The Coverage Provisions in the Affordable Care Act: An Update

Introduction

The enactment of the Affordable Care Act (ACA) on March 23, 2010 ushered in sweeping changes to the U.S. health care system. While the law touched almost every aspect of our health care system, from how coverage is obtained to how the health care services are provided, the parts of the law that have garnered the most attention, and generated the most controversy, are those relating to the availability and affordability of health insurance coverage. The coverage provisions in the law were aimed at improving access to insurance, especially for those with pre-existing medical conditions, enhancing the quality of coverage by imposing minimum benefit standards, and increasing the affordability of coverage through expanded public programs and new subsidies for private coverage. This brief examines these coverage provisions, providing an update on how they have been implemented and assessing their impact. It also discusses key issues looking ahead.

Framework of the ACA

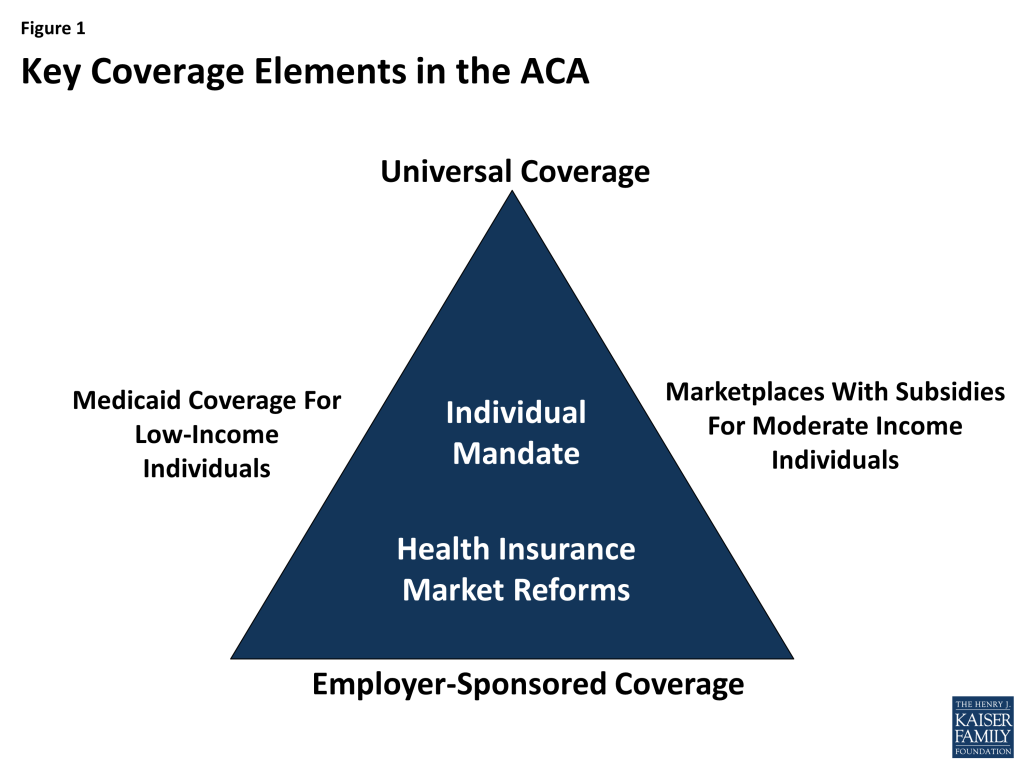

Like previous attempts at health care reform, the ACA was structured to address the gaps and limitations of our public-private health insurance system. It builds on employer-based coverage, restructures the individual insurance market, and broadens access to and affordability of coverage by expanding Medicaid for the low-income population and extending tax subsidies for the purchase of private insurance to those with moderate incomes (Figure 1).

As enacted, the ACA created a framework for enhancing access to health coverage. It imposed new regulations on health plans in the individual and small group markets, including guarantee issue and rate restrictions, to ensure everyone could purchase coverage regardless of their health status. In addition, the law created state-based health insurance Marketplaces through which individuals would be able to purchase private insurance coverage with premium and cost-sharing assistance on a sliding scale for those individuals and families with income between 100% and 400% of the federal poverty level (FPL, $11,770-$47,080 for an individual in 2015). These Marketplaces were to be established by the states; however, the law provided for the federal government to establish a Marketplace in any state that chose not to run its own. For the low-income population, Medicaid coverage was extended to all adults with income at or below 138% FPL. The law also imposed new requirements on individuals to purchase insurance, with some exceptions, and large employers to offer insurance to their employees.

The ACA relies heavily on states to implement the coverage provisions in the law. While some provisions went into effect without state action, many others were influenced by state decisions. For example, states were given responsibility for defining the set of benefits that would be offered by all plans in the individual and small group markets. They were permitted to impose tighter restrictions on insurance companies in some areas, such as premium rating. They were also provided the option of establishing a state-run Marketplace, and with the Supreme Court ruling in June 2012, states were given the choice whether or not to adopt the Medicaid expansion. These decisions have had important implications not only on the cost of coverage available in the states, but also on the number of people who have newly gained coverage as a result of the ACA. Consequently, as it did prior to implementation of the ACA, health insurance coverage continues to look different across the states.

Issue Brief: Health Insurance Market Reforms

Consumer Protections

On September 23, 2010, a number of ACA provisions took effect, including the elimination of lifetime limits on coverage, restrictions on annual limits on coverage, prohibition on rescinding coverage except in cases of fraud, and the elimination of pre-existing condition exclusions for children. These early market reforms were intended to provide immediate relief to consumers, especially those with high health care needs, who faced limits on coverage or the potential loss of coverage. Other ACA provisions that took effect six months after enactment included protections allowing consumers the right to choose their own doctors, the right to appeal health plan decisions, and the right to access out-of-network emergency care.1

All individual and group health plans must provide coverage to any applicant, regardless of health status, gender, or any other factors.2 Prior to the ACA, insurers in the individual market were allowed to deny people coverage based on their perceived health risk. As a result, those without access to employer-sponsored insurance who had acute or chronic health conditions, such as cancer or diabetes, were often unable to purchase coverage. Even women, especially those of childbearing age, could be denied coverage because of their expected higher use of health care services. The ACA required guaranteed issue and renewability of coverage and prohibited insurers from imposing pre-existing condition exclusions on coverage. These provisions went into effect on January 1, 2014. Prior to the implementation of the guaranteed issue requirement, the ACA created the temporary Pre-Existing Condition Insurance Plan for those who had been denied coverage and who had been uninsured for at least six months. While this program provide stopgap coverage for some, the coverage was unaffordable for many.

On January 1, 2014, new premium rating rules went into effect for plans in the individual and small group markets.3 These rules prohibit insurers from adjusting premiums based on a person’s health status. Insurers may only adjust premiums based on the following factors:

- Individual versus family enrollment: insurers may vary rates based on the number of family members enrolled in the plan.

- Geography: insurers may charge different rates in different areas across the state.

- Age: insurers may charge older adults more than younger adults; however, the variation in premiums is limited to 3 to 1, meaning insurers can’t charge older adults more than three times what they charge younger adults.

- Tobacco use: insurers may charge tobacco users up to 1.5 times what they charge those who do not use tobacco products.

To ease the transition to the new market reforms, the ACA exempted certain plans from some of the new health insurance requirements. These plans, referred to as grandfathered plans, are plans that were in place as of March 23, 2010 (the day the ACA was enacted) and have undergone minimal changes over time. To maintain grandfathered status, plans must not eliminate benefits to diagnose or treat a condition; increase cost sharing beyond certain specified limits; or reduce the employer share of the premium by more than five percentage points.4 Grandfathered plans are exempt from some of the new insurance market rules, including those relating to essential health benefits, the provision of preventive services with no cost-sharing, and review of premium increases of 10% or more.5 They must, however, extend coverage to dependents up to age 26 and eliminate lifetime and annual limits on coverage. In addition, grandfathered group plans can no longer impose pre-existing condition exclusions on children or adults. According the Kaiser/HRET 2014 Employer Health Benefits Survey, 26% of covered workers were enrolled in grandfathered plans in 2014, down from 36% in 2013.6

All group and individual health plans must provide a uniform summary of benefits and coverage (SBC) to applicants and enrollees. The ACA requires insurers and health plans to provide consumers with standardized and easy-to-read information about the plan using a common form that is intended to make it easier for consumers to compare plans. The SBC must describe the main features of the plan, including covered benefits along with any limitations or exclusions, cost sharing requirements, and whether it meets minimum essential coverage and value standards. The SBC must also include examples of how the policy or plan would cover care for certain health conditions or scenarios, showing hypothetical costs for consumers and how much the plan would pay. Currently, the form shows coverage examples for a normal delivery and managing type 2 diabetes. Finally, the SBC includes uniform definitions of common insurance-related terms. A recently released proposed rule would make some changes to the SBC effective for plan years and open enrollment periods beginning after September 1, 2015.7

Coverage of Preventive Services

Private health insurance plans generally must provide coverage for a range of preventive health services without requiring any patient cost-sharing (co-payments, deductibles, or co-insurance). These rules apply to all private plans, including individual, small group, large group, and self-insured plans, though grandfathered plans are exempt from this requirement.8 The list of required preventive services may be divided into three broad categories:

- Evidence-based services rated A or B by the U.S. Preventive Services Task Force (USPSTF).

- Routine Immunizations recommended by the Advisory Committee on Immunization Practices, which include coverage for both adult and child immunizations such as influenza, meningitis, hepatitis A and B, human papillomavirus (HPV), measles, mumps, rubella, and varicella (chicken pox).

- Preventive services for children and youth recommended by the Health Resources and Services Administration’s Bright Futures Project, including immunizations, behavioral and development assessments, and screening for autism, vision and hearing impairment, tuberculosis, and certain genetic diseases.

Private health insurance plans generally must provide coverage for an additional set of preventive health services for women without cost-sharing requirements. These services include well-woman visits, all FDA-approved contraceptives, broader screening and counseling for sexually-transmitted infections, breastfeeding support and supplies, and domestic violence screening. Certain religious employers (houses of worship) are specifically exempt from the contraceptive coverage requirement and are not required to include coverage for contraceptives in their health plans. An accommodation was established for certain non-profit religious organizations that object to providing these services (such as religiously-affiliated hospitals or universities). Organizations that qualify for the accommodation do not have to arrange or pay for contraceptive coverage, but must instead send a form to HHS or their insurance company stating their objection to covering contraceptives. The insurance company then provides the coverage without cost-sharing.9 In June 2014, the Supreme Court held in the Burwell vs. Hobby Lobby decision that some closely-held for-profit corporations may also exclude contraceptive coverage from their health plans if their owners have sincerely held religious objections to this requirement.10 In response to the Court’s decision, the Obama Administration issued a proposed rule to expand the “accommodation” in place for non-profit organizations with religious objections to birth control services to closely-held for-profit companies.11

Approximately 76 million people (including almost 19 million children) have received no-cost coverage for preventive health services since the ACA preventive services coverage rules took effect.12 This coverage went into effect on September 23, 2010 for new individual and employer-based coverage (grandfathered plans are exempt). Despite the length of time the benefit has been in place, awareness of the coverage remains low.13

The ACA improves access to preventive services in Medicare and Medicaid. The ACA eliminates cost-sharing for certain Medicare covered preventive services (those recommended A or B by the USPSTF), waives the Medicare deductible for colorectal cancer screenings, and provides coverage for personalized prevention plan services, which include an annual health risk assessment. In Medicaid, the ACA provides states that offer coverage for recommended preventive services with no cost sharing a one percentage point increase in the Federal Medical Assistance Percentage (FMAP) for those services. As of January 30, 2014, ten states (California, Colorado, Hawaii, Kentucky, Nevada, New Jersey, New Hampshire, New York, Ohio, and Wisconsin) had submitted State Plan Amendments (SPA) to cover all required preventive services, and eight SPAs had been approved.14

Extension of Dependent Coverage to Young Adults

The ACA extends dependent coverage to young adults up to age 26 beginning in September 2010. This provision allows young adults to remain on their parents’ health plans until they turn 26. Young adults can qualify for this coverage even if they are no longer living with a parent, are not a dependent on a parent’s tax return, or are no longer a student. While it is difficult to assess the effect of this dependent coverage provision independent of other factors, analysis of data from the National Health Interview Survey indicates that 3.1 million young adults had gained coverage by December 2011.15

Controlling Premium Growth

Medical Loss Ratio (MLR) Requirements

The MLR provisions in the ACA limit the amount of premium dollars insurers can spend on administration, marketing, and profits. They require most health insurers in the small group and individual market to spend at least 80% of premiums on health care claims and quality improvement. Health insurers in the large group market face a higher standard and must spend at least 85% of premiums on health care claims and quality improvement. Insurers were required to begin reporting MLRs in August 2011. Insurers not meeting the thresholds must issue rebates to consumers annually, beginning in August 2012. In the case of employer-sponsored plans, in which the cost of the premium is shared between employers and employees, insurers must provide a rebate to employees that is proportionate to their share of the premium.16

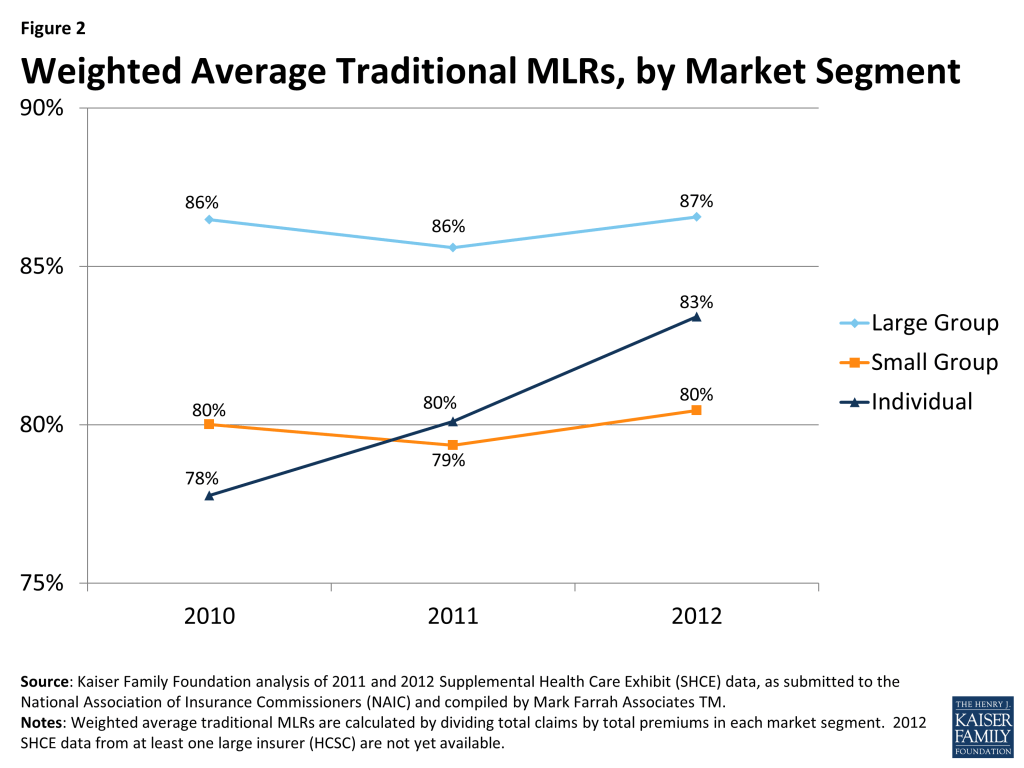

Insurers issued rebates totaling $519 million across all markets in August 2012 and $332 million in 2013. The drop in rebates in 2013 suggests that insurers were coming closer to meeting the MLR thresholds. Analysis of insurer data indicates this is the case. While most plans sold in the large and small group markets were already in compliance with the MLR requirements before the law went into effect, in the individual market, fewer than half of plans were in compliance. Since implementation of the law, the MRLs in this market have increased (Figure 2). The full impact of the MLR goes beyond just the rebates and includes the savings consumers experience from lower premiums than what would have been charged had the MLR provisions not been in place. While it is difficult to assess the full impact of the MLR provisions, an analysis by the Kaiser Family Foundation suggested that MLR savings to consumers totaled $1.2 billion in 2011 and $2.1 billion in 2012, with most of the savings resulting from lower premiums.17

Premium Rate Review

The ACA creates new standards for the review of premium rate increases proposed by insurers in the individual and small group markets to ensure the increases are based on accurate and verifiable data and are reasonable. While many states had rate review programs in place prior to the ACA, these programs were variable and set different standards for review. The ACA established minimum standards for an effective rate review program, permits federal regulators to review rates in states that do not have effective programs, and requires states or the federal government to review premium rate increases of 10% or more beginning September 2011. As of April 2014, 46 states and DC were deemed to have effective rate review programs in place. The five states without an effective program are Alabama, Missouri, Oklahoma, Texas, and Wyoming.18

An analysis of rate filings before and after the rate review requirements went into effect suggests these programs have had an impact on premiums. The premiums that went into effect in 2011 were, on average, 20% lower than the rates requested by insurers, though there were differences across states and markets.19 In addition, early evidence indicated that insurers were submitting fewer rate increases above the 10% threshold, and rate requests above the 10% threshold were more likely to be denied, reduced, or withdrawn following implementation of the new requirements in September 2011.

Risk Adjustment, Reinsurance, and Risk Corridors

The ACA includes three provisions designed to promote premium stability during the early years of ACA implementation. Changes in the insurance market—guarantee issue, rate restrictions and new subsidies available in the Marketplaces—make it easier for people with high health needs to purchase coverage. This possibility for adverse selection—when a disproportionate number of people with high health needs enroll in a plan—creates uncertainty for insurers. To encourage insurers to participate in the new Marketplaces and to compete on the basis of quality and value, rather than avoiding high risk enrollees, the ACA includes three premium stability programs: risk adjustment, reinsurance, and risk corridors, collectively known as the “three Rs”. Risk adjustment is a permanent program that transfers funds from insurers with lower risk enrollees to plans with higher risk enrollees. The temporary reinsurance program uses payments from all health insurance issuers and self-insured plans to partially offset the expenses for high-cost enrollees. The risk corridors program protects insurers against large losses by limiting insurers’ gains and losses beyond an allowable range.20 While the risk adjustment and reinsurance programs are required to be budget neutral, the risk corridor program is not. As a result, the risk corridor program has generated some controversy, with some critics characterizing the program as a bailout to insurers.

Health Plan Benefit Design

The ACA makes significant changes to health plan benefit design, setting uniform standards for covered benefits and cost sharing in the individual and small group markets. The ACA requires all non-grandfathered plans in the individual and small group markets, including those sold both inside and outside the Marketplaces, to cover ten categories of essential health benefits.21 These categories include:

- Ambulatory patient services

- Emergency services

- Hospitalization

- Maternity and newborn care

- Mental health and substance use disorders, including behavioral health treatment

- Prescription drugs

- Rehabilitative and habilitative services and devices

- Laboratory services

- Preventive and wellness services and chronic disease management

- Pediatric services, including vision and dental care

Rather than establish a uniform benefit package to be offered by all plans, regulatory guidance required states to select an EHB benchmark plan that would define the essential health benefits that must be offered by plans in the state. Any benefits covered by this benchmark plan would be considered an essential health benefit. In addition, any limits on amount, duration, and scope of benefits would be included in the definition of the EHB.22 States had to select the benchmark plan by December 26, 2012 from among the following ten plans operating in the state: the three largest small group plans, the three largest state employee health plans, the three largest federal employee health plan options, or the largest HMO offered in the state’s commercial market. If a state did not recommend a benchmark plan, the default benchmark was the largest small group plan in the state. The majority of states (45) selected or defaulted to a small group plan, while four chose the largest commercial HMO, and two selected a state employee plan.23

If a state’s EHB benchmark plan did not include services in all of the required benefit categories, states were required to identify supplemental coverage to complete their EHB benchmark packages. Except for habilitative services, the benchmark plan could be supplemented by adding benefits for any missing categories from another benchmark plan. For habilitative services, states had the option to define the services to be included in that category or, if they chose not to make that determination, insurers were required to provide parity with rehabilitative services or define which habilitative services to cover and report to HHS.

Special rules govern coverage for abortion services. Abortion services are explicitly excluded from the list of essential health benefits that all health insurance plans are required to offer. No health plan is required to cover abortion services. States may allow private insurers to offer a plan in their state Marketplace that includes coverage of abortions beyond what is allowed under federal law (to save the life of the woman and in cases of rape and incest); however, premium payments must be segregated into two separate accounts – one for the value of the abortion benefit and one for the value of all other services. States may also prohibit coverage for any abortions by all plans, and at least one plan within a state Marketplace must offer coverage that excludes abortions outside those permitted under federal law.24

Plans sold in the Marketplaces and in the individual and small group markets must also fit into one of four metal tiers defined by their actuarial value (AV), which is the share of health costs covered, on average, by the plan. The four metal tiers and their AV are:

- Bronze: 60% AV

- Silver: 70% AV

- Gold: 80% AV

- Platinum: 90% AV

Insurers have flexibility to alter the cost-sharing features within metal tiers, for example setting deductibles at different levels or applying copayments instead of coinsurance, as long as the overall AV of the plan meets the required percentage.25

The ACA establishes a limit on the amount of cost-sharing consumers can be expected to pay for services covered by the plan. Once this overall limit is met, the plan must cover 100% of remaining health care costs for the year. The maximum out-of-pocket limit for 2014 was set at $6,350 per individual and $12,700 per family. These limits increased to $6,600 per individual and $13,200 per family in 2015. The out-of-pocket limits are lower for those with incomes below 250% FPL who are eligible for cost-sharing reductions. They drop to $2,250 per individual and $4,500 per family for those with incomes 100-200% FPL and to $5,200 per individual and $10,400 per family for those with incomes 200-250% FPL.

While the goal of the benefit changes enacted by the ACA was to improve the adequacy of coverage offered to consumers, particularly in the individual market, many people have faced disruptions because their plans were canceled, either because the plans did not comply with the new ACA requirements or because insurers chose not to continue offering the plans. Estimates from the Urban Institute indicate that about 2.6 million people had their plans canceled because the plans did not meet the ACA requirements and another 840,000 had plans canceled for other reasons.26 Many consumers whose plans were canceled were able to find comparable coverage through the Marketplaces or in the individual market outside the Marketplaces, though some had to pay more for the coverage. According to the findings from the Kaiser Survey of Non-Group Health Insurance Enrollees, of respondents who switched from non-compliant to compliant plans, similar shares reported paying higher or lower premiums for the new coverage (39% vs. 46%). However, plan switchers were less likely to report being satisfied with the plan costs and less likely to perceive their coverage as a good value, perhaps because about half of plan switchers reported having their previous plan canceled.27

Issue Brief: Individual And Employer Requirements

Requirements for Individuals to Have Coverage

Individuals are required to have health coverage, with some exceptions. Beginning in 2014, the ACA requires individuals to have minimum essential coverage or pay a penalty.28 This requirement was included in the ACA to guard against the potential that young, healthy people would choose to forego insurance, referred to adverse selection. The penalty phases in over time. In 2014, the penalty was the greater of $95 (up to $285 for a family) or 1% of income. The penalty increases to the greater of $325 (up to $975 for a family) or 2% of income in 2015 and $695 (up to $2,085 for a family) or 2.5% of income in 2016.29 There are exemptions to the requirement, including for coverage that is not affordable (costs more than 8% of household income), for religious objections, for members of Indian tribes, for those with income below the tax filing threshold, and for short gaps in coverage of less than three consecutive months. Individuals can also claim hardship exemptions, including those with incomes below 138% FPL who live in states that did not adopt the Medicaid expansion.

Individuals will be required to report health coverage on their 2014 taxes. The individual mandate is enforced through the tax filing process. For the first time, tax filers must document that they had insurance coverage during the year when they file their 2014 taxes. If they did not and they do not qualify for one of the exemptions, they will be assessed a penalty in the form of an additional tax for the months in which they did not have health coverage. Those who were uninsured during 2014 can request certain exemptions when they file their taxes (e.g., for unaffordable coverage, short gaps in coverage, or member of an Indian tribe), while other exemptions must be obtained through the health insurance Marketplace (e.g., for hardship exemptions, religious objections). On February 20, 2015, HHS announced there would be a one-time special enrollment period allowing people who first learned of the penalty for not having insurance when they filed their taxes to enroll in coverage through the Marketplaces. This special enrollment period for the federal Marketplace will run from March 15, 2015 through April 30, 2015. Many states running their own Marketplaces have announced or are considering similar special enrollment periods.

The IRS estimates that roughly 30 million taxpayers who lacked coverage for some or all of the year will qualify for an exemption in 2014, while 3 to 6 million will owe a penalty for not having insurance. The IRS also estimates that 75% of 2014 taxpayers will have had minimum essential coverage for the entire year and so will be able to check a single box on their tax form indicating they complied with the individual shared responsibility requirement. Separately, the Congressional Budget Office (CBO) estimates that about four million people will pay a penalty for not having insurance in 2016, and approximately $4 billion in penalty payments will be collected that year.30

Employer Requirements

Beginning in 2015, large employers are required to provide coverage to full-time employees or face a penalty. In 2015, employers with 100 or more full-time equivalent employees will be assessed a fee up to $2,000 per full-time employee (in excess of 30 employees) if they do not offer coverage to at least 95% of full-time workers and their dependents (defined as children up to age 26; does not include spouses) and if they have at least one employee who receives a premium tax credit through a Marketplace. Final regulations issued by the IRS provide transition relief to these large employers in 2015: employers are only subject to the penalty if they do not offer affordable coverage to 70% of full-time workers; and the penalty payments is calculated as up to $2,000 per full-time employee minus up to 80 employees.31 These requirements go into effect for employers with 50-99 full-time equivalent employees in 2016. To avoid penalties, employers must offer insurance that pays for at least 60% of covered health care expenses, and the employee share of the premium must not exceed 9.5% of family income. This requirement does not apply to employers with fewer than 50 workers.

For purposes of employer mandate, full-time work is defined as 30 or more hours per week. Opponents of the law are critical of this definition of full-time worker, claiming it unduly burdens certain industries, such as retail and hospitality where part-time employment is more common, and provides disincentives to employers to hire full-time workers. Supporters argue changing the definition will lead to more people being shifted from full-time to part-time work. Proposals to change the definition of full-time from 30 hours per week to 40 hours per week will likely be debated in this Congress.

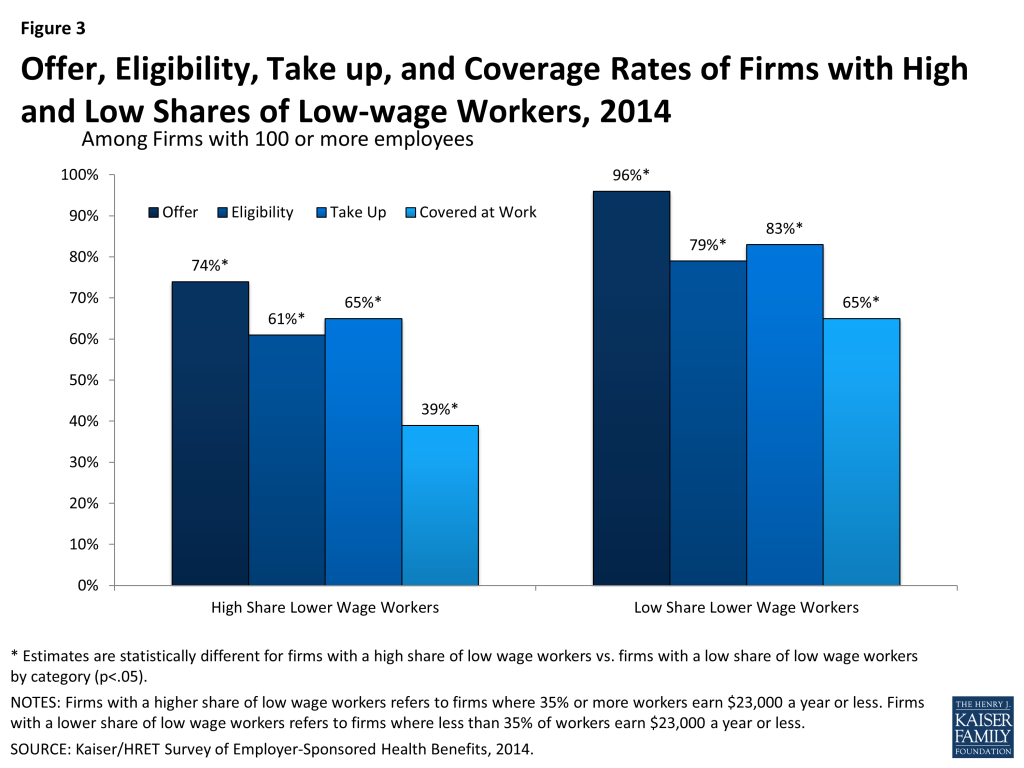

Firms with large shares of low-wage workers are less likely to offer health coverage, and as a result, may have more difficulty meeting the employer requirements. According to data from the Kaiser/HRET Survey of Employer-Sponsored Health Benefits, among firms with 100 or more employees where 35% or more of workers earn $23,000 a year or less, 74% offer health insurance to workers compared to 96% of firms with a low share of low-wage workers (Figure 3).32 In addition, fewer workers in firms with a large share of low-wage workers are eligible for coverage if it is offered (workers may not be eligible for coverage because of waiting periods or because they do not work enough hours per week).

Issue Brief: Expanding Coverage

Health Insurance Marketplaces

The ACA creates new health insurance Marketplaces (also referred to as Exchanges) where individuals and small businesses can purchase insurance. Marketplaces are designed to create a more organized and competitive market for health insurance by offering a choice of health plans, establishing common rules regarding the offering and pricing of insurance, and providing information to help consumers better understand the options available to them. The Marketplaces serve individuals and small businesses (the Marketplace for small businesses is called the Small Business Health Options Program (SHOP)). Coverage through the Marketplaces is available to nearly all U.S. citizens and legal resdients (undocumented immigrants and those who are incarcerated are not permitted to buy coverage in the Marketplaces), though financial assistance is only available to those meeting income and other requirements. Plans sold through the Marketplaces must meet certain standards and must be certified as Qualified Health Plans (QHPs).

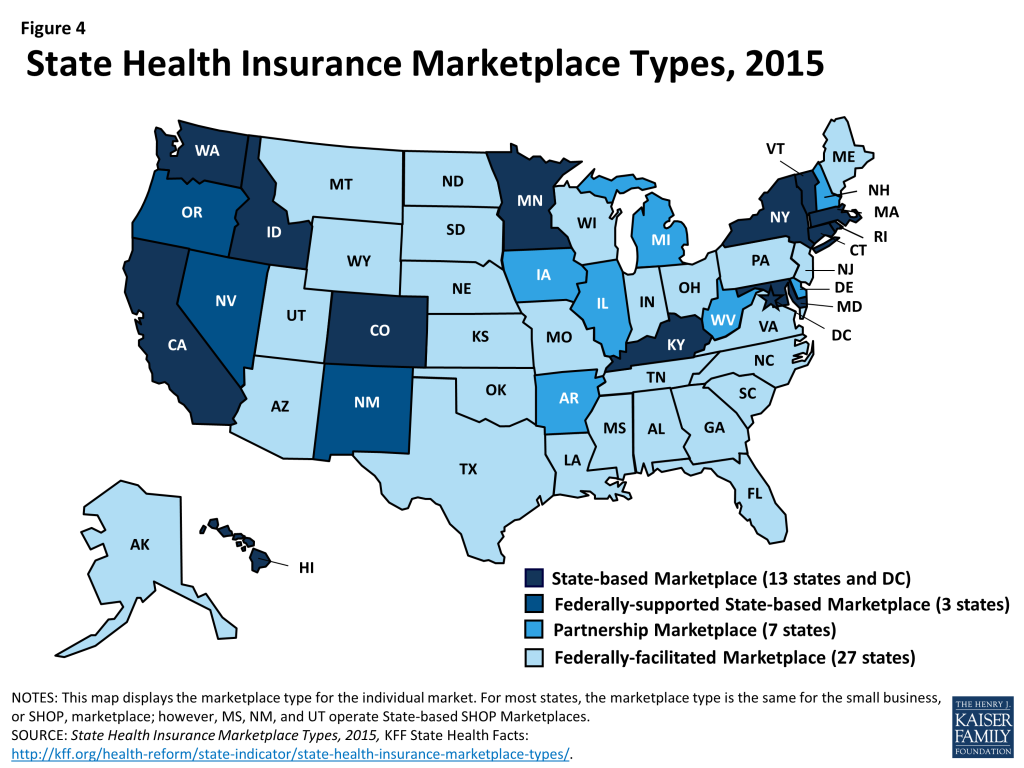

States approaches to the Marketplaces differ. The ACA envisioned that all states would implement State-based Marketplaces (SBMs); however, political opposition among Republican Governors and state legislatures led many states to opt for a Federally-facilitated Marketplace (FFM). Thirty-four states rely on a Marketplace fully run by the federal government, while seven states adopted a hybrid approach (a State-Partnership Marketplace) in which the states assume some Marketplace responsibilities, including plan management and consumer assistance. In all, 17 states have established SBMs, with 14 of these fully run the states. Three SBMs (Nevada, New Mexico, and Oregon) that struggled to establish functional websites through which consumers could apply for and enroll in coverage have chosen to use the federal healthcare.gov portal for 2015 (Figure 4).

To assist states in setting up the Marketplace, the ACA provided federal funding to states through Exchange Planning and Establishment grants. This funding was available to states through December 2014. Nearly $5 billion in funding was provided to states through these grants.33

One of the most significant challenge states and the federal government have faced in establishing the Marketplaces has been building the online portal or website through which individuals and small employers can apply for and enroll in coverage. Last year, healthcare.gov, the federal website, launched with nearly catastrophic problems. Many state websites also experienced problems and while many of these issues were resolved before the end of the open enrollment period, websites in several states never worked well and have since been scrapped. During the second open enrollment period, the federal website and most state websites were free of the serious problems encountered last year.

Health insurance Marketplaces were marked by volatility in first two years of operation. Most Marketplaces offered consumers a choice of plans in the first year, and premiums overall were lower than expected. In year two, new insurers entering Marketplaces in many states are enhancing competition and increasing consumer choice in those areas. However, decisions by some insurers to leave certain markets have left many consumers with the need to find new coverage and fewer coverage options.34 Overall, premium growth in 2015 was modest, but it masked large variation across states, from increases as large as 28% in Alaska and 18% in Minnesota to declines of 15% and 25% in Colorado and Mississippi, respectively.35 As insurers adjust their premium pricing strategies, some consumers are facing higher prices to remain in the same plan.

Premium Tax Credits and Cost Sharing Reductions

Premium tax credits and cost-sharing reductions are available through the Marketplaces to make coverage more affordable for qualifying individuals. Premium tax credits are available to U.S. citizens and legally residing immigrants who have income between 100% and 400% FPL and who do not have access to affordable coverage through an employer or public coverage (Medicaid, CHIP, or Medicare). Married consumers must file taxes jointly in order to qualify. The tax credits work by limiting the amount consumers must pay for coverage to a percentage of their income. In 2015, the required premium contributions range from 2.01% of income for those with income 100-133% FPL to 9.56% of income for those with incomes 300-400% FPL.36 The tax credit amounts are tied to the second-lowest cost Silver plan (the benchmark plan), though consumers may use these tax credits to purchase less or more expensive plans.

Cost sharing reductions are available to individuals eligible for premium tax credits with incomes between 100 and 250% FPL. The cost sharing reductions lower deductibles, copayments, and other out-of-pocket costs. They work by increasing the actuarial value of Silver level plans from 70% to 94% for those with incomes 100-150% FPL, 87% for those with incomes 150-200% FPL, and 73% for those with incomes 200-250% FPL. To take advantage of the cost sharing reductions, consumers must purchase a Silver plan.

Consumers who are eligible for tax credits may receive advance payment of those tax credits based on their projected income for the coverage year; however, they will need to reconcile receipt of the advance payments when they file their taxes. Consumers who received advance payment of premium tax credits in 2014 are reconciling those payments for the first time this year. Consumers who received payments that were too high based on their annual income for the year will be required to repay some or all of the excess payments. Limits are placed on repayment amounts for those with incomes less than 400% FPL. In addition, an exception is made to the repayment requirements for consumers who received advance payment of the tax credits during the year but whose income later fell below Medicaid eligibility levels, or below the poverty level, by the end of the year. These consumers are not required to repay the payments they received. Consumers who received payments that were too low based on their annual income will receive a refund.

Due to what is referred to as the family glitch, many working low-income families for whom the cost of family coverage through an employer is not affordable are not eligible to access subsidized coverage in the Marketplace. Under the ACA, premium tax credits in the Marketplaces are not available to those who have an affordable offer of coverage from their employer. An offer is considered affordable if the employee share of the premium for single coverage costs less than 9.5% of the employee’s income. This definition applies even if the employee needs to purchase family coverage that may cost more than 9.5% of income. Estimates suggest that as many as 3.9 million dependents are excluded from accessing premium tax credits that would lower their cost of coverage.37 While these dependents are exempt from any penalties related to not having insurance, without an affordable coverage option, many may forego insurance.

Cost sharing in Marketplace plans is high, but cost sharing subsidies meaningfully reduce the out-of-pocket burden for many low and modest-income consumers. In general, consumers enrolling in plans in the Marketplace face high out-of-pocket costs when they access health services. Overall, across the states using healthcare.gov, deductibles for Silver plans averaged $2,556 and the average out-of-pocket limit was $5,826. These amounts were reduced in plans that applied the cost sharing reductions (CSR plans). Deductibles averaged $2,077 in CSR73 plans, $737 in CSR87 plans, and $229 in CSR94 plans while out-of-pocket costs were capped on average at $4,624 in CSR73 plans, $1,692 in CSR87 plans, and $881 in CSR94 plans.38 Particularly for those eligible for CSR94 and CSR87 plans, these reductions in cost sharing amounts can help to alleviate the financial burden of accessing needed health care services.

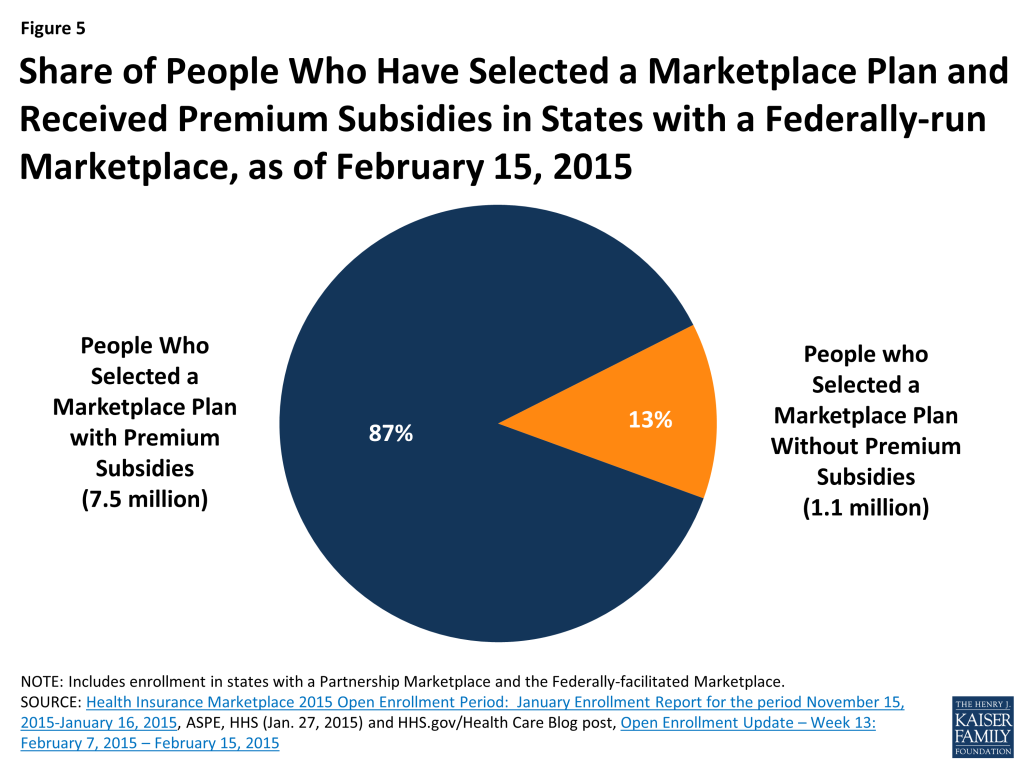

A decision in the case, King vs Burwell, currently before the Supreme Court, will determine whether the federal government has the authority to continue providing subsidies to consumers in states that do not have a state-run Marketplace. The plaintiffs in the case argue that a strict interpretation of the language of the ACA prohibits subsidies in states that do not have a Marketplace “established by the state.”39 A ruling for the plaintiffs in this case would invalidate premium tax credits and cost sharing reductions for consumers in the 34 states that rely on the Federal Marketplace or operate a Partnership Marketplace. Subsidies in the three SBM states that rely on the healthcare.gov web portal may also be at risk. As of February 15, 2015, there were over 7.5 million people in the 34 states whose subsidies could be at risk. A ruling by the Court in this case is expected in June 2015 (Figure 5).

Basic Health Program

To date, only Minnesota has adopted the Basic Health Program (BHP) option, which allows states to create an alternative coverage program for adults with income between 133 and 200% FPL who would otherwise be eligible for coverage through the Marketplace. The BHP provides states with the option of offering coverage that is more affordable and/or more comprehensive than what would be available to consumers in the Marketplaces. States have flexibility in designing this coverage, but it must be at least as comprehensive and affordable as subsidized coverage in the Marketplaces. To finance the BHP, the federal government pays states 95% of what BHP enrollees would have received in Marketplace subsidies.40 States can implement BHP beginning in 2015. So far, only states that offered more comprehensive Medicaid coverage prior to the ACA are considering adopting the BHP.

Outreach and Enrollment

Marketplaces are required to establish and finance Navigator programs to conduct outreach and provide enrollment assistance to consumers. According to a survey of assister programs nationwide, a total of 28,000 assisters provided enrollment assistance to over 10 million consumers during the 2014 open enrollment period.41 These assisters have proven instrumental in educating consumers with limited experience purchasing private insurance and who face challenges, such as language barriers and lack of access to the internet, to applying for and enrolling in coverage. While states running their own Marketplaces have been able to use federal grant funds to support robust assister programs during the first two years, support for Navigators in FFM states has been more limited.42 Future funding for assisters is a concern in both state Marketplaces and the FFM.

At the end of the first open enrollment period, over eight million people had selected a Marketplace plan. Despite a slow start to enrollment due to website problems that hindered early enrollment, a surge in sign-ups during the last two weeks of the open enrollment period pushed enrollment above eight million. By October, 6.7 million people were enrolled and paying premiums, a fall-off that was somewhat expected as people’s situations changed and difficulties arose in paying premiums.

As of February 15, 2015, over 11.6 million people had signed up for coverage through the Marketplaces. While the second open enrollment period officially ended on February 15, 2015, extensions were granted in many states for those who were “in line” on the closing date. As a result, the total number of people signing up for coverage in 2015 will increase. Based on the preliminary enrollment data from states using healthcare.gov, about 52% of those enrolling in coverage in 2015 were new to the Marketplace, while 42% renewed their coverage from 2014. Less than half of consumers renewing coverage were automatically reenrolled in their current plan, while 53% of renewing consumers returned to the Marketplace and selected a new plan.43

Medicaid Expansion

The ACA sought to fill one of the most notable gaps in Medicaid’s role as a source of coverage for the low-income population— the exclusion of adults without dependent children no matter how poor, unless a state obtained a waiver to provide them coverage (and few states had such waivers). The ACA intended to remove the categorical eligibility requirements for Medicaid coverage stemming from its welfare heritage and convert Medicaid coverage to be based on income— establishing a national minimum income eligibility level effectively at 138% FPL in all states. This standard would apply mostly to adults as all states cover children to substantially higher levels through Medicaid and CHIP with median eligibility at 255% of poverty. The expansion population is 100% federally financed in 2014-2016 with the federal match phasing down to 90% in 2020 and thereafter. Consistent with previous Medicaid policy, undocumented and recent lawfully present immigrants remain excluded from enrolling in coverage.

As enacted, the ACA expanded Medicaid eligibility to adults with income at or below 138% FPL, although this core provision was effectively made a state option by the Supreme Court’s 2012 ruling on the ACA. However, other eligibility changes in the law were unaffected by the Court’s decision, including establishing a new minimum coverage level of 138% FPL for children of all ages in Medicaid, helping to align Medicaid coverage across children. The ACA also changed the method for determining financial eligibility for Medicaid for children, pregnant women, parents, and adults and CHIP to a standard based on modified-adjusted gross income (MAGI). This new approach, effective January 1, 2014, is intended to prevent gaps in coverage between programs by aligning with the method for determining eligibility for subsidies to purchase Marketplace coverage.

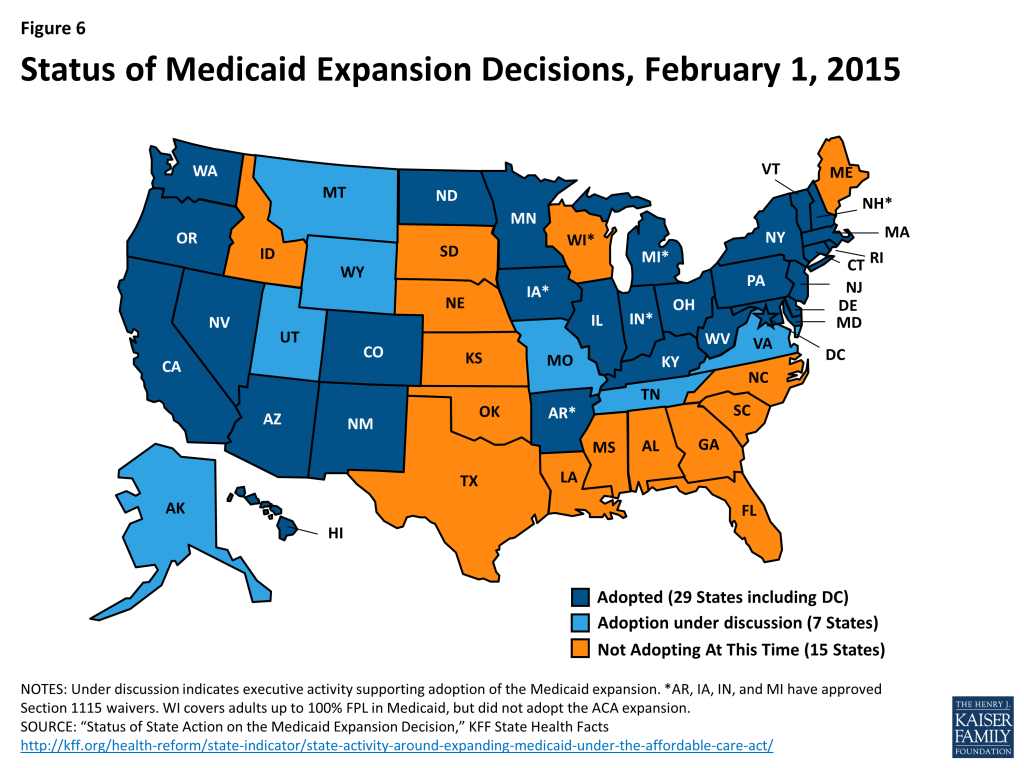

As of February 2015, 29 states and the District of Columbia have implemented the Medicaid expansion to low-income adults (Figure 6). Most states expanded Medicaid consistent with federal rules and options provided under the ACA, but five states (Arkansas, Iowa, Indiana, Michigan, and Pennsylvania) obtained Section 1115 waivers to implement the expansion in ways that extend beyond the flexibility provided by the law (the Governor of Pennsylvania recently announced the state would not proceed with implementing the waiver, but would instead expand Medicaid through the State Plan Amendment process).44 Notably, Arkansas has implemented the expansion with a waiver that allows it to implement a mandatory premium assistance program where the state enrolls the expansion population into QHPs in the Marketplace. Other states have used waivers to impose premiums for individuals with incomes between 100 and 138% FPL or to add healthy behavior incentives to coverage.

Medicaid Coverage Gap

Large gaps in coverage persist for parents and other low-income adults in the 22 states that have not yet expanded Medicaid since Medicaid eligibility levels for parents remain very low and childless adults remain ineligible for full Medicaid benefits in all but one of the non-expansion states. Among the non-expansion states, the median eligibility level is 46% FPL for parents and 0% for other adults, compared to 138% FPL for parents and adults in expansion states.

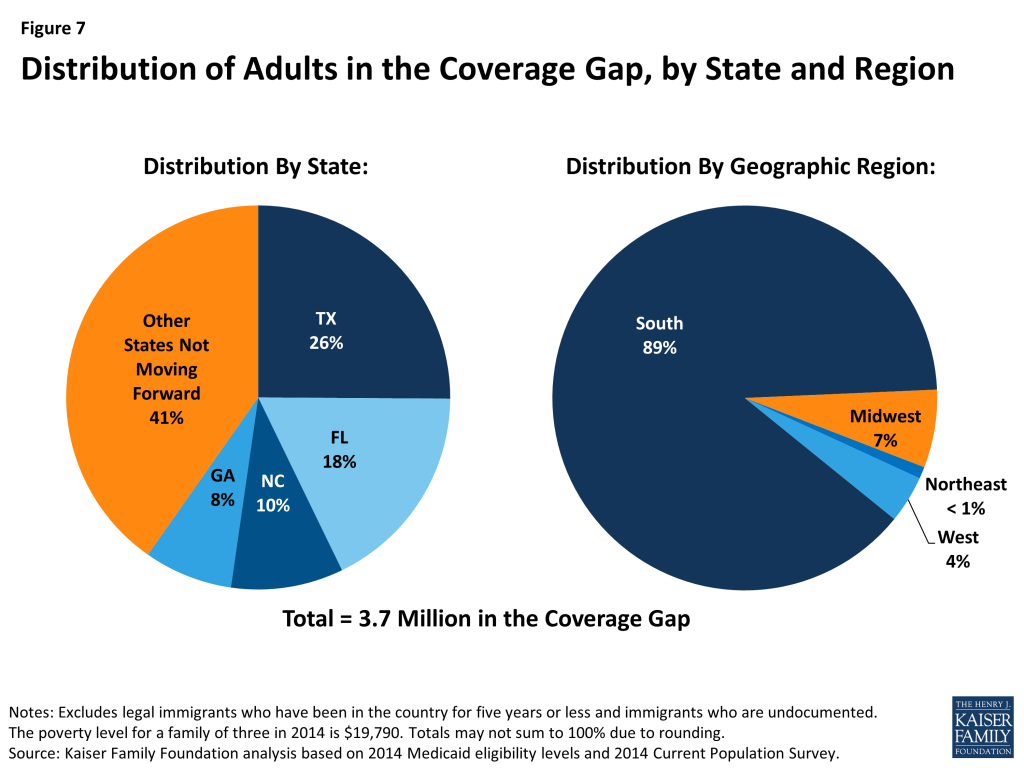

As a result of these limited eligibility levels, 3.7 million poor uninsured adults fall into a coverage gap because they earn too much to qualify for Medicaid and too little to qualify for subsidies for Marketplace coverage, which begin at 100% FPL.45 Because the ACA was enacted assuming the Medicaid expansion would go forward in all states and everyone below the poverty level would be covered, the law only provided access to subsidies through the Marketplace for individuals above the poverty level up to 400% FPL. Thus, those individuals between 100-138% FPL, who would have been covered by Medicaid if the state expanded, are able to access subsidized coverage in the Marketplace but those below poverty are ineligible for subsidies. Of the 3.7 million adults in the coverage gap, nearly 90% live in the south and over half are Black or Hispanic (Figure 7).

Even in states that do expand Medicaid, undocumented immigrants and many recent lawfully present immigrants will remain ineligible. Because many uninsured non-citizens are in low-income working families, many are in the income range to qualify for the ACA Medicaid expansion. However, under federal rules, undocumented immigrants may not enroll in Medicaid. Many lawfully present non-citizens who would otherwise be eligible for Medicaid remain subject to a five-year waiting period before they may enroll, and some groups of lawfully present immigrants remain ineligible regardless of their length of time in the country.

Medicaid Enrollment

Medicaid enrollment has grown under the ACA. Enrollment data show that as of December 2014, Medicaid and CHIP enrollment has grown by over 10.7 million since the period just prior to the beginning of the initial open enrollment period for the Marketplaces in October 2013.46 This change represents an 18.6% increase in enrollment over the period across all states. Enrollment increases were higher (27%) among states that chose to expand Medicaid eligibility under the ACA, compared to states that had not expanded (7%), suggesting that the Medicaid expansion is contributing to greater enrollment growth. However, some who are eligible remain unenrolled due to limited awareness about the Medicaid program and their eligibility or other enrollment challenges.

Streamlining Application and Enrollment Processes

The ACA also enacted sweeping changes to streamline and modernize application, enrollment, and renewal processes in Medicaid and CHIP and coordinate with the Marketplaces which all states must implement regardless of their Medicaid expansion decisions. Together these processes are intended to achieve the ACA’s vision to provide “no wrong door” access to all health coverage options, minimize the paperwork burden on consumers and state agencies, and enhance the consumer experience.47 States must provide multiple options for individuals to apply for health coverage, including online, by phone, by mail, and in person, using a single streamlined application for Medicaid, CHIP, and Marketplace coverage. In addition, states must seek to rely on electronic data to verify eligibility criteria and renew coverage.

Impact on the Uninsured

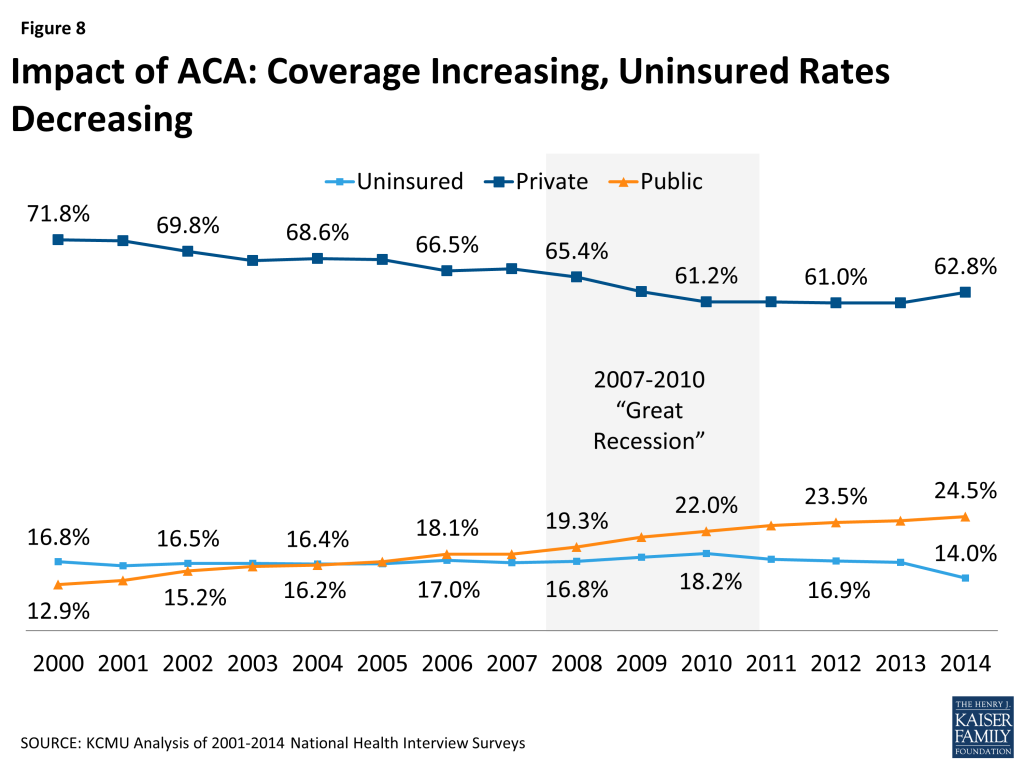

New coverage options available through the ACA have resulted in many uninsured gaining coverage. Increased coverage through employers, the Marketplaces, and Medicaid is bringing down the uninsured rate. Data from the National Health Interview Survey shows a drop in the uninsured rate among the non-elderly from 16.6% in 2013 to 14.0% in the second quarter of 2014, with the most significant decline for the low-income and minority uninsured population (Figure 8).48 In addition, a survey by the Kaiser Family Foundation indicates 11 million uninsured adults gained coverage in 2014.49 Other poll data show similar results.

The uninsured rate is dropping more precipitously in states that have embraced the ACA’s coverage expansions. Data from the National Health Interview Survey indicate that there was a greater decline in the uninsured rate in states that are expanding Medicaid. Among states adopting the Medicaid expansion, the uninsured rate dropped by 4.3 percentage points from 18.4% in 2013 to 14.1% through the second quarter of 2014. In contrast, the uninsured rate dropped by only 2.5 percentage points in states not adopting the Medicaid expansion, from 22.7% in 2013 to 20.2% through the second quarter 2014.50 Other evidence from the Gallup Healthways Well-Being Index reveals the largest reductions in the uninsured have been in Arkansas and Kentucky.51

Looking Ahead

Looking Ahead

Four years after the law was enacted, the ACA remains controversial. While many support individual provisions included in the law, Americans are divided in their opinions on the law overall. The political future of the law continues to be debated in Congress and in state legislatures across the country, and ongoing legal challenges create uncertainty. Yet, in the face of these many hurtles and setbacks, real progress has been made in implementing key features of the ACA and important steps have been taken to improve access to and affordability of health coverage for millions of people.

As implementation of the ACA moves forward, a number of key challenges persist:

- The future of the ACA’s coverage expansions remains uncertain. The biggest potential threat to the long-term stability of the Marketplaces is the impending Supreme Court decision in the King v. Burwell A decision in favor of the plaintiffs will not only cut off subsidies in states with a federally-run Marketplace pushing many people back into the ranks of the uninsured, but the viability of the Marketplaces in these states will be threatened as premiums rise. At the same time, debate over the Medicaid expansion will continue in a few states in the coming year given that there is no deadline for expanding Medicaid. More governors may pursue alternative models through waivers; however, opposition to the Medicaid expansion remains strong in state legislatures. Nevertheless, decisions by even a small number of states to expand Medicaid would increase the number of people with access to affordable health coverage. Further complicating the coverage picture, funding for the Children’s Health Insurance Program (CHIP) expires in 2015. While CHIP has maintained broad bipartisan support, the debate over funding and CHIP’s future will be complicated by the availability of coverage through the Marketplaces and questions over how best to integrate CHIP with Medicaid, Marketplace, and employer-sponsored coverage.

- Although enrollment in the second year was strong, many uninsured remain unaware of the requirements to have coverage and of subsidies available to make coverage more affordable. Public opinion polls find over half of the uninsured do not know that the law provides financial help to low and moderate income Americans and nearly four in ten uninsured expect to remain uninsured.52 With limited funding for marketing and outreach, reaching these potentially eligible consumers will be harder. Navigators and other enrollment assisters will continue to play an important role in supporting enrollment, especially among hard to reach populations; however, as Marketplace funding for these programs shrinks, their role may be jeopardized.

- Affordability of coverage is a concern. Premium growth for both employer group coverage and in the new Marketplaces has been modest overall. However, it is unclear whether the moderate premium growth seen over the past couple of years will continue. While subsidies in the Marketplaces will protect many consumers from sharp increases in premiums, those who purchase coverage without financial assistance would feel the full impact of the cost growth. In addition to premiums, high deductibles and other cost sharing in plans in the Marketplaces place a significant financial burden on those who need health services. While, overall, the increase in health insurance coverage appears to be reducing cost-related barriers to accessing health care, the high cost sharing in Marketplace plans may limit access to needed care for some and premiums can still be a financial impediment to coverage.

- Despite progress in lowering the number of uninsured, many people are left out of the ACA’s coverage expansions. State decisions not to expand Medicaid have left over 3.7 million poor adults in the coverage gap. In addition, undocumented immigrants are ineligible for either Medicaid or Marketplace coverage. Without access to affordable insurance, these individual will likely continue to rely on safety net providers for care. While these providers have traditionally cared for the uninsured and other vulnerable, low-income populations, the funding they have relied on to finance this care is declining. In particular, cuts to the Medicare and Medicaid Disproportionate Share Hospital programs will, over time, dramatically reduce the financial support for indigent care. Providers, especially in states that do not expand Medicaid where the uninsured will be increasingly concentrated, will feel the financial squeeze of the continued demand for care and more limited financing to support that care.

The ACA remains a work in progress and a subject of sharp partisan disagreement. The individual market has been reformed, the long-standing barrier to Medicaid coverage for adults without dependent children has been removed in many but not all states, new health insurance Marketplaces are in place, and the ranks of the uninsured have been significantly reduced, while significant legal political and implementation challenges remain.

Endnotes

- Health Insurance Reform Requirements for the Group and Individual Health Insurance Markets. 45 CFR Part 147 (2010) ↩︎

- 45 CFR §§ 147.104, 147.106, 147.108 ↩︎

- Fair health insurance premiums. 45 CFR § 147.102 (2014) ↩︎

- Preservation of right to maintain existing coverage. 45 CFR § 147.140 (2010) ↩︎

- Levitt L. September 8, 2011. “Grandfathering Explained.” Kaiser Family Foundation. https://modern.kff.org/health-reform/perspective/grandfathering-explained/ ↩︎

- Kaiser Family Foundation and Health Research & Educational Trust. 2014. 2014 Kaiser/HRET Employer Health Benefits Survey. https://modern.kff.org/health-costs/report/2014-employer-health-benefits-survey/ ↩︎

- Jost T. December 23, 2014. “Implementing Health Reform: Proposed Changes to the Uniform Summary of Benefits and Coverage, Uniform Glosssary (Updated).” Health Affairs Blog. http://healthaffairs.org/blog/2014/12/23/implementing-health-reform-proposed-changes-to-summary-of-benefits-and-coverage-uniform-glossary/ ↩︎

- Coverage of preventive health services. 45 CFR § 147.130 (2013) ↩︎

- Kaiser Family Foundation. September 2014. “How Does Where You Work Affect Your Contraceptive Coverage?” https://modern.kff.org/womens-health-policy/fact-sheet/how-does-where-you-work-affect-your-contraceptive-coverage/ ↩︎

- Burwell v. Hobby Lobby, 573 U.S. __ (2014). Opinion available at http://www.supremecourt.gov/opinions/13pdf/13-354_olp1.pdf ↩︎

- Center for Consumer Information and Insurance Oversight. “Fact Sheet: Women’s Preventive Services Coverage, Non-Profit Religious Organizations, and Closely Held For-Profit Entities.” Available at http://www.cms.gov/CCIIO/Resources/Fact-Sheets-and-FAQs/womens-preven-02012013.html ↩︎

- Burke A and Simmons A. June 27, 2014. “Increased Coverage of Preventive Services with Zero Cost Sharing under the Affordable Care Act.” Office of the Assistant Secretary for Planning and Evaluation, Department of Health and Human Services. http://aspe.hhs.gov/health/reports/2014/preventiveservices/ib_preventiveservices.pdf ↩︎

- Hamel L; Firth J and Brodie M. March 2014. “Kaiser Health Tracking Poll: March 2014.” Kaiser Family Foundation. https://modern.kff.org/health-reform/poll-finding/kaiser-health-tracking-poll-march-2014/ ↩︎

- Department of Health and Human Services, Report to Congress on Preventive Services and Obesity-related Services Available to Medicaid Enrollees, 2014. http://www.medicaid.gov/Medicaid-CHIP-Program-Information/By-Topics/Quality-of-Care/Downloads/RTC-Preventive-Obesity-Related-Services2014.pdf ↩︎

- Sommers B. June 2012. “Number of Young Adults Gaining Insurance Due to the Affordable Care Act Now Tops 3 Million.” ASPE, Department of Health and Humans Services. http://aspe.hhs.gov/aspe/gaininginsurance/rb.cfm ↩︎

- Kaiser Family Foundation. February 29, 2012. “Explaining Health Care Reform: Medical Loss Ratio (MLR).” https://modern.kff.org/health-reform/fact-sheet/explaining-health-care-reform-medical-loss-ratio-mlr/ ↩︎

- Cox C, Claxton G and Levitt L. June 6, 2013. “Beyond the Rebates: How Much Are Consumers Saving from the ACA’s Medical Loss Ratio Provisions.” Kaiser Family Foundation. https://modern.kff.org/health-reform/perspective/beyond-rebates-how-much-are-consumers-saving-from-the-acas-medical-loss-ratio-provision/ ↩︎

- The Kaiser Family Foundation State Health Facts. Data source: State Effective Rate Review Programs, The Center for Consumer Information & Insurance Oversight (CCIIO), CMS; April 16, 2014.https://modern.kff.org/health-reform/state-indicator/rate-review-program-effectiveness/ ↩︎

- Kaiser Family Foundation. October 1, 2012. “Quantifying the Effects of Health Insurance Rate Review.” https://modern.kff.org/health-costs/report/quantifying-the-effects-of-health-insurance-rate/ ↩︎

- Kaiser Family Foundation. January 2014. “Explaining Health Care Reform: Risk Adjustment, Reinsurance, and Risk Corridors.” https://modern.kff.org/health-reform/issue-brief/explaining-health-care-reform-risk-adjustment-reinsurance-and-risk-corridors/ ↩︎

- 78 FR 12866, February 25, 2013. ↩︎

- Kaiser Family Foundation. January 2013. “Implementing New Private Health Insurance Market Rules.” https://modern.kff.org/health-reform/issue-brief/implementing-new-private-health-insurance-market-rules-2/ ↩︎

- The Kaiser Family Foundation State Health Facts. Data compiled by KFF staff through a review of state documents and the final EHB rule from the Department of Health and Human Services. https://modern.kff.org/health-reform/state-indicator/ehb-benchmark-plans/ ↩︎

- Salganicoff A, et. al. September 2014. “Coverage for Abortion Services and the ACA.” Kaiser Family Foundation. https://modern.kff.org/womens-health-policy/issue-brief/coverage-for-abortion-services-and-the-aca/ ↩︎

- Levitt L, Claxton G and Pollitz K. February 28, 2012. “Private Insurance Benefits and Cost-Sharing under the ACA.” Kaiser Family Foundation. https://modern.kff.org/health-reform/perspective/private-insurance-benefits-and-cost-sharing-under-the-aca ↩︎

- Clemens-Cope L and Anderson N. March 3, 2014. “How Many Non-Group Policies Were Canceled: Estimates from December 2013.” Health Affairs Blog. http://healthaffairs.org/blog/2014/03/03/how-many-nongroup-policies-were-canceled-estimates-from-december-2013/ ↩︎

- Hamel L, et al. June 19, 2014. “Survey of Non-Group Health Insurance Enrollees.” Kaiser Family Foundation. https://modern.kff.org/health-reform/report/survey-of-non-group-health-insurance-enrollees/ ↩︎

- Individual Shared Responsibility Payment for Not Maintaining Minimum Essential Coverage. 26 CFR §§1.5000A-1 through 1.5000A-5 (2014). ↩︎

- For individuals and families who owe a penalty based on percentage of income, the penalty is based on income above the tax filing threshold, which is $10,150 for an individual/$20,300 for joint filers in 2014. This penalty is also capped at the national average premium for a bronze plan. In 2014, that amount is $2,448 for an individual, $12,240 for a family of five. ↩︎

- Congressional Budget Office. June 5, 2014. “Payments of Penalties for Being Uninsured under the Affordable Care Act: 2014 Update.” http://www.cbo.gov/publication/45397 ↩︎

- 79 FR 8543. February 12, 2014. Shared Responsibility for Employers Regarding Health Coverage. https://www.federalregister.gov/articles/2014/02/12/2014-03082/shared-responsibility-for-employers-regarding-health-coverage ↩︎

- Kaiser Family Foundation. December 18, 2014. “Web Briefing for Journalists: How the ACA’s Employer Requirements and Related Provisions Affect Businesses and Workers.” https://modern.kff.org/health-reform/event/december-18-web-briefing-for-journalists-how-acas-employer-requirements-and-related-provisions-affect-businesses-and-workers/ ↩︎

- The Kaiser Family Foundation State Health Facts. Data source: “Creating a New Competitive Health Insurance Marketplace,” CMS.gov. https://modern.kff.org/health-reform/state-indicator/total-exchange-grants/ ↩︎

- Kaiser Family Foundation State Health Facts. Data Source: Kaiser Family Foundation analysis of health plan information available through healtlhcare.gov and insurance company rate filings to state regulators. https://modern.kff.org/other/state-indicator/number-of-issuers-participating-in-the-individual-health-insurance-marketplace/ ↩︎

- Kaiser Family Foundation State Health Facts. Data Source: Kaiser Family Foundation analysis of premium data from healthcare.gov and insurer rate filings to regulators. https://modern.kff.org/other/state-indicator/monthly-silver-premiums-for-a-40-year-old-non-smoker-making-30000year-2014-2015/ ↩︎

- Kaiser Family Foundation. October 27, 2014. “Explaining Health Reform: Questions about Health Insurance Subsidies.” https://modern.kff.org/health-reform/issue-brief/explaining-health-care-reform-questions-about-health/ ↩︎

- Kaiser Family Foundation. April 24, 2011. “Measuring the Affordability of Employer Health Coverage.” https://modern.kff.org/health-costs/perspective/measuring-the-affordability-of-employer-health-coverage/ ↩︎

- Claxton, G and Panchal, N. February 11, 2015. “Cost-Sharing Subsidies in Federal Marketplace Plans.” Kaiser Family Foundation. https://modern.kff.org/health-costs/issue-brief/cost-sharing-subsidies-in-federal-marketplace-plans/ ↩︎

- Musumeci M. February 2015. “Are Premium Subsidies Available in States with a Federally-run Marketplace? A Guide to the Supreme Court Argument in King v. Burwell.” Kaiser Family Foundation. https://modern.kff.org/health-reform/issue-brief/are-premium-subsidies-available-in-states-with-a-federally-run-marketplace-a-guide-to-the-supreme-court-argument-in-king-v-burwell/ ↩︎

- Dorn S and Tolbert J. November 2014. “The ACA’s Basic Health Program Option: Federal Requirements and State Trade-offs.” Kaiser Family Foundation. https://modern.kff.org/health-reform/report/the-acas-basic-health-program-option-federal-requirements-and-state-trade-offs/ ↩︎

- Pollitz K, Tolbert J, and Ma, R. July 15, 2014. “Survey of Health Insurance Marketplace Assister Programs.” Kaiser Family Foundation. https://modern.kff.org/report-section/survey-of-health-insurance-marketplace-assister-programs-section-2/ ↩︎

- Kaiser Family Foundation. September 24, 2013. “Helping Hands: A Look at State Consumer Assistance Programs under the Affordable Care Act.” https://modern.kff.org/health-reform/issue-brief/helping-hands-a-look-at-state-consumer-assistance-programs-under-the-affordable-care-act/ ↩︎

- HHS.gov/HealthCare Blog. February 25, 2015. “Open Enrollment 2015 Re-Enrollment Snapshot.” Department of Health and Human Services. http://www.hhs.gov/healthcare/facts/blog/2015/02/open-enrollment-2015-re-enrollment.html ↩︎

- Rudowitz R, Artiga S, and Musumeci M. February 2015. “The ACA and Medicaid Expansion Waivers.” Kaiser Family Foundation. https://modern.kff.org/medicaid/issue-brief/the-aca-and-medicaid-expansion-waivers/ ↩︎

- Garfield R, et. al. November 2014. “The Coverage Gap: Uninsured Poor Adults in States that Do Not Expand Medicaid—An Update.” Kaiser Family Foundation. https://modern.kff.org/health-reform/issue-brief/the-coverage-gap-uninsured-poor-adults-in-states-that-do-not-expand-medicaid-an-update/ ↩︎

- Centers for Medicare and Medicaid Services. February 2015. “Medicaid and CHIP: December 2014 Monthly Applications, Eligibility Determinations and Enrollment Report.” http://www.medicaid.gov/medicaid-chip-program-information/program-information/downloads/december-2014-enrollment-report.pdf ↩︎

- Kaiser Family Foundation. December 11, 2012. “Medicaid Eligibility, Enrollment Simplification, and Coordination under the Affordable Care Act: A Summary of CMS’s March 23, 2012 Final Rule.” https://modern.kff.org/medicaid/issue-brief/medicaid-eligibility-enrollment-simplification-and-coordination-under-the-affordable-care-act-a-summary-of-cmss-march-23-2012-final-rule/ ↩︎

- Kaiser Commission on Medicaid and the Uninsured analysis of 2001-2014 National Health Interview Surveys. ↩︎

- Garfield R and Young K. 2015. “Adults Who Remained Uninsured at the End of 2014.” Kaiser Family Foundation. https://modern.kff.org/health-reform/issue-brief/adults-who-remained-uninsured-at-the-end-of-2014/ ↩︎

- Kaiser Commission on Medicaid and the Uninsured analysis of 2013-2014 National Health Interview Surveys. ↩︎

- Witters D. August 5, 2014. “Arkansas, Kentucky Report Sharpest Drops in Uninsured Rate.” Gallup. http://www.gallup.com/poll/174290/arkansas-kentucky-report-sharpest-drops-uninsured-rate.aspx#1 ↩︎

- DiJulio B, Firth J, and Brodie M. January 28, 2015. “Kaiser Health Tracking Poll: January 2015.” Kaiser Family Foundation. https://modern.kff.org/health-costs/poll-finding/kaiser-health-tracking-poll-january-2015/ ↩︎