Medicaid Financial Eligibility in Pathways Based on Old Age or Disability in 2022: Findings from a 50-State Survey

Key Takeaways

Medicaid is an important source of health and long-term care coverage for seniors and people with disabilities. The Medicaid pathways in which eligibility is based on old age or disability are known as “non-MAGI” pathways because they do not use the Modified Adjusted Gross Income (MAGI) financial methodology that applies to pathways for pregnant people, parents, and children with low incomes. In addition to considering old age/disability status and income, many non-MAGI pathways also have asset limits.

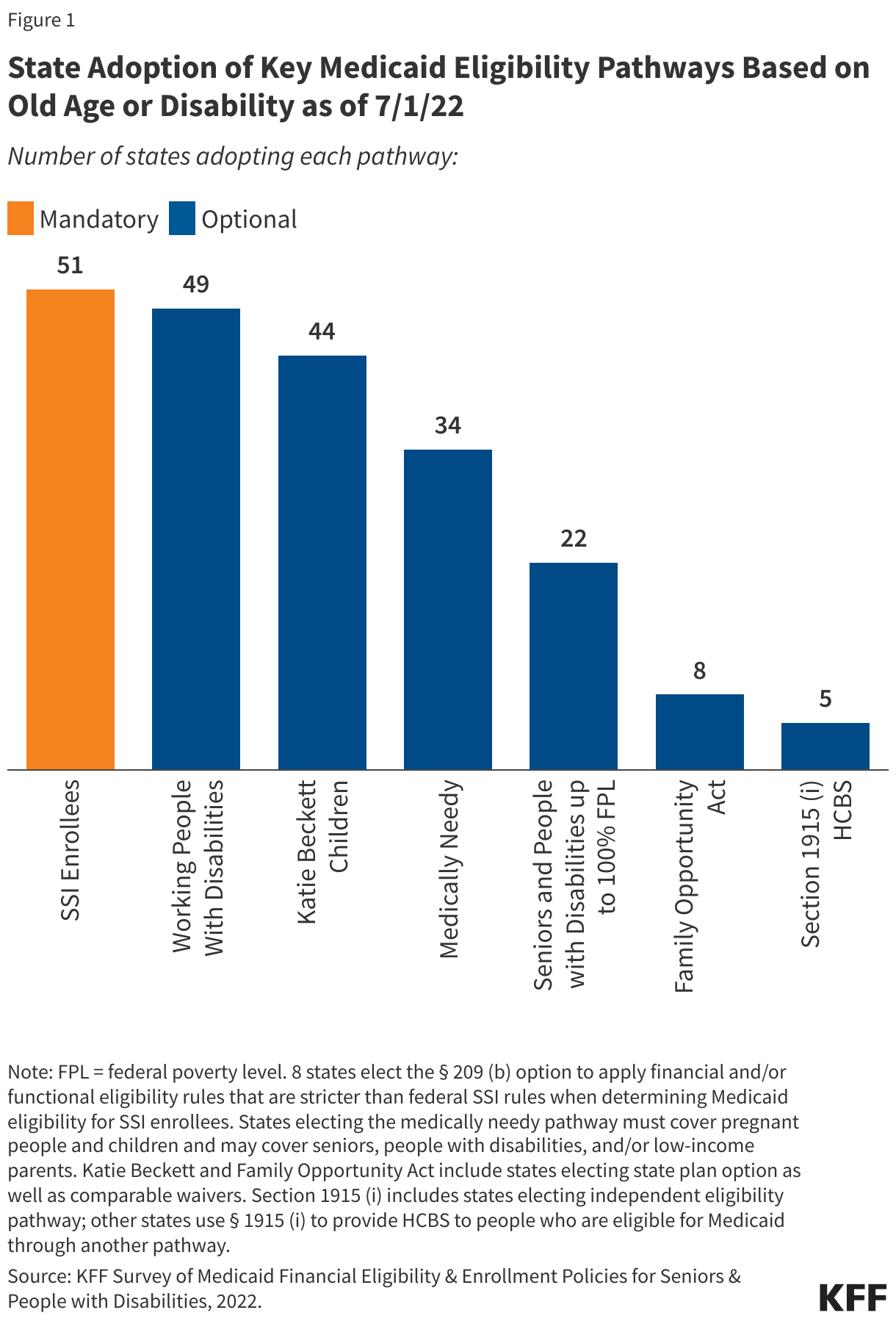

Nearly all non-MAGI pathways are optional, resulting in substantial state variation (Figure 1). Each group has different rules about income and assets, making eligibility complex. The Appendix provides details about the major non-MAGI pathways included in this survey, including pathways available to seniors and people with disabilities generally and pathways limited to people using long-term services and supports (LTSS) in nursing homes or other institutions or in the community. This issue brief presents state-level data on Medicaid financial eligibility criteria and adoption of the major non-MAGI pathways as of July 2022. The data were collected from March through May 2022 in KFF’s survey of Medicaid state eligibility officials. Overall, 50 states and the District of Columbia responded to the survey, though response rates to specific questions varied. Responses were supplemented with publicly available information where available. The Appendix tables contain detailed state-level data.

At least five states have adopted new financial eligibility expansions in non-MAGI pathways that take effect after July 2022. In January 2023, New York will join increase the income limit for seniors and people with disabilities to 138% FPL ($1,563 per month for an individual in 2022), the same limit as for MAGI populations. New York’s non-MAGI asset limits also will increase by about 50% in January 2023 (from $16,800 to $28,134 for an individual and from $24,600 to $37,908 for a couple). Between July 2022 and January 2024, California will phase in the elimination of asset limits in its pathway for seniors and people with disabilities up to 138% FPL and its working people with disabilities buy-in, placing access to coverage on the same financial terms as MAGI pathways which do not have an asset limit. Three other states are adopting changes that take effect July 1, 2022: Connecticut is increasing its income limit for seniors and people with disabilities up to 100% FPL; Maryland is eliminating its income limit for the working people with disabilities buy-in; and Minnesota is increasing its income limit for medically needy seniors and people with disabilities to 100% FPL.

Though many states adopted policies to expand Medicaid eligibility for non-MAGI groups using emergency authorities during the PHE, very few states reported plans to continue these policies after the PHE ends. The only policy that some states plan to continue is reducing or eliminating premiums. Of the 20 states that reported adopting that policy, only 3 states (CA, IL, NH) reported plans to continue reducing or eliminating premiums.

Looking ahead, Medicaid remains an essential, and often the sole, source of medical and LTSS coverage for many seniors and nonelderly adults and children with disabilities. While the income limits associated with the non-MAGI pathways vary among states, they generally remain low. However, a notable minority of states are adopting non-MAGI financial eligibility expansions, including some that adopt the same financial eligibility limits that apply to MAGI populations (138% FPL and no asset test). States’ choices about which pathways to cover are an important baseline from which to monitor seniors and people with disabilities’ access to coverage, including LTSS.

Issue Brief

Medicaid is an important source of health and long-term care coverage for seniors and people with disabilities. As of 2019, there were 8.5 million Medicaid enrollees ages 65 or older and another 10.0 million enrollees for whom eligibility is based on disability. Other people with disabilities qualify for Medicaid solely based on their low income. The Medicaid pathways in which eligibility is based on old age or disability are known as “non-MAGI” pathways because they do not use the Modified Adjusted Gross Income (MAGI) financial methodology that applies to pathways for pregnant people, parents, and children with low incomes. In addition to considering old age/disability status and income, many non-MAGI pathways also have asset limits. The fact that most non-MAGI pathways are optional results in substantial state variation.

The non-MAGI pathways include people receiving Supplemental Security Income (SSI) benefits, which all states that choose to participate in Medicaid must cover, and an array of additional groups that can be covered at state option (Figure 1 and Appendix Table 1). In addition to SSI enrollees, the main non-MAGI pathways to full Medicaid eligibility include state options to expand coverage to working people with disabilities; Katie Beckett children with significant disabilities living at home; medically needy seniors and people with disabilities who “spend down” by deducting incurred medical expenses from their income; seniors and people with disabilities up to 100 percent of the federal poverty level (FPL, $1,133/month for an individual in 2022); the Family Opportunity Act buy-in for children with significant disabilities; and Section 1915 (i) which allows states to provide an independent eligibility pathway for people with functional needs that are less than an institutional level of care. Each group has different rules about income and assets, making eligibility complex. The Appendix provides detailed information about each of these pathways as well as pathways available to people who need LTSS. Some Medicaid enrollees also may have Medicare as their primary source of coverage, but there is no pathway to full Medicaid eligibility dedicated to Medicare enrollees.

This issue brief presents state-level data on Medicaid financial eligibility criteria and adoption of the major non-MAGI pathways as of July 2022. It includes mandatory and optional pathways to full Medicaid eligibility as well as state options to expand Medicaid financial eligibility for people who need long-term services and supports (LTSS) in nursing homes or other institutions or in the community. It also highlights state actions to expand non-MAGI financial eligibility that have been adopted and take effect after July 2022. The data were collected from March through May 2022 in KFF’s survey of Medicaid state eligibility officials. Overall, 50 states and the District of Columbia responded to the survey, though response rates to specific questions varied. Responses were supplemented with publicly available information where available. The Appendix tables contain detailed state-level data. A related brief presents a snapshot of non-MAGI enrollment during the COVID-19 public health emergency (PHE) and anticipated changes after the PHE ends as well as key state enrollment and renewal policies as of July 2022 and state plans for resuming normal eligibility and enrollment operations after the PHE ends.

Medicaid Eligibility Based on Old Age or Disability

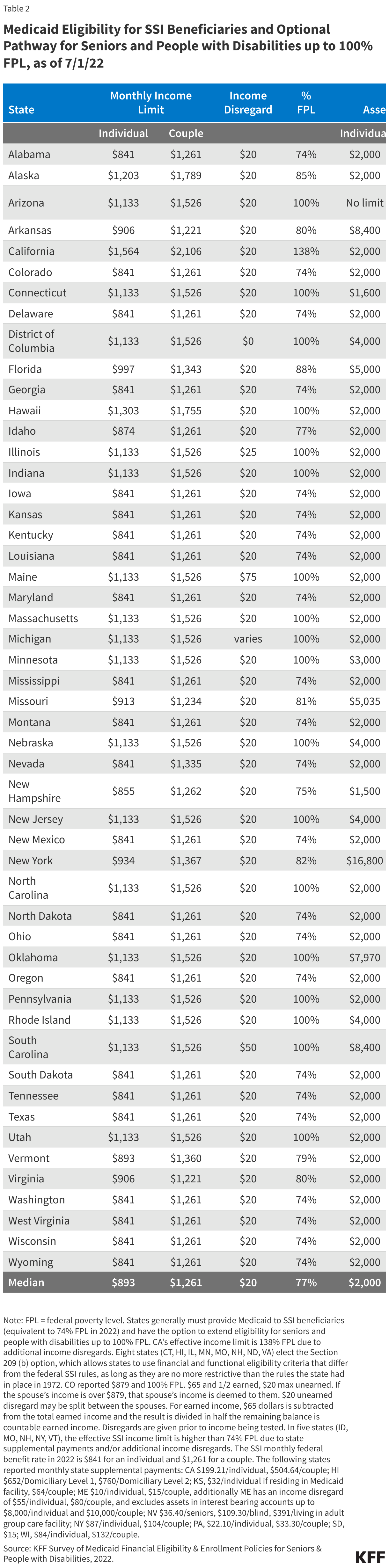

SSI enrollees are the only non-MAGI pathway that states must cover in their Medicaid programs. Not all people with disabilities qualify for SSI due to the program’s low income and asset limits and stringent definition of disability. The SSI federal benefit rate is equivalent to 74% FPL ($841/month for an individual and $1,261/month for a couple in 2022), and assets are limited to $2,000 for an individual and $3,000 for a couple. (Appendix Table 2).

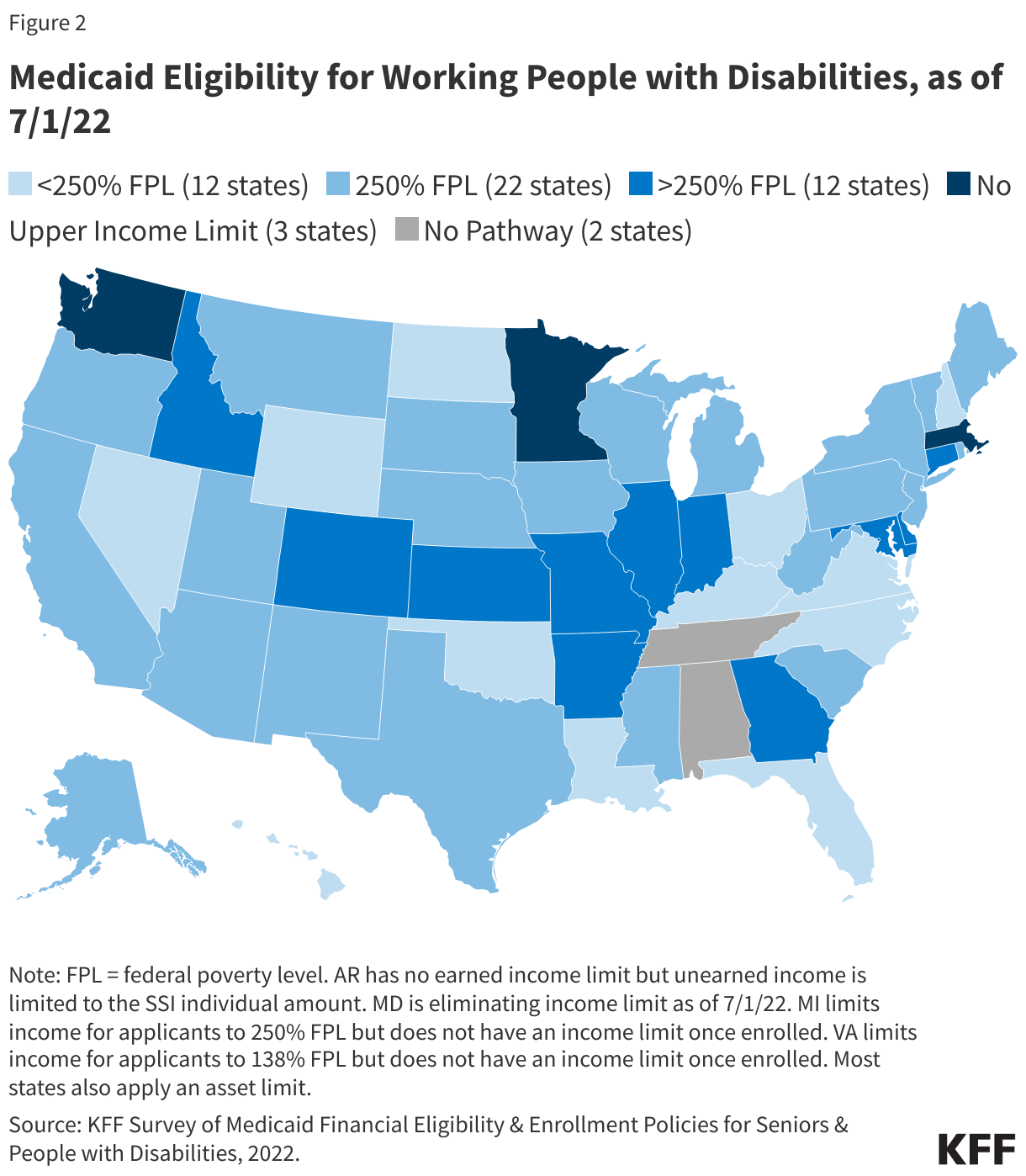

Among the optional non-MAGI pathways, nearly all states (49 of 51) adopt the buy-in for working people with disabilities (Figure 2 and Appendix Table 3). The median income limit for this pathway is 250% FPL ($2,832/month for an individual in 2022), and the median asset limit is $10,000 for an individual. Two states (MA, WA) cover working people with disabilities without an income or asset limit. One other state (MN) does not apply an income limit, and five other states (AZ, AR, CO, DC, WY) do not apply an asset limit. Additionally, 12 states have income limits above 250% FPL, ranging from 275% FPL in Delaware to 552% FPL in Connecticut, and a dozen states have asset limits above $10,000, ranging from $12,000 in Iowa to $25,000 in Illinois. Medicaid is an important source of coverage for services that support the ability of people with disabilities to work, such as personal care, prescription drugs, and assistive technology. Eliminating or increasing income and asset limits enables people with disabilities to retain access to these services while also accepting pay raises as they advance in their careers and accruing savings for retirement.

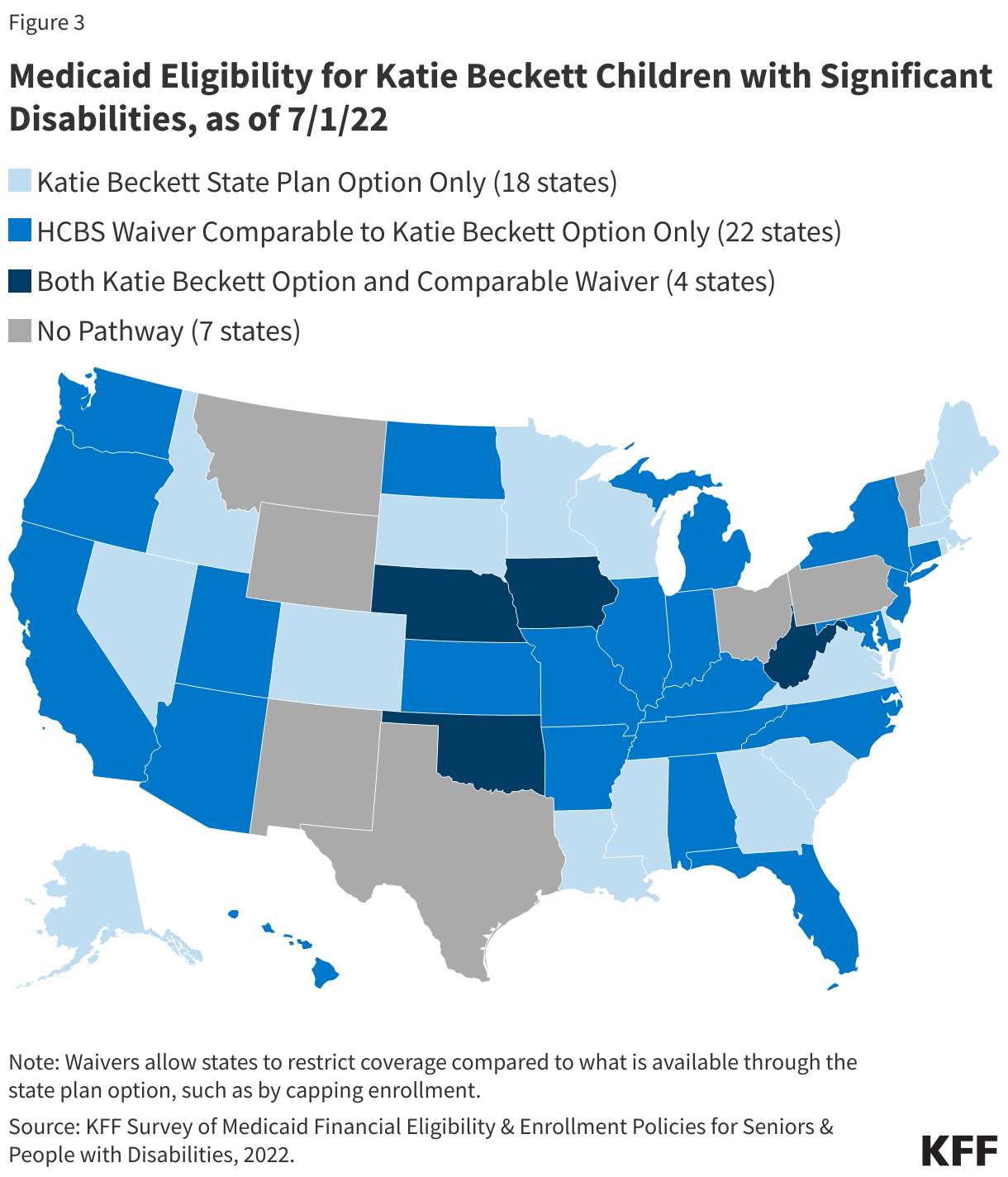

Forty-four states adopt the Katie Beckett state plan option to cover children with significant disabilities living in the community or provide coverage through a comparable waiver (Figure 3 and Appendix Table 1). Eighteen of these states adopt the Katie Beckett state plan option, 22 states offer a waiver that covers a comparable population, and four states cover some children through the state plan option and others through a waiver. Waivers allow states to restrict coverage compared to what is available through the state plan option, such as by capping enrollment.

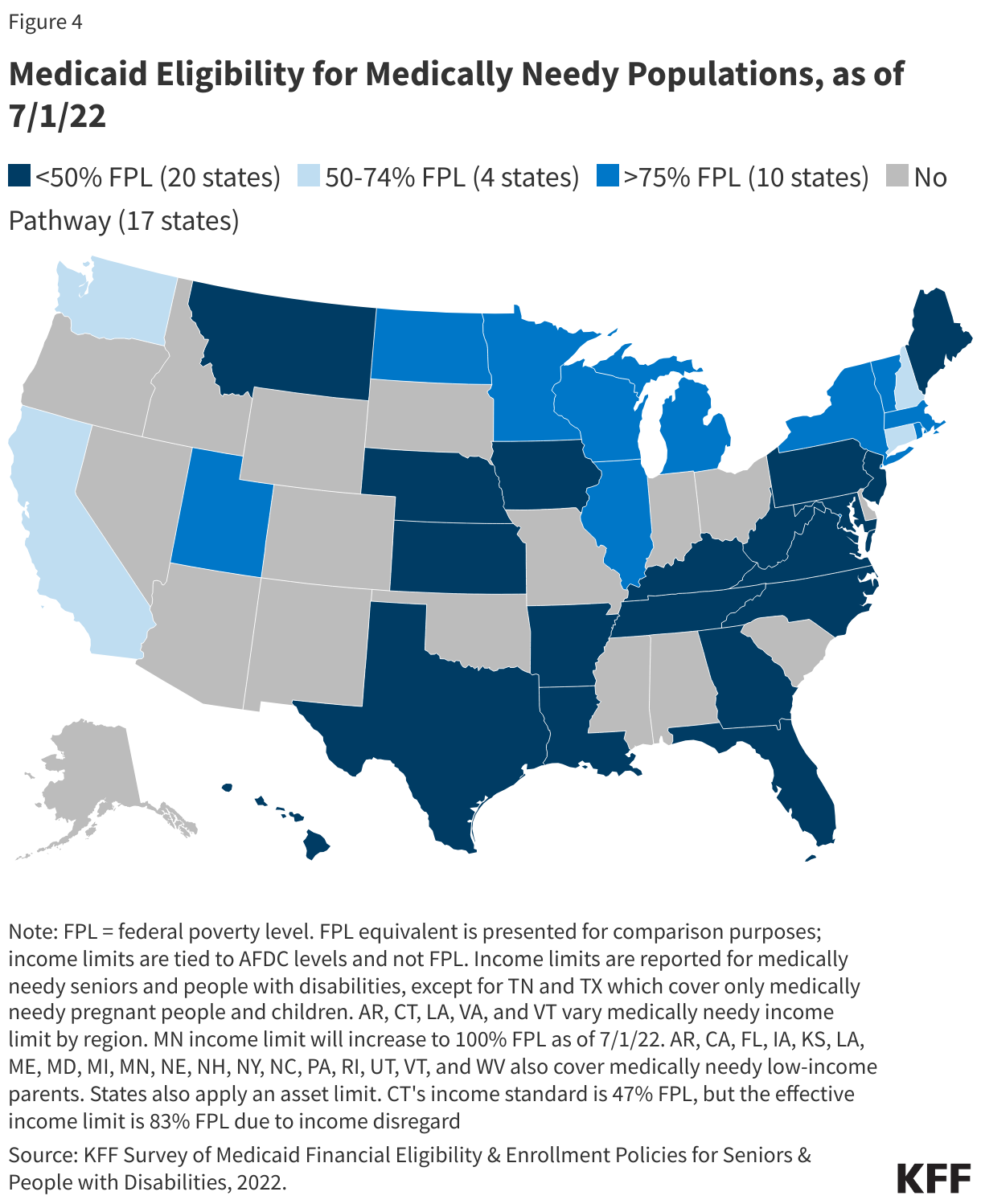

More than three in five states (34 of 51) adopt the medically needy pathway (Figure 4 and Appendix Table 4). Two of these states (TN, TX) offer medically needy coverage only for pregnant people and children and do not extend this coverage to seniors and people with disabilities. The median income limit (after deducting incurred medical expenses) medically needy seniors and people with disabilities is tied to cash assistance limits and is less than 50% FPL,1 and the median asset limit is $2,000 for an individual. As of June 2022, five states cover medically needy seniors and people with disabilities up to or above 100% FPL (DC, IL, UT, VT, WI). A dozen states have medically needy asset limits above the SSI limit, ranging from $2,400 in PA to $16,800 in NY. Over 80% of the states that cover medically needy seniors and people with disabilities (27 of 32) opt to include nursing home services in the benefit package offered to these enrollees, making this pathway another means of accessing long-term institutional care.

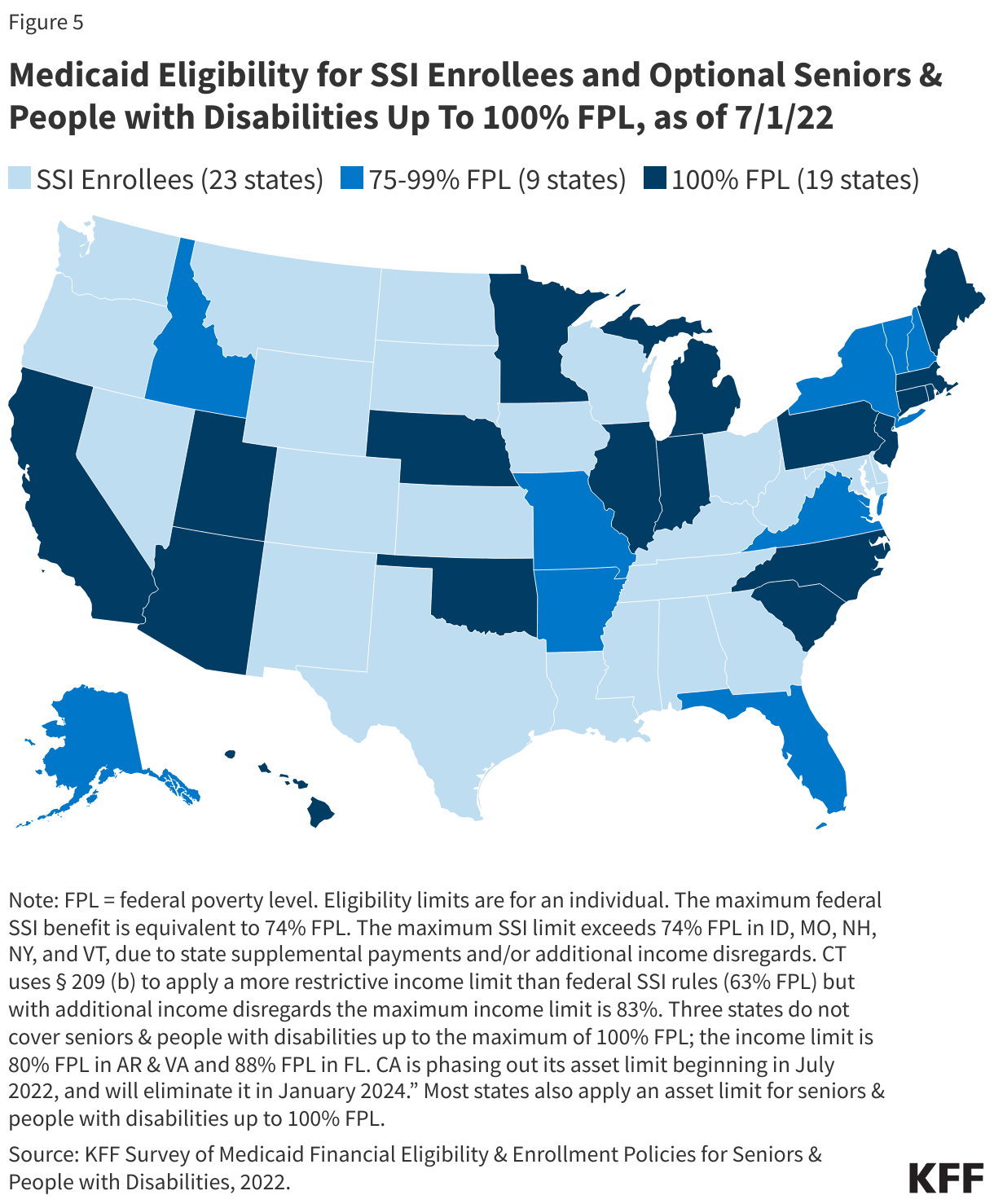

Less than half of states (22 of 51) opt to expand coverage for seniors and people with disabilities beyond federal SSI limits, up to the federal poverty level (Figure 5 and Appendix Table 2). Nearly all states electing this pathway adopt the federal maximum of 100% FPL. Notably, California is the first state to increase the income limit in this pathway to 138% FPL (($1,563 per month) for an individual in 2022, by using income disregards, effective December 2020), at the same level as ACA expansion adults. Most states apply the SSI asset limit of $2,000 for an individual. As of June 2022, AZ has no asset limit for this pathway, and 11 other states set the asset limit above the SSI level, ranging from $3000 in MN to $16,800 in NY.

Eight states adopt the Family Opportunity Act (FOA) state plan option to provide buy-in coverage to children with significant disabilities or provide comparable coverage through a waiver (Appendix Table 1). Four of these states elect the state plan option, three offer a waiver, and one offers both the state plan option and a waiver. Three states (CO, IA, KY) provide coverage up to the federal maximum of 300% FPL, while four states (LA, NJ, ND, TX) adopt a lower income limit for this pathway. Notably, unlike Katie Beckett waivers which typically involve enrollment caps or other limitations compared to coverage available under the state plan option, Massachusetts’ FOA-like waiver does not have an enrollment cap or an income limit and therefore expands coverage beyond what the state plan option would provide.2 Most (5 of 8) states with the FOA option or a comparable waiver choose to charge premiums. The exceptions are Iowa, Kentucky, and New Jersey. Colorado charges premiums of $70 per month beginning at 134% FPL, Texas charges $50 per month beginning at 151% FPL, North Dakota charges 5% of gross family income beginning at 200% FPL, and Louisiana charges $15 per month beginning at 201% FPL. In Massachusetts’ FOA-like waiver, sliding scale premiums apply to children in families with income over 150% FPL, beginning at $12 per month.

Five states adopt the Section 1915 (i) state plan option to expand eligibility to people with functional needs that are less than an institutional level of care (Appendix Table 5).3 Indiana was the first state to use Section 1915 (i) as an independent pathway to Medicaid eligibility. It began doing so in 2014 for adults with behavioral health conditions up to 150% FPL ($1,699 per month for an individual in 2022), and in 2019, it adopted another Section 1915 (i) eligibility pathway for adults with certain mental health diagnoses up to 150% FPL.4 Since 2017, Ohio has used Section 1915 (i) to provide Medicaid eligibility to adults with certain mental health or physical disabilities up to 150% FPL.5 In 2019, Maryland began using Section 1915 (i) to provide Medicaid eligibility to children with mental illness up to 150% FPL.6 Beginning in 2021, Alabama uses Section 1915 (i) to provide Medicaid eligibility to adults with intellectual disabilities up to 150% FPL,7 and Connecticut uses Section 1915 (i) to provide Medicaid eligibility for adults with complex health conditions and risk factors who have been homeless and would otherwise be eligible for an HCBS waiver, up to 300% SSI ($2,523 per month for an individual in 2022).8 There is no asset limit for Section 1915 (i) eligibility, similar to the MAGI pathways.

States Expanding Financial Eligibility after July 2022

At least five states have new financial eligibility expansions in non-MAGI pathways that take effect after July 2022. These changes include the following:

- As of January 2023, New York will join California (noted above) as the second state to increase the income limit for seniors and people with disabilities to 138% FPL, the same limit as for MAGI populations. New York’s non-MAGI asset limits also will increase by about 50% as of January 2023 (from $16,800 to $28,134 for an individual and from $24,600 to $37,908 for a couple).

- California is eliminating asset limits in its pathway for seniors and people with disabilities up to 138% FPL (joining AZ) as well as its working people with disabilities buy-in pathway (joining AZ, AR, CO, DE, DC, MA, WA, WY), placing access to coverage on the same financial terms as MAGI pathways which do not have an asset limit. This change will be phased in by increasing the asset limit to $130,000 for an individual, and an additional $65,000 for each additional family member up to 10 people, as of July 1, 2022. The asset limit will be entirely eliminated as of January 1, 2024.

Three other states are adopting changes that take effect July 1, 2022:

- Connecticut is increasing its income limit for seniors and people with disabilities up to about 100% FPL.9

- Maryland is eliminating the income limit for the working people with disabilities buy-in. With this change, Maryland is establishing premiums up to 7.5% of monthly income for those with income over 600% FPL.

- Minnesota is increasing its income limit for medically needy seniors and people with disabilities to 100% FPL.

State Options to Expand Medicaid LTSS Eligibility

Most states adopt the special income rule to expand financial eligibility for people who need Medicaid LTSS up to 300% SSI ($2,523 per month for an individual in 2022, Appendix Table 6). Specifically, 40 states adopt the special income rule for institutional LTSS, while 41 states do so for HCBS. Two states (MA, WV) adopt the special income rule only for HCBS, while one state (NH) does so only for institutional LTSS. All states electing the special income rule set financial eligibility at 300% SSI, except Delaware, which uses 250% SSI. Most states electing the special income rule apply the SSI asset limit of $2,000. A minority of states adopt an asset limit above the SSI level, ranging from $2,500 in Maryland and New Hampshire to $4,000 in the District of Columbia, Mississippi, and Rhode Island. Additionally, Pennsylvania applies a $6,000 disregard to the $2,000 asset limit, making the effective asset limit $8,000.

Most states allow individuals to establish eligibility for Medicaid LTSS by using certain types of trusts (Appendix Table 7). Specifically, 46 states allow individuals with certain types of trusts to qualify for institutional LTSS, while 47 states do so for HCBS waiver eligibility. North Dakota allows trusts only for institutional LTSS eligibility, while the District of Columbia and New York do so only for HCBS eligibility.

Nearly three-quarters of states (37 of 51) limit home equity to the federal minimum of $636,000 for individuals seeking Medicaid LTSS eligibility (Appendix Table 7). Eleven other states adopt the federal maximum of $955,000, while two states use $750,000 (ID, WI). California is the only state that does not place a limit on home equity for an individual’s principal residence. Effective July 9, 2022, Washington increased its home equity limit from the federal minimum of $636,000 to the federal maximum of $955,000.

Medicaid LTSS Post-Eligibility Treatment of Income

The median personal needs allowance for a Medicaid enrollee residing in an institution is $50 per month (Appendix Table 8). This amount ranges from $30/month, the federal minimum, in three states (AL, NC, SC) to $200/month in Alaska.

The median maintenance needs allowance for a Medicaid enrollee receiving HCBS is $2,523 per month (Appendix Table 8). This amount ranges from $72/month in Washington, to $2,523 (the amount reported by most states). Nine states reported amounts that vary by waiver program, while six states do not have a maintenance needs allowance.

Spousal Impoverishment Rules

The median monthly community spouse needs allowance is $3,435 (Appendix Table 8). Thirteen states adopt the federal minimum ($2,178), while 21 states adopt the federal maximum ($3,435).

The median community spouse asset limit is $137,400 (Appendix Table 8). Two states adopt the federal minimum ($27,480), while 28 states adopt the federal maximum ($137,400).

State Plans to Retain Emergency Authorities Post-PHE

Though many states adopted policies to expand or streamline Medicaid eligibility and enrollment for non-MAGI groups using emergency authorities, very few reported plans to continue these policies after the PHE ends. A variety of Medicaid emergency authorities are available to states during the COVID-19 public health emergency (PHE), and states have used these authorities to adopt temporary policy changes that expand Medicaid financial eligibility in non-MAGI pathways, such as expanding income and/or asset limits and reducing or eliminating premiums. States have the option to continue many policies adopted under when they return to normal operations, and CMS guidance encourages states to consider retaining policy changes that expand access to HCBS.

The only policy change adopted using emergency authorities that a few states are planning to or may retain after the PHE ends is reducing or eliminating premiums. These include three states (CA, IL, NH) out of the 20 that reported adopting this policy. California waived premiums during the PHE and passed legislation to eliminate premiums for the working people with disabilities pathway effective July 1, 2022. New Hampshire also eliminated premiums during the PHE, pursuant to a governor’s emergency order, and has legislation pending that would continue this policy change.

Looking Ahead

Medicaid remains an essential, and often the sole, source of medical and LTSS coverage for many seniors and nonelderly adults and children with disabilities. Aside from the core group of SSI enrollees, pathways to full Medicaid eligibility based on old age or disability are provided at state option, which results in substantial variation among states. Additionally, the income limits associated with the non-MAGI pathways vary among states but generally remain low. However, a notable minority of states are adopting non-MAGI financial eligibility expansions, including some that adopt the same financial eligibility limits that apply to MAGI populations (138% FPL and no asset test). States’ choices about which pathways to cover are an important baseline from which to monitor seniors and people with disabilities’ access to coverage, including LTSS.

Appendix

Description of Pathways to Full Medicaid Eligibility Based on Old Age or Disability

MANDATORY PATHWAY

Supplemental Security Income (SSI) Enrollees

States generally must provide Medicaid to people who receive federal Supplemental Security Income (SSI) benefits.10 This is the only pathway where eligibility is based on old age or disability that states must include in their Medicaid programs. To be eligible for SSI, people must have low incomes, limited assets, and an impaired ability to work at a substantial gainful level as a result of old age or significant disability. The maximum SSI federal benefit rate is $841 per month for an individual and $1,261 for a couple11 in 2022, which is 74 percent of the federal poverty level (FPL). The effective SSI income limit may be somewhat higher than 74% FPL in some states, due to state supplemental payments and/or additional income disregards.12 SSI enrollees also are subject to an asset limit of $2,000 for an individual and $3,000 for a couple.13

SSI eligibility is determined by the Social Security Administration (SSA). If states do not want to accept SSA’s determination of an SSI enrollee’s income, assets, and/or disability status when determining Medicaid eligibility, states can use different rules under Section 209 (b). Specifically, states can use financial and/or functional eligibility criteria that are more restrictive than the federal SSI rules, as long as the state’s rules are no more restrictive than the rules it had in place in 1972, when the SSI program was established.14

OPTIONAL PATHWAYS

Working People WIth Disabilities

States can choose to cover working people with disabilities whose income and/or assets exceed the limits for other eligibility pathways.15 This option enables people with disabilities to retain access to the medical and LTSS they need as their income increases. Medicaid often is especially important to working people with disabilities because private insurance typically does not cover all of the services and supports they need to live independently and to work.16 States can choose to apply an asset limit to this pathway. Eliminating asset limits, or increasing them beyond the SSI limit of $2,000 for an individual and $3,000 for a couple, recognizes that enrollees are likely to incur expenses related to work or community living and enables them to accrue some savings to meet future expenses. States also can choose to charge monthly premiums, usually on a sliding scale based on income.

Katie Beckett Children With Disabilities

States can choose to elect the “Katie Beckett” option to extend coverage to children up to age 19 with significant disabilities living at home, without regard to household income. These children must meet SSI medical disability criteria and otherwise qualify for an institutional level of care according to functional eligibility criteria set by the state. States can target different populations based on the type of institutional care (hospital, skilled nursing facility, intermediate care facility, intermediate care facility for individuals with “mental disease,”17 intermediate care facility for individuals with intellectual or developmental disabilities) that would be required if the child was not receiving Medicaid services in the community.

Katie Beckett income limits are generally 300% of SSI ($2,523 per month in 2022), with a $2,000 asset limit, considering only the child’s own income and assets. Under the Katie Beckett pathway, parental income and assets are disregarded when determining Medicaid eligibility for children with disabilities living at home, just as they are for children with disabilities residing in an institution. This option makes it possible for children to receive necessary care while remaining at home with their families.

Katie Beckett children can be covered through the optional state plan pathway or through a home and community-based services (HCBS) waiver.18 These waivers allow states to expand financial eligibility and offer HCBS to seniors and people with disabilities who would otherwise qualify for an institutional level of care and can be targeted to a specific population. Providing coverage through a waiver also allows states to cap enrollment, which can result in waiting lists and is not permitted under state plan authority.

Medically Needy Populations

States can choose to adopt the medically needy option to extend Medicaid to people with high medical expenses who would be eligible in a categorically needy pathway, except that their income and/or assets exceed the maximum limit for that pathway.19 See Box 1 below for an explanation of how medically needy pathways differ from categorically needy pathways. All states electing medically needy coverage must include pregnant people and children. States also can choose to extend medically needy coverage to other groups such as seniors, people with disabilities, and/or low-income parents. Medically needy income limits are typically very low.20 States also can choose to apply an asset limit to medically needy pathways. The asset limit is typically the SSI amount of $2,000 for an individual and $3,000 for a couple, though it can be higher at state option.

Box 1: Categorically Needy vs. Medically Needy Pathways

Before the Affordable Care Act (ACA), Medicaid eligibility was limited to certain categories of people.21 These “categorically needy” groups include children, pregnant people, low-income parents, seniors, and people with disabilities. The ACA eliminated the need to fit into one of these categories by expanding Medicaid to nearly all adults with incomes up to 138% FPL ($1,563 per month for an individual in 2022). In states that have not adopted the ACA Medicaid expansion, people still must fit into one of the specified categories to qualify for coverage today. In addition, these categories remain relevant to determining Medicaid eligibility under the “medically needy” option because people who qualify as “medically needy” must fit into one of the traditional categories. States cannot use the medically needy option to cover people who do not fit into one of the traditional categories, such as childless adults, regardless of how poor they are or how extensive their medical needs are.

There are two ways that individuals can qualify for Medicaid through a medically needy pathway.22 First, people with income above the categorically needy income limit associated with a certain population but below the state’s medically needy income limit may be eligible as medically needy. Second, people who “spend down” to the state’s medically needy income limit by subtracting incurred medical or long-term services and supports (LTSS) expenses from their income may qualify. States select a budget period between one and six months during which an individual must incur enough expenses to decrease their income below the medically needy limit. Using a longer budget period may be administratively simpler for states and enrollees and provide continuity of coverage.

States have the option to provide a more limited benefit package to people who qualify for Medicaid in a medically needy, as opposed to categorically needy, pathway. Under federal law, states must include nursing facility services in the benefit package for categorically needy populations but can choose whether to include these services in their medically needy benefit package. In states electing this option, the medically needy pathway can be an important means of expanding coverage for those with overwhelming medical and/or LTSS expenses.

Seniors and People with Disabilities up to 100% FPL

States can chose to expand Medicaid to seniors and people with disabilities whose income exceeds the SSI limit but is below the federal poverty level ($1,133 per month for an individual in 2022).23 The federal maximum income limit for this pathway is 100% FPL.24 States also can choose to apply an asset limit to this pathway. The asset limit is typically the SSI amount of $2,000 for an individual and $3,000 for a couple, though it can be higher at state option.

Family Opportunity ACt Children with Disabilities

The Family Opportunity Act (FOA) pathway provides another option for states to cover children with significant disabilities living at home. These children must meet SSI medical disability criteria and can have family income up to 300% FPL ($5,758 per month for a family of three in 2022).25 Assets are not considered when determining a child’s FOA eligibility. Unlike the Katie Becket pathway which only considers the child’s own income, the FOA option considers household income. The FOA pathway only requires SSI medical disability criteria, while the Katie Beckett option also requires an institutional level of care. Under the FOA option, states are permitted to charge premiums equal to no more than 5 percent of the family’s monthly gross countable income (up to $288 per month in premiums for a family of 3 with income at 300% FPL, $5,758 per month in 2022). FOA children can be covered through the state plan option or through a waiver that covers a similar population while deviating from state plan eligibility rules.

Section 1915 (i) HCBS for people at risk of institutional care

States can elect the Section 1915 (i) pathway to provide Medicaid eligibility to people at risk of institutional care. The ACA amended Section 1915 (i) to create an independent pathway to Medicaid eligibility.26 This allows states to provide full Medicaid benefits to people who are not eligible through another pathway and who meet the Section 1915 (i) financial and functional eligibility criteria.27 Specifically, states can cover (1) people with income up to 150% FPL ($1,699 per month for an individual in 2022) with no asset limit who meet functional eligibility criteria; and/or (2) people with income up to 300% SSI who would be eligible for Medicaid under an existing HCBS waiver. Section 1915 (i) functional eligibility requires people to have needs that are less than what is required to qualify for an institutional level of care, which enables states to offer HCBS as preventive services in efforts to delay or foreclose the need for costlier future care or institutionalization. Like HCBS waivers, states can target Section 1915 (i) services to a particular population. Unlike HCBS waivers, states are not permitted to cap enrollment or maintain a waiting list for Section 1915 (i) Medicaid eligibility. However, states can manage enrollment under Section 1915 (i) by restricting functional eligibility criteria if the state will exceed the number of beneficiaries that it anticipated serving

State Options to Expand Medicaid LTSS Financial Eligibility

Medicaid LTSS include nursing home and other institutional services as well as home and community-based services (HCBS). Medicaid remains the primary payer for LTSS, as Medicare does not cover long-term care, private insurance coverage is limited, and out-of-pocket costs often are unaffordable. Medicaid also is an important source of federal funds to support states in meeting their community integration obligations under the Americans with Disabilities Act and the Olmstead decision.28

Special income rule

States can elect the “special income rule” option to allow people with functional needs who require an institutional level of care to qualify for Medicaid LTSS with incomes up to 300% SSI ($2,523 per month for an individual in 2022).29 States also can apply an asset limit under the special income rule, usually the SSI amount of $2,000 for an individual and $3,000 for a couple.

States using the special income rule can apply it to people in institutions, such as nursing homes, and/or people receiving LTSS in the community.30 Aligning financial eligibility rules across long-term care settings is important to eliminating programmatic bias toward institutional care. If people can qualify for institutional services at higher incomes than required to qualify for community-based services, they may choose to enter a nursing facility when they need care instead of going without necessary care while spending down to the lower HCBS income limit.

Trusts

Qualified Income or “Miller” Trusts

States can choose to allow individuals residing in an institution to qualify for Medicaid LTSS with income higher than 300% of SSI if their excess income is administered through a special type of trust, known as a qualified income or “Miller” trust.31 States can choose whether to cap the amount of money that can be put into a Miller trust when establishing eligibility for LTSS. States allowing Miller trusts for institutional care can also allow individuals to use Miller trusts to qualify for Medicaid HCBS. As noted above, using the same financial eligibility rules for institutional care and HCBS helps alleviate bias toward institutional care.

Income from a Miller trust can be used to fund the Medicaid enrollee’s personal needs allowance as well as a monthly allowance for the beneficiary’s spouse who remains in the community under the spousal impoverishment rules (both discussed below). Any additional income from the trust goes toward the enrollee’s cost of care, and states can recover funds remaining in the trust after the individual’s death to reimburse the cost of care.

Supplemental Needs and Pooled Income Trusts

States can allow individuals to qualify for Medicaid LTSS using supplemental needs32 and pooled income33 trusts. Both of these types of trusts contain assets for the benefit of non-elderly people with disabilities, which are excluded from Medicaid financial eligibility determinations. States can choose whether to cap the amount of money that can be put into these trusts. The trust beneficiary must have a disability based on SSI criteria. Both types of trusts can be established by the individual’s parent, grandparent, legal guardian or a court and must provide that the state can receive any amount remaining in the trust upon the beneficiary’s death to cover the cost of Medicaid services provided. Pooled income trusts are established and managed by a non-profit association, with a separate account for each beneficiary, but assets are combined for purposes of fund investment and management. This option can enable individuals with relatively small trust amounts to benefit from economies of scale by being part of a larger pool of funds for investment and management purposes.

Home Equity Limits

States can choose the amount of home equity that people seeking Medicaid LTSS can have as an allowable asset.34 The federal minimum home equity limit is $636,000 in 2022, and the upper limit is $955,000.

Personal/Maintenance Needs Allowance

Once eligible for Medicaid, individuals in institutions, such as nursing homes, generally must contribute most of their monthly income to the cost of their care, with the exception of a small allowance used to pay for personal needs that are not covered by Medicaid, such as clothing.35 The federal minimum personal needs allowance is $30 per month, though states can choose to adopt a higher amount.

Certain Medicaid enrollees receiving HCBS must contribute a portion of their income to their cost of care, though states generally allow them to retain a monthly maintenance needs allowance.36 The maintenance needs allowance generally exceeds the institutional personal needs allowance described above, recognizing that, unlike those in nursing homes, individuals living in the community must pay for room and board. There is no federal minimum HCBS maintenance needs allowance; instead, states may use any amount as long as it is based on a “reasonable assessment of need” and subject to a maximum that applies to all enrollees under the HCBS waiver.37 The maintenance needs allowances established by states play a critical role in determining whether individuals can afford to remain in the community and avoid or forestall institutional placement.

Spousal Impoverishment Rules

Congress created the Medicaid spousal impoverishment rules in 1988 to protect a portion of a married couple’s income and assets and ensure that the “community spouse” is able to meet their living expenses when the other spouse seeks Medicaid LTSS. The spousal impoverishment rules supersede rules that would otherwise require Medicaid financial eligibility determinations to account for a spouse’s financial responsibility for a Medicaid applicant or enrollee by contributing to their cost of care.38 The protected income is called the spouse’s “monthly maintenance needs allowance.” The federal minimum monthly maintenance needs allowance is 150% FPL for a household of two ($2,178 as of July 1, 2021), and the federal maximum is $3,435 as of January 1, 2022.39 The protected assets are known as the “community spouse resource allocation.” The federal minimum community spouse resource allocation is $27,480 as of 2022, and the federal maximum is $137,400. States also can choose to apply a formula that allows the community spouse to retain an amount of protected assets that is the greater of either the federal minimum or one-half of the couple’s total combined assets but not to exceed the federal maximum.

States must apply the spousal impoverishment rules when a married Medicaid enrollee is receiving nursing home or other institutional care, but prior to 2014, states could choose whether to apply the spousal impoverishment rules when a married individual sought home and-community based waiver services.40 Beginning on January 1, 2014, ACA Section 2404 requires states to apply the spousal impoverishment rules to HCBS waivers.41 The ACA provision originally was set to expire at the end of 2018, but Congress subsequently adopted several short-term authorizations. The provision currently expires on September 30, 2023.42

Appendix Tables

Appendix Table 3: Medicaid Eligibility for Working People with Disabilities, as of 7/1/22

Appendix Table 4: Medicaid Eligibility Through the Medically Needy Pathway, as of 7/1/22

Endnotes

- % FPL equivalent is presented for comparison purposes only; several states reported that income limits are tied to AFDC limits and not based on a percentage of poverty. ↩︎

- Under Massachusetts’ waiver, state plan “base populations” include all infants under age one (based solely on income) through 200% FPL and children with disabilities under age 19 through 150% FPL. Waiver expansion populations include “higher income children with disabilities” with no income limit. CMS Special Terms and Conditions, MassHealth Medicaid Section 1115 Demonstration, #11-W-00030/1,Table A, p. 10, 16, 21 (approved July 1, 2017-Sept. 30, 2022, amended June 27, 2018), https://www.medicaid.gov/Medicaid-CHIP-Program-Information/By-Topics/Waivers/1115/downloads/ma/ma-masshealth-ca.pdf. ↩︎

- States’ survey responses in this section were supplemented with the state plan amendments posted on Medicaid.gov. ↩︎

- The effective income limit in IN is 300% FPL, because the state disregards income in the amount of the difference between 150% FPL and 300% FPL. IN SPA #18-011, § 1915 (i) HCBS, Attachment 2.2-A, page 23g (approved 5/16/19, effective 6/1/19); IN SPA #13-013, § 1915 (i) HCBS, Attachment 2.2-A, page 23g (approved 5/30/14, effective 6/1/14). ↩︎

- The effective income limit in OH is higher because the state disregards income in the amount of the difference between 150% FPL and 300% SSI. Physical health diagnoses include HIV/AIDS, cancer, sickle cell anemia, hemophilia, immune deficiency, cystic fibrosis, end state renal disease, and previous transplant. OH #17-017, § 1915 (i) HCBS, Attachment 3.1-I, page 6-7 (approved 8/23/17, effective 7/1/17). ↩︎

- The effective income limit in MD is higher because the state disregards income in the amount of the difference between 150% FPL and 300% FPL. MD #19-0004, Individuals Receiving State Plan Home and Community-Based Services, (approved 9/5/19, effective 10/1/19) (p. 14 of pdf). ↩︎

- AL SPA #21-0005-A, Eligibility (approved 6/14/21, effective 4/1/21). ↩︎

- CT#21-0001-A, Eligibility (approved and effective 8/16/21). ↩︎

- CT’s increase reflects changes to the underlying financial methodology which will tie cash assistance payments to a percentage of the federal poverty level and in turn set the Medicaid income limit for seniors and people with disabilities at 143% of the cash assistance payment, along with a $409/month unearned income disregard. ↩︎

- 42 U.S.C. § 1396a (a)(10)(A)(i)(II); but see 42 U.S.C. § 1396a (f). ↩︎

- The couple rate applies when both individuals qualify for SSI. ↩︎

- Under federal SSI rules, there is a general income disregard of $20 per month. Earned income is subject to an additional disregard of $65 plus half of the remaining amount. ↩︎

- Certain assets, such as an individual’s home, one car used for household transportation, and a certain amount of funds for prepaid burial expenses, are excluded from the SSI asset limit. ↩︎

- Section 209 (b) states must allow SSI beneficiaries to establish Medicaid eligibility through a spend-down by deducting unreimbursed out-of-pocket medical expenses from their countable income (described later in this Appendix). Section 209 (b) states also must provide Medicaid to children who receive SSI and who meet the financial eligibility rules for the state’s Aid to Families with Dependent Children program as of July 16, 1996. 42 U.S.C. § 1396a (f); see also 42 U.S.C. § 1396a (a)(10)(C)(i)(III) and (ii); 42 C.F.R. § 435.121 (d). ↩︎

- 42 U.S.C. § § 1396a (a)(10)(A)(ii)(XV), (XVI); 1396o (g). ↩︎

- See, e.g., KFF, Benefits and Cost-sharing for People with Disabilities in Medicaid and the Marketplace (Oct. 2014). ↩︎

- An antiquated term in the statute. ↩︎

- For more about HCBS waivers, see KFF, Medicaid Home and Community-Based Services: People Served and Spending During COVID-19 (March 2022), ; KFF, State Policy Choices About Medicaid Home and Community-Based Services Amid the Pandemic (March 2022). ↩︎

- 42 U.S.C. § § 1396a (a)(10)(C); 1396d (a)(iii), (iv), (v). ↩︎

- States’ medically needy income limits are so low because they are tied to the Aid to Families with Dependent Children (AFDC) payment levels that were in place in 1996. Federal rules require medically needy income levels to be no higher than 133 1/3% of the state’s maximum AFDC payment level for a family of two without any income or assets as of July 16, 1996. States can raise their medically needy income limits if they increase their TANF income standards, but few states have done so (TANF replaced AFDC in 1996). 42 U.S.C. § § 1396b (f)(1)(B)(i); 1396u-1 (b), (f)(3). ↩︎

- Unless the state had a Section 1115 waiver that used cost savings to expand coverage. ↩︎

- For more information on medically needy eligibility and how to calculate spend down, see KFF, The Medically Needy Program: Spending and Enrollment Update (Dec. 2012), ↩︎

- 100% FPL for an individual in Hawaii is $1,303/month in 2022. ↩︎

- 42 U.S.C. § § 1396a (a)(10)(A)(ii)(X); 1396a (m). ↩︎

- 42 U.S.C. § § 1396a (a)(10)(A)(ii)(XIX); 1396a (cc)(1). ↩︎

- Section 1915 (i) also allows states to provide an HCBS benefit package, as a state plan option instead of a waiver, to people who are eligible for Medicaid through another eligibility pathway. ↩︎

- 42 U.S.C. § 1396a (a)(10)(A)(ii)(XXII). ↩︎

- In Olmstead, the Supreme Court held that the unjustified institutionalization of people with disabilities violates the Americans with Disabilities Act. KFF, Olmstead’s Role in Community Integration for People with Disabilities Under Medicaid: 15 Years After the Supreme Court’s Olmstead Decision (June 2014). ↩︎

- Those in institutions must have resided there for at least 30 days. 42 U.S.C. § 1396a (a)(10)(ii)(V) and (VI). ↩︎

- States also use § 1915 (c) and § 1115 waivers to expand financial eligibility for HCBS. See generally KFF, Medicaid Home and Community-Based Services: People Served and Spending (March 2022); KFF, State Policy Choices About Medicaid Home and Community-Based Services Amid the Pandemic (March 2022). ↩︎

- See Miller v. Ibarra, 746 F. Supp. 19 (D. Colo. 1990). This option is not available in medically needy states unless they do not offer nursing facility services to medically needy populations. 42 U.S.C. § 1396p (d)(4)(B). ↩︎

- 42 U.S.C. § 1396p (d)(4)(A). ↩︎

- 42 U.S.C. § 1396p (d)(4)(C). ↩︎

- 42 U.S.C. § 1396p (f). ↩︎

- 42 U.S.C. § 1396a (q). ↩︎

- These individuals are eligible for Medicaid via a Section 1915 (c) HCBS waiver because they would be eligible under the Medicaid state plan if institutionalized, meet an institutional level of care, and would be institutionalized if not receiving waiver services. 42 U.S.C. § 1396a (a)(10)(A)(ii)(VI). They sometimes are referred to as the “217-group,” because they are described in 42 C.F.R. § 435.217. 42 C.F.R. § 435.726. ↩︎

- 42 C.F.R. § 435.726 (c). States use different methodologies to determine the monthly maintenance needs allowances for HCBS enrollees. Most states allow individuals to deduct their uncovered medical bills from income. ↩︎

- 42 U.S.C. § 1396r-5 (a)(1). The rules permit (and sometimes require) that a married individual seeking Medicaid LTSS whose spouse is not institutionalized is treated differently for financial eligibility purposes from other individuals seeking Medicaid LTSS. 42 U.S.C. § 1396r-5 (a)(2). For more information, see KFF, Potential Changes to Medicaid Long-Term Care Spousal Impoverishment Rules: States’ Plans and Implications for Community Integration (Feb. 2019). ↩︎

- While the community spouse maximum income maintenance allowance and minimum and maximum asset allowances are adjusted each January, the community spouse minimum monthly maintenance needs allowance is adjusted as of July 1st. CMCS Informational Bulletin, 2022 SSI and Spousal Impoverishment Standards (Nov. 23, 2021). ↩︎

- Specifically, states could opt to apply the rules to individuals who are eligible for Medicaid by reason of a Section 1915 (c) HCBS waiver, under 42 U.S.C. § 1396a (a)(10)(A)(ii)(VI) (describing individuals who would be eligible under the Medicaid state plan if institutionalized, meet an institutional level of care, and would be institutionalized if not receiving waiver services, sometimes referred to as the “217-group,” because they also are described in 42 C.F.R. § 435.217). 42 U.S.C. § 1396r-5 (h)(1)(A). ↩︎

- Section 2404 also expanded the spousal impoverishment rules to the Section 1915 (i) HCBS state plan option, Community First Choice (CFC) attendant care services and supports, and individuals eligible through a medically needy spend down. ↩︎

- The spousal impoverishment rules were extended through March 31, 2019 in the Medicaid Extenders Act of 2019, § 3, Pub. L. No. 116-3 (Jan. 24, 2019); through September 30, 209 in the Medicaid Services Investment and Accountability Act of 2019, § 2, Pub. L. No. 116-16 (April 18, 2019); through December 31, 2019 in the Sustaining Excellence in Medicaid Act of 2019, Pub. L. No. 116-39 (Aug. 8, 2019); through May 22, 2020 in the Further Consolidated Appropriations Act, Pub. L. No. 116-94 (Dec. 20, 2019); and through September 30, 2023 in the Consolidated Appropriations Act of 2021, Pub. L. No. 116-260 (Dec. 27, 2020). ↩︎