Fraud in Marketplace Enrollment and Eligibility: Five Things to Know

Rooting out fraud has been one of the primary reasons given for changes to Marketplace enrollment and eligibility standards included in the Trump administration’s final Marketplace integrity and affordability rule (“final regulation”), and budget reconciliation legislation, named the “One Big Beautiful Bill Act,” passed in the U.S. House of Representatives and moving its way through the Senate. In the final regulation, the Centers for Medicare and Medicaid Services (CMS) points to “dramatic levels of improper enrollment” in Marketplace plans that CMS says have involved fraudulent actions by some agents, brokers, and web brokers. The final regulation and the budget reconciliation legislation seek to address alleged fraud by instituting new standards for consumers to enroll in Marketplace coverage, from additional paperwork requirements to “verify” a consumer’s estimated household income to obtain advanced premium tax credits (APTC) to significant new administrative steps and new payments for consumers to continue Marketplace coverage. Few changes are made in the final regulation concerning oversight of entities alleged to have engaged in fraudulent activities, and none are proposed in the budget reconciliation legislation.

This brief explains what is known about fraud and improper enrollment in Marketplace plans and what the final regulation and budget legislation would do to change current Marketplace enrollment and eligibility standards.

1. The Affordable Care Act (ACA) gives the federal government broad authority to combat Marketplace fraud, alongside existing state oversight of private health insurance.

The Affordable Care Act (ACA) gives the Secretary of the Department of Health and Human Services (HHS) the authority to determine appropriate activities to reduce fraud and abuse in the administration of Marketplaces and to investigate Marketplace activity, “in coordination with” the Inspector General (OIG) of HHS. The HHS Secretary oversees these functions through the Center for Medicare and Medicaid Services (CMS), with at least two CMS offices involved in combating ACA fraud—the Center for Consumer Information and Insurance Oversight (CCIIO) and the Center for Program Integrity (CPI). These agencies, along with the HHS OIG, have a role in protecting the financial and program integrity of ACA programs. The Department of Justice litigates civil and criminal actions involving alleged health care fraud and abuse.

Fraud oversight is just one part of these agencies’ program integrity functions. These agencies are charged with protecting government resources, as well as program beneficiaries (consumers), by making sure that enrollment and required government payments are accurate and provided without delay. This involves ongoing audits of actors involved in the administration of Marketplaces and oversight of all individuals involved in ACA Marketplace enrollment and eligibility—from the agencies that run the program, to consumers and insurers, as well as those who assist in enrolling consumers, from agents and brokers to Navigators.

Improper enrollment or improper government payments of federal subsidies are fraudulent only if there is an intentional act to deceive or misrepresent facts in order to enroll or receive these benefits. The ACA does not have its own definition of “fraud” specific to Marketplace plans, but agencies can look to existing definitions that have been part of Medicare and Medicaid program integrity standards for some time.

In addition to this broad authority to oversee program integrity in the Marketplace, the ACA provides that if an applicant for Marketplace coverage or subsidies “knowingly and willfully” provides false or fraudulent information, the applicant may be subject to a civil penalty of up to $250,000 (smaller penalties apply where a consumer negligently provides false information in applying for Marketplace coverage). The civil penalty extends to “any person,” including an agent or a broker that directly provides false or incorrect information related to a Marketplace enrollment. In addition, any person who receives information from a Marketplace applicant in order to apply for coverage is subject to a civil penalty if they do not keep this information confidential.

The ACA also states that any payments made in connection with Marketplaces are subject to the False Claims Act if these payments include any federal funds. The False Claims Act is a century-old law that is designed to prevent and punish any individual or organization that defrauds the federal government. This could include circumstances where an individual intentionally presents, or causes to be presented, a false or fraudulent claim to the federal government. The ACA increased the penalties available for False Claims Act violations.

Marketplaces were created by the ACA as a platform for individuals to enroll in private insurance coverage and to apply for income-based federal subsidies. While the coverage is private—making it different from the public programs like Medicare and Medicaid, Marketplaces rely on federal dollars to (1) pay for and administer advance premium tax credits (APTCs) and cost-sharing reductions (CSRs) that help most enrollees pay for coverage, and (2) fund the agency, CMS, that runs the federally-facilitated Marketplace (FFM) (HealthCare.gov) for the states that elect not to operate their own Marketplace. CMS, along with the Internal Revenue Service (IRS) (part of the Treasury Department), set up a complex process to determine who is eligible for Marketplace coverage and financial assistance.

Oversight of these processes and the extent of each federal agencies’ authority to police the program at the federal level is still developing, as federal regulators and enforcers interpret and implement existing requirements. Recent federal activity in this area is discussed below.

The federal government functions exist alongside state oversight. States are the primary regulators of the private insurance coverage available in the Marketplaces and 20 states run their own Marketplace. As a result, each state has its own parallel authority to oversee the integrity of the programs they run and have their own fraud and abuse authority to deal with bad actors in the system, including insurers and those that sell insurance for these insurers, such as agents and brokers. As discussed below, states license the agents and brokers that sell Marketplace coverage.

2. Improper enrollment in Marketplace coverage and subsidies is not the same as fraud.

The ACA contains a unique structure for determining eligibility for Marketplace coverage and for eligibility for financial assistance (APTCs and CSRs). Eligibility is largely determined based on the projected household income of a consumer for the coming year—not on the consumer’s past or current income. Specifically, at open enrollment in the fall before the January 1 coverage year, the consumer is asked to estimate what their household income will be in the coming year.

In addition to open enrollment, there are limited special opportunities for individuals to enroll in Marketplace plans during the coverage year. These “special enrollment periods,” or SEPs, allow individuals to enroll in Marketplace coverage and obtain APTCs during the year if they meet specific criteria. Determining eligibility for SEPs also requires consumers to make an educated guess (estimate) about what their total annual household income will be at the end of the year.

Consumers, especially those with low incomes, often face difficulty predicting future income. KFF analysis found that individuals, especially those with low wages and unstable work, experience significant swings in income throughout the year. For those near poverty, predicting annual income may be especially difficult. Many people with incomes just above poverty at the beginning of the year end up below the federal poverty level (FPL) by the end of the year, and conversely, many who start out with incomes below poverty end up with incomes above poverty. Three in five (61%) people with starting incomes below poverty end the year with an income more than 20% different than their income during the first three months of the year. People with incomes below poverty ($15,060 for a single person in 2025) are not eligible for premium tax credits.

In setting up the Marketplace enrollment structure, Congress recognized that an individual’s annual income might end up being higher or lower than what they estimated when they applied for coverage. This difference could mean that a consumer appears to be “improperly enrolled” in Marketplace coverage or “improper payments” of Marketplace subsidies are paid by the federal government, even though the consumer did not intend to deceive or misrepresent their income. Recognizing this possibility, Congress provided for a process to “reconcile” APTC payments at the end of the year, once a consumer’s actual household income is known.

This is how the process works now: If a consumer is eligible for an APTC, these payments are made by the IRS directly to the insurer of the Marketplace plan that the consumer selects. The consumer does not directly receive these APTCs. If an individual’s actual household income at the end of the year was higher than the consumer estimated, the IRS may have paid too much money on behalf of the consumer to the insurer for APTCs. As a result, the consumer must “repay” the IRS the excess premium tax credit when the consumer files their income tax. Congress included provisions in the ACA that prohibit the federal government from requiring individuals below certain income levels to pay the full amount of excess premium tax credits (often referred to as “repayment limits or caps”). The example below illustrates how this works under current law:

Carla is a 27-year-old rideshare driver in Florida who also does seasonal work throughout the year. She estimated her 2024 income at $27,000 (179% of the FPL) and received a $3,136 advance premium tax credit (APTC), which was applied to purchase a benchmark Silver plan with a monthly premium of $3,595. She ended up working more that year than she initially expected and as a result, she earned $37,650 (about 250% FPL), higher than what she estimated it would be. When filing taxes in 2025, she finds out that she should have received only $2,089 in APTC based on her actual income, meaning that her insurer was paid $1,047 more than Carla was eligible for in APTC. Due to her low income, however, Carla is not required to pay the full $1,047 to the IRS. Under repayment caps, Carla pays $950.

In this example, although Carla’s insurer received more APTC amounts than it should have, Carla did not intentionally underestimate her expected income (engage in fraud) in order to gain undue tax credits. She made an estimate that was reconciled at the end of the year when her actual household income was known, following the process Congress created in the ACA. The budget reconciliation bill would eliminate the repayment limits.

3. To date, allegations of fraud related to Marketplace enrollment have primarily focused not on the actions of consumers, but on agents, brokers, web brokers and/or third parties that assist these entities in generating business.

Agents and brokers are state-licensed professionals who sell health insurance and assist consumers with selecting and enrolling in a health plan. Agents and brokers generally receive commissions from health insurance companies for enrolling individuals in health plans. A “web broker” is an individual or group of agents, brokers or business entities registered with the federal Marketplace that “develops and hosts” a non-Marketplace website that interfaces with the Marketplace to assist consumers with direct enrollment in Marketplace plans. Accusations of fraud have involved actions by these entities to fraudulently enroll consumers in Marketplace coverage in order to obtain commission payments from insurance companies. These fraudulent enrollments typically involve one of the following scenarios:

- Unauthorized Enrollment: Enrolling an individual in Marketplace coverage without their consent

- Unauthorized Switching: Switching an individual already enrolled in a Marketplace plan to another Marketplace plan without their consent

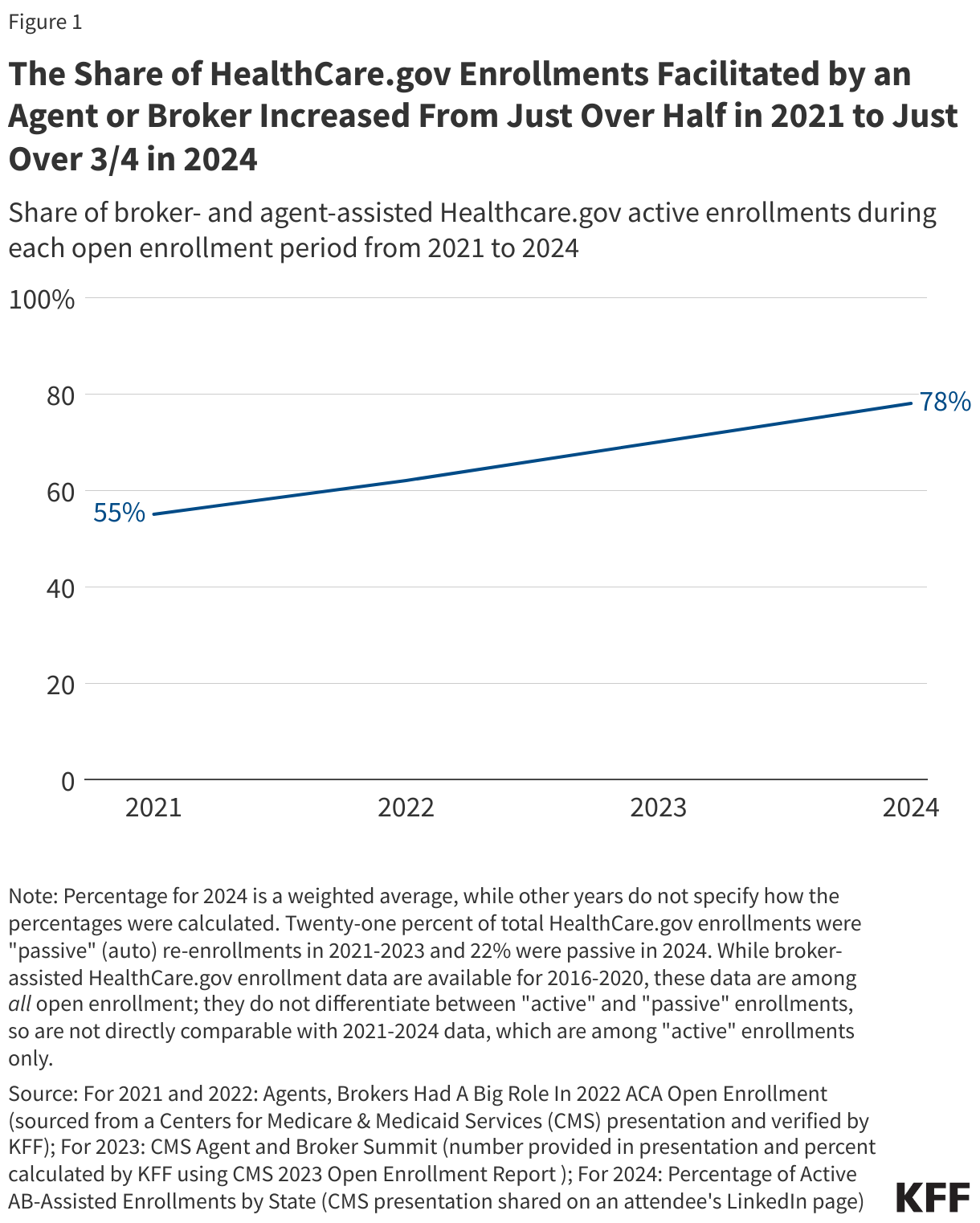

Brokers have played a large part in the Marketplace enrollment surge in recent years (Figure 1). According to KFF analysis of CMS data, during open enrollment for the 2021 plan year, brokers assisted 55% of active plan selections in HealthCare.gov states, increasing to 78% for 2024. Approximately one in five of all HealthCare.gov enrollments were “passive” (automatic) re-enrollments during these years (21% for 2021-2023, and 22% for 2024). We do not know how many of those who were automatically re-enrolled may have been assisted by a broker at some point during open enrollment. Broker-assisted enrollment data from 2016 to 2020 are among all HealthCare.gov enrollments, including automatic re-enrollments, so are not directly comparable with the 2021-2024 data. For context, however, 40% of all HealthCare.gov enrollments in 2016 were broker-assisted.

Between January 2024 and August 2024, CMS received 183,553 complaints of unauthorized enrollments, and 90,863 complaints of unauthorized switching of plans sold on the FFM (HealthCare.gov). CMS suspended 850 brokers for reasonable suspicion of fraudulent or abusive behaviors related to unauthorized plan switches and unauthorized enrollments between June and October 2024. Some of the entities suspended were web brokers approved and registered by CMS to host an application for Marketplace coverage on their own websites through processes called direct enrollment (DE) and enhanced direct enrollment (EDE). These functions are discussed below.

CMS took action to resolve the complaints, putting safeguards into place to protect consumers from broker fraud. For example, CMS announced that starting in July 2024, it would block agents and brokers from modifying a consumer’s HealthCare.gov enrollment unless the agent or broker has already assisted the consumer with enrollment in the past. Also, agents and brokers must enter into a three-way call with consumers and the Marketplace Call Center when trying to make changes to an account they are not already associated with.

Fraud allegations brought wide-ranging reactions from Congress in the summer of 2024. Some House Republican leaders called for further investigation, alleging that recent legislative and regulatory changes made to Marketplace rules (specifically, enhanced APTCs and Biden-era regulations aimed at reducing barriers for consumers signing up for Marketplace coverage) created incentives that encouraged Marketplace fraud. Democratic Congressional leaders, on the other hand, introduced legislation aimed at improving oversight and accountability for agents, brokers and marketing entities that engage in fraud.

Consumers sued brokers alleging fraudulent enrollment. In April 2024, consumers (and some brokers) brought class action litigation against specific brokers, web brokers, and marketing companies that generate sales leads (called “lead generators”) alleging, among other things, that the unauthorized switching and enrollment were part of a widespread scheme to obtain broker commissions that resulted in harm to enrollees and to brokers that originally placed an enrollee in coverage before the switch. While the case has since been dismissed, the plaintiffs alleged that the parties involved “created, sold, purchased and/or financed the purchase of leads that deceived consumers into thinking that they would receive cash cards and other cash benefits.” Leads include information such as consumer names and contact information that agents and brokers use to generate business. Many individuals and groups are in the business of lead generation and are not themselves licensed as agents and brokers. They sell or provide this information to those licensed to sell insurance.

How the alleged scheme worked: The complaint alleged a complicated scheme involving multiple parties. Marketing agencies and other individuals developed social media ads that falsely offered free cash rewards. Consumers that clicked on the ad were brought to a landing page where they were asked to provide specific information with the promise of cash. This information was captured and sold to agents and brokers who, using an enhanced direct enrollment platform, enrolled consumers in Marketplace coverage without their knowledge or switched their existing coverage to another plan.

Some brokers involved in the case brought an action against the federal government. In August 2024, TrueCoverage, LLC and Benefitalign LLC, two of the entities that had been sued in the April 2024 litigation and that had been suspended from the ACA Marketplaces, sued HHS and CMS after they were blocked for engaging in conduct that “compromised and placed consumers’ personally identifiable information (“PII”) and the integrity of the Exchanges at risk.” The case was dropped by the plaintiffs in October 2024, following a court decision denying the plaintiffs’ request for emergency relief. The court found that current regulation permits CMS to suspend direct enrollment entities based on “circumstances” that pose a “risk” that is “unacceptable.” Proof that systems have been compromised is not required.

Many suspended brokers were reinstated in 2025, according to CMS. It was reported that by March 2025, CMS had reinstated at least some of the brokers that had been suspended. It is not clear whether the reinstated brokers had demonstrated to HHS that they had remedied the cause of the suspension, as required in a regulation finalized by the Biden administration in January 2025. In June 2025, CMS released a Frequently Asked Questions (FAQs) document related to the removal of more than 1,000 brokers from its agent/broker suspension and termination list.

While these fraud allegations received nationwide attention in 2024, federal investigations of agents and brokers date back to at least 2018 (before the availability of enhanced APTCs and the Biden administration’s enrollment changes). Law enforcement action against agents and brokers include allegations of activity as far back as 2018. For example:

- The Justice Department, in February 2025, charged two individuals with intentionally enrolling consumers in fully subsidized Marketplace plans between 2018 and 2022 that they were not eligible for in order to obtain commission payments. The indictment alleges that the individuals used misleading and deceptive sales tactics that targeted low-income individuals and provided false addresses and social security numbers. The trial is scheduled for later this year.

- Another recent Justice Department indictment alleges similar activity dating back to 2019.

- Annual HHS/DOJ reports on health fraud and abuse enforcement note investigations of agents and brokers going back to 2019. For example, the annual report on fraud enforcement activity for FY 2019 noted that CMS “reviewed cases of agent and broker misconduct and took administrative actions including terminating CMS’s agreements with agents and brokers and imposing civil monetary penalties on those agents and brokers who were found to have engaged in misconduct.” An FY 2023 report stated that CMS had received over 73,000 consumer complaints involving such misconduct as consumers being enrolled in federal Marketplace policies without their consent. That year, CMS “conducted over 80 investigations of outlier and high-risk agents and brokers, and made recommendations for administrative action, including suspension and termination of an agent’s and/or broker’s registration to sell policies on the FFM.”

4. Agents and brokers (including web brokers) who assist in Marketplace enrollment are regulated by both the federal government and states.

Clearing the pathway to allow brokers to assist consumers to enroll in Marketplace plans aligns with an ACA goal to increase consumer access to comprehensive health coverage. However, the history of broker-related fraudulent enrollment activity points to the importance of oversight of these entities. This not only protects consumers but also ensures that brokers operating in good faith with adequate control and accountability for the third parties that assist them can still provide enrollment help for Marketplace consumers. Both the federal government and states have authority to regulate agents and brokers.

Federal Marketplace oversight related to brokers’ conduct has developed over time aimed at protecting consumers from fraud, as well as preventing deceitful marketing practices and other potentially harmful conduct. The ACA requires the Secretary of HHS to establish procedures where States may allow agents and brokers to enroll individuals in Marketplace plans and assist them in applying for Marketplace subsidies. With this authority, CMS has developed and continues to update requirements agents and brokers must meet in order to assist consumers to enroll in Marketplace coverage. CMS has developed a framework that is different from CMS agent and broker requirements for Medicare Advantage plans. In Medicare Advantage, the insurers have a legal responsibility to ensure agents and brokers comply with federal (and state) requirements. For Marketplace plans, CMS has set standards to regulate agents and brokers directly, without accountability flowing through the insurers that hire them.

In the early years of ACA Marketplace regulation, rules largely included in annual CMS regulations added a range of requirements including a process for broker termination and suspension, standards for the display of Qualified Health Plan (QHP) information and disclaimers that must be posted when certain QHP information is not available, and standards of conduct for agents and brokers selling plans on the FFM.

New technology allows more consumers to enroll in Marketplaces but raises new concerns. “Direct Enrollment” (DE) is a process that allows insurers and web brokers to enroll consumers in coverage directly from their websites. Initially, the direct enrollment pathway allowed the consumer to start the process on a web broker’s own website, but then had to be redirected back to HealthCare.gov to complete the eligibility application before returning to the web broker site to select a plan. Improved technology has added new enrollment pathways that allow agents and brokers to complete the entire eligibility application and enroll consumers in coverage on their own third-party website platforms, without being redirected to HealthCare.gov. This process is known as “Enhanced Direct Enrollment” (EDE).

Although EDE was praised for its potential to increase HealthCare.gov enrollments, as with any new technology, there are and continue to be concerns about privacy and security of consumer information, the potential for fraud, and the possibility that EDE could lead to consumers receiving inaccurate or misleading information that might affect eligibility determinations and consumer choice. In March 2016, CMS announced its intent to implement this new enrollment pathway in the federally-facilitated Marketplace but delayed implementation of the EDE pathway until 2018 and added new safeguards, including a process for HHS-approved third-party entities to periodically monitor and audit agents and brokers using the DE or EDE pathways.

Use of EDE begins and grows; CMS makes further changes to agent and broker standards. The Trump administration expanded the use of the EDE pathway for the federal Marketplace with CMS’s approval of its first Enhanced Direct Enrollment partner, HealthSherpa, in December 2018.

- CMS reported that DE and EDE pathways were utilized for 37% of all active HealthCare.gov plan selections during 2021 open enrollment, up from 29% during 2020 open enrollment, attributing its growth to increased use of the EDE pathway. The EDE process has historically only been available in HealthCare.gov states; however, in 2024, Georgia became the first state-based Marketplace (SBM) to partner with EDE entities.

- HealthSherpa reported that more than 95% of total EDE enrollments came through its EDE implementations during the 2021 open enrollment.

- CMS implemented Help On Demand, a referral service allowing consumers using HealthCare.gov to request enrollment assistance from licensed agents and brokers.

- CMS added new requirements specific to issuers, agents, and brokers as direct enrollment grew. In 2019, the Trump administration rescinded a requirement that only HHS-approved auditors conduct third-party audits of these entities, allowing issuers, agents, and brokers to choose their own auditors.

Continuing consumer complaints of unauthorized agent and broker enrollment resulted in further changes to agent and broker oversight. Regulations issued during the Biden administration updated agent and broker oversight requirements, including:

- In 2023, to address enrollments done without consumer consent, CMS established new requirements that require agents, brokers, and web brokers in the federal Marketplace to verify that the eligibility application information they collected has been reviewed and confirmed by the consumer before submission. Receipt of the consumer’s consent has to be documented by agents, brokers, and web brokers.

- To clarify the reach of federal enforcement against agents and brokers, standards finalized in January 2025 allow CMS to hold “lead agents”—typically executives or others in leadership of broker agencies –accountable for misconduct or noncompliance that they direct or oversee.

- CMS clarified its authority to take immediate action to suspend a broker’s or agent’s access to the DE and EDE pathways and their ability to transmit information to the Marketplace when circumstances pose an “unacceptable risk” to enrollees, the accuracy of the Marketplace’s eligibility determinations, or the Marketplace’s information technology systems.

States also oversee insurance agents and brokers. Agents and brokers are required to be licensed in every state where they sell health insurance and are also required to complete the CMS Agent and Broker Federally-facilitated Marketplace (FFM) registration to sell Marketplace plans. To further combat fraud and other deceptive practices, the National Association of Insurance Commissioners (NAIC) reports that every state and the District of Columbia (DC) has made insurance fraud a crime for at least some lines of insurance, and 42 states and DC have insurance fraud bureaus that investigate claims of illegal insurance activities and work to prosecute insurance fraud. The NAIC’s model state law, Unfair Trade Practices Act (Model 880), which describes activities considered “unfair or deceptive acts or practices” in the insurance industry, has been adopted in some form by 45 states and the District of Columbia.

States that operate their own Marketplaces currently have considerable flexibility to establish additional policies and procedures in their Marketplaces for agents and brokers. States can go beyond the requirements set out in federal regulations for oversight. For example, Idaho’s SBM stated that its online platform requires multi-factor authorization and only consumers can add an agent to their account. Massachusetts’s SBM does not use brokers nor does it permit EDEs to enroll consumers. California’s SBM requires that agents be specifically added by the consumer through their consumer portal (or consent can be verified through a three-way call), and consumers can edit and remove permissions on that portal.

Some states have been proactive in law enforcement actions related to Marketplace agent and broker fraud. For example, Massachusetts and California took action related to fraudulent Marketplace enrollments concerning a scheme involving substance use disorder treatment centers a few years ago. Although there have been allegations of Marketplace broker fraud in Florida in recent years, information on recent enforcement activity by the state is not available.

5. Final regulation and pending legislation introduce new paperwork and other enrollment requirements for Marketplace consumers but make few changes to broker oversight.

In the final Marketplace Integrity and Affordability rule, released on June 20, 2025, CMS says that Marketplace fraud occurred due to the widespread availability of zero-dollar out-of-pocket premium plans following the implementation of enhanced premium tax credits and enrollment policy changes during the Biden administration. The final regulation introduces many significant changes to Marketplace enrollment standards, verification processes, and documentation requirements. Some of these changes apply to both the federal Marketplace and state-based marketplaces and many will expire at the end of the 2026 plan year. The federal budget reconciliation bill passed by the House in May 2025 and currently working its way through the Senate, if enacted, would codify many of the provisions in the final regulation (without an expiration date) and includes additional enrollment changes.

The final regulation addresses concerns about fraud in the Marketplace primarily by implementing stricter consumer-facing verification and eligibility procedures and by limiting enrollment opportunities. Some examples of these procedures include:

- Requiring Marketplaces to generate a data matching inconsistency (DMI) if a consumer estimates that their income will be between 100% and 400% of the FPL (between $15,650 and $62,600 for a single person in 2025), but IRS data or other data sources show their past income was below 100% of the FPL.

- No longer requiring Marketplaces to accept an applicant’s or enrollee’s estimate of projected household income when tax return data is unavailable. Under the regulation, Marketplaces will be required to confirm income with other data sources and require that applicants submit documentation that confirms their income.

- Requiring consumers in FFM states who are automatically re-enrolled in a $0-premium plan (because tax credits fully cover their premium) to confirm or update their eligibility during Open Enrollment or face a $5 monthly charge.

- Removing the low-income SEP that allows low-income consumers to enroll in a Marketplace plan during the year if their estimated income is no more than 150% of the FPL ($23,475 for a single person in 2025).

- Shortening the Open Enrollment period so that, for all Marketplaces, Open Enrollment must begin no later than November 1 and end no later than December 31.

Note that all of these provisions are scheduled to expire at the end of plan year 2026, except for the provision on Open Enrollment periods.

Although there are several overlapping provisions in the final regulation and the budget reconciliation legislation, the legislation contains several additional provisions related to eligibility and enrollment (many of which do not expire). For example, the legislation would:

- Establish a new pre-enrollment verification process that begins on August 1 for the coming plan year, requiring consumers to verify specific information. Consumers would still be permitted to enroll in a health plan while awaiting confirmation of eligibility, but they would not receive APTCs or CSRs until after their eligibility is verified.

- Essentially end the ability of Marketplaces to automatically re-enroll consumers in the same coverage they had in the prior year.

- Remove APTC repayment limits and require all enrollees, including those with low incomes, to repay the entirety of any excess premium tax credits that were paid to their insurer.

See this KFF analysis for additional details on the ACA-related provisions in the House-passed budget reconciliation bill and the draft Senate bill.

Changes include few reforms to agent and broker oversight. There is only one provision in the final rule that specifically addresses agents and brokers. The final regulation clarifies the standard that CMS must prove to terminate a broker contract as the “preponderance of the evidence” standard of proof. The rule defines “preponderance of the evidence” as proof by evidence that, when compared to opposing evidence, leads to the conclusion that the fact at issue is more likely true than not. This provision appears to be aimed at providing more transparency to agents and brokers about the standard the government will use to determine whether they have breached their contract with CMS or other standards of conduct agents and brokers are required to meet. No reforms to broker and agent oversight are included in the budget reconciliation legislation.