How Are Private Insurers Covering At-Home Rapid COVID Tests?

Under the Families First Coronavirus Response Act (FFCRA) and the Coronavirus Aid, Relief, and Economic Security (CARES) Act, two COVID-19 emergency measures passed by Congress, private insurance companies generally have been required to cover COVID-19 tests ordered by providers, typically those conducted on site, such as in clinical or pop-up environments (providers can also seek federal reimbursement for testing uninsured patients). This broad coverage requirement has been in place since the early days of the pandemic, and the only exceptions are that private insurers do not have to reimburse for tests conducted for public health surveillance or workplace requirements.

The Biden Administration announced on December 2, 2021 (followed by detailed guidance released on January 10, 2022) that private insurers would be required to also begin covering the cost of rapid at-home COVID-19 tests purchased over-the-counter starting January 15, 2022.

Under the new guidance, private insurance companies must cover up to 8 FDA-authorized rapid tests per member per month. This averages out to be about 2 rapid tests per week for those eligible. This policy applies to all private health insurers, and does not apply to Medicaid managed care or Medicare Advantage plans. Private insurers are required to provide a coverage mechanism for their members, though some are just beginning to set up these processes. In addition to offering reimbursement for tests purchased out-of-pocket, the guidance also encourages insurers to set up “direct coverage” options. In these arrangements, enrollees can buy rapid at-home tests without paying anything up front or navigating a complicated reimbursement process if the test is obtained through a preferred network of pharmacies or retailers, or through a mail order option. Enrollees in plans with direct coverage options can still seek reimbursement for tests purchased at non-preferred retailers as well, but the guidance allows insurers to cap reimbursement at $12 per test. If the insurance company does not have a direct coverage option, then it must reimburse the enrollee for the full cost of the test. The aims of these provisions are to both simplify coverage for consumers (though the direct coverage option) and mitigate inflationary effects on test prices (through the cap). Insurers have an incentive to set up direct coverage options because the $12 reimbursement cap can also help limit their costs. If many or most insurers set up these programs and implement the $12 cap, it could also impact the price of tests as retailers and manufactures aim for the reimbursement target.

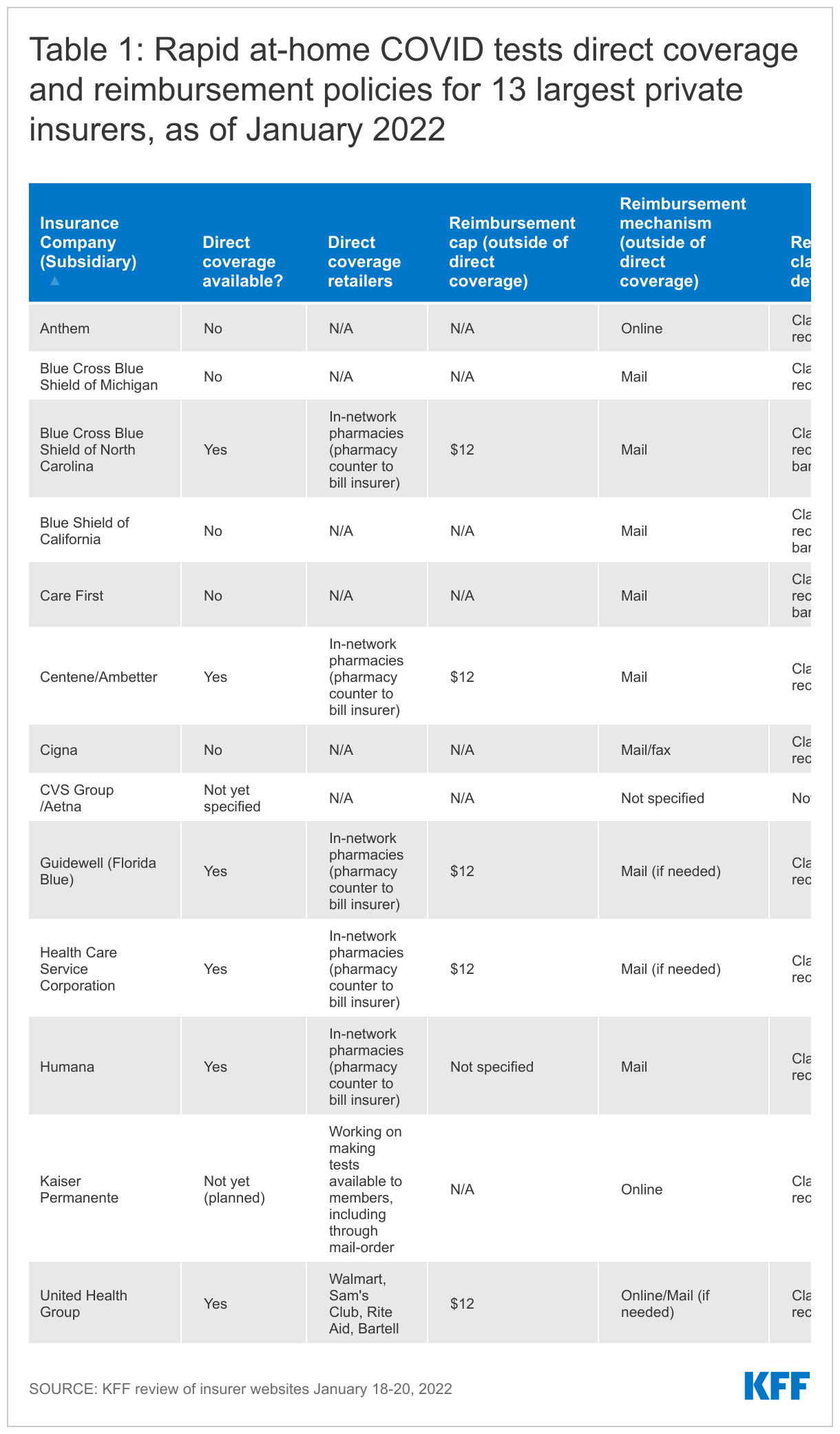

To assess how insurers are beginning to implement this policy, from a consumer perspective, we reviewed publicly available rapid at-home COVID tests coverage and reimbursement policies for the 13 private insurers with at least 1 million fully-insured members across their U.S. subsidiaries (Table 1) between January 18, 2022 and January 20, 2022. These private insurers cover about 6 in 10 people in the fully-insured commercial market. Most of these parent companies have the same coverage and reimbursement policy across all of their subsidiaries, but when that was not the case, we include the policy for their largest subsidiary.

Findings

At this time, about half of the insurers reviewed are implementing their testing coverage policy using only reimbursement.

- 7 insurers (Anthem, Blue Cross Blue Shield of Michigan, Blue Shield of California, Care First, Cigna, CVS Group/Aetna, and Kaiser Permanente) are currently relying on reimbursement practices (i.e., do not have a direct coverage option) and have varied reimbursement policies. (Anthem also has “a limited number of at-home diagnostic test kits available for certain members to order online.”)

- 4 of the 7 insurers (Blue Cross Blue Shield of Michigan, Blue Shield of California, Care First, Cigna) require receipts and a form be mailed in (typically one submission per receipt per member). One insurer (Cigna) also offers a fax option. None of these appear to provide an email or online submission. One insurer (CVS Group/Aetna) notes they will reimburse enrollees but does not describe the reimbursement procedure.

- 2 insurers offer an online option for submitting reimbursement forms (Anthem and Kaiser Permanente).

- 3 insurers also require Universal Product Code (UPC) or product barcode information to be mailed with the receipt.

The remaining half of the top insurers had a direct coverage option set up at the time of review.

- 6 of the 13 top insurers have a direct coverage option at this time. Blue Cross Blue Shield of North Carolina, Centene/Ambetter, Health Care Service Corporation, Guidewell (Florida Blue), Humana, and United Health Group commercial plan enrollees can purchase rapid tests at an in-network or preferred pharmacy and will not have to pay anything up front. Kaiser Permanente says they will have direct coverage in the future but do not yet provide this option.

- 5 of the 6 insurers with a direct coverage option (Blue Cross Blue Shield of North Carolina, Centene/Ambetter, Guidewell (Florida Blue), Humana, and United Health Group) also lay out how enrollees can seek reimbursement for costs they have fronted with retailers outside the preferred network, typically by mail and one also providing an online option. Another insurer, (Health Care Service Corporation) does not provide any specific information and instead instructs enrollees to contact their health plan administrator.

Enrollees in plans with a direct coverage option may have reimbursement limited to $12 per test if a test is purchased outside of this option.

- Of the 6 insurers with the direct coverage option, 5 specify that claims outside the preferred network are subject to a maximum reimbursement of $12 per test. These insurers include: Blue Cross Blue Shield of North Carolina, Centene/Ambetter, Guidewell (Florida Blue), Health Care Service Corporation, and United Health Group

- One insurer (Humana) with direct coverage did not list a maximum reimbursement amount.

Conclusion

The success of this policy hinges on two main factors: the availability of tests and the ability of enrollees to navigate the reimbursement or direct coverage process. As we have written elsewhere, despite recent efforts to increase supply of tests, it can still be challenging to find a home COVID-test online and at pharmacies. If supply remains limited and tests are not widely available, a reimbursement or direct coverage mechanism does not do much to improve access.

People who do find rapid tests may also have difficulty navigating the reimbursement or direct coverage process. As our analysis shows, in the early days of implementation, insurers have varying coverage policies, including whether they have a direct coverage option or require enrollees to request reimbursement, and when enrollees seek reimbursement, whether they do so online or through mail or fax. Some of these processes will inevitably be more consumer friendly than others and will either facilitate coverage or put up additional barriers. Even if the cost is eventually reimbursed, many families could face financial barriers if their insurer requires upfront payment. Many people do not have easy access to printers or fax machines, required by some insurers for reimbursement, which will likely mean that some claims will never be submitted. Additionally, as noted, this policy applies only to those with private insurance so those who are uninsured or those with other coverage, will have to navigate different options, including ordering tests directly from the federal government (with a current limit of four per household). Still, this new policy is a step towards improving COVID-19 test accessibility and affordability in the U.S.