Proposed Mental Health Parity Rule Signals New Focus on Outcome Data as Tool to Assess Compliance

New proposed updates to the regulations under the Mental Health Parity and Addiction Equity Act (MHPAEA) seek to strengthen the law’s implementation by employer plan sponsors and insurers in the group and individual insurance market. If finalized as proposed, it would establish a new three-part framework for plans and insurers (collectively, “plans”) to show that certain treatment limits on behavioral health coverage comply with the parity law. The proposal would require plans to apply a new mathematical test to determine whether certain limits on behavioral health coverage are no more restrictive than limits on medical coverage. In addition, plans have to document that the “processes, strategies, evidentiary standards and other factors” used to design and apply specific limits on behavioral health are comparable and not more stringent than those used to design and apply limits on medical benefits. The third part of the framework would require plans to take affirmative steps to collect, evaluate and analyze specific types of “outcome data.” This is data designed to show the impact of certain restrictions on coverage (such as prior authorization rules and provider networks limitations) that apply to both behavioral health and medical care. Disparities in this data that show more restrictive limits on behavioral health than medical care would serve as an indicator of a possible violation of parity and trigger requirements on plans to take action to address the problem.

The focus on use of data analysis for compliance and enforcement represents an effort to look beyond just written plan descriptions of coverage, provider directories, and insurer marketing materials to see how coverage works in practice—for example, how claims are actually processed and evaluated, the results of that process, and how these affect insured individuals.

Background

Setting up a mechanism in MHPAEA rules to easily compare behavioral health coverage to medical coverage has been difficult, especially when comparing limits on coverage beyond cost sharing amounts, where it is relatively simple to evaluate parity. Much agency guidance has focused on how to compare so-called nonquantitative treatment limits (NQTLs), such as prior authorization, for behavioral health coverage to those for medical care. The Consolidated Appropriations Act (CAA) of 2021 requires plans and issuers to document that all NQTLs on behavioral health benefits meet parity standards through a written “comparative analysis” submitted to federal or state authorities upon request (and—for some plans—to consumers upon request).

The agencies are looking to revamp ways to measure compliance with parity—and make the required comparative analysis more useful—by requiring plans to conduct quantitative analyses of certain coverage features, including ways to measure the impact of NQTLs on actual consumer access to behavioral health care.

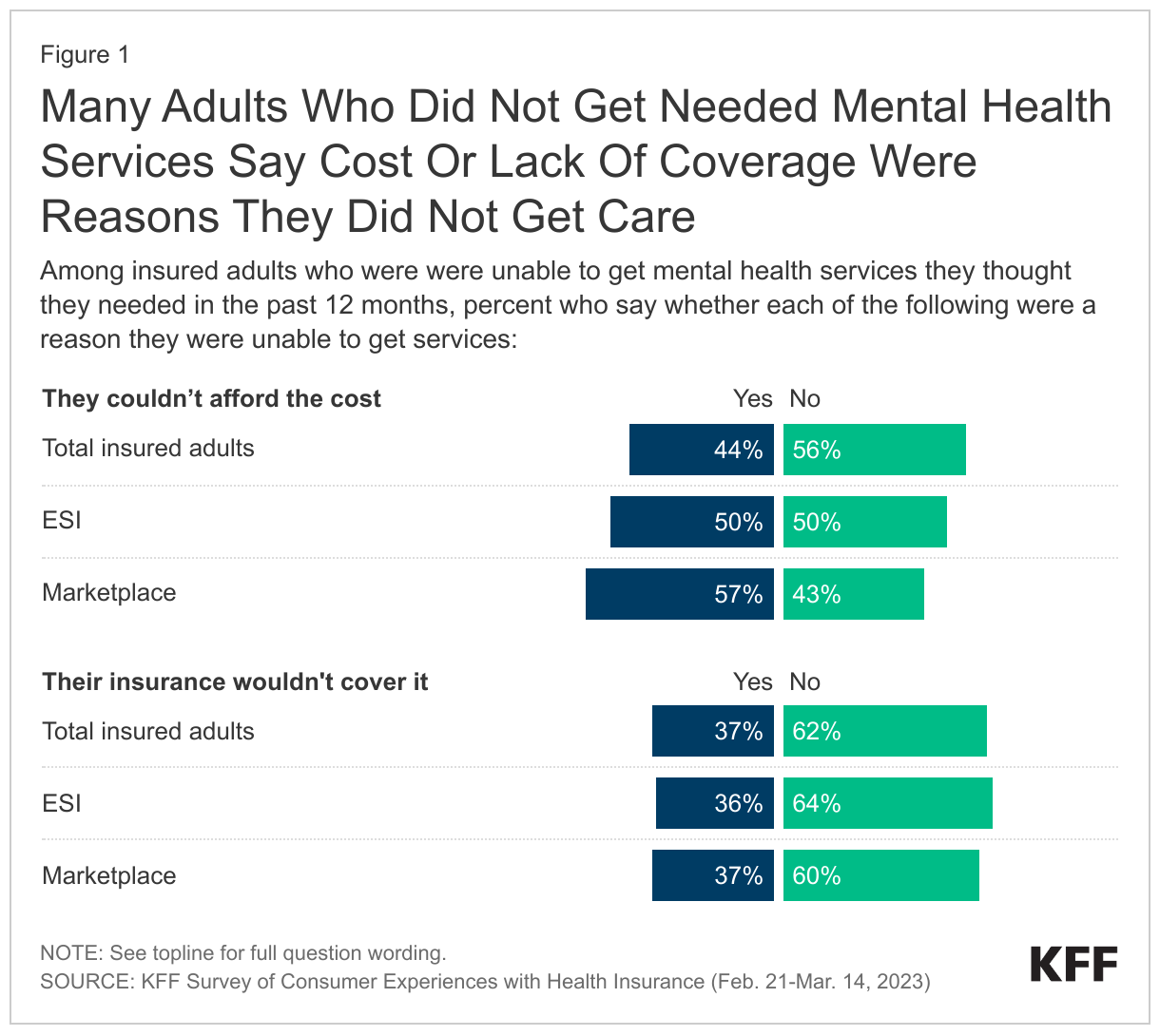

The recent KFF Survey of Consumer Experiences with Health Insurance found 17% of insured adults indicated that even with health coverage, they did not get mental health care that they thought they needed in the past year. Of these individuals, more than 4 in 10 (44%) indicated that one of the reasons they did not get needed mental health care was that they could not afford the cost. Additionally, about a third of insured adults who did not get needed mental health services in the past year say their insurance not covering the services was a reason they did not get the care.

A recent Peterson-KFF Health System Tracker study also highlighted the affordability burden. That study looked at commercial claims data from a sample of large employer plans and found that enrollees treated for depression and/or anxiety pay a larger share out-of-pocket for mental health services than for other services.

How are the agencies proposing to use outcome data for mental health parity?

Insurers and group health plans would be required to collect and evaluate data deemed relevant to assess the impact of the use of each NQTL on access to behavioral health care versus medical care. The agencies would specify in future guidance the type of data, as well as the form and manner of collection. At a minimum all plans would collect data on “the number and percentage of claim denials” as part of its review and assessment of each NQTL.

If analysis of the data shows material differences in access to behavioral health treatment when compared to medical, the agencies will consider this a strong indicator that there is a violation of the parity law. Plans would then need to take “reasonable action” to mitigate these material differences to avoid violating the parity law. The CAA-required comparative analysis would have to include the data results and actions taken to address the material difference (actions might include increased reimbursement of providers or enhanced use of behavioral telehealth). The agencies seek information about how to define “material difference” in a tangible quantitative manner using statistical tools.

An exception applies for the use of independent professional medical or clinical standards. Plans can avoid having to do this outcome analysis for an NQTL, if it “impartially” applies independent professional medical or clinical standards when designing and applying an NQTL. Plans sometimes use clinical criteria that they develop internally to make decisions about whether a service or medication is medically necessary and covered by insurance. Challengers to use of certain internal criteria claim that the criteria are inconsistent with generally accepted standards of care, create a financial conflict of interest for a plan or are not transparent to patients. This rule might give plans an incentive to use independently developed clinical criteria to avoid having to conduct an outcome analysis.

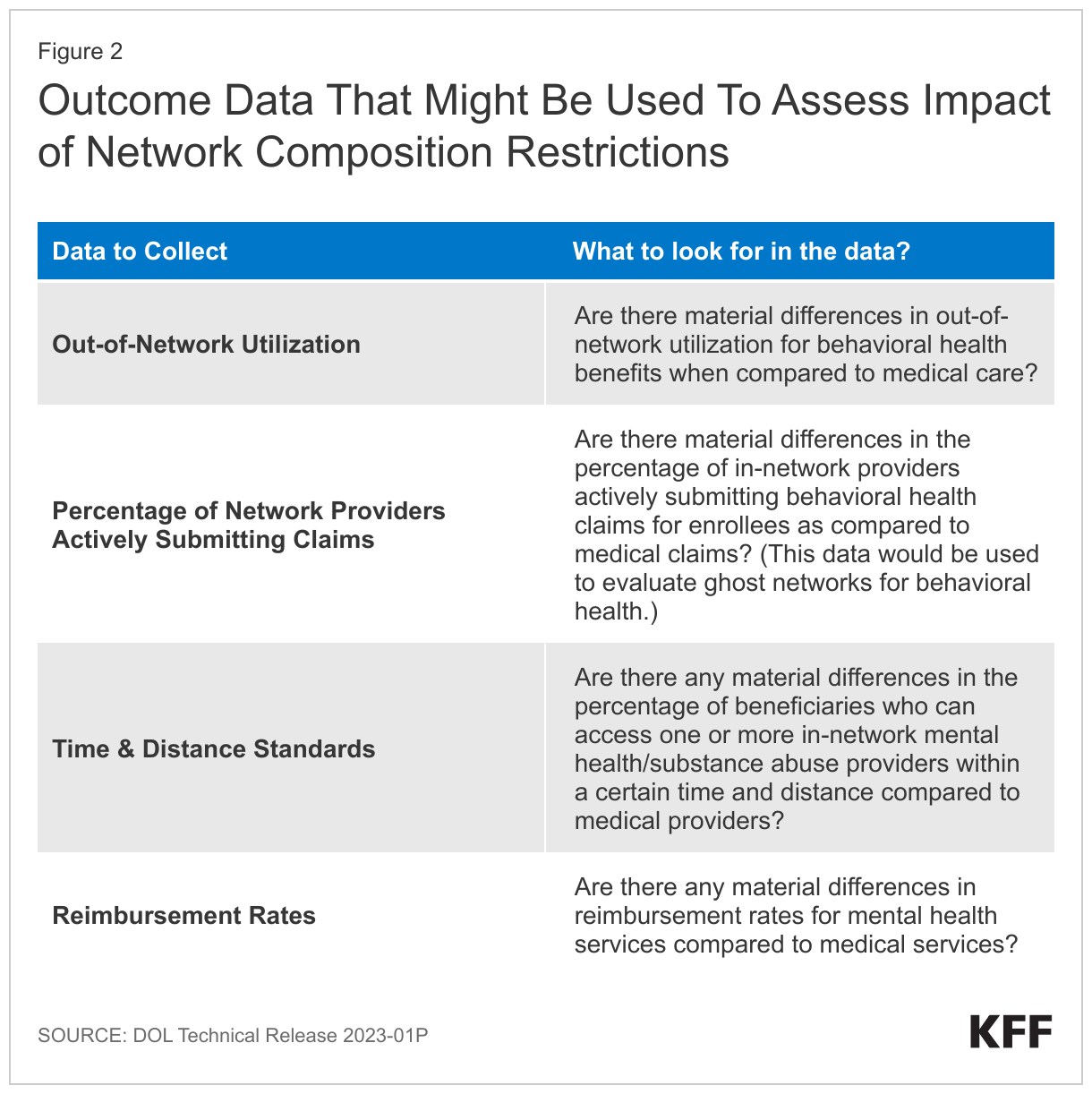

Special rules would apply to NQTLs that affect network composition. The agencies note a particular concern about NQTLs that limit access to in-network behavioral health providers and subject these to a higher level of scrutiny than all other NQTLs. The agencies note studies that indicate lower provider reimbursement rates and higher levels of use of out-of-network providers for behavioral health services when compared to medical. Where outcomes data show disparities in access to in-network behavioral care when compared to in- network medical care, the plan would automatically violate the parity law under the new proposed rule. The DOL issued Technical Release 2023-01P that requests comment on four types of data it might collect as relevant outcomes data for NQTLs that involve network composition.

What are the key issues to watch?

The proposal’s data-informed approach to compliance would essentially require all plans to take action to audit the possible impact of certain coverage limits on behavioral health if they want to continue to use those limits. Some states have started approaches that go beyond disclosure of outcome data upon request but instead involve ongoing plan reporting of similar metrics such as claim denials, though those requirements do not extend to self-insured employer plans as the federal regulations would.

The parity proposal would for the first time specifically require private self-insured employers to review and document the status of their behavioral health networks. These plans would also have to disclose, upon request, claim denial information.

Expect questions on what data is a good indicator or benchmark for spotting a potential parity violation. The cost, complexity, and value of plans having to collect and evaluate this data are also issues for consideration, as well as the relative legal responsibilities of insurers and employers to know how their coverage is working on the ground. Enhanced enforcement of these rules will continue to be the focus as some advocates point to plan use of medical management techniques to improperly deny behavioral health claims, while plans point to provider shortages beyond their control as limiting access to behavioral health care.

This work was supported in part by a grant from the Robert Wood Johnson Foundation. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.