Medicaid Enrollment & Spending Growth: FY 2016 & 2017

Executive Summary

For FY 2016 and FY 2017, national Medicaid enrollment and total spending continue to grow, but much more slowly after high growth in FY 2015 primarily due to the implementation of the Medicaid expansion in the Affordable Care Act. This brief discusses these trends based on interviews and data provided by state Medicaid directors as part of the 16th annual survey of Medicaid directors in all 50 states and the District of Columbia. Conducted by the Kaiser Commission on Medicaid and the Uninsured (KCMU) and Health Management Associates (HMA), the survey focuses on trends and Medicaid policy actions taken by states in FY 2016 and FY 2017. Key findings are described below and provided in a companion report.

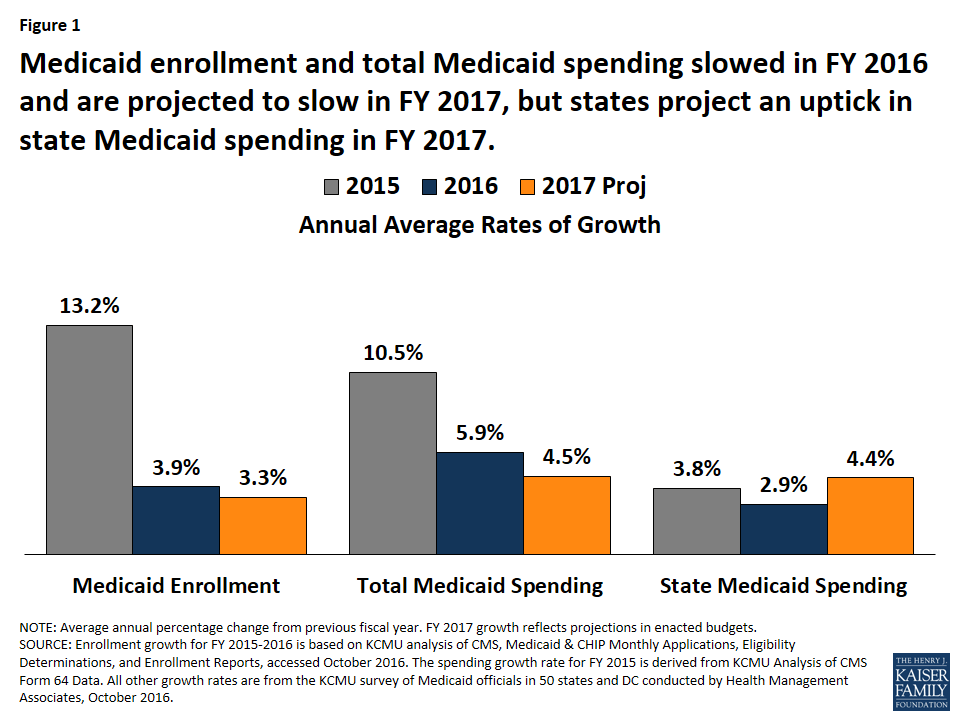

Enrollment and Total Spending. Following significant increases in FY 2015 related to the implementation of the Affordable Care Act (ACA), Medicaid enrollment and total spending growth slowed substantially in FY 2016 and FY 2017 as ACA related enrollment tapered (Figure 1). Medicaid officials identified the high costs of specialty drugs and payment increases for specific provider groups as upward pressures on spending. Slower state revenue growth in FY 2017 added pressure on states to control Medicaid costs.

State Medicaid Spending. Adopted budgets for FY 2017 project an uptick in state Medicaid spending primarily due to the phase-down in the federal share for the expansion population from 100 percent to 95 percent. In FY 2017, state Medicaid spending and total Medicaid spending are projected to grow at the same pace. Eight of the Medicaid expansion states (Arkansas, Arizona, Colorado, Illinois, Indiana, Louisiana, New Hampshire, and Ohio) reported plans to use provider taxes or fees to fund all or part of the state share of costs of the ACA Medicaid expansion.

Looking Ahead. Since 2014, an improving economy and the implementation of the ACA have been the primary drivers of Medicaid enrollment and spending trends. Going forward, ACA-related enrollment is expected to stabilize and trends will be influenced more by the economy, upward spending pressures like rising prescription drug costs, and state policy actions. In addition, federal and state elections will have implications for state decisions about whether to implement the ACA and for the future of the ACA more broadly.

Issue Brief

Introduction

Medicaid has become one of the nation’s largest health programs. According to the Centers for Medicare and Medicaid Services (CMS), a total of 72.8 million Americans had health coverage through state Medicaid programs or the related Children’s Health Insurance Programs (CHIP) in June 2016.1 Total Medicaid spending was $509 billion in FY 2015 with 62 percent paid by the federal government and 38 percent by states.2 Medicaid accounts for one in six dollars spent in the health care system, but 50 percent of long-term care spending and 9 percent of prescription drug spending.3 The key factors affecting total Medicaid spending and enrollment changes over the last decade have been The Great Recession followed by the implementation of the Affordable Care Act (ACA). As of September 2016, 32 states including DC have adopted the ACA Medicaid expansion, with two states newly implementing the expansion in FY 2016 (Alaska and Montana) and Louisiana implementing at the beginning of FY 2017. Under the law, the federal government provided 100 percent of the cost of expansion from calendar years 2014-2016 and this gradually phases down to 95 percent in CY 2017, 94 percent in CY 2018, 93 percent in CY 2019, and 90 percent in CY 2020 and beyond.

This report provides an overview of Medicaid enrollment and spending growth with a focus on the most recent state fiscal year, FY 2016, and current state fiscal year, FY 2017. Findings are based on interviews and data provided by state Medicaid directors as part of the 16th annual survey of Medicaid directors in all 50 states and the District of Columbia conducted by the Kaiser Commission on Medicaid and the Uninsured (KCMU) and Health Management Associates (HMA).

A more detailed description of the methodology used to calculate enrollment and spending growth is in the methodology at the end of this brief. Additional information about Medicaid financing, the role of Medicaid in state budgets, and Medicaid and the economy is in the Appendix.

Context: Recent Trends in the Economy

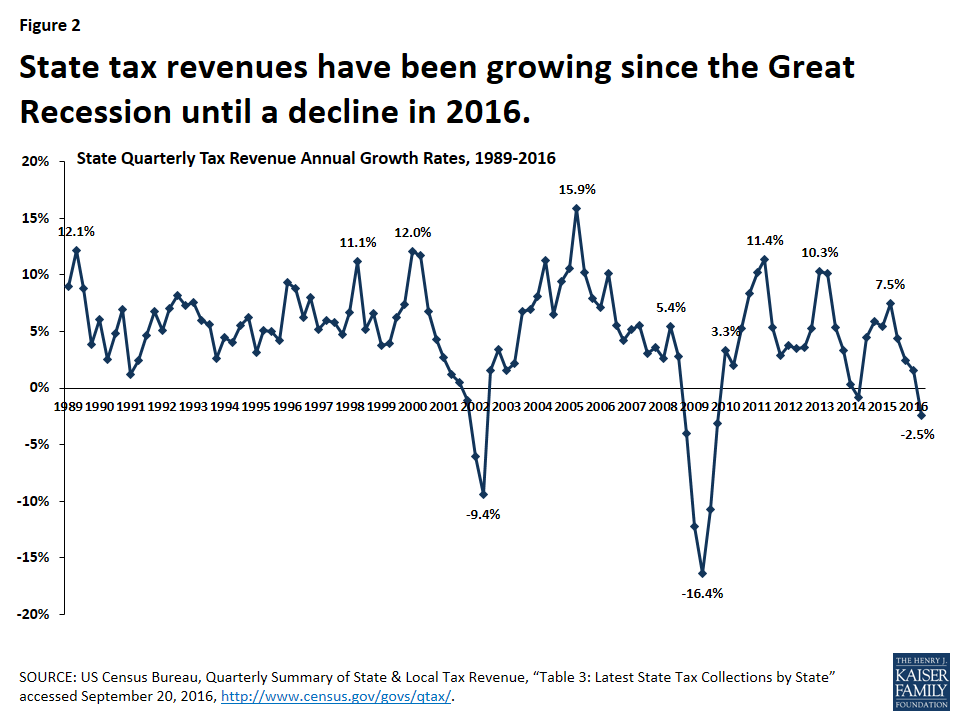

Since the end of the “Great Recession” in 2009, the economy has experienced slow growth and has stabilized in recent years. Unemployment rates peaked at 10 percent in October 2009, dropped to as low as 4.7 percent in May 2016, and have been steady at around 5 percent for the past year. In FY 2016, aggregate state general fund spending and revenues surpassed peak levels from 2008 in real terms (after adjusting for inflation)4 Across all states, general fund expenditures grew by 5.5 percent (higher than in previous years) and general fund revenues grew by 2.8 percent (less than stronger growth in 2015).5 Overall state revenue collections experienced steady growth since the Great Recession, but declined in the second quarter of 2016 (Figure 2). Early data suggest that state revenue collections may slow further in FY 2017 which could constrain overall state spending.6 A volatile stock market and declines in oil prices contribute to an uncertain outlook for state budgets.7

Across the country, unemployment rates range from below three percent in South Dakota and New Hampshire to higher than six percent in Louisiana, New Mexico, Nevada, and Alaska. In addition, general fund spending and revenues are still below pre-recession levels in many states, and a 70 percent decline in oil prices since 2014 is causing significant revenue issues in oil dependent states (Alaska, Louisiana, New Mexico, North Dakota, Oklahoma, Texas, West Virginia, and Wyoming). Alaska and North Dakota were hardest hit with declines in total tax revenue of 41.4 and 34.7 percent, respectively,8 causing significant budget shortfalls. Proposals to address the shortfalls include tax increases and also stark budget cuts.9 Lower revenues and budget cuts have direct implications for Medicaid in these states.

Medicaid Enrollment and Spending: FY 2016 and FY 2017

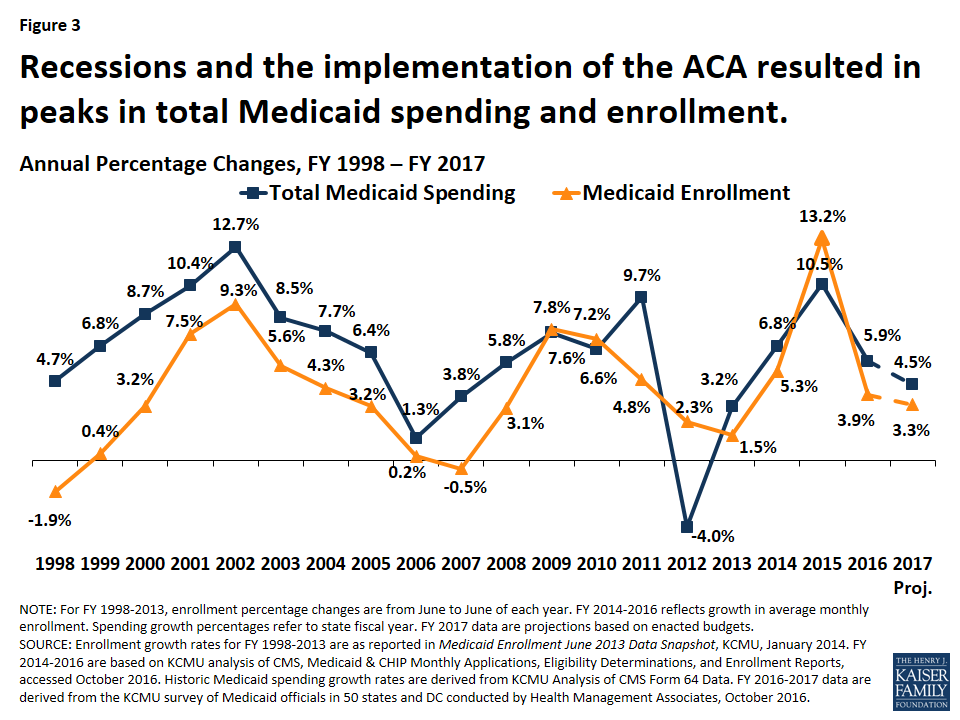

Following significant increases in FY 2015, Medicaid enrollment and total spending growth slowed substantially in FY 2016 and FY 2017. High growth in FY 2015 was due to the implementation of the ACA and the recent trends reflect the tapering of ACA related enrollment and improvements in the economy (Figure 3). A number of states noted that the resolution of eligibility redetermination backlogs that developed in FY 2014 and FY 2015 when the MAGI eligibility and new enrollment systems were implemented contributed to slowing growth. Enrollment trends along with efforts to control costs due to budget pressures contributed to lower total spending growth. However, Medicaid officials identified the high costs for prescription drugs, especially for specialty drugs, as well as policy decisions to increase payment rates to specific provider groups as factors putting upward pressures on spending. For FY 2016, state projections reported in last year’s survey were on target for enrollment growth (4.0 percent projected and 3.9 percent experienced), while actual total spending growth was less than projected (6.9 percent projected and 5.9 percent experienced).

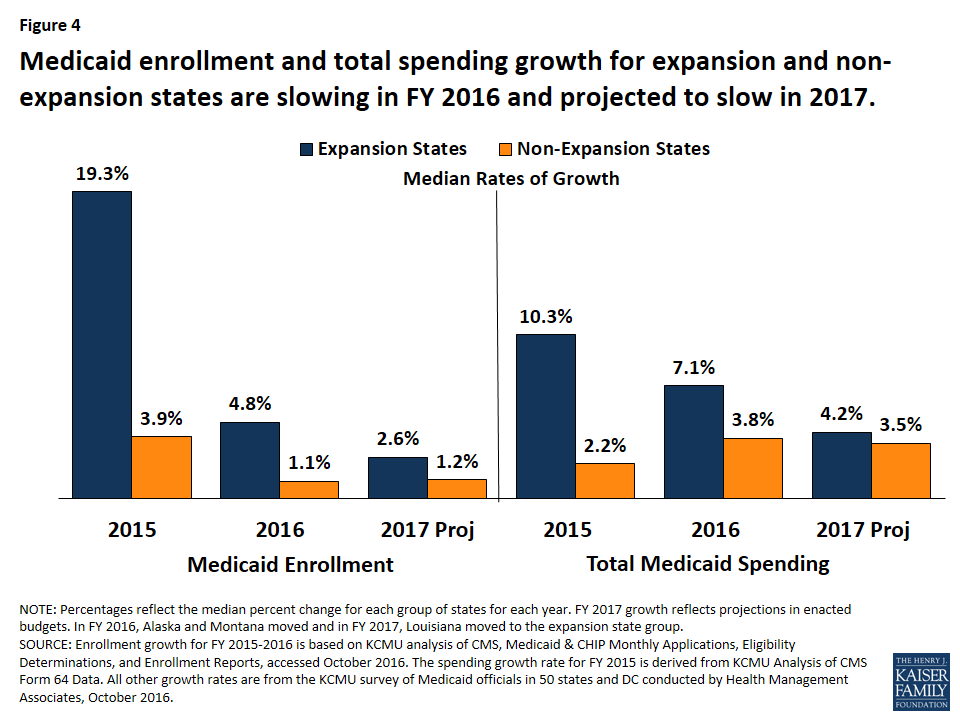

Trends for slowing enrollment and total spending growth hold true across expansion and non-expansion states. Median growth rates were calculated to show the experience of the typical state in each of these groups. Medicaid enrollment and total spending in FY 2016 and FY 2017 slowed for both expansion and non-expansion states. The typical expansion state, compared to a non-expansion state, experienced higher Medicaid enrollment and total spending growth in FY 2016, and that differential is projected to continue in FY 2017, although the size of the differential is narrowing (Figure 4).

Significant variation in enrollment and total spending growth occurs within each group of states, that may be due to timing of the Medicaid expansion decisions, Medicaid policy and state budget decisions. For example, states that implemented the Medicaid expansion in FY 2016 and FY 2017 (Alaska, Montanta, and Louisiana) experienced and project higher enrollment and spending growth relative to other expansion states.

State spending for Medicaid grew slower than total spending in FY 2016; but adopted budgets for FY 2017 project an uptick in state Medicaid spending.10 Historically, the state share of Medicaid spending and total Medicaid spending have increased at similar rates, except during temporary statutory changes in federal matching rates. Congress provided fiscal relief to states during each of the last two economic downturns by increasing the federal Medicaid matching rate, which lowered growth in state Medicaid spending. Beginning in 2014, the ACA Medicaid expansion resulted in a divergence in growth rates for total and state Medicaid spending. States that expand Medicaid qualify for 100 percent federal funding of Medicaid costs for newly eligible enrollees for calendar years 2014-2016. The federal share phases to 95 percent in 2017, 94 percent in 2018, 93 percent in 2019, and 90 percent in 2020 and thereafter, well above traditional FMAP rates in every state.

Largely due to the 100 percent FMAP for newly eligible enrollees in expansion states, state spending for Medicaid across all states increased slower than total spending in both FY 2015 and FY 2016. In FY 2015, the differential in these growth rates was large (3.8 percent state Medicaid spending growth compared to 10.5 percent total Medicaid spending growth). The differential narrowed in FY 2016 (Figure 5).

State Medicaid spending growth is often viewed in the context of overall state general fund spending for all programs in the state budget. For FY 2016, the National Association for State Budget Officers (NASBO) estimated overall general fund expenditure growth of 5.5 percent, the largest increase since the Great Recession.11

In FY 2017, state Medicaid spending and total Medicaid spending are projected to grow at a nearly identical pace across all states. State Medicaid spending growth is projected to be higher in FY 2017 compared to the previous year as expansion states begin paying the 5 percent share of the costs of the expansion in January of 2017.

Growth in state Medicaid spending in expansion states has been lower relative to non-expansion states, but an uptick is projected in FY 2017 as expansion states pay a small share of the costs of newly eligible enrollees. In FY 2015 and FY 2016 expansion states experienced slower growth in state Medicaid spending compared to total Medicaid spending largely due the 100 percent FMAP for the expansion population. This differential was very large in FY 2015 (10.3 percent total spending growth compared to 2.4 percent state spending growth) and was smaller in FY 2016. In addition, the growth in state Medicaid spending in expansion states was lower than growth in non-expansion states in FY 2015 and FY 2016.

In FY 2017, the median growth in state Medicaid spending for expansion states is projected to be 5.9 percent, up from 1.9 percent in FY 2016, as the five percent share of costs for the expansion population phases in on January 1, 2017, mid-way through the state fiscal year (Figure 6). Eight of the Medicaid expansion states (Arkansas, Arizona, Colorado, Illinois, Indiana, Louisiana, New Hampshire, and Ohio) will use provider taxes or fees to fund all or part of the state share of costs of the ACA Medicaid expansion while others will use general funds. Non-expansion states are not affected by the enhanced ACA match rates, and median state Medicaid spending growth for non-expansion states remained fairly stable and consistent with total Medicaid spending.

As with total spending and enrollment, significant variation in state Medicaid spending occurs across expansion and non-expansion states. In some cases, this variation was not related to state implementation of the ACA expansion. For example, Alaska anticipates a decline in state Medicaid spending in FY 2017 due to budget issues. Florida experienced high growth in state Medicaid spending in FY 2016 when federal funding for the state’s Low-Income Pool (LIP) declined under the terms of a renewed waiver. In other states, formula driven changes in the traditional federal Medicaid match rate affect state spending growth. For example, the Texas FMAP declined significantly, from 58.1 in FFY 2015, to 57.1 percent in FFY 2016, and then 56.2 percent in FFY 2017, resulting in large growth in state funds. These annual FMAP changes reflect changes in state average personal income relative to the national average, but data is lagged by three years.

Conclusion and Looking Ahead

In recent years, the slow economic recovery and the 2014 implementation of the ACA have been the primary drivers of enrollment and total Medicaid spending growth. State implementation of the ACA Medicaid coverage expansions was the major driver of total Medicaid spending and enrollment growth in FY 2014 and FY 2105. As ACA related enrollment tapers, states experienced slower enrollment and total spending growth in FY 2016 and these trends are expected to continue in FY 2017. The primary upward pressures on total Medicaid spending identified by Medicaid directors are rising prescription drug costs and state policy actions such as reimbursement rate increases.

The requirement for states to start paying five percent of the costs of expansion resulted in an uptick in state Medicaid spending growth in FY 2017; however, looking ahead, the state share increasing from five percent to six percent in January 2018 should not affect growth rates as much as a change from zero to five percent. Changes in enrollment and spending should be considered in the broader context of findings about the impact of the ACA Medicaid expansion. Research on the effects of Medicaid expansions under the ACA shows that the expansion has resulted in significant coverage gains, increased access to care and utilization of health care services among the low-income population, and positive effects on multiple economic outcomes despite Medicaid enrollment growth initially exceeding projections in many states.

States continue to focus on improving their programs through value based purchasing and other delivery system strategies aimed at improving care and outcomes while controlling costs. Pressure to control Medicaid spending continues as growth in overall state revenues slows, or in some states, declines. Looking ahead, the trajectory of the economy nationally and in individual states as well as the outcome of federal and state elections will have implications for Medicaid enrollment and spending and influence the way in which the ACA and Medicaid expansion are addressed across the country.

The authors express their appreciation to the Medicaid directors and staff in all 50 states and the District of Columbia who completed the survey on which this brief is based. We also thank Dennis Roberts, who managed the database.

Methodology

Methodology

Definition of Medicaid Spending. Total Medicaid spending includes all payments to Medicaid providers for Medicaid covered services provided to enrolled Medicaid beneficiaries. Medicaid spending also includes special disproportionate share hospital (DSH) payments that subsidize uncompensated hospital care for persons who are uninsured and unreimbursed costs care for persons on Medicaid. Not included in total Medicaid spending are Medicaid administrative costs and federally mandated state “Clawback” payments to Medicare (to help finance the Medicare Part D prescription drug benefit for Medicaid beneficiaries who are also enrolled in Medicare.) States are also asked to exclude costs for the Children’s Health Insurance Program (CHIP) though a few states provided percentage changes for spending that reflected Medicaid and CHIP combined. Total Medicaid spending includes payments financed from all sources, including state funds, local contributions, and federal matching funds. Historical state Medicaid spending refers to all non-federal spending, which may include local funds and provider taxes and fees as well as state general fund dollars. State spending for FYs 2016-2017 collected as part of this survey reflect state spending, largely state general fund dollars.

Methodology. The Kaiser Commission on Medicaid and the Uninsured (KCMU) commissioned Health Management Associates (HMA) to survey Medicaid directors in all 50 states and the District of Columbia to identify and track trends in Medicaid spending, enrollment, and policy making. This is the sixteenth annual survey, conducted at the beginning of each state fiscal year from FY 2002 through FY 2017.

The KCMU/HMA Medicaid survey for this report was sent to each Medicaid director in June 2016. Medicaid directors and staff responded to the written survey and participated in follow-up telephone interviews from June through August 2016. The telephone discussions are an integral part of the survey to ensure complete and accurate responses and to record the complexities of state actions. All 50 states and DC completed surveys and participated in telephone discussions. At the time of the survey, Illinois did not have an enacted state budget for FY 2017; certain portions of the Illinois survey could not be completed.

For FY 2016 and FY 2017, annual rates of growth for Medicaid spending were calculated as weighted averages across all states. Weights for spending were derived from the most recent state Medicaid expenditure data for FY 2015, based on estimates prepared for KCMU by the Urban Institute using CMS Form 64 reports, adjusted for state fiscal years. These data were also used for historic Medicaid spending. In FY 2013, there was wide inexplicable variation between states, which inflated the overall growth rate. To adjust for this anomaly, spending growth from FYs 2012, FY 2013, and FY 2014 was averaged to estimate growth in FY 2013. The resulting estimate is similar to trends reported by the National Association of State Budget Officers (NASBO).

Medicaid average annual growth rates for enrollment were calculated using weights based on Medicaid and CHIP monthly enrollment data for June 2016 published by CMS.12 Historical enrollment trend data for FY 1998 to FY 2013 reflects the annual percentage change from June to June of monthly enrollment data for Medicaid beneficiaries collected from states.13 Enrollment trend data for FY 2014 to FY 2016 reflects growth in average monthly enrollment based on Medicaid & CHIP Monthly Applications, Eligibility Determinations, and Enrollment Reports from CMS. The baseline for FY 2013 was the monthly average of July 2013 through September 2013 as of August 2015. FY 2014 was estimated by averaging the monthly average of July 2013 through September 2013 with the monthly average of January 2014 through June 2014.

The data reported for FYs 2016 and FY 2017 Medicaid spending and FY 2017 for Medicaid enrollment are weighted averages, and therefore, data reported for states with larger enrollment and spending have a larger effect on the national average. To understand variation across expansion and non-expansion states, median growth rates were calculated based on Medicaid expansion status in each year for FY 2015 – FY 2017.

Additional information collected in the survey on policy actions taken during FY 2016 and FY 2017 can be found in the companion report at: www.kff.org

Appendix

Appendix: Background on Medicaid Financing

Medicaid Financing Structure. The Medicaid program is jointly funded by states and the federal government. The federal government guarantees match funds to states for qualifying Medicaid expenditures. The federal match rate (Federal Medical Assistance Percentage, or FMAP) is calculated annually for each state using a formula set in the Social Security Act which is based on a state’s average personal income relative to the national average; poorer states have higher FMAPs. According to the formula, the FMAP in FFY 2017 varies across states from a floor of 50 percent to a high of 74.6 percent.14 Personal income data are lagged, so data used for FFY 2017 FMAPs are from the three years of 2012 to 2014. Even small changes in a state’s FMAP can mean large changes in the amount of state general funds needed to maintain current programs, with decreases in FMAP increasing pressure on state budgets.

As a result of the federal matching structure, Medicaid has a unique role in state budgets as both an expenditure item and a source of federal revenue for states. In FY 2014, Medicaid accounted for 25.6 percent of total state spending for all items in the state budget, but 18.4 percent of all state general fund spending, a far second to spending on K-12 education (35.4 percent of state general fund spending.)15 Medicaid is the largest single source of federal funds for states, accounting for half (50.4 percent) of all federal funds for states in FY 2014 (Figure 7).

Medicaid and the Economy. Medicaid is a countercyclical program. During economic downturns more people qualify and enroll in Medicaid, which increases program spending at the same time that state tax revenues level or fall. To help mitigate these budget pressures, Congress has twice passed temporary increases to the FMAP rates to help support states during economic downturns, most recently in 2009 as part of the American Recovery and Reinvestment Act (ARRA). The ARRA-enhanced match rates were the primary vehicle for federal fiscal relief to states during the “Great Recession,” providing states over $100 billion in additional federal funds over 11 quarters, ending in June 2011.16 During this recession, unemployment soared, state revenues plummeted, and Medicaid spending and enrollment peaked.

Medicaid and the ACA. Effective January 1, 2014, the ACA expanded Medicaid eligibility to millions of non-elderly adults with income at or below 138 percent of the federal poverty level (FPL) – about $16,394 for an individual in 2016. The law also provided for 100 percent federal funding of the expansion through 2016, declining gradually to 90 percent in 2020 and future years. The Supreme Court ruling on the ACA in June 2012 effectively made the Medicaid expansion optional for states. As of September 2016, 32 states (including the District of Columbia) have implemented the ACA Medicaid expansion. The ACA also required all states to implement new streamlined and coordinated application, enrollment, and renewal processes, including transitioning to a new income standard (Modified Adjusted Gross Income or MAGI) to determine Medicaid financial eligibility for non-elderly, non-disabled populations.

Endnotes

- Centers for Medicare and Medicaid Services, Medicaid & CHIP Monthly Application, Eligibility Determinations, and Enrollment Reports. (Washington, DC: Centers for Medicare and Medicaid Services, June 2016), http://www.medicaid.gov/medicaid-chip-program-information/program-information/medicaid-and-chip-enrollment-data/medicaid-and-chip-application-eligibility-determination-and-enrollment-data.html. ↩︎

- The Kaiser Commission on Medicaid and the Uninsured analysis of Centers for Medicare and Medicaid Services, Form CMS-64 Data, accessed September 2016. ↩︎

- Centers for Medicare and Medicaid Services. National Health Expenditures (Washington, DC: Centers for Medicare and Medicaid Services, December 2015). http://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-andReports/NationalHealthExpendData/NationalHealthAccountsHistorical.html. ↩︎

- National Association of State Budget Officers, The Fiscal Survey of States (Washington, DC: National Association of State Budget Officers, Spring 2016), http://www.nasbo.org/mainsite/reports-data/fiscal-survey-of-states. ↩︎

- National Association of State Budget Officers, The Fiscal Survey of States (Washington, DC: National Association of State Budget Officers, Spring 2016), http://www.nasbo.org/mainsite/reports-data/fiscal-survey-of-states. ↩︎

- Lucy Dadayan and Donald Boyd, Slowing Growth in State Tax Revenues (New York, NY: The Nelson A. Rockefeller Institute of Government, June 2016), http://www.rockinst.org/pdf/government_finance/state_revenue_report/2016-06-30-SRR_103_final.pdf. ↩︎

- Lucy Dadayan and Donald Boyd, Slowing Growth in State Tax Revenues (New York, NY: The Nelson A. Rockefeller Institute of Government, June 2016), http://www.rockinst.org/pdf/government_finance/state_revenue_report/2016-06-30-SRR_103_final.pdf. ↩︎

- Lucy Dadayan and Donald Boyd, Double, Double, Oil and Trouble (New York, NY: The Nelson A. Rockefeller Institute of Government, February 2016), http://www.rockinst.org/pdf/government_finance/2016-02-By_Numbers_Brief_No5.pdf. ↩︎

- Lucy Dadayan and Donald Boyd, Double, Double, Oil and Trouble (New York, NY: The Nelson A. Rockefeller Institute of Government, February 2016), http://www.rockinst.org/pdf/government_finance/2016-02-By_Numbers_Brief_No5.pdf. ↩︎

- Historical state Medicaid spending refers to all non-federal spending, which may include local funds and provider taxes and fees as well as state general fund dollars. Data for state spending for FYs 2016-2017 collected through this survey reflect state spending, largely state general fund dollars. ↩︎

- National Association of State Budget Officers, The Fiscal Survey of States (Washington, DC: National Association of State Budget Officers, Spring 2016), http://www.nasbo.org/mainsite/reports-data/fiscal-survey-of-states. ↩︎

- Centers for Medicare and Medicaid Services, Medicaid & CHIP Monthly Application, Eligibility Determinations, and Enrollment Reports. (Washington, DC: Centers for Medicare and Medicaid Services, June 2016), http://www.medicaid.gov/medicaid-chip-program-information/program-information/medicaid-and-chip-enrollment-data/medicaid-and-chip-application-eligibility-determination-and-enrollment-data.html. ↩︎

- Laura Snyder, Robin Rudowitz, Eileen Ellis and Dennis Roberts, Medicaid Enrollment: June 2013 Data Snapshot (Washington, DC: Kaiser Commission on Medicaid and the Uninsured, January 29, 2014), https://modern.kff.org/medicaid/issue-brief/medicaid-enrollment-june-2013-data-snapshot/. ↩︎

- The Kaiser Family Foundation State Health Facts. Data Source: 80 Fed. Reg. 73779 – 73782 (Nov. 5, 2015) accessed September 8, 2016, https://modern.kff.org/medicaid/state-indicator/federal-matching-rate-and-multiplier/. ↩︎

- Kaiser Commission on Medicaid and the Uninsured estimates based on the data reported in: National Association of State Budget Officers, State Expenditure Report – Examining Fiscal 2012-2014 State Spending (Washington, DC: National Association of State Budget Officers, November 2014), http://www.nasbo.org/publications-data/state-expenditure-report/state-expenditure-report-fiscal-2012-2014-data. ↩︎

- To be eligible for ARRA funds, states could not restrict eligibility or tighten enrollment procedures in Medicaid or CHIP. Vic Miller, Impact of the Medicaid Fiscal Relief Provisions in the American Recovery and Reinvestment Act (ARRA) (Washington, DC: Kaiser Commission on Medicaid and the Uninsured, October 2011), https://modern.kff.org/medicaid/issue-brief/impact-of-the-medicaid-fiscal-relief-provisions/. ↩︎