Medicare supplement insurance, known as Medigap, helps cover Medicare Part A and Part B cost-sharing requirements, including deductibles, copayments, and coinsurance. Medigap policies, which are sold by private insurance companies, are a key source of supplemental coverage for people in traditional Medicare without employer-sponsored retiree benefits or Medicaid (Medigap does not work with Medicare Advantage). In 2022, 12.5 million Medicare beneficiaries, or 42% of all traditional Medicare beneficiaries, had a Medigap policy. However, federal requirements that prohibit the use of medical underwriting by insurers when issuing Medigap policies – known as guaranteed issue protections – are limited, which means it may be hard or impossible for people with pre-existing conditions, like asthma or cancer, to get a Medigap policy, outside of specified time periods. (For more information on the basics of Medigap, see Key Facts About Medigap Enrollment and Premiums for Medicare Beneficiaries).

Federal law requires Medigap insurers to issue Medigap policies without medical underwriting during a one-time, six-month Medigap open enrollment period for beneficiaries ages 65 and older when first enrolling in Medicare Part B, and for certain qualifying events, such as during a Medicare Advantage trial period. But federal law allows Medigap insurers to use medical underwriting to either deny Medicare beneficiaries a policy or charge higher premiums outside of guaranteed issue periods. Federal law also does not require Medigap insurers to issue Medigap policies to people who choose to disenroll from a Medicare Advantage plan, except under limited circumstances, or to beneficiaries under age 65 who qualify for Medicare due to a long-term disability. Some lawmakers have proposed to strengthen federal guaranteed issue protections for the Medigap market, though doing so could impact premiums.

This issue brief analyzes federal and state guaranteed issue rules and how they impact beneficiaries’ access to Medigap, including the implications for Medicare beneficiaries with pre-existing conditions and those under age 65 with long-term disabilities. This brief also explores a recently finalized rule: Nondiscrimination in Health Programs and Activities regarding Section 1557 of the Affordable Care Act that may have implications for the Medigap market. This analysis is based on KFF review and collection of federal and state insurance regulations, insurers’ Medigap applications, other publicly available information, and KFF analysis of data from the Centers for Medicare & Medicaid Services (CMS) Chronic Conditions Data Warehouse Master Beneficiary Summary File (MBSF), 2022.

Key Takeaways

- Federal law provides some guaranteed issue protections for Medicare beneficiaries who seek to purchase a Medigap policy, such as during the first six months after signing up for Medicare Part B or if their Medicare Advantage plan terminates coverage in their area. However, in all but four states, beneficiaries may be denied a Medigap policy if they have a pre-existing condition if they choose to switch from Medicare Advantage to traditional Medicare outside the initial trial period or seek to purchase a Medigap policy years after enrolling in Medicare.

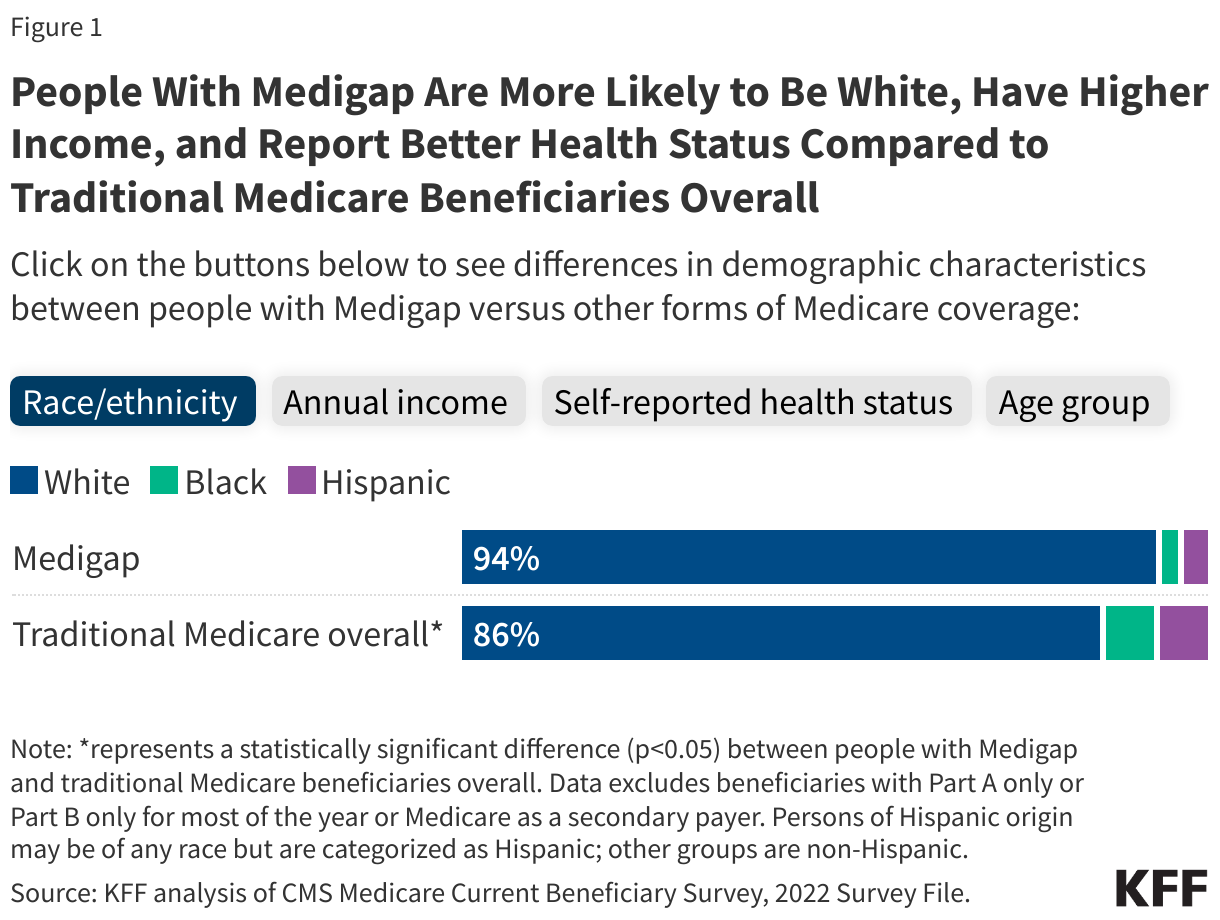

- Nine out of ten (90%) Medicare Advantage enrollees ages 65 and older, or 22.4 million people, do not have guaranteed issue protections to purchase Medigap beyond the initial Medicare Advantage trial period, as of 2022.

- The list of potentially deniable medical conditions includes Alzheimer’s disease, asthma, cancer, congestive heart disease, diabetes with complications, end-stage renal disease (ESRD), high blood pressure, limitations of daily activities, stroke and other conditions, based on KFF’s review of Medigap applications of leading insurers. Applicants may also be charged higher Medigap premiums if they have conditions such as diabetes with no complications, bipolar disorder, or osteoporosis that is treated with infusion. The Affordable Care Act prohibits insurance companies from denying coverage or charging higher premiums based on pre-existing conditions, but does not apply to Medigap insurers.

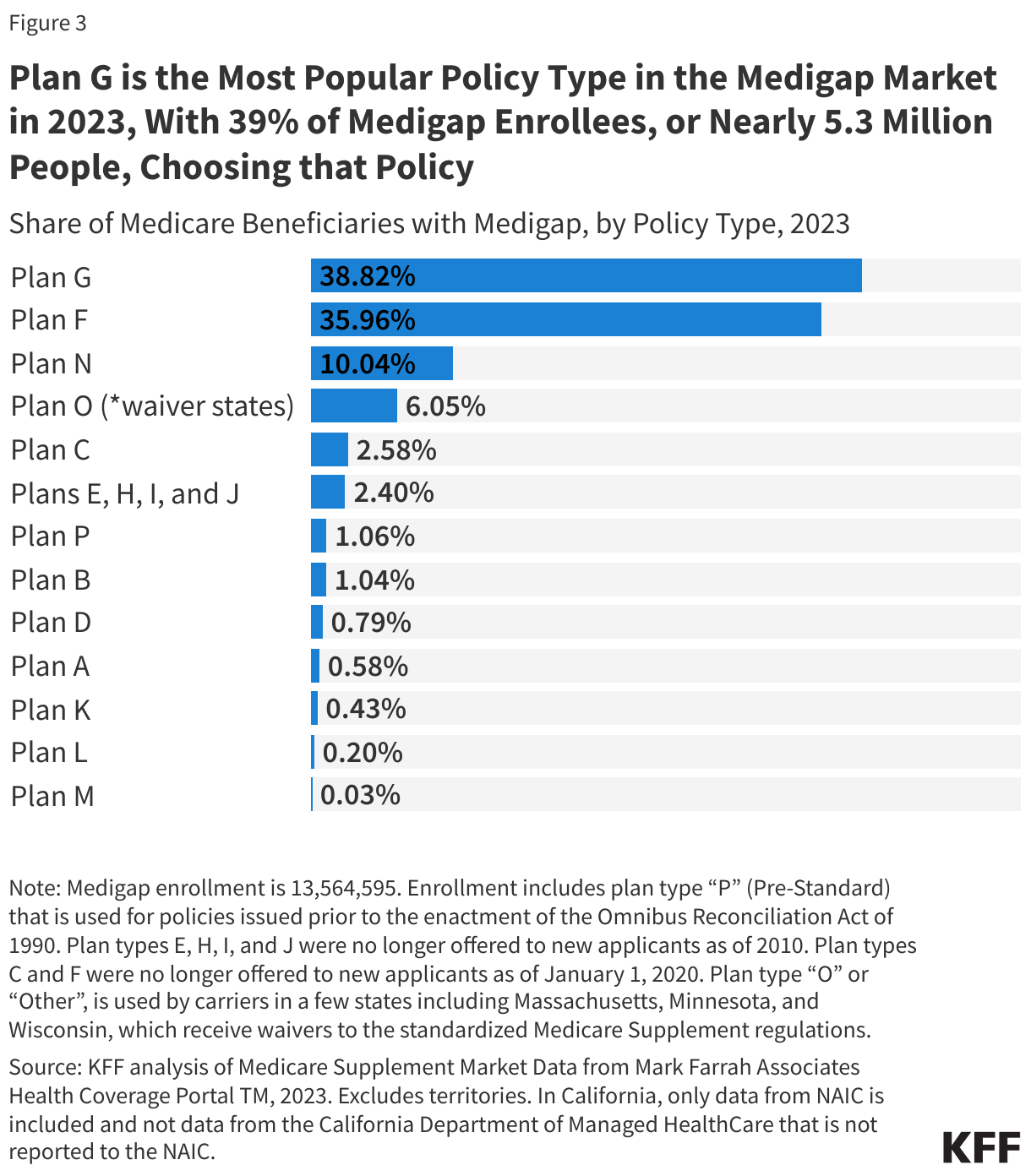

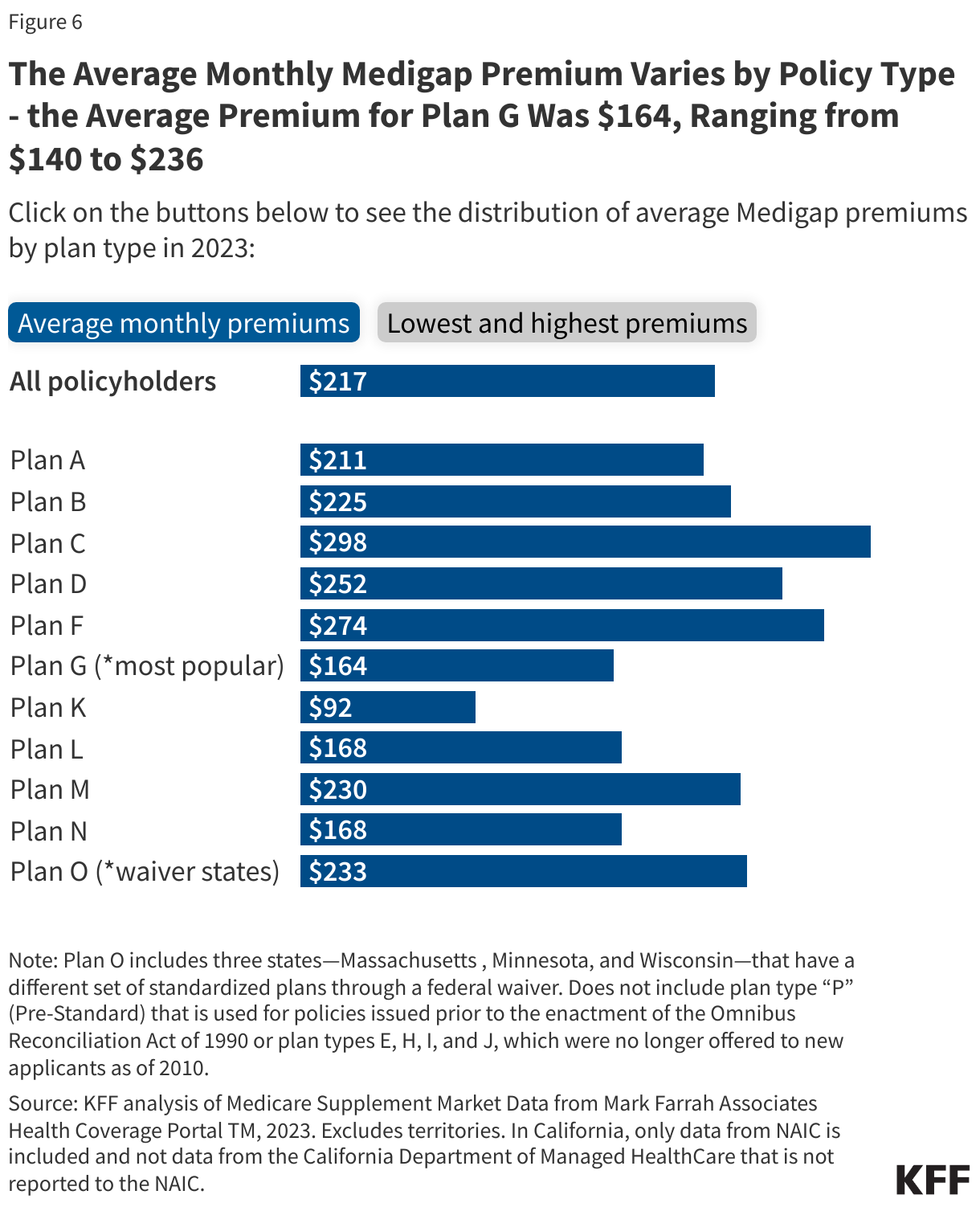

- Four states (CT, MA, ME, NY) require either continuous or annual guaranteed issue protections for Medigap for all beneficiaries ages 65 and older, regardless of medical history. With continuous enrollment, insurers are required to issue Medigap policies at any time during the year in Connecticut, Massachusetts and New York; in Maine, which has a one-month guaranteed issue period each year, insurers are required to offer only Medigap Plan A, which is less comprehensive than some Medigap plans, such as Plan G – the most popular policy in 2023. Minnesota enacted legislation to institute annual guaranteed issue protections, which are slated to go into effect on August 1, 2025, though there are indications that implementation may be delayed.

- Thirty-five states require Medigap insurers to issue policies to Medicare beneficiaries ages 65 and older due to certain qualifying events, such as when an applicant has a change in their employer (retiree) coverage (29 states) or when beneficiaries lose their Medicaid eligibility (10 states).

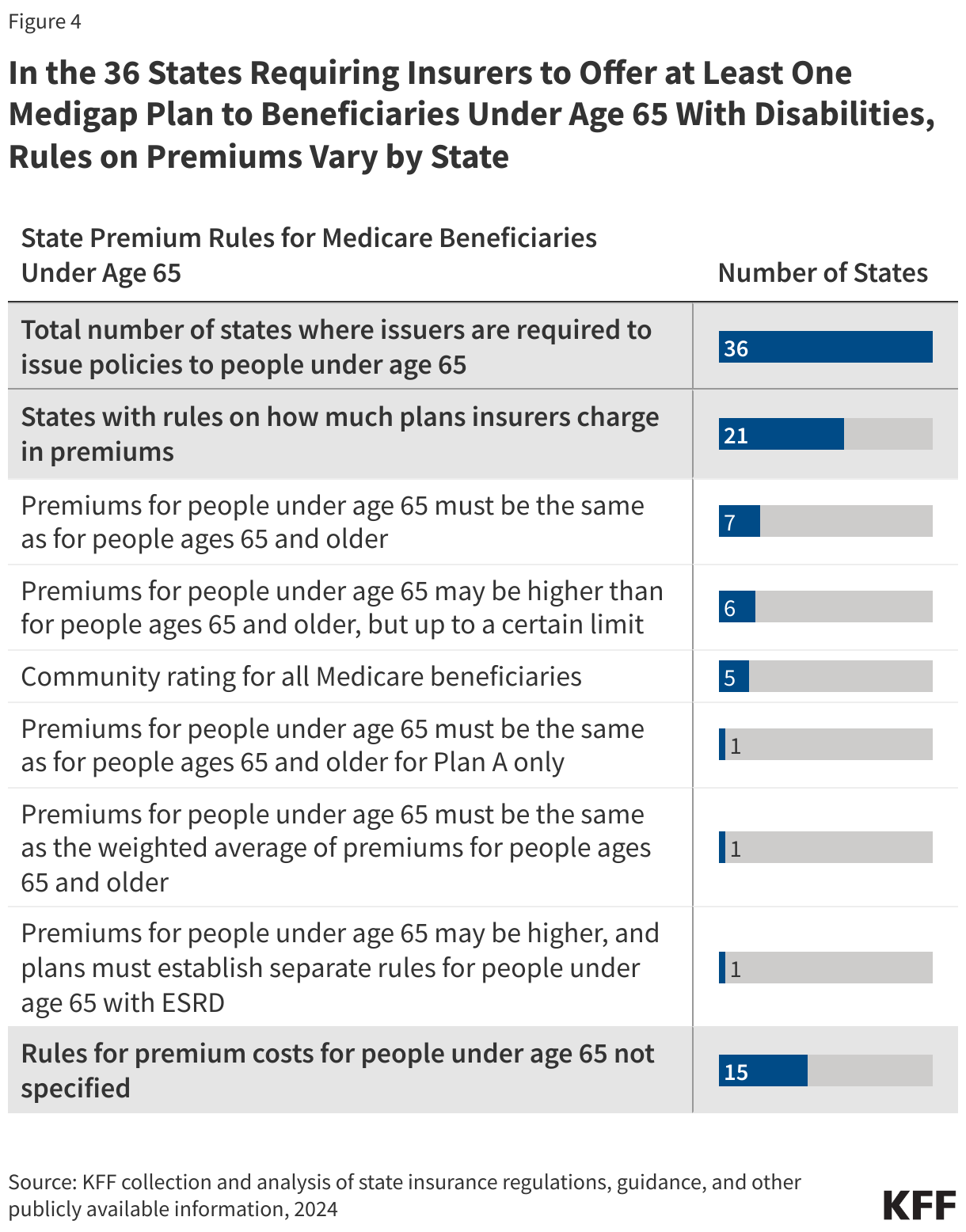

- Thirty-six states require insurance companies to offer at least one kind of Medigap policy to Medicare beneficiaries under age 65 with disabilities during an initial open enrollment period, regardless of medical conditions.

The Role of Federal Law in Regulating Medical Underwriting in the Medigap Market

In general, Medigap insurance is state regulated, but also subject to certain federal minimum requirements. Medigap was first federally regulated through the Social Security Disability Amendments, also referred to as the “Baucus Amendments,” in 1980, followed by a second key set of federal regulations that were enacted as part of the Omnibus Budget Reconciliation Act of 1990 (OBRA-90). That law required:

- The institution of a six-month open enrollment period beginning the first month a beneficiary is enrolled in Medicare Part B, for beneficiaries ages 65 and older

- A standardized set of benefits across Medigap policies, leading to 10 standard Medigap policies available to beneficiaries. (Three states – Massachusetts, Minnesota, and Wisconsin – have a different set of standardized policies.)

- Guaranteed plan renewability (with few exceptions)

- Minimum medical loss ratio requirements

- Limiting the exclusion period for pre-existing conditions to six months.

The Medicare Access and CHIP Reauthorization Act of 2015 (MACRA) made some additional changes to the Medigap market, prohibiting insurers from issuing new policies that cover the full Part B deductible, making Plans C and F no longer available to beneficiaries who turned age 65 on or after January 1, 2020.

Pursuant to the requirements mentioned above, federal law provides guaranteed issue protections for Medigap policies during a one-time, six-month Medigap open enrollment period for beneficiaries ages 65 and older, which begins the first month of Medicare Part B coverage, and for certain qualifying events (Table 1). During these defined periods, Medigap insurers cannot deny a Medigap policy to any qualifying applicant based on factors such as age, gender, or health status, nor can they vary premiums based on an applicant’s pre-existing medical conditions or exclude coverage for a pre-existing medical condition (i.e., medical underwriting).

The one-time, six-month guaranteed issue period is intended to mitigate potential selection issues in the Medigap market. Rather than waiting until they incur high health care costs before purchasing a Medigap policy, beneficiaries must generally purchase a policy during the initial open enrollment period or risk not being able to purchase a Medigap policy later. This also has the effect of ensuring that the risk pool includes a mix of both healthier and sicker enrollees, which could keep premiums lower, on average. However, as discussed in more detail below, the one-time open enrollment period also has the effect of locking people out of the Medigap market who might not be at higher risk of incurring high medical expenses in the short term. This could include, for example, a beneficiary who has been enrolled in a Medicare Advantage plan for a few years and wants to switch to traditional Medicare because of network restrictions in Medicare Advantage, but faces medical underwriting based on having pre-existing conditions.

Under federal law, Medigap insurers may impose a waiting period of up to six months to cover services related to pre-existing conditions if the applicant did not have at least six months of prior continuous creditable coverage. For qualifying events that have guaranteed issue rights, people ages 65 and older in Medicare generally have 63 days to apply for a Medigap policy.

Beneficiaries with Traditional Medicare and Employer Retiree Coverage: Medicare beneficiaries have federally qualified guaranteed issue rights to purchase Medigap if their employer cancels their retiree coverage. However, they do not have guaranteed issue rights to purchase Medigap if their retiree coverage changes or if they voluntarily drop retiree coverage.

Beneficiaries with Traditional Medicare and Medigap: Federal law requires that a trial period applies to Medicare beneficiaries in traditional Medicare who cancel their Medigap policy when they enroll in a Medicare Advantage plan (this is not limited to just the first year of enrolling in Medicare). These beneficiaries have time-limited guaranteed issue rights to purchase their same Medigap policy if, within a year of first signing up for a Medicare Advantage plan, they decide to disenroll to return to traditional Medicare. Guaranteed issue rights also apply if their Medigap insurance company goes bankrupt or Medigap coverage ends through no fault of their own, or their Medigap insurance company commits fraud.

Beneficiaries who currently have Medigap do not have federal guaranteed issue protections to switch Medigap policies. They also do not have guaranteed issue protections if they voluntarily drop Medigap and wish to purchase a policy again later. However, beneficiaries may suspend Medigap for up to two years if they become eligible for Medicaid, in which case they have no new medical underwriting or waiting periods for pre-existing conditions when they restart their Medigap.

Beneficiaries with Medicare and Medicaid: Medicare beneficiaries who are dually-eligible individuals, meaning they have both Medicare and Medicaid have premium and cost-sharing protections through Medicaid. Therefore, they typically do not need Medigap protections and in general, Medigap insurers cannot sell Medigap policies to people with Medicaid. If dual-eligible individuals lose their Medicaid eligibility, they are not entitled to a guaranteed issue period to purchase Medigap. However, as noted above, this is not the case for beneficiaries who had Medigap before becoming eligible for Medicaid, in which case they have no new medical underwriting or waiting periods for pre-existing conditions when they restart their Medigap (as long as they did not have Medicaid for more than two years).

Beneficiaries Under Age 65: The federally guaranteed one-time, six-month Medigap open enrollment period does not extend to beneficiaries who qualify for Medicare under age 65. However, when these beneficiaries turn age 65, federal law requires that they are entitled to the same time-limited six-month open enrollment period for Medigap that is available to new beneficiaries ages 65 and older. As discussed below, many states have rules in place that go beyond minimum federal requirements and require insurance companies to offer at least one kind of Medigap policy to Medicare beneficiaries under age 65 with disabilities during an initial open enrollment period, regardless of medical conditions.

Beneficiaries with Medicare Advantage. Medicare Advantage enrollees with pre-existing conditions have limited opportunities to buy Medigap policies if they want to switch to traditional Medicare. Federal law requires that Medigap policies be sold with guaranteed issue rights during a specified trial period for Medicare Advantage plans. This trial period is during the first year adults ages 65 and older enroll in Medicare. During that time, older adults can try a Medicare Advantage plan, but if they disenroll within the first year, they have guaranteed issue rights to purchase any Medigap policy that is sold in their state.

Medicare Advantage enrollees also have guaranteed issue rights to purchase a Medigap policy to supplement coverage under traditional Medicare if:

- their Medicare Advantage plan discontinues coverage in their area

- they move to a new area and can no longer access coverage from their Medicare Advantage plan

- their Medicare Advantage plan is terminated

- their Medicare Advantage plan commits fraud.

Outside of the trial period and other limited circumstances, Medicare Advantage enrollees who disenroll and obtain coverage under traditional Medicare can be denied a Medigap policy if they have a pre-existing condition. This includes Medicare Advantage enrollees who voluntarily leave a retiree health plan through Medicare Advantage and who seek to purchase a Medigap policy. In the majority of states that allow medical underwriting for Medigap, Medicare Advantage enrollees with pre-existing conditions may be reluctant to switch to traditional Medicare if they are unable to purchase a Medigap policy. This is because Medigap provides added financial protection as a supplement to traditional Medicare, which does not have an out-of-pocket cap for services covered under Medicare Parts A and B, unlike most health insurance plans. In contrast, Medicare Advantage plans are required to have an out-of-pocket limit for Parts A and B.

Nine out of ten (90%) Medicare Advantage enrollees ages 65 and older, or 22.4 million people, are subject to medical underwriting and may be denied coverage if they apply for a Medigap policy outside of the Medicare Advantage trial period or other specific guaranteed issue periods, as of 2022 (Figure 1; Appendix Table 1; see below for state-specific information on guaranteed issue rules).

The vast majority of Medicare Advantage enrollees do not live in one of the four states with rules in place that require continuous or annual rights to purchase a Medigap policy if they choose coverage under traditional Medicare. Only 10% of Medicare Advantage enrollees ages 65 and older live in these four states, which require insurers to issue Medigap policies without regard to pre-existing conditions, even after their Medicare Advantage trial period ends. (For more detail on the 4 states, see section below: Only Four States Require Continuous or Annual Guaranteed Issue Protections for Medigap for People Ages 65 and Older.)

The total number of Medicare Advantage enrollees who may not be able to switch to traditional Medicare and a purchase a Medigap policy would be even higher if Medicare Advantage enrollees under age 65, who also do not have guaranteed issue protections, were included.

Medigap Insurers Can Deny Coverage Based on Pre-Existing Conditions, Except Under Limited Circumstances

Under current federal law, insurance companies that sell Medigap policies may refuse to sell a policy to an applicant with certain medical conditions, or who has had certain medical procedures or used specific prescription drugs, outside of open enrollment or a guaranteed issue period. This contrasts with other insurance products, like plans sold in the ACA Marketplace or Medicare Advantage, which are not permitted to deny coverage based on pre-existing conditions at any time.

Based on a KFF review of 15 Medigap policy applications from 12 major Medigap insurers, several medical conditions and prescription drugs are listed as possible reasons for medical underwriting or coverage denial (Table 2):

- Medical conditions: Medical conditions that are listed by Medigap insurers as reasons for a potential denial on the application include but are not limited to: Alzheimer’s disease, asthma that requires use of inhalers, cancer, congestive heart failure, diabetes with complications (e.g., neuropathy), ESRD, high blood pressure, and stroke (Table 2). Insurers also deny applicants who have undergone certain related procedures, such as a bone marrow, stem cell, or organ transplant or implant of a pacemaker. Many of these conditions are prevalent among Medicare beneficiaries. For example, about two-thirds (67%) of people on Medicare have hypertension, more than a quarter (26%) have diabetes, 19% have chronic kidney disease, 12% have been diagnosed with heart failure, and 10% have had prostate cancer.

- Functional status: Several applications list indicators of functional status as a potential reason for denial, including having any difficulty performing activities of daily living, being dependent on a wheelchair or motorized device, or being confined to the home.

- Medications: Underwriting guidelines include long lists of medications that will lead to a potential denial. These medications include insulin greater than 50 units per day to treat diabetes, Zestril for high blood pressure, Revlimid for cancer, Remicade for rheumatoid arthritis, and Lasix for heart disease. For example, one application states, “if the application has taken one or more of the following [medications] within the past 12 months, do not submit the application.”

- Medical advice: Some applications cite medical advice that has not been addressed as reason for denial. For example, one application asks, “within the past 12 months, have you been advised by a medical professional to have treatment, further evaluation, diagnostic testing, or surgery that has not been performed or do you have pending test results?”

- Medical service use: Utilization of home health services, rehabilitation services, inpatient hospitalization within a specific time frame (e.g., three or more times within the past two years), or confinement to a nursing facility are also listed as reasons for a declined application.

Several Medigap applications instruct individuals not to submit applications if they have any of the listed pre-existing conditions. For example, one application states, “if the answer to any question…is yes, the application should not be submitted.” Another specifies that “if you answer YES to any [health] question, you are not eligible for coverage.”

A few applications list conditions that will result in higher Medigap premiums but may not result in someone being denied a policy. Examples of these conditions include diabetes with no complications or that requires 50 or less units of insulin, hemophilia, macular degeneration that does not require injections, bipolar disorder or schizophrenia, and osteoporosis that is treated with infusion.

Only Four States Require Continuous or Annual Guaranteed Issue Protections for Medigap for People Ages 65 and Older

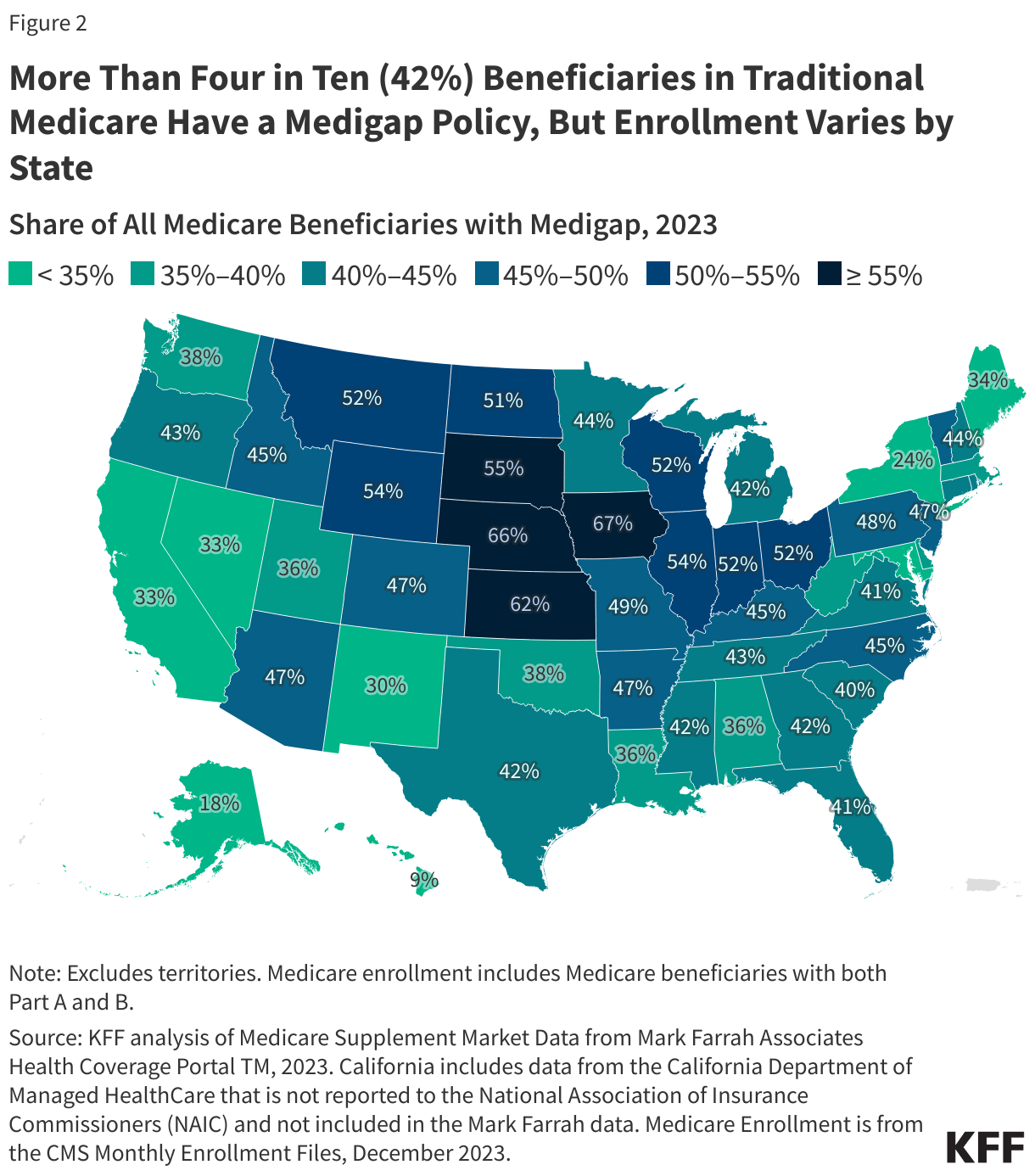

States can establish Medigap consumer protections that go further than the minimum federal standards. Only four states – Connecticut, Massachusetts, Maine, and New York – require Medigap insurers to offer policies either continuously throughout the year or once per year to Medicare beneficiaries ages 65 and older without regard to their medical conditions, consistent with prior KFF analysis (Figure 2; Appendix Table 2).

Two of these states – Connecticut and New York – have continuous open enrollment, with guaranteed issue rights throughout the year. Massachusetts regulation requires an annual guaranteed issue open enrollment period from February 1st to March 31st, but all insurers in Massachusetts offer continuous open enrollment throughout the year. Maine requires insurers to issue Medigap Plan A during an annual one-month open enrollment period of the insurer’s choosing.

Minnesota has enacted legislation that includes the institution of two guaranteed issue open enrollment periods (one during the annual Medicare open enrollment period from October 15 to December 7 and one during the Medicare Advantage open enrollment period, from January 1 to March 31), which require insurers to issue Medigap policies during these time frames without medical underwriting. Institutionalized individuals can purchase Medigap on a continual basis, with guaranteed issue rights throughout the year. These new rules are slated to go into effect on August 1, 2025, though there are indications that implementation may be delayed.

Consistent with federal law, Medigap insurers in New York, Connecticut, and Maine may impose up to a six-month “waiting period” to cover services related to pre-existing conditions if the applicant did not have six months of continuous creditable coverage prior to purchasing a policy during the initial Medigap open enrollment period. Massachusetts prohibits pre-existing condition waiting periods for its Medicare supplement policies.

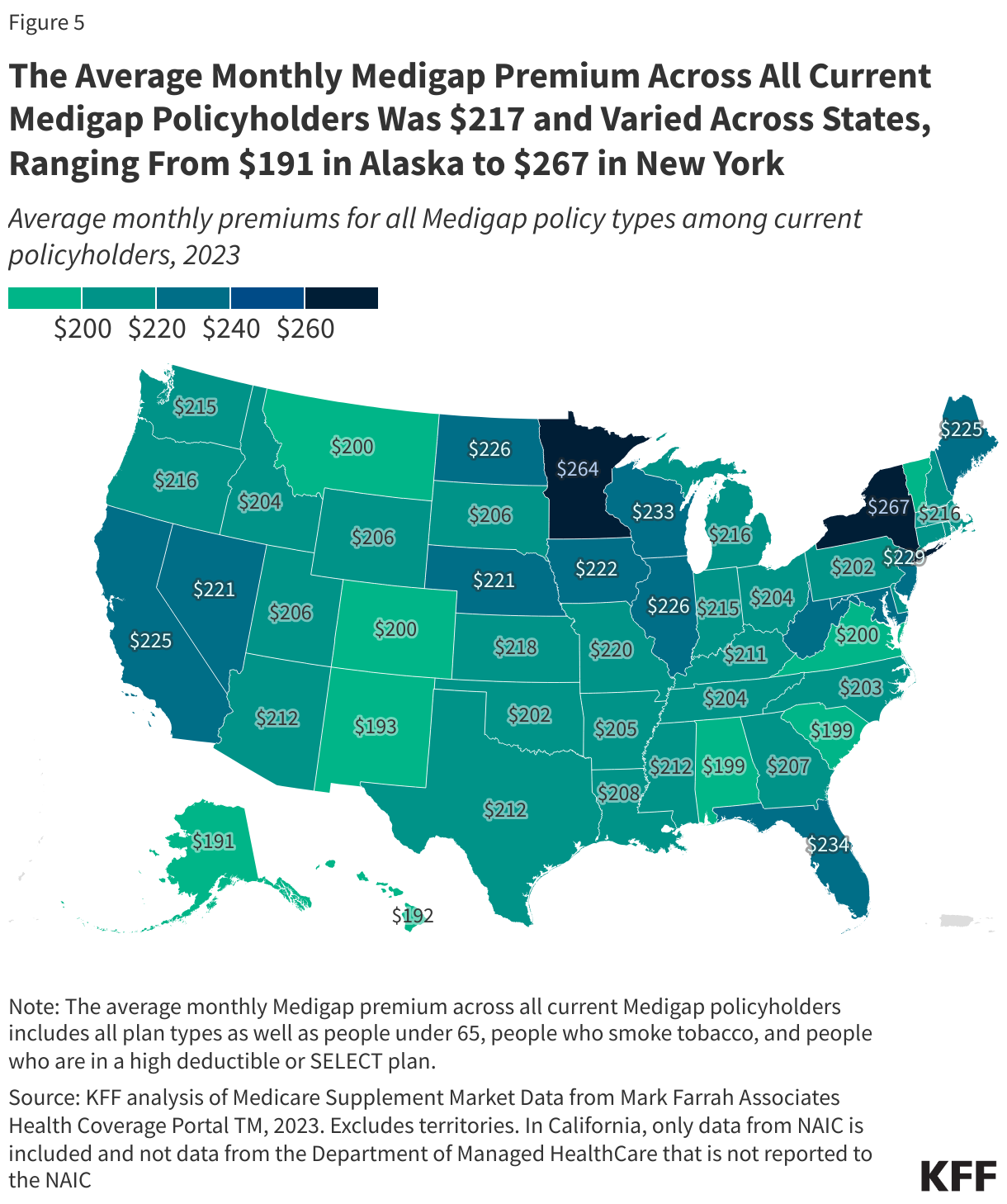

States establish certain rules for Medigap insurers, including how to set premiums, and premiums may be based on factors such as a policyholder’s age, smoking status, gender, residential area, and rating system, even during open enrollment and guaranteed issue periods. Premiums can also vary across states due to states’ guaranteed issue requirements, the characteristics of the Medicare population, the number of Medicare beneficiaries, Medicare Advantage penetration, urbanicity of the county, and health care cost and usage patterns. Due to the variety of factors at play, KFF analysis shows that there is not a clear relationship between states with continuous or annual guaranteed issue protections and having consistently higher premiums for Medigap than in other states. However, for Plan G, the states with the three highest average premiums do have more robust guaranteed issue protections. Further, Minnesota recently commissioned a study on the impact of instituting annual guaranteed issue protections and estimated that average annual premiums across all Minnesota Medigap plans would be 6% higher during the first year of implementation, with enrollment in Medigap expected to be 32% higher than if these changes were not in effect.

Thirty-Five States Require Medigap Insurers to Issue Medigap Policies to Beneficiaries Ages 65 and Older Due to Certain Qualifying Events

An additional thirty-three states (as well as Maine and Minnesota since they only have annual guaranteed issue protections) require Medigap insurers to offer policies to eligible applicants ages 65 and older based on certain qualifying events beyond the minimum federal standards (Figure 3, Appendix Table 2):

- Twenty-nine states require Medigap insurers to issue policies when an applicant has an change in their employer (retiree) coverage, such as a reduction in benefits or an increase in costs, depending on the state. This qualifying event is more expansive than federal law, which applies only when retiree coverage is completely eliminated.

- Ten states require Medigap insurers to issue policies if Medicare beneficiaries lose their Medicaid eligibility. Medicare beneficiaries who are dually-eligible individuals would no longer have premium and cost-sharing protections through Medicaid if they lose their Medicaid coverage.

- Twelve states have guaranteed issues rules for other types of qualifying events. For example, Maine extends the federally-required Medicare Advantage trial period from one year to three years. California allows Medicare Advantage enrollees to purchase a Medigap policy from the same Medicare Advantage insurer they are enrolled in (if it sells one) if their Medicare Advantage plan reduced any of its benefits, increased cost sharing, or terminated a contract with a provider currently treating them. If a Medigap policy is not available from their current Medicare Advantage insurer, they can purchase a Medigap policy from a different company if their Medicare Advantage plan increased premiums or copayments by 15% or more, reduced benefits, or terminated a contract with a provider currently treating them.

Additionally, some states have a guaranteed issue period for individuals who missed their 6-month Medigap enrollment period because they were enrolled in Medicaid during the COVID-19 public health emergency (PHE). These individuals were not terminated from Medicaid when they became eligible for Medicare Part B because of the continuous enrollment policy during the PHE, but were later terminated from Medicaid following the end of the PHE.

Some of these states provide guaranteed issue protections for current Medigap policyholders who want to switch policies (Figure 3, Appendix Table 2):

- Nine states have what are called “birthday rules” (CA, ID, IL, KY, LA, MD, NV, OK and OR), which require Medigap insurers to allow current policyholders switch each year to a different Medigap policy with equal or lesser benefits from either the same or different insurance carrier, depending on the state, around the time of their birthday. Depending on the state, these Medigap policyholders have between 30 and 63 days to switch policies. (This allowance does not enable beneficiaries who do not already have Medigap to newly purchase a Medigap policy.)

- Missouri requires Medigap insurers to allow current Medigap policyholders to switch to an equivalent policy from a different insurer within 30 days before or after the annual anniversary date of their policy.

- Maine requires Medigap insurers to allow current Medigap policyholders to switch to a policy with equal or less generous benefits at any time during the year if there is less than a 90-day gap in coverage.

- Washington requires Medigap insurers to allow Medigap policyholders to switch to a policy with equal or less generous benefits at any time during the year if there is less than a 90-day gap in coverage, though policyholders with Medigap Plan A are limited to switching to another Plan A, while those with Plans B through N can switch to any other Plan B through N.

Access to Medigap Is More Limited for Medicare Beneficiaries Under Age 65 with Disabilities

Under federal law, Medigap insurers are not required to sell Medigap policies to the over 7 million Medicare beneficiaries who are under age 65, a majority of whom qualify for Medicare based on having a long-term disability and receiving Social Security disability benefits (a small number qualify due to having ESRD or ALS). Higher rates of Medicaid coverage among these beneficiaries, who tend to have relatively low incomes, also contribute to low enrollment in Medigap among beneficiaries under age 65. For these reasons, a significantly smaller share of traditional Medicare beneficiaries under age 65 have Medigap compared to beneficiaries with traditional Medicare ages 65 and older: 7% vs. 46% in 2022 (Figure 4). When these beneficiaries turn age 65, federal law requires that they are entitled to the same six-month open enrollment period for Medigap that is available to new beneficiaries ages 65 and older.

Although Not Required Under Federal Law, Most States Require Medigap Insurers to Offer an Initial Guaranteed Issue Period to Purchase Medigap to People Under Age 65 with Disabilities

Thirty-six states require insurers to issue at least one kind of Medigap policy to beneficiaries under age 65, typically through an initial open enrollment period (Figure 5, Appendix Table 3). Of these 36 states, 25 require insurers to sell all plan types to people under age 65 during the guaranteed issue period. Starting January 1, 2025, Nebraska will require insurers to offer at least one kind of Medigap policy to beneficiaries under age 65, and Indiana, which currently requires insurers to sell only Plan A to people under age 65, will extend this requirement to all Medigap plan types offered by insurers.

In addition to the initial open enrollment period it already offers, when Minnesota institutes two annual Medigap guaranteed issue open enrollment periods: one during the annual Medicare open enrollment period from October 15 to December 7 and one during the Medicare Advantage open enrollment period, from January 1 to March 31, these will apply for beneficiaries ages 65 and older as well as people under age 65 with disabilities.

Requirements for People with ESRD: Of the 36 states that require insurers to issue at least one kind of Medigap policy to people under age 65 with disabilities, 26 states explicitly require insurers to also sell these policies to people with ESRD. Four states (California, Massachusetts, Vermont, and Indiana) explicitly state that insurers are not required to sell policies to people with ESRD, though Indiana has enacted a new law requiring insurers to sell Medigap policies to people under 65 with ESRD starting January 1, 2025. The remaining six states are silent on whether insurers must sell at least one policy to people with ESRD.

Requirements for People with ALS: Of the 36 states that require insurers to issue at least one kind of Medigap policy to people under age 65 with disabilities, 25 states specify that they must be sold to people with ALS. Eleven states (including CA, MA, and VT) are silent on whether insurers must sell policies to people with ALS.

This is in addition to the 14 states and D.C that do not require insurers to sell a Medigap policy to people under age 65 with disabilities, including people with ESRD and ALS.

The same four states that have expanded Medigap guaranteed issue rights most broadly for beneficiaries ages 65 and older also require broader access to Medigap for people under age 65.

In addition to offering an initial guaranteed issue period to purchase Medigap, Massachusetts, Maine, New York, and Connecticut require continuous or annual guaranteed protections for people under age 65 with disabilities, though with slightly different requirements than for people ages 65 and older: in Massachusetts, insurers are not required to issue policies to people with ESRD, while in Connecticut, insurers must issue Plan A to people under age 65, as well as Plans B, C, and/or D for insurers that sell these plan types to people ages 65 and older. In Maine, all Medigap plan types must be available to beneficiaries under age 65 with disabilities during the open enrollment period, but after this period, insurers are only required to issue Medigap Plan A to beneficiaries under age 65 during the one-month open enrollment period that happens each year (the same as for people ages 65 and older).

19 of the 36 States That Require Medigap Insurers to Offer Policies to Eligible Applicants Under Age 65 During an Initial Open Enrollment Period Also Do So for Certain Qualifying Events

Nineteen states require Medigap insurers to offer policies to eligible applicants under age 65 based on certain qualifying events (Figure 6, Appendix Table 4):

- Ten states require Medigap insurers to issue policies when an applicant under age 65 has a change in their employer (retiree) coverage. These 10 states (CA, CO, FL, ID, IL, MN, MO, OR, TX, and VA) also offer guaranteed issue rights for applicants ages 65 and older who have a change in their employer (retiree) coverage. However, some states have more restrictive policies for people under age 65. For example, in Texas, this guaranteed issue right applies only for Medigap Plan A for people under age 65.

- Five states (CA, CO, OR, TN, and TX) require insurers to issue Medigap policies to beneficiaries under age 65 who lose their Medicaid eligibility. These five states also offer the same guaranteed issue protections for people ages 65 and older, but in the case of Texas, the guaranteed issue right for people under age 65 applies only in the case of Plan A.

- Ten states have other types of qualifying events:

- Eight states (CA, ID, KY, ME, MD, MO, OK, OR) require Medigap insurers to allow Medigap policyholders under age 65 to switch to a policy with equal or less generous benefits (e.g., under “birthday rules”).

- Illinois extends the same federal Medicare Advantage guaranteed issue protections that are available to people ages 65 and older, to people under age 65 in the state. For example, Medicare Advantage enrollees under age 65 in Illinois who move out of their Medicare Advantage plan’s service area, or whose Medicare Advantage plan goes out business, have a 6-month guaranteed issue right to purchase a Medigap policy.

- Oregon requires that insurers offer a guaranteed issue period to individuals who move to Oregon from a state that does not require Medigap insurers to issue policies to people under age 65.

A New Federal Rule May Have Implications for the Medigap Market

A new federal rule – Nondiscrimination in Health Programs and Activities – has the potential to bring changes to the Medigap market. To date, Medigap policies have not been subject to Section 1557 of the Affordable Care Act, which prohibits discrimination on the basis of race, color, national origin, sex, age, or disability in certain health programs and activities. In May 2024, the Department of Health and Human Services (HHS) issued a final rule clarifying that Section 1557 would apply to Medigap policies offered by insurers that are “principally engaged” in providing health insurance coverage beginning January 1, 2025, and may not engage in behavior that is discriminatory, which could include charging higher rates based on age. This could mean that some current medical underwriting or premium rating practices in the Medigap market could violate Section 1557. The new rule would not apply to companies that sell Medigap policies that do not engage principally in the provision of health insurance coverage, such as those that primarily provide home or auto coverage.

It is unclear the extent to which this rule will change Medigap insurers’ practices and how the rule will be enforced. The rule is also subject to ongoing litigation, including a postponement of the rule in its entirety in Texas and Montana, which could further delay its implementation.

Federal and State Proposals to Enhance Consumer Protections for Medigap

Federal legislation: The Elijah E. Cummings Lower Drug Costs Now Act, which passed the House of Representatives in December 2019, included provisions that would have provided some guaranteed issue protections to Medicare beneficiaries, including requiring the one-time, six-month Medigap open enrollment period to apply to all Medigap-eligible beneficiaries, without regard to age (meaning it would apply to people under age 65), and providing a one-time opportunity for Medicare Advantage enrollees to switch to Medigap, even if they had been in Medicare Advantage beyond the one-year trial period. CBO estimated that these provisions would increase Medicare spending by $14 billion over 10 years (2020-2029). CBO did not estimate the impact on Medigap premiums.

While CBO did not provide a detailed explanation of its cost estimate, certain assumptions might explain the projected increase in Medicare spending. For example, beneficiaries who switch to traditional Medicare may use more services because they have the protection of Medigap coverage, substantially limiting their out-of-pocket costs, which studies show can increase utilization of health care services. The higher use of services under traditional Medicare would have the effect of increasing Medicare spending and raising Medigap premiums. It is not clear whether CBO’s estimate took into account potential savings associated with covering more beneficiaries under traditional Medicare than Medicare Advantage, since Medicare currently pays more, on average, for similar beneficiaries in Medicare Advantage than traditional Medicare.

A change in rules could also impact Medigap premiums if broadening guaranteed issue protections results in “adverse selection” in the Medigap market. Studies show that sicker Medicare Advantage enrollees disenroll into traditional Medicare at relatively higher rates, such as beneficiaries who have 2 or more complex chronic conditions or impairments in activities of daily living. If higher cost beneficiaries gain access to Medigap, premiums could rise. However, if Congress adopted an out-of-pocket cap for traditional Medicare, as some lawmakers have proposed, this might mitigate an increase in premiums or even reduce premiums because Medigap insurers would no longer be liable for costs that enrollees incur above the new limit.

Other bills previously introduced would prohibit medical underwriting in Medigap at all times, except for people who qualify for Medicare on the basis of ESRD or would expand the initial federal guaranteed issue period to all Medicare beneficiaries, including those under age 65 with disabilities, among other changes.

State legislation: Some states have also introduced legislation to expand consumer protections in Medigap. For example, California lawmakers introduced legislation that would require guaranteed issue rights during a 90-day annual open enrollment period. Iowa lawmakers introduced legislation to require guaranteed issue rights during a 30-day annual open enrollment period. Vermont lawmakers also introduced legislation that would provide guaranteed issue rights for people switching from Medicare Advantage to traditional Medicare around the time of their birthday. Other states have bills pending that would offer “birthday rules” in their state – allowing people who currently have Medigap policies to switch policies around the time of their birthday including South Dakota and Wisconsin. None of these legislative efforts have been signed into law.

Methods

The analysis on the share of Medicare Advantage enrollees 65 and older subject to medical underwriting outside of the Medicare Advantage trial period is based on based on Centers for Medicare & Medicaid Services (CMS) Chronic Conditions Data Warehouse Master Beneficiary Summary File (MBSF), 2022.

The state-level analyses on guaranteed issue protections for people ages 65 and older and people under age 65 with disabilities are based on a review of each state’s regulations, guidance documents/manuals, directives, and other publicly accessible government-issued documents.

Additionally, KFF staff contacted states’ insurance departments or State Health Insurance State Health Insurance Department Program (SHIP) offices for clarity in cases where publicly accessible documents were silent on a particular issue.

For the state-level analysis for people ages 65 and older:

- States are marked as “no” if their regulations or other publicly accessible documents do not specify any additional qualifying events (beyond the federal standard).

For the state-level analysis for people under age 65:

- States are marked as “no” to having any special qualifying events if 1) they do not require insurers to offer Medigap policies to people under age 65, or 2) they do not have any specified qualifying events or guaranteed issued protections for people under age 65, based on KFF review of state regulations, guidance documents, and contact with insurance departments or State Health Insurance Department Program (SHIP).

- States are marked as “not specified” if publicly accessible documents do not specify requirements pertaining to each guaranteed issue qualifying event. These qualifying events were identified based on whether they are available to people 65 and older in that state.

Although best efforts were made to check each state’s regulations, guidance documents, and call insurance departments/SHIP offices, it is possible that states marked as “not specified” have rules that were not identified by the research team.