policymakers. Higher Medicare spending affects the solvency of the Medicare Hospital Insurance (HI) Trust Fund and increases Medicare premiums for beneficiaries in both Medicare Advantage and traditional Medicare.

In light of these spending projections, here we lay out 10 reasons why Medicare Advantage enrollment has been growing and why we can expect more growth in the years to come.

People with Medicare are drawn to Medicare Advantage for the extra benefits. Medicare Advantage plans offer extra benefits, like reduced cost-sharing, dental coverage, gym memberships and debit cards for over-the-counter medical supplies that are not covered by traditional Medicare. These extra benefits are funded by what are known as “rebates,” that is, the difference between the amount that plans bid (estimated spending per enrollee on Medicare-covered services) and the benchmark (the maximum amount Medicare will pay per enrollee in a given county). Plans are required to use rebate dollars to reduce cost sharing or premiums, or provide extra benefits, while also keeping a share of rebate dollars for profit and administrative overhead.

People with Medicare are drawn to Medicare Advantage plans that are marketed as “zero premium” products. Like traditional Medicare beneficiaries, Medicare Advantage enrollees are required to pay the Medicare Part B premium, but unlike beneficiaries in traditional Medicare, they typically do not pay a separate premium for additional coverage or for Part D prescription drug premium because Medicare Advantage rebate dollars cover these costs.

Premiums for Part D stand-alone prescription drug plans that supplement traditional Medicare are rising rapidly. On a related note, beneficiaries in traditional Medicare are seeing premiums for stand-alone prescription drug plans rising rapidly, which may lead some to switch to Medicare Advantage to lower monthly expenses. The estimated enrollment-weighted premium for Part D stand-alone drug plans is projected to increase by 21% between 2023 and 2024, from $40 to $48 per month, according to KFF analysis.

People with Medicare are attracted to the financial protection that comes with an annual out-of-pocket limit that Medicare Advantage plans are required to provide. In contrast, traditional Medicare, with about 30 million beneficiaries, does not have an out-of-pocket limit. The Affordable Care Act requires private employer and individually-purchased insurance plans to cap out-of-pocket costs.

Beyond financial benefits, people with Medicare are attracted to the simplicity and convenience of Medicare Advantage, which provides all coverage in one plan, obviating the need to obtain a Medicare Part D plan and a Medigap plan, as many traditional Medicare beneficiaries have.

Brokers have a financial incentive to encourage enrollment in Medicare Advantage plans because commissions are higher for Medicare Advantage than for Medigap and Part D plans that are purchased to complement traditional Medicare.

A growing share of large employers are shifting their Medicare-age retirees into Medicare Advantage plansfor both Medicare and supplemental benefits. KFF research has shown that employers are shifting their retirees to Medicare Advantage as a strategy to maintain benefits, simplify administration and lower their own costs. The shift to Medicare Advantage may reduce costs to employers and unions but also means that retirees may not have the option to choose traditional Medicare, unless they forfeit their retiree health benefits.

Medicare beneficiaries may be reluctant to switch from Medicare Advantage to traditional Medicare if they run the risk of being denied a Medigap policy due to a pre-existing condition. Medicare Advantage enrollees can switch to traditional Medicare during the annual open enrollment period but may not be able to purchase a Medigap policy. Federal law provides very limited protections for people with pre-existing conditions to enroll in a Medigap policy. Only four states have guaranteed issue protections for Medigap.

Beneficiaries may not be familiar with potential tradeoffs in choosing Medicare Advantage over traditional Medicare. For example, Medicare Advantage plans may have network restrictions that could prevent enrollees from being seen by certain doctors, hospitals and skilled nursing facilities, and often use prior authorization to manage utilization, which may make it difficult for some enrollees to get treatment or may delay treatment recommended by their doctors, and creates administrative hassles for their providers.

As Medicare Advantage enrollment continues to climb, traditional Medicare is on track to diminish as a source of Medicare coverage, leaving in its place a program that looks more like a marketplace of private health insurance plans, funded by the federal government. This doesn’t come as a surprise. Policy choices made over the years have resulted in higher payments to plans relative to spending for similar people in traditional Medicare, allowing plans to reduce cost sharing and offer extra benefits that appeal to beneficiaries and have boosted enrollment well beyond expectations.

At the same time, gaps in data make it difficult to assess the impact of Medicare Advantage coverage on people who enroll in these plans, particularly those with significant health needs. Given these trends, policymakers are likely to struggle in the years ahead with how to contain the cost to the federal government of Medicare Advantage, what that means for enrollees, and what the future holds for traditional Medicare.

This work was supported in part by Arnold Ventures. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

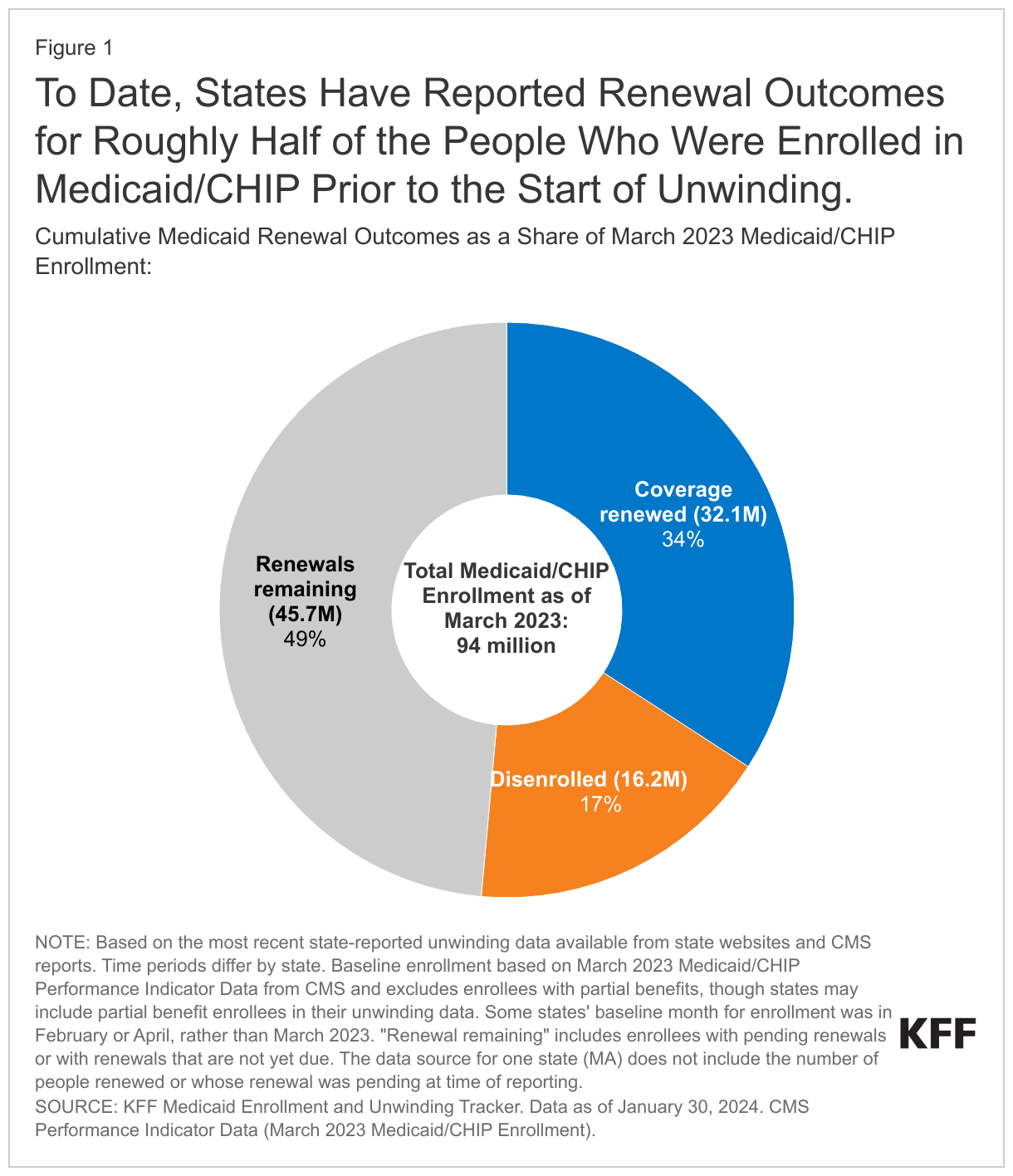

Ten months into the unwinding of the Medicaid continuous enrollment provision, states have reported renewal outcomes for half of all enrollees whose eligibility needs to be reviewed during the unwinding period, including 34% (32.1 million) who have had their coverage renewed, and 17% (16.2 million) who have been disenrolled, according to KFF’s latest analysis of state-level data.

There are reasons to expect disenrollment rates to moderate in the second half of the unwinding as states reduce procedural disenrollments and work through “likely ineligible” populations.

Since the start of the unwinding, Medicaid enrollment has declined by about 10% nationally based on the latest available data, with decreases in every state, ranging from 32% in Idaho to 1% in Maine. Two states—South Dakota and North Carolina—expanded Medicaid in 2023, which should limit enrollment declines in those states.

Other state and federal policies could also affect Medicaid enrollment and access to other coverage in the months ahead. Several states may consider proposals to adopt the Affordable Care Act (ACA) Medicaid expansion this year, though the outcomes of those debates are uncertain. In the 10 states that have not adopted Medicaid expansion, nearly 1.5 million uninsured individuals fall into the “coverage gap,” and are not eligible for Medicaid or ACA Marketplace subsidies.

Implementation of 12-month continuous coverage for children and postpartum individuals, as well as extended multi-year continuous eligibility for children in some states, could help to stabilize coverage after the unwinding.

Still, the Medicaid unwinding’s impact on broader coverage trends remains to be seen. While national data show record enrollment in ACA Marketplace coverage, a relatively small share of this growth appears to come from people who have transitioned from Medicaid to the Marketplace. Also, data on the number of people reenrolling in Medicaid after being dropped, transitioning to employer coverage, or becoming uninsured are currently limited.

As the start of 2024, many issues are at play that will affect Medicaid coverage, financing, and access. Medicaid is the primary program providing comprehensive health and long-term care coverage to one in five low-income Americans. The unwinding of the Medicaid continuous enrollment provision started on April 1, 2023, and will continue to be the dominant Medicaid policy issue in 2024. However, adoption of the Affordable Care Act (ACA) Medicaid expansion and other coverage and access expansions, efforts to address social determinants of health and facilitate re-entry for individuals transitioning from incarceration, long-term services and supports (LTSS) workforce, and Medicaid financing are also key areas to watch. Medicaid may not be a major issue in the presidential election, but debate about repeal and replace of the ACA, Medicaid work requirements, and federal financing for Medicaid could emerge as national election issues. In addition, as a major source of coverage for births, Black, Hispanic, American Indian or Alaska Native and Native Hawaiian or Other Pacific Islander populations, some lawfully present immigrants, low-income children, working-age people with disabilities, and people needing long-term services and supports, Medicaid may underpin larger 2024 election issues. At the same time, many states have seen revenues decline recently, which could increase pressure to reduce spending in Medicaid and other programs. This issue brief provides context for these Medicaid issues and highlights key issues to watch in the year ahead.

Unwinding of the Continuous Enrollment Provision

The unwinding of the continuous enrollment provision will be the dominant Medicaid policy issue in 2024. Policies put in place to pause Medicaid disenrollments during the pandemic ended on March 31, 2023. At the start of the unwinding period, in April 2023, Medicaid enrollment peaked at 94.5 million, an increase of 23 million or 32 percent from before the pandemic. As of the end of January 2024, states have reported renewal outcomes for half of all enrollees, including 34% (32.1 million) who have had their coverage renewed and 17% (16.2 million) who have been disenrolled. The share of disenrollments occurring for procedural or paperwork reasons remains high in many states, and amid growing concern over loss of Medicaid coverage for children, in December 2023, federal officials issued new data and additional guidance highlighting strategies to reduce procedural disenrollments for children. The Secretary of HHS also sent letters to nine states with large declines in Medicaid child enrollment, urging them to take up additional policy options to prevent procedural disenrollments. As unwinding continues in 2024, data and experiences on the ground can provide insights about effective strategies to promote continuity of coverage and minimize procedural disenrollments. Overall, the Medicaid enrollment has declined by nearly 10% across states since the start of unwinding in each state, with rates ranging from 32% in Idaho to 1% in Maine.

Medicaid Coverage and Access Expansions

At the start of state legislative sessions, several non-expansion states may consider proposals to adopt the ACA Medicaid expansion. South Dakota and North Carolina implemented the Medicaid expansion in 2023. In the 10 states that have not adopted the ACA Medicaid expansion, nearly 1.5 million uninsured individuals fall into the “coverage gap.” These individuals do not qualify for Medicaid but have incomes below poverty, making them ineligible for premium subsidies in the ACA Marketplace. The American Rescue Plan Act (ARPA) included a temporary fiscal incentive designed to encourage states to newly adopt the expansion that has helped to reignite expansion discussions. While legislative leaders in Florida remain opposed to expansion, Republicans in Georgia, Alabama, and Mississippi may be open to a non-traditional Medicaid expansion that would include provisions not otherwise allowed under current law (Arkansas, Indiana, Michigan and Utah are examples of states that operate Medicaid expansion through an approved Section 1115 waiver). In addition, the Kansas governor, a longtime proponent of expansion, once again included the proposal in her recently released budget, along with a proposed work requirement. While some states may be debating expansion, former President Trump announced he would renew efforts to replace the ACA if elected, which could result in reduced Medicaid coverage and financing.

Other state and federal policies may expand coverage for certain groups. Nearly all states (47) have adopted an option to extend postpartum coverage from 60 days to 12 months. The Consolidated Appropriations Act included a requirement for all states to implement 12 months of continuous eligibility for children as of January 2024, and Oregon, Washington, and New Mexico have gone further, receiving waiver approval to provide continuous eligibility for children from birth to age 6. Other states are pursuing similar proposals. KFF analysis shows that continuous eligibility policies help to provide coverage stability for children. At the federal level, the Biden Administration proposed broad regulations to make it easier for individuals to obtain and maintain coverage; and finalized the provisions to help low-income Medicare beneficiaries gain access to Medicaid coverage of Medicare premiums and often, cost sharing, through the Medicare Savings Programs.

In addition to policies to expand coverage, there is likely to be a continued effort to help ensure access to services in Medicaid. Compared to adults with private coverage or Medicare, Medicaid enrollees are more likely to face problems with provider availability and prior authorization; however, because of federal rules that limit out-of-pocket costs, Medicaid enrollees are less likely to report cost-related problems. Pending federal rules aim to help address availability of providers and access in Medicaid by strengthening Medical Care Advisory Committees (to allow for more meaningful engagement from Medicaid enrollees), increasing transparency for fee-for-service (FFS) and managed care payments, establishing national maximum appointment wait time standards for managed care enrollees, and requiring state monitoring related to access and network adequacy for managed care plans. In addition, the Biden administration recently finalized rules to streamline prior authorization processes for Medicaid and other payers. At the state level, efforts to expand the scope of covered services (particularly for behavioral health), implement initiatives to address health disparities and enhance payment rates are key strategies underway to help bolster access to care for Medicaid enrollees.

Social Determinants of Health and Re-Entry

States and the Administration are implementing strategies to leverage Medicaid to address social determinants of health (SDOH). To expand opportunities for states to use Medicaid to address health-related social needs (HRSN) such as housing instability and nutrition insecurity, CMS announced new flexibilities available to states through managed care and through Section 1115 demonstration waivers. New CMS guidance accompanies the Biden-Harris Administration’s release of the U.S. Playbook to Address Social Determinants of Health and HHS’s Call to Action to Address Health-Related Social Needs. As of January 2024, CMS has approved Section 1115 demonstrations in eight states (Arizona, Arkansas, California, Massachusetts, New Jersey, New York, Oregon, and Washington) under the new HRSN 1115 framework that authorize evidence-based HRSN services for specific high-need populations. Approvals include coverage of rent/temporary housing and utilities for up to 6 months and meal support up to three meals per day (up to 6 months). These initiatives also require states to meet minimum provider payment rate requirements for primary care, behavioral health, and obstetrics services to bolster access and to complement (rather than replace) other efforts.

California and Washington received approval and a number of other states have proposals pending for waivers to facilitate re-entry for individuals who are incarcerated. In April 2023, CMS released guidance encouraging states to apply for a new Section 1115 demonstration opportunity to test transition-related strategies to support community re-entry and care transitions for individuals who are incarcerated. This opportunity allows states to partially waive the statutory Medicaid inmate exclusion policy, which prohibits Medicaid from paying for services provided during incarceration (except for inpatient services). Congress is also considering several re-entry provisions in debate about reauthorization of the SUPPORT Act (major legislation passed in 2018 to address the opioid epidemic) including preventing Medicaid disenrollment due to incarceration, a policy that could help ensure continuity of Medicaid coverage after leaving incarceration.

Workforce Challenges in Long Term Services and Supports and Behavioral Health

Federal and state governments are responding to increased workforce shortages and unmet needs among people who use long-term services and supports (LTSS). The Administration proposed a rule creating new staffing requirements in nursing facilities, requiring state Medicaid agencies to report the percentage of Medicaid spending for institutional LTSS that goes to compensation for direct care workers and support staff, and providing funding for individuals to enter careers in nursing facilities. A proposed rule aimed at ensuring access to all Medicaid services addresses the LTSS that are provided in non-institutional settings, which are often referred to as home- and community based services (HCBS). The proposed rule would establish requirements regarding states’ payment rates for HCBS, among other provisions intended to address access to HCBS and Medicaid services more broadly.States have responded to workforce challenges by increasing Medicaid payment rates for nursing facilities and HCBS as reported to KFF in a 2023 survey; but employment levels remained 10% below pre-pandemic levels in October 2023. As the primary payer of LTSS, pressure to further increase staffing and raise reimbursement rates may fall disproportionately to Medicaid, where financing is shared between states and federal government.

Lack of adequate workforce to meet increasing demands for mental health and substance use disorder services is likely to persist in 2024. States are working to expand Medicaid access to behavioral health services through efforts to build out the behavioral health continuum of care, integrate physical health and behavioral health services, implement mobile crisis services, and expand behavioral health services in schools. However, access depends on the availability of a mix of services and the capacity of the behavioral healthworkforce. To help bolster the behavioral health workforce, states are implementing several strategies including increasing rates, reducing burden and adding incentives for providers to participate in Medicaid, and extending workforce.

Medicaid Financing

Slowing state revenue growth could have implications for Medicaid policy and spending. Medicaid financing is shared by the federal government and the states. Consequently, economic factors that affect state revenues including inflation, supply chain issues, labor force participation rates, and changes in the stock market have fiscal implications for states. As state legislatures develop FY 2025 budgets, they are facing declining revenues and the expiration of pandemic-era supports from the federal government, that could limit Medicaid investments or prompt proposals to cut Medicaid spending to help maintain balanced budgets. In 2024, declines in enrollment will contribute to lower Medicaid spending growth but the expiration of enhanced federal matching funds will increase state spending. Heading into FY 2025, considerable uncertainty remains about overall Medicaid enrollment and the health care needs of enrollees that retain coverage. Even though national economic indicators remain strong, pandemic-related supports for households have also expired and families are still struggling to cover costs from record inflation during the pandemic. Broader debates about Medicaid financing could arise during the Presidential election related to efforts to reduce the federal deficit and limit entitlement spending; these are areas of considerable policy differences between Republican candidates and President Biden.

What to Watch

The issues identified in this policy watch could have major implications for Medicaid coverage, financing, and access. As these issues play out, the following key questions will be at the forefront:

Who will win the presidency and control Congress, which will have major implications for Medicaid policy going forward?

How will the Medicaid unwinding affect Medicaid enrollment and changes in coverage, including increases in the number of people who are uninsured?

Will states adopt Medicaid coverage expansions in 2024, including Medicaid expansion or multi-year continuous eligibility for children?

How many states will advance new initiatives to use Medicaid to address health-related social needs or facilitate transitions from incarceration in 2024?

How will federal and state efforts to address workforce shortages for LTSS and behavioral health evolve in 2024?

How will state fiscal conditions and broader economic factors affect Medicaid spending as well as state and federal Medicaid policy?

Ten months into the unwinding of the Medicaid continuous enrollment provision, states are continuing to reverify the eligibility of the roughly 94 million enrollees in the program. KFF tracking shows that states have reported outcomes for roughly half of the people expected to undergo renewals during the unwinding period. This policy watch examines the latest data and key issues to watch during the next phase of the unwinding.

What Do the Data Show?

As of the end of January 2024, states have reported renewal outcomes for half of all enrollees, including 34% (32.1 million) who have had their coverage renewed and 17% (16.2 million) who have been disenrolled (Figure 1). Due to lags in data reporting, which vary from one to three months across states, the number of completed renewals is an undercount. Prior to the start of the unwinding, KFF projected that 17 million people would be disenrolled during the unwinding based on state estimates, but noted the range could be 8 to 24 million people disenrolled because of the uncertainty and expected variation across states. Given how many renewals are left to complete, disenrollments are highly likely to exceed 17 million.

There is significant variation in the share of completed renewals across states, ranging from 87% in Oregon to 22% in Wyoming (Figure 2). Some of this variation reflects when states resumed disenrolling people as well as differences in the pace of processing renewals. But actions some states have taken in response to inappropriate or high procedural disenrollment rates are also a factor. In August and September, 30 states were required to reinstate coverage and temporarily pause disenrollments for some enrollees to address non-compliance with federal rules. Some states also voluntarily extended renewal deadlines to delay procedural disenrollments while they conduct additional outreach to enrollees. Finally, the variation across states also reflects differences in how states report unwinding data and the frequency of updates.

Since the start of unwinding, Medicaid enrollment has declined in every state, ranging from 32% in Idaho to 1% in Maine (Figure 3). Overall, the Medicaid enrollment has declined by nearly 10% across states since the start of unwinding. The enrollment declines shown here are measured against each state’s baseline enrollment, which is enrollment in the month prior to when the state resumed disenrollments and which varies by state. Due to the lags in reporting, current enrollment declines are greater in some states. Changes in enrollment reflect the people who disenroll from Medicaid as well as those who newly enroll, and those who re-enroll within a short timeframe following disenrollment, also known as “churn.” Two states, South Dakota and North Carolina, implemented the Medicaid expansion since the start of unwinding (in July and December 2023, respectively), which should mitigate enrollment declines in these states.

Looking Ahead

Disenrollment rates could moderate in the second half of the unwinding as states continue efforts to reduce procedural disenrollments and because some states have worked through “likely ineligible” populations. Many states continue to adopt flexibilities during the unwinding to improve ex parte renewal processes, which reduce paperwork burden on enrollees and can reduce procedural termination rates. In addition, some states have worked through renewals for people the state flagged as likely ineligible, who the states prioritized for renewals early in the unwinding. The remaining population in these states is more likely to still be eligible and, therefore, less likely to be disenrolled. For example, Arkansas and Idaho recently announced that they completed renewals for “likely ineligible” enrollees after six months of unwinding, and the number and rate of disenrollments declined in subsequent months (the total number of renewals also declined steeply in both states).

The unwinding’s implications for broader coverage trends are not yet known. There is currently limited data on how many people losing Medicaid are reenrolling in Medicaid, transitioning to other sources of health coverage, including employer coverage and coverage through the Affordable Care Act (ACA) Marketplaces, or becoming uninsured. Data for 2022 showed the national uninsured rate had dropped to 7.9%, the lowest level on record. While the unwinding will likely contribute to increases in the number of people who are uninsured and in the uninsured rate, it is unclear what the magnitude of these increases will be. Federal survey data will not be available to understand these trends until well after the unwinding period ends, and surveys that rely on self-reported health insurance status significantly undercount Medicaid enrollment. In the meantime, state and national administrative data on ACA Marketplace enrollment and private insurance coverage can shed some light on the coverage picture. However, while national data show record enrollment in Marketplace coverage, Medicaid unwinding is only one factor contributing to that growth and a relatively small share of people disenrolled from Medicaid are transitioning to Marketplace or Basic Health Plan coverage. It will be some time before there is a more complete picture at the national level of how many people losing Medicaid find other coverage or become uninsured.

Ahead of the 2024 general election, a new KFF brief examines abortion ballot initiatives in progress in 13 states. These 13 states could follow six other states that have voted on constitutional amendments to protect or restrict abortion since the Supreme Court’s Dobbs decision overturning Roe v. Wade in 2022. In those six states, the side favoring access to abortion prevailed.

Citizen-led abortion ballot initiatives have captured nationwide attention and promise to be closely watched; advocacy groups on both sides of the issue have sought to use this powerful tool to address the legality of abortion in their state and drive voter turnout at the polls this November. However, in many states that currently ban or severely restrict abortion, there is no legal pathway for a citizen-initiated constitutional amendment to make it on the ballot.

“Addressing Abortion Access through State Ballot Initiatives” also outlines the processes states can use to place initiatives on the ballot and explains why advocates on both sides of the abortion issue, seeking more stable abortion laws, have turned to ballot initiatives.

Social determinants of health (SDOH) are the conditions in which people are born, grow, live, work and age. While there are limits, states can use Medicaid – which, by design, serves a primarily low-income population with greater social needs – to address social determinants of health. To expand opportunities for states to use Medicaid to address health-related social needs, The Centers for Medicare & Medicaid Services or CMS announced new flexibilities available to states through managed care and through Section 1115 demonstration waivers. New CMS guidance accompanies the Biden-Harris Administration’s release of the U.S. Playbook to Address Social Determinants of Health and HHS’s Call to Action to Address Health-Related Social Needs. While health programs like Medicaid can play a supporting role, CMS stresses the new HRSN initiatives are not designed to replace other federal, state, and local social service programs but rather to complement and coordinate with these efforts. The resources provided to date through Medicaid are relatively modest in comparison to the social needs that exist. This brief outlines the range of Medicaid authorities and flexibilities that can be used to add benefits and design programs to address the social determinants of health (Figure 1).

Figure 1: State Medicaid programs have some flexibility to address enrollee social determinants of health.

What Are Social Determinants of Health?

Social determinants of health are the conditions in which people are born, grow, live, work and age.1They include factors like economic stability, education, neighborhood and physical environment, employment, and social support networks, as well as access to health care (Figure 2).

Figure 2: Though health care is essential to health, research shows that health outcomes are driven by many factors.

Though health care – and, by extension, health coverage – is essential to health, research shows that health outcomes are driven by an array of factors, including underlying genetics, health behaviors, social, economic, and environmental factors. While there is currently no consensus in the research on the magnitude of the relative contributions of each of these factors to health, studies suggest that health behaviors and social and economic factors are primary drivers of health outcomes, and social, and economic factors can shape individuals’ health behaviors. There is extensive research that concludes that addressing social determinants of health is important for improving health outcomes and reducing health disparities.2

Both health and non-health sectors have been engaged in initiatives to address social determinants of health. Outside of the health care system, non-health sector initiatives seek to shape policies and practices in ways that promote health and health equity. Within the health care sector, a broad range of initiatives have been launched at the federal, state, and local levels and by plans and providers to address social determinants of health, including efforts within Medicaid.

How Can Medicaid be Used to Address Social Determinants of Health?

State Medicaid programs can add certain non-clinical services to home and community-based services (HCBS) programs to support seniors and people with disabilities. Generally, states have not been able to use federal Medicaid funds to pay the direct costs of non-medical services like housing and food.3 However, within Medicaid, states can use a range of state plan and waiver authorities (e.g., 1905(a), 1915(i), 1915(c), or Section 1115) to add certain non-clinical services to the Medicaid benefit package including case management, housing supports, employment supports, and peer support services. Historically, non-medical services have been included as part of Medicaid home and community-based services programs for people who need help with self-care or household activities as a result of disability or chronic illness.

Outside of Medicaid HCBS authorities, state Medicaid programs have historically had more limited flexibility to address social determinants of health. Certain options exist under Medicaid state plan authority as well as Section 1115 authority to add non-clinical benefits. Additionally, under federal Medicaid managed care rules, managed care plans have some flexibility to pay for non-medical services. Other Medicaid payment and delivery system reforms, like the formation of Accountable Care Organizations (ACOs), may provide flexibility or opportunities to cover non-medical services that support health as well.

To expand opportunities for states to use Medicaid to address health-related social needs, CMS announced new flexibilities available to states through Medicaid managed care authority and through Section 1115 demonstration waivers. CMS defines health-related social needs (or “HRSN”) as an individual’s unmet, adverse social conditions (e.g., housing instability, homelessness, nutrition insecurity) that contribute to poor health and are a result of underlying social determinants of health. New CMS guidance builds on guidance released in 2021. The remaining sections outline the primary Medicaid authorities and flexibilities that can be used to add benefits and design programs to address the social determinants of health beyond HCBS programs. Some efforts may address a single issue (e.g., housing, or food security) while other efforts and initiatives are designed to address a range of social determinants of health.

Medicaid Managed Care Plan Authority

Withover two-thirds of Medicaid beneficiaries enrolled in comprehensive, risk-based managed care plans nationally, health plans can be an important part of efforts to address enrollee social determinants of health. States pay Medicaid managed care organizations (MCOs) a set per member per month payment for the Medicaid services specified in their contracts. Capitation rates provide upfront fixed payments to plans for expected utilization of covered services, administration costs, and profit.

Under federal Medicaid managed care rules, Medicaid MCOs can be given flexibility to pay for non-medical services through “in-lieu-of” authority. States may allow Medicaid MCOs the option to offer (and provide beneficiaries the option to receive) services or settings that substitute for standard Medicaid benefits (referred to as “in lieu of” services (or “ILOS”)) if the substitute service is medically appropriate and cost-effective. For example, a state could authorize in-home prenatal visits for at-risk pregnant beneficiaries as an alternative to traditional office visits or services provided by peer supports, as an alternative to psychosocial rehabilitation services for members with behavioral health needs. The costs of the ILOS are built into managed care rates. In January 2023, CMS released guidance that paves the way for states to allow Medicaid MCOs to offer services, like housing and nutrition supports, as substitutes for standard Medicaid benefits.4 The new guidance establishes financial guardrails and new requirements for ILOS and clarifies these substitute services can be preventive in nature instead of an immediate substitute (e.g., providing a dehumidifier to an individual with asthma before emergency care is needed). This guidance follows the approval of a California proposal to use ILOS. In May 2023, the Biden administration issued a proposed rule related to managed care access, finance, and quality. In the proposed rule, CMS seeks to codify its January 2023 ILOS guidance.5KFF’s 2023 survey of state Medicaid directors found few states permitted MCOs to cover SDOH-related services (e.g., housing, food, or other) as ILOS as of July 2023.

Under federal rules, Medicaid MCOs can pay for non-medical services as “value-added” services. “Value-added” services are extra services MCOs voluntarily provide outside of covered contract services. These services cannot be built into managed care rates.6 Examples include safe sleeping spaces for infants, repairs and cleaning services to reduce asthma triggers, installation of a shower grab bar, and health play and exercise programs.

States may implement MCO procurement and contracting strategies, including quality requirements linked to SDOH.7In a 2023 KFF survey of Medicaid directors, most MCO states reported leveraging Medicaid MCO contracts to promote at least one strategy to address social determinants of health in FY 2023 (Figure 3). More than half of MCO states reported requiring MCOs to screen enrollees for social needs, screen enrollees for behavioral health needs, provide referrals to social services, and partner with community-based organizations (CBOs). Fewer states reported requiring MCO community reinvestment (i.e., directing plans to reinvest a portion of revenue or profits into the communities they serve) compared to other strategies. States can use incentive payments or quality withhold arrangements to reward plans for investments and/or improvements in SDOH. For example, states may provide incentive payments to plans that screen enrollees for social needs or make other strategic investments in addressing health-related social needs or incentive payments to improve or maintain quality while lowering costs. Additionally, many plans have developed initiatives and engaged in activities to address enrollees’ social needs beyond state requirements; however, it is difficult to compile national data to reflect this.

In the Institute for Medicaid Innovation’s 2023 Medicaid managed care survey, plans indicated state Medicaid agencies could support MCO efforts to address enrollee social needs by improving data sharing (e.g., between the state and MCOs and between government agencies), increasing financial resources (including to support the facilitation of partnerships and new payment models), and facilitating contracting with CBOs.

States can direct managed care plans to make payments to their network providers to further state goals and priorities, including those related to addressing social determinants of health. States can seek CMS approval to require MCOs to implement value-based purchasing models for provider reimbursement (e.g., pay for performance, bundled payments) or participate in multi-payer or Medicaid-specific delivery system reform or performance improvement initiatives. For example, a state may require managed care plans to implement alternative payment models (APMs) or incentive payments to encourage providers to screen for socioeconomic risk factors.

Section 1115 Waivers

Through Section 1115 authority, states can test approaches for addressing SDOH including requesting federal matching funds to test SDOH related services and supports in ways that promote Medicaid program objectives. Section 1115 waivers generally reflect priorities identified by states and CMS, as well as changing priorities from one presidential administration to another. While not required by statute, longstanding policy requires that Section 1115 waivers be budget neutral for the federal government. As outlined in CMS’s 2021 guidance, states can request federal matching funds through Section 1115 to test the effectiveness of providing SDOH-related services and supports. States can also test alternative payment methodologies designed to address SDOH under Section 1115 authority. Prior to the Biden administration announcement of new HRSN waiver flexibilities (discussed in more detail below), a number of states had approved Section 1115 waivers that aimed to address enrollee social determinants of health. These SDOH waivers were generally narrow in scope (services and target populations) or pilot programs targeting specific regions. For example, in October 2018, CMS approved North Carolina’s Healthy Opportunities Pilots that operate in three geographic regions of the state and provide services to address enrollee needs related to housing, food, transportation, and interpersonal safety. Some waivers allowed MCOs or ACOs flexibility to offer health-related services but stopped short of requiring them to do so.In December 2022, CMS announced a Section 1115 demonstration waiver opportunity to expand the tools available to states to address HRSN. In November 2023, CMS issued a detailed Medicaid and CHIP HRSN Framework accompanied by an Informational Bulletin (CIB). HRSN services that will be considered under the new framework include housing supports, nutrition supports, and HRSN case management (and other services on a case-by-case basis) (Figure 4). As of January 2024, CMS has approved Section 1115 demonstrations in eight states (Arizona, Arkansas, California, Massachusetts, New Jersey, New York, Oregon, and Washington) that authorize evidence-based HRSN services for specific high-need populations. Approvals include coverage of rent/temporary housing and utilities for up to 6 months and meal support up to three meals per day (up to 6 months). HRSN services must be medically appropriate (using state-defined clinical and social risk factors) and voluntary for enrollees. States can add HRSN services to the benefit package and may require managed care plans to offer the services to enrollees who meet state criteria. Federal expenditures are also available to build the capacity of community based HRSN providers that may require technical assistance and infrastructure support to become Medicaid providers. Additionally, the Biden administration has expressed support for “community care hubs” (or similar models) that focus on aligning health and social care and may facilitate care coordination as well as develop, manage, and support a network of CBOs.

CMS guidance specifies spending for HRSN cannot exceed 3% of total annual Medicaid spend. CMS indicates HRSN spending will not require offsetting savings (that may otherwise be required for services authorized/financed under Section 1115). State spending on related social services (before the waiver) must be maintained or increased. To strengthen access, states must also meet minimum provider payment rate requirements for primary care, behavioral health, and obstetrics services. HRSN services are subject to monitoring and evaluation requirements, including reporting on quality and health equity measures. In November 2023, HHS and HUD announced the launch of a new learning collaborative that will support states with the implementation of Section 1115 housing-related supports, including helping states improve collaboration and coordination between organizations and systems that provide housing services.

State Plan Authority & Delivery System Reform Models

States may elect to include optional benefits that address social determinants under Section 1905(a) State Plan authority. For example, states may include rehabilitative services, including peer supports and/or case management (or “targeted” case management8 ) services, under their Medicaid state plan. States that choose to offer these services frequently target services based on health or functional need criteria. Peer supports can help individuals coordinate care and social supports and services, facilitating linkages to housing, transportation, employment, nutrition services, and other community-based supports. Case management services can also assist individuals in gaining access to medical, social, educational, and other services. Case management services are frequently an important component of HCBS programs but can also be used to address a broader range of enrollee needs.

States can provide broader services to support health through the optional health home state plan benefit option established by the ACA. Under this option (Section 1945), states can establish health homes to coordinate care for people who have chronic conditions. Health home services include comprehensive care management, care coordination, health promotion, comprehensive transitional care, patient and family support, as well as referrals to community and social support services (such as housing, transportation, employment, or nutritional services). States receive a 90% federal match rate for qualified health home service expenditures for the first eight quarters under each health home.9,10 A federally funded evaluation of the Health Homes model found that most providers reported significant growth in their ability to connect patients to nonclinical social services and supports under the model, but that lack of stable housing and transportation were common problems for many enrollees that were difficult for providers to address with insufficient affordable housing and rent support resources.11

Integrated care models, including patient-centered medical home (PMCHs) and Accountable Care Organizations (ACOs), often emphasize person-centered, comprehensive care and typically involve partnerships with community-based organizations and social services agencies. 12Integrated care models might address social determinants of health through interdisciplinary care teams or care coordination services. Payment mechanisms tied to these models (e.g., per member per month payments (with or without quality or cost incentives) or shared savings/risk models with quality requirements) may provide incentives for providers to address the broad needs of Medicaid beneficiaries.

Looking Ahead

While health programs like Medicaid can play a supporting role, guidance from CMS stresses the new HRSN initiatives are not designed to replace other federal, state, and local social service programs but rather to complement and coordinate with these efforts. The resources provided through Medicaid to address social determinants of health are relatively modest in the face of the social needs that exist, and there is ongoing debate over how effectively the health care system can meet these needs.

Areas to watch include which health-related services states may gain approval to integrate under managed care authority and/or Section 1115, how states define target populations, and how CMS and states negotiate budget neutrality terms (an issue that Republican members of the US House Energy and Commerce have raised concerns about).

States that have not pursued but may be interested in new HRSN flexibilities can learn from the implementation experience of early adopters, including how states and plans work with community-based organizations and coordinate with federal, state, and local social service programs. While there is some evidence, 13,14,15,16,17 ILOS and Section 1115 monitoring and evaluation reports may yield new data involving how addressing certain enrollee social needs may impact health care utilization, spending, and health outcomes. Finally, whether states can sustain funding streams for HRSN longer term and how future changes in Administration may affect states’ ability to pursue these initiatives through waivers will be important to watch.

Federal financial participation is not available to state Medicaid programs for room and board except in certain medical institutions, as codified in multiple regulatory provisions. See, for example, 42 CFR § 441.310(a)(2) and 42 CFR §441.360(b). CMS defines board as three meals a day or any other full nutritional regimen, and room as hotel or shelter type expenses including all property related costs such as rental or purchase of real estate and furnishings, maintenance, utilities, and related administrative services. See section 4442.3 of the State Medicaid Manual at www.cms.gov/regulations-andguidance/guidance/manuals/paper-based-manuals-items/cms021927. ↩︎

An ILOS must not violate any applicable federal requirements, including general prohibitions on payment for room and board under title XIX of the Social Security Act. ↩︎

Medicaid Program; Medicaid and Children’s Health Insurance Program (CHIP) Managed Care Access, Finance, and Quality, 88 FR 28092 (May 3, 2023) (to be codified at 42 CFR 430, 42 CFR 438, 42 CFR 457) ↩︎

Costs associated with value-added services are included in the numerator of the MLR calculation (either as incurred claims or quality-related activities). ↩︎

If managed care plans implement SDOH activities that meet certain federal requirements (in 45 CFR § 158.150(b) and are not excluded under 45 CFR § 158.150(c)), managed care plans may include the costs associated with these activities in the numerator of the MLR as activities that improve health care quality (under 42 CFR § 438.8(e)(3)). ↩︎

When states provide case management services under the state plan without regard to “statewideness” and “comparability” requirements, the benefit is referred to as “targeted case management.” ↩︎

States can (and have) created more than one Health Home program to target different populations. ↩︎

For SUD health homes approved on or after October 1, 2018, states can receive ten quarters of enhanced federal match. ↩︎

Lauren M. Gottlieb, Holly Wing, and Nancy E. Adler, “A Systematic Review of Interventions on Patients’ Social and Economic Needs,” American Journal of Preventative Medicine 53 no. 5 (July 2017): 719-729, https://pubmed.ncbi.nlm.nih.gov/28688725/↩︎

La mayoría de los inmigrantes hispanos dicen que sus vidas son mejores en Estados Unidos, pero enfrentan desafíos financieros y de atención médica: Encuesta 2023 de KFF/LA Times sobre inmigrantes

Los inmigrantes hispanos conforman la mayor proporción de la población inmigrante en Estados Unidos, y alrededor de un tercio de los adultos hispanos o latinos en Estados Unidos son inmigrantes. Este informe ofrece una mirada en profundidad sobre las experiencias variadas de los inmigrantes hispanos que viven en Estados Unidos y destaca los desafíos únicos que enfrentan muchos de ellos, ya que los inmigrantes hispanos tienen más probabilidades que otros grupos de inmigrantes de tener un dominio limitado del inglés (LEP), no ser ciudadanos, tener ingresos familiares más bajos, no tener seguro médico y tener niveles de educación más bajos. Este informe detalla cómo estos factores afectan las experiencias de los inmigrantes hispanos, tanto en el trabajo como en sus comunidades, y en el acceso a la atención médica y a otros servicios.

A pesar de estos desafíos, este informe también destaca la resiliencia y optimismo de la población inmigrante hispana. Revela que, independientemente de su situación económica actual, la mayoría de los inmigrantes hispanos informan una mejor calidad de vida en Estados Unidos que en sus países de origen, y creen que las vidas de sus hijos serán mejores que las suyas.

La mayoría de los inmigrantes hispanos están trabajando, uno de cada cuatro informa ser autónomo o dueño de un pequeño negocio, y muchos apoyan financieramente a sus familias en sus países de origen incluso cuando sus propios ingresos son limitados.

Además, aunque muchos enfrentan desafíos, las circunstancias varían entre los inmigrantes hispanos: aquellos con mayores ingresos y con tarjeta de residencia (green card), visa válida o ciudadanía experimentan mejores resultados en muchos aspectos. Sin embargo, comparten algunas dificultades, independientemente de sus ingresos o estatus migratorio, como el trato injusto en el lugar de trabajo.

Una mejor comprensión de las experiencias de los inmigrantes hispanos no solo proporciona información sobre la diversidad de la población, también puede ayudar a enfocar iniciativas, políticas y recursos para abordar los desafíos que enfrentan.

Este informe se basa en la Encuesta de Inmigrantes, realizada por KFF en colaboración con Los Angeles Times durante la primavera de 2023, hasta la fecha la encuesta más grande y representativa de inmigrantes que viven en Estados Unidos. Con un tamaño de muestra de 3,358 adultos inmigrantes, incluidos 1,207 adultos inmigrantes hispanos, la encuesta proporciona una comprensión profunda de las experiencias de los inmigrantes, reflejando sus múltiples países de origen e historias, ciudadanía y estatus migratorio, identidades raciales y étnicas, y circunstancias sociales y económicas.

La mayoría de los inmigrantes hispanos en Estados Unidos son de México, han sido residentes en Estados Unidos por largo tiempo y están empleados; sin embargo, enfrentan importantes desafíos socioeconómicos. Los inmigrantes hispanos incluyen personas nacidas en México (53%), Centroamérica (17%), Sudamérica (16%) y proporciones más pequeñas de otras regiones y países. Tres de cada cuatro inmigrantes hispanos (77%) han estado en Estados Unidos durante 10 años o más y dos tercios (67%) están empleados, pero la mayoría vive en hogares de bajos ingresos (menos de $40,000 al año). Dos tercios de los inmigrantes hispanos tienen un dominio limitado del inglés (LEP, por sus siglas en inglés), y una proporción similar tiene educación secundaria o menor. La mayoría (56%) no son ciudadanos, incluido uno de cada cuatro que probablemente sean indocumentados.

Como los inmigrantes en general, la mayoría de los inmigrantes hispanos vinieron a Estados Unidos en busca de mejores oportunidades y la mayoría siente que están mejor como resultado de haber migrado, siendo especialmente los de Centroamérica los más propensos a citar la seguridad como un beneficio clave. Alrededor de ocho de cada 10 inmigrantes hispanos dicen que están mejor que sus propios padres, y dos tercios dicen que creen que las vidas de sus hijos serán aún mejores, con niveles particularmente altos de optimismo para el futuro de sus hijos entre los que no son ciudadanos y aquellos de Centroamérica.

La mayoría de los inmigrantes hispanos están empleados, pero muchos enfrentan un trato injusto en el lugar de trabajo, incluso aquellos que son ciudadanos, hablan inglés con fluidez y tienen al menos un título universitario. Dos tercios de los inmigrantes hispanos (67%) están trabajando, principalmente en trabajos por hora. A pesar de las altas tasas de empleo, la mayoría tiene ingresos anuales del hogar inferiores a $40,000, lo que lleva a enfrentar desafíos para cubrir necesidades básicas. Entre los inmigrantes hispanos que trabajan, al menos la mitad (55%) informa haber experimentado discriminación en el lugar de trabajo. Incluso entre aquellos que son ciudadanos (45%), hablan inglés con fluidez (41%) y tienen al menos un título universitario (52%), proporciones sustanciales indican que experimentan maltrato en el trabajo porque son inmigrantes.

Entre los dos tercios de inmigrantes hispanos que tienen dominio limitado del inglés (LEP), la mayoría informa enfrentar desafíos relacionados con el idioma. La mayoría (58%) de aquellos con LEP dice que la dificultad para hablar o entender inglés les ha dificultado el acceso a servicios clave o conseguir un trabajo. Los inmigrantes hispanos con LEP también informan tasas más altas de discriminación en el lugar de trabajo y dificultad para entender las leyes de inmigración de Estados Unidos en comparación con aquellos que hablan inglés con fluidez.

Proporciones sustanciales de inmigrantes hispanos, especialmente aquellos que probablemente sean indocumentados, dicen que no tienen suficiente información sobre las leyes y políticas de inmigración de Estados Unidos, se preocupan de que ellos o un familiar puedan ser detenidos o deportados, y tienen confusión sobre las reglas relacionadas con el uso de programas públicos que ayudan a pagar alimentos, vivienda o atención médica. Alrededor de ocho de cada 10 de los inmigrantes hispanos (79%), llegando a nueve de cada 10 entre aquellos que son indocumentados, no están seguros de si usar programas públicos que ayudan a pagar la atención médica, la vivienda o los alimentos puede disminuir las posibilidades de aprobación de la tarjeta de residencia, o creen incorrectamente que esto es así. Cuatro de cada 10 inmigrantes hispanos, incluidos tres cuartos de aquellos que probablemente sean indocumentados, se preocupan de que ellos o un familiar puedan ser detenidos o deportados.

Los inmigrantes hispanos, en especial aquellos que no tienen seguro médico, enfrentan muchos desafíos para acceder a atención médica. En general, uno de cada cuatro inmigrantes hispanos (26%) no tiene seguro médico, pero este porcentaje aumenta a más de la mitad (55%) entre aquellos que probablemente sean indocumentados, en comparación con el 26% de aquellos con una tarjeta de residencia o visa válida y con el 10% de los que son ciudadanos. Aunque la mayoría de los inmigrantes hispanos han buscado y recibido atención médica recientemente en Estados Unidos, aquellos que no tienen seguro son mucho menos propensos que los que tienen cobertura a buscar atención. Solo la mitad (50%) de los inmigrantes hispanos sin seguro han ido a una cita médica en el último año en comparación con más del 80% de aquellos con cobertura. Los inmigrantes hispanos sin seguro también son menos propensos que sus contrapartes con cobertura a tener una fuente habitual de atención y un proveedor de confianza, y son mucho más propensos a informar que han omitido o pospuesto la atención en el último año.

Los centros comunitarios de salud (CHC, por sus siglas en inglés) son el lugar predominante al que los inmigrantes hispanos suelen acudir cuando están enfermos o necesitan consejo médico. Los CHC facilitan el acceso a la atención para aquellos que no tienen seguro. En general, cuatro de cada 10 inmigrantes hispanos (41%) dicen que un CHC es su fuente habitual de atención, con proporciones sustanciales utilizando CHCs con diferentes tipos de seguros, estatus migratorio y dominio del inglés. Los CHCs son una red nacional de proveedores de atención primaria de seguridad social que atienden a comunidades de bajos ingresos y médicamente desatendidas.

While issues of health care costs and affordability may not be at the forefront of this year’s election issues, they remain a major concern among the public. About a quarter of Americans say they or a family member struggled to pay their medical bills just in the past year, and in recent KFF polling, voters said that health care affordability was very important to discuss in the election.

This new issue brief describes the health cost and affordability issues and trends that could reemerge this year, ranging from recent or proposed prescription drug pricing and transparency requirements to changes in how medical debt is treated on credit reports.

This brief is available through the Peterson-KFF Health System Tracker, an online information hub dedicated to monitoring and assessing the performance of the U.S. health system.

Note: Originally published on Jan. 11, 2024, this post was updated on Jan. 24, 2024, to include more recent data.

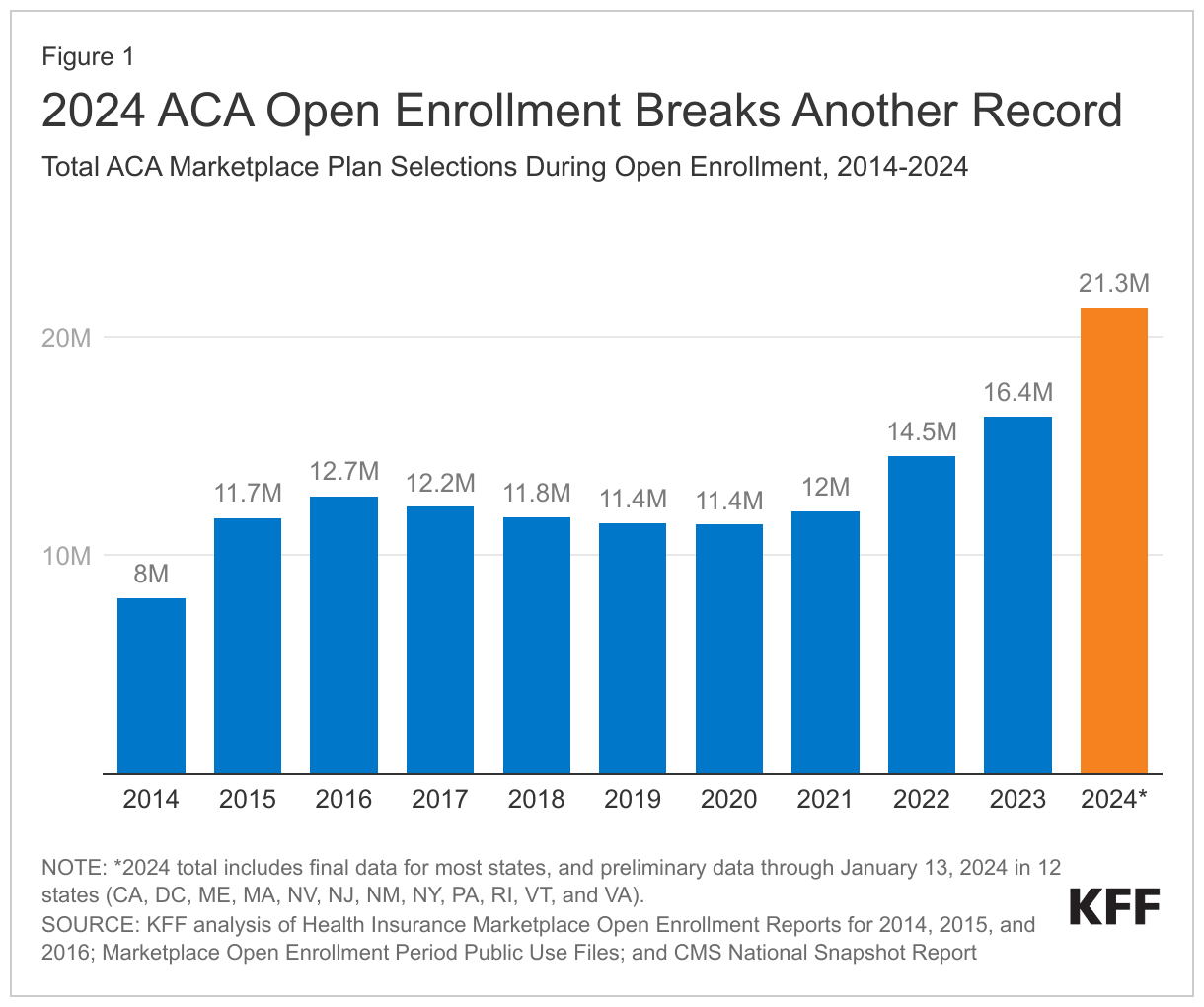

Open enrollment for the Affordable Care Act (ACA) Marketplaces has wrapped up in most states with another record high number of people signing up for coverage. The number of people with Marketplace coverage has grown significantly each year under the Biden Administration, with enhanced subsidies in the American Rescue Plan Act and the Inflation Reduction Act driving most of this growth and increased marketing, outreach, and enrollment assistance also playing a role.

The latest data show that Marketplace signups have reached 21.3 million people, exceeding last year’s record high by another 5 million people. These signup data are not quite final because a few states have ongoing enrollment periods, so the total number of signups will likely inch up. (These signup figures are as of the end of open enrollment for HealthCare.gov and some State-Based Marketplaces, and are preliminary through January 13, 2024 for other State-Based Marketplaces.)

From 2023 to 2024, Marketplace signups grew by 30% or 5 million more people. Three states (Texas, Florida, and Georgia) account for half of the national growth in Marketplace enrollment this year. The five states with the highest percent increase in signups since last year are West Virginia (80%), Louisiana (76%), Ohio (62%), Indiana (60%), and Tennessee (59%). For more state data, see Table 1 below.

Drivers of ACA Marketplace Growth from 2023 to 2024

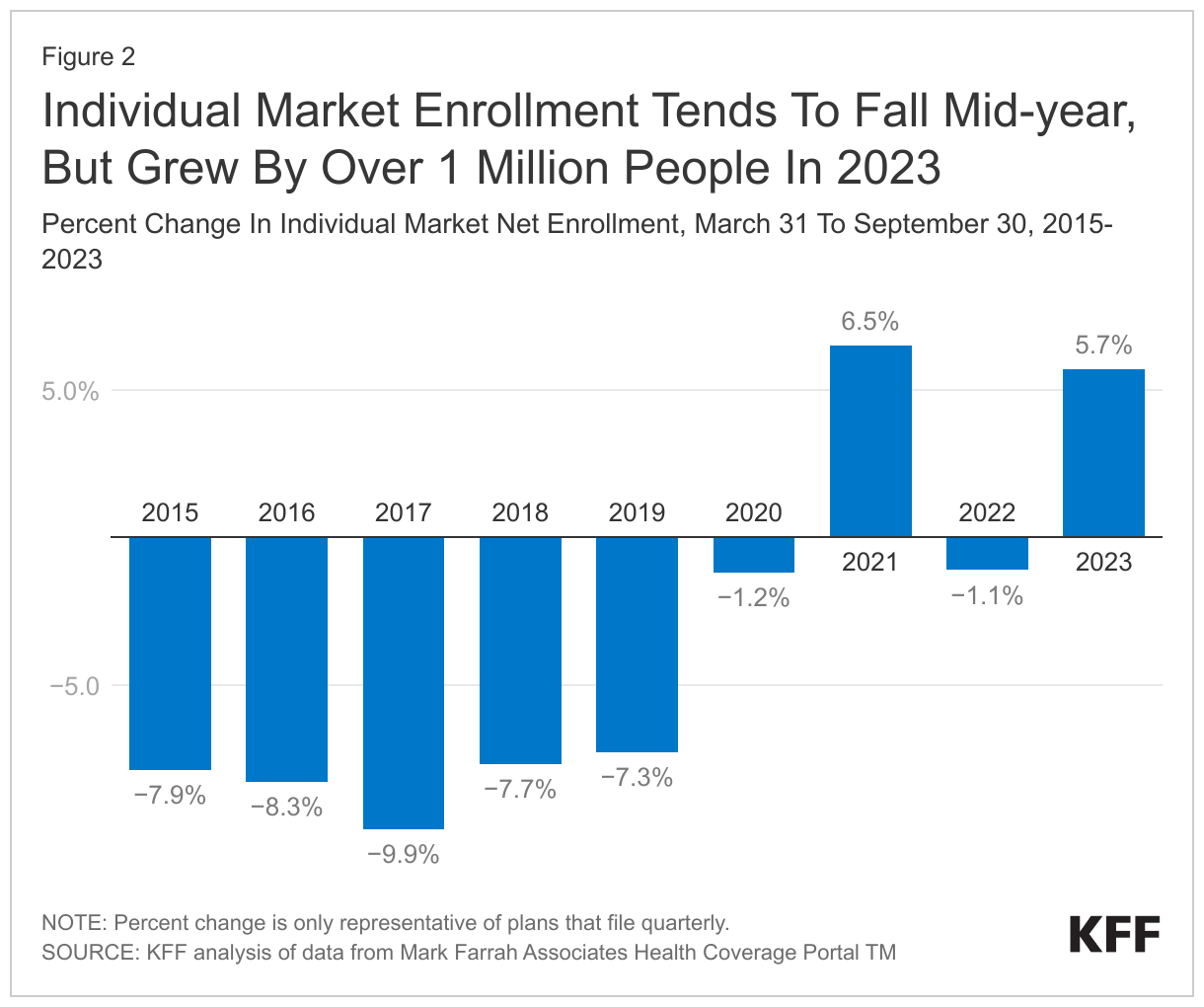

While enhanced subsidies have driven most of the enrollment growth since 2020, Medicaid unwinding is likely also contributing to 2023 to 2024 changes. KFF’s analysis shows that individual market enrollment was already elevated by at least 1 million people before open enrollment began. Some people losing Medicaid coverage made their way onto the ACA Marketplace mid-year 2023, while others may have waited for open enrollment to make the transition.

During most of the COVID-19 pandemic, states had been prohibited from disenrolling people from Medicaid, but these disenrollments started again in April 2023. Since then, while millions of people have been able to renew their Medicaid coverage, more than 15 million have been disenrolled. In some cases, people have been disenrolled because they were determined ineligible for the program, but others have been disenrolled for procedural reasons, meaning they were unable to complete the renewal process, and may still be eligible. Some of those losing Medicaid coverage have been able to reenroll in Medicaid, while others have moved to employer-based coverage or to the Children’s Health Insurance Program (CHIP); however, others have become uninsured. For those who are not eligible for Medicaid, CHIP, or affordable employer coverage, the Marketplace offers subsidies to make private coverage more affordable.

Unlike most previous years, the individual market grew mid-year, outside of the open enrollment window. From early April 2023 to the end of September 2023, before the 2024 open enrollment had begun, enrollment in the individual market (which includes the ACA Marketplaces, as well as off-exchange plans, many of which are also ACA-compliant), grew by 5.7%. This is approximately equivalent to a growth of just over 1 million individual market enrollees mid-year in 2023.

This mid-year growth in individual market enrollment is very unusual; in most recent years, there has been attrition from the market. The individual market is often a place where people come for insurance coverage when they are between other sources of coverage (for example, when they are between jobs or in school). As people leave mid-year, either for other sources of coverage or because they no longer find their Marketplace plan to be affordable, the number of people leaving usually exceeds the number of people coming into the market because there are only limited opportunities for other people to qualify for special enrollment opportunities and it can be burdensome to demonstrate eligibility to signup mid-year. Therefore, individual market enrollment tends to wane in the later part of the year. The only other time this market has seen mid-year growth in recent years was in 2021, when the enhanced subsidies in the American Rescue Plan Act were first rolled out and the Biden Administration and most state-based Marketplaces allowed broad opportunities for mid-year enrollment.

Additionally, the Biden Administration closed the family glitch starting in 2023, so some dependents of people getting employer-based care may be finding a better deal on the Marketplaces than the coverage offered through their family member’s employer.

The enhanced subsidies in the Inflation Reduction Act are also a factor, as enrollment has grown substantially each year since they first became available. People are continuing to find out about the extra premium subsidies through additional outreach, as federal marketing budgets and funding for navigators and in-person assisters have increased under the Biden Administration following substantial reductions under the Trump Administration. The enhanced subsidies make the transition from Medicaid to private coverage easier cost-wise, as zero-premium plans with enhanced subsidies are available for many low-income people, particularly in states that did not expand Medicaid. In addition to drawing new enrollees to the ACA Marketplaces, these enhanced subsidies may also be helping existing enrollees afford to maintain their coverage. In 2022, as shown in Figure 2, there was much less mid-year attrition than had been the case pre-pandemic.

The number of people signing up for ACA Marketplace coverage has grown so rapidly in the past 4 years that 2024 signup numbers are almost double the number of people that signed up in 2020. The enhanced subsidies in the Inflation Reduction Act have helped to make ACA Marketplace coverage more affordable for those transitioning off Medicaid. The enhanced subsidies will last through the end of 2025, at which point Congress must decide whether to let them expire or extend them further, requiring additional funding.

Methods

Enrollment data is sourced from Health Coverage PortalTM, a market database maintained by Mark Farrah Associates Plans. A relatively small number of plans that only file annually (not quarterly) are excluded from this analysis. Insurers that did not file third quarter 2023 data with the NAIC as of December 4, 2023 are excluded from all quarters. We also remove likely Children’s Health Insurance Program, or CHIP, enrollees from the individual market total by using A&H Policy Experience Exhibit data.

While issues of health care costs and affordability may not be at the forefront of this year’s election issues, they remain a major concern among the public. About a quarter of Americans say they or a family member struggled to pay their medical bills just in the past year, and in recent KFF polling, voters said that health care affordability was very important to discuss in the election.KFF’s new brief describes the health cost and affordability issues and trends that could reemerge this year, ranging from recent or proposed prescription drug pricing and transparency requirements to changes in how medical debt is treated on credit reports. In connection to these and other health cost and affordability challenges, key issues and trends to watch in 2024 include:

1. Site-neutral payment reforms2. Price transparency requirements and what they could mean for costs3. Prescription drug pricing policies and the implications for spending and affordability4. Policy changes that could affect PBMs, the so-called prescription drug middlemen 5. New drugs and therapies that could influence health spending and outcomes 6. What virtual care expansion means for costs, access, and affordability 7. State cost control measures and spending8. Recent surprise billing protections and their effects on private insurance premiums 9. Policies addressing out-of-pocket health costs and consumer medical debt10. Shifts to value-based payment and the impact on health care costs11. Antitrust agencies’ efforts to address consolidation in healthcare markets

Drew Altman, KFF’s President and CEO, recently examined how health care costs and affordability are the two health care crises facing the U.S. Read his column.