New Regulations Broadening Employer Exemptions to Contraceptive Coverage: Impact on Women

Issue Brief

The Trump Administration has finalized regulations that significantly broaden employers’ ability to be exempt from the Affordable Care Act’s (ACA) contraceptive coverage requirement. The regulations open the door for any employer or college/ university with a student health plan with objections to contraceptive coverage based on religious beliefs to qualify for an exemption. Any employer, except publicly traded corporations, with moral objections to contraception also qualify for an exemption. Their female employees, dependents, and students will no longer be entitled to coverage for the full range of FDA approved contraceptives at no cost.

These final regulations are very similar to the October 2017 Interim Final Regulations that were issued without an opportunity for public notice and comment, as required under the Administrative Procedure Act. Four nonprofit advocacy groups and 8 states filed lawsuits challenging those regulations. In the cases led by California and Pennsylvania, the federal courts issued preliminary injunctions in December 2017, blocking the enforcement of these regulations pending the outcome of the litigation. These decisions have been appealed to the 3rd and 9th Circuit Courts of Appeal.1 The status of these lawsuits is unclear now that the final regulations have been published. In any event, it is likely that there will be new legal challenges to the final regulations.

On November 15, 2018, the Trump Administration issued final regulations greatly expanding the types of employers that may be exempt from the Affordable Care Act’s (ACA) contraceptive coverage requirement. These regulations are a significant departure from the Obama-era regulations that only granted an exception to houses of worship. One of the regulations allows nonprofit or for-profit employers with an objection to contraceptive coverage based on religious beliefs to qualify for an exemption and drop contraceptive coverage from their plans. The other regulation exempts all but publicly traded employers with moral objections to contraception from the requirement. These new policies, effective immediately, also apply to private institutions of higher education that issue student health plans. The immediate impact of these regulations on the number of women who are eligible for contraceptive coverage is unknown, but the new regulations open the door for many more employers to withhold contraceptive coverage from their plans.

Contraceptive coverage under the ACA has made access to the full range of contraceptive methods affordable to millions of women. This provision is part of a set of key preventive services that has been identified by the Health Resources and Services Administration (HRSA) for women that must be covered without cost-sharing. Since it was first issued in 2012, the contraceptive coverage provision has been controversial. While very popular with the public, with over 77% of women and 64% of men reporting support for no-cost contraceptive coverage, it has been the focus of litigation brought by religious employers, with two cases (Zubik v Burwell and Burwell v Hobby Lobby) reaching the Supreme Court. This brief explains the contraceptive coverage rule under the ACA, the impact it has had on coverage, and how the new regulations issued by the Trump Administration change the contraceptive coverage requirement for employers and affect women’s coverage.

How do the new regulations change contraceptive coverage requirements for employers?

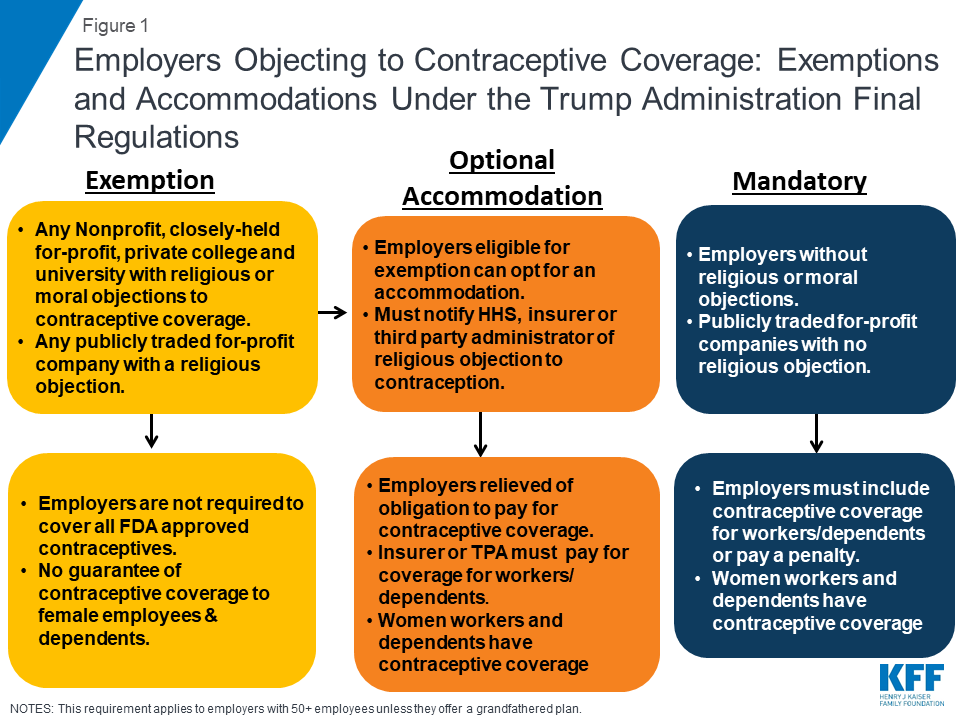

Since they were announced in 2011, the contraceptive coverage rules have evolved through litigation and new regulations. Most employers were required to include the coverage in their plans. Houses of worship could choose to be exempt from the requirement if they had religious objections. This exception meant that women workers and female dependents of exempt employers did not have guaranteed coverage for either some or all FDA approved contraceptive methods if their employer had an objection. Religiously- affiliated nonprofits and closely held for-profit corporations were not eligible for an exemption, but could choose an accommodation. This option was offered to religiously-affiliated nonprofit employers and then extended to closely held for-profits after the Supreme Court ruling in Burwell v. Hobby Lobby. The accommodation allowed these employers to opt out of providing and paying for contraceptive coverage in their plans by either notifying their insurer, third party administrator (TPA), or the federal government of their objection. The insurers were then responsible for covering the costs of contraception, which assured that their workers and dependents had contraceptive coverage while relieving the employers of the requirement to pay for it.

As of 2015, 10% of nonprofits with 5,000 or more employees had elected for an accommodation without challenging the requirement. This approach, however, has not been acceptable to all nonprofits with religious objections.2 In May 2016, the Supreme Court remanded Zubik v. Burwell, sending seven cases brought by religious nonprofits objecting to the contraceptive coverage accommodation back to the respective district Courts of Appeal. The Supreme Court instructed the parties to work together to “arrive at an approach going forward that accommodates petitioners’ religious exercise while at the same time ensuring that women covered by petitioners’ health plans receive full and equal health coverage, including contraceptive coverage.”3

On November 15, 2018, the Trump Administration issued final regulations that greatly expand eligibility for the exemption to all nonprofit and closely-held for-profit employers with objections to contraceptive coverage based on religious beliefs or moral convictions, including private institutions of higher education that issue student health plans (Figure 1). In addition, publicly traded for-profit companies with objections based on religious beliefs also qualify for an exemption. There is no guaranteed right of contraceptive coverage for their female employees and dependents or students. Table 1 presents the changes to the contraceptive coverage rule from the Obama Administration in the Final regulations issued by the Trump Administration.

The accommodation will be available to any employer now eligible for the exemption as well as employers that previously qualified for the accommodation. The federal agencies issuing the regulations posit that these new rules will have limited impact on the number of women losing contraceptive coverage. However, how many employers who were not eligible for either the exemption or accommodation under the old regulations will now seek an exemption is unknown, as is the number of employers previously utilizing the accommodation who will now opt for an exemption (resulting in the loss of contraceptive coverage for their employees and dependents). HHS estimates that the cost of losing contraception is $584 per woman per year.

The Trump Administration has stated that they do not believe it is feasible to resolve the religious objection of employers while still ensuring that the affected women receive full and equal health coverage that includes contraceptive coverage. Instead, the Administration suggests women could receive contraceptive services through Title X clinics or other governmental programs.

While many women who would lose contraceptive coverage because of employers’ religious and moral objections would not qualify for services under the current Title X regulations, on June 1, 2018, the Trump Administration issued Proposed Regulations for the Title X federal family program that would broaden the definition of the group of individuals who qualify for assistance under the program. The proposed regulation would broaden the definition of “low-income” (currently defined as income below 100% of the federal poverty level) to also include women who receive employer-sponsored insurance offered by an employer who does not cover contraceptives in their plan due to religious or moral objections. The revised definition of “low-income” would expand eligibility to this new group of women who do not meet the income guidelines but do not have contraceptive coverage to make them eligible receive services at Title X family planning clinics at no charge.

| Table 1: Summary of Changes in the Contraceptive Coverage Regulations for Objecting Entities | ||

| Obama AdministrationAugust 2012 to January 13, 2019* | Trump AdministrationEffective January 14, 2019 | |

| What types of contraceptives must plans cover withoutcost-sharing? | At least one of each of the 18 FDA approved contraceptive methods for women, as prescribed, along with counseling and related services must be covered without cost-sharing. | No change |

| Are any employers** “exempt” from the contraceptive mandate? | Religious institutions defined as “houses of worship.” Grandfathered plans. No notice to employees is required. Women workers and female dependents must pay for their own contraceptives. | Religious institutions defined as “houses of worship.” Grandfathered plans. Nonprofit or for-profit employers (including publicly traded companies), insurers, or private colleges or universities that issue student insurance plans with a religious objection to contraception. Nonprofit or closely held for-profit employers, insurers, or private colleges or universities that issue student insurance plans with a moral objection to contraception. Notice is only required if the plan previously included contraceptive coverage. Women workers and female dependents must pay for their own contraceptives. |

| Who pays for contraceptive coverage for employees of organizations receiving an exemption? | The cost of contraceptives is borne by women workers and female dependents. There is no guarantee of contraceptive coverage for employees of an exempt organization. The employer may choose to cover some methods, but has no obligation to cover all 18 FDA methods without cost sharing. | No change |

| What type of employers may seek an “accommodation” to avoid paying for contraceptives in their plans? | Closely held for-profit corporations and religiously affiliated nonprofits with religious objections to contraception can opt out of providing and paying for contraceptive coverage. Notice must be provided to either their insurer, third party administrator, or the federal government of their objection. Women workers and female dependents receive no cost contraceptive coverage. | Any entity eligible for an exemption can voluntarily choose the accommodation instead of the exemption. Notice must be provided to either their insurer, third party administrator, or the federal government of their objection. Women workers and female dependents receive no cost contraceptive coverage. |

| Who pays for contraceptive coverage for employees of organizations receiving an accommodation? | Insurance companies of firms obtaining an accommodation must pay for contraceptive coverage. Third-party administrators (TPA) of self-funded health plans must cover the costs of contraceptives for employees. The costs of the benefit are offset by reductions in the fees the TPA pays to participate in the federal exchange. | No change |

| When can entities change from an accommodation to an exemption? | N/A | When an employer or private college or university currently using the accommodation opts for an exemption, the revocation of contraceptive coverage will be effective on the first day of the first plan year that begins 30 days after the date of the revocation or 60 days notice may be given in a summary of benefits statement. The issuer or third party administrator is responsible for providing the notice to the beneficiaries. |

| NOTES: *The Trump Administration issued Interim Final Regulations in October 2017 but two federal courts stayed the regulations in December 2017 while litigation proceeded. The Obama-era regulations have been in effect as the cases have been appealed.** The Trump Administration’s regulations extend the exemption to any employer, organization or sponsor that adopts a health plan established or maintained by an employer eligible for an exemption. | ||

How has the contraceptive coverage rule affected women?

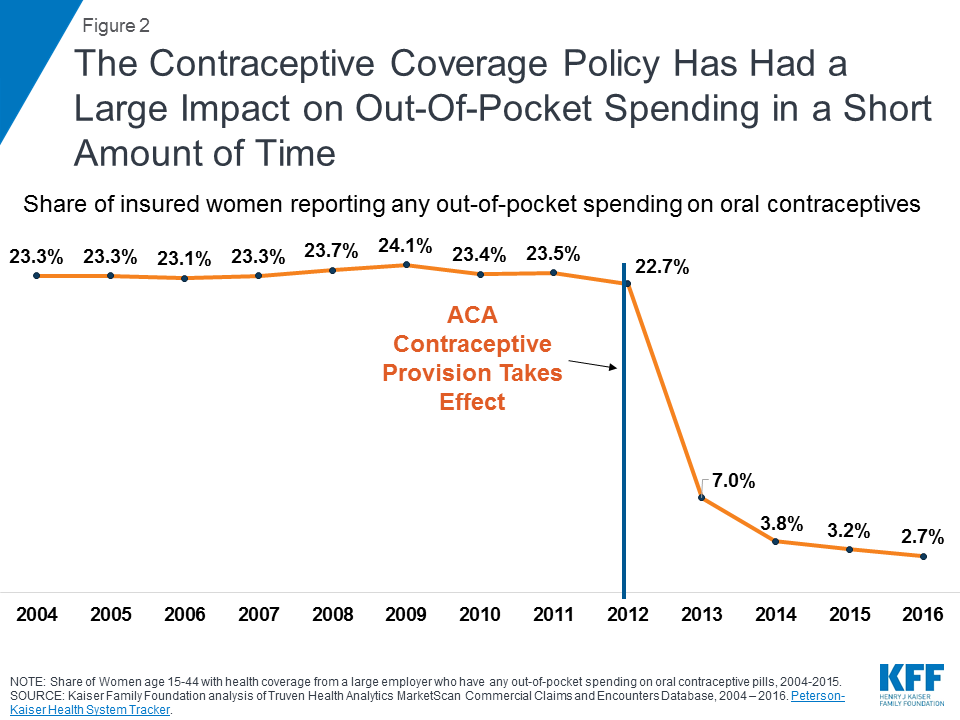

Contraceptive use among women is widespread, with over 99% of sexually-active women using at least one method at some point during their lifetime.4 Contraceptives make up an estimated 30-44% of out-of-pocket health care spending for women.5 Since the implementation of the ACA, out-of-pocket spending on oral contraceptive drugs has decreased dramatically (Figure 2).6 One study estimates that roughly $1.4 billion dollars per year in out-of-pocket savings on the pill resulted from the ACA’s contraceptive mandate.7 By 2013, most women had no out-of-pocket costs for their contraception, as median expenses for most contraceptive methods, including the IUD and the pill, dropped to zero.8

This provision has also influenced the decisions women make in their choice of method. After implementation of the ACA contraceptive coverage requirement, women were more likely to choose any method of prescription contraceptive, with a shift towards more effective long-term methods.9 High upfront costs of long-acting methods, such as the IUD and implant, had been a barrier to women who might otherwise prefer these more effective methods. When faced with no cost-sharing, women choose these methods more often,10 with significant implications for the rate of unintended pregnancy and associated costs of childbirth.11

Finally, decreases in cost-sharing were associated with better adherence and more consistent use of the pill. This was especially true among users of generic pills. One study showed that even copayments as low as $6 were associated with higher levels of discontinuation and non-adherence,12 increasing the risk of unintended pregnancy.

Do states with no-cost contraceptive coverage laws allow exemptions to objecting entities?

The federal standards under Affordable Care Act created a minimum set of preventive benefits that applied to most health plans regulated by the federal government (self-funded plans, federal employee plans) and states (individual, small and large group plans), including contraceptive coverage for women with no cost-sharing. States have also historically regulated insurance, and many have had mandated minimum benefits for decades. State laws, however, have more limited reach in that they only apply to state regulated fully insured plans and do not have jurisdiction over self-funded plans, where 61% of covered workers are insured.13 In self-funded plans, the employer assumes the risk of providing covered services and usually contracts with a third party administrator (TPA) to manage the claims payment process. These plans are overseen by the Federal Department of Labor under the Employer Retirement Income Security Act (ERISA) and are only subject to federally established regulations.14 The ACA sets a minimum standard of coverage for preventive services for all plans. However, state laws regulating insurance, including contraceptive coverage, can require fully insured plans to provide coverage beyond the federal standards.

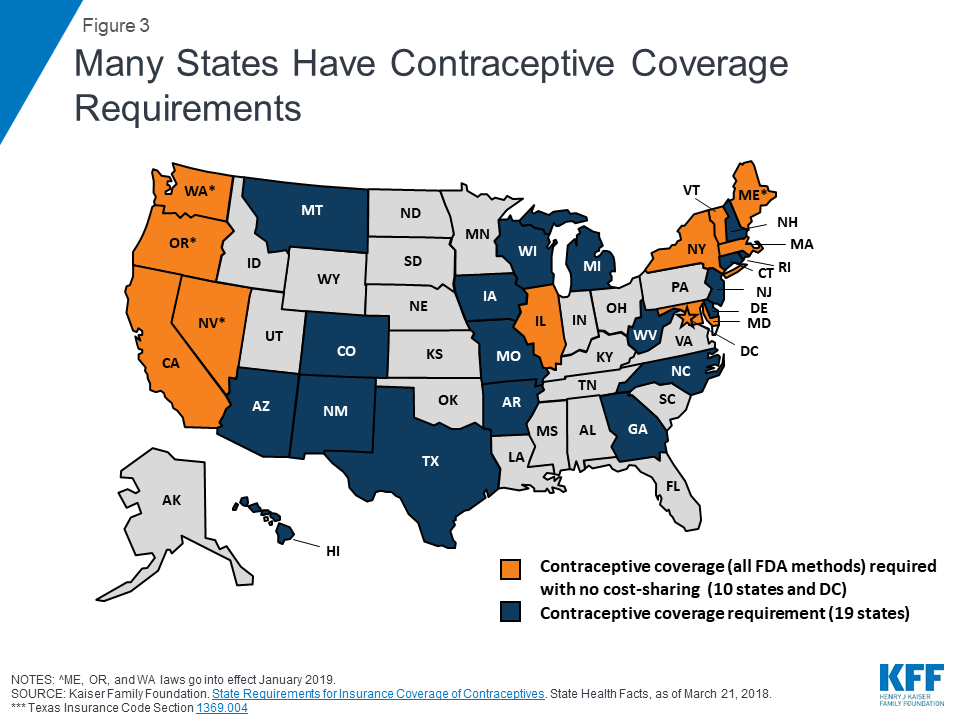

Ten states and DC have strengthened and expanded the federal contraceptive coverage requirement (CA, IL, ME, MD, MA, NV, NY, OR, VT, WA). Another 19 states have contraceptive equity laws that require plans to cover contraceptives if they also provide coverage for prescription drugs, but they do not necessarily require coverage of all FDA-approved contraceptives or ban cost-sharing (Figure 3).

Many of the 29 states that have passed contraceptive coverage laws (both equity and no-cost coverage) have a provision for exemptions, but the laws vary from state to state and only apply to fully insured plans. This means that there may be a conflict between the state and federal requirements when it comes to religious exemptions. In some states with a contraceptive coverage requirement, some employers who are eligible for an exemption under federal law will not qualify for an exemption under state law (Table 2). Employers in those states will have to have to meet the standards established by their state even though they may qualify for an exemption based on the new federal regulations.

| Table 2: State Requirements for No-Cost Contraceptive Coverage | |||||||

| StateDate Effective | Applies to | Coverage required without cost sharing | Exemptions allowed | ||||

| Private plans | Medicaid | With RX all FDA approved | OTC | Vasectomy | Religious | Moral | |

| California January 2015 | X | MCOs | X | Narrowly defined nonprofit religious employers | None | ||

| Illinois January 2017 | X | X | X-except male condoms | Any employer, or insurer with a religious objection | Any employer, or insurer with a moral objection | ||

| District of ColumbiaApril 2018 | X | X | X | X | ^ | None | |

| MaineJanuary 2019 | X | X | Narrowly defined nonprofit religious employers | None | |||

| MarylandJanuary 2018 | X | X | X | X | X | Religious organizations if the coverage conflicts with the organization’s bona fide religious beliefs and practices | None |

| MassachusettsMay 2018 | X | X | X | X-only Emergency Contraception | Narrowly defined nonprofit religious employers | None | |

| NevadaJanuary 2018 | X | X | X | Insurers affiliated with a religious organization | None | ||

| New YorkAugust 2017 | X | X | Narrowly defined nonprofit religious employers* | None | |||

| OregonJanuary 2019 | X | X | X | Narrowly defined nonprofit religious employers | None | ||

| VermontOctober 2016 | X | X-and all other public health assistance programs | X | X | None | None | |

| WashingtonJanuary 2019 | X | X | X | X | None | None | |

| NOTES: *Requires the insurer to offer a rider to policyholders so that women will have contraceptive coverage.^Mirroring the current federal regulations, DC allows for religiously affiliated nonprofits and closely held for-profits to request an accommodation which requires the group health insurer issuer to provide separate payments for contraceptive products and services without imposing any fee or cost-sharing to the employer or policy holders.SOURCE: Kaiser Family Foundation analysis of state laws and regulations. | |||||||

Conclusion

The Trump Administration’s new regulations substantially expand the exemption to nonprofit and for-profit employers, as well as to private colleges or universities with religious or moral objections to contraceptive coverage. It is unknown how many of these employers and colleges will maintain coverage through the accommodation as before and how many will now opt for the exemption leaving their students, employees and dependents without no-cost coverage for the full range of contraceptive methods. As a result of the new regulation, choices about coverage and cost-sharing will be made by employers and private colleges and universities that issue student plans. For many women, their employers will determine whether they have no-cost coverage to the full range of FDA approved methods. Their choice of contraceptive methods may again be limited by cost, placing some of the most effective yet costly methods out of financial reach.

Endnotes

- The Little Sisters of the Poor (LSOP), a religiously-affiliated nursing home that challenged the accommodation under the Obama Administration regulations, requested party status as an intervenor in both the PA and CA cases. The California Northern District Court granted the LSOP party status, the Pennsylvania Eastern District Court denied the LSOP request for party status. The LSOP have appealed the Pennsylvania Eastern District Court decision to deny them party status. The California Northern District Court also granted March for Life Education and Defense Fund, a nonprofit with moral objections to some contraceptive methods, party status. As parties in the case, the LSOP and March for Life Education and Defense Fund have appealed the California Northern District Court decision issuing the preliminary injunction. ↩︎

- Sobel L, Rae M, and Salganicoff A. Data Note: Are Nonprofits Requesting an Accommodation for Contraceptive Coverage?. Kaiser Family Foundation. December 1, 2016. ↩︎

- Supreme Court of the United States, per curium opinion, Zubik v. Burwell, May 16, 2016, page 4. ↩︎

- Guttmacher Institute. Contraceptive Use in the United States. September 2016. ↩︎

- Becker NV and Polsky D. Women Saw Large Decrease in Out-Of-Pocket Spending for Contraceptives After ACA Mandate Removed Cost Sharing. Health Affairs 34, no.7 (2015):1204-1211. doi: 10.1377/hlthaff.2015.0127 ↩︎

- Cox C, Damico A, Claxton G, Levitt L. Peterson-Kaiser Health System Tracker: Examining High Prescription Drug Spending for People with Employer-Sponsored Health Insurance. Kaiser Family Foundation. October 27, 2016. ↩︎

- Becker NV and Polsky D. Women Saw Large Decrease in Out-Of-Pocket Spending for Contraceptives After ACA Mandate Removed Cost Sharing. Health Affairs 34, no.7 (2015):1204-1211. doi: 10.1377/hlthaff.2015.0127 ↩︎

- Sonfield A, Tapales A, Jones RK, and Finer LB. Impact of the federal contraceptive coverage guarantee on out-of-pocket payments for contraceptives: 2014 update. Contraception 91 (2015) 44-48. ↩︎

- Carlin CS, Fertig AR, and Dowd BE. Affordable Care Act’s Mandate Eliminating Contraceptive Cost Sharing Influenced Choices of Women with Employer Coverage. Health Affairs 35, no.9 (2016):1608-1615. doi: 10.1377/hlthaff.2015.1457 ↩︎

- Birgisson NE, Zhao Q, Secura GM, Madden T, Peipert JF. Preventing Unintended Pregnancy: The Contraceptive CHOICE Project in Review. J Womens Health (Larchmt). 2015 May;24(5):349-53. ↩︎

- Ibid. ↩︎

- Pace LE, Dusetzina SB and Keating NL. Early Impact of the Affordable Care Act On Oral Contraceptive Cost Sharing, Discontinuation, And Nonadherence. Health Affairs 35, no.9 (2016):1616-1624; doi: 10.1377/hlthaff.2015.1624 ↩︎

- Kaiser Family Foundation. 2016 Employer Health Benefits Survey. September 14, 2016. ↩︎

- Guttmacher Institute. State Policies in Brief: Insurance Coverage of Contraceptives. As of August 1, 2017. ↩︎