Comparing Private Payer and Medicare Payment Rates for Select Inpatient Hospital Services

As the total number of people who have been hospitalized for COVID-19 continues to rise across the U.S., there is increasing interest in the pandemic’s impact on costs incurred by patients, public and private payers, and revenues for hospitals and other health care providers. With many severely ill COVID-19 patients requiring hospital care, the pandemic provides a window into the large gap between what hospitals charge private insurers and what Medicare pays. As of June 20, 2020, 43% of patients hospitalized for COVID-19 in the United States were age 65 or older,1 virtually all of whom have Medicare coverage. Proposals like a public option or lowering the age of Medicare eligibility would give more people access to coverage with lower payments rates and premiums, while also resulting in lower revenues for health care providers.

This issue brief analyzes hospital payments paid by private payers and by Medicare for a selection of inpatient services, including services requiring similar inpatient treatments for COVID-19, using data from the IBM MarketScan Commercial Claims and Encounters Database and the Medicare Provider Payment and Utilization Data public use files for 2014 to 2017. For each of these services, we compare average payments made by private payers and Medicare, show the 75th and 25th percentile in Medicare and private insurance payments. We also examine the growth in average payments paid by private insurers and Medicare, relative to inflation.

Our analysis finds:

- Private insurance payment rates were between 1.6 and 2.5 times higher than Medicare rates, with some variation among the ten DRGs included in our analysis.

- Private insurance rates varied more widely than Medicare rates.

- The average private insurance payment rates paid for diagnoses related to COVID-19 increased between 9.3% and 22.4% from 2014 to 2017, much faster than Medicare rates.

Background

Private insurance payments for inpatient services vary based on several factors, most notably hospitals’ market power relative to that of insurers.2 In contrast, reimbursements in traditional (fee-for-service) Medicare depend on a set of federal policies and formulas. Inpatient services are categorized into “diagnosis-related groups” (DRGs), which group together patients with similar clinical needs that are expected to require similar levels of hospital resources. Each DRG has a payment weight assigned based on the average resources required to treat Medicare patients grouped in that DRG. These weights are then adjusted for hospital-based factors such as local labor costs and case mix, as well as patient-specific factors such as severity and comorbidities. Hospitals that treat a higher share of low-income Medicare and Medicaid patients receive increased reimbursements, as do teaching hospitals. Medicare also makes additional outlier payments to reimburse hospitals for cases that are particularly costly.

To shed light on differences in Medicare and private payer reimbursement rates for COVID-19-related care, this analysis examines payments for respiratory infections and inflammation with major comorbidities or complications, the principal DRG now used by Medicare to reimburse for COVID-19,3 as well as payments for respiratory system diagnoses with ventilator support. The Trump administration has stated that Medicare rates will be used to reimburse hospitals and other providers that treat uninsured patients with COVID-19, subject to the availability of funds. The CARES Act includes a 20% increase in inpatient reimbursement for Medicare patients with COVID-19 during the COVID-19 Public Health Emergency (PHE) period. This 20% increase was not factored into our analysis because it was not in effect at the time source data were collected, the increase is temporary, and the Department of Health and Human Services has stated that it will not apply to payments for uninsured patients.4 Because we did not account for the 20% temporary increase, the differences we show between private and Medicare payment rates for the three respiratory DRGs in this analysis are somewhat overstated during the period of the public health emergency, as explained below.

In addition to the three respiratory DRGs that include patients requiring similar treatments to those used for patients with COVID-19, we examined seven other inpatient services that had a comparably large number of hospitalizations in both datasets: hip and knee replacements, angioplasties, major bowel surgeries, bariatric surgeries, uterine surgeries, treatment for esophagitis or gastroenteritis, and treatment for cellulitis.5 This group of services includes elective procedures (hip and knee replacements and bariatric surgery), non-elective procedures (treatment for cellulitis and gastroesophageal disease requiring hospitalization), and procedures that can be performed electively for patients who do not emergently require them (major bowel surgeries, uterine surgeries, and angioplasty6).

Overall, hospital volume has declined for services not related to COVID-19 treatment. The largest decreases have been seen for elective procedures, many of which have been delayed or cancelled based on Centers for Medicare & Medicaid Services (CMS) recommendations designed to preserve hospital capacity and personal protective equipment and to help minimize the risk of coronavirus infections.7 As states begin to loosen social distancing restrictions, CMS has issued recommendations related to restarting health care that is not related to COVID-19.8

Key Results

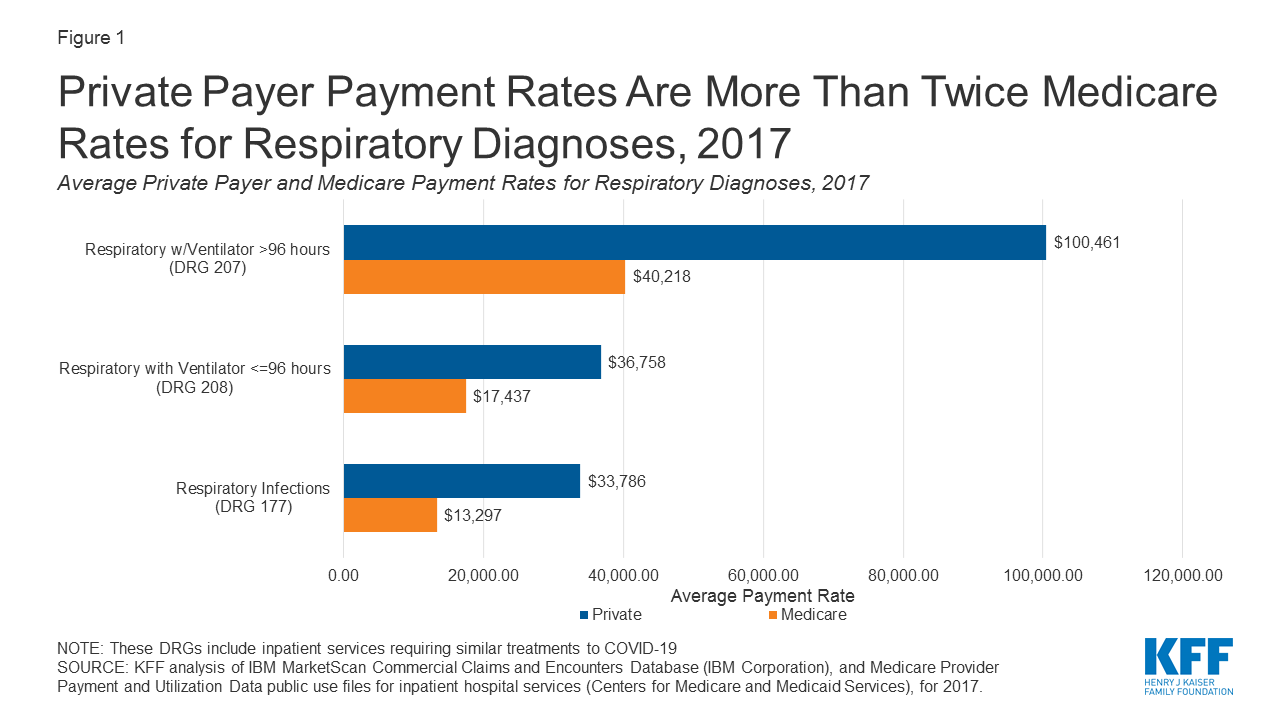

Private insurance paid more than twice what Medicare paid on average for all three respiratory diagnoses related to COVID-19. For patients on a ventilator for more than 96 hours, the average private insurance payment rate is about $60,000 more than the average amount paid by Medicare ($40,218 vs. $100,461). On average, private insurance reimbursement for services related to COVID-19 were between 2.1 and 2.5 times higher than average Medicare reimbursement (Figure 1, Appendix Table 1). The private-to-Medicare payment ratio for both respiratory infections and respiratory diagnosis with ventilator for more than 96 hours are higher than the ratios for any of the seven other DRGs included in this analysis (Figure 2, Appendix Table 1).

Figure 1: Private Payer Payment Rates Are More Than Twice Medicare Rates for Respiratory Diagnoses, 2017

If the 20% add-on that hospitals now get paid by Medicare for COVID-19 inpatients had been in effect in 2017 and if it had been applied to these claims, the difference between Medicare and private payments would be smaller. For example, the average Medicare payment rate for patients on a ventilator for more than 96 hours would increase from $40,218 to $48,262 if all claims were subject to the 20% add-on. Even with the 20 percent increase in Medicare payments for COVID-19 hospitalizations, private insurance payment rates would still be roughly double Medicare rates, ranging from 1.8 to 2.1 times Medicare rates.

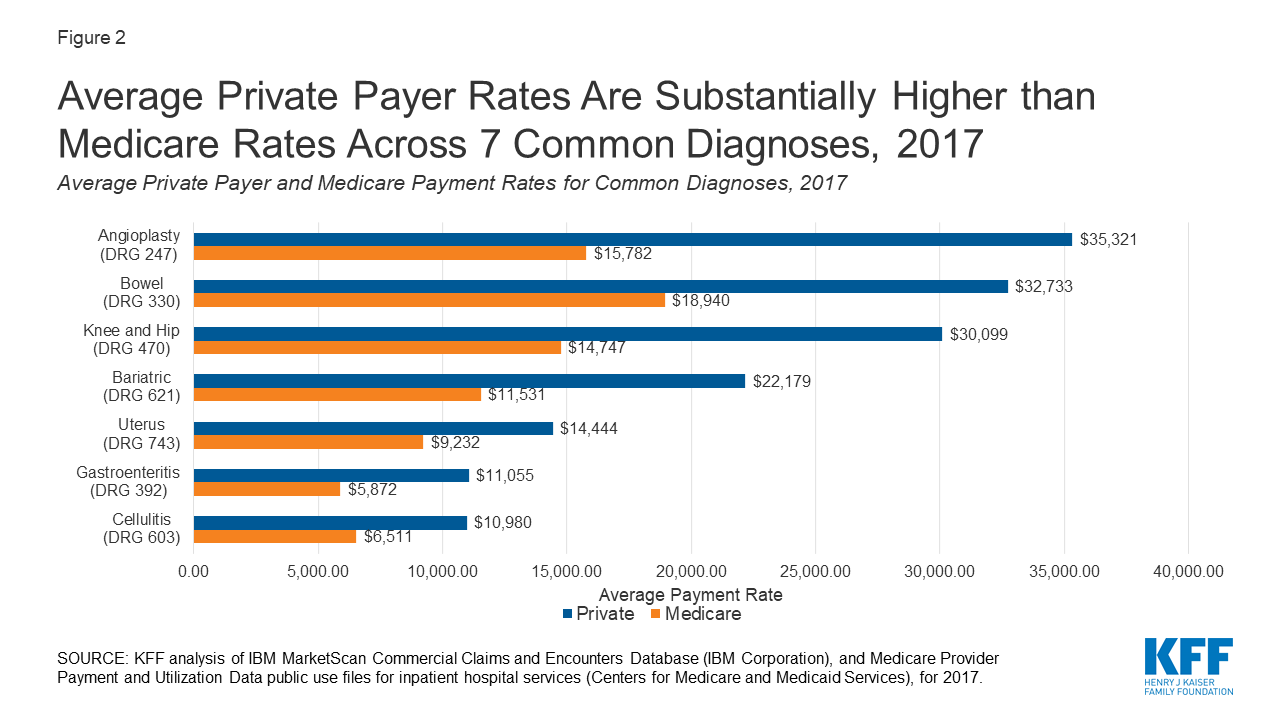

Private insurance paid at least $10,000 more than Medicare rates on average for four of the seven other diagnoses we analyzed. When comparing the ratio of average private insurance and Medicare payments for services not related to coronavirus, private insurance payment rates ranged from 1.6 to 2.2 times higher than average Medicare payment (Figure 2, Appendix Table 1). The three procedures with the highest private-to-Medicare payment ratios are either elective procedures (knee and hip replacements and bariatric surgery) or procedures that can be performed electively for patients who do not emergently require them (angioplasty). The high private-to-Medicare payment ratio for procedures that are often elective helps to explain the financial impact that delays and cancellations of elective procedures have had on hospitals.

Figure 2: Average Private Payer Rates Are Substantially Higher than Medicare Rates Across 7 Common Diagnoses, 2017

There is much wider variation in private insurance payment rates than Medicare payments for all services we analyzed, with particularly wide variation for the three diagnoses similar to COVID-19 treatments. For the ten diagnoses we analyzed, private insurance payment rates at the 75th percentile were between 1.7 and 2.6 times higher than private insurance payments at the 25th percentile for the same diagnosis. In contrast, the 75th percentile payment rates paid by Medicare were about 1.3 to 1.4 times the 25th percentile payment rate. For seven of the ten conditions we analyzed, the 75th percentile private insurance payment rate was at least $10,000 more than the 25th percentile private insurance payment rate. The DRG for respiratory diagnosis with ventilator support for more than 96 hours had the widest variation of the diagnoses in our study, with about a $74,000 difference between the 75th and 25th percentiles of private payment rates.

As discussed earlier, Medicare payments vary only based on several factors including cost of labor where the hospital is located, patient comorbidities, and higher reimbursement for particularly expensive cases, leading to greater uniformity in rates across hospitals compared to private insurance. The substantially larger variation in payment rates paid by private insurers suggests that geographic differences in labor costs and patient severity alone may not fully explain variation in private payment rates. Instead, much of the literature suggests that variation in private insurers’ payments is better explained by local market dynamics, including the degree of hospital consolidation.9

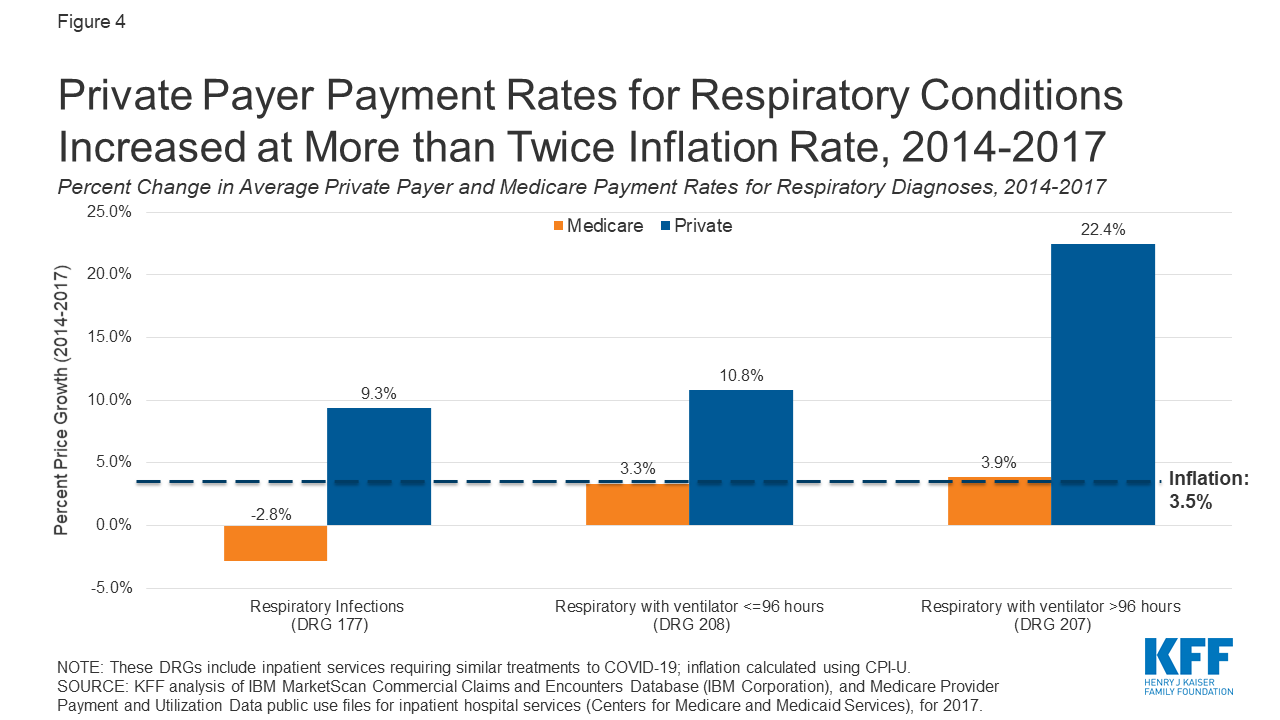

The average private insurance payment rates paid for diagnoses related to COVID-19 increased between 9.3% and 22.4% from 2014 to 2017, much faster than Medicare rates. Those increases are well above inflation over the same time period, which was 3.5%,10 as measured by the Consumer Price Index for All Urban Consumers (CPI-U) (Figure 4). In contrast, the average payment rate increases in Medicare were either close to inflation or—in the case of the respiratory diagnosis—the average payment declined. This decline is likely partly due to a drop in the relative weight used by Medicare to determine payments for that DRG over the same period.11 Other factors could include a decrease in the average length of stay, a healthier case mix, or a decrease in the number of patients for which hospitals received outlier payments.

Figure 4: Private Payer Payment Rates for Respiratory Conditions Increased at More than Twice Inflation Rate, 2014-2017

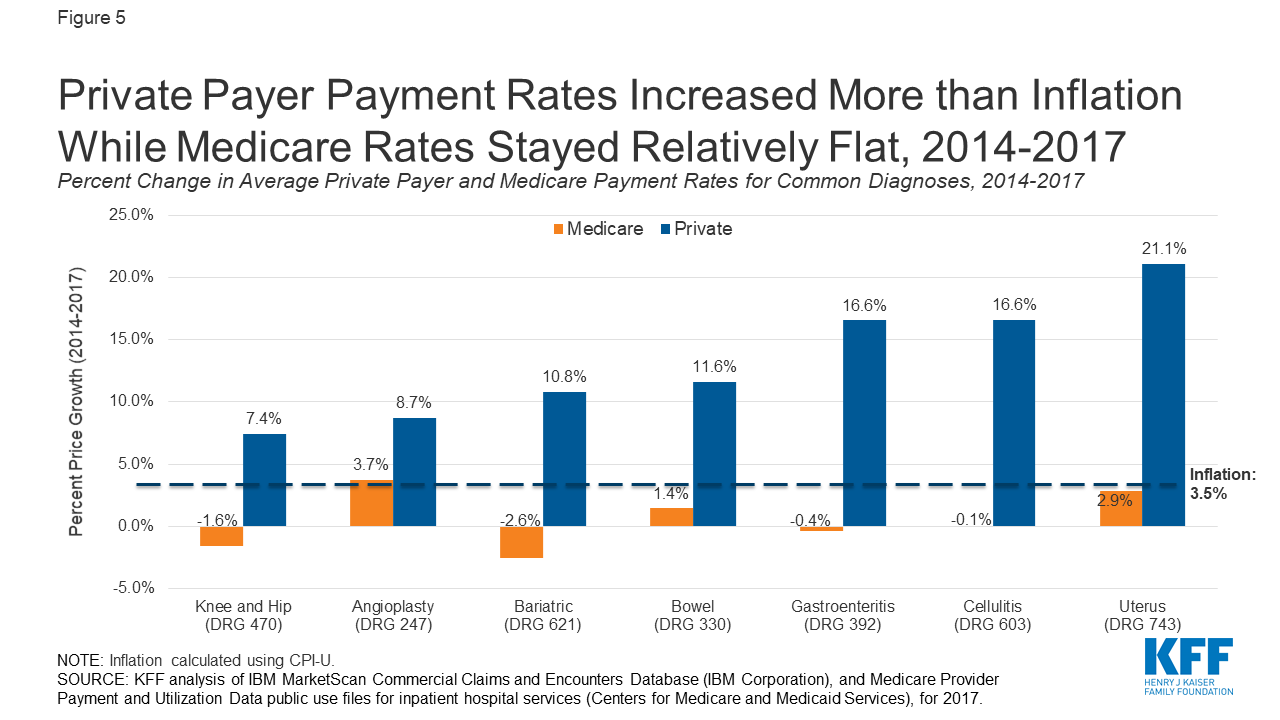

Between 2014 and 2017, private insurance payment rates for the seven non-COVID related services we analyzed increased more than twice the rate of inflation. The growth in private insurance payment rates substantially outpaced Medicare. This finding is consistent with recent Peterson Center on Healthcare and KFF analysis showing that per enrollee spending has been grown much more quickly for private insurance spending than for Medicare.12 The largest percentage increase in payment rate was seen for uterine procedures, which had a payment increase of 21.1% (Figure 5). The three conditions with the smallest percent increase in average payment for private insurance were also the three conditions with the highest private-to-Medicare payment ratio among the seven non-COVID-19 related conditions we analyzed. It is possible that private insurance payment rates increased at a lower rate for these services because their payment rates were already relatively high in 2014 relative to Medicare.

The average Medicare payment for knee and hip replacements as well as bariatric surgery decreased 1.6% and 2.6%, respectively. The Medicare relative weight for those DRGs also declined.13 The declines in the average Medicare payment rates may also be partly due to a healthier case mix or a change in one of the other factors that impacts hospital payment for a DRG.

Figure 5: Private Payer Payment Rates Increased More than Inflation While Medicare Rates Stayed Relatively Flat, 2014-2017

Discussion

Our analysis shows that the pattern of private insurance payment rates vary widely and average about twice Medicare rates, consistent with a robust set of literature comparing private insurance and Medicare rates.14 Notably, we found that private insurance payment rates are more than twice Medicare rates for the services most likely to be used by patients who are hospitalized with COVID-19. The temporary 20% increase in inpatient reimbursement for COVID-19 inpatients during the public health emergency will narrow this gap for these DRGs, but will not impact other DRGs or reimbursement for patients without COVID-19 who receive treatment for respiratory conditions. For the non-COVID-19 DRGs, we found that the private-to-Medicare payment rate ratio was close to two-to-one for most of the seven diagnoses we analyzed, with the highest private-to-Medicare ratios for DRGs that are often elective.

Our analysis also shows a much wider variation in private insurance payment rates when compared to Medicare. Past studies have found that market consolidation has contributed to higher private insurance hospital prices.15 If the coronavirus pandemic leads to even greater hospital consolidation, hospitals may gain even greater leverage to demand higher prices from private insurers, further widening the difference between private and Medicare payment rates, and increasing premiums and other costs for people with private insurance. Proposals to create a public option or allow people to enroll in Medicare earlier could constrain payment rates and make health coverage more affordable, but also decrease revenues for health care providers.

This work was supported in part by Arnold Ventures. We value our funders. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.